ORDER

Note 1: Under Section 100 of the CGST/RGST Act, 2017, an appeal against this ruling lies before the Appellate Authority for Advance Ruling, constituted under Section 99 of CGST/RGST Act, 2017, within a period of 30 days from the date of service of this order.

Note 2: At the outset, we would like to make it clear that the provisions of both the CGST Act and the RGST Act are the same except for certain provisions. Therefore, unless a mention is specifically made to such dissimilar provisions, a reference to the CGST Act would also mean a reference to the same provision under the RGST Act. Further to the earlier, henceforth for the purposes of this Advance Ruling, a reference to such a similar provision under the CGST Act / RGST Act would be mentioned as being under the “GST Act”.

The issue raised by M/s CPL Pharmaceuticals Private Limited, Cadila Corporate Campus, Sarkhej Dholka Road-Bhat, Ahmedabad-382210, GUJARAT (hereinafter “the applicant”) is fit to pronounce advance ruling as they have deposited prescribed Fee under CGST Act and it falls under the ambit of the Section 97(2) given as under:

(d) admissibility of input tax credit of tax paid or deemed to have been paid

A. SUBMISSION OF THE APPLICANT (in brief) :-

Brief facts of the case:

| 1. |

|

M/s CPL Pharmaceuticals Private Limited (hereinafter referred to as “the Applicant”) is a private limited company, inter alia, engaged in the manufacture and supply of Active Pharmaceutical Ingredients (“APIs”), finished formulations, food supplements, biotechnology products, pharmaceutical machinery etc. |

| 2. |

|

The Applicant is setting up a new plant at RIICO, Udaipur, Rajasthan for manufacturing lyophilized injectable drugs. In order to carry out the construction work of the lyophilized injectable plant (hereinafter referred to as “plant” or “factory”) in RIICO – Kaladawas Extension (Phase II) Udaipur, Rajasthan, the Applicant has issued a Purchase Order dated 14.02.2023 (hereinafter referred to as “PO”) to Sribal Construction Company (hereinafter referred to as “SCC”). A copy of the PO dated 14.12.2023 issued to SCC for carrying out construction works in relation to the lyophilized injectable plant is enclosed herewith and marked as Annexure-1. |

|

|

Technical Specification of the Lyophilized Injectable Plant |

| 3. |

|

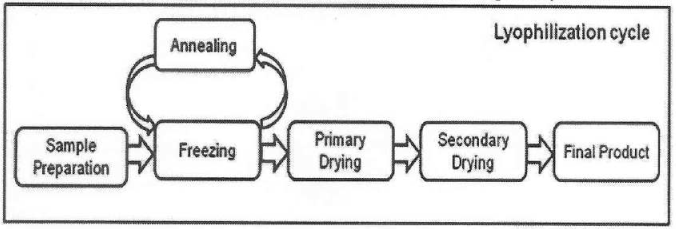

The Applicant states that lyophilization is a freeze-drying process that removes the water from a material. The Applicant uses the lyophilization technique to stabilize and preserve injectable drugs that are sensitive to heat and moisture. In this process, the water is removed from the solution of injectable drugs after the same is frozen. When placed under the vacuum, the ice undergoes sublimation, changing directly from a solid to a vapor without passing through the liquid phase. |

| 4. |

|

The process to manufacture the lyophilized injectable drug is depicted below: |

| 5. |

|

The above manufacturing process contains three primary steps elaborated below: |

| i. |

|

Freezing: The main function of freeze-drying is to separate the solvent from the solute, minimize the thermal degradation of the product, and prevent product foaming when a vacuum is applied. During this stage, most of the water is removed from the drug and excipient. The system separates into multiple phases, and interfaces between the ice and drug phases form. The formulation must be frozen to a sufficiently low temperature to solidify the product. |

| ii. |

|

Annealing: It is an optional step in which the product is held at a temperature above the final freezing temperature for a defined period to crystallize the potentially crystalline components (usually crystalline bulking agents such as mannitol or glycine) in the formulation during the freezing stage. If the bulking agent is not crystallized during the freezing stage, vial breakage may occur during primary drying. Hence, the completion of crystallization may be facilitated by annealing. |

| iii. |

|

Primary Drying: In this stage, the pressure inside the chamber is reduced and heat is applied to initiate the sublimation of ice crystals formed during the freezing stage. The application of a vacuum allows the free migration of water vapor from the frozen mass, which can be regarded as a diffusion process, explaining its relatively slow nature. The solvent vapors resulting from sublimation pass through the opening in the closure. As the sublimation process proceeds, the frozen mass changes into a cake-like structure. Due to the loss of latent heat during sublimation, heat must be continuously applied to the product throughout primary drying. |

| iv. |

|

Secondary Drying: This is the last stage of freeze-drying, in which water that did not freeze is removed by the process of desorption from the solute phase. The objective of secondary drying is to reduce the unbound water (moisture) to a level that is optimal for the stability (less than 1%) of the final product. The shelf temperature in secondary drying is kept much higher than that used for primary drying so that desorption of water may occur at a practical rate. This process is also known as ‘Isothermal Desorption’. |

| 6. |

|

The Applicant submits that manufacturing of lyophilized injectable drugs involves a highly controlled and regulated process to ensure quality, efficacy and safety. Thus, the following equipment will be installed within the plant for manufacturing lyophilized injectable drugs: |

| • |

|

Lyophilizer: This equipment, also known as a freeze dryer, is a device used to remove water from materials through a process called lyophilization or freeze-drying. |

| • |

|

Vial Filling Line (IMA Group): Once the liquid drug formulation is prepared, the same is filled into vials for freeze drying (lyophilization) to remove water content. |

| • |

|

Autoclave: Autoclaving is done for sterilizing equipment, components and the product to ensure sterility and prevent contamination. “Inspection Machine: The vials are inspected to check for defects and contaminants. |

| • |

|

Leak Test Machine: After filling and sealing but before packaging, the vials are checked to ensure the vial integrity. |

| • |

|

Mfg. Skids: Skids are used for precise mixing of drug formulations, ensuring uniformity and consistency. They facilitate the filtration of solutions to remove particulates and contaminants, crucial for maintaining sterility. Skids are employed in purification processes to isolate and purify the active pharmaceutical ingredients (APIs). Additionally, they help in recovering solvents used during the manufacturing process, enhancing efficiency and reducing waste. |

| • |

|

CIP Skid: The equipment is used for automated cleaning and sterilization of various equipment between production batches to maintain hygiene and prevent cross contamination. |

| • |

|

Part Washer: The equipment is used for cleaning and decontaminating various equipment before and after the use of various equipment used in the production of lyophilized injectables. |

| • |

|

Vial Labelling: After inspection, the labels are applied to vials containing details like batch number, expiration date, and drug details. |

| • |

|

Cartonator: It is used for packing vials into cartons for distribution. This is done after labelling and is part of the final packaging process. |

