ORDER

Vimal Kumar, Judicial Member.- Above captioned cross appeals filed by the Department of Revenue and the assessee are against order dated 29.12.2017 of the Learned Commissioner of Income Tax (Appeals), 23, New Delhi [hereinafter referred to as ‘the Ld. CIT(A)’] passed u/s 250 of the Income Tax Act, 1961, [hereinafter referred to as ‘the Act’] arising out of assessment order dated 26.12.2016 of Ld. Assessing Officer/ Assistant Commissioner of Income Tax, Central Cirlce-1, New Delhi [hereinafter referred as ‘the AO’] u/s 143(3) of the Act for Assessment Year 2013-14.

2. Brief facts of the case are that the assessee company filed original return of income on 30.11.2013 declaring income of Rs. Nil after adjusting brought forward losses of Rs.2,39,51,488/- against the profit earned during the year. The assessee company revised computation showing loss of Rs.58,49,38,385/- as the assessee has drawn amount of Rs.60,88,89,873/- being amortization of Foreign Currency Monetary Item Translation as Difference Account. The assessee submitted from Form No.3CEB U/s 92E along with audit report. The case was selected for scrutiny. Notice u/s 143(2) dated 04.09.2014 was issued to the assessee. Notices u/ss. 142(1) and 143(2) along with questionnaire were issued on 24.09.2015. The assessee was asked for certain details vide Notice dated 17.10.2016. S/Shri Sanjeev Singh, Shri Ram Babu Keshari and Anuj Tomar, ARs of the assessee appeared and filed details, produced books of account, bills & vouchers etc. The assessee reported “Receipt of Interest” of Rs.1,39,65,20,274/- on loan granted to its Wholly Owned Foreign Subsidiary Company M/s Aamby Valley Mauritius Limited (AVML). The loan of 480 million (mn) GBP i.e. Rs.35,24,51,61,000/- was granted in the previous financial year i.e. 2010-11. Certain other specified domestic transactions were also reported by the assessee. Because of specified domestic and international transaction, the matter was referred to the TPO 1(1) to determine the arm’s length price u/s 92CA(3) vide letter F. No. ACIT/CC-1/2015-16/1281 dt. 17.02.2016.

2(i) The T.P.O. passed order u/s 92CA(3) of the I.T. Act on 30.09.2016 wherein it was held that:-

“In view of functional and economic analysis of the assessee, no adverse inference is drawn in respect of the domestic and international transactions undertaken by the assessee during the F.Y.2012-13. “

2(ii) On completion of proceeding Ld. AO vide assessment order dated 26.12.2016 made following additions:

| Add: |

PROFITAS PER COMPUTATION OF RETURN OF INCOME (A) |

|

Rs.2,39,51,488/- |

| 1 |

Advances from Customers |

Rs. 8,94,02,760/- |

|

| 2 |

Advertisement & Sales Promotion and Business Promotion Expenses |

Rs.38,42,893/- |

|

| 3 |

Consultancy Charges |

Rs.26,80,635/- |

|

| 4 |

Diversion of Interest bearing funds |

Rs.3,90,73,715/- |

|

| 5 |

Disallowance u/s 14A |

Rs. 395,49,10,222/- |

|

| 6 |

Prior Period Expense |

Rs. 3,66,725/- |

|

| 7 |

Bills not available |

Rs.36,18,203/- |

|

| 8 |

Bills not in the name of the company |

Rs.35,82,247/- |

|

| 9 |

Proper documentary evidences not available |

Rs. 7, 64,083/- |

|

| 10 |

Expenditure not incurred wholly and exclusively for business purpose |

Rs.3,50,000/- |

|

| 11 |

Non deduction of TDS |

Rs.69,12,872/- |

|

| 12 |

Commission and Brokerage Expense |

Rs. 7,02,800/- |

|

| 13 |

Sundry balances Written off |

Rs. 23,01,756/- |

|

| 14 |

Long outstanding Imprest |

Rs. 3,08,144/- |

|

| 15 |

TOTAL ADDITIONS/DISALLOWANCES (B) |

Rs.410,88,17,055/- |

Rs.413,27,68,543/- |

3. Against order dated 26.12.2016 of Ld. AO, the assessee filed appeal before the Ld. CIT(A) which was partly allowed for statistical purposes vide order dated 29.12.2017.

4. Being aggrieved, the Department of Revenue and the assessee preferred the present cross appeals.

5. In ITA No.1352/Del/2018, the Department of Revenue raised following grounds of appeal:

“1. The order of Ld. CIT(A) is not correct in law and on facts.

2. On the facts and circumstances of the case, the Ld. CIT(A) has erred in law in deleting the addition of Rs. 8,94,02,760/- made by the AO on account of advances from customers.

3. On the facts and circumstances of the case, the Ld. CIT(A) has erred in law in deleting the addition of Rs.15,70,622/- made by the AO on account of Advertisement & Sales Promotion and Business Promotion Expenses.

4. On the facts and circumstances of the case, the Ld. CIT(A) has erred in law in deleting the addition of Rs. 14,49,735/- made by the AO on account of disallowance of consultancy charges.

5. On the facts and circumstances of the case, the Ld. CIT(A) has erred in deleting the addition of Rs.3,90,73,715/- made by the AO on account of Diversion of Interest bearing fund.

6. On the facts and circumstances of the case, the Ld. CIT(A) has erred in deleting the addition of Rs.395,49,10,222/-made by the AO on account of disallowance u/s 14.A. of the I.T. Act, 1961.

7. On the facts and circumstances of the case, the Ld. CIT(A) has erred in deleting the addition of Rs.3,66,725/-made by the AO on account of prior period expenses.

8. On the facts and circumstances of the case, the Ld. CIT(A) has erred in deleting the addition of Rs.36,18,203/- made by the AO on account of bills not available.

9. On the facts and circumstances of the case, the Ld. CIT(A) has erred in deleting the addition of Rs.35,82,247/- made by the AO on account of bills not in the name of company.

10. On the facts and circumstances of the case, the Ld. CIT(A) has erred in deleting the addition of Rs. 7,64,083/- made by the AO on account of proper documentary evidence not available.

11. On the facts and circumstances of the case, the Ld. CIT(A) has erred in deleting the addition of Rs. 4,12,528/- made by the AO on account of non-deduction of TDS.

12. On the facts and circumstances of the case, the Ld. CIT(A) has erred in deleting the addition of Rs.3,08,144/-made by the AO on account of long outstanding Imprest.

13. The appellant craves leave to add, amend any/all the ground of appeal before or during the course of hearing of the appeal. “

6. In ITA No.1434/Del/2018, the assessee raised following grounds of appeal:

“1. That the learned CIT(A) has erred in law and on facts and circumstances of the case in not considering the revised computation filed by the appellant during the course of assessment proceedings showing a loss of Rs. 58,49,38,385/-.

2. That the learned CIT(A) has failed to appreciate that the appellant has right to make a legal claim during the course of appellate proceedings and, therefore, he is not justified in ignoring the revised computation filed by the appellant withdrawing the amortization of foreign currency, monetary items translation difference amounting to Rs.60,88,89,873/-.

3. That the learned CIT(A) has erred in law and on facts and circumstances of the case in confirming the disallowance of Rs. 28,18,308/- out of Advertisement, Sales Promotion and Business Promotion Expenses.

4. That the learned CIT(A) is not justified in confirming the disallowance to the extent of Rs. 12,30,900 -out of Consultancy Charges incurred by the appellant.

5. That the learned CIT(A) is not justified in confirming the disallowance of Rs.3,50,000/- out of Advertisement Expenses by holding that the same has not been only and exclusively incurredfor the business of the appellant.

6. That the learned CIT(A) is not justified in confirming the disallowance of Rs.61,65,344/- under section 40(a)(ia) of the I.T. Act, 1961 for alleged non deduction of tax at source, in spite of the fact, that the deductee had filed copy of certificate in Form 26A of the Income Tax Rules, 1962.

7. That the learned CIT (A) has erred in law and on facts and circumstances of the case in confirming the disallowance of Rs. 7,02 800/-on account of Commission and Brokerage Expenses incurred for procurement of residential accommodation for employees

8. That the learned CIT(A) has erred in law and on facts and circumstances of the case in confirming the disallowance of Rs. 23,01,576/- out of outstanding debts written off during the year.

9. That the order passed by the learned CIT (A) is against the facts and circumstances as well as legal aspects of the case and, therefore, the additions confirmed by him deserve to be deleted.

10. That the appellant craves leaves to add, alter, amend, and withdraw any or all of the grounds of appeal on or before the date of hearing. “

7. Ld. Departmental Representative submitted that ground of appeal No.1 of revenue is general. Regarding ground no.2 of appeal of Revenue, he submitted that Ld. CIT(A) erred in deleting additions of Rs.8,94,02,760/- made by Ld. AO on account of advances from customers. Ld. CIT(A) noted that advances pertained to sale of chalets and sale of land. Further, the CIT(A) observed that the appellant had booked advances against sale of chalets as per Percentage of Completion Method and that advances towards sale of land were duly accounted for in the preceding AYs.

