ORDER

Madhusudan Sawdia, Accountant Member.- These appeals are filed by Jamia Osman Bin Affan Education Society (“the assessee”), feeling aggrieved by the separate orders passed by the Learned Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (NFAC), Delhi (“Ld. CIT(A)”) dated 27.03.2024 for the A.Y 2017-18 and order of the Ld. CIT (Exemption), Hyderabad (“Ld. CIT(E)”) dated 06.06.2024 respectively. Since the assessee in both the appeals are same and issues raised by the assessee in these appeals are inter related, for the sake of convenience, these were heard together and are being disposed of by this common and consolidated order.

ITA No. 477/Hyd/2024:

2. The assessee has raised the following grounds of appeal:

| “1) |

|

The order of the learned CIT (A) is erroneous to the extent it is prejudicial to the appellant. |

| 2) |

|

The Assessing Officer and the learned CIT (A) are not justified in holding that an amount of Rs.4,02,74,950/-utilized for construction of school building cannot be considered as utilization for the purposes of claiming deduction u/s 11(2) of the I.T. Act. |

| 3) |

|

The learned CIT (A) ought to have seen that the amount was spent for the objects of the appellant society and, therefore, has to be considered as a part of utilization. |

| 4) |

|

The learned CIT (A) erred in confirming the action of the Assessing Officer in disallowing Rs.7,34,673/-representing the expenses on distribution of auto rikshcaws as an expenditure not allowable for the purpose of Sec.11 of the I.T.Act. |

| 5) |

|

The Assessing Officer ought to have considered the fact that the amount was utilized for the objects of the appellant society and cannot be treated as the income of the appellant and has to be treated as an expenditure which is utilized from out of the funds of the society. |

| 6) |

|

Any other ground/grounds that may be urged at the time of hearing;” |

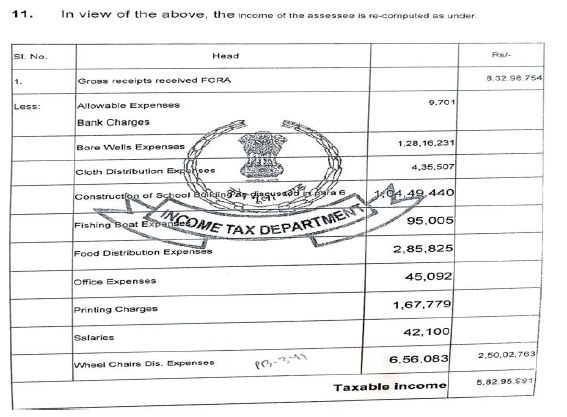

3. The brief facts of the case, as emanating from the record, are that the assessee is a society registered under the Societies Registration Act, Government of Telangana. The assessee is also registered under section 12A and section 80G of the Income Tax Act, 1961 (“the Act”), and is further registered under the provisions of the Foreign Contribution (Regulation) Act, 2010. The assessee filed its return of income for the Assessment Year 2017-18 declaring total income at Nil. During the year under consideration, the gross receipts of the society were at Rs.8,32,98,754/-. After incurring expenditure of Rs.7,24,89,390/-, the assessee has shown excess of income over expenditure at Rs.1,08,09,364/- as per the audited income and expenditure account. Since the assessee claimed that its income was applied for charitable purposes within the meaning of sections 11 and 12 of the Act, the entire surplus was claimed as exempt under section 11(1)(a) of the Act. The case of the assessee was selected for complete scrutiny under CASS and accordingly notice under section 143(2) of the Act was issued by the Learned Assessing Officer (“Ld. AO”). During the course of assessment proceedings, the assessee furnished details and explanations in respect of its activities and application of income. After considering the submissions of the assessee, the Ld. AO examined the nature of expenditure claimed by the assessee and came to the conclusion that only a portion of the expenditure could be treated as application of income in accordance with the objects of the society. Accordingly, the Ld. AO allowed expenditure of Rs.2,50,02,763/- out of the total receipts of Rs.8,32,98,754/- and disallowed the balance expenditure. Consequently, the Ld. AO computed the taxable income of the assessee at Rs.5,82,95,991/- and completed the assessment under section 143(3) of the Act vide order dated 30.12.2019.

4. Aggrieved by the assessment order passed by the Ld. AO, the assessee preferred an appeal before the Ld. CIT(A). Before the Ld. CIT(A), the assessee specifically challenged the additions made by the Ld. AO on account of construction of school building amounting to Rs.4,02,74,950/-, auto distribution expenses amounting to Rs.7,34,673/-, swing machine distribution expenses amounting to Rs.3,54,239/- and depreciation on computer amounting to Rs.62,705/-. The Ld. CIT(A), after considering the submissions of the assessee and examining the material available on record, granted partial relief to the assessee by deleting the additions relating to swing machine distribution expenses of Rs.3,54,239/- and depreciation on computer of Rs.62,705/-. However, the Ld. CIT(A) sustained the additions made by the Ld. AO in respect of construction of school building amounting to Rs.4,02,74,950/-and auto distribution expenses amounting to Rs.7,34,673/-.

