ORDER

Manish Agarwal, Accountant Member.- The captioned appeal is filed by the assessee against the assessment order dated 29.10.2024 passed u/s 143(3) r.w.s. 144C(13) of the Income Tax Act, 1961 (“the Act”) pertaining to assessment year 2021-22.

2. Brief facts of the case are that assessee is a company engaged in the business of manufacturing and trading of garments, menswear, sportswear etc. besides having income from generation of power and energy through windmill. The return of income was filed on 15.03.2022, declaring total income of INR 21,61,874/- and MAT was paid on the book profits of INR 2,84,94,002/- u/s 115JB of the Act. The case of the assessee was selected under CASS and notice was issued u/s 143(2) followed by notices u/s 142(1) alongwith questionnaire. In the instant case, assessee was having transactions with its AE therefore, the matter was referred for determination of ALP of international transaction to the TPO who vide its order dated 13.10.2022 proposed adjustment of INR 53,24,17,100/- on account loan written off. Thereafter, AO passed the draft assessment order dated 30.12.2023 u/s 144C(1) of the Act wherein AO has proposed the following additions/disallowances:-

| S.No. |

Particulars |

Amount (INR) |

| 1. |

T.P. adjustment of loan written off |

53,24,17,100/- |

| 2. |

Disallowance of expenses on Research and Development |

6,59,31,449/- |

| 3. |

Disallowance of expenses pertaining to Unit eligible for deduction u/s 80-IA |

42,16,800/- |

| 4. |

Disallowance of deduction u/s 80-IA of the Act |

21,84,942/- |

| 5. |

Addition on account of interest on loans given to sister concern |

30,28,138/- |

Accordingly, total income of the assessee was proposed to be assessed at INR 60,99,40,303/-.

3. Against the draft order, assessee filed objections before the ld. DRP who vide its order dated 30.09.2024, sustained the additions proposed on account of written-off of loan amount given to its AE and with respect to other additions/disallowance, AO was directed for making certain verifications/adjustments. Thereafter, the AO passed the final assessment order u/s 143(3) r.w.s. 144C (13) of the Act wherein after following the directions of DRP, the AO made the additions/disallowance as proposed in the draft assessment order at INR 60,77,78,429/- and further re-computed the book profit u/s 115JB of the Act by making additions of the amount of INR 60,77,78,429/- and the book profit was thus assessed at INR 63,62,72,431/-.

4. Aggrieved by the said order, the assessee is in appeal before the Tribunal wherein the assessee has raised following grounds of appeal:

| * |

|

“That on facts and circumstances of the case and in law the impugned final assessment order dated 29.10.2024, passed by the learned Assessing Officer (‘AO’) under section 143(3) read with section 144C(13) of Income Tax Act. 1961 (‘the Act’) is without jurisdiction and bad in law. |

| * |

|

That on facts and circumstances of the case and in law the action of Ld. AO in passing the order dated 29.10.2024 under section 143(3) read with section 144C (13) of the Act without due consideration of the replies and submissions of the Assessee/Appellant is bad in law. |

Re: Transfer Pricing Addition: Write-off of loan/business advance given to the Wholly Owned Subsidiary (‘WOS’) of the Assessee/Appellant, i.e. Matrix Clothing Pvt. Ltd. Jordan LLC

| • |

|

That on facts and circumstances of the case, Id. AO and ld. Dispute Resolution Panel (‘DRP’) erred in confirming the adjustment of Rs 53,24,17,100/- proposed by ld. Transfer Pricing Officer (‘TPO’) in the order dated 30.10.2023 passed under section 92CA (3) of the Act, without appreciating it’s scope. |

| • |

|

That on facts and circumstances of the case, Id. AO and Ld. DRP erred in confirming the Transfer Pricing Adjustment proposed by the Id. TPO on the write-off of business advance/loan given by the Assessee/Appellant to its wholly owned subsidiary (‘WOS’), Matrix Clothing Pvt. Ltd Jordan LLC, without appreciating that the said transaction was already disclosed and benchmarked using other method by the Assessee/Appellant. |

| • |

|

That on facts and circumstances of the case, Id. AO and Id. DRP erred in confirming the Arm’s Length Price (‘ALP’) of the write off of loan to its AE determined at ‘NIL’ by Id. TPO, ignoring the status of RBI proceedings. |

| • |

|

That without prejudice to the above, Id. AO and Ld. DRP erred on facts and circumstances of the case in confirming the adjustment proposed by Id. TPO in determining the ALP of loan write-off to its WOS at ‘NIL’ without disputing/discrediting the documents submitted by the Assessee during the course of Transfer Pricing proceedings. |

| • |

|

That on facts and circumstances of the case, Id. AO erred in disallowing the loan write-off without appreciating that the loan extended to WOS was for the purpose of Business of the Assessee/Appellant. |

| • |

|

That on facts and circumstances of the case and in law, Id. AO erred in not appreciating that since the Assessee/Appellant had advanced the loan to its WOS for the purpose of business expansion in Jordan and due to incapacity of the foreign entity, i.e., Indo Jordan Clothing LLC, the loan became irrecoverable and was written off, hence the same is allowable as a business deduction. |

| • |

|

That on facts and circumstances of the case, Id. AO erred in disallowing loan write-off despite the fact that the said loan was advanced to WOS purely on account of commercial expediency for enhancing the business activities of the Assessee/Appellant. |

| • |

|

That on facts and circumstances of the case, Id. AO erred in law and on facts and circumstances of the case in not appreciating that writeoff of the unrealised principal amount of loan and interest accrued thereon would be an allowable deduction in terms of section 36(1)(vii) read with section 36(2) of the Act. |

| • |

|

That without prejudice, Id. AO erred in law and on facts and circumstances of the case, in not appreciating that the amount written off in the present circumstances can be claimed as a loss incidental to business in terms of section 37(1) of the Act. |

| • |

|

That on facts and circumstances of the case and in law, Ld. AO and Ld. DRP erred in confirming the Transfer Pricing adjustment of Rs. 53,24,17,100/-proposed by Id. TPO, without disputing/discrediting the documents submitted by the Assessee/Appellant during the course of Assessment proceedings. |

Re: Research and Development Expenses: Disallowance of deduction of Rs. 6,59, 31. 449 under section 35(2AB) of the Act

| • |

|

That on facts and circumstances and in law, the action of Ld. AO in disallowing the deduction of Rs. 6,59,31,449/- under section 35(2AB) of the Act is bad in law. |

| • |

|

That on facts and circumstances and in law, Ld. AO erred in disallowing the deduction under section 35(2AB) of the Act, merely on surmises and conjectures and without affording adequate opportunity of being heard to the Assessee. |

| • |

|

That on facts and circumstances and in law, Ld. AO erred in disallowing deduction under section 35(2AB) of the Act and stating the no details were submitted by the Assessee/Appellant to substantiate its claim of deduction which is contrary to the records of the case. |

| • |

|

That on facts and circumstances and in law Ld. AO erred in disallowing the deduction of Rs. 6,59,31,449/- under section 35(2AB) of the Act without appreciating that the Assessee/Appellant itself had made an assertion that it is not eligible for weighted deduction under section 35(2AB), however the expenditure towards scientific research are allowable under section 37(1) of the Act. |

| • |

|

That on facts and circumstances of the case, Ld. AO erred in disallowing deduction under section 35(2AB) of the Act by merely following the assessment order for AY 2017-18. |

| • |

|

That on facts and circumstances and in law, Id. AO erred in making the disallowance by arbitrarily holding that no claim under section 37(1) of the Act has been made by the Assessee/Appellant in the Income Tax Return. |

| • |

|

That without prejudice to the above, the claim of expenditure incurred on scientific Research & Development undertaken by the Assessee/Appellant ought to be allowed under section 37(1) of the Act. |

