Double Deduction of Upfront Fee Denied; Corporate Guarantees and SBLC Treated as International Transactions

Issue

-

Upfront Fee (Double Deduction): Can an assessee claim amortization (1/5th) of an upfront fee paid for debentures in the current year if the Tribunal has already allowed the entire amount as a deduction in a previous assessment year?

-

Corporate Guarantee (Transfer Pricing): Does providing a corporate guarantee to an Associated Enterprise (AE) constitute an “international transaction,” and how should the commission be benchmarked?

-

Standby Letter of Credit (SBLC): Does providing an SBLC for an AE using the assessee’s credit limits constitute an international transaction, and what is the limit of the Transfer Pricing (TP) adjustment?

Facts

-

Upfront Fee: The assessee paid a non-refundable fee of Rs. 19.14 crores for issuing Non-Convertible Debentures (NCDs) with a 5-year tenure. While the assessee amortized this cost in its books, the Tribunal had already allowed the entire expenditure as a one-time deduction in an earlier assessment year. Despite this, the AO allowed 1/5th of the amount in the current year (likely following the amortization schedule).

-

Corporate Guarantee: The assessee provided guarantees for its AEs’ project financing. The TPO treated this as an international transaction and calculated a guarantee commission.

-

SBLC: The assessee arranged for a Standby Letter of Credit (SBLC) from its Indian bank (using its own non-fund limits) for its foreign AE. The TPO treated this as a service/transaction requiring a fee.

Decision

1. Regarding Upfront Fee (Section 37(1)):

-

No Double Benefit: Since the Tribunal had already adjudicated that the entire upfront fee was deductible in the year it was incurred (earlier year), there was no unamortized balance left to claim in subsequent years.

-

Reversal: Allowing 1/5th of the amount in the current year would amount to a double deduction for the same expense. Therefore, the AO’s allowance of 1/5th was incorrect and liable to be reversed. [In favour of revenue]

2. Regarding Corporate Guarantee (Section 92B):

-

International Transaction: The Tribunal affirmed that providing a corporate guarantee to an AE falls squarely within the definition of an ‘international transaction’ under Section 92B.

-

Benchmarking Adjustment: However, when determining the Arm’s Length Price (ALP) for the commission, the TPO must account for any reciprocal guarantees or benefits the assessee received from the AEs. [Partly in favour of revenue]

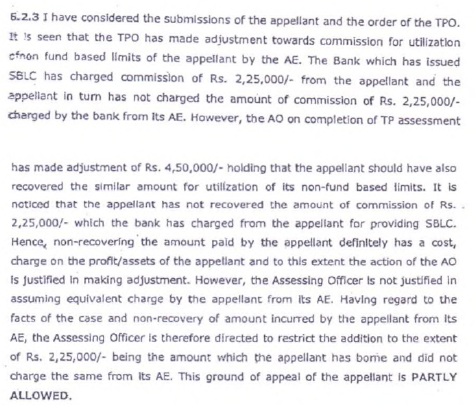

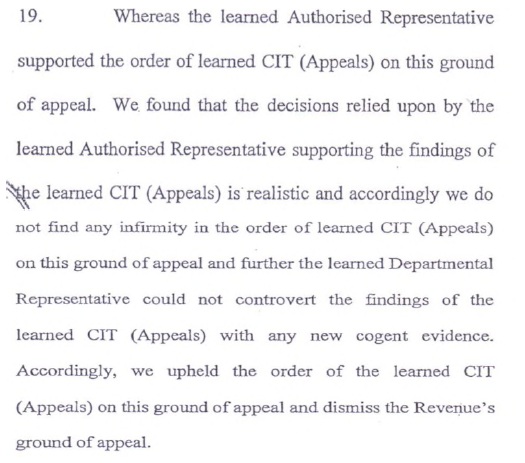

3. Regarding SBLC (Section 92B):

-

Service to AE: Utilizing the assessee’s own credit limits to provide an SBLC for an AE is a valuable service and constitutes an international transaction.

-

Adjustment Cap: The TP adjustment should be restricted to the cost incurred but not recovered. Specifically, the adjustment is limited to the commission paid to the bank (for the SBLC) that was not recovered from the AE. [Partly in favour of revenue]

Key Takeaways

-

One-Time vs. Amortized: If a court allows an expense fully in Year 1 (treating it as revenue expenditure), the taxpayer cannot continue to claim amortization for the same expense in books for tax purposes in future years.

