ORDER

Ramit Kochar, Accountant Member.- This appeal in BMA No.12/Del/2025 for assessment year: 2021-22 is filed by the assessee which has arisen from the appellate order passed by the learned Commissioner of Income Tax (Appeals)-3, Gurgaon The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015(In Short “2015 Act”) dated 29.05.2025 (Appeal No.10011/CIT(A)-3/GGN/2023-24) passed u/s 16 of the 2015 Act, which appeal in turn has arisen from the assessment order dated 3rd July, 2023 passed by the learned Deputy Director of Income-tax(Investigation)-1, Gurugram being the Assessing Officer u/s. 10(3) of the 2015 Act.

2. The grounds of appeal raised by the assessee in the Memo of Appeal filed with the Income Tax Appellate Tribunal, Delhi Benches, New Delhi , reads as under:-

“1. The Ld. Commissioner of Income Tax, (Appeals) – 3, (‘Ld. CIT-A’) was not justified in confirming the order of the Ld. Deputy Director of Income Tax (Investigation) – 1, (‘Ld. DDIT’) passed u/s 10(3) of the Black Money (UFIA) and Imposition of Tax Act, 2015 (‘the Act’), making an addition of Rs. 2,69,91,144 as undisclosed foreign income to the returned income of the assessee, without appreciating the facts and circumstances of the case and without appreciating the submissions and the information and documents produced during the assessment and appellate proceedings.

2. The Ld. CIT-A was not justified in confirming the order of the Ld. DDIT, passed u/s 10(3) of the Act, making an addition of Rs. 2,69,91,144 to the returned income of the assessee as undisclosed foreign income, ignoring the fact that undisclosed foreign income is assessable in the year in which it is earned, i.e. AY 2017-18 in this case, and not in the year in which it comes to the knowledge of the Assessing officer, i.e. AY 2021-22.

3. The Ld. CIT-A was not justified in confirming the order of the Ld. DDIT, passed u/s 10(3) of the Act, making an addition of Rs. 2,69,91,144 to the returned income of the assessee as undisclosed foreign income, without appreciating the fact that the income pertains to sale proceeds of house property which was situated outside India (USA) and was acquired by the assessee during his stay in USA when he was a non resident, out of his income earned abroad and loan obtained in USA and, therefore, said income does not fall under the definition of ‘undisclosed income and asset’ as per section 2(xii) of this Act and, therefore, is beyond the scope of the said Act.

4. The Ld. CIT-A was not justified in confirming the order of the Ld. DDIT passed u/s 10(3) of the Act, making an addition of Rs. 2,69,91,144 to the returned income of the assessee, without appreciating the fact that the amount pertains to sale proceeds of house property situated in USA, capital gain duly disclosed in USA tax return and the same resulted in a capital loss when computed in accordance with Income Tax Act, 1961 which was not adjustable / allowable in the income tax return filed in India.

5. The Ld. CIT-A was not justified in confirming the order of the Ld. DDIT passed u/s 10(3) of the Act, making an addition of Rs. 2,69,91,144 to the returned income of the assessee, without bringing on record any evidence in support of the allegation that the alleged investment in foreign asset is from so-called black money earned in India.

6. The Ld. CIT-A was not justified in confirming the order of the Ld. DDIT passed u/s 10(3) of the Act, making an addition of Rs. 2,69,91,144 to the returned income of the assessee, without appreciating the submissions of the appellant and without providing sufficient opportunity to the appellant of being heard in the matter and thus he has acted against the Principle of Natural Justice.

7. The appellant craves leave to add, amend, delete, modify and/or rectify any grounds of appeal.”

2.1 The assessee has also raised additional grounds of appeal before the Tribunal:-

“Ground No. 2(a)

The Ld. AO has erred in law and on facts in initiating the proceedings and serving a notice under section 10(1) of Black Money (UFIA) and Imposition of Tax Act, 2015, (“BMA”) on 11.04.2022 for AY 2021-22 w.r.t. foreign income received during Previous Year 2015-16 and 2016-17 and assessing the alleged undisclosed income received in Previous Year 201617 under section 10(3) of BMA Act for the AY 2021-22 which is against the provisions of section 3(1) of the BMA Act, which prescribes for a tax in respect of the total undisclosed foreign income and asset of the previous year at the rate of 30 percent of such undisclosed income and asset.”

“Ground No. 2(b)

The Ld. AO has erred in law and on facts in initiating the proceedings for A.Y. 2021-22 and serving a notice under section 10(1) of Black Money (UFIA) and Imposition of Tax Act, 2015, (“BMA”) on 11.04.2022 upon the appellant w.r.t. the alleged undisclosed foreign income received during Previous Year 2015-16 and 2016-17 and thus assessing the alleged undisclosed foreign income received in Previous Year 2016-17 under section 10(3) of BMA Act for the AY 2021-22. Without prejudice, the Ld. DCIT has erred in serving the said notice and assessing the undisclosed foreign income in the garb of the information received by him on 31.03.2021 prior to the jurisdiction assigned to him on 31.03.2022 that is a year before the jurisdiction was assigned to him.”

2.2 The assessee has pleaded for the admission of aforesaid additional grounds of appeal filed before the Tribunal , and has relied upon the judgment and order(s) of Hon’ble Supreme Court in the case of Chitturi Subanna v. Kudapa Subbanna AIR 1965 SC 1325 as well National Thermal Power Company Ltd. v. CIT [1998] 229 ITR 383 (SC). It is prayed by ld. Counsel for the assessee that these additional grounds of appeal raises question of law which can be raised at any stage of proceedings, and no new facts are to be investigated. The ld. CIT-DR has no serious objection to the admission of these additional grounds of appeal raised by the assessee. After hearing both the parties , we admit the aforesaid additional grounds of appeal filed by the assessee. We order accordingly.

3. The brief facts of the case are that the assessee i.e. Shri Atanu Banerji is an individual being resident of India during the previous year corresponding to the impugned assessment year 2021-22. The AO had information that the assessee has bank account bearing No.8013623334 in PNC Bank, N.J 27, Edison New Jersey, USA. On perusal of the bank statement, it was observed by the AO that the assessee has received $ 1232 per month during financial year 2015-16 and 2016-17 as Social Security amount, but the same was not declared by the assessee in the return of income filed under the provisions of the Income Tax Act,1961 as applicable in India. It was further observed by the AO that the assessee has received credits on account of sale of assets which has also not been disclosed by the assessee in the income-tax returns filed with the Department with in the provisions of Income-tax Act,1961(hereinafter called “1961 Act”) as applicable in India . The proceedings under the provisions of 2015 Act were initiated by the AO by issuing notice u/s 10(1) of the 2015 Act.