8. Ld. Authorized Representative for respondent assessee submitted that as per Note No. X of the financial statements, for the sale of Land/plots, the appellant is recognizing revenue in the financial year in which transfer is made by execution and/or registration of Agreement to Sell.

8.1 For Consideration contracts pertaining to sale of chalets, the Appellant is following AS-7 ‘Construction Contracts’ i.e., recognizing revenue on the basis of Percentage of Completion Method. Refer Financial Statement of the Appellant for AY 2013-14 @ page nos. 1-40 of the paper book @ page no 5.

8.2 Basis the aforesaid, is that out of advance amount of Rs.8,94,02,760 received during the Fy 2012-13, advances aggregating to Rs.6,54,61,094 received against sale of land is already accounted for and offered for tax by the Appellant in preceding years in which Agreement to Sell was executed. Refer Status of advances received against sale of chalets SAP screenshot and copy of ledger regarding advance from customers a page nos. 300-312 of the paper book.

8.3 Further, balance advances aggregating to Rs.2,39,41,666 pertains to sale of chalets which were still under construction. Said advances are accounted for & offered for tax by the Appellant on Percentage of Completion Method

8.4 Therefore, in view of the above, it is submitted that the allegation of assessing officer that sales corresponding to the aforesaid advances received are not booked is incorrect as, in each case, advance has been considered for tax purposes either in the year Agreement to Sell was entered or as per Percentage of Completion Method.

8.5 In AY 2012-13, ITAT remanded the issue to AO for verification.

8.6 It is, however, submitted that in the subject AY, the CIT(A) has deleted the addition after considering the facts on record. In absence of any contrary facts brought on record by the Revenue, it is submitted that CIT(A) enhanced the aforesaid amount of disallowance from Rs.38,42,893/- to Rs.44,69,510. The disallowance of Rs.15,70,522/- deleted by the CIT(A) is wrongly taken as Rs.38,42,893/- in the Department Ground of Appeal.

9. From examination of record in light of aforesaid rival contention, it is crystal clear that Ld. CIT(A) deleted addition of Rs.8,94,02,760/- on account of advances received from booking from various parties Financial Statement of the assessee for AY 2013-14 is at page Nos. 1 to 40 of the PB. The status of advances received against sale of chalets SAP screenshot and copy of ledger regarding advance from customers @ page nos. 300-312 of the paper book. In view of the above documents and agreement to sale entered or as per percentage of completion method the findings of Ld. CIT(A) being meritorious are upheld. Therefore, ground of appeal No.2 of Revenue is rejected.

10. Ld. Departmental Representative, submitted that Ld. CIT(A) erred in deleting the addition of Rs.38,42,893/- made by the AO on account of Advertisement & Sales Promotion and Business Promotion Expenses.

10.1. The AO disallowed an amount of Rs.38,42,839 out of the total expenditure, as compared hereunder:

| S. No. |

Vendor |

Amount claimed as expense |

Amount disallowed |

Reason for disallowance |

| 1. |

Allied Media Networks P Ltd. |

Rs.67,28,685/- |

Ad-hoc disallowance of 50% i.e., Rs.33,64,343 |

Vouchers submitted by Appellant are not properly supported and reason for incurring such huge expense not given. |

| 2. |

International Property Media Ltd. |

Rs.4,78,550 |

Rs.4,78,550 |

Voucher not properly supported and nexus between the business of Appellant and expense was not established. |

| Total |

38,42,893 |

|

|

11. Ld. Authorized Representative for respondent-assessee submitted that Ld. CIT(A) enhanced the aforesaid amount of disallowance from Rs.38,42,893/- to Rs.44,69,510. The disallowance of Rs.15,70,522 deleted by the CIT(A) is wrongly taken as Rs.38,42,893/- in the Department.

11.1. The disallowances deleted by the Ld. CIT(A) and our submissions supporting the findings of the CIT(A), are tabulated hereunder:

| S. No. |

Vendor |

Amount of expense disallowed by the AO |

CIT(A) findings for deleting the disallowance and Our Submissions |

| 1. |

Optimal Media Solutions P Ltd. |

10,22,072 |

CIT(A) allowed deduction in this regard after verification of all the invoices. [Refer PB Page no. 60] |

| 2. |

Allied Media Networks P Ltd. |

70,000 |

CIT(A) allowed deduction in this regard after verification of all the invoices. [Refer PB Page no. 110] |

| 3 |

International Property Media Ltd |

4,78,450 |

The expense pertains to advertisement abroad for International Property Magazine Luxury collection and world best Asia Pacific Seminar. CIT(A) held that the bill is in the name of the Appellant and pertains to the subject AY, therefore, allowed as deduction in captioned AY only. [Refer PB Page nos. 130-132] |

|

Total |

15,70,522 |

|

12. From above, it is evident that, Ld. CIT(A) deleted the disallowance on basis of invoices of the expenses incurred pertaining to advertisement Abroad. In absence of any evidence to the contrary, in support of Ground of Appeal No.3 being devoid of merit is rejected.

13. Ld. Departmental Representative regarding Ground of Appeal No.4 of revenue submitted that, the Ld. CIT(A) has erred in law in deleting the addition of Rs.26,80,635/- made by the AO on account of disallowance of consultancy charges. Ld. AO disallowed consultancy charges incurred amounting to Rs.26,80,635/- on account of no proper supporting/justification given by the assessee.

14. Ld. Authorized Representative for respondent-assessee submitted that, Ld. CIT(A), held as under:

| S. No. |

Party |

Description |

Amount in Rs.) |

Findings of CIT(A) and our submissions. |

| 1. |

Service tax on reverse charge basis |

Service tax paid on consultancy charges for services taken from Dubai based consultant (PB Page nos. 136-139) |

13,49,735 |

CIT(A) correctly allowed the deduction as per section 43B of the Act, after verification of proof of payment |

| 2. |

Sahara Global Mastercraft Ltd. |

Debit note received from Sahara Global Mastercraft Ltd for reimbursement of expense incurred by it on Macedonia Project (PB Page nos. 157-158) |

1,00,000 |

CIT(A) correctly allowed deduction of the said amount on account of being professional fee paid to Sahara Global Mastercraft Ltd, which is incurring expenses on Macedonia Project and nothing being on record to question genuineness of this expense. |

15. From perusal of findings of Ld. CIT(A), it is evident that, the addition of Rs.26,80,635/- made by Ld. AO on account of disallowance of consultancy charges was deleted as Rs.13,49,735/- service tax on reverse charges paid on consultancy charges for services taken from Dubai based consultancy were duly verified. Debit note of Rs.1,00,000/- received from Sahara Global Mastercraft for reimbursement of expense incurred by it on Macedonia Project were found to be genuine.

15.1. In view of above material facts, the deletion of Rs.26,80,635/- on account of disallowance of consultancy charges is upheld.

15.2. Accordingly, ground of appeal No.4 of the revenue is rejected.

16. Ld. Departmental Representative regarding Ground No.5 of Revenue submitted that Ld. CIT(A) erred in deleting addition of Rs.3,90,73,715/- made by AO on account of diversion of interest bearing fund. Ld.AO had observed that assessee should have charged interest on the amount of interest free advance given to the related parties.

16.1. Ld. AO held that appellant had paid interest of Rs.181.16 crores on borrowed funds, therefore, aforesaid advances were clear cut diversion of interestbearing funds. The appellant should have charged interest on the amount of interest free advance given to the related parties, the AO made addition of Rs.3,90,73,715/, being 12% of Rs.33,41,27,447/-.

17. Ld. Authorized Representative for respondent-assessee submitted that, it is well settled law that only real income can be brought to tax; hypothetical income in the nature of notional interest cannot be brought to tax. Ld. AO ignored the chart depicting that aforesaid advances arise out of business transactions and same have been settled in later years. Refer chart a page nos. 369-371 of the paper book. The Appellant has Reserves and Surplus to the tune of Rs.503,91,77,53,077 as at 31.03.2013; amount of impugned advances is comparatively miniscule which, in any case, cannot be said to be out of interest-bearing funds.

17.1. The AO grossly erred in imputing notional income in the hands of the Appellant and in bringing the same to tax. Reliance in this regard is placed on the following decisions wherein it has been categorically held that income-tax cannot be levied on hypothetical income; the same is beyond the scope of total income as per section 5 of the Act:

– Godhra ElectricityCo. Ltd. v. CIT (SC)/[1997] 225 ITR 746 (SC)

– CIT v. Excel IndustriesLtd. (SC)

– CIT v. Shoorji Vallabhdas & Co. [1962] 46 ITR 144 (SC)

– Airport Authority of India v. CIT (Delhi)

– CIT v. Ferozepur Finance(P.) Ltd. (Punjab & Haryana)

– CIT v. Motor CreditCo. (P.) Ltd. (Madras)

17.2. Aforesaid advance arose during normal course of business on which there is no stipulation of charging any interest and therefore, there stands no justification in imputing the interest income on alleged advances. Chart depicting details of business advances along with purpose of such advances, settlement of such advances and GL account of the parties is @ page nos. 369-390 of paper book.