-

Guarantees are Taxable: Providing guarantees or SBLCs for subsidiaries is not a “shareholder activity” generally exempt from TP; it is a chargeable service.

-

Cost Recovery: For SBLCs, the primary TP risk is the bank charges borne by the Indian parent. Recovering these charges from the foreign subsidiary neutralizes most of the TP risk.

and Ms. Padmavathy S., Accountant Member

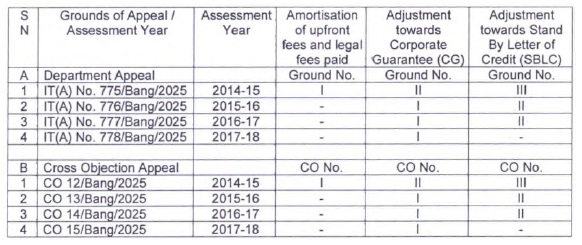

CO Nos. 12-15 (Bang) OF 2025

[Assessment years 2014-15, 2015-16, 2016-17 and 2017-18]

“Ordinarily, expenditure incurred wholly and exclusively for the purpose of business must be allowed in its entirety in the year in which it is incurred. It cannot be spread over a number of years even if the assessee has written it off in his books over a period of years”.

“7. We find that the impugned order of the Tribunal inter alia has followed the decisions of the Bombay Bench of the Tribunal in cases of VVF Ltd. v. Dy. CIT [IT Appeal No. 673 (Mum.) of 2006] and Dy. CIT v. Tech Mahindra Ltd. SOT 141 (Mum.) (URO) to reach the conclusion that ALP in the case of loans advanced to Associate Enterprises would be determined on the basis of rate of interest being charged in the country where the loan is received/consumed. Mr. Suresh Kumar the learned counsel for the revenue informed us that the Revenue has not preferred any appeal against the decision of the Tribunal in VVF Ltd. (supra) and Tech Mahindra Ltd. (supra) on the above issue. No reason has been shown to us as to whythe Revenue seeks to take a different view in respect of the impugned order from that taken in VVF Ltd. (supra) and Tech Mahindra Ltd. (supra). The Revenue not having filed any appeal, has in fact accepted the decision of the Tribunal in VVF Ltd. (supra) and Tech Mahindra Ltd. (supra). 8. In view of the above we see no reason to entertain the present appeal as in similar matters the Revenue has accepted the view of the Tribunal which has been relied upon by the impugned order. Accordingly, we see no reason to entertain the proposed questions of law.”

“15. We have considered the rival submissions as well as the relevant material on record. At the outset we note that the assessee has raised the objection before the DRP as recorded in paras 6.1 and 6.2 as under :

‘6.1 Grounds 1, 2 and 3 are considered together for convenience. Briefly stated the assessee provides software development and information technology enabled services (ITES) to its AEs. During the FY 2005-06 the assessee provided a corporate guarantee to a third party bank on behalf of an AE but failed to charge a fee for the guarantee. The assessee conducted a TP study and concluded that this transaction was at arm’s length however during audit proceedings the TPO rejected the analysis of the assessee and made adjustments to this transaction. The taxpayer cites the order of Four soft Ltd wherein the Hon’ble ITAT Hyderabad observed as under:

“We find that the TP legislation provides for computation of income from international transaction as per section 92B of the Act. The corporate guarantee provided by the assessee company does not fall within the definition of international transaction. The TP legislation does not stipulate any guidelines in respect to guarantee transactions. In the absence of any charging provision, the lower authorities are not correct in bringing aforesaid transaction in the TP study. In our considered view, the corporate guarantee is very much incidental tothe business of the assessee and hence, the same cannot be compared to a bank guarantee transaction of the Bank or financial institution.”

6. 2 It has also been submitted by the assessee that the transaction arising on account of ownership linkage and which derives large from the reputation of the group necessarily implies that there can be no guarantee acceptable to the banker which can be provided by the independent third party. The guarantee provided by financial institutions are characteristically different compared to the guarantee provided by the parent. The advantages arising to the parent itself from providing guarantee in lieu of equity support or financial support is also not capable of being evaluated satisfactorily. These differences between the alleged controlled transaction and the guarantee provided by independent parties in the uncontrolled transaction are not capable of being evaluated so as to arrive at determination of the fair uncontrolled price. In the circumstances, computation methodology of TP exercise may fail. It is undisputed that failure of computation mechanism results in failure of the charge.’

