Intimation Order Merges With Final Scrutiny Assessment Rendering Parallel Appeals Against Intimation Infructuous

Issue

Whether an intimation order passed under Section 143(1) merges into the final scrutiny assessment order under Section 143(3) once a case is selected for scrutiny, thereby rendering any parallel appellate proceedings against the initial intimation infructuous.

Facts

-

Profile: The assessee is an Indian company operating as a subsidiary of a Japanese automotive group. For the assessment year 2021-22, it filed its return of income declaring a financial loss.

-

Initial Processing: The Central Processing Centre (CPC) processed the return under Section 143(1) and made certain adjustments, reducing the declared loss or creating additions.

-

Scrutiny Selection: The case was subsequently selected for detailed scrutiny based on transfer pricing parameters, and statutory notices under Sections 143(2) and 142(1) were issued.

-

Parallel Actions: While the scrutiny was underway, two parallel tracks developed:

-

The assessee filed a rectification application under Section 154 against the CPC intimation, which the Assessing Officer (AO) accepted. The entire scrutiny block eventually culminated in a final assessment order under Section 143(3) read with Section 144C(13).

-

Concurrently, the assessee had also filed an administrative appeal before the Commissioner (Appeals) specifically challenging the original Section 143(1) intimation. The Commissioner (Appeals) allowed this appeal, granting relief.

-

-

The Revenue’s Grievance: The Revenue challenged the Commissioner (Appeals) order before the Income Tax Appellate Tribunal (ITAT), arguing against the relief granted on the intimation order.

Decision

-

Doctrine of Merger Applied: The ITAT/Court held that once a return is selected for comprehensive scrutiny, the preliminary intimation order passed under Section 143(1) effectively merges with the final, detailed scrutiny assessment order passed under Section 143(3).

-

Appeals Rendered Void: Since the additions made by the CPC in the 143(1) intimation were already absorbed and rectified during the assessment pipeline, the original intimation ceased to have an independent legal existence.

-

Dismissal of Litigation: Consequently, the first appeal filed by the assessee before the Commissioner (Appeals) against the intimation had become infructuous. By extension, the Revenue’s subsequent appeal before the Tribunal arising out of that infructuous order was also dismissed as infructuous.

-

Outcome: Decided in favor of the assessee (by eliminating dead litigation).

Key Takeaways

The Doctrine of Merger: In tax law, a preliminary or ad-hoc order (like a Section 143(1) intimation) loses its individual identity and merges into the final, superior adjudication order (like a Section 143(3) scrutiny order) covering the same assessment year.

Extinguishment of Parallel Remedies: Once a final scrutiny assessment order is passed, any ongoing dispute or appellate channel strictly attacking the preliminary adjustments of the CPC becomes a academic exercise. Parties must contest the final assessment order instead.

Procedural Efficiency: Subordinate authorities and tribunals will not expend judicial time on reviewing intimations if the ultimate tax liability has already been superseded and re-fixed under a regular, comprehensive assessment order.

IN THE ITAT DELHI BENCH ‘E’Deputy Commissioner of Income-taxv.Raj Kumar Chauhan, Judicial Member