18. From record, it is evident that Ld. AO had made addition of Rs.3,90,73,715/-on account of diversion of interest bearing fund. The Ld. CIT(A) deleted by observing that only real income can be brought to tax. No hypothetical or notional income can be brought to tax under the I. T. Act. The Ld.AO ignored the chart depicting that aforesaid advances arise out of business transactions and same have been settled in later years. Refer chart @ page no 369-371 of the paper book. The assessee had reserves and surplus to the tune of Rs.503,91,77,53,077/- as at 31.03.2013; amount of impugned advances is comparatively miniscule which, in any case, cannot be said to be out of interest-bearing funds. It is well settled principle of law that income tax cannot be levied on hypothetical income refers to judgment in Godhra Electricity Co. Ltd. (supra). Therefore, Ground of appeal No.5 of the Revenue is rejected.

19. The Ld. Departmental Representative regarding Ground No.6 of appeal of Revenue submitted that Ld. CIT(A) erred in deleting addition of Rs.395,49,10,222/- made by the AO on account of disallowance u/s 14A of the Act. The Assessing Officer made disallowance of Rs.395,49,10,222/- under section 14A of the Act read with Rule 8D of the Income tax Rules, 1962 (“the Rules”) as under:

-under clause (ii) of Rule 8D-Rs.159,43,66,816/-

-under clause (iii) of Rule 8D-Rs.236,05,43,406/-

20. Ld. Authorized Representative for respondent-assessee submitted that Ld. CIT(A) deleted the aforesaid disallowance of Rs. 395.49 crores made under section 14A of the Act, holding that no exempt income has been earned by the assessee during the year under consideration, relying on decision passed by the Delhi High Court in the case of CIT- IV v. Holcim India (P.) Ltd. (Delhi), wherein it has been held that no disallowance can be made under section 14A of the Act in case no exempt income is earned.

20.1. It is well-settled law that no disallowance can be made under section 14A of the Act in case no exempt income is received during the year under consideration. Reliance in this regard is placed on the following decisions of the Delhi High Court:

– Cheminvest Ltd. v. CIT-IV (Delhi)

– PCIT v. IFFCO Ltd. (Delhi)

– Pr. CIT v. IL & FS Energy Development Company Ltd. (Delhi)

– Pr. CIT v. Sahara India Financial CorporationLtd. (Delhi)

– Pr. CIT v. Alchemist Ltd (Delhi)

20.2. In assessee’s own case for AY 2012-13 (supra), this Hon’ble Tribunal deleted similar disallowance made under section 14A of the Act observing that the assessee had not earned any exempt income during the relevant year. Revenue’s appeal has been dismissed by the Hon’ble Delhi High Court in ITA 849/2019. vide order dated 19.07.2024.

20.3. Further, it is submitted that Explanation to section 14A of the Act, inserted by Finance Act 2022, is applicable only prospectively and is thus, not applicable for the year under consideration. Reliance in this regard is placed on the following decisions of the Delhi High Court:

Pr. CIT v. Era Infrastructure (India) Ltd. (Delhi)

Sahara India Financial Corporation Ltd. (supra)

21. From examination of record, in light of above rival contentions shows that, Ld. CIT(A) deleted disallowance of Rs.395.49 crores made u/s 14A of the Act holding that no exempt income had been earned by assessee during the year under consideration. Relying on decision of Hon’ble High Court of Delhi in the case of Holchin India Pvt. Ltd. (supra). Similar disallowance was held in assessee’s own case for AY 2012-13 vide order dated 19.07.2024 by this Tribunal. Therefore, ground of appeal No.6 of the revenue is rejected.

22. Ld. Departmental Representative regarding ground of appeal No.7 of revenue submitted that, Ld. CIT(A) has erred in deleting the addition of Rs.3,66,725/- made by the AO on account of prior period expenses. The assessing officer disallowed expenses of Rs.3,66,725 holding the same to be prior period expenses, not pertaining to the captioned assessment year.

23. Ld. Authorized Representative for respondent-assessee submitted that Ld. CIT(A) has rightly deleted the said disallowance considering that in each case, either the expenses have been crystallized or invoice has been received in the assessment year under consideration.

23.1. Reliance in this regard is placed on the following decisions wherein it has been held that deduction of an expense shall be allowed in the year of crystallization of the liability, even though such expense relates to the earlier years:

-CIT v. Exxon Mobil Lubricants (P.) Ltd. (Delhi)

-Saurashtra Cement & Chemical Industries Ltd. v. CIT (Gujarat)

-CIT v. Nathmal Tolaram [1973] 88 ITR 234 (Gauhati)

24. From examination of record, it is evident that, Ld. CIT(A) deleted disallowance of Rs.3,66,725/- made by AO on account of prior period expenses. Since expenses had crystalized or invoices were received in the assessment year, therefore, deletion cannot be said to be bad in eyes of law.

24.1. The ground of appeal No.7 of revenue being devoid of merit is rejected.

25. Ld. Departmental Representative regarding ground of appeal No.8 of revenue submitted that, the Ld. CIT(A) has erred in deleting the addition of Rs.36,18,203/- made by the AO on account of bills not available. The assessing officer disallowed expenses aggregating to Rs.36,18,203 holding that the expenses incurred are not supported by bills/ vouchers and no justification for the same was provided by the assessee.

26. Ld. Authorized Representative for respondent-assessee submitted that, considering the bills and invoices for the said expenses filed by the assessee during the appellate proceedings, CIT(A) deleted the said disallowance to the extent of Rs.33,95,775 and upheld the disallowance of Rs.2,22,786.

26.1. The assessee is not in appeal for the disallowance upheld by the CIT(A) amounting to Rs.2,22,786.

26.2. For the remaining expenses amounting to Rs.33,95,775, it is respectfully submitted that expenditure of Rs.33,95,775 incurred by the Appellant is on account of telephone charges, internet & broadband charges, air tickets and electricity charges, allowable under section 37(1) of the Act. The CIT(A) has correctly deleted the disallowance after considering the nature of expenses and the fact that they pertained to the subject AY.

26.3. Therefore, the disallowance made by the assessing officer without appreciating the nature of expenditure and supporting documents like vouchers/ bills/ receipts, deserves to be deleted.

Copy of bills for the expense of Rs.33,95,775 is @page nos. 501-532 of the paper book volume-2

27. From perusal of record, in light of aforesaid rival contentions, shows that, Ld. CIT(A) deleted disallowance to the extent of Rs.33,95,775/- and upheld disallowance of Rs.2,22,786/-. The expenses were incurred by assessee on account of telephone charges, internet & broadband charges, air tickets and electricity charges, allowable under section 37(1) of the Act. Copy of bills for the expense of Rs.33,95,775 is @page nos. 501-532 of the paper book.

27.1. In view of above material facts apparent on record, the deletion of Rs.33,95,775/- is upheld.

27.2. Therefore, ground of appeal No.8 of the revenue is rejected.

28. Ld. Departmental Representative regarding ground of appeal No.9 of revenue submitted that, the Ld. CIT(A) has erred in deleting the addition of Rs.35,82,247/- made by the AO on account of bills not in the name of company. The assessing officer disallowed expenses of Rs.35,82,247 holding that the bills for such expenses were not in the name of the assessee but in the name of Sahara India Commercial Corporation Ltd. (“SICCL”).

29. Ld. Authorized Representative for respondent-assessee submitted that, the CIT(A) correctly deleted the aforesaid disallowance for the reasons set out hereunder.

