ORDER

Narender Kumar Choudhry, Judicial Member. – This appeal has been preferred by the Assessee against the order dated 31.01.2025, impugned herein, passed by the Ld. Commissioner of Income Tax (Appeals) (in short Ld. Commissioner) u/s 250 of the Income Tax Act, 1961 (in short ‘the Act’) for the A.Y. 2020-21.

2. In this case, the Assessee being an individual and having earned income from business or profession and interest income during the assessment year under consideration, has declared her total income at Rs.10,84,45,500/- by filing return of income dated 04.02.2021, which was selected for complete scrutiny on the following reasons:

“1. Brought forward TDS credit claimed is substantially less than TDS credit forward in the return of preceding assessment year”

“2. Large payments made u/s 194C to persons who have not filed return of income”

3. Thus, the Assessing Officer (herein after “AO”) in order to examine the aforesaid issues, asked the Assessee to submit various details, as per reasons of selection.

4. The Assessee in response filed copy of return of income along with computation, profit and loss account and balance sheet for the year under consideration and detailed note about her activities.

5. The AO on perusing the capital account of the Assessee found that the Assessee has received gift amounting to Rs. 12,54,54,594/- during the year under consideration and therefore he asked the Assessee to furnish the information, such as name / address of the Donor, PAN, amount, mode of payment, relationship with Donor and evidence with relation thereto.

6. The Assessee in response to the said query/ information sought for by the AO, filed her part reply dated 09.03.2022, inter-alia claiming as under:

“With regard to the para – 7 of your letter dated 02.03.2022, a gift has been received from my husband Shri Ripusudan Kundra for the year ended 31st March, 2020 relevant to the A.Y 2020-21″

7. Thereafter, the AO again issued show cause notices dated 30.08.2022 & 08.09.2022, in response to which, the Assessee filed her reply on 15.09.2022, which read as under:

“The husband of the Assessee Shri Ripu Sudan Kundra having PAN AZUPK9777F has gifted to her wife during the year ended on 31st March, 2020 relevant to the assessment year 2020-21 out of natural love and affection and to hold the same absolutely forever. The copy of the duly signed ‘Gift Deed’ between husband and wife dated 05.03.2020 having full name, PAN, relation, address, full Particulars, amount and signature of witness is enclosed herewith for your honor’s kind perusal alongwith the acknowledgement of income tax return in form ITR V filed on 29.01.2021 vide e-filing acknowledgement number 231839011290121 of husband, Shri Ripu Sudan Kundra, as asked by your goodself. Being the gift received from spouse, the genuineness of the above said gift is beyond doubt.”

8. The AO though considered such reply of the Assessee, however found the same, as not acceptable, mainly on the reason that in spite of repeated opportunities, the Assessee has provided only scanned copy of “gift deed” but no evidence qua mode of payment/ receipt i.e. no bank statement of Shri. Ripu Sudan Kundra and Ms. Shilpa Shetty Kundra, has been submitted, showing the transfer of funds, regarding gift amounting to Rs. 12,54,54,954/-.

9. The AO also observed that PAN of Shri Ripu Sudan Kundra has been provided only, vide reply dated 15.09.2022 i.e. at the fag end, as the case is getting barred on 30.09.2022 so that no further, enquires can be made u/s 133(6) of the Act. Further, return of income of Shri Ripu Sudan Kundra for A.Y 2020-21 is Rs. 27,71,020/-, which does not commensurate with the amount Rs. 12,54,54,954/- as gift given. So, the creditworthiness of Donor could not be established, as even after repeated opportunities, Assessee has not submitted any document to prove creditworthiness of Donor. Since, the case is getting time barred on 30.09.2022, and therefore he does not have time to keep on giving opportunities endlessly. In the absence of bank statement of Shri Ripu Sudan Kundra, the source of funds paid as gift, remained unexplained in this case. As the source of funds received as gift, has not been explained with complete documentary evidence, the genuineness and creditworthiness of the same has not been established, as required u/s 68 of the Act.

10. Thus, the AO on the aforesaid peculiar facts and circumstances and various judgments, as cited in the assessment order which we will deal with in the latter part of this order, ultimately added the amount of Rs. 12,54,54,594/- to the income of the Assessee, as unexplained credit u/s 68 of the Act, chargeable to tax, as per the provisions of Sec. 115BBE of the Act.

11. The Assessee being aggrieved challenged the said addition by filing first appeal before Ld. Commissioner raising various grounds, as mentioned by the Ld. Commissioner in para -3 of the impugned order and also filed her written submissions, which read as under:

“5. During the appellate proceedings, the appellant has submitted a written which is reproduced as under:

FACTS OF THE CASE:

“1. The appellant is an individual and regularly assessed to tax vide PAN ACPPS6622P.