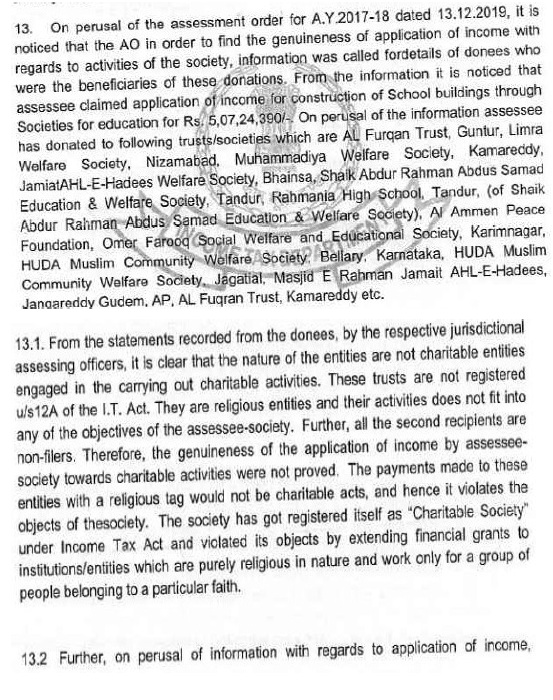

5. Aggrieved with the order of the Ld. CIT(A), the assessee is in appeal before this Tribunal. Before us, the Learned Authorized Representative (“Ld. AR”) submitted that out of the various grounds raised by the assessee, only two issues survive for adjudication, namely, addition of Rs.4,02,74,950/-on account of construction of school building and addition of Rs.7,34,673/- on account of auto distribution expenses, which have been sustained by invoking the provisions of section 13(1)(b) of the Act. In this regard, the Ld. AR invited our attention to para no. 2.2 of the assessment order wherein the Ld. AO has reproduced the aims and objects of the society. He submitted that a perusal of the object clause clearly demonstrates that the society has been established for charitable purposes relating to education and social welfare and none of the objects restrict the activities of the society to any particular religious community or caste. The Ld. AR further submitted that the Ld. AO has wrongly invoked the provisions of section 13(1)(b) of the Act. Inviting our attention to the provisions of section 13(1)(b) of the Act, he submitted that the said provision is applicable only where a trust or institution is created or established for the benefit of any particular religious community or caste. According to him, since the assessee society has not been created for the benefit of any particular religious community, invocation of section 13(1)(b) of the Act is not justified. The Ld. AR further submitted that the Ld. AO himself has accepted substantial expenditure amounting to Rs.2,50,02,763/- as application of income towards charitable purposes. According to him, this itself establishes that the activities of the assessee society are in consonance with charitable objects and are not confined to any particular religious community. The Ld. AR further submitted that the assessee had claimed total expenditure of Rs.5,07,24,390/- on account of construction of school building. Out of the said amount, the Ld. AO has allowed Rs.1,04,49,440/- and disallowed the balance amount of Rs.4,02,74,950/-. He submitted that out of the disallowance, an amount of Rs.75,79,088/- has been disallowed on the ground that it pertains to Financial Year 2015-16. However, the remaining amount has been disallowed on the allegation that the assessee has constructed Masjid and not school building. The Ld. AR strongly contended that the finding recorded by the Ld. AO is factually incorrect. According to him, the assessee has constructed Madrasa and not Masjid. He submitted that Madrasa is an educational institution where education of Quran is imparted and therefore falls within the meaning of “education” under section 2(15) of the Act. The Ld. AR further submitted that even assuming, without admitting, that the construction relates to Masjid, the same would still qualify as charitable activity. In support of this contention, the Ld. AR relied upon the decision of the Hon’ble Andhra Pradesh High Court in the case of CIT v. Social Service Centre 250 ITR 39 (Andhra Pradesh) and submitted that construction of church has been held to be an activity for general public utility. The Ld. AR also placed reliance upon the decision of the Hon’ble Supreme Court in the case of CIT v. Dawoodi Bohra Jamat 364 ITR 31 (SC) and submitted that merely because the beneficiaries belong to a particular religious community, it cannot be inferred that the trust itself has been created for the benefit of such religious community. Accordingly, the Ld. AR prayed before the Bench for deletion of addition of Rs.4,02,74,950/- on account of construction of school building

6. With regard to addition on account of auto distribution expenses of Rs.7,34,673/-, the Ld. AR submitted that the assessee has distributed autos to economically weaker sections of the society in furtherance of its object of providing relief to the poor. He submitted that such expenditure squarely falls within the ambit of charitable purpose. He further submitted that merely because some beneficiaries belong to a particular religious community, it cannot be inferred that the expenditure has been incurred for the benefit of such religious community. Accordingly, the Ld. AR prayed before the Bench for deletion of addition on account of auto distribution expenses of Rs.7,34,673/-.

7. Per contra, the Learned Departmental Representative (“Ld. DR”) strongly supported the orders of the lower authorities. The Ld. DR invited our attention to para no. 2.2 of the assessment order and submitted that the objects of the assessee society are purely charitable and do not include any religious activity. He further invited our attention to para no. 5.4 of the assessment order and submitted that the Ld. AO had carried out detailed enquiry and recorded statements of the persons to whom the buildings have been handed over. The Ld. DR submitted that it is evident from the record that the assessee has not retained the buildings as its own assets but has handed them over to third parties belonging to a particular religious community. He submitted that the construction is either of Masjid or Madrasa and in both situations the activity is religious in nature. The Ld. DR further submitted that even imparting education of Quran through Madrasa is a religious activity confined to a particular religious community. He specifically invited our attention to para no. 42 of the decision of the Hon’ble Supreme Court in the case of Dawoodi Bohra Jamat (supra) and submitted that the Hon’ble Supreme Court has held that the actual activities carried out by the assessee are relevant for examining eligibility under sections 11 and 12 of the Act. The Ld. DR further submitted that though the objects of the assessee society may be general in nature, the actual activities clearly demonstrate that the benefits are confined to a particular religious community. In support of his contention, the Ld. DR relied upon the decision of the Hon’ble Supreme Court in the case of CIT v. Palghat Shadi Mahal Trust (SC)/[2002] 254 ITR 212 (SC) and the decision of the Hon’ble Jammu & Kashmir High Court in the case of Ghulam Mohidin Trust v. CIT 248 ITR 587 (Jammu & Kashmir)

The Ld. DR further submitted that the decision of the Hon’ble Andhra Pradesh High Court in the case ofSocial Service Centre(supra

) is distinguishable on facts since in that case the religious activity was incidental and supported by the object clause, whereas in the present case the activity is substantive and not supported by the objects of the society. Accordingly, the Ld. DR prayed before the Bench for sustaining the additions made by the Ld. AO and confirmed by the Ld. CIT(A).