Thus it is clear that grievance of the assessee against the order of the TPO on the issue of ALP in respect of guarantee fees is limited only regarding the correct ALP. We further note that prior to the decisions of Mumbai Bench in the case of Siro Clinpharm Pvt. Ltd. v. DCIT (supra) there are series of decisions of this Tribunal including the decision in cases of Four Soft Pvt. Ltd. Vs,.DCIT (supra) and Nimbus Communication Ltd. v. ACIT (supra) wherein the Tribunal has taken a consistent view that providing corporate guarantee to AE is an international transaction however, the ALP of such transaction was to be computed having regard to the financial consideration as the nature of transaction between the related parties. The Tribunal has taken a view that the guarantee fees for providing corporate guarantee should not be more than 0.5%. The Hyderabad Benches of this Tribunal in the case of Four Soft Pvt. Ltd. Vs.DCIT (supra) has considered an identical issue in paras 24 to 26 as under :

24. It is noted by the TPO, during the F.Y. 2005-06 the assessee has provided bank guarantees on behalf of its Overseas subsidiary, Foursoft BV, Netherlands for an amount of Rs.69,81,16,000/- which is continuing for the year under consideration also. The TPO following the order passed for A.Y. 2006-07 treated the commission changed by ICICI Bank at 3.75% arms length price for the corporate guarantee provided by the assessee to its AE worked out the TP adjustment of Rs.2,61,79,350/-. The DRP also rejected assessee’s objection on the issue.

25. We have heard the parties and perused the material on record. The sum and substance of the submissions made by the learned AR is, the corporate guarantee provided by the assessee cannot be equated to bank guarantee and resultantly the commissionrate for bank guarantee cannot be applied to the corporate guarantee. It was submitted that the corporate guarantee is nothing but an additional guarantee provided by the parent company and it does not involve any cost or risk to the shareholders. It was submitted that since the corporate guarantee was given keeping in view paramount business interest of the parent company it has to be allowed as business expenditure. It is the further submissions of the learned AR that the retrospective amendment effected to section 92B of the Act, by Finance Act, 2 012 by insertion of Explanation (i)(c) to section 92B also has not enlarged the scope of the ‘international trans action’ to include the corporate guarantee in the nature provided by the assessee. The learned AR further contended that the issue is covered in favour of the assesseeb y virtue of the order passed by the Tribunal in assessee’s own case for AY 2006-07 (supra).

25. 1 The learned DR, on the other hand, submitted that by virtue of the amendment made to section 92B of the Act with retrospective effect from01/04/2002, the corporate guarantee provided by the assessee is to be considered as an international transaction, and, therefore, the Assessing Officer was justified in determining arm ‘s length price of such transaction.

25. 2 Having considered the submissions of the parties, we are unable to accept the contention of the learned AR that corporate guarantee of the nature provided by the assessee will not come within the meaning of international transaction in term s with section 92B of the Act. It is not disputed that section 9 2B of the Act has been amended by the Finance Act, 201 2 with t he insertion of Explanation I (c) with retrospective effect from 01/ 04/200 2. Explanation (i)(c) t o section 92B, reads as under:

“capital financing, including any type of long-term or short-term borrowing, lending or guarantee, purchase or sale of marketable securities or any type of advance, payments or deferred payment or receivable or any other debt arising during the course of business. ”

25. 3 A reading of the aforesaid clause from the Explanation would make it clear that the corporate guarantee provided by the assessee comes within the scope and ambit of ‘ international transaction’ as per the aforesaid clause. Therefore, the contention of the learned AR that the issue is covered in favour of the assessee by virtue of the order passed in assessee ‘s own case for A Y 2006-07 no longer holds good since the order passed by the coordinate bench is prior to the amendment made to provision of sect ion 9 2B of the Act. It will be pertinent to mention here that this issue was also considered by the ITAT Mumbai Bench in case of Mahindra & Mahindra v. DCIT in ITA No. 8597/Mum/2010, 54 SOT (UR) 146. The coordinate bench ofthis Tribunal while considering similar argument advanced on behalf of the assessee by placing reliance on the decision of the Four Soft Ltd.(supra), held as under: “15. 2 After hearing the rival submissions we feel that Assessing Officer will have to follow the decision of the ITAT Hyderabad or the amended provision of the Act in this regard. If the Finance Bill of 2012 is passed by the Parliament amending the provisions of section 92B, with effect from 1st April, 2002, he will have to ignore the decision of the ITAT Hyderabad. In case section 92B is not amended with retrospective effect, he should grant relief to the appellant. ”

