ORDER

Ms. Padmavathy S., Accountant Member. – This appeal by the assessee is against the order of the Commissioner of Income Tax (Appeals)/National Faceless Appeal Centre (NFAC), Delhi, (in short “CIT(A)”) passed u/s. 250 of the Income Tax Act, 1961 (in short “the Act”) dated 04.02.2025 for Assessment Year (AY) 2015-16.

2. The assessee is a company and is engaged in the business of microfinance. The assessee filed the return of income for AY 2015-16 on 30.09.2015 declaring total income of Rs.17,11,72,500/-. The case was selected for scrutiny and the statutory notices were duly served on the assessee. The A.O noticed that during the year under consideration the assessee has issued 75,61,126 rights shares to another NBFC Manappuram Finance Limited at a price of Rs.83.32 per share which includes the share premium of Rs.73.32 per share. The assessee has justified the share premium based on valuation using discounted cash flow method (DCF). The AO rejected the valuation and carried out independent valuation using net asset value method (NAV) to arrive at the value per share at Rs. 48/-. The A.O called on the assessee to justify the valuation and why the difference cannot be added as addition u/s. 56(2)(viib) of the Act. The assessee submitted that the valuation of shares are based on estimation of future cash flows and DCF method is as per Rule 11A of income tax Rules. The assessee further submitted that the valuation is carried out by a Chartered Accountant who has considered the future business of the assessee as accepted by the Rules. The A.O however rejected valuation report stating that the valuation of the C.A is based on the details submitted by the assessee and that the CA clearly stated that he has not conducted any audit or due diligence of the figures given by the assessee. The A.O accordingly treated the difference between the valuation done under the DCF method by the assessee and the valuation by applying NAV method as addition u/s. 56(2)(viib) of the Act amounting to Rs.27,53,76,209/-. On further appeal, the CIT(A) confirmed the disallowance.

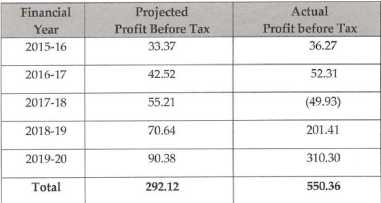

3. The Ld. Authorized Representative (AR) of the assessee submitted that the assessee has issued the shares at premium to another NBFC and both are regulated entities. The Ld. AR further submitted that the entire transaction of rights issues is approved by Reserve Bank of India. The Ld. AR also submitted that the valuation adopted by the assessee is as per Rule 11UA which is certified by the C.A. The Ld. AR argued that the only reason for rejecting the valuation by the A.O is that the C.A in the certificate has stated that the valuation is based on the details submitted by the assessee and that the CA has not carried out any due diligence. The Ld. AR further argued that the actual profits earned by the assessee for five years as compared to projection considered for the purpose of valuation is far more and therefore, the rejection of the valuation by A.O is unwarranted. The Ld. AR in this regard drew our attention to the below table containing the projection and the actual profits earned by the assessee:

4. The Ld. AR submitted that the A.O while making the addition as adopted the NAV method without bringing on record anything to support the allegation that the assessee has any undisclosed receipts towards share premium. The Ld. AR further submitted that the intention behind introduction of section 56(2)(viib) of the Act is to curtail the unaccounted money received as share premium and in assessee’s case the A.O has made the addition without establishing the fact that the assessee has indeed unaccounted money brought into business as share premium. The Ld. AR also submitted that the genuineness of the transaction is substantiated by the assessee and that the assessee has issued shares at the same price to non resident shareholders also. The Ld. AR also submitted that in assessee’s own case for AY 2016-17 Asirvad Micro Finance Ltd. v. Asstt. CIT (Chennai – Trib.)/ (ITA No.1140/Chny/2025 dated 05.12.2025) where a similar addition has been made, the Coordinate Bench has deleted the addition. The ld AR also presented written submissions elaborating the above arguments supported by various case laws and the same has been taken on record.

5. The Ld. Departmental Representative (DR), on the other hand, submitted that the valuation by C.A does not justify the premium charged and is not commensurate with the financials of the company. The Ld. DR further submitted that the assessee has submitted the valuation report dated 21.11.2017 which goes to prove that the valuation is carried out as an afterthought and is not done at the time of issue of shares at a premium. The Ld. DR also submitted that the valuation report obtained after two years of issue of shares cannot be considered as valid under Rule UA since the rule does not permit time travelling. The Ld. DR in summary submitted that as on the date of issue of shares at premium, the valuation report was not existing and therefore, the claim of the assessee that the premium is based on the valuation report under Rule 11UA cannot be accepted.

