Directorate of Income Tax (Systems)

Annual Information Statement (AIS)

Handbook

Version 4.1.0 (February 2026)

Annual Information Statement (AIS) – Handbook

Version 4.1.0 (February 2026)

Document Version Control

Contents

1. About this Document ……………………………………………………………………………………………… 5

2. Background…………………………………………………………………………………………………………… 5

3. Annual Information Statement Overview …………………………………………………………………….. 6

3.1 Objectives ……………………………………………………………………………………………………… 6

3.2 AIS Features …………………………………………………………………………………………………… 6

3.3 AIS Preparation ……………………………………………………………………………………………….. 7

3.4 AIS Feedback ………………………………………………………………………………………………….. 7

3.5 AIS Feedback Processing……………………………………………………………………………………. 7

3.6 Key Terms ……………………………………………………………………………………………………… 9

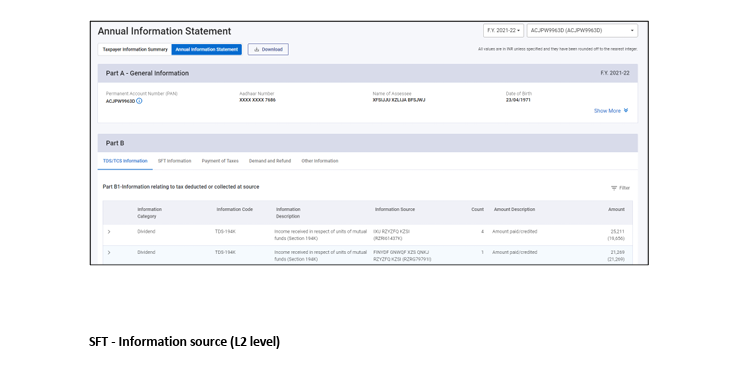

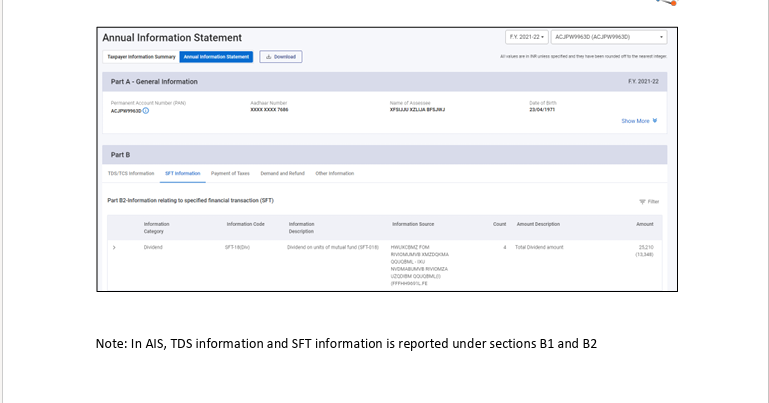

3.7 Illustrations ………………………………………………………………………………………………….. 10

4. AIS Information Category ……………………………………………………………………………………….. 17

4.1 Salary ………………………………………………………………………………………………………….. 19

4.2 Rent received ……………………………………………………………………………………………….. 20

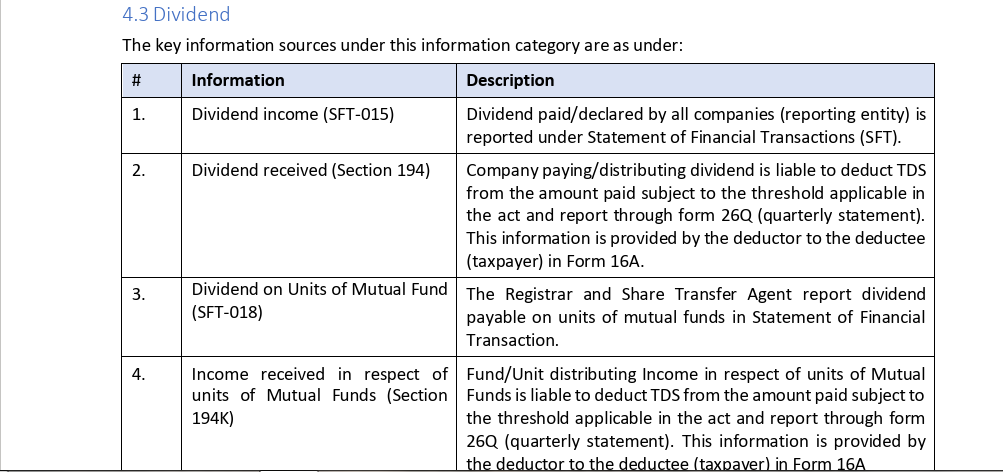

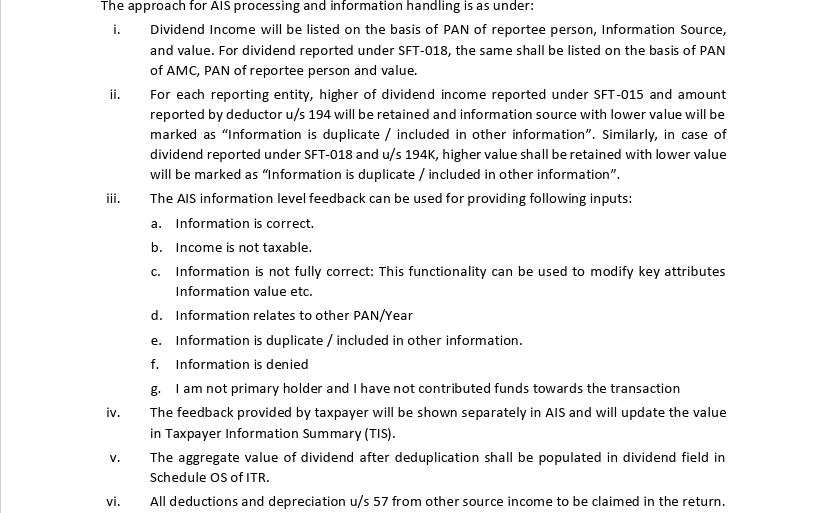

4.3 Dividend ………………………………………………………………………………………………………. 21

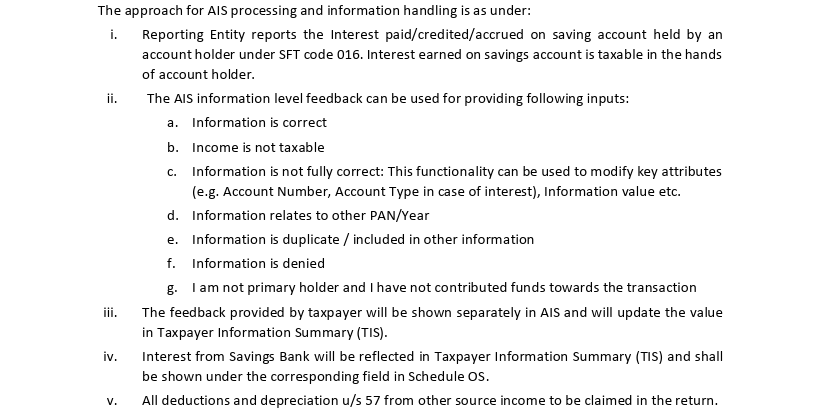

4.4 Interest from savings bank ………………………………………………………………………………. 22

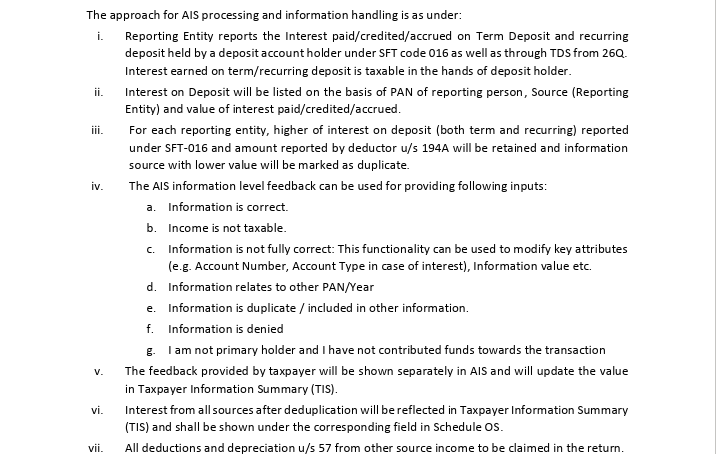

4.5 Interest from deposit ……………………………………………………………………………………… 23

4.6 Interest from others ……………………………………………………………………………………….. 24

4.7 Interest from income tax refund ……………………………………………………………………….. 25

4.8 Rent on plant & machinery ………………………………………………………………………………. 26

4.9 Winnings from lottery or crossword puzzle u/s 115BB……………………………………………. 27

4.10 Winnings from horse race u/s 115BB …………………………………………………………………. 28

4.11 Receipt of accumulated balance of PF from employer u/s 111 …………………………………. 29

4.12 Interest from infrastructure debt fund u/s 115A(1)(a)(iia) ………………………………………. 30

4.13 Interest from specified company by a non-resident u/s 115A(1)(a)(iiaa) …………………….. 31

4.14 Interest on bonds and government securities ………………………………………………………. 32

4.15 Income in respect of units of non-resident u/s 115A(1)(a)(iiab)………………………………… 33

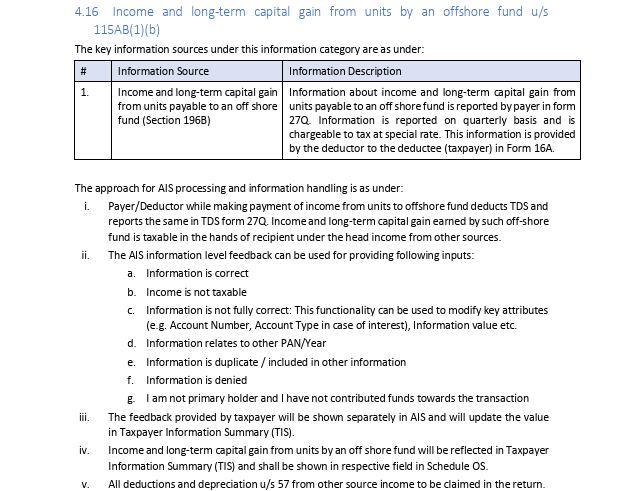

