E-Way Bill required to be simplified

Rule 1 (Draft GST E-Way Bill Rules ) requires the use of e-Way bill for all removals including those involving supply.

Issue

When invoice is already issued, issuance of e-way bill increases the compliance at the time of removal of goods. This is not in line with ease of doing business. Hence, comprehensive suggestion is made to the rules. Clearly few aspects are required:

a) E-way bill not required for intra-State movement all though provision is required for innocent passage via other State

b) Invoice is sufficient for movement ‘by way of supply’ which has IRN generated on common portal. Same facility to be allowed in all other cases of movement where some other document or challan is also generated

c) RFID requirement to be optional for transporter

Suggestion

Owing to the issues enlisted above the entire e-way bill rules be redrafted as follows:

1. Information to be furnished prior to commencement of inter-State movement of goods and generation of e-way bill

(1) Every registered person who causes inter-State movement of goods as follows—

(ii) for reasons, other than supply of consignment value exceeding Rs. 5 lakhs; or

(iii) due to inward supply from an unregistered person of consignment value exceeding Rs 2 lakhs,

shall, before commencement of movement, furnish information relating to the said goods in Part A of FORM GST INS-01, electronically, on the common portal and

(a) where the goods are transported by the registered person as a consignor or the recipient of supply as the consignee, whether in his own conveyance or a hired one, the said person or the recipient may generate the e-way bill in FORM GST INS-1 electronically on the common portal after furnishing information in Part B of FORM GST INS-01; or

(b) where the e-way bill is not generated under clause (a) and the goods are handed over to a transporter, the registered person shall furnish the information relating to the transporter in Part B of FORM GST INS-01 on the common portal and the e-way bill shall be generated by the transporter on the said portal based on the information furnished by the registered person in Part A of FORM GST INS01:

Provided that the registered person or, as the case may be, the transporter may, at his option, generate and carry the e-way bill even if the value of the consignment is less than that specified.

Provided further that where the movement is caused by an unregistered person either in his own conveyance or a hired one or through a transporter, he or the transporter may, at their option, generate the e-way bill in FORM GST INS-01 on the common portal in the manner prescribed in this rule.

Provided further, where no e-way bill is provided on account of intra-State movement of goods by the supplier or other consignor, the transporter may generate e-way bill in FORM GST INS-01 in case the journey involves inter-State innocent passage.

Provided further that where the movement is in relation to supply, the following documents uploaded on the Common Portal against a duly issued Invoice Reference Number or Challan Reference Number or Customs Reference Number and accompanying the consignment will suffice invoice without the requirement to issue an e-way bill separately:

i) invoice issued under Section 31 by a supplier

ii) document issued by ISD for distribution of credit

iii) challan issued under Section 19 in respect of goods sent for job-work by the Principal or by intermediate job-workers to other job-workers

iv) challan issued under sSection 31(7) for sale on approval

v) bill of entry issued under Customs Act in respect of imports including supply from SEZ

vi) challan issued for intra-State movement of goods where consignor and consignee are same registered person

Explanation. – For the purposes of this sub-rule, where the goods are supplied by an unregistered supplier to a recipient who is registered, the movement shall be said to be caused by such recipient if the recipient is known at the time of commencement of movement of goods.

(2) Upon generation of the e-way bill on the common portal, a unique e-way bill number (EBN) shall be made available to the supplier, the recipient and the transporter on the common portal.

(3) Any transporter transferring goods from one conveyance to another in the course of transit shall, before such transfer and further movement of goods, generate a new e-way bill on the common portal in FORM GST INS-01 specifying therein the mode of transport.

(4) Where multiple consignments are intended to be transported in one conveyance, the transporter shall indicate the serial number of e-way bills generated in respect of each such consignment electronically on the common portal and a consolidated e-way bill in FORM GST INS-02 shall be generated by him on the common portal prior to the movement of goods:

Provided that where the consignor has not generated FORM GST INS-01 in accordance with provisions of sub-rule (1) and the value of goods carried in the conveyance is more than fifty thousand rupees, the transporter shall generate FORM GST INS-01 on the basis of invoice or bill of supply or delivery challan, as the case may be, and also generate a consolidated e-way bill in FORM GST INS-02 on the common portal prior to the movement of goods.

(5) The information furnished in Part A of FORM GST INS-01 shall be made available to the registered supplier on the common portal who may utilize the same for furnishing details in FORM GSTR-1:

Provided that when information has been furnished by an unregistered supplier in FORM GST INS-01, he shall be informed electronically, if the mobile number or the e mail is available.

(6) Where an e-way bill has been generated under this rule, but goods are either not being transported or are not being transported as per the details furnished in the e-way bill, the e-way bill may be cancelled electronically on the common portal, either directly or through a Facilitation Centre notified by the Commissioner, within 24 hours of generation of the e-way bill:

Provided that an e-way bill cannot be cancelled if it has been verified in transit in accordance with the provisions of rule 3.

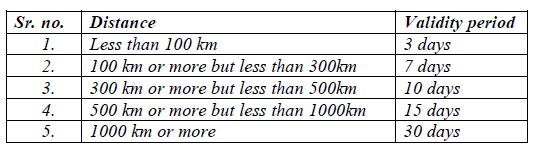

(7) An e-way bill or a consolidated e-way bill generated under this rule shall be valid for the period as mentioned in column (3) of the Table below from the relevant date, for the distance the goods have to be transported, as mentioned in column (2):

Table

Provided that the Commissioner may, by notification, extend the validity period of e-way bill for certain categories of goods as may be specified therein.

Explanation. — For the purposes of this rule, the “relevant date” shall mean the date on which the e-way bill has been generated and the period of validity shall be counted from the time at which the e-way bill has been generated.

(8) The details of e-way bill generated under sub-rule (1) shall be made available to the recipient, if registered, on the common portal, who shall communicate his acceptance or rejection of the consignment covered by the e-way bill.

(9) Where the recipient referred to in sub-rule (8) does not communicate his acceptance or rejection within 72 hours after the of validity of the e-way bill duly made available to him on the common portal, it shall be deemed that he has accepted the said details.

(10) The e-way bill generated under rule 1 of the CGST rules or GST rules of any other State shall be valid in the State.

Explanation. – The facility of generation and cancellation of e-way bill may also be made available through SMS.

Source ICAI Suggestions on GST Rules Submitted to Govt of India