Re: Disallowance of Deduction under section 801A of the Act

| • |

|

The on facts and circumstances of the case and in law, the action of Ld. AO and Ld. DRP in disallowing the deduction of Rs. 21,84,942/-under section 801A and expenditure of Rs. 42,16.800/- is erroneous and bad in law. |

| • |

|

That Ld. AO and Ld. DRP erred on facts and circumstances and in law in making the addition of Rs. 42.16,800/- and Rs. 21,84,942/- under section 801A of the Act, merely on surmises and conjectures, without affording adequate opportunity of being heard to the Assessee. |

| • |

|

That on facts and circumstances of the case and in law, Ld. AO erred in disallowing the deduction under section 801A of the Act without disputing and discrediting the documents submitted by the Assessee in the course of Assessment proceedings. |

| • |

|

That on facts and circumstances of the case and in law, Ld. AO erred in disallowing the deduction under section 801A of the Act, despite the Assessee/Appellant being eligible for deduction as it satisfies the conditions prescribed under section 80-IA of the Act. |

| • |

|

That on facts and circumstances of the case and in law, Ld. AO erred in disallowing the deduction under section 801A of the Act, without establishing as to how the Assessee/Appellant was not eligible under the provisions ascribed under section 80-IA of the Act. |

| • |

|

That on facts and circumstances of the case and in law, Ld. AO erred in disallowing the deduction under section 801A of the Act, without appreciating that the Assessee/Appellant has an agency agreement with Suzlon Global Services Ltd. for management of the windmills in Gujarat and as such no separate administrative expenses have been incurred by the Assessee/Appellant. |

| • |

|

That without prejudice to the above, Ld. AO erred in making addition of Rs. 21,84,942/- by arbitrarily applying rate of 0.15% over total expenditure of Rs. 21,81,12,00,000/- in addition to reducing the claim of deduction under section 801A of the Act from 42,16,800/- to Nil, without ascribing or recording any justifiable reason for the same. |

| • |

|

That without prejudice to the above, Ld. AO erred on facts and circumstances and in law in making the impugned addition, by not appreciating that the disallowance by applying the rate of 0.15% over the head of expenditure mentioned in the show cause notice would at best be Rs. 24,000/-. |

| • |

|

That on facts and circumstances of the case and in law, the action of Ld. AO in disallowing the deduction under section 801A of the Act without appreciating the facts that during previous assessment years the claim of deduction under section 80-1A of the Act has never been disputed or denied by the Department and there being no change in facts for the year under consideration, is against the well settled principles of consistency. |

Re: Interest Free loans given to subsidiary.

| • |

|

That on facts and circumstances of the case and in law, Id. AO erred in making the addition of Rs. 30,28,138/-, merely on conjectures and surmises without affording adequate opportunity of being heard to the Assessee/Appellant. |

| • |

|

That on facts and circumstances of the case, the action of Id. AO in making addition of notional interest on interest fee loans/advances given by the Assessee/Appellant to its subsidiary, Matrix Horizons Pvt. Ltd., of Rs. 30,28,138/-is erroneous and bad in law. |

| • |

|

That on facts and circumstances of the case, the action of Id. AO in imputing rate of interest @10.75% on the amount of loan advanced, i.e., Rs. 2,81,68,722/-, to its subsidiary for commercial expediency, is arbitrary, erroneous and bad in law. |

| • |

|

That on facts and circumstances of the case and in law, Id. AO erred in making the addition of notional interest without disputing/discrediting the submissions regarding availability of own funds with the Assessee/Appellant during the course of assessment proceedings. |

| • |

|

That without prejudice to the above, on facts and circumstances of the case and in law, Id. AO erred in stepping into the shoes of the business of the Appellant/Assessee which is contrary to the well-established principles of law. |

| • |

|

That without prejudice to the above, Id. AO erred in facts and circumstances of the case and in law in arbitrarily holding that similar additions have been made in the previous assessment years, which is contrary to the records.” |

5. Ground of appeal Nos. 1 & 2 raised by the assessee are general in nature, hence not adjudicated.

6. Ground of appeal No.3 raised by the assessee having various sub-grounds in bullets are with respect to the addition of INR 53,24,17,100/- made by disallowing the claim of loan written off which was given to its wholly owned subsidiary company situated at Jordan namely, Matrix Clothing Pvt. Ltd. Jordan LLC (“Matrix Jordan”).

7. Before us, Ld.AR for the assessee submits that assessee company has set up a special purpose vehicle (“SPV”) Matrix Jordan at Jordan. In Matrix Jordan total equity investment of assessee is of 50,000 shares of face value of one Jordan Dinar per share. The said company was incorporated to acquire Indo Jordan Clothing LLC (Jordan LLC), a company engaged in the similar line of business as of the assessee i.e. manufacturing and export of garments accessories. The assessee company has advanced loans to its SPV created since 2016 which bears interest at the rate Libor Plus applicable interest rates and assessee also provided corporate guarantee to the banks in respect of working capital loans and/or credit limits taken by Matrix Jordan. The assessee has advanced loans to Matrix Jordan from FY 2016-17 to FY 2020-21. Ld.AR submits that during the previous year relevant to assessment year under appeal, it was found that the company Jordan LLC has failed to commit the time limit payment of interest as well as principal amount advanced and therefore, the management of the assessee decided to dispose off/sale the investment made in the company Jordan LLC and which were finally sold on 31.01.2021. Thereafter, the assessee had booked the loss of INR 5324.17 Lakhs on account of bad debts being loans written off given to Matrix Jordan in the year under appeal and the balance amount of INR 22,90,14,404/- was claimed as written off of loans in subsequent Assessment Years. Ld.AR further submits that company, Jordan LLC was running smoothly for the period from FY 2017-18 to 2019-20 and due to COVID-19 pandemic, its main buyer M/s Nygard International, USA to whom more than 70% of goods manufactured were sold, filed bankruptcy petition in USA and thus the business of Jordan LLC was very badly affected and ultimately, adversely affected the business of assessee company. The copy of the relevant documents filed by the M/s. Nygard International, USA are placed at page 292 to 295 of the Paper Book. Ld.AR submits that due to this sudden change in the circumstances resulting into almost closure of the business/heavy losses to Jordan LLC and in turn to Matrix Jordan, the management of the assessee has decided to sell the shareholding in Jordan LLC held through SPV i.e. Matrix Jordan.

8. As per share purchase agreement dated 14.02.2021, placed at page 246 to 286, assessee has entered into an agreement for sale of shares with one company namely United Creations Apparel Manufacturing LLC to whom entire shareholding Jordan LLC was transferred for a sum of 35,95,025 USD.

8.1. Thereafter, assessee has worked out the amount of outstanding loans as on the date of sale of sale of shares of Jordan LLC in terms of AS-28 which was claimed as written off during the year. The said amount is tabulated as under:-

| Particulars |

Amount in Rs. |

| Outstanding loan to Matrix Jordan on the date of SPA (14.02.2021) |

71,02,12,802 |

| Add: Interest on outstanding loan |

3,59,98,457 |

| Total Outstanding (A) |

74,62,11,259 |

| Less: Estimated re-sale value of balance inventoiy of IJC @ Pg 23 7 |

4,79,51,304 |

| Less: value of outstanding receivables of Nygard @ Pg 23 7 |

16,58,52,855 |

| Net Write off |

53,24,17,100 |

9. Ld.AR further submits that assessee has filed application before Reserve Bank of India (“RBI”) on 30.09.2021 for granting approval for writing off of loan given to Matrix Jordan. The RBI vide letter dated 08.05.2023 had intimated that since the said application was filed delayed, thus it was suggested to apply for the compounding of offence of delay in filing the application. In compliance thereof, the assessee filed application for compounding of offence before the RBI, all such correspondences are placed at page 332 to 350 of the Paper Book. Ld. AR then drew our attention to the compounding order of RBI dated 30.10.2023, placed at page 357 to 360 of PB, wherein the RBI in terms of section 13 of FEMA Act, had compounded the offence subject to payment of compounding fee of INR 40,78,985/- which was deposited by the assessee. It is thus submitted by Ld.AR that once the RBI has granted approval for writing off loans by way of compounding of offence, the sole allegation of lower authorities for not allowing the deduction towards writing off of loans that no approval was taken from RBI, has duly been complied with and therefore the assessee is entitled for deduction of written off of loan advanced to Matrix Jordan.