6. We have heard the parties, and perused the material available on record. The assessee during the year under consideration has issued shares at a premium of Rs. 73.32 per share using DCF method. The A.O rejected the valuation report stating that the valuation is based on the details submitted by the assessee which were unverified by the CA while issuing the valuation report. The A.O recalculated the value at Rs. 48/- per share to make an addition u/s. 56(2)(viib) of the Act to the tune of Rs. 27,53,76,209/-. The contention of the assessee is that the primary criteria for invoking section 56(2)(viib) of the Act i.e, unaccounted money being infused is not established by the A.O. The assessee further contends that the A.O is not correct in rejected the DCF method and applying NAV method without recording any adverse finding with regard to the method adopted by the assessee. The assessee is also contending that the actual profits of the assessee is far more than what is projected under DCF method and accordingly the valuation of shares is fully justified. The contention of the Revenue is that the valuation report is an afterthought which is obtained after two years of actual issue of shares and therefore cannot be accepted. Since the AO has made the addition u/s.56(2)(viib), we will look at the relevant provisions before proceeding further –

56 – Income from other sources.

(1)****

(2) In particular, and without prejudice to the generality of the provisions of subsection (1), the following incomes, shall be chargeable to income-tax under the head “Income from other sources”, namely :—

(i) to (viia) ****

(viib) where a company, not being a company in which the public are substantially interested, receives, in any previous year, from any person being a resident, any consideration for issue of shares that exceeds the face value of such shares, the aggregate consideration received for such shares as exceeds the fair market value of the shares:

Provided that this clause shall not apply where the consideration for issue of shares is received—

| (i) |

|

by a venture capital undertaking from a venture capital company or a venture capital fund; or |

| (ii) |

|

by a company from a class or classes of persons as may be notified by the Central Government in this behalf. |

Explanation.—For the purposes of this clause,—

(a) the fair market value of the shares shall be the value—

| (i) |

|

as may be determined in accordance with such method as may be prescribed10; or |

| (ii) |

|

as may be substantiated by the company to the satisfaction of the Assessing Officer, based on the value, on the date of issue of shares, of its assets, including intangible assets being goodwill, know-how, patents, copyrights, trademarks, licences, franchises or any other business or commercial rights of similar nature, whichever is higher; |

| (b) |

|

“venture capital company”, “venture capital fund” and “venture capital undertaking” shall have the meanings respectively assigned to them in clause (a), clause (b) and clause (c) of Explanation to clause (23FB) of section 10; |

7. From the plain reading of the above provision it is clear that if a closely held company receives any consideration during the year for issue shares in excess of the face value, then the excess over the fair market value will be treated as Income from Other Sources to be taxed under the Act. Before proceeding further, it is important to understand the intention of the legislature for introducing the stringent provisions of section 56(2)(viib) of the Act The Hon’ble Finance Minister in his speech of Finance Bill 2012 had stated at para 155 as follows

“I propose a series of measures to deter the generation and use of unaccounted money. To this end, I propose— ****

* Increasing the onus of proof on closely held companies for funds received from shareholders as well as taxing share premium in excess of fair market value.

* Taxing of unexplained money, credits, investments, expenditures etc., at the highest rate of 30%., irrespective of the slab of income.”

8. From the above observations of the Hon’ble Finance Minister it is clear that the intention behind introduction of section 56(2)(viib) is to discourage the generation and use of unaccounted money. The coordinate Bench of the Tribunal in the case of Vaani Estates (P.) Ltd. v. ITO (Chennai – Trib.) has made the following observations with regard to interpretation of the provisions of section 56(2)(viib) –

7.2 . **************** Thus in the case of the assessee, when the provisions of Section 56(2)(vi), (viib) & (x) of the Act, are interpreted in a harmonious manner lifting the corporate wheel of the assessee company, it is abundantly clear that the provisions of Section 56(2)(viib) of the Act, has no implication in the case of the assessee company, more-so keeping in view of the speech delivered by the Honble Finance Minister referred herein above. It is also pertinent to mention that in the instant case the benefit of infusing cash into the assessee company by way of equity share with premium by Mrs.Sasikala Raghupathy will not benefit any other shareholders inducted in the company in future because in such event the shares will have to be allotted on the basis of the intrinsic value of the shares of the assessee company otherwise at that point of time the provisions of Section 56(2)(viib) of the Act will be instantly attracted. In the present situation we are also reminded of the principles of harmonious construction explained by Crawford in Statutory Construction “Hence the Court should, when it seeks the legislative intent, construe all the constituent parts of the statute together and seek to ascertain the legislative intention from the whole Act, considering every provision thereof in the light of the general purpose and object of the Act itself and endeavouring to make every part effective, harmonise and sensible “. Further mischief rule of interpretation also propagate that where a statute has been passed to remedy a weakness in the law, the interpretation which will correct that weakness is the one to be adopted.