2. For the assessment year under consideration, the appellant filed her return of income on 04.02.2021 vide efiling acknowledgement number 240116101040221 declaring total income of Rs. 10,84,45,500/-.

3. The case of the appellant was selected for compulsory scrutiny and notice u/s 143(2) and 142(1) of the Act was issued to the appellant. The appellant filed her reply from time to time.

2. It is submitted that the Assessing Officer failed to consider the documents and submissions made by the Appellant and passed the impugned assessment order dated 21.09.2022, u/s 143(3) r.w.s. 1448 of the Act, assessing total income at Rs 23,39,00,094/- on account of alleged addition of Rs 12,54,54,594/- on account of unexplained credit u/s 68 of the Act.

3. Being aggrieved with the impugned assessment order and the additions made without giving adequate opportunity of being heard and in gross violation of principles of natural justice, the appellant has preferred the present appeal before your honour. With the above factual back ground of the case, written submissions are being made for your honour’s kind and careful consideration.

SUBMISSIONS OF APPELLANT:

4. The ground of appeal no. 1, 2, 3 and 4 are as below:

Ground Number 1: On the facts and the circumstances of the appellant’s case and in law the Assessing Officer erred in passing order u/s 143(3) r.w.s 144B by making an addition of Rs. 12,54,54,594/- on account of gift from spouse alleged as unexplained credit u/s 68 of the Act.

Ground Number 2: On the facts and the circumstances of the appellant’s case and in law the Assessing Officer erred in treating gift as unexplained credit which has been received from her husband arising purely out of natural love and affection.

Ground Number 3: On the facts and the circumstances of the appellant’s case and in law the Assessing Officer erred in making an addition of Rs. 12,54,54,594/- u/s 68 of the Act disregarding the fact that gift has been received from her spouse u/s 56 r.w.s. 2(41) of the Act whose genuinity is beyond any doubt.

Ground Number 4: On the facts and the circumstances of the appellant’s case and in law the Assessing Officer before making an alleged addition of gift received from her spouse without issuing notices u/s 133(6) to her husband and without provide an opportunity of being heard to check the veracity of the allegations raised in the impugned order.

5. During the assessment proceedings the Assessing Officer vide show cause notice dated 21.03.2022 called upon the appellant to furnish information regarding gift received amounting to Rs 12,54,54,594/-.

6. In reply to the said notice the appellant vide letter dated 24.03.2022 and 15.09.2022 submitted the relevant documents to prove the genuineness of the said transaction. The relevant portion of letter dated 15.09.2022 is reproduced for your honour’s ready reference:

“2. The husband of the assessee Shri Ripu Sudan Kundra having PAN: AZUPK9777F has gifted to her wife during the year ended on 31st March, 2020 relevant to the assessment year 2020-21 out of natural love and affection and to hold the same absolutely forever. The copy of the duly signed ‘Gift Deed’ between husband and wife dated 05.03.2020 having full name, PAN, relation, address, full particulars, amount and signature of witnesses is enclosed herewith for your honour’s kind perusal alongwith the acknowledgement of income tax return in form ITR V filed on 29.01.2021 vide efiling acknowledgement number 231839011290121 of husband, Shri Ripu Sudan Kundra as asked by your goodself. Being the gift received from spouse, the genuineness of the abovesaid gift is beyond doubt.”

7. It is submitted that to prove the identity, genuineness and creditworthiness of the transaction executed between the party, the appellant during the assessment proceedings submitted the following documents: (enclosed at page number 64-69 of the paper book)

i. Copy of duly signed gift deed dated 05.03.2020 along with signature of two witnesses.

ii. Full name of Doner and Donee.

iii. Details of PAN of Doner and Donee.

iv. Relationship between the Donor and Donee.

v. Full address of Doner and Donee.

vi. Acknowledgement of Income Tax Return of Doner for AY 2020-21.

8. In view of the aforesaid evidences filed during the course of reassessment proceedings, the appellant has fully discharged the burden u/s 68 of the Act and the burden has shifted on to the department and the Assessing Officer has not conducted any enquiries thereafter by confronting these evidences with the Donor or otherwise to shift the burden back on to the appellant. The appellant has received the said gift from her husband out of natural love and affection, therefore the genuineness of the abovesaid gift is beyond doubt.

9. It is pertinent to note that the Assessing Officer has failed to adopt the due process of law by issuing summons under section 131 of the Act for carrying out detailed investigation from the Donor, when the Assessing Officer was already having information regarding PAN details, complete residential address and Income Tax Return of the Donor. In absence of such enquiry conducted by the Assessing Officer, the impugned order passed u/s 143(3) is bad in law and shall be deleted.