4.16 Income and long-term capital gain from units by an offshore fund u/s 115AB(1)(b) ……… 34

4.17 Income and long-term capital gain from foreign currency bonds or shares of Indian

companies u/s 115AC ……………………………………………………………………………………………….. 35

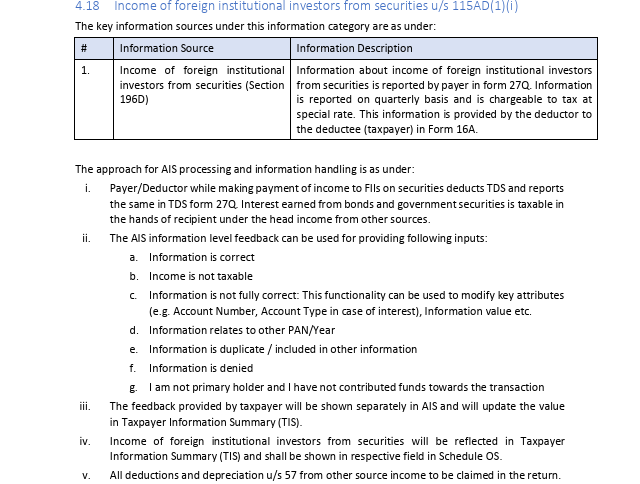

4.18 Income of foreign institutional investors from securities u/s 115AD(1)(i)……………………. 36

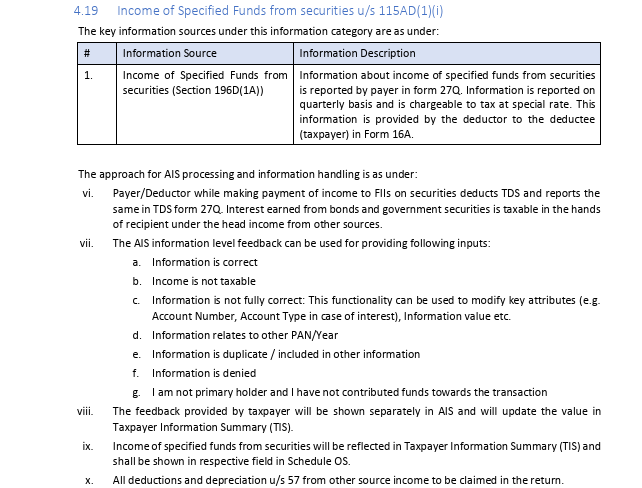

4.19 Income of Specified Funds from securities u/s 115AD(1)(i) ……………………………………… 37

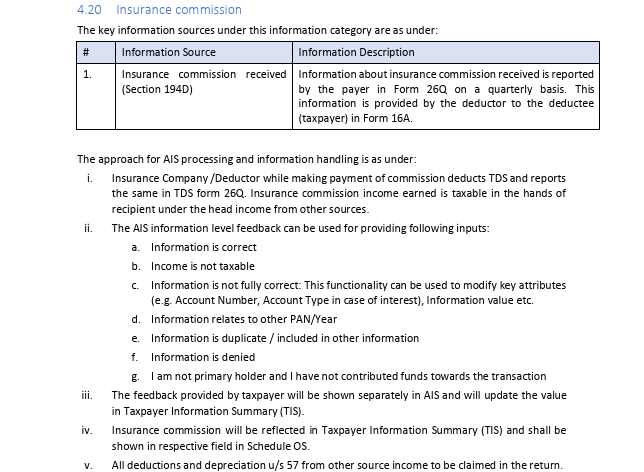

4.20 Insurance commission …………………………………………………………………………………….. 38

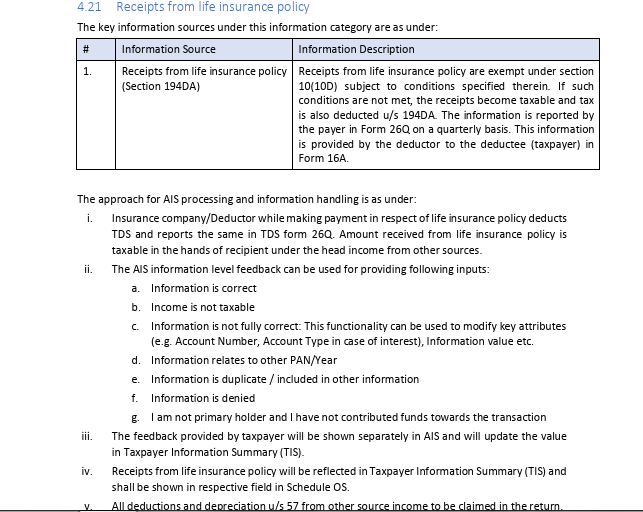

4.21 Receipts from life insurance policy …………………………………………………………………….. 39

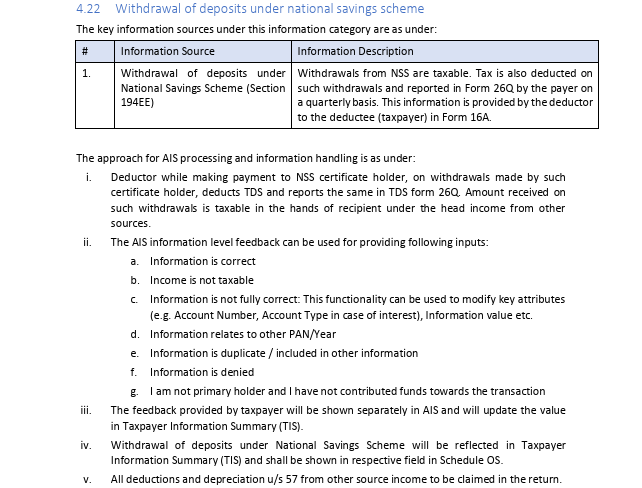

4.22 Withdrawal of deposits under national savings scheme………………………………………….. 40

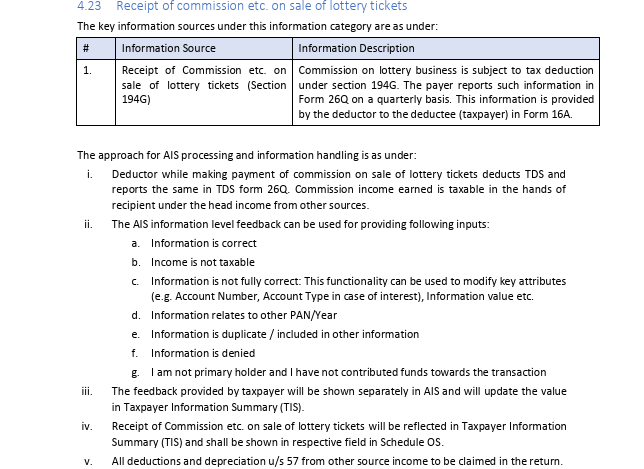

4.23 Receipt of commission etc. on sale of lottery tickets ……………………………………………… 41

4.24 Income from investment in securitization trust …………………………………………………….. 42

4.25 Income on account of repurchase of units by MF/UTI ……………………………………………. 43

4.26 Interest or dividend or other sums payable to government …………………………………….. 44

4.27 Payment to non-resident sportsmen or sports association u/s 115BBA ……………………… 45

4.28 Income of specified senior citizen ……………………………………………………………………… 46

4.29 Sale of land or building ……………………………………………………………………………………. 47

4.30 Receipts from transfer of immovable property …………………………………………………….. 49

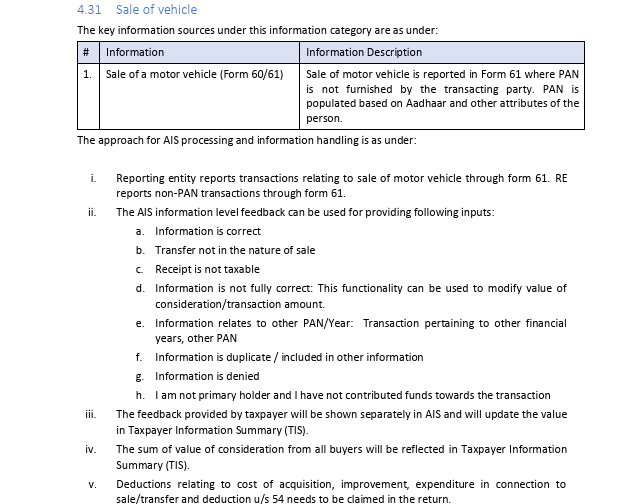

4.31 Sale of vehicle……………………………………………………………………………………………….. 50

4.32 Sale of securities and units of mutual fund ………………………………………………………….. 51

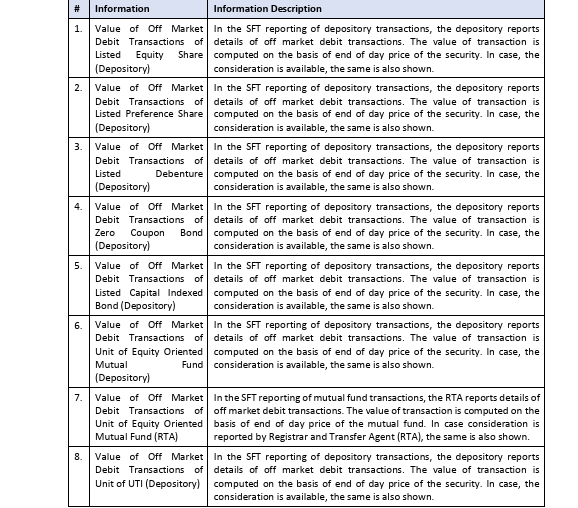

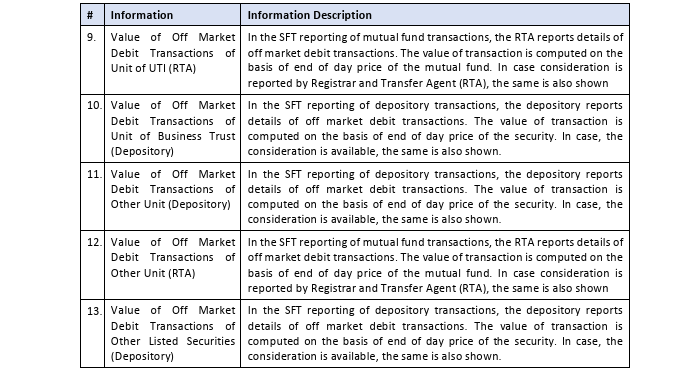

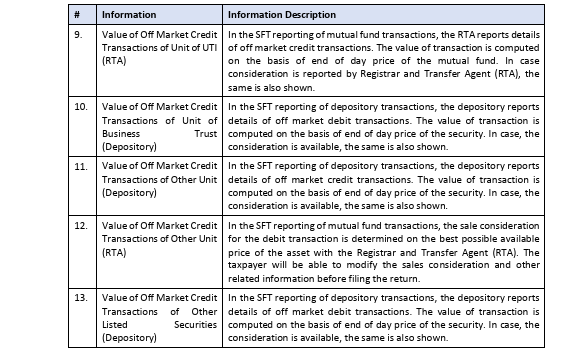

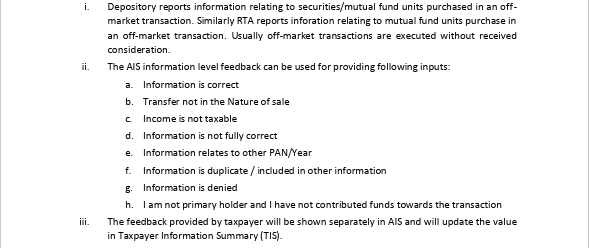

4.33 Off market debit transactions …………………………………………………………………………… 56

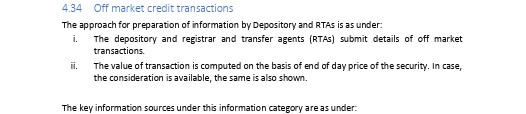

4.34 Off market credit transactions ………………………………………………………………………….. 58

4.35 Business receipts …………………………………………………………………………………………… 60

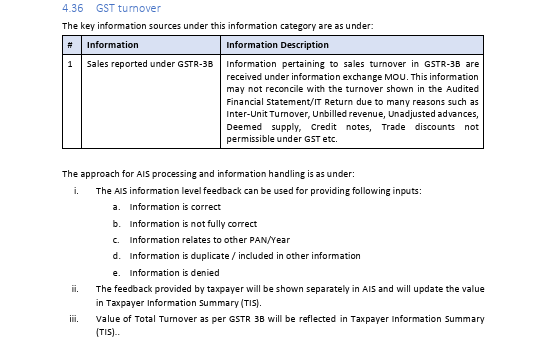

4.36 GST turnover ………………………………………………………………………………………………… 62

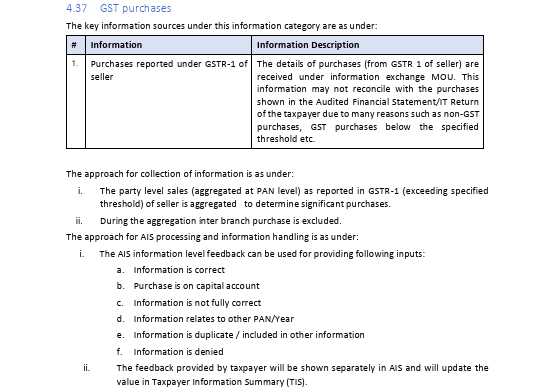

4.37 GST purchases ………………………………………………………………………………………………. 63

