ORDER

Keshav Dubey, Judicial Member.- This appeal at the instant of the assessee is directed against the order of ld. Addl/JCIT(A)-7, Kolkata dated 2.4.2025 vide DIN and Order No. ITBA/APL/S/250/2025-26/1075426187(1) passed u/s. 250 of the Income Tax Act, 1961 (in short “the Act”) for the AY 2017-18.

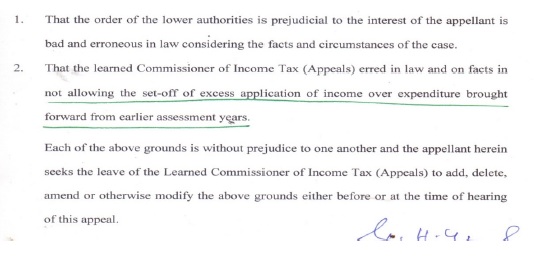

2. The Assessee has raised the following grounds of appeal: –

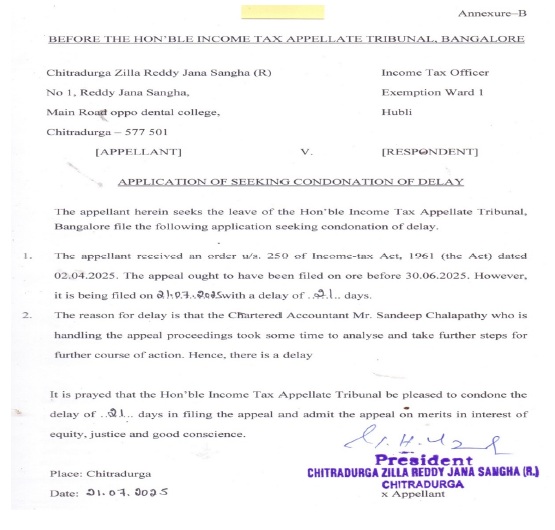

3. At the outset, the ld. A.R. of the assessee submitted that there is a delay of 21 days in filing the appeal before this Tribunal. The ld. A.R. of the assessee also drew our attention on an application for condonation of delay dated 21.7.2025, which is reproduced below for ease of reference and record:

3. 1. On going through the above application for condonation, we find that the assessee could not file the appeal within the prescribed period for the reason that the assessee’s counsel took time to analyze and take steps for further course of action & hence, there is a delay. The ld. A.R. also submitted that the delay is unintentional and no benefit can be attributed to the assessee in filing the appeal belatedly. He thus prayed to condone the delay and requested to consider the issues raised by the assessee on merits.

3. 2 Perused the record and having heard ld. Counsel for the assessee as well as the ld. D.R., it is perceived that the explanation offered in the application dated 21.07.2025 is plausible and sufficient cause being shown by the assessee, which prevented them from filing the appeal within the prescribed period and accordingly, we inclined to condone the short delay of 21 days and admit the appeal for adjudication on merits.

4. Now the brief facts of the case are that the assessee trust being registered u/s 12A of the Act filed its return of income for the assessment year 2017-18 on 14.9.2017 declaring total income of Rs. Nil. The said return was thereafter processed and accordingly intimation u/s 143(1) of the Act was passed on 16.3.2019 disallowing a sum of Rs.76,29,084/- on the ground that the assessee had claimed exemption under “Amount deemed to have been applied to charitable purposes in India during the previous year as per clause (2) of explanation to section 11(1)” but did not exercised his option by e- filing Form-9A before due date as per Rule-17 of the Income Tax Rules.

4.1 The AR of the assessee by way of written submission stated that the assessee trust filed its return of income disclosing gross receipts of Rs.1,73,68,412/- and claimed application of Rs.86,31,373/- towards the revenue expenditure and Rs.11,07,955/- towards the capital expenditure. It is submitted that the entire surplus of Rs.76,29,084/- was inadvertently claimed as amount deemed to have been applied to charitable or religious purposes in India during the previous year as per clause (2) of explanation to section 11(1) of the Act. The assessee trust should have claimed deduction on account of permissible amount of accumulation or set apart for application to charitable or religious purposes to the extent it does not exceed 15% of income derived from property amounting to Rs.26,05,262/- & therefore, the Form No.9A had to be filled for the balance amount of Rs.50,23,822/-[Rs.76,29,084 (-) Rs.26,05,262]. It is also submitted that since the assessee was not aware and was not suggested about the new compliances of filing Form 9A, the assessee could not file the Form 9A along with the return of income. The assessee on becoming aware of the fact also filed an application for condonation of delay in filing form 9A on 20/04/2021 along with the copy of Form 9A, however the ld. CIT(E) rejected the condonation application vide order dated 04/01/2024.

