TDS on Cash Withdrawal from Banks & Post Office

TDS on Cash withdrawal from banks ,Cooperative Banks and Post Office under Section 194N has been changed by Finance Act 2020 w.e.f 01.07.2020

Video Explanation by CA Satbir Singh on Changes in TDS on Cash Withdrawal

section 194N by Finance No (2) Act 2019 w.e.f 01.09.2019

Payment of certain amounts in cash.

194N. Every person, being,—

| (i) | a banking company to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act); | |

| (ii) | a co-operative society engaged in carrying on the business of banking; or | |

| (iii) | a post office, |

who is responsible for paying any sum, or, as the case may be, aggregate of sums, in cash, in excess of one crore rupees during the previous year, to any person (herein referred to as the recipient) from one or more accounts maintained by the recipient with it shall, at the time of payment of such sum, deduct an amount equal to two per cent of sum exceeding one crore rupees, as income-tax:

Provided that nothing contained in this sub-section shall apply to any payment made to,—

| (i) | the Government; | |

| (ii) | any banking company or co-operative society engaged in carrying on the business of banking or a post office; | |

| (iii) | any business correspondent of a banking company or co-operative society engaged in carrying on the business of banking, in accordance with the guidelines issued in this regard by the Reserve Bank of India under the Reserve Bank of India Act, 1934 (2 of 1934); | |

| (iv) | any white label automated teller machine operator of a banking company or co-operative society engaged in carrying on the business of banking, in accordance with the authorisation issued by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007 (51 of 2007); | |

| (v) | such other person or class of persons, which the Central Government may, by notification in the Official Gazette, specify in consultation with the Reserve Bank of India. |

For section 194N of the Income-tax Act, the following section shall be substituted with effect from the 1st day of July, 2020, namely:—

Payment of certain amounts in cash.

‘‘194N. Every person, being,—

(i) a banking company to which the Banking Regulation Act, 1949 applies (including any bank or banking institution referred to in section 51 of that Act);

(ii) a co-operative society engaged in carrying on the business of banking; or

(iii) a post office,

who is responsible for paying any sum, being the amount or the aggregate of amounts, as the case may be, in cash exceeding one crore rupees during the previous year, to any person (herein referred to as the recipient) from one or more accounts maintained by the recipient with it shall, at the time of payment of such sum, deduct an amount equal to two per cent. of such sum, as income-tax:

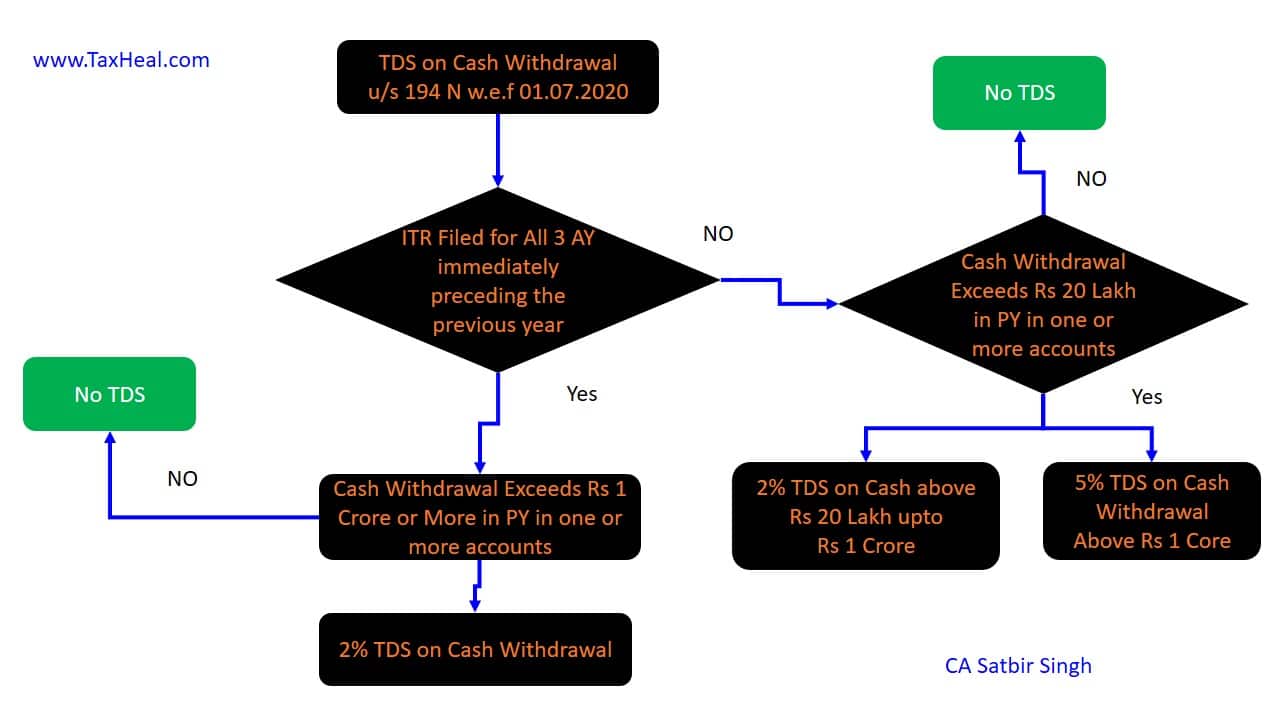

Provided that in case of a recepient who has not filed the returns of income for all of the three assessment years relevant to the three previous years, for which the time limit of file return of income under sub-section (1) of section 139 has expired, immediately preceding the previous year in which the payment of the sum is made to him, the provision of this section shall apply with the modification that—