29.1. Invoices amounting to Rs.1,25,000 issued by M/s Eastern Global Logistics and bill of 29,66,615 issued by Group Gram Panchayat [in the name of SICCL]. Earlier Aamby Valley Project was under SICCL. It was only post demerger that the assessee ie, Aamby Valley Limited was formed and Aamby Valley Project got transferred to it. Some of the parties working for the project from before the demerger date mistakenly issued bills in the name of SICCL: but the bills were related to and in connection with the business of the assessee only and payments for the same are also made by the assessee only. Therefore, considering the submissions of the Appellant, CIT(A) correctly deleted the said disallowance. [PB Page nos. 412-432]

29.2. Invoice amounting to Rs.1,32,500 issued by Markand Gandhi & Co fin the name of assessee The said invoice relates to charges for renewal of trademark Aamby Valley’ and was issued in the name of the assessee only. Therefore, CIT(A) correctly deleted the said disallowance made by AO of Rs. 1,32,500. [PB Page nos. 433-434]

29.3. Invoices amounting to Rs.3,04,524 issued by Smiths Detection Veccone Systems Pvt Ltd [earlier issued in the name SICCL but later corrected to Aamby Valley Ltd). The said invoice was earlier issued in the name of SICCL but it was later corrected to Aamby Valley Ltd. The correction entry was signed by the same person who has signed the invoice. Therefore, the bill was rightly issued in the name of the assessee only and disallowance made by AO was correctly deleted. PB Page nos. 435-436]

29.4. Invoice amounting to Rs.53,068 [issued by Ms Priya Ranade, Advocate in the name of Markand Gandhi & Col Markand Gandhi & Co were the legal consultants of the Appellant who appointed Ms Priya Ranade. Advocate to argue matter in the case of Pramod Pandurang Timblo v. Aamby Valley Limited & Ors before the National Consumer Dispute Redressal Commission. It is a practice that the advocates do not raise bills directly in the name of the client but raise the bill in the name of the advocacy firm who had engaged them. Therefore, CIT(A) has rightly deleted the said disallowance holding that the aforesaid bill, though issued in the name of Markand Gandhi & Co, pertained to services rendered to the assessee for handling legal matters. [PB Page nos. 437-438].

30. From appreciation of record, in light of above said rival arguments reveals that Ld. CIT(A) deleted addition of Rs.35,82,247/- made by ld. AO on account of bills not in name of Company. Ld. CIT(A) on consideration of invoices from Page No.412 to 438 found invoices to be in name of SICCL, assessee or in name of legal consultants of the assessee. The reason for deletion is cogent and sustainable in eyes of law.

30.1 Therefore, ground of appeal No.9 of revenue being devoid of merit is rejected.

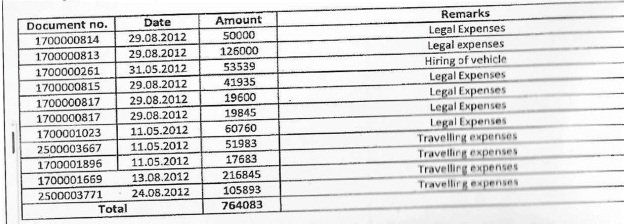

31. Ld. Departmental Representative regarding ground of appeal No.10 of revenue submitted that, the Ld. CIT(A) has erred in deleting the addition of Rs.7,64,083/- made by the AO on account of proper documentary evidence not available. The assessing officer disallowed expenses totaling to Rs.7,64,083 observing that no proper documentary evidence was available for these expenses and therefore, the same may not have been incurred for the purpose of business.

32 Ld. Authorized Representative for respondent-assessee submitted that, Ld. CIT(A) deleted the said disallowance made by the AO after considering the invoices produced during 1 appellate proceedings.

32.1. The snapshot showing the nature of expense incurred is as under:

32.2 . Copy of invoices issued by parties in respect of expenditure incurred is @ page no.439-471 of the paper book on merits.

33. Record apparently shows that Ld. CIT(A), disallowance made by Ld. AO after consideration invoices produced during appellate proceedings which are at page Nos. 439-471 of paper book on merits. Therefore, the deletion of Rs.7,64,083/- was legally deleted.

33.1. Ground of appeal No.10 of revenue being devoid of merit is rejected.

34. Ld. Departmental Representative regarding ground of appeal No.11 of revenue submitted that, the Ld. CIT(A) has erred in deleting the addition of Rs.3,50,000/- made by the AO on account of expenditure not incurred wholly and exclusively for business purpose.

34.1. The said ground has wrongly been raised in as much as, CIT(A) has upheld the disallowance. Kindly refer Ground of Appeal No.5 of chart of issued in Assessee’s Appeal.

35. In view of submission of Ld. Departmental Representative ground of appeal No.11 of revenue is rejected as un-pressed.

36. Ld. Departmental Representative regarding ground of appeal No.12 of revenue submitted that, the Ld. CIT(A) has erred in deleting the addition of Rs.4,12,528/- made by the AO on account of non-deduction of TDS. Assessing Officer disallowed an amount of Rs.69,12,872 under section 40(a)(ia) of the Act on account of non-deduction of tax at source before making payments. The said amount comprises of the following:

| S No. |

Payments made to |

Nature of transaction |

Amount (in Rs.) |

| 1 |

Daimler Financial Services India Pvt. Ltd. |

Interest on vehicle loan taken |

46,39,828 |

| 2 |

ICICI Bank |

Interest on vehicle loan taken |

3,88,854 |

| 3 |

Union Capital Services Ltd. |

Professional fee for valuation of properties |

4,49,440 |

| 4 |

Kathan Mediatix India Ltd. |

Durga Puja Panda |

3,35,000 |

| 5 |

Sahara Hospitality Ltd |

Food, drinks, lounge charges |

4,12,528 |

| 6 |

Sahara Hospitality Ltd. |

Reimbursement of salary bills of Sh. Raquel Sanchez |

|

|

Total |

69,12,872 |

37. Ld. Authorized Representative for respondent-assessee submitted that, while the CIT(A) upheld disallowance mentioned at S.Nos. 1 to 3 & 6.

37.1. With regard to payments of Rs.4,12,528 to Sahara Hospitality Ltd for Food, drinks lounge charges, CIT(A) deleted said disallowance on the ground that no TDS was required to be deducted on such payments. In absence of any provision in Chapter VII-B covering such payments, it is submitted that the CIT(A) has correctly deleted the disallowance.

38. From record, it is evident that, Ld. CIT(A) deleted addition of Rs.4,12,528/-made by AO on account of non-deduction of TDS. Ld. CIT(A) deleted disallowance on the ground that no TDS was required to be deducted. In view of provisions in Chapter VII-B covering such payments, the disallowance is legal.

38.1. The ground of appeal No. 12 of revenue being devoid of merit is rejected.

39. Ld. Departmental Representative regarding ground of appeal No.13 of revenue submitted that, the Ld. CIT(A) has erred in deleting the addition of Rs.3,08,144/- made by the AO on account of long outstanding Imprest. The AO made addition of Rs.3,08,144 being notional interest calculated @ 12% of aforesaid imprest advance amount of Rs.25,67,864/- which has not been cleared during the year.

40. Ld. Authorized Representative for respondent-assessee submitted that, the issue stands covered by the decision of this Hon’ble Tribunal in the Appellant’ own case for AY 2012-13 (supra) wherein similar addition made by AO, considering similar imprest advances, was deleted.

40.1. Revenue’s appeal against the aforesaid decision has been dismissed by the Delhi High Court in ITA849/2019 vide order dated 19.07.2024.

40.2. Further, it is submitted that interest amount alleged by AO has neither been received nor is due to be received; it is not open for the AO to bring to tax notional/ hypothetical income. Reliance is placed on the following decisions wherein it has been categorically held that income tax cannot be levied on hypothetical/ notional income:

– Godhra Electricity Co. Ltd. (supra)

– Excel Industries Ltd. (supra)

– Shoorji Vallabhdas & Co. (supra)

– Airport Authority of India (supra)

41. From perusal of record shows, that Ld. CIT(A), deleted addition of Rs.3,08,144/- on account of long outstanding Imprest. The issue is covered by decision of coordinate Bench in assessee’s own case for year 2012-13.

41.1. Therefore, ground of appeal No.13 of revenue being untenable is rejected.

42. In the result, the appeal of revenue is dismissed.

43. In assessee’s appeal, Ld. Authorized Representative for appellant submitted that Grounds of appeal No.1 & 2 are regarding non-consideration of the revised computation filed by the appellant during the course of assessment proceedings showing a loss of Rs.58,49,38,385/-, and learned CIT(A) has failed to appreciate that the appellant has right to make a legal claim during the course of appellate proceedings and, therefore, he is not justified in ignoring the revised computation filed by the appellant withdrawing the amortization of foreign currency, monetary items translation difference amounting to Rs.60,88,89,873/-.

43.1. It is submitted that the lower authorities have erred in not adjudicating the claim made by the Appellant by way of revised computation of income.

43.2. It is respectfully submitted that the decision of the Supreme Court in the case of Goetze (India) Ltd. (supra) only deals with the power of the assessing officer to admit a claim, which was not raised in the return of income but does not impinge on the power of the appellate authority to entertain additional claims. This position has been upheld by the Supreme Court in the case of National Thermal Power Co. Ltd. v. CIT (SC)/[1998] 229 ITR 383 (SC) and Jute Corpn. of India Ltd. v. CIT (SC)/[1991] 187 ITR 688 (SC).