and S. Rifaur Rahman, Accountant MemberIT Appeal No.989 (DEL) of 2025

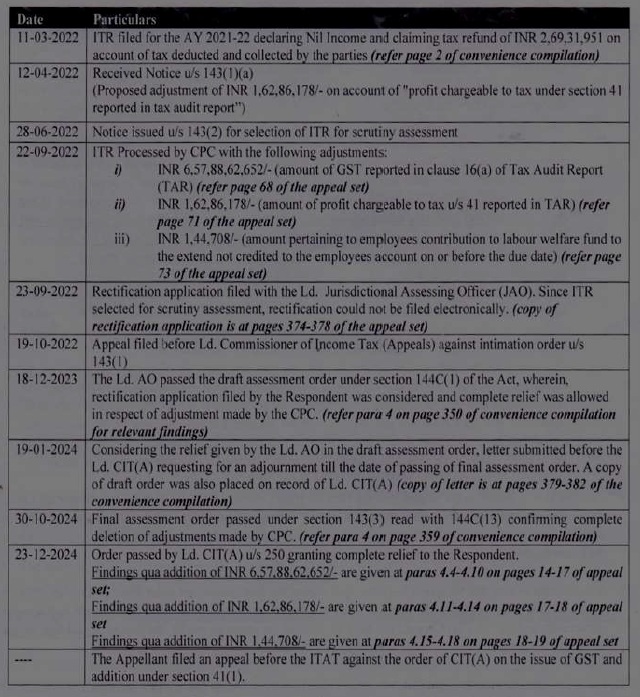

[Assessment year 2021-22]MAY 6, 2026Sanjeev Kumar Yadav, CIT DR for the Appellant. Prashant Maharchandani and Jaineder Singh Kataria, Advs. for the Respondent.ORDERS. Rifaur Rahman, Accountant Member.- This appeal is filed by the assessee against the order of the Ld. Addl. JCIT (Appeals)-1, Chennai [hereinafter referred to as ‘ld. JCIT (A)] dated 23.12.2024 for the Assessment Year 2021-22.2. Brief facts of the case are, assessee is a subsidiary of Denso Corporation, Japan. It commenced its commercial operation in December 1999. It is engaged in the manufacturing of automotive components and mostly sales to automobile manufacturers in India. It has a manufacturing plant in Manesar and Jhajjar District of Haryana. Assessee filed its return of income for AY 2021-22 on 11.03.2022 declaring total loss of Rs.98,58,96,558/-. The return of income was processed by the CPC on 22.09.2022 determining the total income of Rs.5,60,93,96,980/-. The case of the assessee was selected for scrutiny through CASS on the following issues :-

(i) Large value of international transactions in nature of technical service fees (TP Risk Parameter); and

(ii) Larger international transactions in tangible property and low profit before interest & taxes shown in ITR (TP Rish Parameter). 3. Accordingly, notices under section 143(2) and 142(1) of the Income-tax Act, 1961 (for short ‘the Act’) were issued and served on the assessee. The case of the assessee was scrutinized in faceless manner as per the procedure laid down u/s 144B of the Act. Assessee has declared international transactions in Form 3CEB and accordingly, the case was referred to Transfer Pricing Officer (TPO). Ld. TPO proposed adjustment u/s 92CA(3) of the Act. During assessment proceedings, the AO also proposed disallowance towards Clubs Entrance Fees and Subscription to the extent of Rs.2,81,400/- and addition on account of difference in stock to the extent of Rs.15,59,991/-. Further during assessment proceedings, assessee also furnished rectification application u/s 154 of the Act for rectification of the intimation issued u/s 143(1) dated 22.09.2022. Since assessee could not file the rectification through e-filing portal, therefore, the same was filed before the AO during scrutiny proceedings and the AO has accepted the rectification application along with supporting evidences and accordingly draft assessment was passed u/s 144C(1) read with section 144B of the Act. Assessee filed objections before the ld. DRP. After considering the adjustment proposed by the ld. DRP, final assessment order was passed determining the total assessed income u/s 143(3) of the Act at Rs.20,09,23,684/-.4. Further assessee received notice u/s 143(1)(a) of the Act with the proposed adjustment of Rs.1,62,86,178/- on account of profit chargeable to tax to tax u/s 41 of the Act as reported in the tax audit report. The assessee received final intimation u/s 143(1) of the Act on 22.09.2022 with the following adjustments :-

(i) Rs.6,57,88,62,652/- based on the GST reported in Clause 16(a) of the tax audit report;