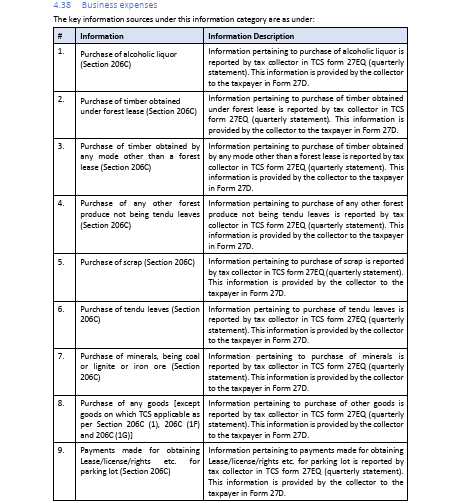

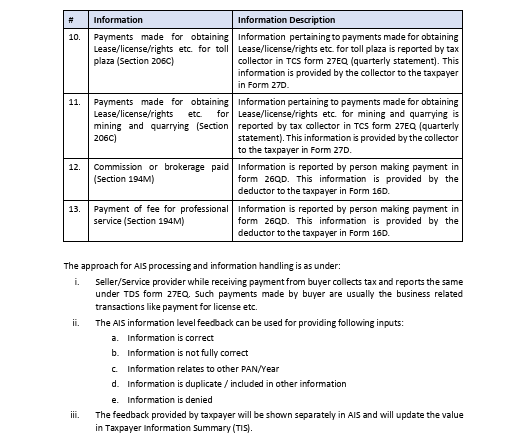

4.38 Business expenses …………………………………………………………………………………………. 64

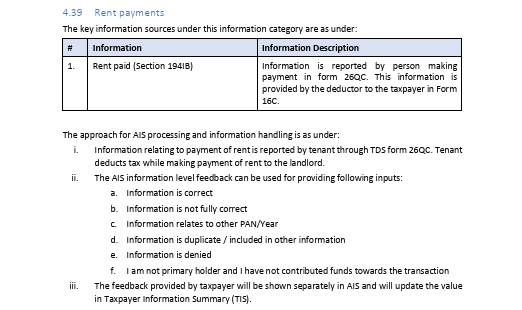

4.39 Rent payments ……………………………………………………………………………………………… 66

4.40 Miscellaneous payments …………………………………………………………………………………. 67

1. About this Document ……………………………………………………………………………………………… 5

2. Background…………………………………………………………………………………………………………… 5

3. Annual Information Statement Overview …………………………………………………………………….. 6

3.1 Objectives ……………………………………………………………………………………………………… 6

3.2 AIS Features …………………………………………………………………………………………………… 6

3.3 AIS Preparation ……………………………………………………………………………………………….. 7

3.4 AIS Feedback ………………………………………………………………………………………………….. 7

3.5 AIS Feedback Processing……………………………………………………………………………………. 7

3.6 Key Terms ……………………………………………………………………………………………………… 9

3.7 Illustrations ………………………………………………………………………………………………….. 10

4. AIS Information Category ……………………………………………………………………………………….. 17

4.1 Salary ………………………………………………………………………………………………………….. 19

4.2 Rent received ……………………………………………………………………………………………….. 20

4.3 Dividend ………………………………………………………………………………………………………. 21

4.4 Interest from savings bank ………………………………………………………………………………. 22

4.5 Interest from deposit ……………………………………………………………………………………… 23

4.6 Interest from others ……………………………………………………………………………………….. 24

4.7 Interest from income tax refund ……………………………………………………………………….. 25

4.8 Rent on plant & machinery ………………………………………………………………………………. 26

4.9 Winnings from lottery or crossword puzzle u/s 115BB……………………………………………. 27

4.10 Winnings from horse race u/s 115BB …………………………………………………………………. 28

4.11 Receipt of accumulated balance of PF from employer u/s 111 …………………………………. 29

4.12 Interest from infrastructure debt fund u/s 115A(1)(a)(iia) ………………………………………. 30

4.13 Interest from specified company by a non-resident u/s 115A(1)(a)(iiaa) …………………….. 31

4.14 Interest on bonds and government securities ………………………………………………………. 32

4.15 Income in respect of units of non-resident u/s 115A(1)(a)(iiab)………………………………… 33

4.16 Income and long-term capital gain from units by an offshore fund u/s 115AB(1)(b) ……… 34

4.17 Income and long-term capital gain from foreign currency bonds or shares of Indian companies u/s 115AC ……………………………………………………………………………………………… 35