8. We have heard the rival submissions and perused the material available on record including the case laws relied upon. The issue arising for our consideration is whether the additions of Rs.4,02,74,950/- on account of construction of school building and Rs.7,34,673/- on account of auto distribution expenses can be sustained by invoking the provisions of section 13(1)(b) of the Act. In this regard, we have gone through para nos. 7 to 7.3 of the order of the Ld. CIT(A), which is to the following effect:

9. On a perusal of the above, we find that both the additions of Rs.4,02,74,950/- and Rs.7,34,673/- have been sustained in the case of the assessee by invoking section 13(1)(b) of the Act alleging that the said amounts have been applied by the assessee for the benefit of a particular religious community. Therefore, it is not the case of the Revenue that the application of these expenses is not towards the objects of the society. The only contention of the Revenue is that these expenses have been incurred for the purpose of a particular religious community in violation of section 13(1)(b) of the Act. Accordingly, the submission made by the Ld. AR and Ld. DR on the issue whether the application of income of the Trust towards the objects of the society or not, is only academic. Now, it is crucial to examine the provisions of section 13(1)(b) of the Act, which is to the following effect:

13. (1) xxxxxx

(a) xxxxxxxxx

(b) in the case of a trust for charitable purposes or a charitable institution created or established after the commencement of this Act, any income thereof if the trust or institution is created or established for the benefit of any particular religious community or caste”

10. On perusal of the above, we find that the provisions of section 13(1)(b) of the Act is applicable only where a charitable trust or institution is created or established for the benefit of any particular religious community or caste. In this regard, we have gone through para nos. 41 to 50 of the decision of the Hon’ble Supreme Court in the case of Dawoodi Bohra Jamat (supra), which is to the following effect:

“41.Therefore, the objects of the trust exhibit the dual tenor of religious and charitable purposes and activities. Section 11 of the Act shelters such trust with composite objects to claim exemption from tax as a religious and charitable trust subject to provisions of Section 13. The activities of the trust under such objects would therefore be entitled to exemption accordingly.

42.We would now proceed to examine the objects under the provisions of Section 13(1)(b) of the Act. It becomes amply clear from the language employed in the provisions that Section 13 is in the nature of an exemption from applicability of Sections 11 or 12 and the examination of its applicability would only arise at the stage of claim under Sections 11 or 12. Thus, where the income of a trust is eligible for exemption under section 11, the eligibility for claiming exemption ought to be tested on the touchstone of the provisions of section 13. In the instant case, it being established that the respondent-trust is a public charitable and religious trust eligible for claiming exemption under Section 11, it becomes relevant to test it on the anvil of Section 13.

43.Thus, the second issue which arises for our consideration and decision is, whether the respondenttrust is a charitable and religious trust only for the purposes of a particular community and therefore, not eligible for exemption under Section 11 of the Act in view of provisions of Section 13(1)(b) of the Act.

44.In the instant case, the Tribunal has found on facts after analysing the objects of the trust that the respondenttrust is a public religious trust and its objects are solely religious in nature and being of the opinion that Section 13(1)(b) is solely meant for charitable trust for particular community, negated the possibility of applicability of Section 13(1)(b) of the Act at the outset. The High Court has also confirmed the aforesaid view in appeal and observed that Section 13(1)(b) would only be applicable in case of income of the trust for charitable purpose established for benefit of a particular religious community. In our considered view, the said view may not be the correct interpretation of the provision.

45.From the phraseology in clause (b) of section 13(1), it could be inferred that the Legislature intended to include only the trusts established for charitable purposes. That however does not mean that if a trust is a composite one, that is one for both religious and charitable purposes, then it would not be covered by clause (b). What is intended to be excluded from being eligible for exemption under Section 11 is a trust for charitable purpose which is established for the benefit of any particular religious community or caste.

46.Such trusts with composite objects would not be expelled out of the purview of Section 13(1)(

b)

per se. The Section requires it to be established that such charitable purpose is not for the benefit of a particular religious community or caste. That is to say, it needs to be examined whether such religious-charitable activity carried on by the trust only benefits a certain particular religious community or class or serves across the communities and for society at large. (Sole Trustee, Loka Shikshana Trust v.

CIT,

(1975) 101 ITR 234

(SC)). The section of community sought to be benefited must be either sufficiently defined or identifiable by a common quality of a public or impersonal nature. (CIT v.

Andhra Chamber of Commerce,

55 ITR 722).

47.This Court in CIT v. Palghat Shadi Mahal Trust, (2002) 9 SCC 685 the Muslim residents of Kerala constituted a trust “for the purpose of constructing and establishing at Palghat-a-Shadi Mahal and other institutions for the educational, social and economic advancement of the Muslims and for religious and charitable objects recognised by Muslim law .” and later clarified that the proceeds would be utilized for the benefit for public at large and upon this basis, the trust made a claim for exemption from tax under Section 11. This Court held that the resolution clarifying the object would not validly amend the object of the trust-deed and since the object confined the benefit to only Muslim community, it would be covered by the restriction under Section 13(1)(b) of the Act even though it functioned for public benefit. Thus, therein the object sufficiently defined or expressly stated beneficiary class and restricted the activities of the trust to a specific community.

48.Further, in State of Kerala v. M.P. Shanti Verma Jain, (1998) 5 SCC 63 this Court has held that propagation of religion and restriction of benefits of activities of trust in its objects to the said community would render the trust as ineligible for claiming exemption under similar provisions of Kerala Agricultural Income Tax Act, 1950. The Court observed as follows:

“.The Deed of Trust and the rules run into more than thirty pages out of which six pages of the Trust Deed narrate the philosophy of Jain Dharma. The objects of the Trust clearly show that the Trust is meant for propagation of Jain religion and rendering help to the followers of Jain religion. Even medical aid and similar facilities are to be rendered to persons devoted to Jain religion and to nonJains if suffering from ailments, but the medical aid could be given to them only if any member of the families managing the Trust, shows sympathy and is interested in their treatment. The Tribunal, in our opinion, was right in its conclusion that the dominant purpose of the Trust in the present case was propagation of Jain religion and to serve its followers and any part of agricultural income of the Trust spent in the State of Kerala also could not be treated as allowable item of the expenses.”

49.In the present case, the objects of the respondent-trust are based on religious tenets under Quran according to religious faith of Islam. We have already noticed that the perusal of the objects and purposes of the respondenttrust would clearly demonstrate that the activities of the trust though both charitable and religious are not exclusively meant for a particular religious community. The objects, as explained in the preceding paragraphs, do not channel the benefits to any community if not the Dawoodi Bohra Community and thus, would not fall under the provisions of Section 13(1)(b) of the Act.

50.In that view of the matter, we are of the considered opinion that the respondent-trust is a charitable and religious trust which does not benefit any specific religious community and therefore, it cannot be held that Section 13(1)(b) of the Act would be attracted to the respondenttrust and thereby, it would be eligible to claim exemption under Section 11 of the Act.”