43.3. Further reliance is placed on the decision of Calcutta High Court in the case of Pr. CIT v. Ankit Metal & Power Ltd. (Calcutta)/[2019] 416 ITR 591 (Calcutta) wherein the assessee had filed original return of income treating the interest subsidy as revenue receipt and thereafter during the assessment proceedings, filed revised computation of income claiming interest subsidy as capital receipt. The assessing officer had denied the aforesaid claim. On appeal, Tribunal allowed the claim of the assessee to treat subsidy as capital receipt. In this regard, the Hon’ble High Court held as under:

“28. The third issue involve in the instant appeal which requires adjudication is whether the action of Tribunal entertaining/allowing the claim which was made by the assessee before the Assessing Officer by filing a revised computation instead of filing a revised return since the time to file the revised return was lapsed, for claiming to treat the incentive subsidies in question as capital receipts instead of revenue receipts as claimed in original return. The Assessing Officer had denied this claim. Revenue has attacked the order of the tribunal by relying on the decision in the case of Goetze (India) Ltd. (supra).

29. This case does not help the revenue/appellant. In this case Supreme Court has made it clear that its decision was restricted to the power of the Assessing authority to entertain a claim for deduction otherwise than by a revised return, and did not impinge on the power of the Appellate Tribunal under Section 254 of the Income Tax Act, 1961. The Hon’ble Supreme Court in the said decision held as follows:

“….In the circumstances of the case, we dismiss the Civil Appeal. However, we make it clear that the issue in this case is limited to the power of the Assessing Authority and does not impinge on the power of the Income Tax Appellate Tribunal under Section 254 of the Income Tax Act, 1961.”

29.1 This judgment was followed by our Court in the case of Britannia Industries Ltd. (supra) holding that Tribunal has the power to entertain the claim of deduction not claimed before the Assessing Officer by filing revised return. Respectfully following the aforesaid decision as well as the view already taken by us in this case that the aforesaid subsidies are capital receipt and not an ‘income’ and not liable to Tax Tribunal in exercise of its power under Section 254 of the Income Tax Act justified this claim though no revised return under Section 139 (5) of the Act was filed before the Assessing Officer. We answer both the question Nos, land 2 in negative and in favour of assessee. “

(emphasis supplied)

43.4. Reliance in this regard is placed on the following decisions wherein the Courts and various Benches of the Tribunal have consistently held that there is no bar/ prohibition on the jurisdiction of an authority (other than the assessing officer) to consider fresh claim(s) made by the Appellant by way of revised computation:

– CIT v. Jai Parabolic Springs Ltd. (Delhi)

– CIT v. Sam Global Securities Ltd. (Delhi), SLP dismissed by the Supreme Court vide order dated 04.04.2014

– DIT v. Ajay G. Piramal Foundation (Delhi)

– Raghavan Nair v. Asstt. CIT, Circle-2(1) (Kerala)

– RachnaS. Talreja v. Dy. CIT (Mumbai).

The CIT(A), was thus, duty bound to consider the claim made by the Appellant by way of revised computation of income and render findings on merits of the claim.

43.5. The Appellant advanced loan to its wholly owned foreign subsidiary, viz., Aamby Valley Mauritius Ltd (“AVML”) during the preceding AY 2011-12 which was outstanding during the captioned AY. Copy of Loan agreement dated 13.12.2010 entered between the assessee and Aamby Valley Mauritius Ltd and addendum to the said loan agreement is @ page nos. 472-500 of the paper book volume 2. The said loan was shown as an Asset’ under the head “Long term Loans and Advances” in the financial statements of the Appellant. Further, the loan was provided in foreign currency and repayment of the said loan by AVML was also to take place in foreign currency. Copy of financial statements of the Appellant for AY 2013-14 is @ page nos. 1-40 of the paper book.

43.6. In connection with the above transactions with AVML, there was foreign exchange gain/ loss arising to the Appellant on restatement of the loan on each balance sheet date. Hence, the Appellant revised value of the said loan in its balance sheet on account of any gain/ loss arising or accrued on forex fluctuations. The accounting treatment followed by the Appellant for forex fluctuation gain/ loss was in accordance with the provisions of AS-11 “The Effects of Changes in Foreign Exchange Rates” Copy of AS 11 is @ page nos. 46-59 of the paper book.

43.7. Para 46A of AS-11 specifies that in case of a long-term foreign currency monetary item relating to acquisition of a depreciable capital asset, any gain or loss arising on account of forex fluctuation is to be added to or deducted from the cost of the asset. Further, it is specified that in other cases, any exchange differences arising on reporting of long-term foreign currency monetary items can be accumulated in a “Foreign Currency Monetary Item Translation Difference Account” (“FCMITD Account”) in the financial statements and amortized over the balance period of such long-term asset or liability. The relevant extracts of AS 11 are reproduced hereunder:-

“Accounting Standard (AS) 11

The Effects of Changes in Foreign Exchange Rates

……………….

46. In respect of accounting periods commencing on or after 7th December, 2006 and ending on or before 31st March, 2010, at the option of the enterprise (such option to be irrevocable and to be exercised retrospectively for such accounting period, from the date this transitional provision comes into force or the first date on which the concerned foreign currency monetary item is acquired, whichever is later, and applied to all such foreign currency monetary items), exchange differences arising on reporting of long-term foreign currency monetary items at rates different from those at which they were initially recorded during the period, or reported in previous financial statements, in so far as they relate to the acquisition of a depreciable capital asset, can be added to or deducted from the cost of the asset and shall be depreciated over the balance life of the asset, and in other cases, can be accumulated in a “Foreign Currency Monetary liem Translation Difference Account in the enterprise’s financial statements and amortized over the balance period of such long-term asset/liability but not bevond 31st March, 202011, by recognition as income or expense in each of such periods, with the exception of exchange differences dealt with in accordance with paragraph 15. For the purposes of exercise of this option, an asset or liability shall be designated as a long term foreign currency monetary item, if the asset or liability is expressed in a foreign currency and has a term of 12 months or more at the date of origination of the asset or liability. Any difference pertaining to accounting periods which commenced on or after 7th December, 2006, previously recognized in the profit and loss account before the exercise of the option shall be reversed in so far as it relates to the acquisition of a depreciable capital asset by addition or deduction from the cost of the asset and in other cases by transfer to “Foreign Currency Monetary Item Translation Difference Account” in both cases, by debit or credit, as the case may be, to the general reserve. If the option stated in this paragraph is exercised. disclosure shall be made of the fact of such exercise of such option and of the amount remaining to be amortized in the financial statements of the period in which such option is exercised and in every subsequent period so long as any exchange difference remains unamortized.

46A (1) In respect of accounting periods commencing on or after the 1st April, 2011, for an enterprise which had earlier exercised the option under paragraph 46 and at the option of any other enterprise (such option to be irrevocable and to be applied to all such foreign currency monetary items), the exchange differences arising on reporting of long term foreign currency monetary items at rates different from those at which they were initially recorded during the period, or reported in previous financial statements, in so far as they relate to the acquisition of a depreciable capital asset, can be added to or deducted from the cost of the asset and shall be depreciated over the balance life of the asset, and in other cases, can be accumulated in a “Foreign Currency Monetary Item Translation Difference Account” in the enterprise’s financial statements and amortized over the balance period of such long term asset or liability, by recognition as income or expense in each of such periods, with the exception of exchange differences dealt with in accordance with the provisions of paragraph 15 of the said rules.

2) To exercise the option referred to in sub-paragraph (1), an asset or liability shall be designated as a long-term foreign currency monetary item, if the asset or liability is expressed in a foreign currency and has a term of twelve months or more at the date of origination of the asset or the liability

(emphasis supplied)

43.8. Thus, taking into consideration the above provisions of the AS-11, the loan given by the Appellant for a period of more than 12 months qualifies as long-term foreign currency monetary item. The Appellant has capitalized the forex gain of Rs 25,56,33,000 arising on account of exchange difference as on balance sheet date and credited the same to FCMITD Account appearing under the head reserves & surplus during the year under consideration. No dispute has been raised by the AO regarding the same. The FCMITD Account had an opening balance of Rs.507,75,75,010. The Appellant has amortized Rs.60,88,89,873 and transferred the same to P&L A/c so as to give effect to the provisions of AS-11.

43.9. The Appellant submits that the amount amortized and credited to P&L A/c will not be chargeable to tax for the reasons submitted hereunder.

43.10. In this regard, it is submitted that the Appellant had loaned funds to its wholly owned subsidiary, AVML with the primary intention of assisting its subsidiary in expansion of business activities. With such assistance, AVML will be in a position to earn more profits and since the Appellant is 100% holding company, it would have also benefited from the same. It is thus, submitted that the said loan given by the Appellant to its subsidiary is of capital nature.

43.11 Further, as per the loan agreement, it was agreed between the parties that the outstanding loan can be converted to preferential shares on mutually agreed terms and conditions, at any time before expiry of the loan period.

43.12. In view of the above, it is submitted that the loan given by the Appellant was on capital account. As a corollary, foreign exchange gain on account of fluctuation in the exchange rates would also be treated as capital accretion/gain.