25.4 In the aforesaid view of the matter, we agree with the TPO that ALP of the corporate guarantee has to be determined as it falls within the scope and ambit of an international transaction after the retrospective amendment to section 92B. However, it appears that the TPO has applied the rate of 3.75 %, which is applicable to bank guarantee issued by the bank. As the corporate guarantee is not in the nature of bank guarantee, the rate applicable to bank guarantee provided by the bank cannot be applied to corporate guarantee which is provided by a group company. In case of Glenmark Pharmaceuticals V s. ACIT in ITA No. 5031/Mum / 2012, dated 13/11/2013, the Mumbai Bench of the Tribunal after analysing the facts in that case had held that 0.53 % corporate guarantee rate in that case was appropriate. The ITAT Hyderabad Bench in case of Infotech Enterprises Ltd. in ITA No.115/Hyd/ 2011 and in ITA No. 2184/Hyd/ 2011, dated 16/01/2014 while considering identical issue of determining ALP of corporate guarantee provided by the assessee to its AE followed the ratio laid down in case of Glenmark Pharmaceuticals v. ACIT (supra) and remitted the issue back to the TPO to decide the quantum of corporate guarantee rate by following the method adopted in case of Glenmark Pharmaceuticals (supra).

26. Since the issue in the present case is identical to the issue decided by the ITAT, Hyderabad Bench in case of Infotech Enterprises (supra), following the same, we also remit this issue to the file of the TPO to decide the quantum of corporate guarantee rates accordingly. If the assessee is able to bring on record any comparables with regard to corporate guarantee, the TPO may also consider the same while determining ALP of corporate guarantee. The TPO must provide a reasonable opportunity of being heard to the assessee before deciding the issue. This ground is allowed for statistical purposes.”

It is pertinent to note that in case of corporate guarantee provided to a bank or financial institution on behalf of the AE, the assessee creates a charge on its assets in favour of the bank/financial institution and to that extent the transaction of providing corporateguarantee is having bearing on the assets of the assessee and in turn the assessee cannot use those assets under charge for the purpose of availing further financial credit/loans from the bank/financial institution. Thus this Tribunal held that by providing corporate guarantee falls in the definition of international transactions as per Section 92B(1) without considering the Explanation to the said Section. As we have discussed in the foregoing part of this order that the Tribunal has been taken a consistent view that corporate guarantee provided to the AE falls in the ambit of international transactions as per Section 92B(1) even without considering the Explanation inserted vide Finance Act, 2012. The Mumbai Bench of this Tribunal in the case of Siro Clinpharm Pvt. Ltd. v. DCIT (supra) has restricted its finding only to the applicability of Explanation in the cases where the assessment was completed prior to the insertion of the said Explanation retrospectively. Even otherwise the earlier decisions of the Tribunal on this issue were not considered by the Delhi Bench of the Tribunal. In the case of M/s. Nimbus Communication Ltd. v. ACIT in ITA Nos.6816/Mum/2010 and 7105/Mum/2011, the Tribunal vide order dt.7.8.2013 has considered an identical issue in paras 4 & 5 as under