9.1. In this regard, Ld.AR made submission before the TPO which are placed at pages 150 to 329 of Paper Book. Ld. AR submits that written-off of loans by the assessee to its wholly own subsidiary company, Matrix Jordan cannot be treated as international transaction u/s 92(1)(vi) of the Act, since it is a unilateral action on the part of the assessee and therefore, it cannot be termed as “transaction” nor could be characterized as “international transaction” as it would have to be demonstrated that the transaction arose pursuant to the arrangement, understanding or action in concert. In this regard, Ld.AR filed a written submission which reads as under:-

“The legal position in this regard is as follows:

| • |

|

Section 92(1) of the Income Tax Act, 1961 (‘the Act’) provides for the computation of ‘income’ arising from an ‘international transaction’ having regard to the arm’s length price. The essential elements that should, thus, exist for the application ofprovision of section 92 of the Act are ‘income’ and ‘international transactions’. |

| • |

|

Sub-section (2) of section 92 of the Act further provides that, where in an international transaction, two or more associated enterprises enter into a mutual agreement or arrangement for allocation or apportionment or contribution to any cost or expenses incurred or to be incurred in connection with the benefit, service or facility provided or to be provided by one or more enterprises, the cost or expense allocated or apportioned or contributed by such enterprise shall be determined having regard to the arm’s length price of such benefit, service or facility as the case may be. |

| • |

|

The term “International transaction” is defined in section 92B of the Act to mean a transaction between two or more ‘associated enterprises, either of whom is a non-resident and covers the following: |

| (a) |

|

Any ‘transaction’ having a bearing on profits, income, losses or assets of the enterprise; |

| (b) |

|

A mutual agreement or arrangement between two or more associated enterprises for allocation or apportionment of any contribution, any cost or expense incurred in connection with benefit, service or facility provided to any of such associated enterprises; |

| (c) |

|

Transactions referred in clauses (a) to (e) of Explanation (i) to that section [inserted by Finance Act, 2012, w.e.f. 1.04.2002] |

In view of the aforesaid, clause (b), which covers agreement or arrangement for allocation or apportionment of cost in terms of the second limb of section 92(8)(1) of the Act, is not applicable because when no cost is incurred, there can be no question of its allocation or apportionment. Therefore, in the aforesaid background facts, the issue for consideration at hand is whether:

| (i) |

|

the write-off of loans in the present case would constitute a ‘transaction’, having bearing on profits. income, losses or assets of such enterprises, so as to be regarded as an ‘international transaction’ in terms of the first limb of sub-section (1) of section 92B of the Act; and |

| (ii) |

|

clauses (a) to (e) of Explanation (i) to section 92B inserted by the Finance Act, 2012 is applicable and even if applicable, whether the transaction corporate guarantee is covered by any of the said clauses. |

It is submitted that the loans given by the assessee to its AE,

| (a) |

|

has been advanced by the assessee as a matter of commercial prudence, i.e., lower landing costs and to achieve economies of scale and |

| (b) |

|

in furtherance of the primary object of the assessee’s business. |

| (c) |

|

the loan advanced was in furtherance of the business since the ultimate utilization of the said loan was facilitation of Indo Jordan Clothing LLC, WOS of Matrix Clothing Pvt. Ltd Jordan LLC (WOS of the Assessee), which is in the same line of business as of the Assessee. |

The assessee had also (i) reported the transactions of loans given and (ii) repayment of loans on a year-on-year basis, which your good self has consistently accepted to be at arm’s length price. Further, as submitted supra, the assessee had been charging interest on such loans.

The write-off of loans is, in the respectful submission of the assessee, is the fall out of the already benchmarked transaction and is not an independent international transaction per-se. It is only due to the persistent losses suffered by the WOS and the consequent closure of SPV on 31.01.2021 the management had no option left but to write off the loans in the books of accounts for the year ended 31.03.2021. In the instant case, the assessee is primarily in the business of manufacturing of manufacturing garments, etc. and held investments in WOS engaged in the same business. The assessee, it is submitted, held a deep business interest in the said WOS by way of controlling interest.

Since the WOS was also engaged in similar business, the assessee, with the sole intent of promoting its business interest, advanced working capital loans to the said WOS.

It would be appreciated that the functions performed by an overseas entity were integrated and are part of the functions/business operations of the assessee. The assessee, for that purpose, as a shareholder and in furtherance of its own interest, was required to provide funds to the said company by way of loans.”

10. Ld.AR further submits that written-off of loans was a commercial decision taken in the interest of business and under commercial expediency which needs to be considered. For this, reliance is placed on the judgment of Hon’ble High Court in the case of CIT v. Cotton Naturals (I) (P.) Ltd.(Delhi) and, claimed that the written-off should be allowed in terms of section 36(1)(vii) r.w.s. 36(2) of the Act.

11. Alternatively, Ld.AR claimed that even otherwise deduction on account of written-off of loan should be allowed as business expenditure u/s 37(1) of the Act, as the loan was granted to the Matrix Jordan who was engaged in the same line of trade i.e. manufacturing of garments as normal business transaction. Ld.AR further submits that loan was given to Matrix Jordan in furtherance of the business of the assessee and had not created any capital assets of enduring nature. In the last, it is submitted that once approval is granted by the RBI as compounding, the amount of loan written-off should be allowed as business expenditure. It is thus, prayed that the lower authorities have wrongly made the disallowed the claim of the assessee of written off of loans advanced to Matrix Jordan made in regular course of business and part of the amount claimed as written off was already offered for tax in the shape of interest income in preceding assessment years therefore, the claim of the assessee should be allowed.

12. On the other hand, Ld.CIT DR for the Revenue vehemently supported the orders of the TPO, AO & Ld. DRP and submits that the assessee has claimed loans given to Matrix Jordan as write off. It was the submission that it is relevant to consider that out of the total sum claimed as bad debt, a sum of INR 33,97,99,500/- was further given as loan to Matrix Jordan during the previous year relevant to year under appeal which is more than 60% of the total claim of loan written off during the year by the assessee. Ld. CIT DR submits that no prudent businessman would made investment even a single penny in the business when it was in his knowledge that such business is not running well and possibility of the recovery of loan is very doubtful. Even the payment of interest on the previous loans was not done. He drew our attention to the fact that the assessee itself claimed that the investment held by its subsidiary Matrix Jordan in Jordan LLC was ultimately sold in terms of Agreement dated 14.02.2021 vide share purchases agreement though on 30.01.2021, buyer had principally agreed to purchase the shares. Ld. CIT DR drew our attention to the submission of the assessee that it was searching for the buyer for past few months even though, fresh funds of more than INR 30 Crores were advanced to Matrix Jordan in the month of January and February-2021 which clearly established that the assessee knowingly gave the fresh funds. Ld. CIT DR further submits that assessee has not taken the approval prior to the written off of the loans from RBI and thereafter had compounding of offence of not obtaining the approval in due course, cannot be termed as deemed approval of written off of loan. As per ld. CIT DR such compounding is towards the offence committed of delay in filing the application for approval of writing off of loan and therefore, claim of the assessee that RBI has granted the approval for written off of loan is not correct. Ld. CIT DR further submits detailed written submissions in addition to the oral arguments on this issue which is reproduced as under:-

“During the hearing in respect of the above-mentioned appeal before the Hon’ble ITAT arguments were made by the undersigned that the orders of lower authorities (TPO, AO and DRP) are justified and may be upheld by the Hon’ble ITAT. The undersigned had also put forth several arguments rebutting the contentions raised by the assessee before the Hon’ble ITAT. Additionally, the following written submission is made in the matter, which may kindly be taken into consideration.

1. Ground No. 1: Disallowance regarding write-off of loan of Rs.53,24,17,100/- given to wholly owned subsidiary Matrix Clothing Pvt. Ltd. Jordan LLC.

1.1 The undersigned strongly rely on the orders of the lower authorities (TPO, AO and DRP) in this regard in support of his arguments. This issue has been discussed by TPO at paras 7 to 11 on pages 5 to 6 of her order (pages 185-186 of the initial paper book filed with the appeal memo) from the arm’s length perspective. The AO has discussed this issue quite elaborately at paras 2.1 to 2.17 on pages 2 to 22 of his order (pages 11-31 of the initial paper book filed with the appeal memo). Ld. DRP has discussed this issue at paras 4.1.1 to 4.1.2 on pages 3 to 5 of their order (pages 124-126 of the initial paper book filed with the appeal memo). As argued by the undersigned, the assessee’s contentions are without merit and substance, and also suffers from contradictions.

1.2 In the grounds of appeal, the assessee has claimed that writeoff of the loan is an allowable deduction u/s 36(1)(vii) read with section 36(2) of the Income-tax Act, 1961 (“the Act”). The assessee has also claimed it as a loss incidental to business u/s 37(1) of the Act.