11. On a perusal of the above, we find that the Hon’ble Supreme Court has categorically held that if any trust incurs expenditure towards charitable objects as well as religious objects, then the provisions of section 13(1)(b) of the Act are not applicable. In other words, the Hon’ble Supreme Court has held that where the trust or society is found to have been engaged in charitable activities also, the provisions of section 13(1)(b) of the Act cannot be invoked merely because certain activities may incidentally benefit a particular religious community. In this regard, we have gone through page no. 47 of the assessment order, which is to the following effect:

12. On perusal of the above, we find that the Ld. AO himself has allowed substantial expenditure amounting to Rs.2,50,02,763/- towards charitable activities. Therefore, there is no dispute regarding the fact that the Ld. AO himself has accepted that substantial activities of the assessee society are towards charitable purposes. Once the Revenue itself has accepted that substantial activities of the assessee are charitable in nature, then, in our considered opinion, the provisions of section 13(1)(b) of the Act cannot be invoked merely because certain expenditures are alleged to have been incurred for persons belonging to a particular religious community. Therefore, without going into the further controversy regarding the exact nature of expenditure, namely, whether the construction relates to Madrasa or Masjid, and without independently adjudicating whether the expenditure is religious or educational in nature, we are of the considered view that once the assessee society is found to be substantially engaged in charitable activities, the provisions of section 13(1)(b) of the Act cannot be attracted in the case of the assessee. Therefore, on the backdrop of the fact that substantial expenditure amounting to Rs.2,50,02,763/- has been accepted by the Ld. AO himself towards charitable activities, we hold that the provisions of section 13(1)(b) of the Act are not applicable in the case of the assessee. Consequently, the additions of Rs.4,02,74,950/- on account of construction of school building and Rs.7,34,673/- on account of auto distribution expenses are unsustainable. Accordingly, we direct the Ld. AO to delete both the additions.

13. In the result, the appeal of the assessee in ITA No. 477/Hyd/2024 is allowed.

ITA No.631/Hyd/2024:

14. The assessee has raised the following grounds of appeal:

| (1) |

|

The order of the learned CIT (Exemptions) passed u/s 12AB (4) of the I.T. Act is erroneous both on facts and in law. |

| (2) |

|

The learned CIT (Exemptions) erred in holding that the appellant did not utilize its funds for the purpose of the objects of the trust; |

| (3) |

|

The learned CIT (Exemptions) erred in holding that the appellant deviated from its objects and utilized the funds for any religious purposes; |

| (4) |

|

The learned CIT (Exemptions) ought to have seen that the entire activity was within the frame work of the objects of the trust and, therefore, should not have withdrawn the registration granted u/s 12AB (4) of the I.T. Act. |

| (5) |

|

The learned CIT (Exemptions) erred in passing the order u/s 12AB (4) of the I.T. Act withdrawing the registration granted to the appellant herein. |

| (6) |

|

The learned CIT (Exemptions) erred in holding that the provisions of Sec.115TD are applicable to the facts of the case of the appellant herein. |

| (7) |

|

Any other ground/grounds that may be urged at the time of hearing”. |

15. The present appeal filed by the assessee is directed against the order passed by the Ld. CIT(E) under section 12AB(4) of the Act dated 06.06.2024, whereby the registration granted to the assessee under section 12A/12AB of the Act has been cancelled retrospectively with effect from 29.07.2016.

16. We have heard the rival submissions and perused the material available on record. We have also gone through para nos. 13 and 14 of the order passed by the Ld. CIT(E), which is to the following effect:

17. On perusal of the above, we find that the principal basis for cancellation of registration granted to the assessee under section 12A/12AB of the Act is the assessment order passed by the Ld. AO for Assessment Year 2017-18 dated 30.12.2019 and the findings recorded therein invoking the provisions of section 13(1)(b) of the Act in the case of the assessee. However, while adjudicating the quantum appeal of the assessee for Assessment Year 2017-18 in ITA No.477/Hyd/2024 we have set aside the additions made by the Ld. AO and has categorically held that the provisions of section 13(1)(b) of the Act are not applicable in the case of the assessee. We have also specifically recorded a finding that since substantial charitable activities of the assessee have been accepted by the Revenue itself, the provisions of section 13(1)(b) of the Act cannot be invoked merely because certain expenditures are alleged to have benefited a particular religious community. Therefore, the very foundation on the basis of which the registration of the assessee has been cancelled under section 12AB(4) of the Act no longer survives.

18. Further, as regards the retrospective cancellation of registration granted under section 12A/12AB of the Act, we have gone through para nos. 6.3 to 6.7 of the order of this Tribunal in the case of Hyderabad Science Society(Exemption) (supra), which is to the following effect:

“6.3. As regards the validity of the impugned order for cancellation of the registration with effect from the assessment year 2015-2016, we find force in the arguments of the learned Authorised Representative of the Assessee as fortified by various decisions of Hon’ble High court as well as this Tribunal. In the case of Amala Jyothi Vidya Kendra Trust v. PCIT(supra), the ITAT, Bangalore Bench has considered an identical issue and held in Para nos.6 to 8 as under:

“6. We have heard the rival submissions and perused the materials available on record. The main contention of the Id. A.R. is that the Ld. PCIT has cancelled the registration granted to the assessee w.e.f. the previous year i.e. 2020-21 relevant to assessment year 2021-22 by applying the provisions as stood on 12-5-2023, which cannot be applied for the violations of the provisions of section 12AA or 12AB of the Act. According to the Ld. A.R., the Id. PCIT has cancelled the registration granted to the assessee since the Id. PCIT was satisfied that one or more specified violations have taken place. The specified violations are mentioned in explanation to section 12AB(4) of the Act as follows:

Explanation: For the purposes of this sub-section, the following shall mean “specified violation”,–

(a) Where any income derived from property held under trust, wholly or in part for charitable or religious purposes, has been applied, other than for the objects of the trust or institution; or

(b) The trust or institution has income from profits and gains of business which is not incidental to the attainment of its objectives or separate books of account are not maintained by such trust or institution in respect of the business which is incidental to the attainment of its objectives; or

(c) The trust or institution has applied any part of its income from the property held under a trust for private religious purposes, which does not ensure for the benefit of the public; or

(d) The trust or institution established for charitable purpose created or established after the commencement of this Act, has applied any part of its income for the benefit of any particular religious community or caste; or

(e) Any activity being carried out by the trust or institution-

(i) is not genuine, or

(ii) is not being carried out in accordance with all or any of the conditions subject to which it was registered; or

(f) The trust or institution has not complied with the requirement of any other law, as referred to in item (B) of sub-clause (i) of clause (b) of sub-section (1), and the order, direction or decree, by whatever name called, holding that such noncompliance has occurred, has either not been disputed or has attained finality.