| • |

|

Track and Trace: The equipment is used for monitoring and recording the movement of drugs through the supply chain to prevent counterfeiting during the production and distribution process. |

| • |

|

Check Weighing: The equipment is used to ensure that the vial or package meets the specified weight requirements. |

| 7. |

|

In addition to the above, the Applicant has also installed boiler, chiller, cooling towers, air compressors, diesel generators and transformers within the factory premises. |

| 8. |

|

The Applicant submits that given the plant’s location within a mountain region, the foundational works have been undertaken with due consideration for the inherent topographical and geological factors. The foundation including RCC flooring works were executed using systematic layering of construction materials to ensure structural integrity, durability, and load-bearing capacity. |

| 9. |

|

The Applicant further submits that the aforementioned equipment which are essential for manufacturing lyophilized injectable drugs are required to be installed on a Reinforced Cement Concrete (“RCC”) foundation coupled with steel structural support. This robust foundation is critical to ensure the inherent stability and strength required for these precision machines and equipment during operation. Such construction is being done while adhering to standards outlined in IS 456:2000 (Code of practice for plain and reinforced concrete) and IS 800: 2007 (General construction in steel – Code of Practice). Furthermore, these foundations for the machinery and equipment are constructed in compliance with IS 2974 (Code of practice for design and construction of machine foundations). |

| 10. |

|

The Applicant submits these machines, and equipment cannot be placed directly on the land or its surface without adequate structures to support them. Given the operational load, torque, and vibrations generated during use, a specifically engineered foundation is essential prior to the installation of such machinery and equipment. The foundation serves critical purposes, including providing structural stability, preventing overturning, absorbing vibrations, and ensuring proper alignment and positioning of the equipment. In the absence of such a foundation, machinery is susceptible to operational damage, misalignment, and potential hazards due to instability. |

| 11. |

|

The Applicant submits that the following construction work has been undertaken for the foundation and steel structures whereon the various machinery and equipment is to be installed in the plant: |

|

Sr.No.

|

Description of the Foundation Work as per PO

|

Nature of Work

|

|

1.

|

Excavation in soil for foundations including trenches, pavements, manholes, wall footings, pipelines pits, tanks etc. including shoring, dewatering

|

Excavation of soil for Foundation: Excavation of the soil is a requisite process for undertaking the foundation works in relation to the installation of the equipment. Heavy Machinery installed in lyophilized injectable plant exerts significant weight (loads) on the ground. The topsoil is often not strong enough to support these concentrated loads. Excavation and filling the excavated space with the specially designed foundation ensures collection of equipment load and spreading the same to the larger area, ensuring safe load transfer.

Excavation for Trenches & Pavements: All rainwater harvesting trenches are designed to connect directly with designated water bodies. These trenches require a properly constructed foundation to ensure efficient water transfer from the collection area to the water bodies.

Excavation for Manholes, pipelines, pits & tanks- The transfer of processed water from the sewage treatment plant (STP) to the facility, and sewage water from the facility to the STP, is facilitated by a network of pipelines and manholes. These components are strategically designed to mitigate choking and prevent discrepancies in water flow. Additionally, tanks are constructed for the storage of processed, raw, and potable water. The above requires excavation and the construction of appropriate foundations which are specifically designed to support the load of all installed equipment and ultimately transfer these loads to the ground.

|

|

2.

|

Excavation in soft/weathered rocks including breaking, removal, stacking etc.

|

The breaking of soft and hard rock along with use of excavated hard rock for soling purposes is paramount for equipment installation in the plant. The work ensures that the heavy equipment, which generates significant static and dynamic loads (e.g. vibrations, impacts), is seated on uniform base and prevents sinking of the entire structure, controls vibrations and maintains critical machine alignment. Therefore, the above works have been undertaken to construct a robust and stable foundation specifically designed to support the heavy equipment installed within the factory premises and ultimately transfer these loads to the ground.

|

|

3.

|

Excavation by Chiseling in hard rock

|

Hard rock is chiseled to construct a stable foundation, crucial for installing equipment within the plant.

|

|

4

|

Backfilling of excavated materials

|

The backfilling of murum is critical for preparing the plant’s plinth below the concrete and for various RCC structures.

This process is directly relevant to equipment installation as it establishes a uniformly stable and unyielding base across the entire plant, crucial for supporting the often massive and vibration-sensitive foundations of specialized equipment in the plant.

|

|

5.

|

Carting away surplus excavated material debris

|

If excess material of excavated soil is available at site, then removing this material is necessary as per approved architect levelling plan.

|

|

6.

|

Soling using dry rubble

|

To stabilize base & avoid settlement of foundations, the hard rock base is laid beneath the concrete foundation and within the plinth area of the building.

This foundation layer is essential for preventing differential settlement and for effectively distributing static and dynamic loads from heavy machinery, ensuring the precise alignment, operational efficiency and extended lifespan of all installed equipment within the plant.

|

|

7.

|

Murum Filling in plinth & flooring including sand filling.

|

The Murum filling in plinth and flooring areas, including sand filling, improves the foundational strength by creating a uniform and stable base that effectively distributes the significant static and dynamic loads from the plant and heavy equipment, thereby preventing differential settlement. The layer reduces water permeability by acting as a capillary break, safeguarding the structure and sensitive equipment from moisture damage. Furthermore, the foundation works ensure a stable platform for the concrete plinth.

|

|

8.

|

Concrete Work and other RCC works

|

This includes creation of RCC structures like trenches, manholes, roads etc.

|

|

9.

|

Trimix Cement Concrete Flooring

|

Trimix cement flooring in building plinths and generally for constructing machinery foundations enhances the concrete’s compressive strength. Such a surface is paramount for effectively supporting the heavy, dynamic loads of industrial machinery, ensuring optimal alignment, minimizing vibrations and contributing to the longevity and operational efficiency of the equipment within the plant.

|

|

10.

|

Formwork and Shuttering

|

Formwork refers to a mold into which wet concrete is poured and held until it gains sufficient strength to be self-supporting. This essential structural element, prepared from wood, plywood, PVC or steel, is indispensable for all RCC structures. Formwork dictates the final shape, size, and surface finish of the concrete, ensuring the structural integrity and precise dimensions required for foundations, columns, beams and slabs.

|

|

11.

|

Providing, bending, erecting & fixing mild steel or TOR steel reinforcement.

|

In RCC structures, reinforcement is used in combination with concrete to achieve high strength and durability. While concrete is excellent in resisting compressive forces, it is relatively weak in tension. To overcome this limitation, steel reinforcement, most commonly TOR steel (Twisted Oval Reinforcement) is embedded within the concrete. TOR steel, known for its high tensile strength and ribbed surface, provides superior bonding with concrete and effectively handles tensile stresses. This synergy between concrete and steel ensures that RCC structures can withstand various loads and stresses.