43.13. Reference in this regard is made to the decision passed by this Hon’ble Tribunal in the Appellant’s own case for AY 2012-13 reported as Aamby Valley Ltd. v. Asstt. CIT (Delhi – Trib.) wherein this very loan provided by the Appellant to AVML was held to be in the nature of capital asset and further, fluctuation gain to be on account of capital accretion. Relevant extracts of the order are reproduced hereunder:

5. On this ground, assessee was show cause on perusal of the balance-sheet, it was observed that the Company has opening balance of Rs.91,17,97,139/- on account of foreign currency monetary item transaction reserve wherein additions has been made during the year amounting to Rs.483,64,47,400/- from foreign currency monetary item transaction whereas the Company has amortized to the extent of Rs.67,06,69,129/- and offered the same for

8. We have considered the rival submissions. The Hon’ble Supreme Court in the case of Sutlej Cotton Mills Ltd. (supra) has held that any foreign exchange gain or loss on capital asset will be adjusted with the value of such asset. It was further held that “The law may, therefore, now be taken to be well settled that where profit or loss arises to an assessee on account of appreciation or depreciation in the value of foreign currency held by it, on conversion into another currency, such profit or loss would ordinarily be trading profit or loss if the foreign currency is held by the assessee on revenue account or as a trading asset or as part of circulating capital embarked in the business. But, if on the other hand, the foreign currency is held as a capital asset or as fixed capital, such profit or loss would be of capital nature.”

8.1 In the present case, assessee has entered into the loan agreement with its subsidiary AVML of which assessee is 100% holding company. The loan was given for a particular period, subject to interest. It was further extended by an Addendum Agreement Dated 14.12.2011 and loan was subject to reduced interest for longer period. The assessee, therefore, has landed its funds to its subsidiary with a primary intention of assisting its subsidiary in its expansion of business activities. The assessee, therefore, rightly contended that with such assistance, subsidiary will be in a position to earn more profits and since the assessee is its 100% holding company, the assessee would be benefitted and can earn higher profits from its subsidiary as well It is, therefore, clear that the said loan advance is in the nature of investment by assessee in its subsidiary company and thus, it was of capital nature. The assessee further explained that as per the loan agreement, it was agreed between the parties that the outstanding loan may be converted into preferential shares on mutually agreed terms and conditions between the parties at any time or before expiry of the Loan terms. Thus, these facts clearly prove that the loan was of capital in nature and as such, it would not prove that loan advanced was connected with any revenue item. Therefore, the loan given to AVML is a capital asset which helps in earning incidental interest income, which is also offered for taxation. Since the loan advanced was its long term asset ie., on account of capital asset and not as part of circulating capital, therefore, foreign fluctuation gain on account of alteration in the rates of exchange would be a capital accretion. The loan is shown as asset under the Head “Long Term Loan and Advance” in accounts. The assessee, thus, rightly followed Accounting Standard-11 as explained above Hence, the loan given by the assessee being a capital asset of the assessee, any loss/gain on account of forex was to be added/subtracted to the loan. Thus, there was no justification for the authorities below to make the addition. The case law relied upon by the Learned Counsel for the Assessee squarely apply to the facts and circumstances of the case. There was, thus, no justification for the authorities below to make the addition against the assessee. We, accordingly, set aside the Orders of the authorities below and delete the entire addition. The Ground No.6 of appeal of assessee is allowed. It may also be stated here that assessee has also raised Additional Ground of Appeal Dated 08.10.2018 connected with this ground amounting to Rs.67,06,69,129/- already amortized and offered to tax. Since we have allowed this ground of appeal of assessee, therefore, there is no need to adjudicate separately on the additional ground of appeal. A.O. is directed to take into consideration findings on this issue while giving effect to the appellate order. Additional Ground of Appeal is also disposed off accordingly.

43.14. Revenue’s appeal against the aforesaid order has been dismissed by the Hon’ble Delhi High Court in ITA 849/2019. vide order dated 19.07.2024.

43.15. Thus, there is no dispute that the loan given by the Appellant to AVML was on capital account. Any gain/ loss on account of forex was to be added/ subtracted to the loan and could not be bought to tax as income. As regards taxability of the amount amortized from foreign exchange gain, the same is only an accounting entry as per requirement of Accounting Standards, which have to be mandatorily followed by the Appellant. The same is, however, beyond the scope of Income as the same is of capital nature.

43.16. In this regard, reliance is placed on the decision of the Supreme Court in the case of Sutlej Cotton Mills Ltd. v. CIT [1979] 116 ITR 1 (SC) wherein it was held that any gain/ loss arising due to foreign exchange fluctuation would be of capital nature if foreign currency is held as a capital asset or as fixed capital. Relevant extracts of the decision are reproduced hereunder:

“The law may, therefore, now he taken to be well settled that where profit or loss arises to an assessee on account of appreciation or depreciation in the value of foreign currency held by it. on conversion into another currency, such profit or loss would ordinarily be trading profit or loss if the foreign currency is held by the assessee on revenue account or as a trading asset or as part of circulating capital embarked in the business. But, if on the other hand, the foreign currency is held as a capital asset or as fixed capital, such profit or loss would be of capital nature.”

43.17. Kind attention is further drawn to the decision of Supreme Court in the case of CIT v. Woodward Governor India (P.) Ltd. (SC)/[2009] 312 ITR 254 (SC), wherein the issued involved was in respect of allowability of forex loss on revenue item. It was held by the apex Court that loss due to foreign exchange fluctuation, which is on revenue account, would be allowed as business expenditure under section 37(1) of the Act.

43.18. Therefore, in view of the above, it is submitted that the foreign fluctuation gain arising to the Appellant on the capital loan is in the nature of capital gain and therefore same will not be chargeable to tax.

43.19. Reliance is also placed on the decision of Mumbai bench of the Tribunal in the case of Aditya Balkrishna Shroff v. ITO (Mumbai – Trib.)/[2021] 189 ITD 587 (Mumbai – Trib.) wherein loan was given by the assessee to his cousin in Singapore on capital account in US dollars. It was held that foreign exchange fluctuation gain due to increase in the value of US dollars is also in the nature of capital receipt and hence, not chargeable to tax.

43.20. Even otherwise, it is submitted that during AY 2014-15, the Appellant had earned forex gain amounting to Rs.858,91,61,000 on account of foreign exchange fluctuation. The Appellant had, similar to the captioned AY, credited the amortization amount of Rs. 171,58,96,852 to the profit and loss account. Thereafter, considering that same is on capital account and not taxable, the Appellant had reduced the amount from computation of income while calculating taxable income. In the assessment order passed for AY 2014-15, there is no addition made by the assessing officer in this regard. The assessing officer, thus, has duly accepted that the forex gain amortized and credited to P&L account from FCMITD Account was not taxable, being capital receipt.

43.21. Similarly, in AYs 2015-16 & 2016-17, deduction claimed in respect of amortized amount of forex gain was accepted and allowed by the AO in the assessment order. Copy of the assessment orders for AYs 2014-15 to 2016-17 is @ pages 501-600 of paper book volume 2.

43.22. In light of the aforesaid, it is submitted that the aforesaid additional claim filed by the Appellant by way of revised computation deserves to be allowed .

44. Ld. Departmental Representative submitted that revised computation was rejected by Ld. CIT(A).

45. From examination of record, in light of aforesaid rival submissions, it is apparent on record that, Ld. CIT(A) failed to consider revised computation filed by assessee showing losses. Revised computation filed by the assessee showed withdrawing of embolization of foreign currency, monetary items and translation differences. Therefore, the matter is restored to the file of Ld. AO for fresh adjudication in accordance with law, after affording fair opportunity of hearing to the assessee.

46. Ld. Authorized Representative for appellant-assessee regarding ground of appeal No.3 of assessee submitted that, the Ld. CIT(A) has erred in law and on facts and circumstances of the case in confirming the disallowance of Rs.28,18,308/- out of Advertisement, Sales Promotion and Business Promotion Expenses.

46.1. During the year under consideration, the Appellant had incurred expenditure on account of advertisement sales promotion and business promotion expenses, qua which deduction was claimed in the return of income filed.