6.1. Thus, the contention of the Ld. A.R. is that these provisions have been inserted by Finance Act, 2022 w.e.f. 1-4-2022 and if there is a violation in previous year 2020-21 relevant to assessment year 2021-22, these provisions cannot be applied to the assessee’s case. For clarity, we will go through the relevant provisions applicable to previous year 2020-21 relevant to assessment year 2021-22 as follows:

“12AB(4): Where registration of a trust or an institution has been granted under clause (a) or clause (b) of subsection (1) and subsequently, the Principal Commissioner or Commissioner is satisfied that the activities of such trust or institution are not genuine or are not being carried out in accordance with the objects of the trust or institution, as the case may be, he shall pass an order in writing cancelling the registration of such trust or institution after affording a reasonable opportunity of being heard.”

6.2. This section has been amended by Finance Act, 2022 w.e.f. 1-4-2022 as follows:

12AB(4): Where registration or provisional registration of a trust or an institution has been granted under clause (a) or clause (b) or clause (c) of sub-section (1) or clause (b) of sub- section (1) of section 12AA, as the case may be, and subsequently,–

(a) The Principal Commissioner or Commissioner has noticed occurrence of one or more specified violations during any previous year; or

(b) The Principal Commissioner or Commissioner has received a reference from the Assessing Officer under the second proviso to sub-section (3) of section 143 for any previous year; or

(c) Such case has been selected in accordance with the risk management strategy, formulated by the Board from time to time, for any previous year;

The Principal Commissioner or Commissioner shall

i. call for such documents or information from the trust or institution, or make such inquiry as he thinks necessary in order to satisfy himself about the occurrence or otherwise of any specified violation;

ii. pass an order in writing, cancelling the registration of such trust or institution, after affording a reasonable opportunity of being heard, for such previous year and all subsequent previous years, if he is satisfied that one or more specified violations have taken place;

iii. pass an order in writing, refusing to cancel the registration of such trust or institution, if he is not satisfied about the occurrence of one or more specified violations;

iv. forward a copy of the order under clause (ii) or clause (iii), as the case may be, to the Assessing Officer and such trust or institution.

Explanation: For the purposes of this sub-section, the following shall mean “specified violation”,–

(a) Where any income derived from property held under trust, wholly or in part for charitable or religious purposes, has been applied, other than for the objects of the trust or institution; or

(b) The trust or institution has income from profits and gains of business which is not incidental to the attainment of its objectives or separate books of account are not maintained by such trust or institution in respect of the business which is incidental to the attainment of its objectives or separate books of account are not maintained by such trust or institution in respect of the business which is incidental to the attainment of its objectives; or

(c) The trust or institution has applied any part of its income from the property held under a trust for private religious purposes, which does not ensure for the benefit of the public; or

(d) The trust or institution established for charitable purpose created or established after the commencement of this Act, has applied any part of its income for the benefit of any particular religious community or caste; or

(e) Any activity being carried out by the trust or institution-

(i) is not genuine, or

(ii) is not being carried out in accordance with all or any of the conditions subject to which it was registered; or

(f) The trust or institution has not complied with the requirement of any other law, as referred to in item (B) of sub-clause (1) of clause (b) of sub-section (1), and the order, direction or decree, by whatever name called, holding that such non-compliance has occurred, has either not been disputed or has attained finality.

6.3. As per section 12AB(4) of the Act as applicable to assessment year 2021-22, the Id. PCIT if he is satisfied that activities of the Trust or institution are not genuine or not being carried out in accordance with the objects of the trust or institution, as the case may be, he shall pass an order in writing cancelling the registration of such trust or institution after affording reasonable opportunity of being heard. As per section 12AB(5) of the Act, when trust or institution complied wholly or in part of the income of such trust or institution in violation of section 13(1) of the Act or if they complied with any other law, for the time being in force by the trust or institution as are material for the purpose of achieving its objectives as mentioned in section 12AB(1)(b)(ii) (B) of the Act. However, in the present case, the Id. PCIT invoked the provisions of section 12AB(4)(a)(ii) of the Act as stood in the assessment year 2022-23. The objection of the Id. A.R. is that for the cancellation of registration for the assessment year 2021-22, he could not invoke the provisions of section 12AB(4)(ii) of the Act which is introduced by Finance Act, 2022 w.e.f. 1-4-2022 and applicable for the assessment year 2022-23 onwards.

6.4. In the case of Isthmian Steamship Lines reported in

20 ITR 572 (SC) wherein the Hon’ble Supreme Court held that “it is a cardinal principle of the tax law that law to be applied is that in force in the assessment year unless otherwise provided expressly or by necessary implication”.

6.5. In the case of

Karimtharuvi Tea Estate Ltd. v.

State of Kerala [1964] 51 ITR 129 (SC) the same view was taken by the Hon’ble Supreme Court.

6.6. Further, the Hon’ble Supreme Court in the case of Shree Choudhary Transport Corpn. v. ITO 426 ITR 289 wherein held as under:

17.4. It needs hardly any detailed discussion that in income-tax matters, the law to be applied is that in force in the assessment year in question, unless stated otherwise by express intendment or by necessary implication. As per section 4 of the Act of 1961, the charge of income-tax is with reference to any assessment year, at such rate or rates as provided in any central enactment for the purpose, in respect of the total income of the previous year of any person. The expression “previous year” is defined in section 3 of the Act to mean “the financial year immediately preceding the assessment year”; and the expression “assessment year” is defined in clause (9) of section 2 of the Act to mean “the period of twelve months commencing on the 1st day of April every year”.

17.5. In the case of

CIT v.

Isthmian Steamship Lines (1951) 20 ITR 572 (SC), a 3-judge Bench of this court exposited on the fundamental principle that “in income-tax matters the law to be applied is the law in force in the assessment year unless otherwise stated or implied.” This decision and various other decisions were considered by the Constitution Bench of this court in the case of

Karimtharuvi Tea Estate Ltd. v.

State of Kerala (1966) 60 ITR 262 (SC) and the principle were laid down in the following terms (at pages 264- 266 of 60 ITR):

“Now, it is well-settled that the Income-tax, as it stands amended on the first day of April of any financial year must apply to the assessments of that year. Any amendments in the Act which come into force after the first day of April of a financial year, would not apply to the assessment for that year, even if the assessment is actually made after the amendments come into force.