3.1 In the instant case, the Principal Director of Income-tax (Investigation), Chandigarh, vide his office order F.No. Pr. DIT/INV/CHD/2021-22 dated 31st March, 2022 assigned the concurrent jurisdiction to the Dy. Director of Incometax (Investigation)-I, Gurugram to exercise powers and perform functions of the AO under the 2015 Act.

3.2 It is stated in the assessment order that information in the case of the assessee has come to the knowledge of the AO on 31st March, 2021 , and for making the assessment relevant date under the 2015 Act is the date of receipt of information by the AO. It is observed by the AO that since the information about the undisclosed foreign asset came to the notice of the AO under the 2015 Act in Financial Year: 2020-21, it became the previous year and consequently the year 2021-22 became the assessment year.

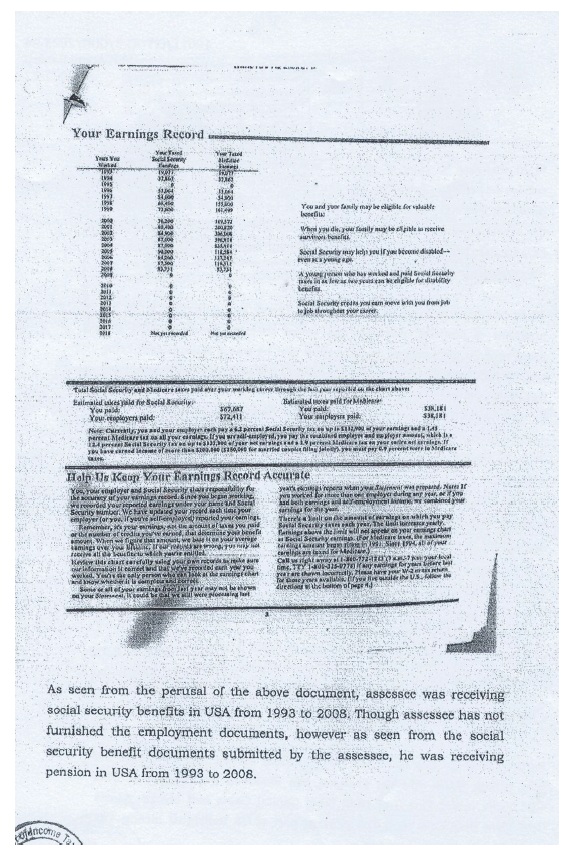

3.3 The AO initiated assessment proceedings by issuing notice dated 11.4.2022 u/s 10(1) of the 2015 Act. The AO granted another opportunity to the assessee vide notice dated 04.05.2023 seeking details of his income from abroad and sources of such income. The assessee submitted its response before the AO wherein the assessee submitted that the assessee is an American(USA) resident since 1996 to 2004 , and had done service in American companies. But from 2008 , the assessee came back to India and was residing in India for more than 182 days in a year since then, hence, his status in India was resident Indian. It was submitted by the assessee that during the financial year 2015-16 and 201617, the assessee had received social security amount of $ 1232 per month in USA which was already shown in the USA Income-tax return filed from time to time with the US Revenue authorities. It was submitted that as per India-USA DTAA-Article 20, Social Security Benefits paid by the Contracting State to the Resident of other Contracting States shall be taxable in the first contracting state i.e. in USA. It was submitted that the assessee has duly reflected social security benefits received in USA in the return of income filed in USA from time to time. This plea of the assessee was accepted by the AO , and the matter rested there itself and no additions were made towards undisclosed foreign income and assets by the AO in the assessment framed under 2015 Act. Thus, there is no dispute between rival parties so far as taxability of social security benefits received by the assessee in USA.

