WRIT JURISDICTION DECLINED WHERE STATUTORY REMEDY EXISTS; ACCOUNTANT’S DEATH NO GROUND TO BYPASS APPEAL

ISSUE

Whether a Writ Petition is maintainable against an assessment order passed ex-parte (without reply/hearing) when the petitioner cites personal difficulties (death of Accountant) for non-compliance, or if the petitioner must exhaust the statutory appellate remedy under Section 107.

FACTS

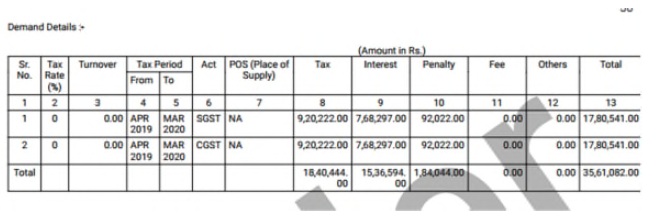

Period: 2019-20.

The Dispute: The petitioner challenged a Show Cause Notice (SCN) and the subsequent Order.

Petitioner’s Defense: The petitioner claimed they had filed all GST returns and discharged their liability. However, they admitted that no reply was filed to the SCN and no personal hearing was availed.

Reason for Default: The petitioner submitted that their Accountant had passed away, which led to the lack of representation/compliance.

The Plea: They approached the High Court seeking to quash the order directly, alleging violation of procedure.

DECISION

Statutory Remedy Available: The High Court noted that since the petitioner failed to file a reply or appear for the hearing, the Assessing Officer passed the order based on available records.

No Writ Interference: The Court declined to exercise its extraordinary writ jurisdiction because a specific statutory remedy (Appeal under Section 107) exists. The death of an accountant, while tragic, is a factual ground for seeking condonation of delay before the Appellate Authority, not a ground to bypass the appellate hierarchy entirely.

Relief: The petition was disposed of with liberty granted to the petitioner to avail the appellate remedy (file an appeal).

Verdict: [In Favour of Revenue] (Writ dismissed, Petitioner relegated to Appeal).

II. VALIDITY OF LIMITATION EXTENSION NOTIFICATIONS (SECTION 168A) SUBJECT TO SUPREME COURT OUTCOME

ISSUE

Whether Notification No. 9/2023-CT and 56/2023-CT, which extended the limitation period for issuing adjudication orders under Section 73 for FY 2019-20 (invoking powers under Section 168A due to force majeure/COVID), are valid or ultra vires.

FACTS

The Challenge: The assessee challenged the validity of the CBIC notifications that extended the time limit for the Department to issue orders for the period 2019-2020.

The Argument: Taxpayers generally argue that Section 168A (Force Majeure) cannot be invoked indiscriminately years after the COVID pandemic to extend limitation periods for routine cases.

DECISION

SC Seisin: The High Court noted that an identical legal issue is currently pending consideration before the Supreme Court in the case of HCC-SEW-MEIL-AAG JV v. Assistant Commissioner of State Tax.

Outcome Linked: The Court held that the challenge raised by the assessee in the present proceedings would be subject to the outcome of the Supreme Court’s decision in the pending matter.

Verdict: [Matter Stayed / Subject to SC Decision]

KEY TAKEAWAYS

The “Accountant Excuse”: Courts are sympathetic to genuine hardships (like the death of staff), but they prefer you to use these facts to argue for Condonation of Delay in an Appeal, rather than asking the High Court to quash the demand directly.

Participation is Crucial: If you ignore the SCN (even for valid reasons), the High Court will almost always refuse a Writ. You must show you tried to participate or that the officer acted without jurisdiction.

Section 168A Extensions: The extension of deadlines for FY 2018-19 and 2019-20 is the “hot topic” in GST litigation. While High Courts are not striking these down immediately, they are tagging cases to the Supreme Court.

Action: If you have a large demand based solely on time-barred limitation (relying on these notifications), file a writ to keep your matter alive and tagged with the SC batch. If the SC rules in favor of HCC-SEW-MEIL, your demand may be quashed later.

CM APPL. no. 75182 of 2025

| • | Notification No. 09/2023- Central Tax dated 31st March 2023 |

| • | Notification No. 09/2023- State Tax dated 22nd June 2023 |

| • | Notification No.56/2023 – Central Tax dated 28th December, 2023 |

| • | Notification No. 56/2023 – State Tax dated 11th July, 2024 (hereinafter, ‘the impugned notifications’). |

“1. The subject matter of challenge before the High Court was to the legality, validity and propriety of the Notification No.13/2022 dated 5-7-2022 & Notification Nos.9 and 56 of 2023 dated 31-3-2023 & 8-12-2023 respectively.

2. However, in the present petition, we are concerned with Notification Nos.9 & 56/2023 dated 31-3-2023 respectively.

3. These Notifications have been issued in the purported exercise of power under Section 168 (A) of the Central Goods and Services Tax Act. 2017 (for short, the “GST Act”).

4. We have heard Dr. S. Muralidhar, the learned Senior counsel appearing for the petitioner.

5. The issue that falls for the consideration of this Court is whether the time limit for adjudication of show cause notice and passing order under Section 73 of the GST Act and SGST Act (Telangana GST Act) for financial year 2019-2020 could have been extended by issuing the Notifications in question under Section 168-A of the GST Act.

6. There are many other issues also arising for consideration in this matter.

7. Dr. Muralidhar pointed out that there is a cleavage of opinion amongst different High Courts of the country. 8. Issue notice on the SLP as also on the prayer for interim relief, returnable on 7-32025.”

“65. Almost all the issues, which have been raised before us in these present connected cases and have been noticed hereinabove, are the subject matter of the Hon’ble Supreme Court in the aforesaid SLP.

66. Keeping in view the judicial discipline, we refrain from giving our opinion with respect to the vires of Section 168-A of the Act as well as the notifications issued in purported exercise of power under Section 168-A of the Act which have been challenged, and we direct that all these present connected cases shall be governed by the judgment passed by the Hon’ble Supreme Court and the decision thereto shall be binding on these cases too.

67. Since the matter is pending before the Hon’ble Supreme Court, the interim order passed in the present cases, would continue to operate and would be governed by the final adjudication by the Supreme Court on the issues in the aforesaid SLP-4240-2025.

68. In view of the aforesaid, all these connected cases are disposed of accordingly along with pending applications, if any.”

“15. At this stage, ld. Counsel for the Petitioner submits that the Petitioner may be permitted to avail of appellate remedy as the present writ petition was filed within the period of limitation prescribed under Section 107 of the Central Goods and 2 Service Act, 2017. Accordingly, the Petitioner is granted time till 31st August, 2025 to avail of its appellate remedy.