” 4. As regards the issue raised in ground No. 2 relating to TP adjustment made on account of guarantee commission in respect of corporate guarantee given by the assessee to its Associated Enterprises (AEs) for obtaining bank loans, the ld. representatives of both the sides have agreed that a similar issue was involved in assessee’s own case for the immediately preceding year i.e. A.Y. 2005 06 and the Tribunal vide its order dated 12-06-2013 passed in ITA No. 3664 & 2359/Mum/2010 has already decided the same vide para No. 9 & 10 which read as under:-“9. We have considered the rival submissions and also perused the relevant material available on record. For the guarantee given to the bank against the financial assistance given to its AEs, no commission was charged by the assessee company on the ground that the said AEs were not benefited by the guarantee so given and it was the assessee who benefited as a result of commercial benefits secured for future. In support of this stand of the assessee, the ld. counsel for the assessee has contended that business strategy should be taken into consideration while making any TP adjustments in respect of such transactions and has relied on the OECD Transfer Pricing Guidelines issued in 2010. As stated in para 1.59 of the said guidelines, the business strategies should also be examined in determining comparability for transfer pricing purposes and certain illustrations of such business strategies are also given therein. As stated in para 1.60 of the said guidelines which has been relied upon by the ld. Counsel for the assessee, business strategies also could include market penetration schemes and taxpayer seeking to penetrate a market or to increase its market share might temporarily charge aprice for its product that is lower than the price charged for otherwise comparable products in the same market. As explained further, a tax payer seeking to enter a new market or expand (or defend) its market share might temporarily incur higher costs and hence achieve lower profit levels than other taxpayers operating in the same market. In our opinion, the relevant facts of the present case do not indicate that there was any such business strategy adopted by the assessee in not charging commission in respect of guarantees issued for its Associated Enterprises. As a matter of fact, there is nothing to suggest that any such business strategy was adopted by the assessee with specific intention or motive and the case has been sought to be made out merely on the basis of commercial expediency by claiming that the assessee was benefited as a result of giving the guarantees in the form of commercial benefits secured for future. In our opinion, such commercial expediency cannot be equated with business strategy, which is specific and well laid out. As rightly held by the ld. CIT(A), a financial loan guarantee is a commitment entered into by the assessee company with a third party lender of its Associated Enterprises which obliges the assessee company to cover the risk of default by its Associated Enterprise and this act thus involves performance or carrying out of service to cover the risk of default for which “price” has to be charged. Even the OECD Transfer Pricing Guidelines 2010 supports this view in para 7.13 where it is explained that where higher credit rating of Associated Enterprise is due to a guarantee by another group member, such association positively enhances the profit making potential of that Associated Enterprise. We, therefore, find ourselves in agreement with the contention of the ld. D.R. that there was a clear benefit accrued to the Associated Enterprises by the guarantee provided by the assessee and when such benefit was passed on by the assessee to the said Associated Enterprises, guarantee commission should have been charged at arm’s length price. The commercial relationship between the assessee and its Associated Enterprises is distinct and separate from the transactions of giving guarantee and such transactions have to be considered and examined independently in order to determine the arm’s length price.

10. As regards the rate of guarantee commission, it is noted that the arm’s length price of guarantee commission was determined by the TPO by applying CUP method and the arithmetic mean of 1.5% of the guarantee commission charged by the HSBC Bank in the range of 0.15 to 3% was taken as arm’s length price. The ld. CIT(A) upheld the CUP method applied by the TPO but adopted the rate of 0.25% of guarantee fee as arm’s length price relying on the decision of French Court in the case of Societe Carrefour. The ld. D.R., at the time of hearing before us has relied on the decision of the co-ordinate Bench of this Tribunal in the case of M/s Everest Kanto Cylinder Ltd. (supra) wherein while accepting the CUP method as the most appropriate method for benchmarking the guarantee fee, the Tribunal accepted0.5% guarantee fee/commission to be at arm’s length after taking into consideration the rates of guarantee commission charged by various banks including the guarantee commission charged by the HSBC Bank in the range of 0.15% to 3%. Since the facts involved in the present case are materially similar to the facts involved in the case of Everest Kanto Cylinder Ltd. (supra), we prefer to follow the decision rendered by the co-ordinate Bench of this Tribunal in the said case over the decision of French Court in the case of Societe Carrefour (supra). We, accordingly modify the impugned order of the ld. CIT(A) on this issue and direct the A.O. to recompute the commission for guarantee given by the assessee to its Associated Enterprises @ 0.5% being the arm’s length price. Ground No. 1 of Revenue’s appeal is thus partly allowed whereas ground No. 2 of assessee’s appeal is dismissed”.

5. As the issue involved in the year under consideration as well as all the material facts relevant thereto are similar to A.Y. 2005-06, we respectfully follow the order of the co-ordinate Bench of this Tribunal for A.Y. 2005-06 and direct the A.O. to restrict the TP adjustment by recomputing the commission for guarantee given by the assessee to its AEs at 0.5% being the arm’s length price. Ground No. 2 of the assessee’s appeal for A.Y. 2006-07 is partly allowed.”

As it is clear that the Tribunal has followed the decision of the Tribunal for the earlier assessment year and while taking a consistent view held that guarantee provided by the assessee gives the benefit to the AE and such benefit was passed on by the assessee to the said AE and therefore should have been charged at ALP.”