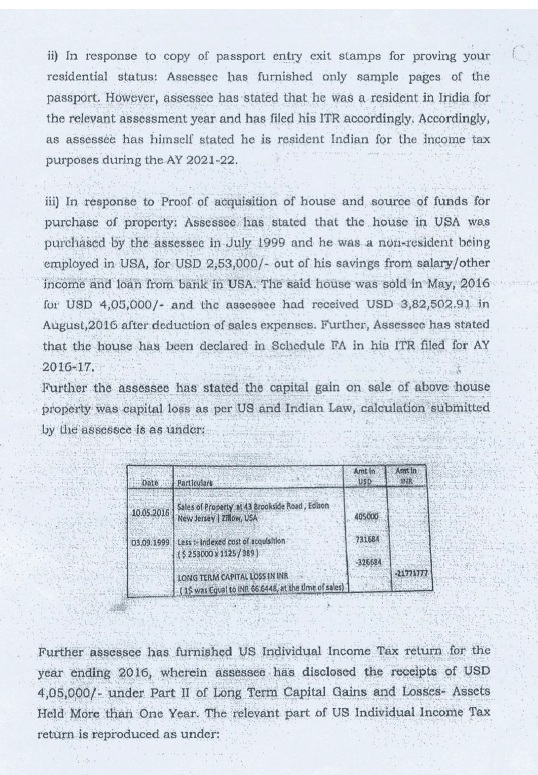

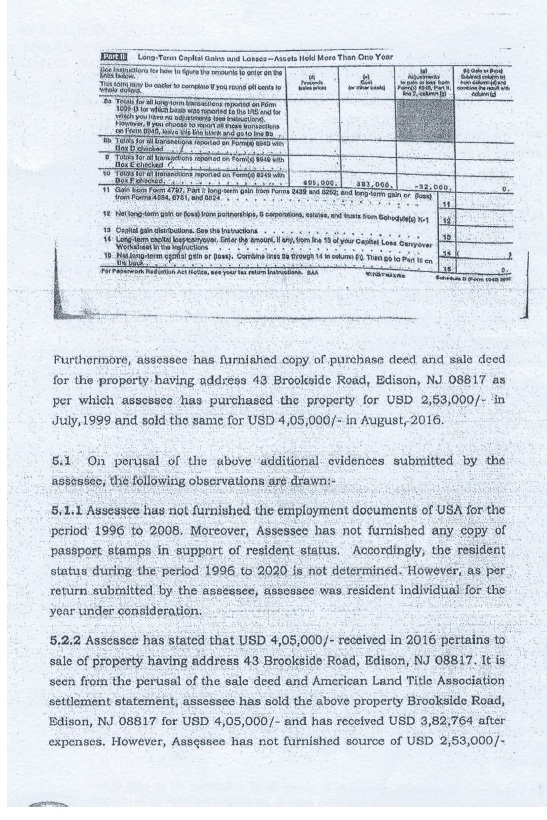

3.4 The dispute has arisen between rival parties with respect to chargeability to tax undisclosed income under 2015 Act to the tune of US$ 4,05,000/- with respect to sale of assessee’s house situated at 43, Brookside Road, Edison , NJ 08817. It was submitted by the assessee before the AO that the assessee has acquired a house situated at 43 Brookside Rd. Edison, NJ 08817 for USD 2,53,000/- on 03rd September 1999 , and the same was sold on 10th May 2016 for USD 4,05,000/- and the assessee had received towards net sale consideration after deductions to the tune of USD 3,82,502.91 on 29th August, 2016 in his PNC Bank account which was duly disclosed in the return of income filed in the USA with US tax authorities. The assessee referred to Article 13 of the India-USA DTAA. The assessee submitted that the assessee was a Resident in India during previous year 2016-17 when this property was sold , and as per the Indian Income-tax law, the said house was held for more than 36 months and after availing indexation benefits there was a long term capital loss incurred by the assessee on this transaction and consequently no income-tax was payable by the assessee in India with respect to sale of the aforesaid property. The assessee submitted before the AO , details of capital gain/loss earned on sale/transfer of the said property. It was submitted that the aforesaid house i.e the foreign assets was acquired in the year 1999 , when the assessee was in service/employment in USA from 1996 to 2004. It was further submitted that the moveable and immovable foreign assets for Financial Year 2015-16(AY:2016-17) and Financial Year:2016-17(AY:2017-18) were duly disclosed in the return of income filed with the Department.

3.5 The AO observed that the assessee is contending that the assessee has sold an immovable property in USA which was claimed by the assessee to have been declared in the return of income filed in the USA with US tax authorities, and as per the ITR filed by the assessee in the USA , the assessee purchased the aforesaid property in September, 1999 for a consideration of USD 2,53,000 and sold the property during August, 2016 for a consideration of USD 4,05,000/- . The AO observed that the assessee has further contended that the property was held for more than 36 months , and that there is a capital loss in this transaction after taking the benefit of indexation and no tax is payable in India as per the provisions of the 1961 Act. The AO issued summons to the assessee to provide the copy of sale deed of the property so that the capital gain or loss earned by the assessee could be ascertained, but the assessee did not provide copy of the sale deed to the AO . Further, the AO could not gauge from the bank statement submitted as to the nature of credits in the said bank account. Thus, in the absence of documentary evidences, the AO brought to tax the amount of USD 4,05,000/-(Rs. 2,69,91,144/-) as an unexplained credits which was added by the AO to the income of the assessee as undisclosed income under the provisions of 2015 Act.

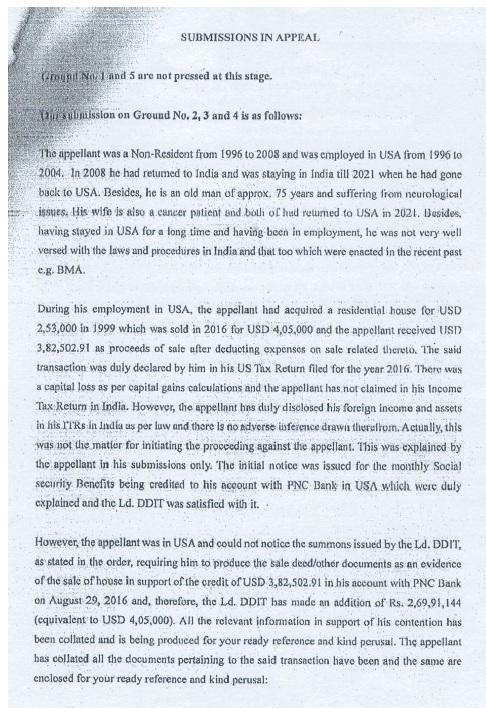

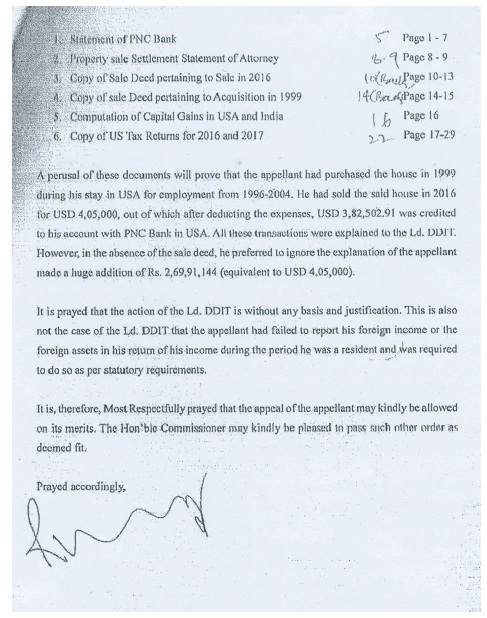

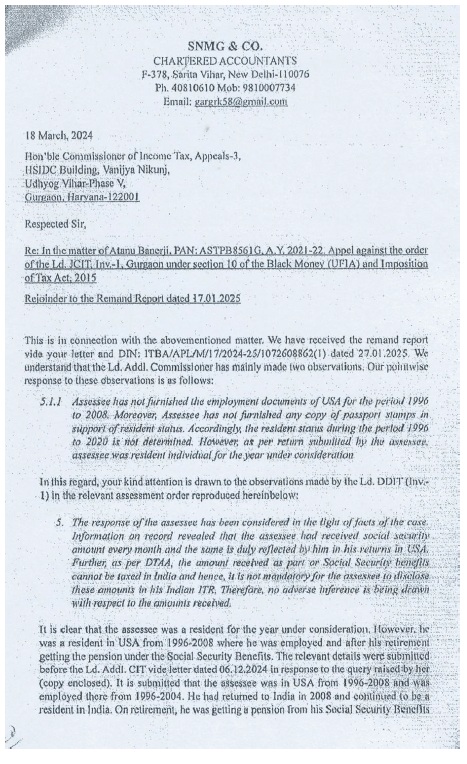

4. Aggrieved, the assessee filed first appeal before the learned CIT(A) The Black Money(Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, wherein the assessee made the following submissions:-

4.1 The Ld. CIT(A) forwarded the aforesaid submissions made by the assessee to the AO, and called for the remand report from the AO.