1.3 . During the hearing before the Hon’ble ITAT, the assessee raised the following contentions:

| (i) |

|

The assessee submitted that it had set up Matrix Clothing Pvt. Ltd. Jordan LLC (“Matrix Jordan”) in Jordan as a Special Purpose Vehicle (SPV) to acquire Indo Jordan Clothing LLC (“IJC Jordan”) which is also a Jordan based company. During the hearing before the Hon’ble ITATT, the assessee asserted at least 5 times that everything was alright before the COVID pandemic and the assessee’s subsidiary’s business in Jordan was doing quite well, and it was only during the COVID that the assessee’s subsidiary’s business suffered due to which the assessee had to write-off the loan given to Matrix Jordan (which had invested in and given loans to JC Jordan). |

| (ii) |

|

The assessee claimed that the sole reason for disallowance of the loan write-off by TPO and AO was lack of RBI’s approval in this regard. It further contended that considering the RBI’s approval vide order dated 31.10.2023 in CA No. 6229/2023 (pages 357-360 of the paper book submitted on 30.10.2025), the disallowance made by AO in this regard may be deleted. |

1.4 As regards the assessee’s first contention at para 1.3(1) above, I had highlighted certain facts during the hearing before the Hon’ble ITAT to establish that these contentions of the assessee are contrary to the facts on record (including those submitted before the AO during the assessment proceedings) and these are merely self-serving contentions of the assessee, I am briefly highlighting some of those facts as below:

| (i) |

|

As per details submitted by the assessee, the assessee has given huge amount of loan of Rs.83,03,95,425/- to Matrix Jordan without any agreement whatsoever in this regard. It is important to note that the assessee and Matrix Jordan are separate legal entities located in different countries. For the impugned huge loan to Matrix Jordan, the assessee didn’t enter into an agreement with Matrix Jordan. inter alia, in respect of loan repayment schedule, loan recovery plans in case of default in the repayment schedule, charging of interest and its recovery, legal rights & legal obligations/responsibilities of Matrix Jordan and the assessee, etc. in this regard, thereby seriously jeopardizing the recovery of the loan given to Matrix Jordan. This is completely contrary to any business prudence and commercial rationale. |

| (ii) |

|

The assessee has given such a huge amount of loan to Matrix Jordan only on the basis of its so-called Board’s resolutions which are nothing but self-created and self-serving documents. The assessee has submitted these so-called Board’s resolutions at pages 1-11 of the paper book filed on 17.11.2025. As it could be seen from these documents, there is no mention, whatsoever, of anything about repayment and recovery of the loan what to talk of any repayment and recovery plans. Also, these documents don’t contain anything about charging of interest on the loan what to talk of its recovery. These conducts of the assessee seriously jeopardize the recovery of the loan given to Matrix Jordan. These are completely contrary to any business prudence and commercial rationale. |

| (iii) |

|

As per date-wise details of the loan given and its part repayment, as submitted by the assessee at page 158 of the paper book filed on 30.10.2025, the total amount of loan of Rs.83,03,95,425/- was given to Matrix Jordan by the assessee on various dates during FY 2016-17 to FY 2020-21. Further, as per details of ‘loan received back’, an amount of Rs.3,45,85,650/- was received back for the first time only on 27.01.2020. Thereafter, the second repayment of Rs.7,74,71,856/- was made only on 23.02.2021. Subsequently, quite small amounts have been shown as received on various dates from 10.06.2021 to 11.01.2022. It may kindly be noted that the total amount of only Rs. 14,56,37,836/- is shown as received back, that too during the period from 27.01.2020 to 11.06.2022. |

| (iv) |

|

As I had argued during the hearing before the Hon’ble ITAT, when the subsidiary’s business in Jordan was doing quite well before the COVID (as the assessee claimed multiple times during the hearing before the Hon’ble ITAT), why there was no repayment of the loan before the COVID except for a small amount of Rs.3,45,85,650/- which was received back for the first time only on 27.01.2020? In fact, as it could be seen from the details filed by the assessee, almost the entire repayment of Rs. 14,56,37,836/- was made during the COVID. In fact, the dates and amounts of repayment suggest that the assessee was apparently trying to create some faqade of repayment in this regard in FY 2020-21 with the intention to justify its scheme under which the loan has been written-off during the impugned FY 2020-21. |

| (v) |

|

It is surprising and contrary to any business prudence to note that during the impugned FY 2020-21, the assessee has written off the loan of Rs.53,24,17,100/-given to Matrix Jordan, while during the impugned FY itself the assessee has also given a huge amount offresh loan of Rs. 33.98 crore to Matrix Jordan, despite their extremely precarious financial condition. |

| (vi) |

|

As per page 198 of the paper book filed by the assessee on 30.10.2025 which is statement of financial position of IJC Jordan as on 31 March 2019 and 31″ March 2020, IJC Jordan had huge accumulated losses of 34,36,697 Jordanian Dinar and 38,43,388 Jordanian Dinar as on 31st March 2019 and 31 March 2020 respectively (i.e. before the COVID). It may kindly be noted that 1 Jordanian Dinar was more than INR 100 during that time. These documents do not suggest at all that IJC Jordan was doing well before the COVID. In fact, these documents suggest that IJC Jordan was making persistent losses, and despite that, the assessee kept on giving huge amount of loans to Matrix Jordan (the assessee’s SPV that had acquired IJC Jordan) for IJC Jordan without any recovery plans and recovery prospect, whatsoever, thereby seriously jeopardizing the recovery of the loan given to Matrix Jordan. This is completely contrary to any business prudence and commercial rationale. |

| (vii) |

|

The assessee’s claim that the Jordan-based subsidiary’s business was doing quite well before the COVID, is also contrary to the assessee’s own submission dated 26.12.2023 made before AO during the assessment proceedings. I am reproducing the relevant part from para 2.14 on page 12 of AO’s order (page 21 of the initial paper book filed with the appeal memo) as below: |

“It is submitted that due to persistent losses for the years, which in the judgement of the management of assessee became irrecoverable. Copies of audited financial statements of Jordan LLC are annexed as annexure 7.7” (Emphasis supplied)

This shows that the assessee kept on giving huge amounts of loans to its Jordan-based subsidiary despite their extremely precarious financial situation, showing no regard for any business prudence or commercial rationale. Now, before the Hon’ble ITAT, the assessee is trying to take undue advantage of the COVID by presenting self-serving claims which are contrary to the facts on record.

1.5 As regards the assessee’s contention at para 1.3(ii), a perusal of the document at pages 357-360 of the paper book filed by the assessee on 30.10.2025 clearly shows that it is only a compounding order (dated 31.10.2023) of RBI for the offence committed by the assessee under FEMA, by writing off the loan without prior approval of RBI in this regard. It cannot be said to be RBI’s approval for write off of the loan by any stretch of imagination. Let’s consider an example – suppose an offence was committed under the Indian Penal Code (IPC) that was compoundable, and the court eventually compounds the offence committed by a person. Is it appropriate to infer from the compounding that the act of the person amounting to the offence itself was approved by the court? The answer is definitely not. Therefore, in the assessee’s case, there is no RBI approval, whatsoever, for write-off of the said loan. In the context of the assessee’s contention at para 1.3(ii) above that the disallowance was made by AO solely for want of RBI’s approval, it could be seen that as per AO’s discussion on page 19 of his order (page 28 of the initial paper book filed with the appeal memo), the AO appears to have taken cognizance of the RBI’s compounding order dated 31.10.2023 which the assessee is claiming as RBI’s approval for write-off of the loan.

1.6 As regards the assessee’s contention at para 1.3(ii) that the sole reason for disallowance of write-off of the loan was lack of RBI’s approval, this is factually incorrect submission on the part of the assessee as I had also submitted during the hearing before the Hon’ble ITAT. The AO has discussed this issue quite elaborately at para 2.14 on pages 12 to 19 of his order (pages 21-28 of the initial paper book filed with the appeal memo) wherein the AO has analyzed this issue from multiple relevant perspectives. At the starting para on page 13 of his order (page 22 of the initial paper book), the AO has mentioned that despite the said entity (Jordan-based subsidiary) continuously making losses, the assessee advanced another loan of Rs. 33.98 crore during the impugned FY also which is not in accordance with common business rationale and prudence that even if the entity is persistently making losses still such a huge loan is given without any Revival Plan. In fact, as per the assessee’s own submissions before AO, the Jordan-based subsidiary had persistent losses, and despite that the assessee kept on advancing loans to Matrix Jordan for IJC Jordan during all these years from FY 2016-17 to FY 2020-21, even without any basic safeguards in the form of any loan agreement, loan repayment plan, loan recovery plan, revival plan for IJC Jordan, terms and conditions regarding the loan and interest, thereby seriously jeopardizing the recovery of the loan given to Matrix Jordan. This is completely contrary to any business prudence and commercial rationale. The AO on second last para on page 13 of his order (page 22 of the initial paper book filed with the appeal memo) has concluded “This clearly shows that the whole arrangement is nothing but a sham arrangement made by the assessee to reduce its tax liability.”

1.7 As per page 33 of the paper book filed on 30.10.2025, the assessee had profit of Rs. 56.96 crore from ordinary business before the claim of write-off of the above loan of Rs.53.24 crore during the impugned FY. As per AO’s discussion on page 14 of his order (page 23 of the initial paper book filed with the appeal memo), the assessee has shown profit of Rs. 14.22 crore and Rs. 17.89 crore during earlier FYs 2018-19 and 2019-20 respectively (as against a huge profit of more than Rs. 56 crore in the impugned FY 2020-21). The AO has discussed this aspect on pages 14-15 of his order (pages 23-24 of the initial paper book filed with the appeal memo) wherein he has also reproduced the relevant part of the assessee’s financials to highlight that the assessee has shown profit before tax (and before the claim of write-off of loan as exceptional item) of Rs. 56.08 crore. After the claim of the loan write-off as exceptional item, the assessee has been able to substantially reduce its taxable profit in India to only Rs. 2.84 crore for the impugned FY as against more than Rs. 56 crore before this claim. The entire factual matrix of the case clearly shows that the whole scheme of arrangement was made by the assessee to reduce its tax liability in India.

