ORDER

Ravish Sood, Judicial Member.- The present appeal filed by the assessee is directed against the order passed by the Additional/Joint Commissioner of Income Tax (Appeals), Panchkula, dated 24/01/2025, which in turn arises from the order passed by the Assessing Officer (for short, “AO”) under section 143(3) of the Income Tax Act, 1961 (for short, “the Act”), dated 18/12/2018 for the Assessment Year (AY) 2016-17. The assessee has assailed the impugned order on the following grounds of appeal:

“1. That under the facts and circumstances of the case, orders passed by the Commissioner of Income-tax (Appeals) (in short ‘CIT(A)’)u/s. 250 of IT Act dated 24-01-2025, confirming the order passed by Assessing Officer (‘AO’) u/s. 143(3) of the IT Act dt. 18-12-2018, is not in accordance with the fact and provisions of law.

Without prejudice to the above grounds,

2. Ld.AO, while making an observation in his order stating that assessee declared the capital gains from sale deeds listed in S no 1 to 10 therein, erred in including a document no. 3923/2015 dt.17-08-2016 (listed by him at S.no 10 at pg 2 & 3 of AO order), which sale pertain to the subsequent FY 2016-17 and not the Impugned year being FY 2015-16.

3. Whereas, in fact, after removing the said incorrect document no. 3923/2015dt.17-08-2016 from the list stated by AO and adding the correct Doc no 3495/2015 dt.23-07-2015 (mentioned at S.no 13 by AO in his order), the total amount works out to Rs.56,25,000/- which matches with the total sale consideration declared by assessee in his ITR filed for the impugned FY, considering this, the observation made by Ld.AO stating that assessee failed to declare capital gains pertaining to Document no 3495/2015 dt.23-07-2015(mentioned at S.no 13 by AO in his order) -is factually incorrect.

4. The Learned CIT(A) by virtue of order passed u/s 250 of the IT Act erred in confirming the additions made by Ld. AO towards capital gains in respect of registered sale deed vide document no.2327/2015 dt.22-05-2015, without appreciating the fact that the said transaction of sale had been subject to revision vide Document no. 2361/2015 dt.25-05-2015 which revised deed has been considered while declaring capital gains in the hands of the assessee. On account of this, the addition made by Ld.AO with respect to document no.2327/2015 dt.22-05-2015 resulted in duplicate of income.

5. The Learned CIT(A) by virtue of order passed u/s.250 of the IT Act erred in confirming the additions made by Ld. AO towards capital gains in respect of registered deed vide document no.2360/2015 dt.25-05-2015, without appreciating the fact that the said deed pertain to General power of attorney given by assessee along with 4 other coowners to a person, which does not convey any title to the other party, to fall under the definition of transfer uls 2(47) of the IT Act.

6. Without prejudice to the above ground no 3, even assuming that the said deed conveys title of the property to the buyer, which amounts to transfer u/s 2(47) of the IT Act, what is taxable in the hands of assessee is only 1/5th of the sale consideration, being assessee’s share, after deducting the relevant cost and not the entire amount mentioned in the said deed.

7. For these and such other grounds, that may be urged at the time of hearing of subject appeal, the appellant prays that the order passed by Ld.AO and confirmed Learned CIT(A) is to be set aside and the issues that resulted in addition may please be sent back to the file of Ld. AO for fresh consideration, or provide such other relief as the Hon’ble Tribunal may deem fit.”

2. Succinctly stated, the assessee had filed his return of income for AY 2016-17 on 29/03/2018, declaring an income of Rs.3,94,000/-. Subsequently, the case of the assessee was selected for “limited scrutiny” under CASS for verifying “large cash deposits in bank account” and purchase/sale of one or more properties during the year. Notice under section 143(2) of the Act, dated 13/08/2018 was issued to the assessee.