10. In order to prove the above contentions, the appellant places reliance on the following judgements:

a. Decision of Hon’ble ITAT, Patna Bench in the matter of Sandeep Bansal v. Assistant Commissioner of Income-tax, Central Circle-2, Patna, (Patna – Trib.). The facts of the case are that pursuant to search and survey conducted upon premises of assessee, gift deeds and affidavits were found. Assessing Officer made additions under section 68. It was noticed that though assessee was in receipt of gifts from various parties, but he had not discharged his onus completely by producing Donors before Assessing Officer or any other documentary evidence to prove creditworthiness of Donors and proving genuinity of gifts. At same time, revenue had not adopted due process of law by issuing summons under section 131 for carrying out detailed investigation from Donors, more particularly when Assessing Officer was already having information regarding PAN of Donors, bank accounts of Donors and other related details. The Hon’ble ITAT held that, on facts, additions under section 68 could not be made and issue of verification of gifts was to be remanded to file of Assessing Officer to decide same afresh.

b. Decision of Hon’ble Gujarat High Court in the matter of Commissioner of Income-tax VI v. Heena Sharma, (Gujarat). The Hon’ble High Court held that where assessee in support of gifts received from Donors submitted requisite documents such as copies of demand drafts, gift deed, PAN cards and acknowledgement of returns of Donors, no addition could be made in respect of gift amount by taking recourse to provisions of section 68.

c. It is submitted that Hon’ble Apex court in the case of CIT v. Divine Leasing & Finance Ltd. has held that if the relevant details of the address or PAN/identity of the creditor are furnished to the Department it would constitute acceptable proof or acceptable explanation by the assessee. In this case, the creditors existence is recognized as the company is in the records of the IT Department, since the appellant has submitted their PAN and also copies of IT. Return.

d. The Hon’ble Supreme Court in the case of CIT Orissa v. Orissa Corp. Pvt. Ltd. [1986] 159 ITR 78, held that:

“In this case, the assessee had given the names and addresses of the alleged creditors. It was in the knowledge of the Revenue that the said creditors were income tax assessee. Their index numbers were in the file of the Revenue. The Revenue, apart from issuing notices under section 131 at the instance of the assessee, did not pursue the matter further. The Revenue did not examine the source of income of the said alleged creditors to find out whether they were creditworthy or were such who could advance the alleged loans. There was no effort made to pursue the so-called alleged creditors. In those circumstances, the assessee could not do anything further. In the premises, if the Tribunal came to the conclusions that the assessee has discharged the burden that lay on him, then it could not be said that such a conclusion was unreasonable or preserve or based on no evidence. If the conclusion is based on some evidence on which a conclusion could be arrived at, no question of law as such arises.”

11. In view of the above submissions, documents and judicial precedents, it is submitted that the appellant has fully discharged its burden u/s 68 of the Act and the burden has shifted on to the department and the Assessing Officer has not discharged the burden u/s 68 of the Act proving the contrary. Thus, the addition of Rs 12,54,54,594/- on account of unexplained credit u/s 68 of the Act shall be deleted.

12. The ground of appeal no. 5 is as below:

“Ground Number 5: On the facts and the circumstances of the appellant’s case and in law the Assessing Officer has erred in initiating penalty proceedings u/s 271AAC of the Act.”

13. We humbly submit that the Assessing Officer has not only passed the impugned assessment order by disregarding the submissions and explanations submitted by the appellant company but also erred in Initiating penalty proceedings u/s 271AAC of the Income Tax Act, 1961.

14. In view of the above facts, the alleged addition and the consequent order passed u/s 143(3) of the Act dated 21.09.2022 is invalid, incorrect, illegal, not as per provisions of law, clearly outside the sanction of law, illegal, bad-in-law, void for want of jurisdiction and thus may kindly be deleted/quashed/annulled.

15. Further, the appellant may kindly be informed, if any further clarification or details/ documents or any further information is required for deciding the matter. The transactions are fully corroborated and supported by the necessary relevant documents and have been furnished but in case any further documents are required, the same can readily be provided before a decision is taken in the matter.

16. In addition to the above, your honour may kindly provide us with an opportunity for further submissions before deciding on the matter.”