4.2 Without prejudice, the assessee submitted that the surplus of Rs.76,29,084/- was inadvertently claimed as deduction under the amount deemed to have been applied to charitable or religious purposes in India during the previous year as per clause (2) of explanation to section 11(1) of the Act instead of Rs. 26,05,262/-towards permissible amount of accumulation or set apart for application to charitable or religious purposes to the extent it does not exceed 15% of income derived from property & balance of Rs.50,23,822/- towards set off the brought forward expenditure/application over income/Receipts with the current year’s income as per the provision contained in section 11(1) of the Act for which no such form 9A was required to be filed. The assessee has also submitted the detailed chart of excess of Applications over the receipts beginning from AY 2010-11 to AY 2017-18.(Placed at Pg.44 of the PB).

5. Aggrieved by the aforesaid intimation dated 16/03/2019 passed u/s 143(1) of the Act, the assessee preferred an appeal before the ld. CIT(A)/Addl/JCIT(A).

6. The ld. Addl/JCIT(A) on the one hand held that the reasons for the delay of 726 days in filing the appeal before him was not at all satisfactory and the appeal is liable to be dismissed being barred by limitation, however on the other hand by considering the merits of the case partly allowed the appeal of the assessee by holding that the assessee was required to apply at least 85% of the total income as per section 11(1)(a) of the Act. However, the assessee could apply only 97,39,328/- on revenue & capital account. Therefore, the disallowance of exemption u/s 11 of the Act should be restricted to the shortfall of 85% of total income from actual amount applied. Hence, the shortfall of Rs. 50,23,822/-(1,47,63,150 – 97,39,328) should be brought to tax instead of Rs.76,29,084/- as done in intimation and accordingly granted relief of Rs.26,05,262/- to the assessee trust.

7. Again aggrieved by the order of ld. Addl/JCIT(A) dated 02/04/2025, the assessee has filed the present appeal before this Tribunal. The assessee has also filed a paper book comprising 70 pages containing therein written submission, ITR-V & Computation of Income for AY 2017-18, Revised Computation, Annexure-1 Deficit Schedule along with the case laws relied upon by the assessee.

8. Before us, the ld. AR of the assessee at the outset drew our attention on the Fund utilization statement marked as Annexure-1 (placed at Pg. No. 44 of the paper book) & submitted that an amount of Rs.50,23,822/- as confirmed by the ld. Addl/JCIT(A) is to be set off against the carried forward deficit of AY 2011-12. The ld. AR further submitted that as per the annexure it is evident that the cumulative deficit available for AY 2017-18 is of Rs.4,33,36,768/-, which is utilized to set off excess income over expenditure for the AY 2017-18 of Rs.50,23,822/-. Further, the ld. AR submitted that in the intimation u/s 143(1) of the Act, the amount of excess deficit claimed adjusted towards the income has been disallowed on the ground of non-filing of form 9A, however such form 9A is not required to be filed when charitable trust is setting off the excess deficit of previous year to the current year’s income.

9. The ld. DR heavily relied on the intimation passed by the CPC & vehemently submitted that the CPC had rightly disallowed a sum of Rs.76,29,084/- on the ground that the assessee in its return had claimed exemption under “Amount deemed to have been applied to charitable purposes in India during the previous year as per clause (2) of explanation to section 11(1)” but did not exercised its option by e- filing Form-9A before due date as per Rule-17 of the Income Tax Rules.