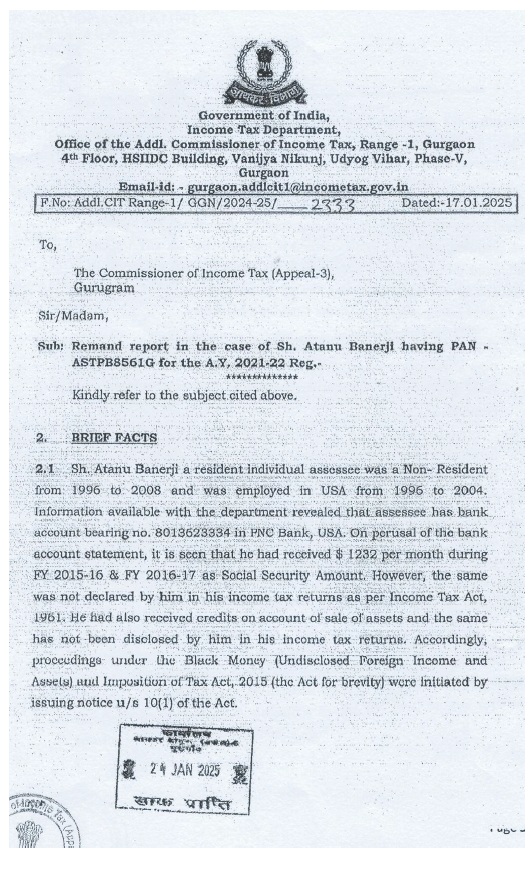

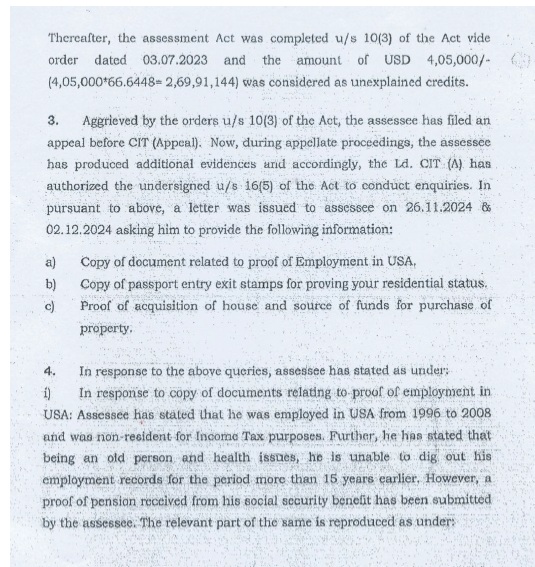

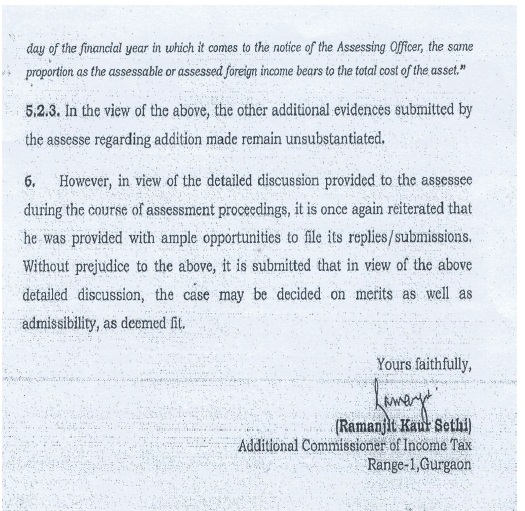

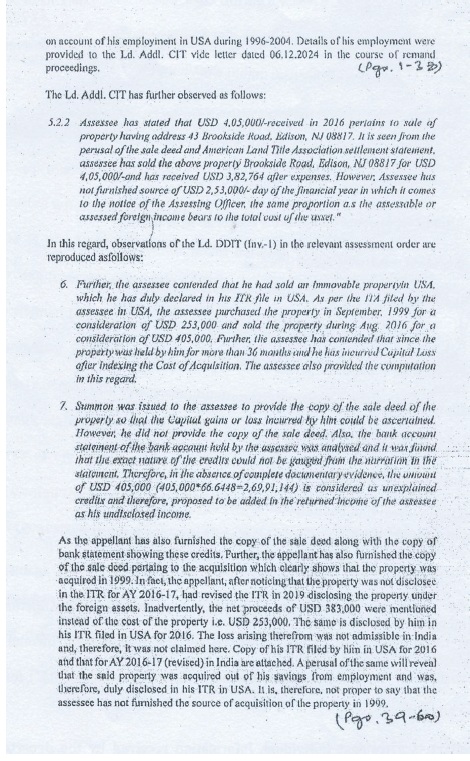

4.2 The AO submitted its remand report vide communication F.No. Addl.CIT Range-1/GGN/2024-25/2333 dated 17th January, 2025 , which is reproduced hereunder:-

4.3 The learned CIT(A) forwarded copy of the remand report to the assessee for filing rejoinder , and the assessee submitted its rejoinder as under:-

4.4 The Ld. CIT(A) observed that the assessee is a resident individual. The learned CIT(A) observed that the sources of purchase of the property situated at 43 Brookside Rd. Edison, NJ 08817, which is owned by the assessee with his spouse remained unexplained. The assessee has not disclosed the credits amounting to US$4,05,000 on account of sale of aforesaid property in the income tax returns filed with Indian tax authorities. This triggered the invocation of proceedings u/s 10(1) of the BM Act,2015. The Ld. CIT(A) observed that the assessee has disclosed the taxation on purchase/sale of property in the tax return filed in the USA with US tax authorities , but the assessee has declared the said transaction in India in the ITR for AY 2016-17 only when the same facts were detected by the Revenue Authorities. The ld. CIT(A) observed that the assessee failed to disclose foreign bank account and the proceeds from the sale of aforesaid property in the income tax return filed with the Indian tax authorities under the provisions of the Income-tax Act, 1961. There is no record available which could demonstrate that the assessee has made any declaration of the foreign income and assets under the Indian income-tax law during the relevant assessment year or for earlier assessment year. The 2015 Act imposes obligation on resident assessee to disclose foreign income and assets. The assessee claimed that there is a long term capital loss on sale of aforesaid property after taking benefit of indexation, the property being long term capital asset held for more than 36 months. The learned CIT(A) also observed that there is no evidence furnished by the assessee to show that the loss was declared or foreign asset was declared under the Indian tax law. The ld. CIT(A) observed that it could not be proved that there is no resultant taxable gain from the said transaction or whether the capital loss computed by the assessee was correct or genuine. There was no disclosure of the foreign asset by the assessee, as is mandated under the 2015 Act. Thus, the action of the AO in invoking the provisions of 2015 Act was upheld by the learned CIT(A) , and the credit of USD 4,05,000 which was not declared in the Indian income-tax return, was held to be an undisclosed foreign asset by the Ld. CIT(A), and the addition of Rs.2,69,91,144/- as was made by the AO being undisclosed foreign income under 2015 Act was sustained by ld. CIT(A).