4.18 Income of foreign institutional investors from securities u/s 115AD(1)(i)……………………. 36

4.19 Income of Specified Funds from securities u/s 115AD(1)(i) ……………………………………… 37

4.20 Insurance commission …………………………………………………………………………………….. 38

4.21 Receipts from life insurance policy …………………………………………………………………….. 39

4.22 Withdrawal of deposits under national savings scheme………………………………………….. 40

4.23 Receipt of commission etc. on sale of lottery tickets ……………………………………………… 41

4.24 Income from investment in securitization trust …………………………………………………….. 42

4.25 Income on account of repurchase of units by MF/UTI ……………………………………………. 43

4.26 Interest or dividend or other sums payable to government …………………………………….. 44

4.27 Payment to non-resident sportsmen or sports association u/s 115BBA ……………………… 45

4.28 Income of specified senior citizen ……………………………………………………………………… 46

4.29 Sale of land or building ……………………………………………………………………………………. 47

4.30 Receipts from transfer of immovable property …………………………………………………….. 49

4.31 Sale of vehicle……………………………………………………………………………………………….. 50

4.32 Sale of securities and units of mutual fund ………………………………………………………….. 51

4.33 Off market debit transactions …………………………………………………………………………… 56

4.34 Off market credit transactions ………………………………………………………………………….. 58

4.35 Business receipts …………………………………………………………………………………………… 60

4.36 GST turnover ………………………………………………………………………………………………… 62