|

|

12.

|

Providing, fabricating, fixing and embedding in position M. S. Plate or structural inserts in concrete or masonry (like corner angles etc.)

|

Embedding MS plates, angles, channels, and other steel components within concrete is essential for facilitating future structural work such as pipe racks and steel frameworks in RCC structures. This ensures the accurate alignment of equipment and efficient load transfer.

|

|

13.

|

Supplying, Straightening, transporting, fabricating, erecting, structural steel work at all levels including cutting, welding, seal welding, bolting, threading, wherever necessary and finishing with sand blasting and one coat of Red Oxide Zinc Chromate primer.

|

The structural steel work is used for the construction of pipe racks, which is used for routing the pipelines installed within the premises of the lyophilized injectable plant.

|

|

14.

|

Providing, fixing, testing and commissioning pipelines within the factory premises.

|

The pipelines are installed to transport raw water, drinking water, steam water for injections, purified water, process water and wastewater. Each of these fluids have unique properties, which determine the material of construction of these pipelines which are installed within the factory premises.

|

| 12. |

|

In this regard, it is submitted that a site inspection dated 16.01.2025 was conducted by the Chartered Engineer, pursuant to which a plant inspection report dated 21.01.2025 has been issued to the Applicant, which certifies that the RCC foundation and steel structural works and other structures as explained above has been undertaken by the Applicant in order to install and support the various equipment and machinery used in the manufacture of lyophilized injectables. As per the report, generally in industries, a number of machineries with different functions are installed. All machinery cannot rest on open land and there is a requirement to create a certain civil structure to support the machinery. This is due to the dead load, torque, vibrations, dynamic load generated due to the usage of machines. Accordingly, the foundation must be designed in such a manner that the machinery installed within the factory premises may not lead to the damage of floor or adjacent structure. The relevant portion of the plant inspection report is reproduced below for your ready reference: |

“Generally in industries, nos. of machines were installed and there are many types of machines with different functions. All machines can not rest on open land or on land surface for that particular civil structure required to support machine.

There are loads affected on machine i.e. Dead load, torque, vibrations, dynamic load and others. To absorb vibration and torque of machine. There has to be foundation design necessary before installing machine.

To support machine in working condition, to stop over turning and reduce vibration effects of machine, there is IS code for design of machine foundation.

If there is no foundation or support for machines, it may damage floor or adjacent structure, there may chances of machine overturning and disturb in positioning.”

(emphasis supplied)

|

|

A copy of the plant inspection report dated 21.01.2025 (without annexures) issued by the chartered engineer is marked and annexed as Annexure – 2. |

| 13. |

|

The Applicant has availed the input tax credit (“ITC”) of tax paid on the purchase of the abovementioned equipment installed within the factory premises of the lyophilized injectables plant, which are used for manufacturing the lyophilized injectable drugs, as the same is eligible to the Applicant in terms of Section 16 and Section 17 of the Central Goods & Service Tax Act, 2017 (hereinafter referred to as “CGST Act”). |

| 14. |

|

The Applicant states that the supplier viz. Sribal Construction Company has issued tax invoices to the Applicant from time to time to recover the consideration for the construction of the foundation works in relation to the installation of equipment within the factory premises and has discharged the tax at the rate of 18% by adopting the SAC 995413 having description “Construction services of industrial buildings such as buildings used for production activities (used for assembly line activities), workshops, storage buildings and other similar industrial buildings”. Illustrative copy of tax invoice issued to the Applicant by Sribal Construction Company is enclosed herewith and marked as Annexure – 3. |

| 15. |

|

During F.Y. 2023-24, Sribal Construction Company has raised tax invoices for total consideration of Rs. 19,68,27,704/-, on which GST amounting to Rs. 3,54,28,987/- has been discharged. It is submitted that the Applicant has availed the proportionate ITC amounting to Rs. 3,54,28,987/- on these input services received from Sribal Construction Company in relation to foundation and structural support for the various equipment installed in the lyophilized injectables plant. The ITC pertains to the foundational work mentioned at Paragraph 2.11 (supra). A copy of the excel sheet containing the details of break-up of the input services used for construction of foundation and structural support for various equipment of the API plant is enclosed herewith and marked as Annexure – 4. |

| 16. |

|

The Applicant is of the view that the works contract services received by the Applicant from Sribal Construction Company for the foundational and structural support for plant & machinery in terms of Explanation to Section 17 of the CGST Act, 2017. Accordingly, ITC on such input services received by the Applicant is eligible in terms of Section 16 and Section 17 of the CGST Act, 2017. |

B. INTERPRETATION AND UNDERSTANDING OF APPLICANT ON QUESTION RAISED (IN BRIEF)

The ITC of tax paid on input services used for the construction of foundation and structural support for various equipment used at the factory of the Applicant for carrying out the manufacturing of lyophilized injectable drugsis eligible in terms of Section 17(5)(c) of the CGST Act, 2017:

| • |

|

The input services procured by the Applicant are in the course or furtherance of business of the Applicant in terms of Section 16 of the CGST Act. |

| 1. |

|

As per Section 2(60) of the CGST Act, the expression “input service” is defined as any service used or intended to be used by a supplier in the course or furtherance of business. |

| 2. |

|

Section 16 of the CGST Act states that every registered person shall be entitled to take credit of input tax charged on any supply of goods or services or both by him which are used or intended to be used in the course or furtherance of his business and said amount will be credited to the electronic credit ledger of such person. |

| 3. |

|

The Applicant submits that the lyophilized injectables plant is to be used for manufacturing lyophilized injectables which will be supplied by the Applicant to its customers. Thus, the input services procured by the Applicant for construction of foundation and structural support for various equipment at the factory of the Applicant is in the course or furtherance of business of the Applicant. |

| 4. |

|

Thus, it is submitted that the Applicant is eligible to avail the ITC on input services received for construction of foundation and structural support for installing the equipment within the factory premises of the Applicant in terms of Section 16 of the CGST Act. |

| • |

|

The input services procured by the Applicant are used for foundation and structural support of the equipment installed for manufacturing lyophilized injectable drugs, which are “plant and machinery’ in terms of Explanation to Section 17 of the CGST Act. |

| 5. |

|

Section 17(5) provides that notwithstanding anything contained in sub-section (1) of section 16 and subsection (1) of section 18, input tax credit shall not be available in respect of the following, namely: – |

“(c) works contract services when supplied for construction of an immovable property (other than plant and machinery) except where it is an input service for further supply of works contract service;”

(Emphasis supplied)

| 6. |

|

As per the above provision, ITC is not restricted where inward supply of works contract services are received for further supply of works contract services, or such services are for construction of plant and machinery. It is pertinent to understand the scope of expression “plant and machinery”. |

| 7. |

|

The Explanation to Section 17 of the CGST Act provides the definition of the expression “plant and machinery” as under: |