The High Court has, however, relied upon a decision of this court in CIT v. Isthmian Steamship Lines 3 where it was held as follows:

‘It will be observed that we are here concerned with two datum lines: (1) the 1st of April, 1940, when the Act came into force, and (2) the 1st of April, 1939, which is the date mentioned in the amended proviso. The first question to be answered is whether these dates are to apply to the accounting year or the year of assessment. They must be held to apply to the assessment year, because in income- tax matters the law to be applied is the law in force in the assessment year unless otherwise stated or implied. The first datum line therefore, affected only the assessment year of 1940-41, because the amendment did not come into force till the 1st of April, 1940. That means that the old law applied to every assessment year up to and including the assessment year 1939-40.

This decision is authority for the proposition that though the subject of the charge is the income of the previous year, the law to be applied is that in force in the assessment year, unless otherwise stated or implied. The facts of the said decision are different and distinguishable and the High Court was clearly in error in applying that decision to the facts of the present case.” (Emphasis Supplied)

17.6. We need not multiply on the case law on the subject as the principles aforesaid remain settled and unquestionable. Applying these principles to the case at hand, we are clearly of the view that the provision in question, having come into effect from April 1, 2005, would apply from and for the assessment year 2005-06 and would be applicable for the assessment in question. Putting it differently, the Legislature consciously made the said sub-clause (ia) of section 40(a) of the Act effective from April 1, 20056, meaning thereby that the same was to be applicable from and for the assessment year 2005-06; and neither there had been express intendment nor any implication that it would apply only from the financial year 2005-06.

6.7. Being so, we find force in the argument of Id. A.R. that in income-tax matters, law to be applied is the law in force in the assessment year unless otherwise stated or implied. In the present case, Id. PCIT is cancelling the registration granted u/s 12AA/12AB of the Act w.e.f. previous year 2020-21 relevant to assessment year 2021-22. In our opinion, the law as stated in the assessment year 2021-22 is to be applied and not the law as stood in the assessment year 2022-23.

6.8. Thus, we are of the view that no retrospective cancellation could be made u/s 12AB(4)(ii) of the Act as it has been provided or is seen to have explicitly provided to have a retrospective character or intended. Therefore, without a specific mention of the amended provisions to operate retrospectively, no cancellation for the earlier years could be made. In this regard, it is appropriate to place reliance on the judgement of Hon’ble Madras High Court on the question as to whether the cancellation will operate from a retrospective date in the case of Auro Lab v. ITO 411 ITR 308 (Mad.) wherein held as under:

“20. On the second question as to whether the cancellation will operate from a retrospective date, it was held that the amendment to section 12AA(3) is prospective and not retrospective in character. The courts reasoned that even when Parliament had plenary powers to enact retrospective legislation in matters of taxation, the amended section is not seen to have explicitly provided to have a retrospective character or intend. Therefore, without a specific mention of the amended provisions to operate retrospectively, the cancellation cannot operate from a past date.

21. On the third question of the effective date of operation of the cancellation order, it was held that the cancellation will take effect only from the date of the order/notice of cancellation of registration. Since the act of cancellation of registration has serious civil consequences and the amended provision is held to have only a prospective effect the effect of cancellation, in’ the event the pending tax appeal is decided in favour of the Revenue, will operate only from the date of the cancellation order, that is December 30, 2010. In other words, the exemption cannot be denied to the petitioner for and up to the assessment year 2010-11 on the sole ground of cancellation of the certificate of registration.”

6.9. In this case, the Id. PCIT has cancelled the registration under the new provisions of the Act i.e. 12AB(4) (ii) of the Act, which specifically provides that cancellation can be done for such previous year and all subsequent previous years, which makes it clear that the cancellation cannot be retrospective, therefore, in view of the above discussion, we are of the opinion that cancellation of registration with retrospective effect is invalid in these cases. Since the Id. PCIT invoked the provisions of section 12AB(4)(ii) of the Act, which has been introduced by the Finance Act, 2022 w.e.f. 1/4/2022 so as to cancel the registration with retrospective effect from assessment year 2021-22, which is bad in law. We also note that same view has been taken by Coordinate bench of Mumbai in the case of Heart Foundation of India v. CIT [IT Appeal No. 1524 (Mum.) of 2023, of vide order dated 27-7-2023], wherein held that registration granted u/s 12A of the Act dated 21-7-1989 cannot be cancelled by ld. PCIT (Central) vide order dated 6-3-2023 w.e.f. assessment year 2016-17, by invoking the provisions of section 12AB(4)(ii) of the Act. Accordingly, we allow the primary ground nos.2, 3, 5 & 12 and order of Ld. PCIT passed u/s 12AB(4)(ii) of the Act is quashed.

7. In view of our findings in ground Nos.2, 3, 5 & 12, the grounds of appeal in Ground Nos. 4,6,7,8,9,10,11,13 & 14 have become infructuous as the order of Id. PCIT itself has been quashed.

8. In the result, appeals of the assessee are allowed.” 6.4. Thus, the Tribunal has held that no retrospective cancellation could be made u/sec.12AB(4) of the Act as it has not been provided in the said provision or intended by the legislature in the absence of any specific mention of retrospective application of the said provision. The Tribunal has relied upon various decisions including the Judgment of Hon’ble Madras High Court in the case of

Auro Lab v.

ITO 411 ITR 308 (Mad.) wherein the Hon’ble Madras High Court has held that the cancellation will take effect only from the date of order/notice of cancellation of registration. Similar view was taken by the Bangalore Benches of the Tribunal in the case of Islamic Academy of Education v. PCIT (

supra). This Tribunal has taken a consistent view of this issue as the Delhi Benches of this Tribunal in

the case of Lakhmi Chand Charitable Society v.

PCIT (supra) has also considered an identical issue in Para nos.18 to 22 as under:

“18. Having regard to the judgment as relied upon by the Ld. A.R we are of the considered opinion that the reference made in terms of 2nd proviso of Section 143(3) of the Act to the PCIT to whom the AO was subordinate is not permissible rather it is the CIT(E) Delhi, having territorial jurisdiction specified in Column 4 of the Notification Nos. 52/2014 and 53/2014 both dated 22.10.2014 from whom exemption inter/alia under Section 12A of the Act is being claimed is the appropriate authority. In fact by and under the said notification the CIT(Exemption) has been constituted separately for the purposes mentioned therein. In that view of the matter the order passed by the PCIT cancelling registration of the appellant society on the reference made by the Assessing Officer is found to be flawed and without jurisdiction.