5. Aggrieved, the assessee filed an appeal with the Tribunal , and the assessee has raised as many as seven grounds of appeal in the Memorandum of Appeal filed with the Tribunal. The assessee has also raised additional grounds of appeal as above. The grounds of appeal as well additional grounds of appeal raised by the assessee are reproduced by us in the preceding para’s of this order. The Ld. Counsel for the assessee opened arguments before the Bench. The ld. Counsel for the assessee submitted that the assessee is an individual of more than 70 years of age. It was submitted that he was Non-Resident from the year 1996 to 2008 , and was employed in the USA from the year 1996 to 2004. It was submitted that the assessee returned to India in the year 2008, and stayed in India till 2021. It was submitted that thereafter the assessee went back to USA. It was submitted by the Ld. Counsel that for the assessment year 2021-22 , the assessee was resident in India having stayed in India for more than 182 days. It was submitted that there were credits in the bank account maintained in USA with PNC bank in the FY 2015-16 and 2016-17 . The AO had issued a notice u/s 10(1) dated 11.04.2022 w.r.t. AY 2021-22 under the 2015 Act. It was submitted that the bank account statements/details were duly submitted. It was submitted that the assessee acquired property being house no. 43, Brookside Road, Edison, NJ 08817(USA) on 03.09.1999 for US$ 2,53,000, when the assessee was Non Resident. It was submitted that the assessee worked in USA in the employment of American Companies from 1996 to 2004. It was submitted that the assessee has sold property in USA in the financial year 2016-17. It was submitted that the said property was acquired in the year 1999 when the assessee was Non Resident. The property documents wrt purchase and sale of the aforesaid property were duly submitted before the authorities below. The first point of contention of the assessee is that as per Section 3 of the 2015 Act, undisclosed foreign income is to be assessed in the year in which it was earned i.e. assessment year 2017-18 and not in the assessment year 2021-22 as was done by authorities below . Thus, it was submitted that the assessment order passed by the AO and as upheld by the learned CIT(A), is bad in law. Further, it is contended by the Ld counsel for the assessee that it is stated in the assessment order that information as to foreign income and assets was received by the AO on 31st March, 2021 . The jurisdiction under provisions of 2015 Act was assigned to the AO by the learned Principal Director of Income-tax(Inv.), Chandigarh , on 31st March, 2022. . It was submitted that as per CBDT Instructions , notice has to be issued within 30 days, but the notice has been issued after a gap of more than one year and, hence, it is bad in law.Further, the learned counsel for the assessee relied upon the guidelines dated 23.01.2018 for handling cases under the 2015 Act, and submitted that the date of assigning of the jurisdiction shall be the date of receipt of information by the AO and, which in the instant case is 31st March, 2022 , and the correct assessment year under the circumstances under the 2015 Act ought to be assessment year 2022-23. It was submitted that the AO erred in framing assessment for the assessment year 202122. Therefore, the assessment framed by AO is bad in law. It was further submitted that as per the instruction dated 23.01.2018 issued by the CBDT, before passing assessment order, the learned AO is under an obligation to issue a Show Cause Notice(SCN) to the appellate , which he failed to do so and, hence, the assessment is bad in law. It is further submitted that the AO has to seek approval from the Addl./Jt. CIT, (Inv.) , and then assessment order has to be issued within seven days from the date of the approval i.e., from 14.06.2023 , while the assessment order has been passed on 03.07.2023 i.e. after a gap of 19 days of the approval and, hence, the said order is bad in law. It was further submitted that the proceedings under 2015 Act were also initiated and concluded for the AY 2019-20 on the similar issues and all the notices issued in AY 201920 was duly complied with. It was submitted that no adverse inference was drawn by the AO and the assessment under 2015 Act was computed at ‘NIL’ income . Thus, it was submitted that the AO cannot frame assessment on piecemeal basis so much so one income earned in FY 2016-17 is assessed in AY 2019-20, and another income earned in the same financial year shall be assessed in AY 2021-22, and, hence, the assessment order passed for AY 2021-22 is bad in law. It is further the contention of the assessee that the assessee availed a mortgage loan on the said property. It was submitted that the said residential property was purchased in the year 1999 when the assessee was Non Resident working/employed in USA. The said property was disposed of in the year 2016 relevant to assessment year 2017-18 when the assessee was resident in India. It was also submitted that the matter is more than 20 years old and the assessee is facing difficulty in getting details regarding his employment during that period. It was also submitted by ld. Counsel for the assessee that in any case, there is long term capital loss on the sale of aforesaid property after taking into account indexation , and hence there is no liability to pay income-tax. It was submitted that in view of losses no income has escaped assessment. Thus, in nutshell, it was submitted by the Ld. counsel that no addition be sustained and prayers were made to delete the additions. In the alternative, ld. Counsel for the assessee submitted that one more opportunity be granted to the assessee and the matter may be set aside, and the assessee shall submit all the necessary documents before the authorities below.

5.1 The Ld. CIT-DR, on the other hand, submitted that the authorities below have rightly made the addition and the information came to the notice of the AO on 31st March, 2021 and, hence, the correct assessment year is AY 2021-22 which has rightly been invoked by the AO as per the provisions of the 2015 Act. The jurisdiction was assigned to AO for framing of the assessment on 31st March, 2022, and on 11th April, 2022 the AO issued notice to the assessee u/s 10(1) of the 2015 Act which is within 30 days . The ld.CIT-DR relied upon the orders of the authorities below.The Ld. CIT-DR submitted that proper opportunity of hearing was duly given by the AO to the assessee. The ld. CIT-DR relied upon the provisions of Section 6 of the 2015 Act, and in particular Section 6(2) and 6(3) of the 2015 Act. It was submitted that it is only when the jurisdiction was assigned in favour of ld. DDIT(Inv.) on 31.03.2022, then only he could have issued notice u/s 10(1) of the BM Act.The ld. CIT-DR prayed to uphold the additions as were made by the AO and sustained by ld. CIT(A) 2015 Act.