“Explanation.- For the purposes of this Chapter and Chapter VI, the expression “plant and machinery” means apparatus, equipment, and machinery fixed to earth by foundation or structural support that are used for making outward supply of goods or services or both and includes such foundation and structural supports but excludes-

| (i) |

|

land, building or any other civil structures; |

| (ii) |

|

telecommunication towers; and |

| (iii) |

|

pipelines laid outside the factory premises.” |

(Emphasis supplied)

| 8. |

|

The terms “equipment” or “apparatus” have not been defined under the GST law. Therefore, recourse may be made to the dictionary meaning of the said terms. |

|

|

Meaning of the term “Equipment” |

| 9. |

|

As per the Collins Dictionary, “equipment” as a noun is defined as whatever a person, group, or thing is equipped with; the special things needed for some purpose; supplies, furnishings, apparatus, etc.; goods used in providing service, esp. in transportation, as the rolling stock of a railroad. |

| 10. |

|

As per the Merriam Webster Dictionary, “equipment” is defined as the set of articles or physical resources serving to equip a person or thing such as the implements used in an operation or activity. |

| 11. |

|

Further, as per the Macmillan Dictionary, “equipment” is defined as the tools, machines, or other things that you need for a particular job or activity. |

|

|

Meaning of the term “Apparatus” |

| 12. |

|

As per the Collins Dictionary, “apparatus” as a noun is defined as a collection of instruments, machines, tools, parts, or other equipment used for a particular purpose. |

| 13. |

|

As per the Merriam Webster Dictionary, “apparatus” is defined as a set of materials or equipment designed for a particular use. |

| 14. |

|

Webster’s Encyclopaedic Unabridged Dictionary of English language defines ‘apparatus’ as: |

| a. |

|

A group or aggregate of instruments, machinery, tools, materials etc., having a particular function or intended for a specific use. |

| b. |

|

Any complex instrument or machine for a particular purpose. |

| c. |

|

Any system or systematic organization of activities, functions, processes, etc., directed toward a specific goal. |

|

|

Meaning of the term ‘machinery’: |

| 15. |

|

The Concise Oxford Dictionary defines the terms ‘Machine’ and ‘Machinery’ as |

| (a) |

|

An apparatus using or applying mechanical power and having several parts, |

| (b) |

|

Each with a definite function and together performing a particular task. Any device that transmits a force or directs its application |

| (a) |

|

Machines collectively or components of a machinery |

| • |

|

Therefore, the term ‘machinery’ signifies an assembly of items designed to perform a mechanical function entailing application of force either manually or otherwise to achieve a pre-determined result. Whereas the terms ‘apparatus’ and ‘equipment’ signify an aggregation of tools, materials or machine designed to perform a specific function. |

| • |

|

Reference may be made to the decision of I.C.B. (P) LTD. v. Collector of Central Excise, Baroda 1997 (95) E.L.T. 239 (Tribunal), wherein the term ‘apparatus’ was defined as a compound instrument designed to carry out a specific function or for a particular use. It was observed that in order to decide, whether a particular object is an apparatus, an inquiry has to be made as to what operation it performs. |

| • |

|

Further, the Bombay High Court in the case of Siemens India Ltd v. Commissioner of Income Tax (Bombay)/[1996] 217 ITR 622 (Bombay) , while deciding whether a particular item is plant or not, referred to the “common parlance or trade or commercial parlance” test and the “functional test” as applied in the judgement of the Hon’ble Supreme Court in the case of Scientific Engineering House Private Limited v. CIT (1986) 1 SCC 11. |

| • |

|

The Hon’ble Supreme Court in the case of Scientific Engineering House Private Limited (supra), relied upon certain foreign decisions while dealing with the question whether technical know-how in the shape of drawings, designs, charts, plans, processing data and other literature falls within the definition of “plant”, gave it a wide meaning under the provisions of Income Tax law and held such books to be a depreciable asset. It was observed by the Supreme Court that “plant” would include any article or object fixed or movable, live or dead, used by businessman for carrying on his business and it is not necessarily confined to an apparatus which is used for mechanical operations or processes or is employed in mechanical or industrial business. It was further observed that in order to qualify as “plant”, the article must have some degree of durability, as for instance, in Hinton v. Maden & Ireland Ltd. [1960] 39 I.T.R. 357 (HL), knives and lasts having an average life of three years used in manufacturing shoes were held to be “plant”. |

| • |

|

In Inland Revenue Commissioner v. Barclay, Curle& Co. Ltd. [1970] 76 I.T.R. 62 (HL), the House of Lords held that a dry dock, since it fulfilled the function of a plant, must be held to be a plant. Lord Reid considered the part which a dry dock played in the assessee company’s operations and observed: |

“It seems to me that every part of this dry dock plays an essential part . The whole of the dock is, I think, the means by which, or plant with which, the operation is performed.”

| • |

|

Lord Guest indicated a functional test in these words: |

“In order to decide whether a particular subject is an ‘apparatus’ it seems obvious that an enquiry has to be made as to what operation it performs. The functional test is, therefore, essential at any rate as a preliminary”.

| • |

|

Further, reference may be made to the scope of the term “machinery” as discussed in the case of Ambica Wood Works v. State of Gujarat (1979) 43 STC 338 (Guj). The Gujarat High Court analyzed the scope of machinery by looking into the dictionary meaning in Webster’s New Twentieth Century Dictionary, Unabridged, Second Edition. From the dictionary meanings, the following understanding was taken by the Court: |

“9. In other words, if there is a combination of things, the harmonious working of which results in a desired end, that collection of things would be known as machinery.”

| • |

|

It was further observed at para 10 that “It is no doubt true that mere assembly of articles or things would not amount to machinery. Some solid structure with no moving parts cannot be termed as machinery. It would be machinery only if such structure, complete in itself, has moving parts in relation with others when they move interdependently by application of force – mechanical or manual – with an avowed object to produce a given product. In other words, in order to be a machinery, the following four factors must exist, namely: (1) a complete and integrated collection of several objects or articles; (2) these objects or articles should interact in unison upon or with each other; (3) this interaction is prompted by application of force which may be manual or motive power; and (4) the movement should be with a view to do some specific activity or to obtain specific or definite result.” |

| • |

|

From the above discussion, the following tests emerge for determining whether a particular product will qualify as plant and machinery: |

| • |

|

In order to qualify as ‘plant and machinery’ in terms of Explanation to Section 17 of the CGST Act, two major requirements need to be satisfied, which are as under: |

| a. |

|

It is an ‘apparatus’, ‘equipment’ or ‘machinery’ fixed to earth by foundation or structural support; and |