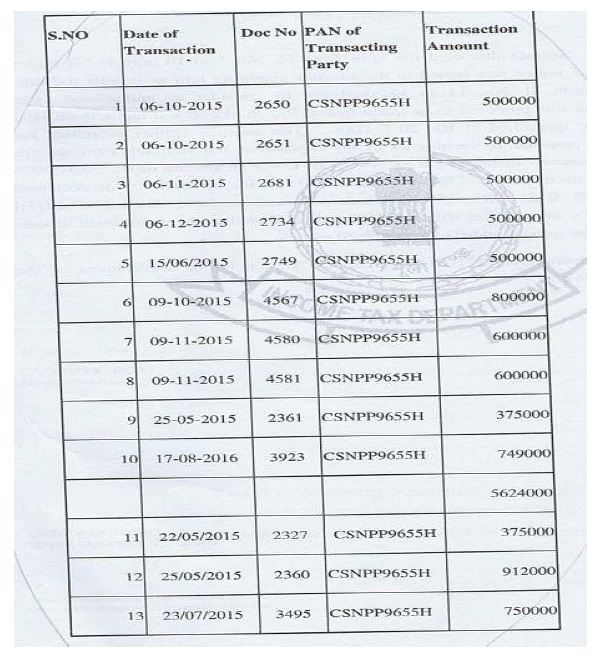

3. During the course of the assessment proceedings, it was observed by the AO that the assessee in the subject year had sold thirteen properties aggregating to an amount of Rs.76,61,000/-, as under:

However, it was observed by him that the assessee had disclosed the sale transactions of only ten properties aggregating to Rs.56,24,000/- in his books of accounts. The AO called upon the assessee to explain as to why the suppressed sale consideration of Rs.20,37,000/- may not be assessee as undisclosed sale proceeds. As the assessee failed to come forth with any explanation, the AO made the addition of the sale consideration of three properties, i.e., Sl No.11 to 13 aggregating to Rs.20,37,000/-.

4. Aggrieved, the assessee carried the matter in appeal before the CIT(A), who after considering the facts available on record took cognizance of the three fold contentions of the assessee, viz., (i) that there was a duplication of addition by the AO with respect to two sale transactions, i.e., Sl. No.11 (original): Rs.3,75,000/- and Sl. No.9 (amended): Rs.3,75,000/-; (ii) sale transaction, i.e., Sl. No.10: Rs.7,49,000/- pertains to succeeding year (though included by the AO) and Sl. No.13: Rs.7,50,000/- pertains to the year under consideration (though not included by the AO); (iii) sale transaction, i.e., Sl. No.12, the assessee was a co-owner with four other parties (1/5th share), set aside the matter to the file of the AO with a direction to verify the factual position and allow the benefit of the same, if found appropriate. For the sake of clarity, we deem it apposite to cull out the observations of the CIT(A), as under:

“7.3 During the course of appeal proceedings, no reply has been filed by the appellant in spite of sufficient opportunities provided as detailed above. I have perused the order of the Assessing Officer and considered the facts of the case. The Assessing Officer has passed a speaking order with detailed discussion on the issue involved therein. The appellant has not pursued the appeal. But the appellant in the Statement of Facts has mentioned that Document No: 2327 (Original) for Rs.375,000/- and document No: 2361 (amended) though represented the same transaction and the A.O considered them as two different transactions and added to the income. Further it has been contended that Document No: 3495 (Original) for Rs. 750,000/- and document No: 3923 (amended in previous year 2016-17) though represented the same transaction and the A.O considered them as two different transactions and added to the income. In view of the above, the AO is directed to verify the contention of the appellant from the related documents and allow the benefit of the same if found appropriate. Therefore, these grounds of appeal are partly allowed for statistical purpose.

7.4 On Ground of Appeal Nos. 3(b):- In this ground of appeal, it is stated that Rs.9,12,000/- was incorrectly added to appellant’s income as it pertains to an A.O.P. in which he is only a member. Despite making this claim, no documentary evidence has been submitted to show the relationship between the assessee and the A.O.P. whereas the property has been registered on the PAN of the appellant as per the assessment order. Since the property has been registered on individual PAN of the appellant, the sale consideration belongs to the appellant if otherwise not proved with evidences. Hence, the addition made by the AO is upheld. Accordingly, this ground of appeal is dismissed.