The AO disallowed an amount of Rs.38,42,839 out of the total expenditure, as computed hereunder:-

| S. No. |

Vendor |

Amount claimed as expense |

Amount disallowed |

Reason for disallowance |

| 1. |

Allied Media Networks (P.) Ltd. |

Rs.67,28,685 |

Ad-hoc disallowance of 50%, i.e., Rs.33,64,343 |

Vouchers submitted by Appellant are not properly supported and reason for incurring such huge expense not given. |

| 2. |

International Property Media Ltd. |

Rs.4,78,550 |

Rs.4,78,550 |

Voucher not properly supported and nexus between the business of Appellant and expense was not established. |

| TOTAL |

38,42,893 |

|

CIT(A) enhanced the aforesaid amount of disallowance from Rs.38,42,893 to Rs. 44,69,510. The disallowance sustained/ made by the CIT(A), which form subject matter of appeal filed by the Appellant before the Hon’ble Tribunal, are tabulated hereunder:

| S. No. |

Vendor |

Amount claimed as expense |

Amount disallowed |

Reason for disallowance |

| 1. |

Allied Media Networks (P.) Ltd. |

Rs. 1,70,000/- |

Rs. 1,70,000/- |

CIT(A) considering that advertisement in newspaper was issued in January 2012, held the same to be prior period expenses and directed that the same may be allowed in AY 2012-13. |

| 2. |

Allied Media Networks (P.) Ltd. |

23,34,205 [Para 10.3(B), Clauses (a) to (j) except (c) of CIT(A) order] |

50%, i.e., 11,67,103 |

CIT(A), after verification of bills, noted that the same were issued in the of Aamby Valley City Developers Ltd. and not the Appellant, upheld the action of AO to disallow 50% of the said expense on ad-hoc basis. |

| 3. |

Allied Media Networks (P.) Ltd. |

31,32,411 |

31,32,411 |

CIT(A), noting that the invoice is dated 25.05.2013 and release of advertisements were from 03.04.2013 to 06.04.2013, held that the expense pertains to AY 2014-15; not to be allowed in the captioned AY. (Refer PB Page nos. 118-119) |

| TOTAL |

|

|

44,69,510 |

|

CIT(A), accordingly, enhanced the disallowance from Rs.38,42,893 to Rs.44,69,510.

46.2. For the disallowance of Rs.1,70,000, the CIT(A) failed to consider the fact that the bill dated 10.02.2012 was received by the Appellant in FY 2012-13 i.e., during the year under consideration and therefore, ought to be allowed in the captioned AY.

46.3. For the disallowance amounting to Rs. 11,67,103 i.e., 50% of the expenses for which bills were in the name of ‘Aamby Valley City Developers Ltd., it is respectfully submitted that there is no such entity in the name of Aamby Valley City Developers Ltd. Rather the bills pertain to the Appellant itself. Further, it is submitted that the assessee is carrying on business of large magnitude and the allegation that it has indulged in booking expenses of such a small amount in the name of other entity is highly arbitrary and without logic.

46.4. Even otherwise, assessing officer had made ad hoc disallowance of 50% of the expenses which is not permissible in law. In this regard attention is drawn to the catena of decisions wherein the Courts and various benches of the Tribunal across the Country, have repeatedly held that there is no scope for making any ad hoc disallowance on mere estimation/ guess work.

– J.JEnterprises v. CIT (SC)

– FriendsClearing Agency (P.) Ltd. v. CIT-II (Delhi)

– DwarkaProsad Agarwal v. ITO [1995] 52 ITD 239/51 TTJ 588 (Calcutta)

– MahendraOil Cake Industries Pvt. Ltd. v. Asstt. CIT [1996] 55 TTJ 711 (Ahmedabad – ITAT),

– RattahMechanical Works Ltd. v. ITO (Chandigarh)(Mag)

46.5. For the disallowance of Rs.31,32,411, the allegation of the CIT(A) is that invoices pertain to AY 2014-15 and therefore, cannot be allowed in the captioned AY. In this regard, it is submitted that if the same cannot be allowed in the captioned AY, the Hon’ble Tribunal may kindly direct that the same be allowed as expenditure in AY 2014-15 itself. Copy of vouchers, invoices and other supporting documents are enclosed in merits paper book @ page number 60-135.

47. Ld. Departmental Representative submitted that, Ld. AO disallowed expenditure due to the extent of 50% as vouchers submitted by appellant were not properly supported. Ld. CIT(A) enhanced amount of disallowance from Rs.38,42,893/- to Rs.44,69,510/-. Vouchers regarding advertisement in newspaper bills etc. filed by the assessee were considered. Copy of vouchers, invoices and other supporting documents are enclosed in merits paper book @ page number 60-135.

47.1. Therefore, the matter is required to be verified by Ld. AO. Accordingly, ground of appeal No.3 is allowed for statistical purposes.

48. Ld. Authorized Representative for appellant-assessee regarding grounds of appeal No.4 of the assessee submitted that, the learned CIT(A) is not justified in confirming the disallowance to the extent of Rs.12,30,900 out of Consultancy Charges incurred by the appellant.

48.1. As regards the payment of Rs.5,25,000/- to Shri Alok Saigal. He is a Consultant who was appointed for carrying on interior decoration work for the Appellant company.

48.2. As regards payment of Rs.4,75,000/-, the same relates to payment to Sri Sham S. Sharma who is also a construction consultant, working for the assessee company. He is giving consultancy in day to day construction work and construction related activities of the Appellant. The amount paid is less than what is stipulated in the agreement; no disallowance is called for.

48.3. As regards payment of Rs.2,30,900/- to Sahara International Airport Private Limited, the same is a reimbursement of expenditure made as they had made payment to ‘Air One Consultancy Servies on behalf of the Appellant. Air One Consultancy Services are providing consultancy in respect of Airport and Helipad, which is existing in Aamby Valley City. In appeal for AY 2012-13, this issue has been remanded back to the AO.

49. Ld. Departmental Representative submitted that, Ld. AO disallowed consultancy charges on account of absence of supporting justification by the assessee.

50. From appraisal of record, in light of above said submissions it is evident that, Ld. CIT(A) confirmed disallowance to the extent of Rs.12,30,900/- out of consultancy charges. Appellant assessee has disputed amounts paid to Sh. Alok Saigal, Sh. Sham S. Sharma and to Sahara International Airport Private Limited and has requested that the matter be restore to the file of Ld. AO.

50.1. In view of above material facts, in interest of justice, it is expedient to remit the matter to the file of Ld. AO for fresh decision in accordance with law after affording fair opportunity of hearing to the assessee.

50.2. Accordingly, ground of appeal No.4 is allowed for statistical purposes.

51. Ld. Authorized Representative for appellant-assessee regarding grounds of appeal No.5 of the assessee submitted that, the learned CIT(A) is not justified in confirming the disallowance of Rs.3,50,000 out of Advertisement Expenses by holding that the same has not been only and exclusively incurred for the business of the appellant.

51.1. Main project of the Appellant is development of Aambay Valley City which is situated in a valley about 20 kms away from Lokhandwala. The entire city is surrounded by forests and various types of permissions have to be taken from the Forest Department for carrying out day to day activities of development in the Lake City and for the purpose of sommoth running of the business of the Appellant.

51.2. In view of above, an expenditure incurred for birthday greetings of Forest Minister who is not a related party, cannot be said to be not incurred for the purpose of the business of the Appellant. Copy of invoice dated 07.01.2013 is @ page no. 161 of the paper book.

52. Ld. Departmental Representative submitted that, Ld. AO disallowed Rs.3,50,000/- out of advertisement expenses as there was no nexus between expenses incurred and the business of the appellant.

53. From the examination of record, in light of aforesaid rival contention, it is crystal clear that, Ld. CIT(A) confirmed disallowance of Rs.3,50,000/- out of advertisement expenses by holding that there was no nexus between expenses incurred and business of assessee. It is a fact that Dr. Patang Rao had nothing to do with the business of assessee. Therefore, the confirmation of disallowance of Rs.3,50,000/- out of advertisement expenses by Ld. CIT(A) is upheld.

53.1. Ground of appeal No.5 of assessee is rejected.

54. Ld. Authorized Representative for appellant-assessee regarding grounds of appeal No.6 of the assessee submitted that, the learned CIT(A) is not the justified in confirming disallowance of Rs.61,65,344/-under section 40(a)(ia) of the IT Act, 1961 for alleged non-deduction of tax at source, in spite of the fact, that the deductee had filed copy of certificate in Form 26A of the Income Tax Rules, 1962.

54.1. For disallowance of Rs. 46,39,828, it is respectfully submitted that the Appellant had duly filed certificate in Form No.26A to show that Daimler Financial Services India Ltd. has already paid taxes on such payments.

54.2. In this regard, section 40(a)(ia) states that where the assessee fails to deduct the whole or any part of the tax on any sum but is not deemed to be an assessee in default in terms of first proviso to sub-section (1) of section 201 of the Act, it shall be deemed that the assessee had deducted and paid the tax on such sum on the date of furnishing return of income.

First proviso to sub-section (1) of section 201 of the Act reads as under:

“Provided that any person, including the principal officer of a company, who fails to deduct the whole or any part of the tax in accordance with the provisions of this Chapter on the sum paid to a payee or on the sum credited to the account of a payee shall not be deemed to be an assessee in default in respect of such tax if such pave-

(i) has furnished his return of income under section 139

(ii) has taken into account such sum for computing income in such return of income, and

(iii) has paid the tax due on the income declared by him in such return of income.