4.37 GST purchases ………………………………………………………………………………………………. 63

4.38 Business expenses …………………………………………………………………………………………. 64

4.39 Rent payments ……………………………………………………………………………………………… 66

4.40 Miscellaneous payments …………………………………………………………………………………. 67

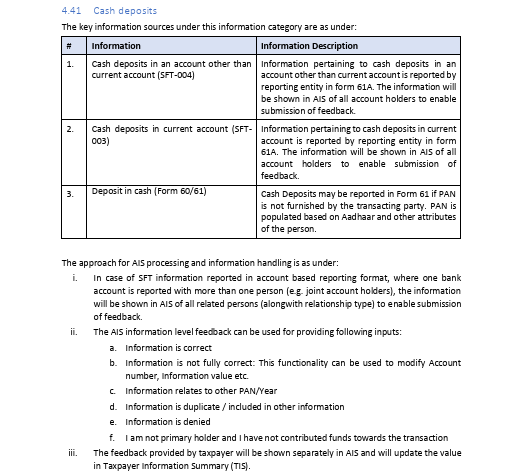

4.41 Cash deposits ……………………………………………………………………………………………….. 68

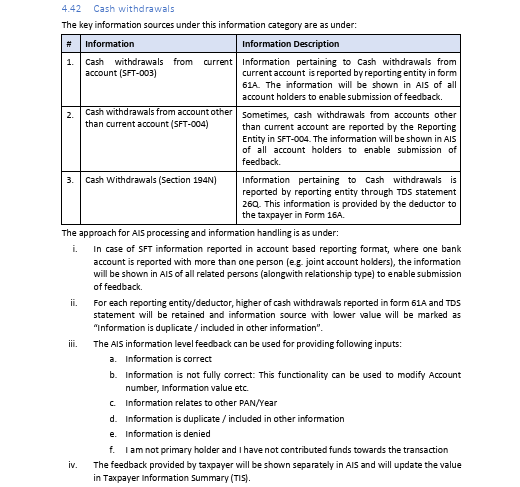

4.42 Cash withdrawals …………………………………………………………………………………………… 69

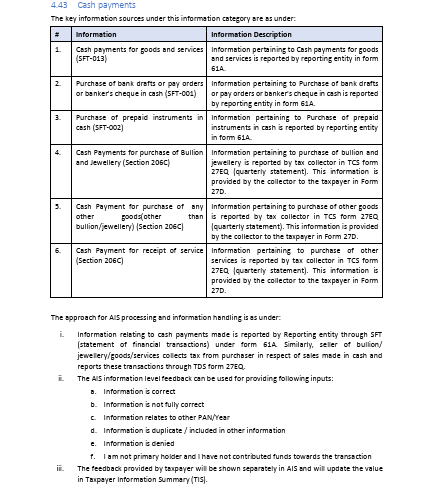

4.43 Cash payments ……………………………………………………………………………………………… 70

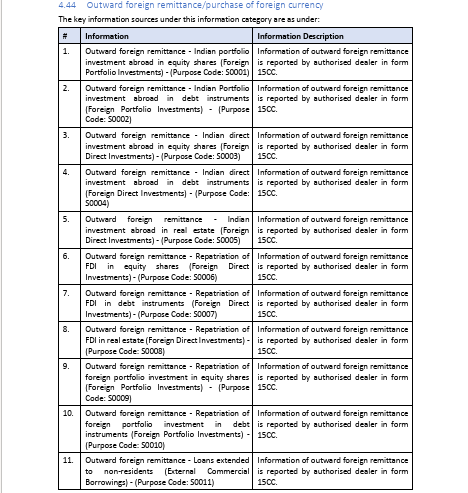

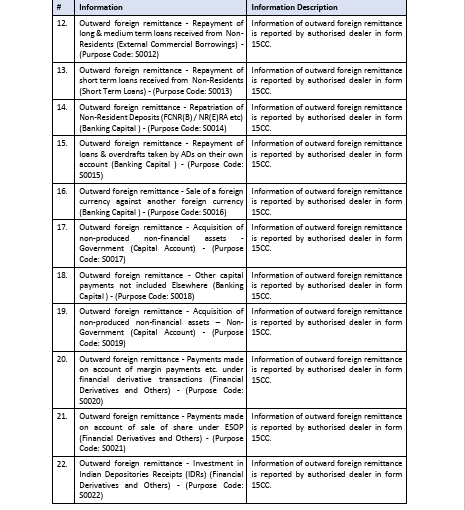

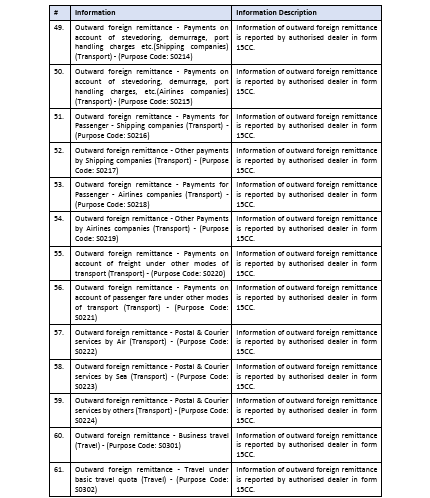

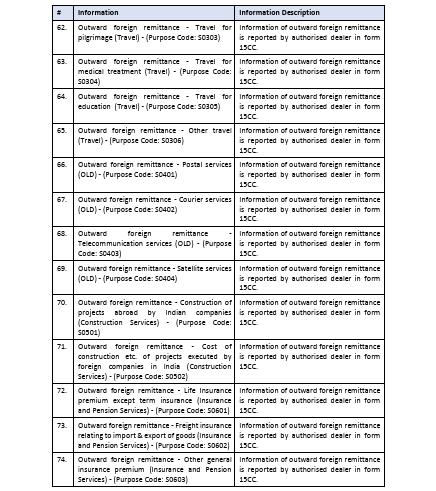

4.44 Outward foreign remittance/purchase of foreign currency ……………………………………… 71

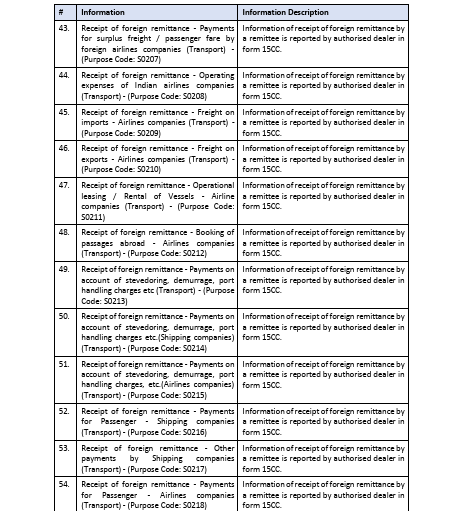

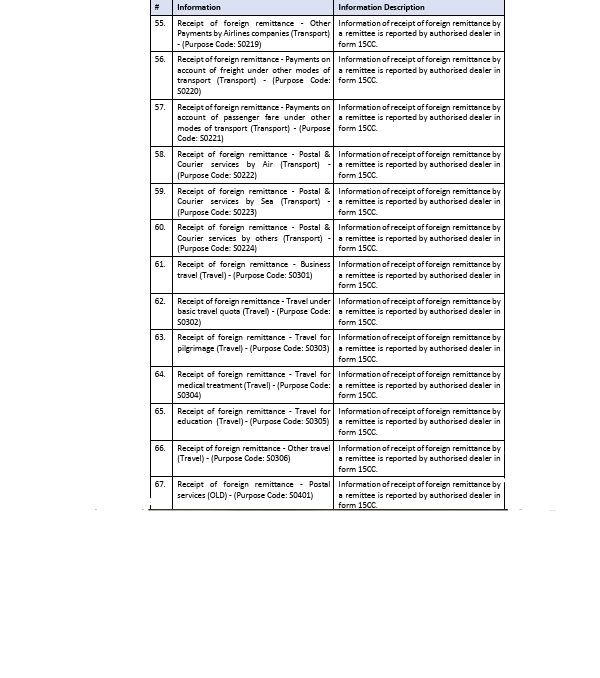

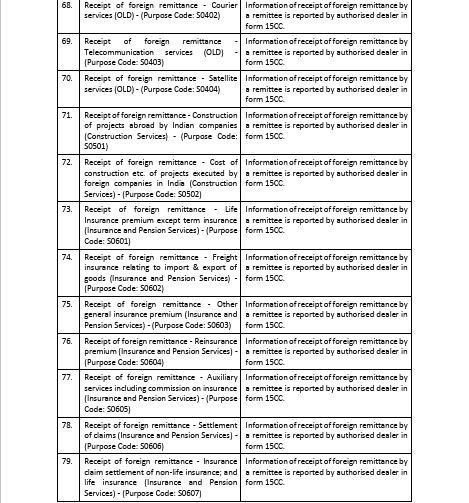

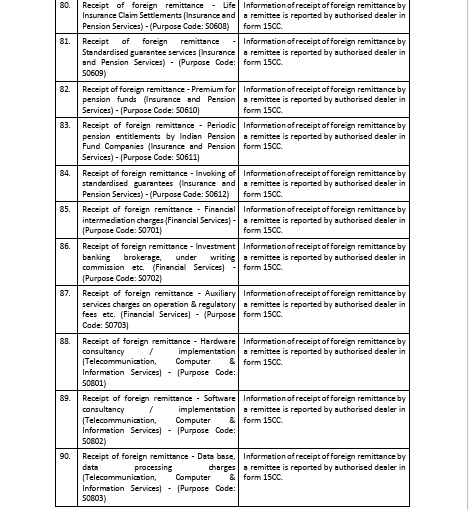

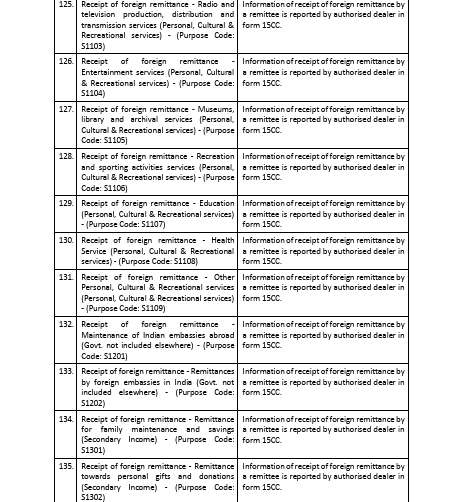

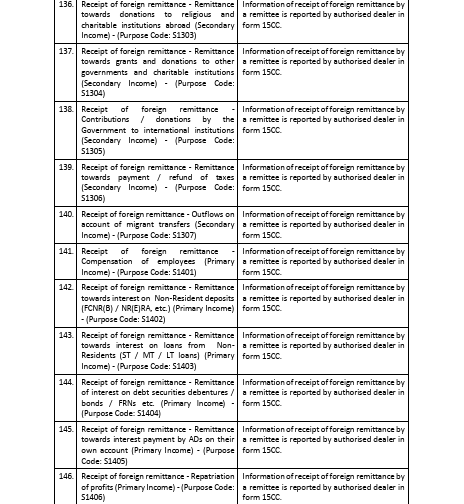

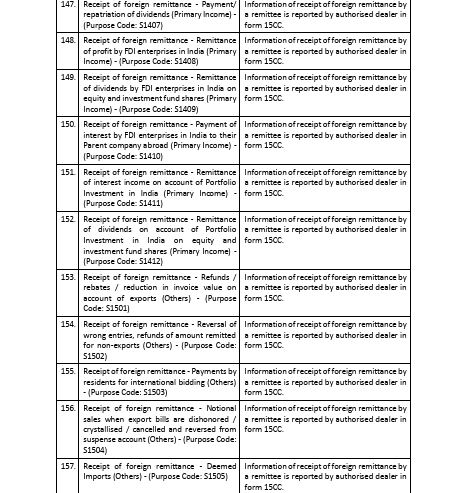

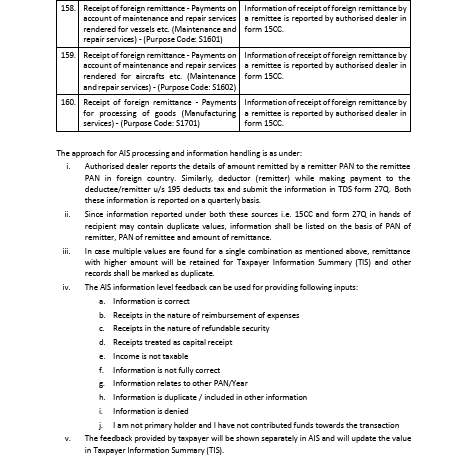

4.45 Receipt of foreign remittance …………………………………………………………………………… 85

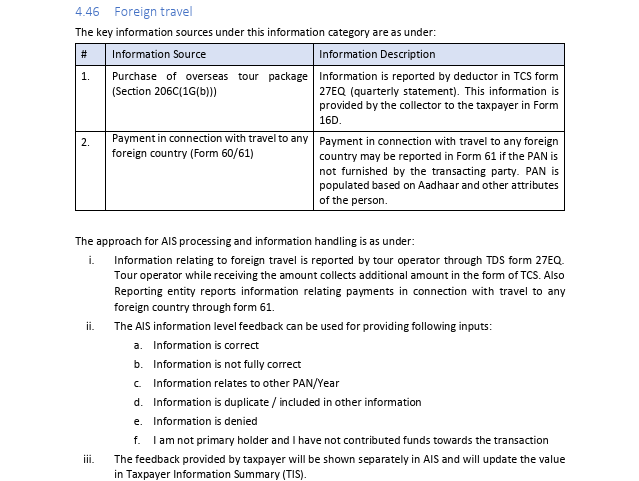

4.46 Foreign travel ……………………………………………………………………………………………… 100

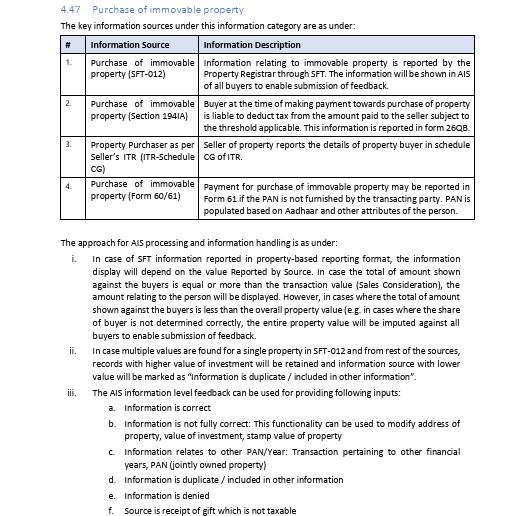