10. We have heard the rival submissions & perused the materials available on record. It is an undisputed fact that the assessee trust is registered u/s 12A/12AA of the Act since 17/08/1978. The claim of the assessee is that while filing the return of income the entire surplus of Rs.76,29,084/- was inadvertently claimed as exemption under “Amount deemed to have been applied to charitable purposes in India during the previous year as per clause (2) of explanation to section 11(1) of the Act”. The assessee by way of written submission is now claiming that this surplus of Rs. 76,29,084/- shall be reduced by an amount of Rs. 26,05,262/- towards permissible amount of accumulation or set apart for application to charitable or religious purposes to the extent it does not exceed 15% of income derived from property & balance of Rs.50,23,822/- towards set off the brought forward expenditure/application over income/Receipts with the current year’s income as per the provision contained in section 11(1) of the Act for which no such form 9A was required to be filed. The CPC however, while passing the intimation u/s 143(1) of the Act dated 16/03/2019 disallowed a sum of Rs.76,29,084/-on the ground that the assessee had claimed exemption under “Amount deemed to have been applied to charitable purposes in India during the previous year as per clause (2) of explanation to section 11(1)” but did not exercised his option by e- filing Form-9A before due date as per Rule-17 of the Income Tax Rules. The ld. ADDL/JCIT(A) however held that the disallowance of exemption u/s 11 of the Act should be restricted to the shortfall of 85% of total income from actual amount applied. Hence, the shortfall of Rs. 50,23,822/- (1,47,63,150 – 97,39,328) should be brought to tax instead of Rs.76,29,084/- as done in intimation and accordingly granted relief of Rs.26,05,262/- to the assessee trust. The assessee now before us taking a standpoint that this amount of Rs.50,23,822/- as confirmed by the ld. ADDL/JCIT(A) should be set off against the carried forward deficit of AY 2011-12. Before us, the assessee has submitted the Fund Utilization Statement marked as Annexure-1 (placed at page-44 of PB) where the assessee has claimed the cumulative deficit available for AY 2017-18 is of Rs.4,33,36,768/-, which is to be utilized to set off excess income over expenditure for the AY 2017-18 of Rs.50,23,822/-.

10.1 Under the above facts & circumstances, the moot issue that is to be decided in the present case is whether any excess expenditure incurred by trust/charitable institution in earlier assessment year can be allowed to be set off against income of subsequent years by invoking section 11? Undisputedly the present case relates to the Assessment Year 2017-18. Section 11 of the Act has been amended vide Finance Act, 2021 w.e.f. 01/04/2022 by inserting the explanation 5 to section 11(1) of the Act which clarified that the calculation of income required to be applied or accumulated during the previous year shall be made without any set off or deduction or allowance of any excess application of any of the year preceeding the previous year. We are of the considered opinion that the fact that the Finance Act categorically specifies ‘w.e.f. 01-04-2022’ is a strong pointer to prospective application. Therefore, in our opinion prior to 01/04/2022 section 11(1) does not contain any words of limitation to the effect that the income should have been applied for charitable or religious purpose only in the year in which the income has arisen. We are, therefore, of the opinion that the adjustment of the excess expenses incurred by the trust for charitable and religious purposes in the earlier years against the income earned by the trust in the subsequent year would amount to applying the income of the trust for charitable and religious purposes in the subsequent year in which such adjustment has been made and will have to be excluded from the income of the trust under section 11(1)(a) of the Act. The form 9A is not required to be filed when the charitable trust is setting off the excess applications of previous years to the current year’s income/receipts. We are also of the opinion that the issue involved in this appeal is no more res integra.

10.2 We also take note of the fact that the above issue is covered against the revenue by co-ordinate bench of this Tribunal in the case of Deputy Director of Income Tax(E) v. Jyothy Charitable Trust (Bangalore – Trib.). The relevant paragraph is reproduced below for ease of reference & convenience-