1.8 The AO has discussed the issue of applicability of the provisions of sections 36, 36(1)(vii), 36(2) and 37(1) of the Act in this regard quite elaborately on pages 15-19 of his order (pages 24-28 of the initial paper book filed with the appeal memo) and he has clearly held that none of the conditions of these sections are fulfilled in the assessee’s case and therefore, the said write-off of the loan cannot be allowed under any of these sections of the Act. I would just like to add that allowance u/s 36(1)(vii) is subject to the provisions of section 36(2) of the Act, and the provisions of section 36(2) requires that such debt must have been taken into account in computing the income of the assessee or represents money lent in the ordinary course of the business of banking or money-lending which is carried on by the assessee. The said debt, being a capital loan, is never taken into account in computing the assessee’s income. Further, the assessee is not in the business of banking or money-lending. Therefore, none of the conditions of section 36(1)(vii) read with section 36(2) of the Act are fulfilled in the assessee’s case. In the context of section 37(1) of the Act, I would just like to add that one of the conditions of section 37(1) is that the expenditure proposed to be claimed u/s 37(1) should not be in the nature of capital expenditure. In the assessee’s case the loan to Matrix Jordan is a capital loan and as per page 25 of the paper book filed on 30.10.2025 (which is financial statement of the assessee), the assessee has shown it under “Long-Term Loans and Advances” (Item 14) which is clearly a capital expenditure for the assessee. Also, the assessee has written it off in violation of law (FEMA in this case) which is a fact admitted by the assessee. Therefore, the conditions of section 37(1) of the Act are not fulfilled in the assessee’s case.

1.9 It is pertinent to highlight that on page 19 of AO’s order (page 28 of the initial paper book filed with the appeal memo), it is mentioned that the Hon’ble ITAT vide order dated 23.03.2018 in the assessee’s own case has upheld the order of AO on this issue. During the hearing before the Hon’ble ITAT, the undersigned handed over copies of this order of the Hon’ble ITAT (in ITA No. 6554/Del/2016) to the Hon’ble Members as well as to the assessee. The discussion made by the Hon’ble ITAT at para 4 onwards of this order is relevant for this issue. The Hon’ble ITAT in the assessee’s own case reversed the findings of Ld. CIT(A) and restored the order of AO on this issue. This case law also highlights that the assessee is in the habit of resorting to such schemes of write-off of loans given to its related parties. In view of the above, the above matter is a covered matter in favour of the Revenue by the Hon’ble ITAT’s order in the assessee’s own case. In view of the above, it is requested that the assessee’s aforesaid ground may be dismissed by the Hon’ble ITAT.

13. Heard the contentions of both the parties at length and perused the material available on record. The assessee has given loan to its wholly owned subsidiary company Matrix Jordan who in turn acquire one company Jordan LLC which was engaged in the same line of business of manufacturing and trading of menswear and sportswear. The assessee claimed that it had given loans on various dates spread over past few years to its wholly owned subsidiary company at Jordan and the said sum was invested by its subsidiary company in acquisition of Jordan LLC. Assessee further claimed that due to persistent losses suffered by Jordan LLC due to Covid-19 pandemic, the capital invested in Jordan LLC was eroded and ultimately investment was disposed at a huge loss leading to the situation where the Matrix Jordan has not been able to repay the loans taken from the assessee. Therefore, the major part of such loans including interest as on date was claimed as written off during the year under appeal which was disallowed by the AO and such disallowance was confirmed by ld. DRP.

14. The loans given to Matrix Jordan on various dates by the assessee after getting approval of the Board in terms of Board resolutions passed is tabulated as under:-

| Sl.No. |

Particulars |

Amount (In INR) |

|

FY 2020-21 |

|

| 1. |

Board Resolution dated 27.01.2021 |

5,83,92,000 |

| 2. |

Board Resolution dated 18.01.2021 |

12,44,88,000 |

| 3. |

Board Resolution dated 11.01.2021 |

8,05,75,000 |

| 4. |

Board Resolution dated 25.12.2020 |

3,15,19,000 |

| 5. |

Board Resolution dated 22.10.2020 |

2,58,23,000 |

| 6. |

Board Resolution dated 15.06.2020 |

1,90,02,500 |

|

TOTAL |

33,97,99,500 |

|

FY 2019-20 |

|

| 7. |

Board Resolution dated 04.11.2019 |

7,12,70,000 |

| 8. |

Board Resolution dated 08.07.2019 |

1,23,58,800 |

| 9. |

Board Resolution dated 17.05.2019 |

5,20,12,500 |

|

TOTAL |

13,56,41,300 |

|

FY 2017-18 |

|

| 10. |

Board Resolution dated 12.03.2018 |

13,02,70,000 |

| 11. |

Board Resolution dated 10.01.2018 |

2,06,84,625 |

| 12. |

Board Resolution dated 18.12.2017 |

2,40,30,000 |

| 13. |

Board Resolution dated 28.09.2017 |

3,26,80,000 |

|

TOTAL |

20,76,64,625 |

|

FY 2016-17 |

|

| 14. |

Board Resolution dated 26.07.2016 |

14,72,90,000 |

15. From the perusal of the above table, it is observed that from FY 2016-17 to FY 2020-21, assessee has given loans on various dates to Matrix Jordan totaling to INR 83,03,95,425/-. The assessee further claimed that the following amounts have been offered for tax as interest income in preceding assessment years:-

| FY |

Amount (In INR) |

| 2016-17 |

32,60,344 |

| 2017-18 |

78,08,864 |

| 2018-19 |

1,68,59,739 |

| 2019-20 |

2,00,69,296 |

16. The assessee further claimed that out of the total loans given upto FY relevant to AY i.e. 31.03.2021, it had received total 12,31,77,177/- as repayment of loans. Further on 14.02.2021 when the share purchase agreement was entered into with the buyer United Creations Apparel Manufacturing LLC with respect to transfer of shares of Indo Jordan Clothing LLC, the total outstanding balance of loan to Matrix Jordan was INR 74,62,11,259/- inclusive of interest upto that date of INR 3,59,98,457/-. It is relevant to state that though the assessee has calculated the amount of interest on outstanding loan of INR 3.59 crores in the gross amount of amount written off claimed during the year. However, from the perusal of the financial statements, it is observed that no such income was included in the financial statements prepared. Thus, on one hand assessee has included the interest in the total outstanding loan as on 14.02.2021 claimed as written off but the same was never offered for tax. Therefore, the interest to the extent of 3,59,98,457/- cannot be allowed as written off.

17. The assessee in terms of the share purchase agreement entered into with United Creations Apparel Manufacturing LLC, placed at pages 240-286 of Paper Book, stated that its wholly owned subsidiary Matrix Jordan has sold its investment in Jordan LLC of total 56,500 shares for a total consideration of 35,95,025 USD. However, from the perusal of financial statements of Matrix Jordan as well as of the assessee company, it is not clear whether the said sale consideration was received by assessee nor any entry in this regard is found recorded. During the course of hearing, bench has specific raised query to ld. AR in this regard but no logical submission to our satisfaction was tendered. Further not a single penny of corresponding Indian Rupee of the said sale consideration was received by the assessee which is clear from the detailed computation of written off claimed as reproduced above, where this sum was never claimed as received by the assessee nor the end use of this sum is ever explained. Assessee further claimed that it has given guarantee to the financial institutions against the working capital and other short terms finance taken by Matrix Jordan and to repay such obligations, fresh loans were advanced however, consideration received from the sale of shares of Jordan LLC was never claimed as utilized for making the payment of such outstanding liabilities by Matrix Jordan. Rather the outstanding loan of INR 71,02,12,802/-claimed was the total amount of loan outstanding as on 14.02.2021, which represents loans given by assessee on various dates to Matrix Jordan totaling to INR 83,03,95,425/- as increased by the amount of interest of INR 4,79,98,243/- and reduced by the amount of repayment received from Matrix Jordan against loan amount. It is further observed that working of written off of amount of INR 53,24,17,100/- as submitted before us in the written submissions filed by the assessee and reproduced herein above, the assessee has reduced the amount of residual value of inventory with Indo Jordan Clothing LLC at INR 4,79,51,304/-.