8. In the result, the appeal is partly allowed.”

5. The assessee, aggrieved with the order of the CIT(A) has carried the matter in appeal before us.

6. We have heard the Learned Authorized Representatives of both parties, perused the orders of the authorities below and the material available on record.

7. Shri Arjun M Solaki, CA, Learned Authorized Representative (for short, “Ld. AR”) for the assessee, at the threshold of hearing of the appeal, submitted that the appeal involved a delay of 191 days. Elaborating on the reasons leading to the delay, the Ld. AR submitted that the same had crept in for the reason that the assessee, an aged person, during the relevant period was suffering with Kidney failure and had been undergoing Dialysis since April, 2024, had thus remained engrossed with his medical issues and hospital visits during the relevant period and could not file the appeal within prescribed time period. The Ld.AR to buttress his contention had taken us through the Medical Certificate/record revealing that the assessee had been undergoing dialysis. The Ld. AR submitted that it was only when the assessee in the last week of September, 2025 was served with a demand notice for penalty levied under section 271(1)(c) of the Act for the subject year that he had gathered about the dismissal of his quantum appeal by the CIT(A). Carrying his contention further, the Ld. AR submitted that the assessee involving no further loss of time had instructed his counsel and preferred the appeal, which by the time involved a delay of 191 days. The Ld. AR submitted that as the delay in filing the appeal had crept in because of justifiable reasons and not on account of any lackadaisical approach of the assessee, the same in all fairness be condoned.

8. Per contra, Shri D. Hema Bhupal, Learned Senior Departmental Representative (for short, “Ld. Sr-DR”) objected to the seeking of the delay in filing of the present appeal.

9. We have given thoughtful consideration and are of a firm conviction that as there are sufficient reasons explaining the delay in filing of the present appeal, the same, in all fairness and interest of justice, merits to be condoned. Our aforesaid view is supported by the recent decision of the Hon’ble Supreme Court in the case of

Vidya Shankar Jaiswal v.

ITO (SC)/Special Leave Petition (Civil) Nos. 26310-26311/2024, dated 31

st January, 2025. The Hon’ble Apex Court while setting aside the order of the Hon’ble High Court of Chhattisgarh, which had approved the declining of the condonation of the delay of 166 days by the Income-Tax Appellate Tribunal, Raipur Bench, had observed, that a justice-oriented and liberal approach should be adopted while considering the application filed by an appellant seeking condonation of the delay involved in filing the appeal.

10. Coming to the merits of the case, the Ld. AR submitted that the core issue therein involved is three facet, viz., (i) inclusion of certain sale transactions in the respective wrong years, viz., Document No.3923 (Sl. No.10) and Document No.3495 (Sl. No.13); (ii) duplication of the sale transactions, viz., Document No.2361 (Sl. No.9) and Document No.2327 (Sl. No.11); and (iii) inclusion of only the proportionate share of the assessee as a co-owner in the transaction, viz, Document No.2360 (Sl. No.12). Elaborating on his contention, the Ld. AR submitted that the assessee had duly included the transactions stated at Sl. Nos. 1 to 10 aggregating to Rs.56.25 lakhs [subject to wrong inclusion of transaction of Document No.3923 (Sl. No.10) instead of Document No.3495 (Sl. No.13)]. The Ld. AR submitted that if the aforesaid wrong inclusion of Sl. No.13 (instead of Sl. No.10) is considered, then the transactions for the subject year reflected by the assessee at Rs.56.24 lakhs are duly reconciled. The Ld. AR had thereafter taken us through the respective transactions which are being considered by us while adjudicating the present appeal.