“14. We have considered his submission. Section 11(1)(a) does not contain any words of limitation to the effect that the income should have been applied for charitable or religious purpose only in the year in which the income has arisen. The application for charitable purposes as contemplated in section 11(1)(a) takes place in the year in which the income is adjusted to meet the expenses incurred for charitable or religious purposes. Hence, even if the expenses for such purposes have been incurred in the earlier years and the said expenses are adjusted against the income of a subsequent year, the income of such subsequent year can be said to be applied for charitable or religious purposes in the year in which such adjustment takes place. In other words, the set-off of excess of expenditure incurred over the income of earlier years against the income of a later year will amount to application of income of such later year. The above is the position of law as held in the case of CIT v. Maharana of Mewar Charitable Foundation (Raj)and CIT v. Plot Swetamber Murti Pujak Jain Mandal [1995] 211 ITR 293 (Guj.). In CIT v. Institute of Banking Personnel Selection (Bom.) it was held that in case of charitable trust whose income is exempt under s. 11, excess of expenditure in the earlier years can be adjusted against income of subsequent years and such adjustment would be application of income for subsequent years and that depreciation is allowable on the assets the cost of which has been fully allowed as application of income under s. 11 in past years. In Govindu Naicker Estate v. Asstt. DIT (Mad.), the Hon’ble Madras High Court held that the income of the trust has to be arrived at having due regard to the commercial principles, that s. 11 is a benevolent provision, and that the expenditure incurred on religious or charitable purposes in earlier year or years can be adjusted against the income of the subsequent year. The principle that the loss incurred under one head can only be set off against the income from the same head is not of any relevance, if the expenditure incurred was for religious or charitable purposes, and the expenditure adjusted against the income of the trust in a subsequent year, would not amount to an incidence of loss of an earlier year being set off against the profit of a subsequent year. The object of the religious and charitable trust can only be achieved by incurring expenditure and in order to incur that expenditure, the trust should have an income. So long as the expenditure incurred is on religious or charitable purposes, it is the expenditure properly incurred by the trust, and the income from out of which that expenditure is incurred, would not be liable to tax. The expenditure, if incurred in an earlier year is adjusted against the income of a later year, it has to be held that the trust had incurred expenditure on religious and charitable purposes from the income of the subsequent year, even though the actual expenditure was in the earlier years, if in the books of account of the trust such earlier expenditure had been set off against the income of the subsequent year. The expenditure that can be so adjusted can only be expenditure on religious and charitable purposes and no other. The High Court relied on the decision in the case of Society of Sisters of ST. Anne (supra).”

10.3 Further, the Hon’ble High Court of Delhi in the case of DIT v. Raghuvanshi Charitable Trust (Karnataka)/[2010] 328 ITR 669 (Karnataka) has held as under-

“6. We find from the order of the Income Tax Appellate Tribunal (hereinafter referred to as ‘the Tribunal’) that the Tribunal has decided the issue in favour of the assessee by placing reliance on the aforesaid judgment of the Gujarat High Court. We have gone through the judgment of Gujarat High Court in Shri Plot Swetamber Murti Pujak Jain Mandal’s case (supra). It could not be disputed by the learned counsel for the Revenue that the question of law raised and answered in the said case was identical to the one raised in the present appeals. This question was decided in favour of the assessee interpreting the provisions of section 11 of the Act. The relevant discussion contained in the said judgment is in the following terms :

“3 . The learned DR sought to rely upon the finding of Assessing Officer. None was present on behalf of the assessee. We find that the issue is answered by Hon’ble Gujarat High Court in the case of CIT v. Shri Plot Swetamber Murti Pujak Jain Mandal [1995] 211 ITR 293 , wherein the High Court observed as under :

“We are, therefore, of the opinion that the adjustment of he (sic. the) expenses incurred by the trust for charitable and religious purposes in the earlier year against the income earned by the trust in the subsequent year would amount to applying the income of the trust for charitable and religious purposes in the subsequent year in which such adjustment has been made and will have to be excluded from the income of the trust under section 11(1)(a) of the Act.”

No contrary decision has been cited. From the aforesaid judgment, it is clear that there is no bar in computing income of subsequent year after allowing set off of excess amount spent on object of trust, as this also amounts to application of income. Thus, there is no infirmity in the order of the learned CIT(A).”

7. The submission of the learned counsel for the revenue, however, was that the aforesaid case does not decide the question correctly. She submitted that the Gujarat High Court proceeded on the premise that there was no limitation in section 11, which provides that the income should have been applied for charitable or religious purposes ‘only’ in the year in which the income has arisen. This, according to the learned counsel, was a wrong premise and contrary to the expression of provision contained in section 11(1)(c) read with Explanation and section 11(1)(c) categorically suggests to the contrary, viz., the income has to be applied for charitable or religious purposes ‘only’ in the year in which it has arisen.