4.47 Purchase of immovable property …………………………………………………………………….. 101

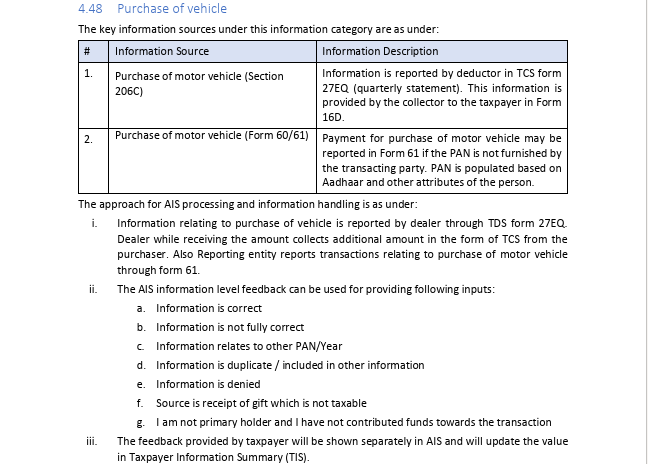

4.48 Purchase of vehicle ………………………………………………………………………………………. 102

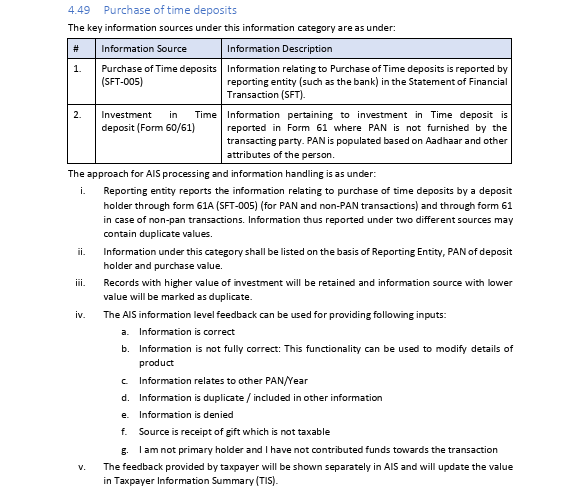

4.49 Purchase of time deposits ……………………………………………………………………………… 103

4.50 Purchase of securities and units of mutual funds ………………………………………………… 104

4.51 Credit/Debit card …………………………………………………………………………………………. 106

4.52 Balance in account ……………………………………………………………………………………….. 107

4.53 Income distributed by business trust ………………………………………………………………… 108

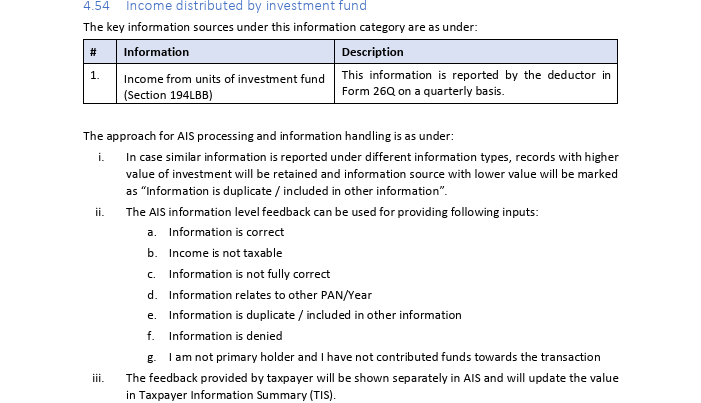

4.54 Income distributed by investment fund …………………………………………………………….. 109

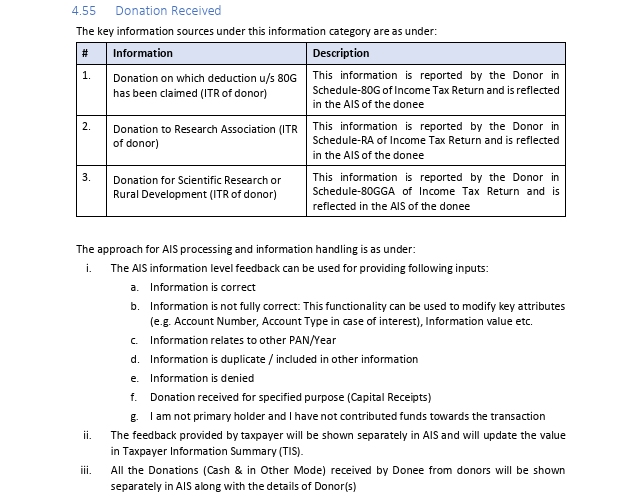

4.55 Donation Received ……………………………………………………………………………………….. 110

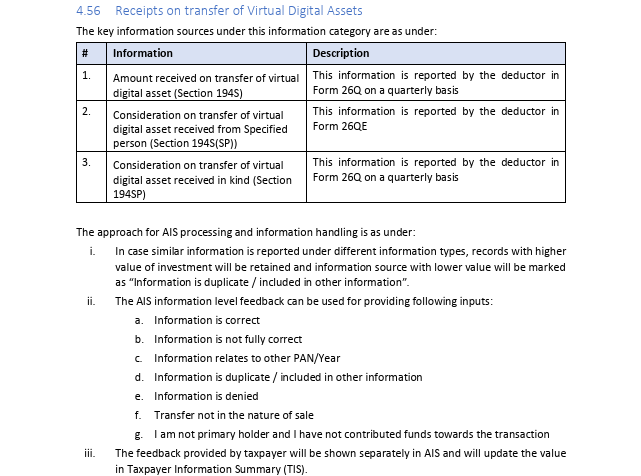

4.56 Receipts on transfer of Virtual Digital Assets………………………………………………………. 111

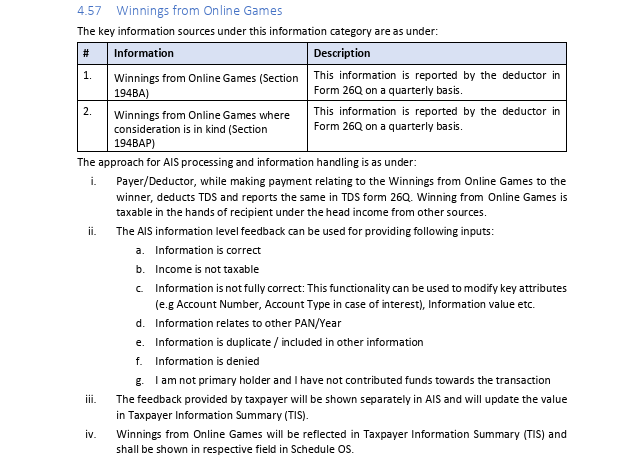

4.57 Winnings from Online Games …………………………………………………………………………. 112

4.58 Receipt of amount by Partners from Partnership Firm………………………………………….. 113

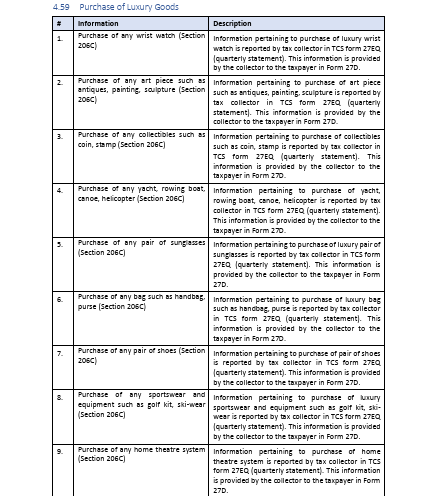

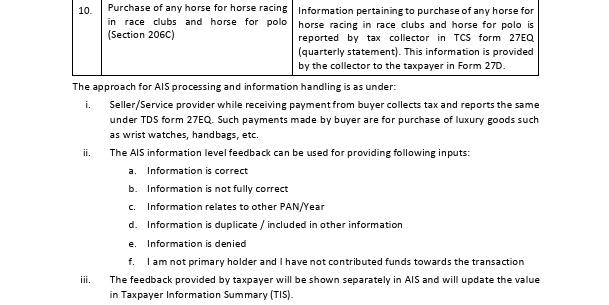

4.59 Purchase of Luxury Goods ……………………………………………………………………………… 114

1. About this Document

The objective of this document is to develop common and shared understanding related to Annual Information Statement (AIS) and various information sources.