11. Per contra, the Ld. Sr-DR relied upon the orders of the lower authorities.

12. We have heard the Learned Authorized Representatives of both parties and perused the material available on record. As the controversy involved in the present appeal is three facet, we deem it apposite to deal with the same, in a chronological manner, as under:

A: Document No.3923, dated 17/08/2016 (Sl. No.10) r.w. Document No.3495, dated 23/07/2015 (Sl. No.13):

13. We find substance in the Ld. AR’s contention that the AO had wrongly included the sale transaction included vide Document No.3923, dated 17/08/2016 (Sl. No.10) which pertains to AY 2017-18, and at the same time had not considered the sale transaction vide Document No.3495, dated 23/07/2015 (Sl. No.13), which in fact pertains to the year under consideration. We find that a perusal of the aforesaid respective documents, viz., Document No.3923, dated 17/08/2016 (Sl. No.10) at Pages-27 to 29 of APB (copy of encumbrance of property) reveals that the said sale transaction was excluded on 17/08/2016 vide agreement-cum-General Power of Attorney for Rs.7,49,000/-, which thus clearly relates the same to the immediately succeeding year, i.e., AY 2017-18 and not the subject year before us. We thus, based on the aforesaid fact, direct the AO to exclude the aforesaid sale transaction while computing the income of the assessee for the subject year.

(ii) Coming to the Document No.3495, dated 23/07/2015, (Sl. No.13), Pages-44 to 49 of APB (translated copy), we find that the same is a sale deed for Rs.50 lakhs executed by the assessee through his Power of Attorney holder, viz., Sri Didla Ashoka Vardhan S/o. Sri Didla Purushottam Rao. As the aforesaid transaction pertains to the year under consideration, therefore, we herein direct the AO to include the same in the sale transaction while computing the income of the assessee for the subject year.

B. Document No.2361, dated 25/05/2015 (Sl. No.9) r.w. Document No.2327, dated 22/05/2015 (Sl. No.11):

14. We find substance in the Ld. AR’s contention that inclusion of both the aforesaid sale transactions had resulted to duplication while quantifying the amount of the sales for the year under consideration. We say so, for the reason that the Document No.2361/2015, dated 25/05/2015, Page Nos.69 to 72 (translated copy) clearly makes a mention that the sale transaction was earlier executed vide Document No.2327/2015, dated 22/05/2015 (Sl. No.11), but due to a computer error, the Survey No.123/1 was mistakenly written in the schedule instead of Survey No.123/1A, therefore as requested by the buyer, viz., Sri Adapa Seshagiri Rao the amended document correcting the aforesaid error is being issued. We thus, concur with the Ld. AR’s contention that the aforementioned Document No.2327, dated 22/05/2015 (Sl. No.11) is not an independent sale transaction but an amendment of the sale transaction already executed vide Document No.2361, dated 25/05/2015 (Sl. No.9). We thus, in terms of our aforesaid observation, direct the AO to exclude the transaction concluded vide Document No.2327, dated 22/05/2015 (Sl. No.11), as the same had already been included in the total sale transactions, vide Document No.2361, dated 25/05/2015 (Sl. No.9).

C: Document No.2360, dated 25/05/2015 (Sl. No.12), Pages-85 to 89 of APB (translated copy):

15. The Ld. AR after arguing on certain other aspects qua the aforesaid sale transaction, had confined his contention to the issue that as the assessee had sold the subject property as one of the co-owner along with four other co-owners, therefore, his share of sale transaction was liable to be restricted only to the extent of Rs.1,82,400/- (1/5th of Rs.9,12,000/-). Apart from that, the Ld. AR had submitted that the AO may also be directed to allow the deduction of indexed cost of acquisition while computing the income/gain element of the assessee on the subject sale transaction.

16. We have given thoughtful consideration and perused the Document No.2360, dated 25/05/2015 (Sl. No.12), Pages-85 to 89 of APB and concur with the Ld. AR that the assessee along with four other persons had sold the subject property as a co-owner. However, as the share of the co-owners is not mentioned in the sale document, therefore, we direct the AO to restrict the share of the assessee in the subject sale transaction to the extent of 1/5th of the total value of Rs.9,12,000/-, i.e., to the extent of Rs.1,82,400/-.

17. We thus, in terms of our aforesaid deliberations, set aside the order of the CIT(A) and direct the AO to modify his order as observed by us herein above.

18. In the result, appeal of the assessee is allowed for statistical purposes in terms of our aforesaid observations.