(i) the sum shall be the amount or the aggregate of amounts, as the case may be, in cash exceeding twenty lakh rupees during the previous year; and

(ii) the deduction shall be—

(a) an amount equal to two per cent. of the sum where the amount or aggregate of amounts, as the case may be, being paid in cash exceeds twenty lakh rupees during the previous year but does not exceed one crore rupees; or

(b) an amount equal to five per cent. of the sum where the amount or aggregate of amounts, as the case may be, being paid in cash exceeds one crore rupees during the previous year:

Provided further that the Central Government may specify in consultation with the Reserve Bank of India, by notification in the Official Gazette, the recipient in whose case the first proviso shall not apply or apply at reduced rate, if such recipient satisfies the conditions specified in such notification:

Provided also that nothing contained in this section shall apply to any payment made

to—

(i) the Government;

(ii) any banking company or co-operative society engaged in carrying on the business of banking or a post office;

(iii) any business correspondent of a banking company or co-operative society engaged in carrying on the business of banking, in accordance with the guidelines issued in this regard by the Reserve Bank of India under the Reserve Bank of India Act, 1934;

(iv) any white label automated teller machine operator of a banking company or co-operative society engaged in carrying on the business of banking, in accordance with the authorisation issued by the Reserve Bank of India under the Payment and Setllement Systems Act, 2007:

Provided also that the Central Government may specify in consultation with the Reserve Bank of India, by notification in the Official Gazette, the recipient in whose case the provision of this section shall not apply or apply at reduced rate, if such recipient satisfies the conditions specified in such notification.

Clarification by CBIC by Press Release on TDS on Cash Withdrawal

CBDT PRESS RELEASE, DATED 30-8-2019

In order to discourage cash transactions and move towards less cash economy, the Finance (No. 2) Act, 2019 has inserted a new section 194N in the Income-tax Act, 1961 (the ‘Act’), to provide for levy of tax deduction at source (TDS) @2% on cash payments in excess of one crore rupees in aggregate made during the year, by a banking company or cooperative bank or post office, to any person from one or more accounts maintained with it by the recipient. The above section shall come into effect from 1st September, 2019.

Since the section provided that the person responsible for paying any sum, or, as the case may be, aggregate of sums, in cash, in excess of one crore rupees during the previous year to deduct income tax @2% on cash payment in excess of rupees one crore, queries were received from the general public through social media on the applicability of this section on withdrawal of cash from 01.04.2019 to 31.08.2019.

The CBDT, having considered the concerns of the people, hereby clarifies that section 194N inserted in the Act, is to come into effect from 1st September, 2019. Hence, any cash withdrawal prior to 1st September, 2019 will not be subjected to the TDS under section 194N of the Act. However, since the threshold of Rs. 1 crore is with respect to the previous year, calculation of amount of cash withdrawal for triggering deduction under section 194N of the Act shall be counted from 1st April, 2019. Hence, if a person has already withdrawn Rs. 1 crore or more in cash upto 31st August, 2019 from one or more accounts maintained with a banking company or a cooperative bank or a post office, the two per cent TDS shall apply on all subsequent cash withdrawals.

NOTIFIED OTHER PERSON OR CLASS OF PERSONS : CASH PAYMENT ALLOWED

Payment in Cash to Cash Replenishment Agencies (CRA’s) and franchise agents of White Label Automated Teller Machine Operators

NOTIFICATION NO. SO 3356(E) [NO. 68/2019 (F.NO. 370142/12/2019-TPL)], DATED 18-9-2019

In exercise of the powers conferred by clause (v) of proviso to section 194N of the Income-tax Act, 1961 (43 of 1961), the Central Government after consultation with the Reserve Bank of India, hereby specifies Cash Replenishment Agencies (CRA’s) and franchise agents of White Label Automated Teller Machine Operators (WLATMO’s) maintaining a separate bank account from which withdrawal is made only for the purposes of replenishing cash in the Automated Teller Machines (ATM’s) operated by such WLATMO’s and the WLATMO have furnished a certificate every month to the bank certifying that the bank account of the CRA’s and the franchise agents of the WLATMO’s have been examined and the amounts being withdrawn from their bank accounts has been reconciled with the amount of cash deposited in the ATM’s of the WLATMO’s.

