Reassessment notice containing the issuing officer’s name and designation is valid without a physical signature.

Issue

Whether a reassessment notice issued under Section 148 of the Income-tax Act, 1961 is legally invalid and unauthenticated under Section 282A if it lacks a handwritten or digital signature but explicitly displays the name and designation of the issuing Assessing Officer.

Facts

-

The assessee filed a writ petition before the High Court challenging a reassessment order passed under Section 147 for the Assessment Year 2022-2023.

-

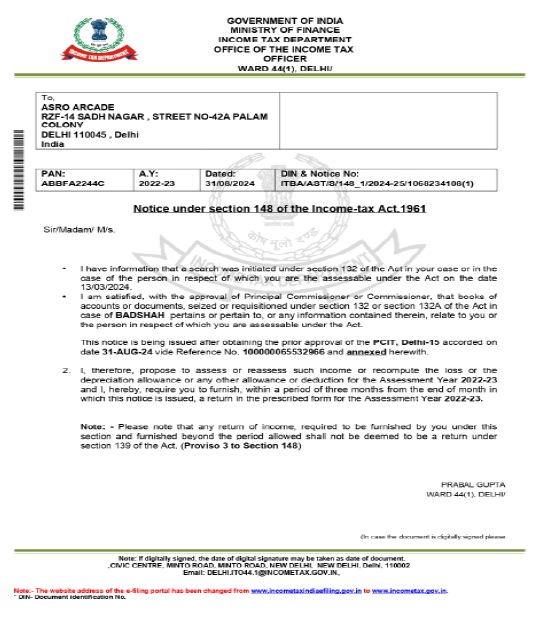

The core contention of the assessee was that the initial notice under Section 148 was invalid because it lacked the physical or digital signature of the Assessing Officer as required under Section 282A.

-

The Assessing Officer had issued the disputed Section 148 notice through the system without appending a physical handwritten or digital signature.

-

However, the notice prominently featured the specific name and official designation of the issuing authority.

-

Following the issuance of this notice, the tax department proceeded to complete the reassessment process under Section 147.

Decision

-

Notice Declared Valid: The High Court ruled that the impugned notice issued under Section 148 was fully valid and legally authenticated.

-

Covered by Statutory Exception: The court held that since the notice explicitly bore the name and designation of the issuing authority, it fell squarely within the enabling ambit of sub-section (2) of Section 282A.

-

Signature Not Mandatory: It was determined that when the name and designation of the issuing officer are clearly mentioned on the face of the statutory communication, a physical or digital signature is not a mandatory prerequisite for validity.

-

Reassessment Upheld: Consequently, the subsequent reassessment order passed under Section 147 was held to be entirely sustainable, and the issue was decided in favour of the revenue.

Key Takeaways

-

Authentication via Name and Designation: Under Section 282A(2), a statutory income tax notice does not require a physical or digital signature to be valid, provided it explicitly mentions the name and designation of the issuing officer.

-

Substance Rules Technicality: System-generated or printed notices cannot be struck down on mere hyper-technical grounds like a missing signature block if the identity and authorization of the issuing official are clear on the record.

-

Revenue Protections: This ruling shields the income tax department from having technical faceless or automated communications invalidated purely due to the absence of traditional signature formats.

CM APPL. No. 24820 & 24852 of 2026