5.2 In rejoinder, the Ld. Counsel for the assessee submitted that information came to the notice of the AO on 31.03.2021. Notice u/s 10(1) of the 2015 Act was issued on 11.04.2022. There is violation of CBDT instructions dated 23.01.2018. The date of assignment of jurisdiction i.e. 31.03.2022 shall be deemed to be the date of receipt of information by the AO. The assessment ought to have been framed for assessment year 2022-23, but the Revenue framed assessment for ay: 2021-22 , which is bad in law. It was submitted that AO has not issued show cause notice and no draft assessment order was framed and, hence the whole assessment is bad in law. It was further submitted by Ld. counsel for the assessee that all documents were furnished before the CIT(A) , and no adverse inference was drawn with regard to the sale/purchase of the said property. The property was purchased in the year 1999 when the assessee was Non Resident and employed in the USA. It was submitted that the assessee has not produced certain documents before the learned CIT(A) such as employment details, evidences relating to the residential status of the assessee when the property was acquired, evidences relating to sources of funds for purchasing the aforesaid property in the year 1999 , as it is an old matter and the assessee being an aged person could not locate the documents concerning his employment and other relevant documents, old bank statements, sources for acquiring the property etc. It was submitted that in any case there is a long term capital loss in the sale of the aforesaid property after taking into account benefit of indexation as the property was held for more than 36 months, there is no revenue loss to the Department, and no income has escaped the assessment. It was further submitted that the assessee has purchased the property in the year 1999 out of his savings/earnings while he was working in USA as well as the loan was taken for purchase of the aforesaid property for which mortgage documents were submitted before the Ld.CIT(A). Further, it was submitted that the sale of property took place in September, 2016, and hence the AO ought to have assessed income for assessment year 2017-18 when the income was earned, and not for the assessment year 2021-22 as was done by authorities below.

6. We have considered rival contentions and perused the material on record . Before proceeding further, it will be relevant to consider in brief the background, and objective of The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015.

6.1 Briefly stating, It is stated in the statement of objects and reasons to the 2015 Act that stashing away of black money abroad by some people with intent to evade taxes has been a matter of deep concern to the nation. ‘Black Money’ is a common expression used in reference to tax-evaded income. Evasion of tax robs the nation of critical resources necessary to undertake programs for social inclusion and economic development. It also puts a disproportionate burden on the honest taxpayers as they have to bear the brunt of higher taxes to make up for the revenue leakages caused by the evasion. The money stashed away abroad by evading tax could also be used in ways which could threaten the national security.

6.2 It is also stated that the Central Government is strongly committed to the task of tracking down and bringing back undisclosed foreign assets and income which legitimately belong to the nation. Thus, this new legislation i.e. 2015 Act deals with undisclosed assets and income stashed away abroad.

6.3 It also recognizes that Hon’ble Supreme Court of India has also expressed concern over this issue. The SIT constituted by the Central Government to implement the decision of the Supreme Court has also expressed the views that measures may be taken to curb the menace of black money . Internationally a new regime for automatic exchange of financial information is fast taking shape, and India is a leading force in this effort.

6.4 The 2015 Act has provided for stringent measures to enable taxation of undisclosed foreign income and assets, and to punish by way of stringent penalties as well prosecution of the persons indulging in illegitimate means of generating money causing loss to the revenue. It also recognizes that the 2015 Act will also prevent such illegitimate income and assets kept outside the country from being utilized in ways which are detrimental to India’s social , economic and strategic interests and its national security.

6.5 Coming back to the facts of the instant case, Briefly stated the assessee is an individual . The assessee has admitted to be Resident in India during impugned assessment year:2021-22. The assessee has claimed that he was employed in USA from 1996 to 2004. It is claimed by the assessee that he was Non Resident from 1996 to 2008. It is further claimed that he returned to India in 2008 , and stayed in India thereafter till 2021. It is claimed by the assessee that in the year 2021 , he returned back to USA and is now staying in USA. The assessee has not filed conclusive and direct evidences such as copies of passport etc. to support its contention that the assessee was Non Resident during 1996 to 2008. The assessee has also not filed evidences relating to his employment while in USA. The assessee has claimed that he is old person of age more than 70 years, and the matter being old, the assessee could not file these details/evidences. The assessee has claimed that he received social security in USA from 1993 to 2008, and the details were furnished as to the amount received in USA from Social Security during 1993 to 2008.

6.6 The AO has received information on 31.03.2021 that the assessee has bank account bearing no. 8013623334 in PNC Bank, N J 27, Edison New Jersey , USA. The said bank account was not disclosed with the Indian Income tax authorities in the return of income filed in India, prior to its detection by the Indian Tax authorities. On perusal of the bank account, the AO observed that the assessee has received US$1232 per month during financial year 2015-16 and 2016-17 as Social Security Amount.It was not disclosed in the return of income filed with Indian tax authorities. The same was however disclosed by the assessee in the return of income filed with US Revenue Authorities. Keeping in view Article 20 of India-USA DTAA, the AO accepted the contentions of the assessee and the said amount of social security received by the assessee was accepted by the AO, and no adverse inference was drawn by the AO. Thus, the matter rested there itself and no additions were made by the AO towards undisclosed foreign income so far as social security is concerned.

6.7 Further, it was observed by the AO that there are credits in the bank account on account of sale of assets , and the said credits were also not disclosed in the return of income filed by the assessee. The aforesaid information came to the notice of AO on 31.03.2021. The concurrent power and jurisdiction to perform functions of the AO under BM Act, 2015 was assigned in favour of ld. DDIT(Inv.)-I, Gurugram by ld. Principal Director of Income Tax(Inv.), Chandigarh vide orders dated 31.03.2022. The AO issued notice u/s 10(1) of the BM Act, 2015 to the assessee on 11.04.2022. The assessee submitted that the amount of US $ 3,82,502.91 was received and credited on 29.08.2016 in his PNC Bank after deductions , towards sale of his house situated at 43, Brookside Rd., Edison, NJ 08817. The gross consideration for sale was US $ 4,05,000 and the amount received after deductions was US $ 3,82,502.91. It is claimed that the said house was purchased on 03.09.1999 for US $ 2,53,000/- . The sale and purchase transactions were claimed to be duly disclosed in the return of income filed with US Revenue authorities in the year when the sale of the said house took place i.e. 2016. The said transactions were not disclosed in the return of income filed with Indian Tax Authorities. The assessee filed copies of sale and purchase deed during appellate proceedings before ld. CIT(A). It was claimed that the said house was purchased in the year 1999 when the assessee was employed in USA. It is claimed that the assessee has availed mortgage loan for acquiring the said house and also the assessee has invested his savings and/or income from employment in USA for purchasing the said house. However, As per the authorities below, the assessee could not explain the sources of making investments in the said house property .The assessee has claimed that the matter being old the assessee could not obtain the contemporaneous evidences to explain the sources for making payments for purchase of property, but it is prayed that one more opportunity be granted to assessee to produce these evidences.