| b. |

|

It is used for making an outward supply of goods or services or both. |

|

|

‘Apparatus’, ‘Equipment’ or ‘Machinery’ |

| • |

|

Relying upon the definitions of the term ‘apparatus’, it can be said that the various equipment which are to be set up for manufacturing lyophilized injectable drugs will qualify as ‘apparatus’ since the system includes setting up of a collection of instruments, tools, parts or other equipment used for a particular well-defined purpose. |

| • |

|

It can also be said to be ‘machinery’ as the complete lyophilized injectables plant is a combination of various things/components and the harmonious working of all such components results in the desired end of manufacturing lyophilized injectable drugs. |

| • |

|

Further, the nature of various equipment installed in the lyophilized injectables plant may be examined on the parameters of the tests referred to in para 4.25 above. |

| • |

|

Common parlance test – In common parlance, all the equipment installed in the lyophilized injectable plant viz. lyophilizer, vial filing line, autoclave, inspection machine, leak test machine, mfg. skids, CIP skid, part washer, vial labelling, cartonator, track and trace and check weighing etc. can be understood as ‘apparatus’ or ‘equipment’. |

| • |

|

Functional test – All these equipment has a well-defined function to manufacture lyophilized injectable drugs. |

| • |

|

Durability test – The above-mentioned equipment is expected to last for several years and hence it also satisfies this test. |

| • |

|

Close Nexus test – The various equipment has a close nexus with the manufacturing of the lyophilized injectable drugs in as much as all these equipment is a sine qua non for setting up the lyophilized injectable plant and without these equipments, the Applicant will not be able to manufacture their end products viz. lyophilized injectable drugs. |

| • |

|

Thus, in light of the above, it is submitted that all the equipment installed within the factory premises for manufacturing the lyophilized injectable drugs satisfy all the tests specified above and fall within the scope of the term ‘plant and machinery’ in terms of Explanation to Section 17 of the CGST Act, 2017. |

| • |

|

Reliance in this regard is also placed on the recent CBIC Circular No. 219/13/2024-GST dated 26.06.2024, wherein it has been clarified that ITC on ducts and manholes used in network of Optical Fiber Cables (“OFCs”) is eligible in terms of Section 17(5) of the CGST Act, 2017. The Circular states that it appears that ducts and manholes are covered under the definition of ‘plant and machinery’ as they are used as part of the OFC network for making outward supply of transmission of telecommunication signals from one point to another. It is further observed in the circular that ducts and manholes used in network of OFCs have not been specifically excluded from the definition of “plant and machinery” in the Explanation to Section 17 of the CGST Act, 2017, as they are neither in the nature of land, building or civil structures nor are in the nature of telecommunication towers or pipelines laid outside the factory premises. The relevant portion of the circular is reproduced below for ease of reference: |

“3. Ducts and manholes are basic components for the optical fiber cable (OFC) network used in providing telecommunication services. The OFC network is generally laid with the use of PVC ducts/sheaths in which OFCs are housed and service/connectivity manholes, which serve as nodes of the network, and are necessary for not only laying of optical fibre cable but also their upkeep and maintenance. In view of the Explanation in section 17 of the CGST Act, it appears that ducts and manholes are covered under the definition of “plant and machinery” as they are used as part of the OFC network for making outward supply of transmission of telecommunication signals from one point to another. Moreover, ducts and manholes used in network of optical fibre cables (OFCs) have not been specifically excluded from the definition of “plant and machinery” in the Explanation to section 17 of CGST Act, as they are neither in nature of land, building or civil structures nor are in nature of telecommunication towers or pipelines laid outside the factory premises.

(emphasis supplied)

| • |

|

Accordingly, it is clarified that availment of ITC is not restricted in respect of such ducts and manhole used in network of optical fibre cables (OFCs), either under clause (c) or under clause (d) of subsection (5) of section 17 of CGST Act. |

| • |

|

As per the above circular, ducts and manholes used in the network of OFCs are falling within the scope of ‘plant and machinery’ in terms of Explanation to Section 17 of the CGST Act, 2017. The Applicant submits that placing reliance on this circular, an inference can be drawn that since various equipment installed within the factory premises are essential and necessary for manufacturing the lyophilized injectable drugs, accordingly, the equipment installed for the said purpose will be covered under the definition of ‘plant & machinery’ as they will be integral part used for making outward supply. |

| • |

|

Further, as per the circular, ducts and manholes are not specifically excluded from the definition of ‘plant and machinery’ in the Explanation to Section 17 of the CGST Act, 2017 as they are neither in nature of land, building or civil structures nor are in nature of telecommunication towers or pipelines laid outside the factory premises. |

| • |

|

The Applicant submits that in the present case as well, the various equipment enumerated above, which are installed in the lyophilized injectable plant are not specifically excluded from the definition of ‘plant and machinery’ as such equipment are neither in the nature of land, building or civil structures nor are in the nature of telecommunication towers or pipelines laid outside the factory premises. |

| • |

|

Thus, the equipments installed for manufacturing lyophilized injectable drugs are falling under the term ‘plant and machinery’ in terms of Explanation to Section 17 of the CGST Act, 2017. |

|

|

Used for making outward supply of goods or services or both. |

| • |

|

Now, examining the second condition which states that the said plant and machinery should be used for making outward supply of goods/services. In present case, the Applicant will manufacture lyophilized injectable drugs by using the equipment installed within the lyophilized injectable plant. Thus, the second condition stands fulfilled as well. |

| • |

|

In light of the above, it is submitted that the equipment installed for the production of lyophilized injectable drugs qualify as ‘plant and machinery’ in terms of Explanation to Section 17 of the CGST Act. |

| • |

|

The ITC on input services procured for undertaking foundation works in relation to the installation of plant and machinery within the factory premises is eligible to the Applicant. |

| • |

|

As per the definition of the expression “plant and machinery” under the Explanation to Section 17 of the CGST Act reproduced at para 4.7 (supra), it includes the foundation or structural support for such plant and machinery. Thus, the foundation or structural support for plant and machinery will also fall within the scope of “plant and machinery” and ITC on works contract services used for such construction of foundation and structural support will be eligible in terms of Section 17(5)(c) of the CGST Act. |

| • |

|

It is pertinent to note that the term ‘foundation and structural support’ has not been defined in the CGST Act. Further, there exists no exclusion from the scope of ‘foundations and structural support’ when such work is undertaken for the installation and erection of the plant and machinery. Consequently, in the absence of such exclusion, all such foundational works undertaken for the installation of plant and machinery shall be deemed to be part of the plant and machinery in accordance with the Explanation under Section 17 of the CGST Act. |

| • |

|

Therefore, let us examine as to what would be covered under the term ‘foundation and structural support’. |

| • |

|

The term “foundation” has not been defined in the CGST Act. Therefore, reference can be made to S.B. Sarkar’s, Words and Phrases of Excise, Customs & Service Tax, 4th Edition (2006), CENTAX Publications Pvt. Ltd., which defines “foundation” as: |