19. Apart from that after considering the 2nd proviso of Section 143(3) of the Act, we find that the reference granted under Section 12AA of the Act is permissible to be made only during the pendency of the assessment proceeding. However, in the case in hand the assessment proceeding has already been concluded on 29.03.2022. In fact, the reference could be made only during the course of assessment proceedings so as to enable the Ld. AO to give effect of the order passed on reference in the Assessment Order itself. More so, the said proviso has been inserted w.e.f 01.04.2022 in the statute to make reference to the PCIT by the AO under Section 12AA, 12AB of the Act. In that view of the matter application of a particular provision of law which was not in existence during the material point of time cannot be said to have been rightly invoked.

20. So far as the provision of Section 12AB(4) of the Act as exercised by the PCIT is concerned the Ld. A.R relied upon a judgment passed by the Bangalore Bench in the case of Islamic Academy of Education v. Pr. CIT (Central) in ITA No. 610/Bang/2023 (Bangalore-Trib.) for Assessment Year 2021-22, a copy whereof has also been annexed to the paper book filed before us by the appellant. While dealing with this particular aspect of the matter the Bench has been pleased to observe as follows:

“8.1.9. Registration Before the amendment by the Finance Act, 2022, Section 12AB(4) provided for cancellation of registration in case of any violation under Section 13. The amended Section 12AB(4) does not consider a violation of Section 13(1)(c) and Section 13(1)(d) as specified violations. Consequently, the registration cannot be cancelled on the ground that the assessee has violated Section 13(1)(c) or Section 13(1)(d).

8.1 .10. The Finance Act 2023 has inserted clause (g) in Explanation to Section 12AB(4) to provide that giving incomplete, false, or inaccurate information in a registration application under Section 12A(/)(ac) will be deemed as a “specified violation” that can lead to the cancellation of registration.

8. 2. Thus, it means that the following registration could be cancelled:

8.2.1. The PCIT/CIT can cancel the following registrations granted to a trust or institution:

(a) Final registration or provisional registration granted under section 12AB(1)(a)/(b)/(c);

(b) Final registration granted under section 12AA(1). The erstwhile provision did not cover cases of provisional registration granted under section 12AB(1)(c). Now, the provisional registration granted for the first time can also be cancelled by the authorities.

8.3. As seen from the above, since the assessee has secured the registration u/s 12A of the Act dated 4.6.1992, which was effective till the date of 23.9.2021 and this registration granted u/s 12A cannot be cancelled u/s 12AB(4)(ii) of the Act for the previous year 2020-21 covering the assessment year 2021-22. On the other hand, he could cancel the registration from assessment year 2022-23 onwards u/s 12AB(4) (ii) of the Act. In our opinion, if there is any violation in the previous assessment year 2020-21 relating to the assessment year 2021-22, this cannot be reason to cancel the registration granted for the assessment year 2022-23 to 2026-27 as the assumption of jurisdiction u/s 12AB(4)(ii) of the Act is itself wrong on the reasons discussed herein above. The specific violation committed by the assessee in any of these assessment years is to be considered independently and not the violation committed in assessment year 2021-22 for cancelling the registration granted u/s 12AB of the Act for the assessment year 2022- 23 to 2026-27. As such, we make it clear that the Id. PCIT at liberty to pass the fresh order of cancellation independently u/s 12AB(4)(ii) of the Act for these assessment years i.e. 2022-23 to 2026-27, if so advised. Accordingly, we allow this ground taken by the assessee. Ordered accordingly.”

21. We find inspiration from the essence of the ratio laid down in the above judgment and observe that in view of the provision of Section 12AA(5) of the Act as the provision of Section 12AA cannot be applied on order after 01.04.2021 the show cause notices issued by the PCIT to the appellant dated 05.07.2023 and 16.08.2023 are, thus, found to be erroneous and therefore liable to be quashed. Once the show cause is found to be non est in the eyes of law, the entire proceeding is naturally found to be on a wrong foundation of law and thus, liable to be set aside. Similarly, invoking the provision of Section 12AB(4) of the Act by the PCIT to cancel registration for specified violation is also not permissible at the same has not seen the light of day prior to 01.04.2022; the same is therefore, not applicable to Assessment Years 2015-16 to 2021-22 as wrongly has been applied in the case in hand.

22. Thus, having regard to these particular facts and circumstances of the case the issuance of show cause notices proposing cancellation of registration alleging specified violation occurred prior to 01.04.2022 i.e. for Assessment Year 2015-16 to 2021-22 and the final order passed by the Ld. PCIT cancelling registration of the appellant society for Assessment Year 2015-16 to 202122 by wrongly invoking the provision of Section 12A r.w.s. 12AA and 12AB(4) of the Act is found to be erroneous, bad in law, whimsical, in non-application of mind and thus, unsustainable.” 6.5. Thus, it is held in the above cited Judgment of Hon’ble High Court and Orders of the Tribunal that the provision of sec.12AB(4) for specific violation do not permit the cancellation of registration with retrospective effect but ITA.No.1128/Hyd./2024 the said provision is only prospective operation and application for cancellation with effect from date of issuing the show cause notice or order of cancellation. The Cuttack Bench of the Tribunal in the case of People Forums v. CIT(E) (supra) has also considered this issue in Para nos.19 and 20 as under:

“19. We have considered the rival submissions. Admittedly, the proceedings for cancellation of the registration u/s.12A to the assessee had been initiated by the Id CIT(E) as early as on 18.10.2016 being after a reasonable period from the date of the survey on the assessee. Admittedly, the assessee had responded to the same and it is an admitted fact that the proceedings did not continue after the show cause notice and reply filed by the assessee. The provisions of section 12AB(4) provide for the time limit in regard to passing of an order in respect of cancellation of the registration but the said provision refers to the first notice to be issued on or after 1st April, 2022. There is no saving provision in regard to the proceedings initiated prior to 1 April, 2022 and which admittedly being not calumniated into an order being served on the assessee. A perusal of the show cause notice issued by the Id CIT(E) on 6.10.2022 admittedly also does not refer to a show cause notice having been issued on 18.10.2016 and, therefore, it cannot be treated as a continuation of the proceedings either. The main crux of the cancellation of the registration is (1) whether the activity of the assessee is business activity or charitable activity. Admittedly, this has reached finality for the assessment year 2009-10 to 2011-12, wherein, the Coordinate Bench of this Tribunal have held the issue in favour of the assessee. The second issue is in regard to donation to Aids Awareness Trust of Orissa and the questioned the existence of the trust. The assessee has produced the assessment order in the case of said trust and the assessment order passed also refers to its registration by the Id CIT(A). Therefore, the second issue could fall to the ground on account of the act of the department itself in regard to the assessment and in regard to registration by the Id CIT(E). It is also admitted by ld CIT(E) that there are no common trustees nor any related trustee between the assessee trust and Aids Awareness Trust of Orissa. In any case, both the issue had been raised by the Id CIT(E) in its original show cause notice which had been culminated in the orders served on the assessee. A new issue which has been raised by the Id CIT(E) in the show cause notice dated 6.10.2022 is the details of the corpus donation. Admittedly, this was the subject matter of 263 proceedings and that the issue had been considered by the Hon’ble Jurisdictional High Court and the Hon’ble High Court had found the orders of Id CIT to be unsustainable and also quashed the same. Thus, all the issues on which the Id CIT(E) has raised the show cause notice for the purpose of cancellation of registration u/s.12A have already been decided by the Appellate Authority and same has also reached finality. The Id CIT(E) by his order dated 20.6.2023 being the impugned order has tried to unsettle issues which are already settled in the case of the assessee. This is not permissible. This being so, as it is noticed that all the issues on the basis of which, ld CIT(E) has cancelled the registration u/s.12A granted to the assessee has already been settled by various appellate authorities on earlier occasion and the issue had reached finality, same cannot be used for cancelling the registration of the assessee. This being so, on merits also, the order passed u/s.12AB(4) by the Id ITA.No.1128/Hyd./2024 CIT(E) on 20.6.2023 cancelling the registration granted to the assessee stands quashed.

20. We are not going into the issue as to whether the registration can be cancelled retrospectively though we are of the view that retrospective cancellation w.e.f. 1.1.2014 is erroneous as we have already quashed the cancellation of registration.”

6.6. This view has been reiterated by the Bangalore Bench of the Tribunal in the case of Amala Jyothi Vidya Kendra Trust v. PCIT (supra) in Para nos.6.8 to 6.10 as under:

“6.8. Thus, we are of the view that no retrospective cancellation could be made u/s 12AB(4)(ii) of the Act as it has been provided or is seen to have explicitly provided to have a retrospective character or intended. Therefore, without a specific mention of the amended provisions to operate retrospectively, no cancellation for the earlier years could be made. In this regard, it is appropriate to place reliance on the judgment of Hon’ble Madras High Court on the question as to whether the cancellation will operate from a retrospective date in the case of Auro Lab Ltd. v. ITO (Madras) therein held as under:

“20. On the second question as to whether the cancellation will operate from a retrospective date, it was held that the amendment to section 12AA(3) is prospective and not retrospective in character. The courts reasoned that even when Parliament had plenary powers to enact retrospective legislation in matters of taxation, the amended section is not seen to have explicitly ITA.No.1128/Hyd./2024 provided to have a retrospective character or intend. Therefore, without a specific mention of the amended provisions to operate retrospectively, the cancellation cannot operate from a past date.

21. On the third question of the effective date of operation of the cancellation order, it was held that the cancellation will take effect only from the date of the order/notice of cancellation of registration. Since the act of cancellation of registration has serious civil consequences and the amended provision is held to have only a prospective effect the effect of cancellation, in’ the event the pending tax appeal is decided in favour of the Revenue, will operate only from the date of the cancellation order, that is December 30, 2010. In other words, the exemption cannot be denied to the petitioner for and up to the assessment year 2010- 11 on the sole ground of cancellation of the certificate of registration. “

6.9 . In this case, the Ld. PCIT has cancelled the registration under the new provisions of the Act i.e. 12AB(4) (ii) of the Act, which specifically provides that cancellation can be done for such previous year and all subsequent previous years, which makes it clear that the cancellation cannot be retrospective, therefore, in view of the above discussion, we are of the opinion that cancellation of registration with retrospective effect is invalid in these cases. Since the Id. PCIT invoked the provisions of section 12AB(4)(ii) of the Act, which has been introduced by the Finance Act, 2022 w.e.f. 1.4.2022 so as to cancel the registration with retrospective effect from assessment year 2018-19, which is bad in law.

6.10. It is noted that coordinate bench of this Tribunal in both assessee’s case for AY 2021-22 has taken similar view and as quashed the retrospective applicability of the new amended provision u/s 12AB(4)(if) of the Act. We also note that same view ITA.No.1128/Hyd./2024 has been taken by Coordinate bench of Mumbai in the case of Heart Foundation of India in ITA No.1524/Mum/2023 vide order dated 27.7.2023, wherein held that registration granted u/s 12A of the Act dated 21.7.1989 cannot be cancelled by Id. PCIT (Central) vide order dated 6.3.2023 w.e.f. assessment year 2016- 17, by invoking the provisions of section 12AB(4)(ii) of the Act. Accordingly, we allow the primary ground nos.2, 3, 5 & 12 and order of ld. PCIT passed u/s 12AB(4) (ii) of the Act is quashed.” 6.7. Accordingly, in the facts and circumstances of the case and in view of the precedents as cited above, we hold that the impugned order passed by the learned CIT(E) cancelling the registration granted u/sec.12AA under the provisions of sec.12AB(4) r.w.s.12AB(5) with effect from assessment year 2015-2016 onwards is not sustainable in law and the same is set aside.”

19. On perusal of the above, we find that the Coordinate Bench of this Tribunal has categorically held that registration granted under section 12A/12AB of the Act cannot be cancelled retrospectively by invoking the provisions of section 12AB(4) of the Act. Therefore, respectfully following the aforesaid decision of the Coordinate Bench and considering the facts and circumstances of the present case, we hold that the retrospective cancellation of registration granted to the assessee under section 12A/12AB of the Act with effect from 29.07.2016 by the Ld. CIT (E) is not sustainable in the eyes of law. Accordingly, we set aside the impugned order passed by the Ld. CIT(E) under section 12AB(4) of the Act.

20. In the result, the appeal of the assessee in ITA No. 631/Hyd/ 2024 is allowed.

21. To sum up, both the appeals of the assessee are allowed.