2. Background

In order to promote transparency and simplifying the tax return filing process, CBDT vide Notification dated May 28, 2020 has amended Form 26AS vide Sec 285BB of Income Tax Act, 1961 r.w.r.114-I of Income Tax Rules, 1962 w.e.f. 01.06.2020. The new Form 26AS is an Annual Information Statement or AIS which will provide a complete profile of the taxpayer for a particular year. The Board may also authorise the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) or any person authorised by him to upload the information received from any officer, authority or body performing any function under any law or the information received under an agreement referred to in section 90 or section 90A of the Income-tax Act,1961 or the information received from any other person to the extent as it may deem fit in the interest of the revenue in the annual information statement . The format of Annual Information Statement is as under:

Part A

Permanent Account Number, Aadhaar Number, Name, Date of Birth/ Incorporation/ Formation, Mobile No., Email Address, Address.

Part B

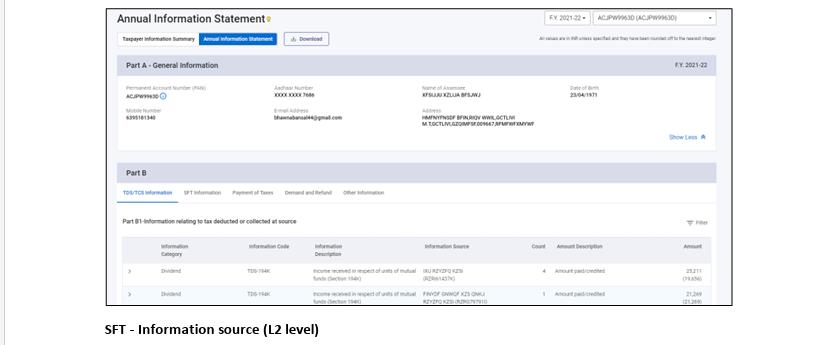

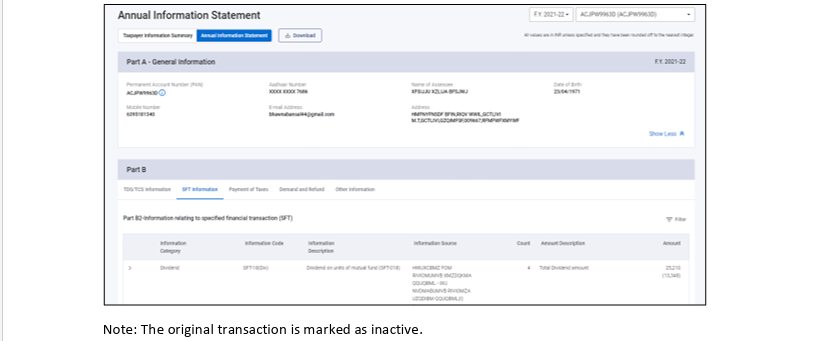

1. Information relating to tax deducted or collected at source

2. Information relating to specified financial transaction (SFT)

3. Information relating to payment of taxes

4. Information relating to demand and refund

5. Information relating to pending proceedings

6. Information relating to completed proceedings

7. Any other information in relation to sub-rule (2) of rule 114-I

3. Annual Information Statement Overview

Annual Information Statement or AIS is comprehensive view of information for a taxpayer displayed in Form 26AS. During preparation of AIS, information processing is required to display complete and accurate information to the taxpayer.

3.1 Objectives

The key objectives of AIS are:

• Display complete information to the taxpayer

• Promote voluntary compliance and enable seamless prefiling of return

• Deter non-compliance

3.2 AIS Features Salient Features of new AIS are as under:

• Inclusion of new information (interest, dividend, securities transactions, mutual fund transactions, foreign remittance information etc.)

• Use of Data Analytics to populate PAN in non-PAN data for inclusion in AIS.

• Deduplication of information and generation of a simplified Taxpayer Information Summary (TIS) for ease of filing return (pre-filling will be enabled in a phased manner).

• Taxpayer will be able to submit online feedback on the information displayed in AIS and also download information in PDF, JSON, CSV formats.

• AIS Utility will enable taxpayer to view AIS and upload feedback in offline manner.

• AIS Mobile Application will enable taxpayer to view AIS and upload feedback on mobile.

Disclaimer: Annual Information Statement (AIS) includes information presently available with Income Tax Department. There may be other transactions relating to the taxpayer which are not presently displayed in Annual Information Statement (AIS). Taxpayer is expected to check all related information and report complete and accurate information in the Income Tax Return.

3.3 AIS Preparation

Some key information processing steps are:

- PAN Population: In case no valid PAN is available in the submitted information, the PAN will

be populated on matching Aadhaar and other key attributes. - Information Display: Generally, the reported information is displayed against the reported

PAN holder. The information display logic for specific information such as property, bank

account, demat account etc. aims to show information to relevant PAN holders to enable

review and submission of feedback. - Information Deduplication: In case where similar information is reported under different

information types (e.g. reporting of interest/dividend in SFT and TDS) the information with

lower value will be marked as “Information is duplicate / included in other information” using

automated rules.

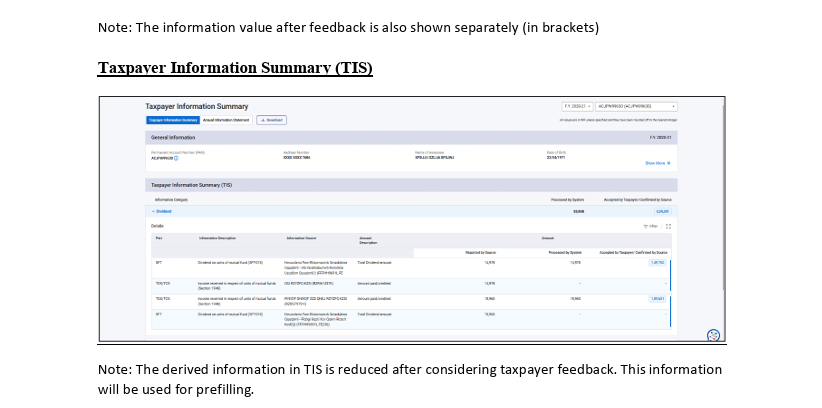

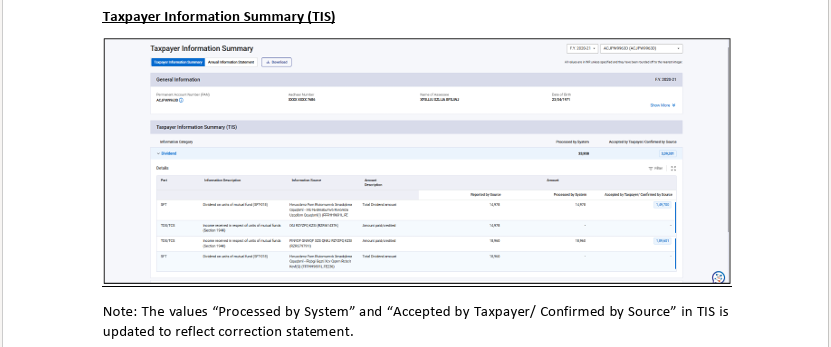

- Taxpayer Information Summary (TIS) preparation: The information category wise aggregated

information summary for a taxpayer is prepared after deduplication of information based on

pre-defined rules. It shows value Processed by System (i.e. value generated after

deduplication of information based on pre-defined rules) and value Accepted by Taxpayer/

Confirmed by Source (i.e. value derived after considering the taxpayer feedback or Source’s

confirmation on taxpayer’s feedback and value Processed by System) under each information

category (e.g. Salaries, Interest, Dividend etc.). The derived information will be used for

prefilling of Return.

3.4 AIS Feedback

The taxpayer will be able to view AIS information and submit following types of response on the

information:

- Information is correct

• Information is not fully correct

• Information relates to other PAN/Year

• Information is duplicate / included in other information

• Information is denied

• Customized Feedback

3.5 AIS Feedback Processing

The AIS Feedback processing approach is as under:

- The feedback provided by assessee will be captured in the Annual Information Statement (AIS)

and value Reported by Source and modified value (i.e. value after feedback or Source’s

confirmation on taxpayer’s feedback) will be shown separately. - The feedback provided by assessee will be considered to update the value Accepted by

Taxpayer/ Confirmed by Source (value derived after considering the taxpayer feedback or

Source’s confirmation on taxpayer’s feedback) in Taxpayer Information Summary (TIS). - The Source may confirm or deny the negative feedback given by the assessee on a particular

information. In case of denial, the value earlier reported by the Source will be updated in the

value Accepted by Taxpayer/ Confirmed by Source in TIS. - Information assigned to other PAN/Year in AIS will be processed and information will be

shown in the AIS of the taxpayer using automated rules.