“inter alia means the lowest load bearing part of the building, typically below ground level; A construction below the ground level that distributes the load of a building, wall etc. (The New Collins) – Solid ground or base, natural or artificial, on which building rests, lowest part of the building usually below ground-level”

(emphasis supplied)

| • |

|

In this context, reference can also be placed upon the decision of Hon’ble Karnataka High Court in the case of J.K. Cement Works v. State of Karnataka (Karnataka)/[2017] 7 GSTL 408 (Karnataka)(2017) 7 GSTL 408 (Kar.), wherein it has been held that the plant and machinery for manufacturing of cement by itself would be nothing and would be useless, unless they are properly installed and erected with proper foundations and civil works for erection thereof and in that process, the use of cement for construction of such foundations/civil works would constitute an integral part of the overall cost of the plant and machinery itself. |

| • |

|

On the combined reading of the above, it appears that the term ‘foundation’ will include all construction activities carried out at ground level and below ground level that are essential for distributing the load of the plant and machinery installed for manufacturing operations. |

| • |

|

In the present case, the foundation works have been executed in accordance with IS 2974 part 5: 1987 (Design and Construction of Machine Foundation) considering the machine loads and dynamic force, torque & vibrations of machines. The IS code provides that the installation of machines and equipment involves careful design of their foundations taking into consideration the impact and related vibration characteristics of the load and the condition of the soil on which the foundation rests. While many of the special features relating to design and construction of such machine foundations will have to be as advised by the manufacturers of these machines, still most of the details will have to be according to the general principles of design. This standard lays down the general principles of planning and design of reinforced machines and equipment other than the hammers. A copy of the IS 2974 part 5: 1987 (Design and Construction of Machine Foundation) is enclosed herewith and marked as Annexure – 5. |

| • |

|

Furthermore, to ensure that the structural base within the factory premises can adequately bear the load of the installed machinery and to prevent any risk of subsidence due to such load, the design and construction of the foundation works have been carried out in accordance with the provisions of IS 800:2007 and IS 456:2000. These standards provide the necessary guidelines for structural steel and reinforced concrete design, respectively, thereby ensuring the safety, durability, and stability of the foundation system supporting the plant and machinery. Copies of the IS 800:2007 and IS 456:2000 have been enclosed herewith and marked as Annexure – 6. |

| • |

|

It is submitted that the foundational works undertaken, comprising of excavation of soil, chiseling in hard rock, backfilling, carting away, soling, murum filling, concrete works, trimix cement concrete flooring, formwork and shuttering, and TOR steel reinforcement as detailed in para 2.9 (supra) have been executed considering the machine loads, dynamic forces, torque and vibrations generated by the plant and machinery installed within the factory premises. These specialized foundation works are critical to ensuring structural integrity, preventing subsidence and enabling the foundation to effectively absorb operational loads. |

| • |

|

The Applicant submits that since the equipment installed for the production of lyophilized injectable drugs qualifies as ‘plant and machinery’ in terms of Explanation to Section 17 of the CGST Act and thus, the various foundational works detailed in para 2.9 (supra) is in the nature of ‘foundation and structural support’ for these equipment. |

| • |

|

The Applicant further submits that in addition to the above foundation works, SCC has also undertaken the construction of pipe racks and steel frameworks. The structural steel works have been performed for the pipelines which are installed within the factory premises for the transportation of raw water, drinking water, steam water for injection, purified water, process water and wastewater etc. These pipelines enable the transfer of materials between storage tanks and various process units and other connected facilities. Therefore, structural steel is used to provide primary support and stability to the pipe racks, bearing both the self-load of the pipe rack and the dynamic load of the materials being transported. |

| • |

|

As the foundation and structural works have been undertaken specifically for the installation of pipelines within the factory premises, such works do not fall within the exclusions outlined in the definition of ‘plant and machinery’ under the Explanation to Section 17(5) of the CGST Act, 2017. Accordingly, the foundational and structural support works directly attributable to the installation of such internal pipelines shall be considered part of the plant and machinery, and therefore, the Applicant is eligible to avail the ITC on such foundation and structural works. |

| • |

|

Reliance in this regard is placed on the recent ruling issued by the Appellate Authority for Advance Rulings, Gujarat in the case of KEI Industries Ltd., In re (AAAR – GUJARAT). In this case, the applicant had filed an appeal against the ruling passed by AAR Gujarat on the issue of ITC eligibility on inputs and input services used for construction of a concrete tower to act as foundation and structural support for VCV manufacturing line. It was held that the VCV manufacturing line qualifies as ‘plant and machinery’ and accordingly, the concrete tower is an essential foundation and structural support for such VCV manufacturing line. It was further observed that the concrete structure is not a general building but a specialized support system that is integral to the functioning of the machinery, providing stability and absorbing vibrations. The relevant portion of the ruling is reproduced below for ease of reference: |

“16. Ongoing through the layout of the VCV line which is reproduced in the impugned ruling, the process inside VCV tower undertaken at each floor and the weight of the significantly heavy components to be placed on each floor [reproduced supra], we are in agreement with the appellant’s averment that the concrete structure is essential to support and erect the VCV lines. It is more so since the appellant has stated that the concrete structure in the form of VCV tower serves as a critical foundation and support system for the manufacturing process; that it provides stable base for tower components; that it absorbs vibrations & ensures accurate positioning of extruder, cross head and other elements. Given these facts, we find that plant and machinery in terms of the second explanation, placed beneath section 17, ibid, specifically includes foundation and structural support. The exclusions from plant and machinery are also listed viz (i) land, building or any other civil structures; (ii) telecommunication towers; and (iii) pipelines laid outside the factory premises. Further, ‘other civil structures’ means civil structures other than foundation and structural support to plant and machinery.

17. Thus, the moment it is held that the ITC sought is on construction of foundation and structural support relating to plant and machinery, it moves out of the ambit of section 17(5)(c) and (d) even if it is on their own account. This being the case, we find that the applicant is eligible for availing the ITC on inputs and input services used for construction of concrete tower to support and erect the VCV lines at the factory of the appellant for manufacture of EHV cables.

18. … Drawing the analogy from the aforementioned clarification, we find that when ITC is not restricted even in respect of ducts and manhole used in OFCs under section 17(5) of the CGST Act, 2017, the ITC, on inputs and input services used for construction of concrete tower to support and erect the VCV lines, for manufacture of EHV cables also, similarly, cannot be restricted.”