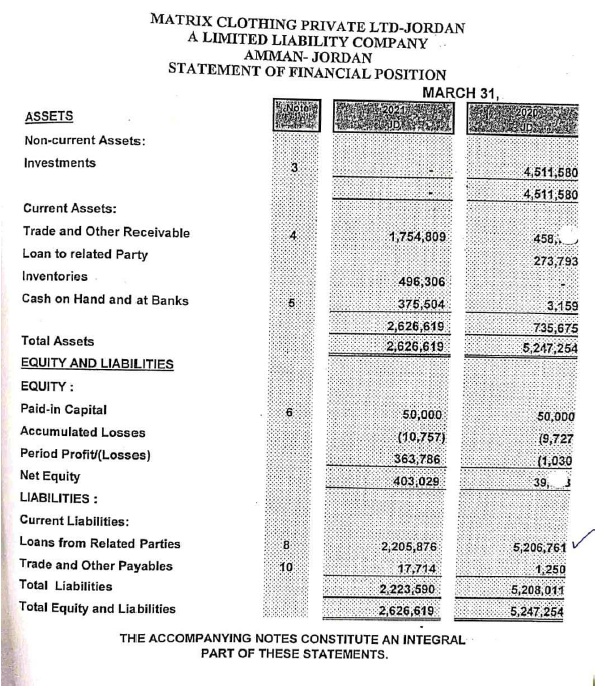

18. Further, the assessee has reduced the outstanding receivable of M/s. Nygard International, USA of INR 16,58,52,855/- which as per the assessee is the outstanding receivables of Matrix Jordan. From the perusal of the Balance Sheet of Matrix Jordan, placed at page 237 of Paper Book, it is observed that in the Liability side under the head “loans from related parties” i.e. assessee company, as on 31.03.2020 amount of 52,06,761/- Jordan Dinar and as on 31.03.2021 amount of 22,05,876/- Jordan Dinar was shown. Thus, according to these amounts declared in the Balance Sheet by the Matrix Jordan, it appears that a reduction in amount of the loan by 30,00,885/- Jordan Dinar is claimed by the subsidiary company as against which assessee claimed only INR 7,74,71,856/- received as repayment against loan on 23.02.2021. Assessee has not been able to explain the treatment given in its books of accounts of the sum received as repayment of loan and consideration from the sale of investment in Jordan LLC during the year under appeal which leads to the conclusion that the balance outstanding loan as on 14.02.2021 is not correct and accordingly the amount claimed written off during the year is not verifiable. The relevant balance sheet of Matrix Jordan at page 237 is reproduced as under:-

19. From the above discussion, it is clear that the assessee has deliberately increased the amount of claim of written off by the interest component added of INR 3,59,98,457/- which was not offered for tax and further a sum of INR 7,74,71,856/- received on 23.02.2021 had also not been reduced from the amount claimed as written off. Besides this, consideration received from the transfer of shares of Indo Jordan Clothing LLC of 35,95,025/- USD (corresponding INR 23,36 crores approx. by taking the conversion rate of INR 65/- per USD) was never claimed to have been received by the assessee. All these facts raised serious doubts about the claim of the assessee and it appears that the assessee never come with clean hands while making claim of written off of bad debts out of the total loans given including outstanding interest.

20. Now coming to the allowability of claim of written off of loan u/s 36(1)(vii)/36(2) of the Act, the relevant provision of section 36(1)(vii) and 36(2) of the Act are reproduced as under:-

36(1)(vii) “subject to the provisions of sub-section (2), the amount of any bad debt or part thereof which is written off as irrecoverable in the accounts of the assessee for the previous year: Provided that in the case of an assessee to which clause (viia) applies, the amount of the deduction relating to any such debt or part thereof shall be limited to the amount by which such debt or part thereof exceeds the credit balance in the provision for bad and doubtful debts account made under that clause: Provided further that where the amount of such debt or part thereof has been taken into account in computing the income of the assessee of the previous year in which the amount of such debt or part thereof becomes irrecoverable or of an earlier previous year on the basis of income computation and disclosure standards notified under sub-section (2) of section 145 without recording the same in the accounts, then, such debt or part thereof shall be allowed in the previous year in which such debt or part thereof becomes irrecoverable and it shall be deemed that such debt or part thereof has been written off as irrecoverable in the accounts for the purposes of this clause. Explanation 1.—For the purposes of this clause, any bad debt or part thereof written off as irrecoverable in the accounts of the assessee shall not include any provision for bad and doubtful debts made in the accounts of the assessee. Explanation 2.—For the removal of doubts, it is hereby clarified that for the purposes of the proviso to clause (vii) of this sub-section and clause (v) of sub-section (2), the account referred to therein shall be only one account in respect of provision for bad and doubtful debts under clause (viia) and such account shall relate to all types of advances, including advances made by rural branches;

———–

36(2). “In making any deduction for a bad debt or part thereof, the following provisions shall apply— (i) no such deduction shall be allowed unless such debt or part thereof has been taken into account in computing the income of the assessee of the previous year in which the amount of such debt or part thereof is written off or of an earlier previous year, or represents money lent in the ordinary course of the business of banking or money-lending which is carried on by the assessee; (ii) if the amount ultimately recovered on any such debt or part of debt is less than the difference between the debt or part and the amount so deducted, the deficiency shall be deductible in the previous year in which the ultimate recovery is made; (iii) any such debt or part of debt may be deducted if it has already been written off as irrecoverable in the accounts of an earlier previous year (being a previous year relevant to the assessment year commencing on the 1st day of April, 1988, or any earlier assessment year), but the Assessing Officer had not allowed it to be deducted on the ground that it had not been established to have become a bad debt in that year; (iv) where any such debt or part of debt is written off as irrecoverable in the accounts of the previous year (being a previous year relevant to the assessment year commencing on the 1st day of April, 1988, or any earlier assessment year) and the Assessing Officer is satisfied that such debt or part became a bad debt in any earlier previous year not falling beyond a period of four previous years immediately preceding the previous year in which such debt or part is written off, the provisions of sub-section (6) of section 155 shall apply; (v) where such debt or part of debt relates to advances made by an assessee to which clause (viia) of sub-section (1) applies, no such deduction shall be allowed unless the assessee has debited the amount of such debt or part of debt in that previous year to the provision for bad and doubtful debts account made under that clause.”

21. From the above, it is clear that to claim bad debt, Two conditions have to be fulfilled (i) amount claimed as bad debt has to suffer tax and (ii) necessary entry of write-off should be passed in the books of accounts of the assessee. This proposition is confirmed by Hon’ble Supreme Court in the case of TRF Ltd. (supra). Now coming to the facts of the present case, assessee has to establish that the amount claimed as written off is offered for tax in any of the preceding years. As observed above, out of the total loans claimed as written off, a sum of INR 4,79,98,243/- was offered for tax as interest from FYs 2016-17 to 2019-20 and therefore, this amount could be claimed as written off u/s 36(2)/36(1)(vii) of the Act. For the remaining amount claimed, we are of the view that the assessee has not acted as a prudent businessman where, as stated above, the assessee despite of knowing the fact that Indo Jordan Clothing LLC was suffering huge losses and had transferred around INR 34 crores during the year under appeal which includes around INR 30.00 crores given in the month of January & February 2021 when the process of sale of shares of Indo Jordan Clothing LLC by Matrix Jordan was in progress. This clearly established that assessee has made bet on the horse was going to lose the race. Under these circumstances, no prudent businessmen would burn its money on such dying enterprises. Even under commercial expediency, this cannot be held as the decision taken in the benefit of and for the furtherance of the business carried out by any prudent businessman.

22. In the case of the assessee itself in AY 2012-13, similar of loan given to sister concern was claimed as written off which was held as taxable by the coordinate bench of Delhi Tribunal in ACIT v. Matrix Clothing (P.) Ltd. [IT Appeal No. 6554 (Delhi) of 2016] vide order dated 23.03.2018. The relevant observations of the Co-ordinate Bench as contained in para 4.6 to 4.10 allowing the appeal of the Revenue are as under:-

4.6. “We have perused the submissions advanced by both the sides in the light of the records placed before us.

4.7. The issue before us is that assessee who is engaged in the business of manufacturing of garments advanced loans to certain concerns and the same have become non-recoverable which were written off and claimed before Ld. AO as bad debts. Assessing Officer disallowed it as it did not satisfy the conditions of section 36 (2) of the Act. Before Ld. CIT (A) assessee took the plea that it would be business loss which has been accepted by Ld. CIT (A). It is now the case of assessee that such losses are allowable as bad debts. Ld. DR has argued that even the loss is not allowable. According to us any loss is allowable to assessee under section 28 itself while computing business income of assessee if: ■ such loss has been arisen during the course of the business of assessee; and it should have occurred during the year under concern.