7.3 It should be also kept in mind that provisions of Section 56(2)(viib) of the Act creates a deeming fiction and while giving effect to such legal fictions all facts and circumstances incidental thereto and inevitable corollaries thereof have to be assumed. At this juncture we are reminded of the decision of the Hon ‘ble Kolkata High Court in the case M.D. Jindal v. CIT , wherein it was held that “legal fictions are created only for a definite purpose and they are limited to the purpose for which they are created and should not be extended beyond the legitimate field. But the legal fiction has to be carried to its logical conclusion within the framework of the purpose for which it is created.” Further it is apparent from the Finance Minister’s speech that the provisions of Section 56(2)(viib) has been enacted to deter the generation and use of unaccounted money. At this juncture we are also reminded of the decision of the Honble Apex Court in the case Allied Motors (P.) Ltd. v. CIT, wherein it was held that the Finance Minister’s Budget speech explaining the provisions are relevant in construing the provisions.************

9. Further the coordinate bench in the case of Ambattur Developers Private Ltd v. ITO (Chennai – Trib.) has considered an identical issue in the light of various judicial precedence on the impugned issue and held that section 56(2)(viib) is not applicable unless the revenue has made out a case of infusion of unaccounted money. The coordinate bench further held that the AO is not correct in rejecting the valuation report and adopting a different method for valuation without considering the actual position is not permissible. The following principles emerge from the combined perusal of the legislative intent and the various judicial precedences –

| i. |

|

Section 56(2)(viib) is an anti-abuse provision introduced to the statute to check and regulate introduction of unaccounted money through share premium. |

| ii. |

|

The bonafide nature of the transaction also needs to be considered in the light of the legislative intent |

| iii. |

|

For the harmonious interpretation of section 56(2)(viib), the corporate veil is to be lifted while testing transaction viz., between relatives, existing shareholders, holding and subsidiary companies etc. |

| iv. |

|

Once the assessee has exercised an option for valuation of an unquoted equity share, in terms of Rule 11UA either as per NAV Method or as per DCF Method, the AO is bound to follow the valuation unless the AO brings in cogent material on record to establish perversity in the method adopted by the assessee. |

10. In the light of the above legal position we will now look at the facts in assessee’s case. The AO/CIT(A) have not recorded anything doubting the genuineness of the transaction and nothing has been brought on record to establish that the assessee has brought in unaccounted money in the guise of share premium. We notice that the only reason for invoking the provisions of section 56(2)(viib) is that the C.A. has mentioned in the report the inputs are provided by the management of the assessee company. However the AO has not brought on record any record to show why the projections made using DCF method are incorrect. We further notice that the AO has recorded an incorrect finding with regard to mismatch in the profits projected for AY 2015-16 & AY 2016-17 (refer para 3.9.9 of AO’s order) by comparing the Earnings Before Interest and Tax (EBIT) with the Profit Before Tax (PBT) as declared in the return of income. We also notice the over all actual profits of the assessee far exceeds the projection under DCF method even after considering the loss made in FY 2017-18 as can be seen from the table as extracted in the earlier part of this order. It is also relevant mention here that impugned transaction of issue of shares at a premium is approved by the RBI including the rate of share premium of Rs.73.32 per share. With regard to the contention of ld DR that the valuation is obtained two years after the issue of shares at a premium, the ld AR drew our attention to the observations of the coordinate bench in the case of Sri Sakthi Textiles Ltd. v. Dy. CIT ITD 946 (Chennai – Trib.)/ (I.T.A No.1228/Chny/2019) where it is held that “When the assessee has substantiated share price to the satisfaction of the AO with the help of valuation report, even if, such valuation report is obtained subsequent to the date of issue of shares, it does not alter the situation”. In view of these discussions and considering the judicial precedence, we are of the view that with given facts discussed (supra), the addition made by the AO u/s.56(2)(viib) cannot be sustained and the AO is accordingly directed to delete the same. Ground No.2 raised by the assessee in this regard is allowed.

11. Ground No.1 & 4 are general not warranting any specific adjudication. The ld AR during the course of hearing did not press Ground No.3 raised with regard to disallowance of ESOP expenditure. Therefore the said ground is dismissed as not pressed.

12. In result the appeal of the assessee is partly allowed.