6.8We have already seen the purpose and purport of 2015 Act being a Special Act enacted to deal with the menace of black money stashed abroad, and to bring to tax undisclosed foreign assets and income. Stringent penalties and prosecution provisions are incorporated in the Act to deal with menace of black money stashed abroad. The 2015 Act is applicable to residents within the meaning of Section 6 of the Income-tax Act, 1961(hereinafter called 1961 Act) as well to Non-resident or not ordinarily residents in India within meaning of clause (6) of Section 6 of the 1961 Act in the previous year, who were resident in India either in the previous year to which the income referred to in section 4 of 2015 Act relates ; or in the previous year in which the undisclosed asset located outside was acquired : provided that the previous year, in case of acquisition of undisclosed asset outside India , shall be determined without giving effect to the provisions of clause(c) of section 72.

6.9 The assessee has stated that the assessee is resident in the impugned assessment year. Thus, the assessee is covered by the provisions of the 2015 Act. The information of the undisclosed foreign income and asset came to the knowledge of the AO on 31.03.2021. The concurrent jurisdiction and powers to act as AO was conferred by ld. Principal Director of Income-tax(Inv.), Chandigarh in favour of ld. DDIT(Inv.)-I, Gurugram vide orders dated 31.03.2022. The notice u/s 10(1) of the 2015 Act was issued on 11.04.2022. The asset being House No. 43, Brookside Rd., Edison, NJ 08817 came to the knowledge of the AO on 31.03.2021. As per deeming fiction created by clause (c) of Section 72 where any asset has been acquired or made prior to commencement of the 2015 Act, and no declaration in respect of the such asset is made under Chapter VI of 2015 Act, such asset shall be deemed to have been acquired or made in the year in which a notice under section 10 is issued by the Assessing Officer and the provisions of the 2015 Act shall apply accordingly. The 2015 Act has come into force on 01.07.2015. As per charging Section 3 of the 2015 Act, the undisclosed asset located outside India shall be charged to tax on its value in the previous year in which such asset comes to the notice of the AO. The assessee being resident during assessment year 2016-17 has not made any declaration under Chapter VI of 2015 Act of the undisclosed foreign income and asset. The assessee has claimed to have disclosed the aforesaid foreign asset in the Schedule FA filed for assessment year 2016-17. Moreover, disclosure in Schedule FA itself is not sufficient , and the assessee being resident is required to substantiate that the asset has not been acquired from the amount which are chargeable or assessable to income-tax in India at the relevant times , or if it is so chargeable or assessable to income-tax in India during the relevant time, the same has been duly offered to tax and due taxes paid in India. Similar is the situation for repayment of mortgage loan.

6.10 It is also observed by the authorities below that it is only after detection by the Revenue that the assessee came forward and disclosed the said foreign income and assets. The assessee has not disclosed capital gain/loss arisen on sale of the said house in the return of income filed for assessment year 2017-18(the said house being sold in August , 2016). It is only after detection by the tax authorities in India, the assessee being resident came forward and declared the transactions related to sale of the said property and consequential capital gain/loss on the transfer of said property in return of income filed with Indian tax authorities. The assessee has claimed that the said asset being held for more than 36 months and is long term capital asset, there was long term capital loss incurred by the assessee after availing the benefit of indexation under the 1961 Act, and hence the same cannot be brought to tax under 2015 Act. The argument is fallacious , and rather it is against the mandate of the 2015 Act . It was incumbent on the assessee being resident in India during the impugned assessment year to have explained the sources of acquisition of the said house property as also sources of repayment of mortgage loans, otherwise consequences will follow. The 2015 Act is enacted to deal with the menace of stashing away of black money abroad in the form of undisclosed foreign income and assets which is causing wreck to economic fabric of the nation , and to bring to tax , penalties and prosecution w.r.t. undisclosed foreign income and assets. Reference is drawn to provisions of Section 2(11) which stipulates that “undisclosed asset located outside India” means an asset(including financial interest in any entity) located outside India, held by the assessee in his name or in respect of which he is a beneficial owner, and he has no explanation about the source of investment in which asset or the explanation given by him is in the opinion of the AO unsatisfactory. Similarly, “undisclosed foreign income and asset” means the total amount of undisclosed income of an assessee from a source located outside India and the value of an undisclosed asset located outside India, referred to in Section 4 of the 2015 Act, and computed in the manner laid down in Section 5 of the 2015 Act.Section 3 is a charging section which stipulates that there shall be charged on every assessee for every assessment year commencing on or after the 1st day of April, 2016, subject to the provisions of the 2015 Act , a tax in respect of his total undisclosed foreign income and asset of the previous year at the rate of thirty percent of such undisclosed income and asset. Provided that an undisclosed asset located outside India shall be charged to tax on its value in the previous year in which such asset comes to the notice of the Assessing Officer. Even undisclosed foreign bank account (even if it is closed prior to enactment of 2015 Act) is an undisclosed asset within the four corner of the 2015 Act. Further, it stipulates that “value of an undisclosed asset” means the fair market value of an asset (including financial interest in any entity) determined in such manner as may be prescribed. Section 4 of the 2015 Act , provide for scope of total undisclosed foreign income and asset which stipulates that the subject to provisions of the 2015 Act, the total undisclosed foreign income and asset of any previous year of an assessee shall be the income from a source located outside India , which has not been disclosed in the return of income furnished within the time specified in Explanation 2 to sub-section (1) or under sub-section (4) or sub-section (5) of Section 139 of the Income-tax Act ; the income from a source located outside India, in respect of which a return is required to be furnished u/s 139 of the 1961 Act but no return of income has been furnished within the time specified in Explanation 2 to sub-section (1) or under sub-section (4) or sub-section (5) of Section 139 ; and the value of an undisclosed asset located outside India. There is no time barring period stipulated under 2015 Act for initiating assessment or reassessment proceedings to bring to tax undisclosed foreign income and assets. As per Section 10(1) of the 2015 Act, for the purpose of making assessment or reassessment under 2015 Act, the AO may, on receipt of an information from an income-tax authority under the 1961 Act or any other authority under any law for the time being in force or on coming of any information to his notice, serve on any person, a notice requiring him to on a date to be specified to produce or cause to be produced such accounts or documents or evidence as the AO may require for the purpose of the 2015 Act and may, from time to time , serve further notices requiring the production of such other accounts or documents or evidences as he may require. No order of assessment or reassessment shall be made u/s 10 after the expiry of 2 years from the end of the financial year in which notice u/s 10(1) was issued by the AO. In the instant case notice u/s 10(1) was issued on 11.04.2022, while assessment was framed u/s 10(3) on 03.07.2023, which is within the time stipulated under the statute. There is no time limit stipulated under the 2015 Act for issuance of notice u/s 10(1) of the BM Act, 2015 after coming to knowledge of the AO of the undisclosed foreign income and asset , but time limit is stipulated for completion of the assessment or re-assessment. It is further observed that vide Section 6(1) of the 2015 Act, the income-tax authorities specified in Section 116 of the 1961 Act shall be the tax authorities for the purposes of the 2015 Act. It is provided in Section 6(2) of 2015 Act that every such authority shall exercise the powers and perform the functions of a tax authority under the 2015 Act in respect of any person within his jurisdiction. It is further stipulated vide Section 6(3) of 2015 Act that subject to the provisions of Section 6(4) of 2015 Act, the jurisdiction of a tax authority under the 2015 Act shall be the same as has been under the 1961 Act by virtue of orders or directions issued u/s 120 of the 1961 Act (including orders or directions assigning the concurrent jurisdiction) or under any other provision of the 1961 Act. It is further stipulated vide Section 6(4) of the 2015 Act that the tax authority having jurisdiction in relation to an assessee who has no income assessable to incometax under the 1961 Act shall be the tax authority having jurisdiction in respect of the area in which the assessee resides or carries in its business or has its principal place of business. The information in the instant case as to foreign income and asset came to knowledge of the AO on 31.03.2021, while the concurrent jurisdiction to act as AO under 2015 Act was assigned on 31.03.2022. The notice u/s 10(1) was issued on 11.04.2022. The assessment has been framed for assessment year 2021-22. No time limit has been provided for issuance of notice u/s 10(1) of 2015 Act. The notice u/s 10(1) was issued on 11.04.2022 i.e. within 12 days of assigning of concurrent jurisdiction on 31.03.2022. The assessment has been framed by the AO on 03.07.2023 i.e. within the statutory time as provided under 2015 Act i.e. within 2 years from the end of the financial year on which notice u/s 10(1) was issued by the AO(Section 11(1) of 2015 Act). Reference is also drawn to Explanation 2 to Section 11 which stipulates that where, by an order referred to in Section 11(3) , any undisclosed foreign income and asset is excluded from the total undisclosed foreign income and asset for any assessment year in respect of an assessee, then , an assessment of such undisclosed foreign income and asset for another assessment year shall, for the purposes of Section 10 and Section 11 , be deemed to be on made in consequence of, or to give effect to, any finding or directions contained in the said order. Section 11(3) refers to the assessment or reassessment made in consequence , or to give effect to any finding or direction contained in an order u/s 15 or Section 18 or Section 19 or Section 22 of 2015 Act or in an order of any court in a proceeding otherwise than by way of appeal under the 2015 Act. It further stipulates that such order shall be passed within 2 years from the end of the financial year in which such order is received by the ld. PCIT or ld. CIT. Further, there is no time limit for initiation of assessment or reassessment proceedings under 2015 Act, and no time limit is stipulated for issuance of notice u/s 10(1). The proceedings have to be initiated for assessment year corresponding to the previous year in which information related to foreign income and asset has come to the knowledge of the AO. The assessment or reassessment is to be framed within 2 years from the end of the financial year in which the notice u/s 10(1) is issued by the AO .