4.8. In the present case the write off of loss has not arisen during the course of business of assessee as money lending is not the activity that is carried on by assessee and it has never been the claim of assessee nor it has been proved before the authorities below. There has been no evidence that is placed on record to prove that the loss has occurred during the year. Therefore the claim of loss by assessee does not hold good on both these counts. The reasons given by Ld. CIT (A) to allow the claim as business loss are irrelevant and is without considering the provisions of the Act. Ld. CIT (A) also accepted that the issue stands covered in the favour of assessee by the decision of Page 11 of 12 Hon’ble Gujarat High Court in the case of Manohar N Shah reported in 280 ITR 462. We have perused the said decision of the Hon’ble Gujarat High Court, and it is observed that the loss was proved to have been arisen during the year which was actually a business loss.

4.9. Therefore, we are inclined to reverse the findings of Ld. CIT (A) and restore the order of Ld. AO.

4.10. Accordingly this ground raised by revenue stands allowed.”

23. The assessee placed reliance on various judgements where it is held that written off of advances given as business loans and allowable as deduction u/s 37(1) of the Act. However, as observed above, in the instant case, it is found that assessee has not only claimed of higher amount of loss by not reducing the amount of sale consideration received from the transfer of shares coupled with the facts that interest amount has been deliberately added to the outstanding loan to inflate the amount of claim of bad debt and further not reduced the amount of repayment received subsequently. Therefore, these judgements are of no help to the assessee who had deliberately made incorrect claim of write off of loan.

24. One more fact which needs to be considered at this stage is that during the year under appeal, the net profit declared by the assessee in the year under appeal and of preceding two Assessment Years is as under:-

| Year ended |

Profit before tax. (in Cr.) |

Exceptional item (in Cr) |

Profit before tax (in Cr) |

Total Revenue (in Cr) |

Expenses (in Cr) |

| 31.03.2019 |

14.22 |

0 |

14.22 |

386 |

371 |

| 31.03.2020 |

17.89 |

0 |

17.89 |

394 |

376 |

| 31.03.2021 |

56.08 |

53.24 |

2.84 |

337 |

281 |

25. From the perusal of the above, it is clear that during the year under appeal, net profit of the assessee had increased sharply as compared to preceding years despite of the fact that the business in this year was adversely hit by Covid-19 pandemic and claim of bad debts of INR 53.24 crores might be made to reduce tax liability arisen on net profits earned during the year since the circumstances as discussed herein above, are not warranted that such loan should be claimed as bad debt in the year under appeal, more particularly, when assessee has infused fresh funds of more than INR 33 crores in the year itself and claimed that such funds were sent to revive Jordan LLC. In this case, from facts as stated above, it emerges undeniably and concrete evidence suggests that whole exercise was scripted and executed, was nothing but a colourable device, for the purpose of lending legitimacy to the act to reduce the income, and for evading taxes. Further, the facts discussed above in detail should also be tested against the touchstone of human probability. Time and again, in cases of financial and economic fraud, assessee has raised questions about the legitimacy of evidence rooted in circumstances, and the test of human probability. Though, in this case, given the detailed facts and circumstances of the case outlined above, there is little room for the assessee to do so. The Hon’ble Supreme Court in the case of CIT v. Durga Prasad More [1971] 82 ITR 540 (SC) held that human probability and circumstantial evidence must be kept in mind to decide the genuineness of the transactions. The Hon’ble court observed as under:

“Science has not yet invented any instrument to test the reliability of the evidence placed before a Court or Tribunal, Therefore the Courts and Tribunals have to judge the evidence before them by applying the test of human probabilities. Human minds may differ as to the reliability of a piece of evidence. But in that sphere the decision of the final fact finding authority is made conclusive by law.”

26. The coordinate bench of ITAT, Delhi in the case of Hersh W. Chadha v. Dy. DIT, International Taxation (Delhi)/I.T.A. Nos. 3088 to 3098 & 3107/Del/2005, held as under:

“The admissibility of documents, evidence or material differs greatly in income tax proceedings and criminal proceedings respectively. In criminal proceedings, the charge is to be proved by the State against the accused, establishing it beyond doubt, whereas as per the settled proposition of law, the income tax liability in the cases of suspicious transactions is ascertained on the basis of the material available on record, the surrounding circumstances, human conduct and preponderance of probabilities.”

27. The Hon’ble Supreme Court in the case of Sumati Dayal v. CIT(SC) has held as under:

“As laid down by this Court, apparent must be considered real until it is shown that there are reasons to believe that the apparent is not the real and that the taxing authorities are entitled to look into the surrounding circumstances to find out the reality and the matter has to be considered by applying the test of human probabilities.”

28. In the instant case, the ‘apparent’ is not ‘real’ and the ‘apparent’ wears the mask of legitimacy, while the ‘real’ is a sham and a farce. According to Oxford English Dictionary, a ‘sham’ means “a thing that is not what it is purported to be”. What is ‘purported to be’ in this case is an attempt to claim written off of legitimate outstanding loan granted during the year itself and what is ‘real’ is actually a sinister design to cheat the revenue authorities and other arms of the Government, by making bogus claim, and thus, willfully evade taxes through deliberate planning and strategy. The hon’ble Supreme court in the case of Mc Dowell & Co. Ltd. v. Commercial tax Officer (SC) has held as under

“Colourable devices cannot be part of tax planning and it is wrong to encourage or entertain the belief that it is honorable to avoid the payment of tax by resorting to dubious methods. It is the obligation of every citizen to pay the taxes honestly without resorting to subterfuges.”

29. In the light of the above discussion and the facts of the case, we uphold the disallowance of INR 53,24,17,100/- made and uphold by the lower authorities of written off of loan by the assessee. Here it is relevant to stated that though the assessee is having RBI approval in the form of compounding of offence of not filing petition for approval of writing off of loan, does not mean that such deemed approval grant the immunity for claiming incorrect claim under Income tax Act which is a separate code and every claim made under the Income Tax Act has to be examined as per the provision of Income Tax Act independently.

30. Accordingly, we find no error in the orders of the lower authorities in not allowing the claim of written off of loans given. The Ground of appeal No. 3 raised by the assessee with respect to the transfer pricing adjustments is hereby, dismissed.

31. The next Ground of appeal No.4 raised by the assessee is with respect to the disallowance of deduction of INR 6,59,31,499/- u/s 35(2AB) of the Act.

32. Before us, Ld.AR for the assessee submits that the assessee has not claimed weighted deduction u/s 35(2AB) of the Act which is very much clear from the perusal of the computation of income placed at page 1 of PB. It is further submitted that the assessee had claimed normal deduction for the expenses incurred on scientific research and development u/s 37(1) of the Act which are wholly and exclusively incurred for the purpose of business therefore, the same should be allowed as claimed. In the alternate, the assessee submits that Auditor has certified expenses by filing its report in Form 3CLA placed page 366 to 372 of PB and further, in-house research facility approved by the Department of Scientific and Industrial Research (“DSIR”) and Form 3CM was issued by DSIR according to which the R&D facility was approved upto 31.03.2022, placed at page 408 of PB. Ld.AR submits that in terms of Form 3CM, assessee was granted approval from DSIR for in-house research and development facility and expenses claimed includes the salary and wages paid to employees engaged in the research and development activity. The necessary copy of Form 16 issued to those employees were also placed in the Paper Book. It was the submission that total claim of expenditure @ 100% of INR 6.59 crores deserves to be allowed. Ld.AR further drew our attention to the judgment of the Co-ordinate Bench in assessee’s own case itself in Matrix Clothing (P.) Ltd. v. ACIT (Delhi – Trib.)/ITA No.760/Del/2022 [AY 2017-18] wherein the Co-ordinate Bench vide its order dated 01.12.2025 has allowed deduction u/s 35(2AB) of the Act to the assessee. However, it is submitted that since the assessee has not claimed the weighted deduction u/s 35(2AB) of the Act therefore, the said amount be allowed as normal deduction u/s 37(1) of the Act as business expenditure.

33. On the other hand, Ld.CIT DR for the Revenue vehemently supports the orders of lower authorities and made following submissions:-

2. Ground No. 2: Disallowance of Rs.6,59,31,449/- claimed as R&D expenses u/s 35(2AB) of the Act.

2.1 At the outset, the assessee claimed that this matter is covered in its favour by the Hon’ble ITAT’s order for AY 2017-18 in the assessee’s own case. However, as pointed out by the undersigned during the hearing before the Hon’ble ITAT, the facts of the impugned AY are materially and substantially different from the facts of AY 2017-18 on this issue. Also, the undersigned strongly rely on the orders of the lower authorities (AO and DRP) in support of his arguments.