(ii) Rs.1,62,86,178/- based on the audit report; and

(iii) Rs.1,44,708/- towards employee contribution to labour welfare fund to the extent not credited in the employee account. 5. A rectification application filed by the assessee before the jurisdictional AO on 23.09.2022 for the reason that rectification application could not be filed through e-portal. In the meantime, on 19.10.2022, assessee filed appeal before the ld. CIT (A) against the order u/s 143(1). On 18.12.2023, the AO passed draft assessment order u/s 144(1) of the Act and during assessment proceedings, the AO considered the rectification application filed by the assessee and accordingly, the AO gave relief to the assessee in the draft assessment order itself and subsequently final assessment order was passed u/s 143(3) r.w.s. 144C(13) confirming the complete deletion of adjustments proposed by the CPC. Ld. CIT (A) gave complete relief to the assessee by passing the order on 23.12.2024. Against the above order, Revenue is in appeal before us raising following grounds of appeal :-“1. Whether on the facts and circumstances of the case .and in law, the ld. CIT(A) has erred in allowing the appeal of the assessee by deleting the addition made by the AO amounting to Rs.6,57,88,62,652/- on account of Goods & Services Tax.2. Whether on the facts and circumstances of the case and in law, the ld. CIT(A) has erred in deleting the addition, ignoring the extant provisions of section 145A which prescribe that valuation of inventory shall be adjusted to include the amount of any tax, duty, cess or fee, actually paid/incurred.3. Whether on the facts and circumstances of the case and in law, ld. CIT(A) has erred in ignoring the decision of Hon’ble Delhi High Court in CIT v. lakshmi Sugar Mills Co. Ltd, wherein the Hon’ble High Court held that section 145A of the Act begins with non obstante clause and provisions section 145A direct inclusions of amount of tax, duty etc. for the purpose of valuation of inventories.4. Whether on the facts and circumstances of the case and in law, the ld CIT(A) has erred in allowing the appeal of the assessee by deleting the addition made by the AO u/s 41(1) of the Income Tax Act, amounting to Rs. 1,62,86,178/- on account of provision for technical general fees and provisions for test and sample.”6. At the time of hearing, ld. DR brought to our notice grounds of appeal filed by the Revenue and submitted that the additions proposed by the CPC u/s 143(1)(a) is separate appealable order and ld. CIT (A) gave relief without considering merits of the case and ld. CIT (A) deleted the addition ignoring the provisions of section 145A of the Act and he supported the findings of CPC.7. On the other hand, ld. AR of the assessee brought to our notice list of dates and events as below :-8. After that ld. AR relied on the following case laws :-

(i) South India Club v. ITO (Delhi – Trib.);

(ii) Hon’ble Madras High Court in Tamil Nadu Magnesite Ltd. v. CIT (Madras) (Madras);

(iii) Hero Fincop Ltd. v. ACIT [IT Appeal No.2542 (Del) of 2024, dated 16-1-2026]; 9. Considered the rival submission and material placed on record. We observed that certain adjustments were made by the CPC u/s 143(1)(a) of the Act based on certain observations from the tax audit report. Subsequently, the case of the assessee was selected for scrutiny and during assessment proceedings and the AO has considered the rectification application filed by the assessee u/s 154 of the Act. After considering the same, the AO gave relief to the assessee based on the merits in the case and since assessee has filed an appeal against the order passed u/s 143(1) of the Act before the ld. CIT (A) and ld. CIT (A) also gave relief to the assessee. Before us, Revenue is not in fact against the relief granted by the ld. CIT(A). As per the factual matrix available on record, we observed that the additions made by the CPC u/s 143(1)(a) of the Act was subsequently rectified by the AO. Therefore, once the assessment is selected for scrutiny, the intimation order passed u/s 143(1)(a) is merged with the scrutiny assessment under section 143(3) of the Act. That being the case, the assessment order passed u/s 143(1)(a) is already merged with the order passed u/s 143(3) which has no locus standi. Therefore, as held in the case of South India Club (supra), it was held that when the assessment was processed under regular assessment then the intimation loses its individuality and merges with the regular assessment. The coordinate Bench was in agreement with the findings of the ld. CIT (A) that intimation u/s 143(1) merges with the order passed u/s 143(3) of the Act and appeal against the above intimation becomes infructuous. Therefore, in our considered view, the appeal filed by the assessee before ld. CIT (A) is infructuous and the Revenue preferred to file the above appeal against the abovesaid infructuous appeal before us is also infructuous.10. In the result, the appeal filed by the Revenue is dismissed as infructuous.