(emphasis supplied)

| • |

|

As per the above ruling, the AAAR Gujarat has held that ITC on inputs and input services used for construction of concrete tower to support and erect the VCV lines at the factory of the applicant for manufacture of EHV cables is eligible to the applicant as it constitutes foundation and structural support for ‘plant and machinery’ in terms of Explanation to Section 17 of the CGST Act, 2017. The exclusion for ‘land, building or any other civil structure’ does not apply, as the tower qualifies as a ‘structural support’ which is specifically included in the definition of ‘plant and machinery’. |

| • |

|

Placing reliance on the above ruling, the Applicant submits that the ITC on the input services procured for the construction of RCC foundation and structural support for the various equipment enumerated hereinabove is eligible as such construction qualifies as ‘foundational and structural support for plant and machinery’ in terms of the Explanation to Section 17 of the CGST Act, 2017. |

| • |

|

In light of the above submissions, the Applicant submits that the ITC on input services procured for foundation and structural works within the factory premises for the installation of the plant and machinery will be eligible in terms of Section 16 and Section 17 of the CGST Act. |

C. QUESTIONS ON WHICH THE ADVANCE RULING IS SOUGHT:

Q-1 Whether the Applicant is eligible to avail ITC on input services used for construction of foundation and structural support for plant and machinery installed at the factory of the Applicant for manufacture of lyophilized injectables, in terms of Section 17(5)(c) of the CGST Act, 2017?

D. COMMENTS OF THE JURISDICTIONAL OFFICER:-

Comments received from the OFFICE, Joint Commissioner, State Tax, Circle-B, Zone- Udaipur, Room No. 201, New Kar Bhawan, Near Patel Circle, UDAIPUR, Rajasthan vide letter No.SR/DC/B/UDR/428 dated 19.09.2025 are as under:

Comments on Application of Advance Ruling of Firm

M/s CPL Pharmaceuticals Private Limited (hereinafter referred to as “the Applicant”) is a private limited company, inter alia, engaged in the manufacture and supply of Active Pharmaceutical Ingredients (“APIS”), finished formulations, food supplements, biotechnology products, pharmaceutical machinery etc. The Applicant is setting up a new plant at RIICO, Udaipur, Rajasthan for manufacturing lyophilized injectable drugs.

The Applicant submits that given the plant’s location within a mountain region, the foundational works have been undertaken with due consideration for the inherent topographical and geological factors. The foundation including RCC flooring works were executed using systematic layering of construction materials to ensure structural integrity, durability, and load-bearing capacity.

The applicant submit following Submission

1. Excavation in soil for foundations including trenches. pavements, manholes, wall footings, pipelines pits, tanks ete. including shoring, dewatering

Comments- All above process mentioned by applicant are related to process of construction of a building immovable property. Such as trenches. pavements, manholes, wall footings. pipelines pits, tanks etc. The applicant is paying GST on construction activity is of immovable nature. The provisions of ITC for the said supply of goods is covered under Section 17(5)(d). Therefore, ITC on GST paid on such supply as mentioned above will not be available to the extent of capitalisation of the said goods as mentioned in Explanation of Section 17(5) of the CGST/RGST Act, 2017.

So applicant is not eligible to avail ITC on above Point.

2. Excavation in soft/weathered rocks including breaking.

Comments- In above processes the The breaking of soft and hard rock along with use of excavated hard rock for soling purposes is paramount for equipment installation in the plant. All above process mentioned by applicant are related to process of construction of a building immovable property So applicant is not eligible to avail ITC on above Point.

3. Excavation by Chiseling in hard rock

Comments- In above processes the Hard rock is chiseled to construct a stable foundation involved, above process mentioned by applicant are related to process of construction of a building immovable property.

So applicant is not eligible to avail ITC on above Point

4. Backfilling of excavated materials-

Comments-Backfilling is the process of strategically refilling an excavated area with suitable materials, typically after a foundation, trench, or other structure has been built. This involves placing the material in layers and compacting it to achieve a dense and stable fill done by Excavators, crans, loaders, also used in work contract activity in any premises related to process of construction of a building immovable property

So applicant is not eligible to avail ITC on above Point

5. Carting away surplus excavated material debris

Comments – Carting away excavated material, also known as process of construction of a building immovable property

So applicant is not eligible to avail ITC on above Point

6. Soling using dry rubble

Comments – Rubble soling is the procedure of laying hard stones of required specifications adjacent to one another, with minimal voids in between them. The gaps are filled with stone chips or moorum to firmly pack the soling as required. Dealer used all process which are related to construction of immovable structure / premises. So applicant is not eligible to avail ITC on above Point

7. Murum Filling in plinth & flooring including sand filling.-

Comments – Murum filling in a plinth involves the layer-by-layer compaction of a granular soil material called murrum (a mixture of gravel, rock particles, and minerals) to create a stable base for a building’s floor. Which is clearly construction of immovable structure, area of machine set up also not mentioned.

So applicant is not eligible to avail ITC on above Point

8. Concrete Work and other RCC works. –

Comments – Process used to strengthen base/plinth again part of works of construction.

So applicant is not eligible to avail ITC on above Point

9. Trimix Cement Concrete Flooring –

Comments – All above process mentioned by applicant are related to process of construction of a building immovable property

So applicant is not eligible to avail ITC on above Point

10. Formwork and Shuttering

Comments – Formwork and shuttering are moulds or structures that give wet concrete its desired shape and support until it sets and hardens. Made from materials like timber, steel, aluminum, or plastic, these molds hold the concrete in place, allowing it to cure and achieve its designed strength and dimensions for structural elements such as beams, columns, and slabs it is very clear with the definition of said process that this is also nothing but construction of immovable property.

So applicant is not eligible to avail ITC on above Point

11. Providing, bending, erecting & fixing mild steel or TOR steel reinforcement.-

Comments- Dealer used all process which are related to construction of immovable structure / premises.

So applicant is not eligible to avail ITC on above Point

12. Providing, fabricating, fixing and embedding in position M.S. Plate or structural inserts in concrete or masonry (like corner angles etc.)

Comments -This civil work is required in any factory building construction, which is an immoveable property.

So applicant is not eligible to avail ITC on above Point

13. Supplying, Straightening, transporting. fabricating. erecting, structural steel work at all levels including cutting, welding. seal welding. bolting, threading, wherever necessary and finishing with sand blasting and one coat of Red Oxide Zine Chromate primer.

Comments- This process adheres fabrication, and erection to ensure structural integrity and quality. This process directly related to Straightening of iron structure.

So applicant is not eligible to avail ITC on above Point

14. Providing, fixing, testing and commissioning of pipelines within the factory premises.

Comments -Dealer used all process which are related to construction of immovable structure / premises

So applicant is not eligible to avail ITC on above Point

Conclusion

Section 17(5) in The Central Goods and Services Tax Act, 2017 Section 17(5) of the CGST Act, 2017, restricts the availability of Input Tax Credit (ITC) under GST.

(c) works contract services when supplied for construction of an immovable property (other than plant and machinery) except where it is an input service for further supply of works contract service;

(d) goods or services or both received by a taxable person for construction of an immovable property (other than plant or machinery) on his own account including when such goods or services or both are used in the course or furtherance of business.