However, we find that the Gujarat High Court has discussed this issue in greater detail and relying upon the Circular No. 100, dated 24-1-1973 issued by the Central Board of Direct Taxes and the judgment of the Rajasthan High Court in the case of CIT v. Maharana of Mewar Charitable Foundation [1987] 164 ITR 439. We may also point out at this state that the aforesaid view of Rajasthan High Court and Gujarat High Court has been consistently followed by other High Courts in the following judgments :

| (i) |

|

CIT v. Institute of B ankingPersonnel Selection (IBPS) [2003] 264 ITR 110 (Bom.); |

| (ii) |

|

Siddaramanna Charities Trust v. CIT [1974] 96 ITR 275 (Mys.); and |

| (iii) |

|

CIT v. Matriseva Trust [2000] 242 ITR 20 (Mad.); |

8. It would be fruitful to refer to the discussions contained in Institute of Banking Personnel Selection (IBPS)’s case (supra), Per Hon’ble Mr. Justice S.H. Kapadia, which is advanced before us by the learned counsel for the revenue to repel the same in the following words :

“Now coming to question No. 3, the point which arises for consideration is : whether excess of expenditure in the earlier years can be adjusted against the income of the subsequent year and whether such adjustment should be treated as application of income in the subsequent year for charitable purposes? It was argued on behalf of the Department that expenditure incurred in the earlier years cannot be met out of the income of the subsequent year and that utilization of such income for meeting the expenditure of earlier years would not amount to application of income for charitable or religious purposes. In the present case, the Assessing Officer did not allow carry forward of the excess of expenditure to be set off against the surplus of the subsequent years on the ground that in the case of a charitable trust, their income was assessable under self-contained code mentioned in section 11 to section 13 of the Income-tax Act and that the income of the charitable trust was not assessable under the head “Profits and gains of business” under section 28 in which the provision for carry forward of losses was relevant. That, in the case of a charitable trust, there was no provision for carry forward of the excess of expenditure of earlier years to be adjusted against income of the subsequent years. We do not find any merit in this argument of the Department. Income derived from the trust property has also got to be computed on commercial principles and if commercial principles are applied then adjustment of expenses incurred by the trust for charitable and religious purposes in the earlier years against the income earned by the trust in the subsequent year will have to be regarded as application of income of the trust for charitable and religious purposes in the subsequent year in which adjustment has been made having regard to the benevolent provisions contained in the section 11 of the Act and that such adjustment will have to be excluded from the income of the trust under section 11(1)(a) of the Act. Our view is also supported by the judgment of the Gujarat High Court in the case of CIT v. Shri Plot Swetamber Murti Pujak Jain Mandal [1995] 211 ITR 293 . Accordingly, we answer question No. 3 in the affirmative, i.e., in favour of the assessee and against the Department.”

9. It is clear from the above that as many as five High Courts have interpreted the provision in an identical and similar manner. Learned counsel for the revenue could not show any judgment where any other High Court has taken contrary view. Since we are in agreement with the view taken by the aforesaid High Court, we answer these questions in favour of the assessee and against the revenue.”

10.4 The Apex Court in the case of Commissioner of Income Tax (Exemption) v. Subros Educational Society (SC) has also approved the same by dismissing the Misc. application of the Revenue which is reproduced below-

“ORDER

1. In this application filed by the Income-tax Department it is stated that Civil Appeal No. 5171 of 2016 arises out of Special Leave Petition (C) . . . CC No. 8982/2016 was tagged with other appeals and the batch matters were decided by this Court on 13-12-2017. However, the following question was also raised in the instant appeal which was not the subject matter of those appeals:

“(a) Whether any excess expenditure incurred by the trust/charitable institution in earlier assessment year could be allowed to be set off against income of subsequent years by invoking Section 11 of the Income-tax Act, 1961?”

2. To this extent, Mr. K. Radhakrishnan, learned senior counsel appearing on behalf of the applicant/appellant is correct. Therefore, we have heard him on the aforesaid question of law as well but did not find any merit therein.

The miscellaneous application is dismissed”

10.5 In view of the above discussions & respectfully following the above decisions of the Co-ordinate Bench, Hon’ble High Court of Delhi as well as Apex Court, we are inclined to held that any excess expenditure incurred by the assessee trust in earlier assessment years would be allowed to be set off against the income of Rs. 50,23,822/- for the AY 2017-18 by invoking section 11 of the Act. With the above observations, we are remitting the issue to the file of AO to allow the set off of earlier years excess expenditure/applications after proper verification of the same. Needless, to say a reasonable opportunity of being heard must be granted to the assessee. The assessee is also directed to produce the revised computation of income for the AY 2017-18, copy of the Audit reports for the AY 2010-11 to AY 2017-18 along with the details of the funds utilization statement for the verification & examination by the AO. It is ordered accordingly.

11. In the result the appeal filed by the assessee is partly allowed for statistical purposes.