In case the assigned information is modified/denied, the feedback will be processed in

accordance with risk management rules and high-risk feedback will be flagged for seeking

confirmation from the information source.

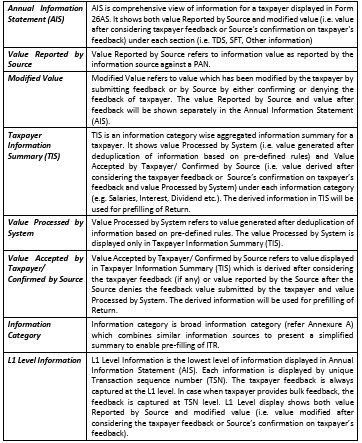

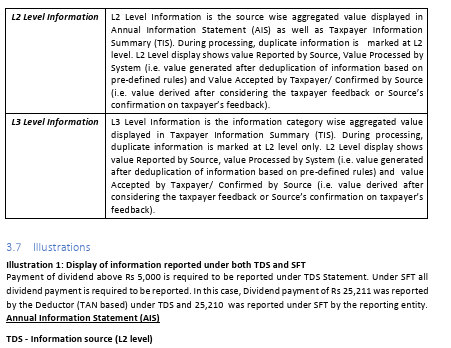

3.6 Key Terms

- AIS Information Category

The broad categories of Information in Taxpayer Information Summary (TIS) are as under:

The key information sources, approach for Annual Information Statement (AIS) processing and

Taxpayer Information Summary (TIS) preparation is explained in following paragraphs.

1. Salary

2. Rent received

3. Dividend

4. Interest from savings bank

5. Interest from deposit

6. Interest from others

7. Interest from income tax refund

8. Rent on plant & machinery

9. Winnings from lottery or crossword puzzle u/s 115BB

10. Winnings from horse race u/s 115BB

11. Receipt of accumulated balance of PF from employer u/s 111

12. Interest from infrastructure debt fund u/s 115A(1)(a)(iia)

13. Interest from specified company by a non-resident u/s 115A(1)(a)(iiaa)

14. Interest on bonds and government securities

15. Income in respect of units of non-resident u/s 115A(1)(a)(iiab)

16. Income and long-term capital gain from units by an off shore fund u/s 115AB(1)(b)

17. Income and long-term capital gain from foreign currency bonds or shares of Indian companies’

u/s 115AC

18. Income of foreign institutional investors from securities u/s 115AD(1)(i)

19. Income of Specified Fund from securities u/s 115AD(1)(i)

20. Insurance commission

21. Receipts from life insurance policy

22. Withdrawal of deposits under national savings scheme

23. Receipt of commission etc. on sale of lottery tickets

24. Income from investment in securitization trust

25. Income on account of repurchase of units by MF/UTI

26. Interest or dividend or other sums payable to government

27. Income of specified senior citizen

28. Sale of land or building

29. Receipts for transfer of immovable property

30. Sale of vehicle

31. Sale of securities and units of mutual fund

32. Off market debit transactions

33. Off market credit transactions

34. Business receipts

35. GST turnover

36. GST purchases

37. Business expenses

38. Rent payment

39. Miscellaneous payment

40. Cash deposits

41. Cash withdrawals

42. Cash payments

43. Outward foreign remittance/purchase of foreign currency

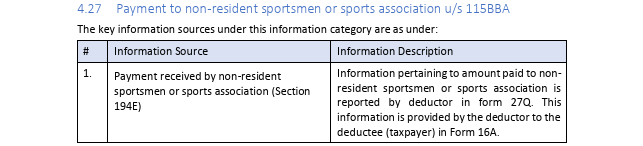

44. Receipt of foreign remittance 45. Payment to non-resident sportsmen or sports association u/s 115BBA

46. Foreign travel

47. Purchase of immovable property

48. Purchase of vehicle

49. Purchase of time deposits

50. Purchase of securities and units of mutual funds

51. Credit/Debit card

52. Balance in account

53. Income distributed by business trust

54. Income distributed by investment fund

55. Donation received

56. Receipt on transfer of Virtual Digital Assets

57. Winning from Online Games u/s 115BBJ

58. Receipt of amount by Partners from Partnership Firm

59. Purchase of Luxury Goods

The approach for AIS processing and information handling is as under:

- For an employer (TAN) and employee (PAN), if salary reported in TDS Annexure II is equal or

more than the sum of salary payment in Quarterly TDS Statements (Section 192), all salary

payment amount in Quarterly TDS Statements (Section 192) will be marked as “Information is

duplicate / included in other information”. - For an employer (TAN) and employee (PAN), if sum of salary payment in Quarterly TDS

Statements (Section 192) is more than the salary reported in TDS Annexure II, salary reported

in TDS Annexure II will be marked as “Information is duplicate / included in other information”.

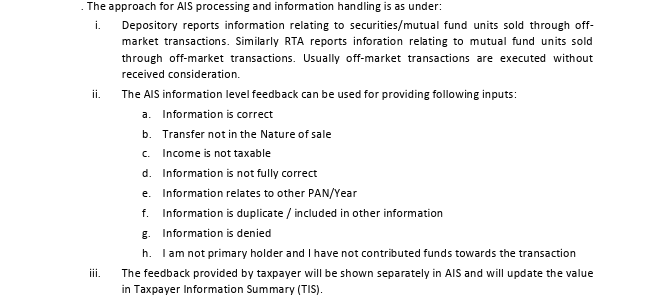

3. The AIS information level feedback can be used for providing following inputs:

a. Information is correct

b. Income is not taxable

c. Information is not fully correct – This functionality can be used to modify salary details.

d. Information relates to other PAN/Year

e. Information is duplicate / included in other information

f. Information is denied

4.The feedback provided by taxpayer will be shown separately in AIS and will update the value in

Taxpayer Information Summary (TIS).

5.The sum of salary received from all employers will be reflected at Taxpayer Information

Summary.

6.All exempt allowances should be included in Gross Salary. Allowances to the extent exempt u/s

10 and deduction u/s 16 needs to be claimed in the return.

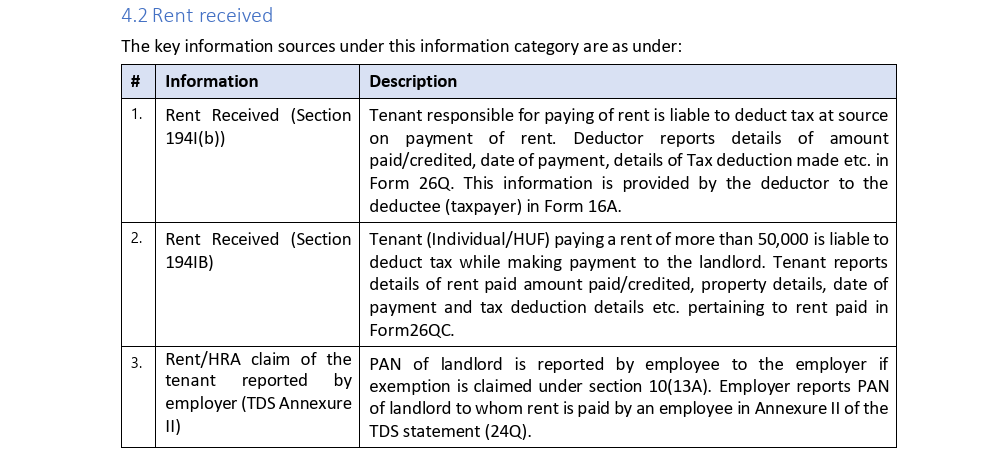

- Information reported under section 194I(b), 194IB and co-owner will be summed up at

deductor PAN level.

ii. For each tenant (PAN), higher of rent reported through TDS statement (194I(b)+194IB) and

rent reported by co-owner of property or reported in Annexure II will be retained for a

‘Landlord -Tenant’ combination and information source with lower value will be marked as

“Information is duplicate / included in other information”.

iii. Employer reports PAN of landlord to whom rent is paid by an employee in Annexure II of the

TDS statement (24Q). This information will only be shown only when the rent received from

the tenant is not reported under other sources. The landlord can use the feedback option

‘’Information is not fully correct’’ to modify rent details.

iv. The AIS information level feedback can be used for providing following inputs:

a. Information is correct

b. Income is not taxable

c. Information is not fully correct: This functionality can be used to modify rent details

d. Information relates to other PAN/Year

e. Information is duplicate / included in other information

f. Information is denied

g. I am not primary holder and I have not contributed funds towards the transaction

v. The feedback provided by taxpayer will be shown separately in AIS and will update the value

in Taxpayer Information Summary (TIS).

vi. The sum of rent received from all tenants will be reflected at Taxpayer Information Summary

(TIS).

vii. All deductions from house property income like interest on borrowed capital, standard

deduction to be claimed in the return.