The Applicant states that the supplier viz. Sribal Construction Company has issued tax invoices to the Applicant from time to time to recover the consideration for the construction of the foundation works in relation to the installation of equipment within the factory premises and has discharged the tax at the rate of 18% by adopting the SAC 995413 having description “Construction services of industrial buildings such as buildings used for production activities (used for assembly line activities), workshops, storage buildings and other similar industrial buildings”.

Applicant itself declared that Sribal Construction Company having description “Construction services of industrial buildings such as buildings used for production activities. It is very clear that the Bills are related to construction of Imoveable property.

Final Comments- In the Light of above points ITC received from Sribal Construction

Company is also part of works contract. So applicant is not eligible to avail ITC on all points.

E. PERSONAL HEARING:

In the matter, personal hearing was granted to the applicant on 04.09.2025. Ms. Priyanka Kalwani, Advocate and Mr. Devanshi Sharma Advocate &Authorized Representative appeared for personal hearing. They stated that they will submit the details within 7 days regarding time of supply, the date of eligibility of ITC, Ledger copy, Whether ITC has been availed, whether 9C has been filed and details of payment mode in respect of construction of lyophilized injectable plant.

F. DISCUSSIONS AND FINDINGS

| 1. |

|

We have carefully examined the statement of facts, the application filed by the applicant, the submissions made during the hearing, and the comments from the jurisdictional Tax Authority. We also considered the issues involved for which the advance ruling is sought, along with other relevant facts. |

| 2. |

|

The issue raised by M/s CPL Pharmaceuticals Private Limited, Kaladawas Extension (Phase II), Plot No. SP 02, RIICO Industrial Area, Udaipur, Rajasthan, is fit to pronounce an advance ruling as it falls under the ambit of Section 97(2)(d) of the CGST Act, 2017. This section covers the admissibility of input tax credit of tax paid or deemed to have been paid. |

| 3. |

|

The core issue for determination is whether the construction services used for the foundation and structural supports for heavy machinery qualify as ‘works contract services for construction of an immovable property (other than plant and machinery)’ attracting the blockage under Section 17(5)(c) of the CGST Act, 2017. |

| 4. |

|

We first refer to the relevant provisions of the Central Goods and Services Tax Act, 2017: |

Section 17(5)(c): “Notwithstanding anything contained in sub-section (1) of section 16 and subsection (1) of section 18, input tax credit shall not be available in respect of the following, namely:-

(c) works contract services when supplied for construction of an immovable property (other than plant and machinery) except where it is an input service for further supply of works contract service.”

Explanation “For the purpose of clause (c) and (d), the expression “Construction” includes reconstruction, renovation, additions or alterations or repairs, to the extent of capitalization, to the said immovable property”

Explanation to Section 17: “For the purposes of this Chapter and Chapter VI, the expression “plant and machinery” means apparatus, equipment, and machinery fixed to earth by foundation or structural support that are used for making outward supply of goods or services and includes such foundation and structural supports but excludes-

(i) land, building or any other civil structures;

(ii) telecommunication towers; and

(iii) pipelines laid outside the factory premises.”

| 5.1 |

|

On a plain reading of the Explanation to Section 17, it is clear that the definition of “plant and machinery” is inclusive, and it explicitly includes the “foundation and structural supports” used to fix the equipment to the earth, provided they are used for making outward supply of goods or services but excludes land, building any other civil structure, telecommunication towers and pipelines laid outside the factory premises. |

| 5.2 |

|

Further, for the purpose of section 17(5)(C), the expression “Construction”, which is capitalized to the said immovable property will only be eligible for taking ITC. |

| 6. |

|

The applicant submitted details of time of supply and ledger copy of M/s Sribal construction company but no document regarding details of date of eligibility of ITC, payment made, whether the ITC has been availed or not and filing of 9C has been provided. These documents and submission were required to ascertain the type of construction work, authenticity of transactions, time-period of transactions and value of ITC availed but they are not helpful to decide the quantum of ITC as its requires on-site inspection, verification of the books of accounts, contracts, measurement books, and invoices. However, on perusal of ledger of the contractor, suggests that the construction of foundation and structural supports for heavy machinery has already been done prior to date of filing application for Advance Ruling. Even the applicant himself at the time of filling application has stated that during 2023-24, the contractor has raised tax invoices for the total consideration which suggest that the construction activity has been completed in 2023.24 i.e. prior to the date of filling application. |

| 7.1 |

|

Further, as per Section 31 of the CGST Act, 2017, an invoice for supply of services needs to be issued before or after the provisions of service but not later than thirty days from the date of provision of service. |

| 7.2 |

|

Further, the time of supply of services will be earliest of the following dates: |

| • |

|

Date of issue of invoice by the supplier (if the invoice is issued within the legally prescribed period under Section 31(2) of the CGST Act) or the date of receipt of payment, whichever is earlier |

| • |

|

Date of provision of services (if the invoice is not issued within the legally prescribed period under Section 31(2) of the CGST Act) or the date of receipt of payment, whichever is earlier |

| • |

|

Date on which the recipient shows the receipt of service in his books of account, in case the aforesaid wo provisions do not apply |

|

|

The supply of goods or services shall be deemed to have been made to the extent it is covered by the invoice or by the payment, as the case may be. |

| 8. |

|

From the documents submitted by the applicant, it is found that they have received services of construction service for construction of foundation and structural supports for heavy machinery. Thus these activities have already been rendered and completed in the years 2023-24 and 2024-25. |

| 9. |

|

Section 95 of the CGST Act, 2017, defines Advance ruling as below: – |

Section 95. Definitions of Advance Ruling:-

In this Chapter, unless the context otherwise requires, –

(a)” advance ruling” means a decision provided by the Authority or the Appellate Authority'[or the National Appellate Authority] to an applicant or on questions specified in sub- section (2) of section 97 or sub-section (1) of section 100 [or of section 101C], in relation to the Supply of goods or services or both being undertaken or proposed to be undertaken by the applicant:”

|

|

As per the above definition, Advance ruling means a decision provided by the relevant authority on question to the supply of gods or services or both being under taken or proposed to be undertaken by the applicant. Hence, the activities have to be either undertaken in the present or should be proposed to be undertaken to seek a ruling. In the present case, the applicant had furnished details for the activities already done in the yester years. Hence, this authority is constrained in considering this question on merits. Therefore, no ruling is extended in respect of this question as the same is not related to the activities being undertaken or proposed to be undertaken. |

G. In view of the foregoing facts, circumstances, and provisions of GST law, we pass the following ruling: –

RULING

Q-1 Whether the Applicant is eligible to avail ITC on input services used for construction of foundation and structural support for plant and machinery installed at the factory of the Applicant for manufacture of lyophilized injectable, in terms of Section 17(5)(c) of the CGST Act, 2017?

Ans-1 As discussed in Para 9 above.