2. The notification shall be deemed to have come into force with effect from the 1st day of September, 2019.

NOTIFICATION NO. SO 3427 (E) [NO. 70/2019 (F.NO. 370142/12/2019-TPL (PART-I)], DATED 20-9-2019

In exercise of the powers conferred by clause (v) of the proviso to section 194N of the Income-tax Act, 1961 (43 of 1961), the Central Government after consultation with the Reserve Bank of India, hereby specifies the commission agent or trader, operating under Agriculture Produce Market Committee (APMC), and registered under any Law relating to Agriculture Produce Market of the concerned State, who has intimated to the banking company or co-operative society or post office his account number through which he wishes to withdraw cash in excess of rupees one crore in the previous year along with his Permanent Account Number (PAN) and the details of the previous year and has certified to the banking company or co-operative society or post office that the withdrawal of cash from the account in excess of rupees one crore during the previous year is for the purpose of making payments to the farmers on account of purchase of agriculture produce and the banking company or co-operative society or post office has ensured that the PAN quoted is correct and the commission agent or trader is registered with the APMC, and for this purpose necessary evidences have been collected and placed on record.

2. The notification shall be deemed to have come into force with effect from the 1st day of September, 2019.

NOTIFICATION NO. S.O. 3719(E) [NO. 80/2019 (F.NO. 370142/12/2019-TPL (PART20))], DATED 15-10-2019

In exercise of the powers conferred by clause (v) of proviso to section 194N of the Income-tax Act, 1961 (43 of 1961), the Central Government, after consultation with the Reserve Bank of India (RBI), hereby specifies,-

| (a) | the authorised dealer andits franchise agent and sub-agent; and | |

| (b) | Full-Fledged Money Changer (FFMC) licensed by the Reserve Bank of Indiaand its franchise agent; |

maintaining a separate bank account from which withdrawal is made only for the purposes of,-

| (i) | purchase of foreign currency from foreign tourists or non-residents visiting India or from resident Indians on their return to India, in cash as per the directions or guidelines issued by Reserve Bank of India; or | |

| (ii) | disbursement of inward remittances to the recipient beneficiaries in India in cash under Money Transfer Service Scheme (MTSS) of the Reserve Bank of India; |

and a certificate is furnished by the authorised dealers and their franchise agentand sub-agent, and the Full-Fledged Money Changers (FFMC) and their franchise agent to the bank that withdrawal is only for the purposes specified above and the directions or guidelines issued by the Reserve Bank of India have been adhered to.

Explanation – For the purposes of this notification, “authorised dealer” means a person authorised as an authorised dealer under sub-section (1) of section 10 of the Foreign Exchange Management Act, 1999 (42 of 1999).

2. The notification shall be deemed to have come into force with effect from the 1st day of September, 2019.

Explanatory Memorandum : It is certified that no person is being adversely affected by giving retrospective effect to this notification.

Credit of TDS deducted :

Person can adjust this TDS deducted u/s 194N at the time of filing of his Income Tax Return

Commentary on TDS on Cash Withdrawal from Banks

All Bank Accounts are to be taken : cash withdrawn from one or more accounts means, all the accounts from which the cash can be drawn. They can be Savings Account, Current A/c, Overdraft Account, Escrow account, cash credit account, debit card, credit card, ATM transaction linked to any account, and such cash drawals are mechanised, personalised, automated or otherwise in excess of Rs 1 crore

Joint Accounts : In case of joint holding,whether the first name holder would be considered as the person withdrawing cash for the purposes of the section ?

Belated return filing u/s 139(4) (after Due date) will not be Considered. as section talks about only Section 139(1) of Income Tax Act.

w.e.f 01.07.2020 In case of a recepient who has not filed the returns of income for all of the three assessment years relevant to the three previous years, for which the time limit of file return of income under sub-section (1) of section 139 has expired, immediately preceding the previous year in which the payment of the sum is made to him, the provision of this section shall apply with the modification that

(i)the sum shall be the amount or the aggregate of amounts, as the case may be, in cash exceeding twenty lakh rupees during the previous year; and

(i) the deduction shall be

(a) an amount equal to two per cent. of the sum where the amount or aggregate of amounts, as the case may be, being paid in cash exceeds twenty lakh rupees during the previous year but does not exceed one crore rupees; or

(b) an amount equal to five per cent. of the sum where the amount or aggregate of amounts, as the case may be, being paid in cash exceeds one crore rupees during the previous year:

For Latest Notifications and Circular refer Govt of India website on Income Tax Click here

_______________________________________________________________

In this Article you got answer to following Questions

1. when TDS will be deducted u/s 194N as per Finance Act 2020 if cash withdrawal from bank and Income tax return not filed.

2. Who are persons whose TDS will not be deducted if even is cash withdrawal exceeds Rs 1 Crore

3. TDS on cash withdrawal exceeding Rs 20 Lakh

4. Amendments in Section 194 of #incomeTax if cash withdrawn from Bank

5. tds on cash withdrawal circular,

6.tds on cash withdrawal exemption

7 tds on cash withdrawal section 194n

8. tds on cash withdrawal is refundable or not

9 tds on cash withdrawal notification

10 tds on cash withdrawal above 1 crore

11 cash withdrawal tds effective date

12 amendment in section 194n

13 faq on 194n

14 cash withdrawal limit for individual

15 2 percent tds on cash withdrawal

16 5 percent TDS on Cash Withdrawal

17 white label atm 2 tds

18 section 194n exemption

Pingback: TaxHeal - GST and Income Tax Complete Guide Portal