54.3. ICICI Bank Rs.3,88,854

The assessing officer disallowed the expense of Rs.3,88,384 paid to ICICI Bank towards interest on vehicle loan taken under section 40(a)(ia) for non-deduction of tax at source. CIT(A) confirmed the same without giving any finding or observation, which is not correct in law and deserves to be deleted. Further, there is no liability in the hands of the Appellant to deduct TDS on payment made to ICICI Bank towards interest on loan.

In this regard, section 194A contains provisions for liability to deduct tax in case of interest other than ‘interest on securities. Clause (iii) of sub-section (3) of section 194A clearly specifies that ‘where any such income is credited or paid to any banking institution to which the Banking Regulation Act, 1948 applies, no tax has to be deducted’. The Relevant extracts of Section 194A of the Act is reproduced hereunder:

Interest other than “Interest on securities”.

194A. (1) Any person, not being an individual or a Hindu undivided family, who is responsible for paving to a resident any income by way of interest other than income by way of interest on securities, shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct income-tax thereon at the rates in force:

………………….

(3) The provisions of sub-section (1) shall not apply

………………….

(iii) to such income credited or paid to

(a) any banking company to which the Banking Regulation Act, 1949 (10 of 1949), applies, or any co-operative society engaged in carrying on the business of banking (including a co-operative land mortgage bank), or

…………..

(emphasis supplied)

As per the above provisions, it is submitted that the payment made by the Appellant to the ICICI Bank which is regulated by the Banking Regulations Act, 1949 is duly covered by the clause (iii) of sub-section (3) to section 194A of the Act and therefore there is no liability in the hands of the Appellant to deduet TDS on the same. In this regard, the disallowance made by the AO and CIT(A) for non-deduction of TDS is not sustainable and deserves to be deleted.

54.4. Unicorn Capital Services Ltd. – Rs.4,49,440

For disallowance of Rs.4,49,440, it is respectfully submitted that the assessee had duly deducted TDS under section 194J of the Act on payment made to Unicorn Capital Services Ltd. towards professional services taken. The said deduction of TDS is evident from Form 16A which finds place @ Page Nos. 256-257 of the paper book. Therefore, the said disallowance deserves to be deleted.

54.5. Katha Mediatix India Ltd. – Rs.3,35,000

The disallowance made by AO of Rs.3,35,000 was deleted by CIT(A) holding that TDS had been duly deducted by the Appellant and the same is not pressed by the Department.

54.6. Sahara Hospitality Ltd. – Rs.4,12,528

For the expense of Rs.4,12,528 paid to Sahara Hospitality Ltd. towards food, drinks, lounge charged etc, CIT(A) deleted the disallowance made by AO holding that there is no requirement to deduct TDS on these payments.

54.7. Sahara Hospitality Ltd. – Rs.6,87,222

In respect of the disallowance of Rs.6,87,222 being reimbursement of salary bills of Raquel Sanchez, it is submitted that while making payment to Raquel Sanchez, TDS was duly deducted by Sahara Hospitality Ltd. under section 194J of the Act. In this regard Form no. 16A, evidencing that TDS was duly deducted by Sahara Hospitality Ltd., finds place @ page nos. 262-265 of the paper book. Therefore, no disallowance can be made for the non-deduction of TDS in the hands of the Appellant as the same constitutes reimbursement of expenses to Sahara Hospitality Ltd. without any element of income embedded therein.

55. Ld. Departmental Representative submitted that, Ld. AO had disallowed amount of Rs.69,12,872/- on account of non-deduction of tax at source. Ld. CIT(A) confirmed disallowance of Rs.46,39,828/-. The matter is restored to be sent to the file of Ld. AO for verification.

56. From examination of record, in light of aforesaid rival contention, it is crystal clear that, Ld. CIT(A) confirmed disallowance of Rs.46,39,828/-, Rs.4,49,440/-, Rs.6,87,222/- and deleted other additions. The matter is required to be verified by AO. Therefore, the matter is restored to the file of Ld. AO. Ground of Appeal No.6 of the assessee is allowed for statistical purposes.

57. Ld. Authorized Representative for appellant-assessee qua of ground of appeal No.7 submitted that, the learned CIT(A) has erred in law and on facts and circumstances of the case in confirming the disallowance of Rs.7,02,800/- on account of Commission and Brokerage Expenses incurred for procurement of residential accommodation for employee.

57.1. That during the assessment proceedings, the Appellant had duly submitted the complete details of the persons to whom brokerage is paid along with their PANs, details of the flat taken on rent for which brokerage is paid, etc. Further, the Appellant had duly deducted TDS under section 194H of the Act before making payment towards brokerage commission charges.

57.2 It is submitted that the expenditure incurred towards commission/ brokerage charges paid for residential accommodation of the employees is directly incurred for the purpose of the business of the Appellant as these charges are essential to facilitate the functioning of the business and ensure the well-being of its employees. Therefore, such expenses qualify as fully allowable deductions under section 37(1) of the Act.

57.3. In this regard, Supreme Court in the case of CIT v. Malayalam Plantations Ltd. [1964] 53 ITR 40 observed that the expression “for the purpose of the business” is wider in scope than the expression “for the purpose of earning profits” and not only the day-to-day running of the business but also many other acts incidental to the carrying on of the business comes under the purview of ‘for the purpose of business.’

57.4. Coming to the facts of our case, reliance is placed on the decision of Kerala High Court in the case of CIT v. Premier Cotton Spg. Mills Ltd. (Kerala)/[1997] 223 ITR 440 (Kerala) wherein assessee had acquired land, divided it into plots and allotted them to its employees. On the said land, assessee had incurred expenditure on laying of roads etc and claimed deduction of the same. The assessing officer disallowed the claim for deduction holding it to be capital expenditure. On appeal, Tribunal allowed the deduction claimed by the assessee. The Hon’ble High Court, in this regard, held as under:

“16. On the facts found by the Tribunal, we are also clearly of the opinion that the expenditure incurred on roads, wells, etc., was only for the benefit of the employees who purchased properties and constructed buildings in it, that this did not bring into existence an enduring advantage for the assessee’s business and that the expenditure being in the nature of a staff welfare expenditure is an expenditure incurred wholly and exclusively for the purposes of the assessee’s business, The Tribunal, according to us, has rightly held that the expenditure is an allowable deduction in the computation of the assessee’s income for the assessment year under consideration.

17. In view of the above, we hold that the expenditure incurred by the assessee is revenue expenditure. The question is answered accordingly in favour of the assessee and against the revenue. “

(emphasis supplied)

57.5. Therefore, in view of the above, the expenditure incurred by the Appellant on account of brokerage commission charges is in the nature of staff welfare expenditure incurred wholly and exclusively for the purpose of Appellant business, allowable under section 37(1) of the Act.

57.6. Details of payment made for commission and brokerage expenses alongwith copy of leave and license agreement is page nos. 268-288 of the paper book.

58. Ld. Departmental Representative submitted that, Ld. CIT(A) considered the rent agreement submitted by the Appellant and observed that these are entered between employees and the owner of the residential properties and the Appellant only pays HRA to its employees. Therefore, CIT(A) confirmed the disallowance made by AO holding that the same cannot be allowed under section 37(1) of the Act.

59. From record, it is amply clear that Ld. AO made addition of Rs.7,02,800/- on account of commission and brokerage expenses incurred for apartment of residential accommodations which were confirmed by Ld. CIT(A). It is a fact that assessee had submitted complete detail of persons to whom brokerage was paid along with their PAN details of flat taken on rent for which brokerage was paid. Appellant had deducted the TDS. Detail of payments along with copy of lease and license agreement are at Page Nos. 268-288 of the paper book. The rejection of commission and brokerage expenses is not just fair and reasonable and is set aside. Ground of appeal No.7 of the assessee is accepted. Addition of Rs.7,02,800/- on account of commission and brokerage expenses is deleted.

60. Ld. Authorized Representative submitted that, the learned CIT(A) has erred in law and on facts and circumstances of the case in confirming the disallowance of Rs.23,01,576/- out of outstanding debts written off during the year.

60.1. The party-wise breakup of bad debts written off amounting to Rs.23,01,756 finds place at page nos. 289-299 of the paper book.

60.2. In this regard, it is submitted that the balances written off related to advances given in the past and it is not a case of applicability of section 36(2)(i) of the Act. Rather, the bad debts written-off deserves to be allowed as business losses.

60.3 Reference, in this regard, is placed on the decision of the Bombay High Court in the case of Harshad J. Choksi v. CIT (Bombay)/[2012] 349 ITR 250 (Bombay), wherein the assessee claimed deduction of advance written off as bad debt under section 36(2) of the Act. The assessing officer rejected the claim of the assessee holding that for claiming deduction under section 36(2), the amount shall be offered to tax in earlier previous years, which finding was affirmed by CIT(A) and Tribunal. The High Court, however, held that even if a deduction is not allowable as bad debt, the Tribunal should have considered the assessee’s claim for deduction as business loss. The relevant extract of the judgement is as under: