The Jurisdictional Validity Of Faceless Reassessment Prior To Statutory Notification (AY 2017-18)

This ruling addresses a fundamental jurisdictional conflict that arose during the transition of the Indian Tax Department to a fully digital, faceless ecosystem. It clarifies when the National Faceless Assessment Centre (NFAC) officially gained the legal power to conduct reassessments under Section 147.

The Legal Issue

Can a reassessment order passed by the National Faceless Assessment Centre (NFAC) under Section 144B be considered legally valid if it was issued before the Central Government officially notified the specific scheme for faceless reassessments under Section 151A?

Facts of the Case

-

Original Assessment: The assessee, a partnership firm, originally filed a return declaring a business loss, which was initially accepted.

-

The Reopening Trigger: Based on information that ₹15 lakhs from cash deposits made by a third party during the 2016 Demonetization period were transferred to the assessee, the case was reopened under Section 147.

-

The Faceless Order (30-03-2022): The NFAC (Faceless Regime) passed the final reassessment order, making an addition to the income as “unexplained.”

-

The Legal Mismatch: Section 151A, which provides the specific legal framework for “Faceless assessment of income escaping assessment,” was formally notified by the Government on March 29, 2022, through the e-Assessment of Income Escaping Assessment Scheme, 2022.

The Decision

The Court ruled in favour of the assessee, setting aside the reassessment order:

-

Absence of Operating Jurisdiction: The Court held that for any authority to exercise power, that power must be granted by the statute. While Section 144B governed faceless regular assessments, it did not automatically cover reassessments under Section 147 until the notification of Section 151A.

-

Effective Date of the Scheme: The specific power to conduct faceless reassessments (including issuance of notices under Section 148) only came into existence and became operational on March 29, 2022.

-

Invalid Proceedings: Since the reassessment proceedings were initiated and the final order was passed through the faceless regime prior to (or at the very cusp of) the legal authorization of that regime for reassessment purposes, the entire process was deemed “without jurisdiction.”

-

Outcome: Even if the underlying facts of the ₹15 lakhs transfer were valid, the procedural illegality of using an unauthorized forum (NFAC for reassessment before the scheme was active) made the order void.

Key Takeaways for Taxpayers

-

Jurisdictional Error is Fatal: In tax law, an order passed by an authority without the legal right to do so on that date is a “nullity.” This applies even if the tax addition itself is factually correct.

-

Timeline Analysis: If you received a reassessment order passed by the NFAC/Assessment Unit between 2021 and early 2022, check the specific dates. If the process was conducted facelessly before the March 29, 2022 notification, the order may be challenged on jurisdictional grounds.

-

Faceless vs. Jurisdictional AO: This ruling reinforces that the transition to “faceless” required specific statutory enabling at each level (Assessment, Penalty, Appeal, and Reassessment).

and S. Rifaur Rahman, Accountant Member

[Assessment year 2017-18]

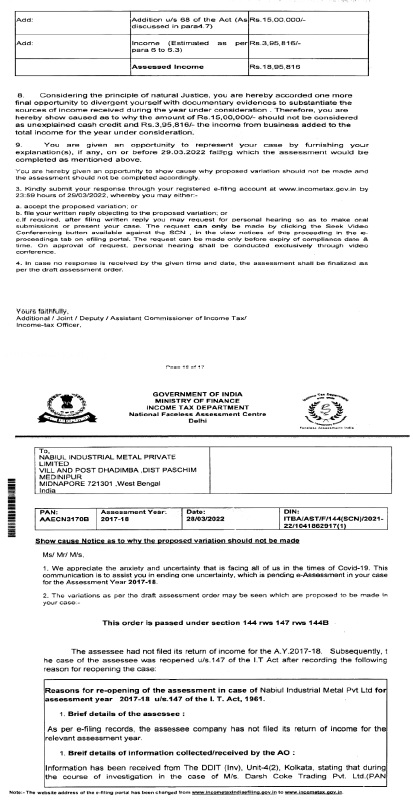

“1.1. The brief facts of the case of the appellant are that the assessee Nabiul Industrial Metal Pvt. Ltd. did not file the return of income for the AY 2017-18 as a result of which case of the assessee was re-opened u/s 147 of the Act. The Assessing Officer (hereinafter referred to as ld. ‘AO’) received information from the investigation wing, Kolkata wherein it was mentioned that in course of the investigation in the case of M/s. Darsh Coke Trading Pvt. Ltd., it was revealed that the said company is a paper company through which entry operators provide bogus entries and layer money in exchange of commission. It was also found that the one of the beneficiaries is the assessee company which has received Rs. 15,00,000/- from a paper concern namely Tanishi Commotrades Pvt. Ltd. During the course of reassessment, the assessee was asked to explain the transactions with Tanishi Commotrades Pvt. Ltd. In response, the assessee submitted that in the current year i.e. FY 2016-17 the assessee took a loan/ advance from this party against sale of goods and in the immediately succeeding year i.e. FY 2017-18 sales were made to Tanishi Commotrades Pvt. Ltd and said sale was duly credited in the Profit and Loss account of the company and tax was duly paid. However, the AO was not convinced with the submission filed by the assessee and accordingly, added the sum of Rs. 15,00,000/- to the income of the assessee u/s 68 of the Act. The said assessment order has been challenged before the ld. CIT(A) wherein in absence of any response from the appellant the case of the assessee has been dismissed.

Being aggrieved and dissatisfied with the impugned order, the present appeal has been preferred.

1.2. The ld. Counsel for the assessee challenges the impugned order by taking several grounds but he, in course of hearing, took an additional ground being the legal ground and he pressed only legal ground which are as follows:

“That the National Faceless Assessment Centre erred in having assumed jurisdiction u/s 151A r.w.s 144B of the Act from 29.11.2021 when they were not empowered under any notification about the applicability of the faceless scheme for making assessment in faceless manner prior to 29.03.2022.”

1.3. Ld. Counsel for the assessee submitted that the provisions of Section 151A of the Act came in the statute on 01.11.2021 but it was notified with effect from 29.03.2022. But in the present case, assessment proceedings to the NFAC started on 29.11.2021 which is evident from the notice u/s 142(1) of the Act. Ld. Counsel for the assessee further submits that the show cause notice has also been issued and the date has been mentioned as 28.03.2022 that is prior to 29.03.2022. Ld. Counsel for the assessee further submits that the assumption of jurisdiction by the NFAC was without jurisdiction. Consequently, the whole assessment is without jurisdiction and unsustainable in law. Ld. Counsel for the assessee further drew the attention of this Bench on the issuance of show cause notice and submitted that it was served on 29.03.2022 and asked the assessee to furnish explanation on or before 29.03.2022,it means without giving the assessee any opportunity before framing of the assessment order. Ld. Counsel for the assessee has filed the following papers:

(a) Notification of Ministry of Finance dated 29.03.2022.

(b) Notice issued u/s 142(1) of the Act.

(c) Show cause notice dated 28.03.2022.

1.4. Ld. D/R though supports the impugned order but did not raise any objection on the legal ground.

2. We have perused the records and the papers filed by the assessee. It appears that Notification with respect to Section 151A of the Act has been made with effect from 29.03.2022 which is as under:

“S.O. 1466(E).—In exercise of the powers conferred by subsections (1) and (2) of section 151A of the Income-tax Act, 1961 (43 of 1961), the Central Government hereby makes the following Scheme, namely:-

1. Short title and commencement.—(1) This Scheme may be called the e-Assessment of Income Escaping Assessment Scheme, 2022.

(2) It shall come into force with effect from the date of its publication in the Official Gazette.

2 .Definitions.—(1) In this Scheme, unless the context otherwise requires, —

(a)”Act” means the Income-tax Act, 1961 (43 of 1961);

(b) “automated allocation” means an algorithm for randomised allocation of cases, by using suitable technological tools, including artificial intelligence and machine learning, with a view to optimise the use of resources.

(2)Words and expressions used herein and not defined, but defined in the Act, shall have the meaning respectively assigned to them in the Act.

3. Scope of the Scheme.—For the purpose of this Scheme,—

(a) assessment, reassessment or re-computation under section 147 of the Act,

(b)issuance of notice under section 148 of the Act, shall be through automated allocation, in accordance with risk management strategy formulated by the Board as referred to in section 148 of the Act for issuance of notice, and in a faceless manner, to the extent provided insection 144B of the Act with reference to making assessment or reassessment of total income or loss of assessee.”

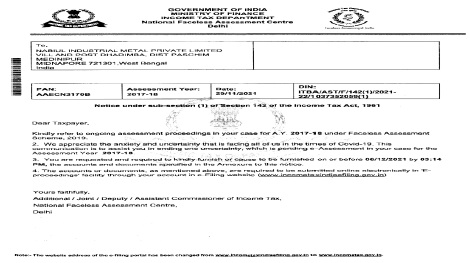

2.1. We have also gone through the notice u/s 142(1) of the Act dated 29.11.2021 which is as follows:

2.2. We further find the show cause notice issued that also reflects the date 28.03.2022 which is as follows:

………………………………………………….

2.3. It appears from the show cause notice issued on 28.03.2022 that at the bottom of the page it was digitally signed thereby giving date 29.03.2022 at 00:20:37 IST.

2.4. We further find that in the show cause notice the assessee has been directed to furnish explanation on or before 29.03.2022. It is surprising that when it was issued on 29.03.2022 at 00:20:37 IST and directed the assessee to explain the explanation before 29.03.2022.

3. Keeping in view the entire facts and discussions made above, we find substance in the argument of the ld. CIT(A) that assumption of jurisdiction prior to 29.03.2022 by the ld. AO is to be held to be without jurisdiction. Accordingly, the assessment order, passed, is to be deemed without jurisdiction. Subsequently, all the orders passed are hereby held to be without jurisdiction.”