Scope of Enquiry and Jurisdictional Validity in Renewal of Trust Registration

Facts

-

Background: The Assessee is an educational society originally registered under Section 12AA. Following a search on the group, its registration was cancelled, but the Tribunal later set aside that cancellation.

-

New Scheme Compliance: Under the revamped registration regime, the Assessee obtained provisional/regular registration (Form 10AC) for AYs 2022-23 to 2026-27.

-

Settlement Commission: For historical search years (AY 2013-14 to 2020-21), the Settlement Commission admitted the Assessee’s plea, noting no conclusive evidence of siphoning or diversion of funds.

-

The Dispute: The Assessee applied for a five-year renewal of registration under Section 12A(1)(ac)(ii).

-

Rejection: The Principal Commissioner (Central) rejected the renewal by relying on search material from AY 2014-15 to 2019-20 and the income disclosed before the Settlement Commission.

-

Jurisdiction Issue: The application was originally filed before the Commissioner (Exemptions) but was transferred to and adjudicated by the Principal Commissioner (Central) due to the “centralization” of the Assessee’s PAN.

Decision

-

Final Verdict: In favour of the Assessee (Registration directed to be renewed).

-

Ratio Decidendi:

-

Limited Scope of Section 12AB: The Court held that the enquiry for renewal is strictly limited to the genuineness of activities and compliance with other laws.

-

Temporal Restriction: Per Rule 17A, the Commissioner’s examination is restricted to the three immediately preceding years. By relying on search material from 2014-15, the Principal Commissioner exceeded his statutory mandate.

-

Improper Linkage: Renewal proceedings cannot be used as a back-door for cancellation proceedings. Since the activities (education) were per se charitable and the AO confirmed their genuineness, renewal could not be denied based on “stale” search material.

-

Lack of Jurisdiction: Following established precedents and Notifications No. 52 and 53 of 2014, the power to adjudicate registration/renewal rests solely with the Commissioner (Exemptions). The Principal Commissioner (Central) lacks subject-matter competence and territorial jurisdiction for Section 12AB orders, even if the PAN is centralized for assessment.

-

Key Takeaways

-

Jurisdictional Shield: “Centralization” of a case for search assessment does not automatically grant the Central Circle PCIT the power to cancel or refuse 12AB registration. Always verify the designation of the officer passing the order against CBDT notifications; orders by non-Exemption Commissioners are void ab initio.

-

The “Three-Year” Rule: Use Rule 17A to block the Department from digging into old search materials during a renewal cycle. The law explicitly limits their gaze to the three years immediately preceding the application.

-

Genuineness vs. Disclosure: Disclosure of income before a Settlement Commission or during a search does not automatically render a trust’s activities “non-genuine,” especially if the core activity (education) continues to be performed.

-

IT Act 2025 Preparedness: Under the renumbered Sections 332 and 351, the separation of “Assessment Jurisdiction” (Central Circle) and “Registration Jurisdiction” (Exemption Wing) remains a critical compliance check for Chartered Accountants.

and Manoj Kumar Aggarwal, Accountant Member

[Assessment year 2026-27]

| (a) | The ld. PCIT has no jurisdiction to adjudicate application for renewal of registration u/s 12A(1)(ac)(ii) ; |

| (b) | The ld. PCIT has erred in rejecting this application and declining the prayer of assessee for grant of registration. |

| 1. | The order rejecting renewal of registration of the assessee society under 12A(1)(ac)(ii) of the Act, dated 26.12.2025, passed by the learned PCIT(Central) is bad in law, contrary to facts, and based on erroneous interpretation of statutory provisions and judicial precedents, and is therefore liable to be set aside. |

| 2. | That the jurisdiction assumed by the learned PCIT (Central) Gurgaon in the proceedings under section 12A of the Act is bad in law on account of following: |

| 2.1 | That the PCIT (Central), Gurgaon has erred in exercising jurisdiction in a proceedings under section 12A of the Act in the case of the assessee society since, in view of Notification No. 52/2014 [F.No.187/38/2014(ITA.I)], the jurisdiction to take any action regarding registration under section 12A of the Act in the instant case, vested exclusively with the Ld. CIT (Exemptions), Chandigarh. |

| 3. | That the learned PCIT (Central), Gurgaon exceeded the jurisdiction vested in law in a proceeding under section 12A of the Act on account of following: |

| 3.1 | That the learned PCIT (Central), erred in law by relying on records of A.Ys. 2014-15 to 2019-20 in the Show Cause Notice dated 17-12-2025 and final rejection order dated 26.12.2025, which is in contravention to Rule 17A of the Income-tax Rules, 1962, which permits examination of only three assessment years preceding the year of application. As the application before learned PCIT (Central) pertained to A.Y. 202627, only A.Ys. 2023-24 to 2025-26 could have been examined; hence, the show cause notice based on earlier years is legally untenable. |

| 3.2 | That the impugned order of the Ld. PCIT (Central), Gurgaon, founded solely on allegations relating to Assessment Years 2014-15 to 2019-20 (i.e., prior to 01.04.2022), is unsustainable in law, as the appellant trust had already been granted registration on 15.10.2021 for AYs 2022-23 to 2026-27, after the search dated 03.10.2019, and no adverse action could thereafter be taken on the basis of alleged past violations. |

| 4. | That the order of learned PCIT (Central), Gurgaon is violative of principles of natural justice since; |

| 4.1 | The learned PCIT (Central), Gurgaon, erred in cancelling the registeration of the assessee society on various grounds which were never show caused to the assessee, hence, the order dated 26.12.2025 is bad in law. |

| 5. | That the order of the learned PCIT (Central), Gurgaon, is legally flawed and hit by the principle of judicial discipline since; |

| 5.1 | That the Ld. PCIT (Central), Gurgaon has erred in law and on facts in cancelling the registration of the appellant trust by completely ignoring the fact that the order passed by the Income-tax Settlement Commission (IBS) under section 245D(4) contains no finding, observation, or direction whatsoever for withdrawal or denial of exemption to the appellant trust on the basis of the allegations made by the Department. That in the absence of any such adverse finding in the order passed under section 245D(4), the impugned cancellation of registration is arbitrary, without jurisdiction, and unsustainable in law. |

| 6. | That the learned PCIT (Central) has erred in law and on facts in rejecting the appellant’s application ignoring the actions of the Learned Jurisdictional Assessing Officer; |

| 6.1 | The learned PCIT (Central) erred in rejecting the application of the assessee on issues pertaining to Assessment Years 2014-15 to 2019-20, by completely ignoring the fact that no reference was made by the Assessing Officer, as mandated under the second proviso to section 143(3), for the Assessment Years 2014-15 to 2019-20, despite the fact that the order of the Settlement Commission was passed on 30 December 2023. |

| 6.2 | The learned PCIT (Central) erred in rejecting the application of the assessee trust while completely ignoring the fact that learned Assessing Officer had duly submitted an inspection report of the assessee trust affirming that it is conferring education to around 40,000 students as per its objectives. |

| 7. | That the PCIT(Central) erred in law and on facts in cancelling the registration of the appellant by alleging that the genuineness of activities and compliance with the requirements of other laws had not been complied with. The learned PCIT failed to bring on record any cogent material or documentary evidence to demonstrate which specific provisions of any other law were violated, or how the activities of the trust were not genuine. The cancellation is thus based on vague, unsubstantiated allegations and is arbitrary, unjustified, and liable to be quashed. |

| 8. | That the Ld. PCIT (Central), Gurgaon has erred in law and on facts in rejecting the exemption/registration of the appellant society by making various unfounded assertions regarding alleged misutilisation of funds, which are contrary to the material on record and the binding findings of the Settlement Commission. |

| 8.1 | That the Ld. PCIT (Central) has erred in law and on facts in rejecting the registration by ignoring the categorical findings of the Settlement Commission that no siphoning, diversion, or misutilisation of funds was established, and that the mere absence of vouchers relating to capital work-in-progress cannot, by itself, justify any adverse inference. The allegation of diversion of funds by the trustees, being wholly unsupported by evidence, is arbitrary and unsustainable in law. |

| 8.2 | That the Ld. Pr. CIT(C) has erred in law and on facts in rejecting the application for registration by relying upon seized material which is prior to the introduction of section 12AB and unrelated to the year under consideration, without appreciating that such material partly represented anonymous donations and partly income already offered to tax by the trustee i.e Rashpal Singh Dhiman, and that no funds were siphoned off or used for the personal benefit of the trustee. The rejection of registration on such basis is beyond the scope of enquiry at the registration stage and is unsustainable in law. |

| 9. | The appellant craves leave to add, amend or alter any of the grounds of appeal. |

| Sl. No | Particulars | Section | Date | Remarks |

| 1 | Registration Granted | 12AA | 31-10-2001 | Registration granted under Section 12AA of the Income-tax Act, 1961 (Refer page no. 1 of PB) |

| 2 | Search on Chandigarh Group | 132 | 03-10-2019 | Search conducted under Section 132 of the Act. |

| 3 | Cancellation of Registration | 12AA(4) | 22-03-2021 | Registration cancelled by invoking Section 12AA(4). |

| 4 | Appeal before ITAT -Matter Rv. stored | 31-08-2021 | ITAT set aside cancellation and remanded matter for fresh adjudication (Refer page nos. 92-124 of PB-2) | |

| 5 | Application before Interim 3oard for Settlement | 245C | 17-09-2021 | Application filed seeking settlement of issues. |

| 6 | Application in Form 10AC | 12A(l)(ac)(i) | 15-10-2021 | Application filed for registration under amended provisions post 01-04- 2021 and granted registration from AY 2022-23 to AY 2026-27 (Refer page no. 2-4 of PB) |

| 7 | Appeal before Punjab & Haryana High Court | 260A | 03-02-2022 | Department filed appeal; substantial questions of law admitted |

| 8 | Order by IBS | 245D(4) | 30-12-2023 | Settlement order passed; binding on the Department (Refer page no. 23-88 of PB) |

| 9 | Assessment Order for AY 2022-23 | 143(3) | 29-03-2024 | Accepted the activities of the trust as genuine (Refer page nos. 89-91 of PB- 2) |

| 10 | Transfer of Exemption application by CIT(E) to PCIT(C) | 13-11-2025 | (Refer page no. 3 of rejection order) | |

| 11 | Report of AO in response to PCIT letter dated 04-12-2025 | 04-12-2025 | (Refer page nos.136-138 of PB-2) | |

| 12 | Application in Form 10AB | 12A(1)(ac)(ii) | 19.05.2025 | Registration rejected by PCIT (Central) (Refer page Nos. 5-13 of PB) |

—(i) where the trust or institution is registered under section 12A [as it stood immediately before its amendment by the Finance (No. 2) Act, 1996 (33 of 1996)] or under section 12AA [as it stood immediately before its amendment by the Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020 (38 of 2020)], within three months from the first day of April, 2021;

(ii) where the trust or institution is registered under section 12AB and the period of the said registration is due to expire, at least six months prior to expiry of the said period;

(iii) where the trust or institution has been provisionally registered under section 12AB, at least six months prior to expiry of period of the provisional registration or within six months of commencement of its activities, whichever is earlier;

(iv) where registration of the trust or institution has become inoperative due to the first proviso to sub-section (7) of section 11, at least six months prior to the commencement of the assessment year from which the said registration is sought to be made operative;

(v) where the trust or institution has adopted or undertaken modifications of the objects which do not conform to the conditions of registration, within a period of thirty days from the date of the said adoption or modification;

(vi) in any other case, where activities of the trust or institution have –

(A) not commenced, at least one month prior to the commencement of the previous year relevant to the assessment year from which the said registration is sought;

(B) commenced and no income or part thereof of the said trustor institution has been excluded from the total income on account of applicability of sub-clause (iv) or sub-clause (v) or sub-clause (vi) or sub-clause (via) of clause (23C) of Section 10, or Section 11 or Section 12, for any previous year ending on or before the date of such application, at any time after the commencement of such activities and such trust or institution is registered under Section 12AB;]

x x x

12AB. [Procedure for fresh registration.

12AB. (1)The Principal Commissioner or Commissioner, on receipt of an application made under clause (ac) of sub-section (1) of section 12A, shall,—

(a)where the application is made under sub-clause (i) of the said clause, pass an order in writing registering the trust or institution for a period of five years;

(b)where the application is made under sub-clause (ii) or sub-clause (iii) or sub-clause (iv) or sub-clause (v) or item (B) of sub-clause (vi) of the said clause,-

(i) call for such documents or information from the trust or institution or make such inquiries as he thinks necessary in order to satisfy himself about—

(A) the genuineness of activities of the trust or institution; and

(B) the compliance of such requirements of any other law for the time being in force by the trust or institution as are material for the purpose of achieving its objects;

(ii) after satisfying himself about the objects of the trust or institution and the genuineness of its activities under item (A) and compliance of the requirements under item (B), of sub-clause (i),—

(A) pass an order in writing registering the trust or institution for a period of five years; or

(B) if he is not so satisfied, pass an order in writing-

(I) in a case referred to in sub-clause (ii) or subclause (iii) or sub-clause (v) of clause (ac) of subsection (1) of Section 12A rejecting such application and also cancelling its registration ;

(II) in a case referred to in sub-clause (iv) or in item (B) of sub-clause (vi) of sub-section (1) of Section 12A, rejecting such application, after affording a reasonable opportunity of being heard;

(c) where the application is made under item (A) of sub-clause (vi) of the said clause or the application is made under sub-clause (vi) of the said clause, as it stood immediately before its amendment vide the Finance Act, 2023, pass an order in writing provisionally registering the trust or institution for a period of three years from the assessment year from which the registration is sought, and send a copy of such order to the trust or institution.

x x x

| (a) | The genuineness of activities of the Trust or Institution, |

| (b) | The compliance of such requirements of any other law for the time being in force by the Trust or Institution as are material for the purpose of achieving its objectives. |

(a) the Principal Commissioner or Commissioner has noticed occurrence of one or more specified violations during any previous year; or

(b) the Principal Commissioner or Commissioner has received a reference from the Assessing Officer under the second proviso to sub-section (3) of section 143 for any previous year; or

(c) such case has been selected in accordance with the risk management strategy, formulated by the Board from time to time, for any previous year,

the Principal Commissioner or Commissioner shall—

(i) call for such documents or information from the trust or institution, or make such inquiry as he thinks necessary in order to satisfy himself about the occurrence or otherwise of any specified violation;

(ii) pass an order in writing, cancelling the registration of such trust or institution, after affording a reasonable opportunity of being heard, for such previous year and all subsequent previous years, if he is satisfied that one or more specified violations have taken place;

(iii) pass an order in writing, refusing to cancel the registration of such trust or institution, if he is not satisfied about the occurrence of one or more specified violations;

(iv) forward a copy of the order under clause (ii) or clause (iii), as the case may be, to the Assessing Officer and such trust or institution.

(a) where any income derived from property held under trust, wholly or in part for charitable or religious purposes, has been applied, other than for the objects of the trust or institution; or

(b) the trust or institution has income from profits and gains of business which is not incidental to the attainment of its objectives or separate books of account are not maintained by such trust or institution in respect of the business which is incidental to the attainment of its objectives; or

(c) the trust or institution has applied any part of its income from the property held under a trust for private religious purposes, which does not enure for the benefit of the public; or

(d) the trust or institution established for charitable purpose created or established after the commencement of this Act, has applied any part of its income for the benefit of any particular religious community or caste; or

(e) any activity being carried out by the trust or institution—

(i) is not genuine; or

(ii) is not being carried out in accordance with all or any of the conditions subject to which it was registered; or

(f) the trust or institution has not complied with the requirement of any other law, as referred to in item (B) of sub-clause (i) of clause (b) of sub-section (1), and the order, direction or decree, by whatever name called, holding that such noncompliance has occurred, has either not been disputed or has attained finality; or

(g) the apo referred to in clause (ac) of sub-section (1) of Section 12A is not complete or it contains false or incorrect information.

| (a) | The genuineness of activities of the Trust or Institution; |

| (b) | The compliance of such requirements of any other law for the time being in force by the Trust or Institution as are material for the purpose of achieving its objectives. |

| Sr no. | Name of the Case | Citation | Tribunal/Court | |

| CASE LAWS REGARDING NO CANCELLATION OF REGISTRATION ON ABSENCE OF BILLS OR VOUCHERS | ||||

| 1. | Kunhitharuvai Memorial Charitable Trust v. CIT (Central) | [IT Appeal No. 246 (Coch.) of 2014, dated 16-1-2018]/2017 (1)TMI 1671 | ITAT COCHIN | |

| 2. | Kosuke Sports Foundation v. Dy. CIT | [IT Appeal Nos. 1194 and 1195 (PUN) of 2025, dated 29-08-2025]/2025 (II)TMI 452 | ITAT PUNE | |

| 3. | Saraswati Educational & Welfare Society v. CIT, Exmp | [IT Appeal No. 157 (Asr.) of 2020, dated 16-8-2021]/2021 (9) TMI 840 | ITAT AMRITSAR | |

| 4. | CIT v. B.K.K. Memorial Trust | Punjab & Haryana | ||

| 5. | CIT v. Baba Deep Singh Educational Society | Punjab & Haryana | ||

| 6. | DIT v. Garden City Educational Trust | Karnataka | ||

| 7. | CIT v. Surya Educational & Charitable Trust | 53/[2013] 355 ITR 280 (Punjab & Haryana) | Punjab & Haryana | |

| 8. | CIT v. Red Rose School | (Allahabad) | HIGH COURT OF ALLAHABAD | |

| 9. | Ajit Education Trust v. CIT | [2010] 42 SOT 415 (Ahmedabad – ITAT) | ITAT AHMEDABAD | |

| 10. | Mata Parvati Educational & Innovative Society v. CIT (E) | [IT Appeal No. 2296 (DEL) of 2018, dated 29.03.2019]/2019 (4) TMI 213 | ITAT DELHI | |

| 11. | Vidyadayani Shiksha Samiti v. CIT (Exemption) | [IT Appeal No. 309 (Delhi) of 2016, dated 14-12-2017]/2017(12] TMI1251 | ITAT DELHI | |

| 12. | Bhartiya Kisan Sangh Sewa Niketan v. CIT (Exemptions) | (Delhi – Trib.)/ 2017(8] TMI 1065 | ITAT DELHI | |

| CASE LAWS REGARDING PROSPECTIVE APPLICATION OF SECTION 12AB | ||||

| 13. | Ram Saran Das Kishori Lal Charitable Trust v. CIT (Exemption) | (Delhi – Trib.) | ITAT DELHI | |

| 14. | Islamic Academy of Education v. Pr. CIT (Central) | (Bangalore – Trib.) | ITAT BANGALORE | |

| 15. | CIT v. Apeejay Education Society | (Punjab & Haryana)/2015 (4) TMI 303 | PUNJAB & HARYANA HIGH COURT | |

| 16. | CIT(Central) v. Islamic Academy of Education | (Karnataka)/2015(9] TMI 450 | KARNATAKA HIGH COURT | |

| 17. | M.M. Patel Charitable Trust v. Pr. CIT (Central) | PUNE TRIBUNAL | ||

| 18. | Seth PannaLal Charitable Trust v. CIT (Exemptions) | DELHI TRIBUNAL | ||

| 19. | Raya Naik Memorial Gowshala Trust v. CIT (Exemptions) | (Bangalore – Trib.) | BANGALORE TRIBUNAL | |

| 20. | Vishwayatan Yogasharam v. CIT (Exemption) | [IT Appeal No. 428 (Asr) of 2016, dated 13-12-2017]/2017 (21) TMI 1546 | ITAT AMRITSAR | |

| 21. | Prabhat (A House of Hope for Special Children) v. CIT (Exemptions) Chandigarh, And Vice-Versa | [IT Appeal Nos. 687 & 688/Chd/2015, dated 9-2-2016]/2016(21 TMI | ITAT | |

| 1097 | CHANDIGARH | |||

| 22. | Gopsai Avinandan Sangha v. CIT (Exemption), Kolkata reported in | [IT Appeal Nos. 232 & 233 (KOL) of 2020, dated 12-04-2021]/2021 (4) TMI 731 | ITAT KOLKATA | |

| 23. | Punjab Heritage & Tourism Promotion Board v. CIT (Exemptions) | ITAT CHANDIGARH | |

| 24. | Dera Sacha Sauda v. Pr. CIT (Central) | [IT Appeal No. 21 (CHD) of 2024, dated 25-04-2025]/2025 (4) TMI 1736 | ITAT CHANDIGARH |

| 25. | Aryans Educational & Charitable Trust v. CIT(Exemptions) | ITAT CHANDIGARH | |

| 26. | Ram Saran Das Kishori Lal Charitable Trust (supra) | ||

| 27. | Rukmini Educational Charitable Trust v. Pr. CIT (Central) | ITAT BANGALORE | |

| 28. | Sushila Devi Centre for Professional Studies and Research v. Pr. CIT (Central) | ITAT DEHRADUN | |

| 29. | Lakhmi Chand Charitable Society v. Pr. CIT, Central | ITAT Delhi | |

| 30. | Sushila Devi Centre for Professional Studies and Research (supra) | ||

| CASE LAWS REGARDING LACK OF JURISDICTION WITH PCIT | |||

| 31. | Aggarwal Vidya Pracharni Sabha v. Pr. CIT | [IT Appeal No. 1308 (Delhi) of 2023, dated 8-1 2024] | ITAT Delhi |

| 32. | Pacific Academy of Higher Education and Research Society v. Pr. CIT (Central) | [IT Appeal No. 4 (Jodh) of 2020, dated 25-1-2023]/2023 (l)TMI | ITAT |

| 1283 | JODHPUR | ||

| 33. | Lala Sher Singh Memorial Jeevan Vigyan Trust Society v. Pr. CIT (Central) | DELHI TRIBUNAL | |

| 34. | Meenakshi foundation v. Pr. CIT | DELHI TRIBUNAL | |

| 35. | Hemkunt Foundations v. Pr. CIT, Central | DELHI TRIBUNAL | |

| 36. | Dera Sacha Sauda (supra) | ||

| 37. | ITAT DEHRADUN | ||

| 38. | Wholesale Cloth Merchant Association v. Pr. CIT (Central) | [IT Appeal No.688 (JP) of 2019, dated 6-1-2021]/2021 (1) TMI 876 | ITAT JAIPUR |

| 39. | Devi Shakuntala Thkaral Charitable Foundation v. Pr. CIT (Central) | [IT Appeal Nos.117 (Ind) of 2020, dated 29-7-2022]/2022 (7) TMI 1591 | ITAT INDORE |

| 40. | Oriental University Indore v. Pr. CIT (Central) | [IT Appeal Nos.115 & 116 (Ind) of 2020, dated 29-7-2022]/2022 (7) TMI 1609 | ITAT INDORE |

| 41. | Arya Smaj Model Town v. Pr. CIT, Central | (Delhi – Trib.)/2025 (7) TMI 31 | ITAT DELHI |

| 42. | Ambernath City Hospital (P.) Ltd. v. UOI [ | (Bombay) | HIGH COURT OF BOMBAY |

| 43. | Reuters Asia Pacific Ltd. v. Dy. CIT, International Taxation | ITAT MUMBAI | |

| 44. | Vijay Corporation v. ITO | ITAT MUMBAI |

| (a) | Activities which are per-se charitable, namely education, yoga, medical relief, relief to poor, etc. |

| (b) | The advancement of any other object of general public utility. |

| (a) | Activities of the assessee Trust are genuine, |

| (b) | It has not violated any other allied laws |

| 1. | Aggarwal Vidya Pracharni Sabha v. PCIT, ITA No. 1308 /DEL/2023 dated 08.01.2024 (ITAT Del.) |

| 2. | Heart Foundation of India v. CIT (Central), ITA 1524/Mum/2023 dated 27.07.2023 (ITAT Mum.) |

| 3. | Pacific Academy of Higher Education and Research Society v. PCIT (Central) ITA 04-05/Jodh/2020 dated 25.01.2023, (ITAT Jodh.) |

| 4. | Wholesale Cloth Merchants Association v. PCIT (Central), ITA 688/JP/2019 dated 06.01.2021 (ITAT Jaipur) |

| 5. | M/s. Amala Jyothi Vidya Kendra Trust, Bangalore v. PCIT(Central), ITA No.l41/Bang/2024 dated 16.04.2024 (ITAT Bang.) |

| 6. | Laskhmi Chand Charitable Society v. PCIT (Central- 3) ITA 1803/Del/2024 dated 22.08.2024. |

“The aforementioned case came up for hearing before the Hon’ble Bench on 05.03.2025.

2. The appellant assessee has taken an additional ground of appeal challenging the jurisdiction of the Ld. PCIT in cancelling the registration u/s 12AA. The appellant has contended that it is the Commissioner of Income Tax (Exemptions)- CIT(E) – and not the Principal Commissioner of Income Tax -(PCIT), who was the competent authority to cancel the registration. The appellant also submitted copies of few judgments of the Hon’ble ITAT Benches in support of his contentions, including the judgment of the Hon’ble ITAT Bench, Delhi in the case of Lakhmi Chand Charitable Society v. PCIT, Cen- 3, New Delhi in ITA No. 1803/Del/2024 pronounced on 22.08.2024.

3. In this regard, it is submitted that from the plain reading of the text of sections 12AB(4) and second Proviso to section 143(3), it is abundantly clear that the intent of the legislature was to provide the powers of cancellation of registration u/s 12AA to both the CIT(E) as well as the PCIT. This is because the words ‘Principal Commissioner of Income Tax’ have been used in marked distinction to the words ‘Commissioner of Income Tax (Exemptions)’ in both the sections. It is pertinent to mention here that the scheme of the Income Tax Act, 1961 provides for only the Commissioner rank officers to hold the charge of Exemptions. The Income Tax Act, 1961 nowhere provides for a Principal Commissioner rank officer to hold the charge of Exemptions. This would evidently imply that other than the Commissioner of Income Tax (Exemptions), the legislature in its wisdom has decided to endow other officers also – viz Principal Commissioners of Income Tax, who are higher in rank to the Commissioner (Exemptions) and are not holding the charge of Exemptions with the authority to cancel the registration under Section 12AA of the Act.

4. In support of the above contentions, the undersigned is relying on the judgment of the Hon’ble ITAT Pune Bench in the case of Sinhgad Technical Education Society v. PCIT – (copy enclosed) . The registration cancelled by the Ld. PCIT has been upheld by the Hon’ble Bench in the said case.

5. In the latest judgment dated 02.04.2025 of the Hon’ble ITAT Dehradun Bench, New Delhi rendered in the case of M/s Sri Krishan Educational Trust v. DGIT (Inv) – ITA No. 4092/DDN/2015 (copy enclosed), the Hon’ble Bench has categorically observed vide para 4 of the judgment that the prescribed authority for granting the approval or cancelling the approval u/s 10(23C)(vi) of the Act is the Principal Commissioner of Income Tax or the Commissioner of Income Tax (Exemptions). It shall be pertinent to mention here that although the said judgment has been rendered in the context of section 10(23C)(vi), but by drawing a parallel analogy, the intention of the Hon’ble ITAT Bench is extendable to the provisions of the registration u/s 12AA as well. This is because the schemes of sections 10(23C)(vi) and 12AA are the same and the words used in section 10(23C)(vi) are the same as in section 12AB(4), i.e. both the Principal Commissioner of Income Tax and the Commissioner of Income Tax (Exemptions) are competent to cancel the registration under both the respective sections when a reference is received from the assessing officer under second Proviso to section 143(3) of the Act. The text and the content of the 15th proviso to section 10(23C) is the same as that of section 12 AB(4). To augment my contention, the relevant 15th Proviso of section 10(23C)(vi) is reproduced below:

“Provided also that where the fund or institution referred to in sub-clause (iv) or trust or institution referred to in sub-clause (v) or any university or other educational institution referred to in sub-clause (vi) or any hospital or other medical institution referred to in sub-clause (via) is approved or provisionally approved under the said clause and subsequently –

(a) the Principal Commissioner or Commissioner has noticed occurrence of one or more specified violations during any previous year’; or

(b) the Principal Commissioner or Commissioner has received a reference from the Assessing Officer under the second proviso to sub-section (3) of section 143 for any previous year; or..”

6. Furthermore, the judgment rendered in the case of Sri Krishan Educational Trust (supra) is the latest judgment of the Hon’ble ITAT, New Delhi and shall prevail over the earlier judgments rendered by the coordinate Benches of ITAT, Delhi which have been relied upon by the appellant assessee. It will also not be out of place to state that the judgment of the Hon’ble ITAT, Delhi Bench in the case of Lakhmi Chand Charitable Society v. .PCIT, Cen-3, New Delhi, so heavily relied upon by the assessee, has been challenged by the Department before the Hon’ble Delhi High Court (screenshot attached as evidence).

7. Thus, when there are contradictory decisions of the coordinate Benches of the Hon’ble ITAT on the impugned issue, it shall be prudent to await the orders of the Hon’ble Delhi High Court.Even otherwise, the latter decision of the Hon’ble ITAT, Delhi shall prevail over the earlier decisions rendered by the coordinate Benches of Hon’ble ITAT, Delhi as already argued above.

8. It is therefore, humbly submitted that the additional ground raised by the assessee challenging the jurisdiction of the PCIT in cancelling the registration u/s 12 AA, is without any basis and therefore, deserves to be dismissed.”

“Jurisdiction of income-tax authorities.

120. (1) Income-tax authorities shall exercise all or any of the powers and perform all or any of the functions conferred on, or, as the case may be, assigned to such authorities by or under this Act in accordance with such directions as the Board may issue for the exercise of the powers and performance of the functions by all or any of those authorities.

Explanation.—For the removal of doubts, it is hereby declared that any income-tax authority, being an authority higher in rank, may, if so directed by the Board, exercise the powers and perform the functions of the income-tax authority lower in rank and any such direction issued by the Board shall be deemed to be a direction issued under sub-section (1).

(2) The directions of the Board under sub-section (1) may authorise any other income-tax authority to issue orders in writing for the exercise of the powers and performance of the functions by all or any of the other income-tax authorities who are subordinate to it.

(3) In issuing the directions or orders referred to in sub-sections (1) and (2), the Board or other income-tax authority authorised by it may have regard to any one or more of the following criteria, namely :—

(a) territorial area;

(b) persons or classes of persons;

(c) incomes or classes of income; and

(d) cases or classes of cases.

(4) Without prejudice to the provisions of sub-sections (1) and (2), the Board may, by general or special order, and subject to such conditions, restrictions or limitations as may be specified therein,—

(a) authorise any Principal Director General or Director General or Principal Director or Director to perform such functions of any other income-tax authority as may be assigned to him by the Board;

(b) empower the Principal Director General or Director General or Principal Chief Commissioner or Chief Commissioner or Principal Commissioner or Commissioner to issue orders in writing that the powers and functions conferred on, or as the case may be, assigned to, the Assessing Officer by or 471 of 801 under this Act in respect of any specified area or persons or classes of persons or incomes or classes of income or cases or classes of cases, shall be exercised or performed by an Additional Commissioner or an Additional Director or a Joint Commissioner or a Joint Director, and, where any order is made under this clause, references in any other provision of this Act, or in any rule made thereunder to the Assessing Officer shall be deemed to be references to such Additional Commissioner or Additional Director or Joint Commissioner or Joint Director by whom the powers and functions are to be exercised or performed under such order, and any provision of this Act requiring approval or sanction of the Joint Commissioner shall not apply.

(5) The directions and orders referred to in sub-sections (1) and (2) may, wherever considered necessary or appropriate for the proper management of the work, require two or more Assessing Officers (whether or not of the same class) to exercise and perform, concurrently, the powers and functions in respect of any area or persons or classes of persons or incomes or classes of income or cases or classes of cases; and, where such powers and functions are exercised and performed concurrently by the Assessing Officers of different classes, any authority lower in rank amongst them shall exercise the powers and perform the functions as any higher authority amongst them may direct, and, further, references in any other provision of this Act or in any rule made thereunder to the Assessing Officer shall be deemed to be references to such higher authority and any provision of this Act requiring approval or sanction of any such authority shall not apply.

(6) Notwithstanding anything contained in any direction or order issued under this section, or in section 124, the Board may, by notification in the Official Gazette, direct that for the purpose of furnishing of the return of income or the doing of any other act or thing under this Act or any rule made thereunder by any person or class of persons, the income-tax authority exercising and performing the powers and functions in relation to the said person or class of persons shall be such authority as may be specified in the notification.”

“9. After giving thoughtful consideration to the facts and circumstances of the case and to the submissions, it comes up that the admitted case of the Revenue is that there was no specific order under any provisions of the Act other than the order dated 26.10.2020 passed u/s 127 of the Act centralizing the case of M/s Aggarwal Vidya Pracharni Sabha consequent to a search and seizure action u/s 11 ITA No. 1308/Del/2023 132(1) of the Act to vest Ld. PCIT, Gurgaon the powers to pass the impugned order. The ld. DR has relied on the Explanation attached to section 127 of the Act to submit that the word, ‘case’ has been defined for the purpose of section 127 and consequent to the centralization of the assessment, the ld.PCIT, Gurgaon had got powers to commence proceedings u/s 12AB(4) of the Act for cancellation of registration of the assessee.

9.1 In this context, the ld. counsel for the assessee has heavily relied on the CBDT Notification No.52/2014 made available at page 2 to 6 of the paper book submitting that in regard to powers u/ss 11 and 12 of the Act, the CIT (Exemptions), Chandigarh had specific jurisdiction and which could not have been transferred. Relying on the order u/s 127 of 26.10.2020, it was submitted that the order specifically mentions the transfer of case for carrying out post search investigation and meaningful assessment and not for any other purpose like cancellation of the registration.

10. Now to decide the question of valid exercise of jurisdiction by ld.PCIT, Gurgaon, it will be first relevant to reproduce the section 127 of the Act as follows:-

“Power to transfer cases.

127. (1) The Principal Director General or Director General or Principal Chief Commissioner or Chief Commissioner or Principal Commissioner or Commissioner may, after giving the assessee a reasonable opportunity of being heard in the matter, wherever it is possible to do so, and after recording his reasons for doing so, transfer any case from one or more Assessing Officers subordinate to him (whether with or without concurrent jurisdiction) to any other Assessing Officer or Assessing Officers (whether with or without concurrent jurisdiction) also subordinate to him.

(2) Where the Assessing Officer or Assessing Officers from whom the case is to be transferred and the Assessing Officer or Assessing Officers to whom the case is to be transferred are not subordinate to the same Principal Director General or Director General or Principal Chief Commissioner or Chief Commissioner or Principal Commissioner or Commissioner,—

(a) where the Principal Directors General or Directors General or Principal Chief Commissioners or Chief Commissioners or Principal Commissioners or Commissioners to whom such Assessing Officers are subordinate are in agreement, then the Principal Director General or Director General or Principal Chief Commissioner or Chief Commissioner or Principal Commissioner or Commissioner from whose jurisdiction the case is to be transferred may, after giving the assessee a reasonable opportunity of being heard in the matter, wherever it is possible to do so, and after recording his reasons for doing so, pass the order;

(b) where the Principal Directors General or Directors General or Principal Chief Commissioners or Chief Commissioners or Principal Commissioners or Commissioners aforesaid are not in agreement, the order transferring the case may, similarly, be passed by the Board or any such Principal Director General or Director General or Principal Chief Commissioner or Chief Commissioner or Principal Commissioner or Commissioner as the Board may, by notification in the Official Gazette, authorise in this behalf.

(3) Nothing in sub-section (1) or sub-section (2) shall be deemed to require any such opportunity to be given where the transfer is from any Assessing Officer or Assessing Officers (whether with or without concurrent jurisdiction) to any other Assessing Officer or Assessing Officers (whether with or without concurrent jurisdiction) and the offices of all such officers are situated in the same city, locality or place.

(4) The transfer of a case under sub-section (1) or sub-section (2) may be made at any stage of the proceedings, and shall not render necessary the re-issue of any notice already issued by the Assessing Officer or Assessing Officers from whom the case is transferred.

Explanation.—In section 120 and this section, the word “case”, in relation to any person whose name is specified in any order or direction issued there under, means all proceedings under this Act in respect of any year which may be pending on the date of such order or direction or which may have been completed on or before such date, and includes also all proceedings under this Act which may be commenced after the date of such order or direction in respect of any year.

“Section 12AB; “12AB. Procedure for fresh registration.—(1) The Principal Commissioner or Commissioner, on receipt of an application made under clause (ac) of sub-section (1) of section 12A, shall,—

(a) where the application is made under sub-clause (i) of the said clause, pass an order in writing registering the trust or institution for a period of five years;

(b) where the application is made under sub-clause (ii) or sub-clause (iii) or subclause (iv) or sub-clause (v) of the said clause,—

(i) call for such documents or information from the trust or institution or make such inquiries as he thinks necessary in order to satisfy himself about—

(A) the genuineness of activities of the trust or institution; and

(B) the compliance of such requirements of any other law for the time being in force by the trust or institution as are material for the purpose of achieving its objects; and

(ii) after satisfying himself about the objects of the trust or institution and the genuineness of its activities under item (A), and compliance of the requirements under item (B), of sub-clause (i),—

(A) pass an order in writing registering the trust or institution for a period of five years;

(B) if he is not so satisfied, pass an order in writing rejecting such application and also cancelling its registration after affording a reasonable opportunity of being heard;

(c) where the application is made under sub-clause (vi) of the said clause, pass an order in writing provisionally registering the trust or institution for a period of three years from the assessment year from which the registration is sought,

and send a copy of such order to the trust or institution.

(2) All applications, pending before the Principal Commissioner or Commissioner on which no order has been passed under clause (b) of subsection (1) of section 12AA before the date on which this section has come into force, shall be deemed to be an application made under sub-clause (vi) of clause (ac) of sub-section (1) of section 12A on that date.

(3) The order under clause (a), sub-clause (ii) of clause (b) and clause (c), of sub-section (1) shall be passed, in such form and manner as may be prescribed, before expiry of the period of three months, six months and one month, respectively, calculated from the end of the month in which the application was received.

(4) Where registration of a trust or an institution has been granted under clause (a) or clause (b) of sub-section (1) and subsequently, the Principal Commissioner or Commissioner is satisfied that the activities of such trust or institution are not genuine or are not being carried out in accordance with the objects of the trust or institution, as the case may be, he shall pass an order in writing cancelling the registration of such trust or institution after affording a reasonable opportunity of being heard.

(5) Without prejudice to the provisions of sub-section (4), where registration of a trust or an institution has been granted under clause (a) or clause (b) of sub-section (1) and subsequently, it is noticed that—

(a) the activities of the trust or the institution are being carried out in a manner that the provisions of sections 11 and 12 do not apply to exclude either whole or any part of the income of such trust or institution due to operation of sub-section (1) of section 13; or

(b) the trust or institution has not complied with the requirement of any other law, as referred to in item (B) of sub-clause (i) of clause (b) of sub-section (1), and the order, direction or decree, by whatever name called, holding that such noncompliance has occurred, has either not been disputed or has attained finality, then, the Principal Commissioner or the Commissioner may, by an order in writing, after affording a reasonable opportunity of being heard, cancel the registration of such trust or institution.”.

Rule 17A “(5) On receipt of an application in Form No. 10A, the Principal Commissioner or Commissioner, authorised by the Board shall pass an order in writing granting registration under clause (a), or clause (c), of sub-section (1) of section 12AB read with sub-section (3) of the said section in Form No. 10AC and issue a sixteen digit alphanumeric Unique Registration Number (URN) to the applicants making application as per clause (i) of the sub-rule (1).

(6) If, at any point of time, it is noticed that Form No. 10A has not been duly filled in by not providing, fully or partly, or by providing false or incorrect information or documents required to be provided under sub-rule (1) or (2) or by not complying with the requirements of sub-rule (3) or (4), the Principal Commissioner or Commissioner, as referred to in sub-rule (5), after giving an opportunity of being heard, may cancel the registration in Form No. 10AC and Unique Registration Number (URN), issued under sub-rule (5), and such registration or such Unique Registration Number (URN) shall be deemed to have never been granted or issued.

(7) In case of an application made under sub-clause (vi) of clause (ac) of sub-section (1) of 4 [section 12A as it stood immediately before its amendment vide the Finance Act, 2023,] during previous year beginning on 1st day of April, 2021, the provisional registration shall be effective from the assessment year beginning on 1st day of April, 2022.

(8) In case of an application made in Form No. 10AB under clause (ii) of the sub-rule (1), the order of registration or rejection or cancellation of registration under sub-clause (ii) of clause (b) of sub-section (1) of section 12AB shall be in Form No. 10AD and in case if the registration is granted, sixteen digit alphanumeric number Unique Registration Number (URN) shall be issued by the Principal Commissioner or Commissioner referred to in of sub-section (1) of section 12AB.

(9) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall:

(i) lay down the form, data structure, standards and procedure of ,-(a) furnishing and verification of Form No. 10A or 10AB ,as the case may be;

(b) passing the order under clause (a), sub-clause (ii) of clause (b) and clause (c) of subsection (1) of section 12AB.

(ii) be responsible for formulating and implementing appropriate security, archival and retrieval policies in relation to the said application made or order so passed as the case may be.]

” Order u/s 127 (2) of the Income Tax Act, 1961 Consequent to the search & seizure operations u/s 132 of the I.T. Act, 1961 in Dev Wines Group (D.O.S 19.02.2020), the Pr. Commissioner of Income Tax (Central), Gurugram vide letter F.No. Pr.CIT(C)/GGM/Cent./Dev Wines/2020-21/969 dated 24.08.2020 has been given concurrence and requested for centralization of the following cases related M/s Dev Wines Group to DCIT, Central Circle2, Faridabad for coordinated post search investigation & meaningful assessment.

Accordingly, in exercise of power conferred by sub-section (2) of Section 127 of the Income Tax Act, 1961 and under all other powers enabling me in this behalf, I, the Commissioner of Income Tax(Exemptions), Chandigarh hereby transfer the following case(s), particulars of which are mentioned hereunder in Columns (2) and (3) from the Assessing Officer mentioned in Column (4) therein, to the of the Assessing Officer mentioned in Column (5) –

| .Sl. No. | Name and Address of the Assessee | PA N | From | To |

| 1 | (2) | (3) | (4) | (5) |

| M/s Aggarwal vidhya Pracharni Sabha (Aggarwal College, Ballabhgarh) | AABTA34 09 | Circle-2 (E), Chandigarh | DCIT, Central Circle-2, Faridabad DLC-CC-136-4 |

This order shall take effect from 26.10.2020.”

[Notification No. 52 /2014/F. No. 187 /38 /2014 (ITA.I)] DEEPSHIKHA SHARMA, Director”

Sub: Clarification regarding Form No 10AC issued till the date of this Circular – reg.

Finance Act, 2022 has inserted sub-section (4) in section 12AB of the Income tax Act, 1961 (the Act) allowing the Principal Commissioner or Commissioner of Income-tax to examine if there is any “specified violation” by the trust or institution registered or provisionally registered under the relevant clauses of sub-section (1) of section 12AB or subsection (1) of section 12AA. Subsequent to examination by the Principal Commissioner or Commissioner of Incometax, an order is required to be passed for either cancellation of the registration or refusal to cancel the registration. Similar provisions have also been introduced in clause (23C) of section 10 of the Act by substituting the 21 ITA No. 1308/Del/2023 fifteenth proviso of the said clause with respect to fund or institution trust or institution or any university or other educational institution or any hospital or other medical institution referred under sub-clauses (iv), (v), (vi), (via) of this clause and which have been approved or provisionally approved under the second proviso to the said clause. These amendments are effective from 1st April, 2022. In addition to the specified violations referred above, the power of cancellation has also been granted under sub-rule (5) of rule 17A and subrule (5) of rule 2C of the Income-tax Rules, 1962 (the Rules) to the Principal Commissioner or Commissioner authorised by the Board. This Circular only relates to cancellation of registration/approval or provisional registration/approval in the case of “specified violation”.

“Sub: Proposal for cancellation of registration granted u/s 12AA/12AB of the Act as per provisions of Section 12AB(4) of the Act in the case of ‘Aggarwal Vidya Pracharni Sabha ‘ ” – Reg.

“4.10 In the light of above facts of the case, it appears that the assessee trust has made specified violation in terms of explanation to Section 12AB(4) of the Income Tax Act, 1961. As such, following information from the assessee trust was called for under Section 12AB of the Act vide this office letter dated 08.09.2022 to examine the activities of the Aggarwal Vidya Pracharni Sabha with a view to ascertain whether the same are covered under the clause of explanation to the provisions of Section 12AB(4) of the Act and other provisions of the Act. Details of information called for the relevant period i.e. AY 2014-15 to 2020-21 is as under:

“d) Further, vide this office letter dated 08.09.2022, the assessee was requested to furnish details of capital and revenue expenditure incurred for various assessment years. In response, the assessee only submitted copy of Form 10B which is not supported with the details of capital expenditure and copy of accounts and documentary evidence. Further, no activity was specified for which accumulated funds were utilized.”

“(a) where any income derived from property held under trust, wholly or in part for charitable or religious purposes, has been applied, other than for the objects of the trust or institution;”

“14. We found that the above facts and proceedings of power of transfer U/s 127 was only for a limited purpose of Co-Ordinate Assessment. Neither any search & Seizure action nor any notice u/s 153A or 153C of the Act or assessment u/s 153A or 153C of the Act in the case of assessee were initiated and there was only a survey u/s 133A of the Act in the case of assessee. The assessment has been completed u/s 148/143(3) of the act vide order dated 19.12.2018. As the assessment has been completed, the purpose of transfer u/s 127A has also been completed. Although No notices regarding the transfer of the cases u/s 127 have been sent to the assessee for the purpose of Co-ordinate assessment and the purpose of transfer was only Co-Ordinate Assessment as clearly mentioned in the transfer letter 19.08.2016. The assessment was completed u/s 148 r.w.s 143(3) 19.12.2018 and the proposal was sent to the Pr. CIT(C) which has been received on 31.12.2018 in the office of Pr. CIT(C) on 23.01.2019 after a lapse of more than one month.

15. Even otherwise, in the said notification, there is no mention where CIT(E) can transfer to other CIT or Pr.CIT. The said notification of CBDT has authorized the CIT(E) to issue order in writing for the exercise of the powers and functions by the Addl.CIT or JCT or TRO who are “subordinate” to them and has authorised the Addl.CIT to issue order in writing for the exercise of the powers by the Assessing Officer who are the subordinate to them. In section 124 of the Act, the jurisdiction of Assessing Officer has been given and not ‘Jurisdiction of Commissioner’.”

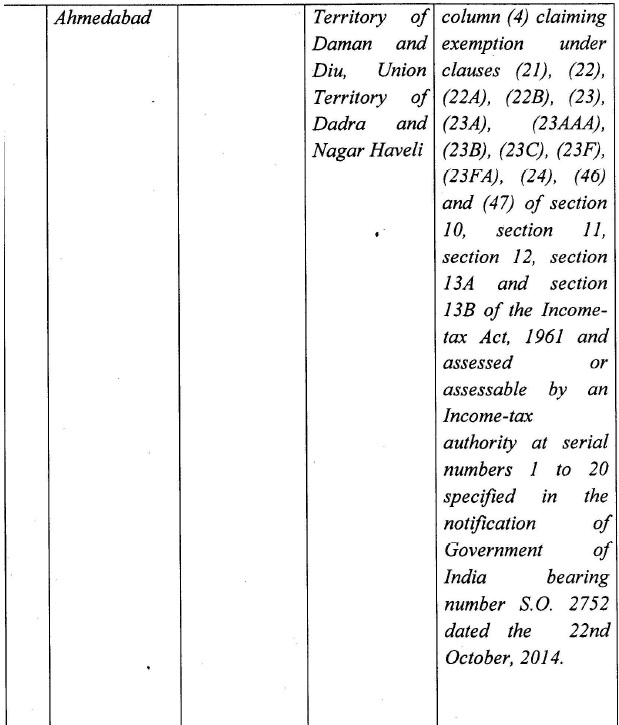

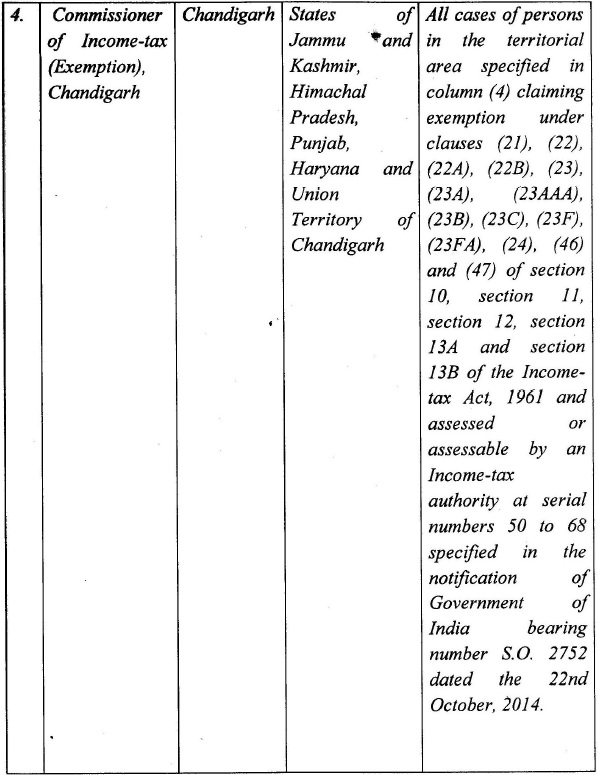

“18. We also observe that as per Sec. 120(6) of the Act, the CBDT by its Notification No. 52/2014 and 53/2014 dated 22.10.2014 has given power to CIT(Exemption) Jaipur for the State of Rajasthan for all cases of persons in the territorial area specified in column (4) claiming exemption under clauses (21), (22), (22A), (22B), (23), (23A), (23AAA), (23B), (23C), (23F), (23FA), (24), (46) and (47) of section 10, section 11, section 12, section 13A and section 13B of the Act and assessed or assessable by an Income-tax authority at serial numbers 131 to 140 specified in the notification of Government of India bearing number S.O.2752 dated the 22nd October, 2014. Thus firstly as per above notification and provisions of Sec. 120 and 127 the ld. CIT(Exmp.) cannot transfer or hand over or given his work or power or duties to the other same rank of CIT at all to cancel the Registration u/s 12AA. However, in case, if it is necessary to do so then there has to be proper proceedings in writing. As there has to be some order in writing from higher authorities i.e. from Chief Commissioner of Income Tax (Exmp.) Delhi or CBDT in writing and an opportunity of being heard is to be given to the assessee before transferring the case whereas all these are absent in the present case and nothing has been demonstrated by the department.

19. We further observe that Sec. 127 of the Act empower to transfer cases among Assessing Officers but not to Commissioners of Income Tax as CIT is not an Assessing Officer. In our view, to pass an order u/s 12A for registration or cancellation is not within the jurisdiction or power of an Assessing Officer. Hence registration u/s. 12A can be withdrawn only by the ‘Prescribed Authority’ who has been empowered to grant the same and by the Notification dated 22.10.2014 the ld.CIT(Exmp.) has empowered for the same, hence the Pr.CIT (Central) cannot cancelled the same.

20. In assessee’s case, the case u/s 127 was transferred to the Central Circle for limited purpose of Co-Ordinate assessment admittedly which do not mean that the Section 12A proceeding has been transferred to the Pr.CIT(Central) Automatically, when both the proceedings are separately or independent and also has to be done or conducted by the different rank Authorities. More particularly when for the purpose of Exemption cases or 12A registration a Separate Commissioner of Income Tax has been Authorized for whole of Rajasthan by the CBDT by its Notification dated 22.10.2014. In support of the above contention, the ld AR has relied on the decision in the case of Dilip Tanaji Kashid v. M.I. Karmakar PR. CIT& ANR. (2018) 304 CTR 0436 (Bom) wherein It has been held:

“Transfer of jurisdiction–Power of competent officers–Centralization of case–Dissenting note–Assessee was issued notice enshrining proposal for transfer of his case from Kolhapur to Mumbai, so as to centralise cases relating to D.Y. Patil Group–Assessee objected that such notice did not referred to any agreement being reached by officers of equal rank at Mumbai and Kolhapur–These objections were however overruled and assessee’s case was transferred–High Court quashed purported transfer u/s 127–Held, “Centralisation Committee” which took decision for transfer of jurisdiction, is not authority envisaged u/s 127(2)– Counter-affidavit filed on behalf of Revenue does not disclose that there was any agreement between authorities of equal rank,as a pre-condition for invoking powers u/s 127– “Absence of dissenting note” from officer of equal rank who has to agree to proposed transfer would not constitute agreement, envisaged u/s 123(2)(a)–Assessee’s petition allowed.”

21. It was also been brought to our notice that the AR had inspected the records of the case but there was no agreement between both the CIT’s regarding initiation of proceedings U/s 12A of the Act. The entire communication on record is with regard to limited purpose of CoOrdinate assessments only. Even the Instruction No. F.No.286/88/2008IT(Inv-II) dated 17.09.2008 has relied upon by the Revenue also relates to “search assessment” and was not with regard to proceedings U/s 12A or other proceedings. Even no agreement for initiation proceedings U/s 12AA of the Act has been found out on record. Even, the proposal for centralization was not sent within the statutory time of 30 days from the date of search as admittedly the search was conducted on 30.06.2016 and the proposal was sent on 19.08.2016 i.e. after 30 days of the search. In this respect, the ld AR has relied upon the decision in the case of Rentworks India (P) Ltd. v. Pr.CIT & ANR. (2017) 100 CCH 0258 Mum HC wherein it has been held that:

” Income tax authorities–Power to transfer cases–Jurisdiction– CIT, issued notice to assessee taking recourse to subsection 2 of Section 127–Assessee was put to notice that there was proposal to transfer case of assessee to DCIT, for proper co-ordinated investigation–Impugned order was made by Principal CIT under subsection 2 of section 127 by which case of assessee was transferred to DCIT–Held, in Noorul Islam Educational Trust it was held that as Income-tax/assessment file of assessee had been transferred from one AO in Tamil Nadu to another AO in Kerala and two AO were not subordinate to same Director General or Chief Commissioner or Commissioner of Income Tax u/s 127(2) (a) agreement between Director General, Chief Commissioner or Commissioner, as case might be, of two jurisdictions was necessary– Counter affidavit filed on behalf of Revenue did not disclose that there was any such agreement–In fact, it had been consistently and repeatedly stated in said counter affidavit that there was no disagreement between two Commissioners– Existence of agreement between two jurisdictional Commissioners was condition precedent for passing order of transfer-Clause (b) of sub-section (2) of section 127 provides for consequences when there was no such agreement–When jurisdiction to pass order of transfer under clause (a) of subsection (2) of Section 127 could be exercised only when there was such agreement, fact that such agreement exists ought to had been stated in show cause notice as same was jurisdictional fact- -It was on basis of written document that finding was recorded that there was agreement between Jurisdictional Commissioners 35 ITA No. 1308/Del/2023 of Ranchi and Delhi–Even going by case made out by revenue, no such agreement was spelt out.

8. The Apex Court has categorically held that the absence of disagreement will not be tantamount to an agreement as visualized under section 127(2)(a) which contemplates positive state of mind of the two jurisdictional Principal Commissioners of Income Tax. The agreement contemplated by clause (a) of subsection (2) of section 12 7 may not be a drawn up agreement. What is necessary is that there has to be an agreement which will involve positive state of mind of the two jurisdictional Principal Commissioners. Both of them must consent to the transfer after application of mind.

9. In the present case, it is not even the case made out in the show cause notice that the agreement as contemplated by the first part of clause (a) of sub-section (2) of section 127 exists. The existence of such agreement between two jurisdictional Commissioners is a condition precedent for passing the order of transfer.Except for the request which came from the investigation office, Chennai of transferring the case, 38 ITA 688/JP/2019_ M/s Wholesale Cloth Merchant Association v. Pr.CIT there is no reference whatsoever to any such agreement. Clause (b) of subsection (2) of section 127 provides for consequences when there is no such agreement. When the jurisdiction to pass an order of transfer under clause (a) of sub-section (2) of Section 127 can be exercised only when there is such an agreement, the fact that such an agreement exists ought to have been stated in the show cause notice as the same is a jurisdictional fact. Apart from the failure to mention the same in the show cause notice, the only stand of the revenue is that there is an agreement by implication. This stand is completely contrary to paragraph 5 of the decision of the Apex Court in the case of Noorul Islam Educational Trust (supra). The decision in the case of Ramswaroop (supra) will also bind this Court for the reasons stated above.

10. Coming to the decision in the case of Jharkhand Mukti Morcha, relevant facts are in paragraph 12. In the said case, specific reliance was placed on a document dated 2 7th November 2016. It is on the basis of the written document that a 36 ITA No. 1308/Del/2023 finding was recorded that there was an agreement between the Jurisdictional Commissioners of Ranchi and Delhi. In the present case, even going by the case made out by the respondent, no such agreement is spelt out. In absence of any such agreement, the first respondent had no jurisdiction to pass the order of transfer.

11. As the impugned order cannot be sustained on above ground, it is not necessary to into other challenges.

12. Accordingly, for the reasons quoted above, we pass following order:

Impugned order dated 25th May 2 017 (Exhibit-H to the petition) is hereby quashed and set aside. Rule is made absolute on above terms with no order as to costs.

“The CBDT sent a notice to the appellants under s. 127 proposing to transfer their case files “for facility of investigation” from the respective ITO at Nellore to the ITO, B Ward, Special Circle II, Hyderabad. By this notice they were also asked to submit in writing if they had any objection to the proposed transfer within 15 days of receipt of the notice. The appellants made their representation objecting to the transfer and on 26th July, 1973, the Central Board passed the impugned order transferring the cases from Nellore to Hyderabad. The short question that arises for consideration is whether failure to record the reasons in the order which was communicated to the appellants is violative of the principles of natural justice for which the order should be held to be invalid.

Held :

The requirement of recording reasons under s. 127(1) is a mandatory direction under the law and non-communication thereof is not saved by showing that the reasons exist in the file although not communicated to the assessee. When law requires reasons to be recorded in a particular order affecting prejudicially the interests of any person, who can challenge the order in Court, it ceases to be a mere administrative order and the vice of violation of the principles of natural justice on account of omission to communicate the reasons is not expiated. Non- communication of the reasons in the order passed under s. 127(1) is a serious infirmity in the order for which the same is invalid.–Kashiram Aggarwalla v. Union of India (1965) 56 ITR 14 (SC) : TC69R.660 and S. Narayanappa v. CIT (1972) 86 ITR 741 (All) : TC51R.651 distinguished; Sunanda Rani Jain v. Union of India 1975 CTR (Del) 135 : (1975) 99 ITR 391 (Del) : TC69R.693 overruled; Judgment and order dt. 12th Sept., 1974, of the Andhra Pradesh High Court in Writ Appeal No. 626 of 1974 set aside.

Special Leave Petition–Transfer of case–Validity–High Court of Madras, Madurai Bench, upheld order of C.I.T.1, Madurai, Tamil Nadu, transferring file of assessee from Tamil Nadu to Kerala–Held, as Income-tax/assessment file of assessee has been transferred from one Assessing Officer in Tamil Nadu to another Assessing Officer in Kerala and two Assessing Officers are not subordinate to same Director General or Chief Commissioner or Commissioner of Income Tax, u/s 127(2) (a) an agreement between Director General, Chief Commissioner or Commissioner, as the case may be, of two jurisdictions is necessary– Absence of disagreement cannot tantamount to agreement as visualized under Section 127(2) (a) which contemplates a positive state of mind of two jurisdictional Commissioners of Income Tax which is conspicuously absent– Transfer of Income-tax/assessment file of assessee from Assessing Officer, Tamil Nadu to Assessing Officer, Kerala is not justified–High Court order set aside–Special appeal allowed. Although, the ld DR has relied upon the decision of Hon’ble Rajasthan High Court in the case of Lalit Hans v. PCIT DP Special Appeal (Writ) 249/2015 but the facts of the above case are entirely different. Hence, the said judgment is of no help to the Revenue on the facts of the present case. Thus, keeping in view our above discussions, we are of the view that the ld. PCIT had no jurisdiction to pass order U/s 12AA(3) & 12AA(4) of the Act and the same is not sustainable in the eyes of law and accordingly stands quashed.”

21. In the light of the aforesaid discussion and the law cited before us, we are of the considered view that the impugned order has been passed by Ld. PCIT, Gurgaon, without jurisdiction in context to territorial powers and subject matter as well not in accordance with law and same is liable to be quashed. Accordingly, the additional ground raised by the assessee is allowed. Since the relief is granted to assessee by allowing additional ground itself, the adjudication of other grounds raised by the assessee become academic in nature and are left open. Resultantly, the appeal of the assessee is allowed and the impugned order is quashed.

Order pronounced in the open court on 08.01.2024.”

“16. Then, the next question that comes up for our consideration is that whether or not Ld. POT was justified in cancelling the registration of trust with retrospective effect from financial year 200708. Without delving into the issue whether the Commissioner had been empowered to cancel registration with retrospective effect, it is suffice to hold that in the present case, Hon’ble Bombay High Court in Writ Petition filed by the appellant challenging the show cause notice for cancellation of registration held that the contents of order dated 910-2007 passed by the Commissioner cancelling registration shall be treated as show cause notice to the appellant as extracted supra and this finding had not been reversed till date. In the interest of judicial discipline, the ld. PCIT is bound to obey the Directions of Hon’ble High Court and rightly cancelled the registration w.e.f. financial year 2007-08.”