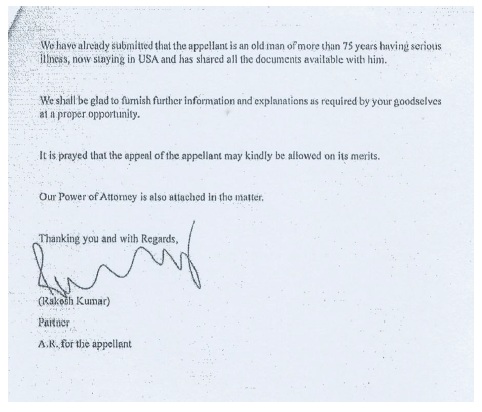

6.11 As per authorities below, the assessee could not produce evidences to support its contention viz. status as Non-Resident when the aforesaid house is stated to be acquired in 1999,evidences relatable to his employment in USA during 1993-2004, evidences related to sources of making investments in the aforesaid house acquired in 1999, but only statement is made that he was working in USA from 1993 to 2004 , and social security details for the period from 1993 to 2007 are submitted. The evidences presently submitted do not conclusively support the contentions of the assessee more so keeping in view stringent provisions and mandate of statute viz. 2015 Act. It is also claimed in written synopsis that the assessee filed certain documents viz. copy of mortgage documents and the copy of the passport, which was filed before ld. CIT(A) vide letter dated 21.04.2025 on 24.04.2025 which was filed after the conclusion of remand report proceedings by the AO but the same were not considered by ld. CIT(A). The assessee has chosen not to file such aforesaid evidences before the Tribunal. It is also contended by the assessee before the Tribunal that he is of old age and matter being very old, and that if some more time is granted to the assessee and accordingly if one more opportunity is provided to the assessee , then the assessee will get all the relevant documents to support his contentions. However, it is observed that the assessee has stated that he is more than 70 years of age suffering from disease and matter being old and the statute being new albeit stringent, assessee has contended one more opportunity be provided to produce the relevant evidences/documents.

6.12 Thus, keeping in view of the peculiar facts and circumstances of the case as narrated in preceding para’s of this order , fairness to both the parties and in the interest of justice, we are of the considered view that one more opportunity is required to be provided to the assessee to furnish details/conclusive evidences/explanations w.r.t. sources of making investment in the aforesaid foreign assets, sources of making repayments of mortgage loans and also to prove its residential status during the previous years in which the payment for acquisition of the said property or repayments of mortgage loans were made. Thus, the matter is restored back to the file of ld. CIT(A) for fresh adjudication on merits in accordance with law after giving proper opportunity of being heard to the assessee. We clarified that we have not commented on the merits of the issue both legal and factual , and all the contentions are kept open. The ld. CIT(A) shall denovo adjudicate the appeal un-hindered by our observations in this order. The assessee has also raised legal challenges to assessment framed on procedural grounds before us for the first time challenging the legality and validity of the assessment framed by the AO by , inter-alia, referring to internal guidelines issued by CBDT vide F.No. 414/134/2015-IT(Inv.I)(Pt.) dated 23.01.2018. These requires investigation of facts. Further, it is observed that these guidelines are for internal use of the departmental office and are stated to be ‘Confidential/strictly for department use’. Further, these guidelines are not in public domain. However, we allow the assessee to raise all such legal grounds and contentions before ld. CIT(A) in donovo proceedings for adjudication. Thus, appeal of the assessee is allowed for statistical purposes. We order accordingly.

7. In the result, the appeal of the assessee is allowed for statistical purposes in the manner indicated above