2.2 The Hon’ble ITAT vide its order for AY 2017-18 on this issue has observed that once a certificate has been issued DSIR duly certifying the figures eligible for deduction u/s 35(2AB), the AO again cannot go beyond the said certificate. The Hon’ble ITAT has further observed that in the event of AO not agreeing with the certificate of DSIR, then the AO should follow the procedure provided in section 35(3) of the Act which in the instant case was not followed by AO. However, on perusal of the facts of the impugned AY 2021-22 as discussed by the AO at paras 3.1 to 3.15 on pages 22-33 of his order (pages 31-42 of the initial paper book filed with the appeal memo) make it clear that despite AO’s request to provide relevant documents including Form 3CL and Form 3CM, the assessee failed to provide such documents to AO during the assessment proceedings. Considering the assessee’s failure to provide these documents during the assessment proceedings, the AO had to resort to inquiry under section 133(6) of the Act to obtain relevant documents from DSIR directly. This aspect has been specifically discussed by AO at paras 3.6 and 3.7 on page 25-26 of his order (pages 34-35 of the initial paper book filed with the appeal memo) wherein the AO has clearly held that from the reply of DSIR, it was clear that Form 3CM in the case of the assessee was valid till 31.03.2020 only. Further, as per para 3.7 of the AO’s order (page 35 of the initial paper book filed with the appeal memo), the assessee failed to produce copy of Form 3CL that forms the basis of expenditure incurred on R&D activities and certified by DSIR. The discussion made by the AO at para 3.12 on page 30-31 of his order (pages 39-40 of the initial paper book filed with the appeal memo) are quite critical for the issue during the impugned AY.

2.3 During the hearing before the Hon’ble ITAT, the assessee referred to page 408 of the paper book filed on 30.10.2025, which is apparently a Form 3CM, to claim that its R&D facilities were approved by DSIR till 31.03.2022 and the impugned AY 2021-22 is covered under that period. However, a careful perusal of aforesaid page 408 which is apparently DSIR order dated 13.09.2021 (Form 3CM), reveals that the assessee’s R&D facilities were approved for the purpose of section 35(2AB) only till 31.03.2020 which is clearly mentioned in the order itself. The concluding sentence of the said order of DSIR (Form 3CM) is reproduced below:

“The above Research & Development facilities is approved for the purpose of section 35(2AB) from 01.04.2019 to 31.03.2020 subject to the conditions underlined therein.” (Emphasis supplied)

This fact of DSIR’s approval only till 31.03.2020 was also established by the AG’s enquiry u/s 133(6) of the Act as discussed above. It is, therefore, clearly established that there was no DSIR’s certificate/approval (including Form 3CM and Form 3CL) in respect of the assessee for the impugned AY 2021-22 (FY 2020-21).

2.4 In view of the materially different facts for AY 2017-18 and the impugned AY 2021-22 as discussed above, it is clear that the assessee’s case for the impugned AV 2021-22 is not covered by the Hon’ble ITAT’s order for AY 2017-18 on this issue. In view of the above, it is requested that the assessee’s aforesaid ground may be dismissed by the Hon’ble ITAT.

2.5 In the ground of appeal on this issue, the assessee has taken a plea that it is not eligible for weighted deduction u/s 35(2AB), however, the expenditure towards scientific research is allowable u/s 37(1) of the Act. As per this plea of the assessee, it has admitted that it is not eligible for deduction u/s 35(2AB) of the Act. Therefore, the assessee’s reliance on the Hon’ble ITAT’s order for AY 2017-18 in its own case, as mentioned above, is completely misplaced on this ground as well. Coming to the assessee’s claim that the expense was also allowable u/s 37(1) of the Act, it is submitted that the assessee never claimed this expenditure u/s 37(1) of the Act in its Income Tax Return (ITR) filed for the impugned AY 2021-22. On page 29 of AO’s order (page 38 of the initial paper book filed with the appeal memo), relevant part of the assessee’s ITR’s screenshot is duly placed which clearly shows that the expense has been claimed u/s 35(2AB), and not u/s 37(1) in the ITR. Further, the AO at para 3.8 on page 27 of his order (page 36 of the initial paper book filed with the appeal memo) has mentioned about survey proceedings u/s 133A(1) of the Act conducted on 27.03.2019 in the assessee’s case and subsequent investigations which led to the findings about bogus claim of R&D expenses by the assessee. Also, the AO at paras 3.12 to 3.13 on pages 30-31 of his order (pages 39-40 of the initial paper book filed with the appeal memo) has discussed about the claim of bogus R&D deduction. In view of these facts and without prejudice to the above, the said expense cannot be allowed to the assessee u/s 37(1) of the Act also. Therefore, it is requested that the assessee’s aforesaid ground may be dismissed by the Hon’ble ITAT.”

34. Heard the contentions of both the parties at length and perused the material available on record. In the instant case, assessee though in the return of income filed, had claimed expenditure of INR 6,59,31,449/- u/s 35(2AB) of the Act. However, weighted deduction was not claimed in accordance with the provisions of section 35(2AB) and only 100% deduction is claimed. The assessee also filed copy of the Audit Report and Form 3CM issued by the prescribed authority i.e. approval by DSIR however, for claiming weighted deduction u/s 35(2AB) of the Act, further approval from the PCCIT or PDGIT is mandatory, as provided u/s 35(2AB)(iv) of the Act. Since such mandatory approval of R&D facility from the PCCIT or PDGIT was not obtained by the assessee therefore, weighted deduction u/s 35(2AB) of the Act cannot be allowed.

35. However, admittedly assessee has incurred expenses which were incurred on scientific research and development and are related to day to day business activity of the assessee and thus otherwise, is allowable as business expenses u/s 37(1) of the Act. Accordingly, we direct the AO to allow the deduction of expenses claimed of INR 6,59,31,449/- as business expenditure u/s 37(1) of the Act. Ground of appeal No. 4 raised by the assessee is thus, partly allowed.

36. Ground of appeal No.5 raised by the assessee is with respect to the disallowance of deduction u/s 80IA of INR 21,84,942/- and of INR 42,16,800/-claimed on the income from Wind Mill Plants installed.

37. Before us, Ld.AR for the assessee submits that assessee has installed Two Wind Mill Plants in Gujarat and the electricity produced was sold to Electricity Boards. The assessee had claimed the deduction u/s 80-IA of the Act on the income so earned from such activity. The AO alleged that expenses claimed in the Profit & Loss Account were not attributed to this activity and therefore, he apportioned 0.15% of the total expenditure being attributable to such activity which comes to INR 42,16,800/- and reduced the deduction claimed u/s 80IA to this extent. The AO further observed that by reducing the amount of 42,16,800/- from the amount of deduction claimed u/s 80IA of the Act, the total amount of deduction claimed u/s 80IA of the Act of INR 21,84,942/- reduced to NIL.

38. Ld. AR submits that assessee consistently claimed deduction u/s 80-IA of the Act on the Wind Mill Plants since its installation in the Assessment Year 2012-13 and was allowed consistently without raising any doubts in the assessment orders passed u/s 143(3) of the Act for the income generated from Wind Mill Plants. As per ld. AR, the assessment year under appeal is the last year of eligibility of claiming deduction. Ld.AR further submits that assessee has managed separate books of accounts of specified business of electricity generation and the Audit Report in Form 10CCB statutorily prescribed for claiming deduction u/s 80-IA of Act was obtained from the Auditors and filed alongwith the return of income filed. It is thus, submitted that AO has wrongly apportioned the expenditure which has resulted into reduction of amount of deduction of INR 21,84,942/- which is contrary to the settled history of the assessee and thus deserves to be allowed as claimed. The necessary copy of Audit Report is placed at pages 811 to 837 of PB for the year under appeal and for preceding Assessment Years, placed at Pages 811 to 888 of the Paper Book. He prayed accordingly.

39. On the other hand, Ld.CIT DR for the Revenue supports the orders of the lower authorities and submits that principal of res-judicata is not applied to Income Tax proceedings and heavily placed reliance on the judgment of the lower authorities.

40. Heard the contentions of both the parties at length and perused the material available on record. It is an admitted position that in the case of the assessee, deduction u/s 80-IA of the Act was claimed for the first time in AY 2012-13 which was allowed with any doubts. Thereafter for all the assessment years till the year under appeal such claim was allowed without any doubts. It is further observed that assessment for preceding Assessment Years were completed u/s 143(3) of the Act wherein no disallowance was made out of deduction claimed u/s 80IA of the Act. The assessee has also filed a table in its written submissions containing the date of passing of the orders u/s 143(3) for AY 2012-13 to 2020-21 and wherein claim of deduction u/s 80-IA was never doubted. Thus, by respectfully following the Rule of Consistency, deduction claimed by the assessee u/s 80IA of the Act for the last year of the block period, cannot be disbelieved merely on assumptions and presumptions where the AO has made the adhoc disallowance at 0.15% of the total expenses without pointing out any specific expenses related to electricity generation activity and had not been apportioned.