12. The Ld. Commissioner by considering the assessment order and the submissions of the Assessee, and examining the case in detail, ultimately affirmed the addition of Rs. 12,54,54,594/- made by the AO, as unexplained credit u/s 68 of the Act, by more or less observing and holding as under:

“That the Assessee has submitted a copy of “gift deed”, however no evidence regarding mode of payment/receipts i.e. no bank statement of her husband and the Assessee, was submitted, showing the transfer of funds in respect of gift. Further, the AO has found that Shri Ripu Sudan Kundra has shown income of Rs. 27,71,020/- in his return of income for A.Y 2020-21, which does not commensurate with the amount of gift of Rs. 12,54,54,594/- given to the Assessee. Further during the appellate proceedings, the Assessee has submitted that she had provided copy of gift deed and PAN and address of the Donor and copy of the acknowledgment return for A.Y 2020-21. Further she has discharged the burden cast u/s 68 of the Act and AO has not carried out investigation from the Donor by issuing summons u/s 131 of the Act and has relied on various case laws. Though the Assessee has received gift of Rs. 12,54,54,594/- from her husband, Shri Ripu Sudan Kundra. However, the Assessee has not submitted a copy of bank statement of herself, as well as of her husband before the AO or before him. Moreover, it is found that Shri Ripu Sudan Kundra has shown income of Rs. 27,71,020/- for the A.Y 2020-21, which does not commensurate with the gift of Rs. 12,54,54,594/- given by him to the Assessee. Therefore, genuineness and creditworthiness of the donor, is not established. Further, the Assessee could not be able to furnish the source of fund received as gift, in the absence of bank statement of her husband. Therefore, the AO has rightly relied on the case laws and from the decisions, it is clear that primary onus of proof lies on the Assessee, as she has made claim of gift received in her return of income. In view of the facts and judicial precedents referred above, since the Assessee has failed to prove genuineness and creditworthiness of the Donor, addition of Rs. 12,54,54,594/- made by the AO, as unexplained credit u/s 68 of the Act, is confirmed.”

13. The Assessee being aggrieved challenged the said decision of the Ld. Commissioner in sustaining the addition vide impugned order, which is under consideration before us.

14. The Ld. Counsel for the Assessee at the outset submitted that the Assessee had duly filed the relevant documents and details substantiating the donation under consideration, such as full name of the Donor and Donee, details of PANs of Donor and Donee, relationship between the Donor and Donee, full address of Donor and Donee and acknowledgment of income tax return of Donor for the A.Y 2020-21 and therefore the Assessee has discharged her primary onus cast u/s 68 of the Act. The Ld. Counsel for the Assessee also relied on various judgments including the decisions of Hon’ble Apex Court in the cases of CIT v. Orissa Corporation (P) Ltd. AIR 1986 SC 1849 and CIT v. Divine Leasing & Finance ltd ITR 268 (Delhi), which we will deal with, in the latter part of the order. The Ld. Counsel also placed on record, the copy of gift deed executed by the husband of the Assessee and clarificatory affidavits of the Assessee and her husband qua gift.

15. On the contrary, Ld. DR refuted the claim of the Assessee by submitting that before either of the authorities the Assessee has not submitted the details of the transaction involved and / or the mode of payment of gift. Further the Assessee did not file the bank statement despite being asked specifically by the authorities below, on various occasions. Even the return of income of the Donor, is not commensurate with the gifted amount given. The PAN of the donor was only provided on dated 15.09.2022 i.e. at the fag end of the assessment proceedings and therefore in the constrained circumstances, the AO was unable to enquire about the gift from the Donor through the process u/s 133(6) of the Act. Further, the Assessee despite asking specific queries by this court as well, has not filed the relevant individual bank statements of the Assessee and her husband demonstrating the actual movement of transactions carried out. Somehow, on many persuasions by this Court only, the Assessee has filed the Punjab National Bank Statement, wherein the Assessee and her husband jointly holding the bank account, wherein certain amount has allegedly been shown/claimed as received from overseas by the husband of the Assessee and out of the said amount the amount of Rs. 12,54,54,594/- has been claimed as gifted by the Assessee’s husband to the Assessee, without any actual moment of money and / or transferring the amount of gift from one account to another. The Ld. DR also submitted that the judgments relied upon by the Assessee are factually dissimilar and thus not applicable to her case. And thus, the Assessee’s claim is liable to be disallowed by affirming the addition made and confirmed by the AO and the Ld. Commissioner respectively.

16. Heard the parties and perused the material available on record. The controversy involved in the instant case pertains to the amount of Rs.12,54,54,594/- which has been claimed as gift received by the Assessee from her husband and accordingly declared the said amount in her return of income, which came into consideration, during the assessment proceedings and thus, the AO issued show cause notices to the Assessee to justify the gift amount received from her husband, by producing the relevant documents including the bank statements etc.

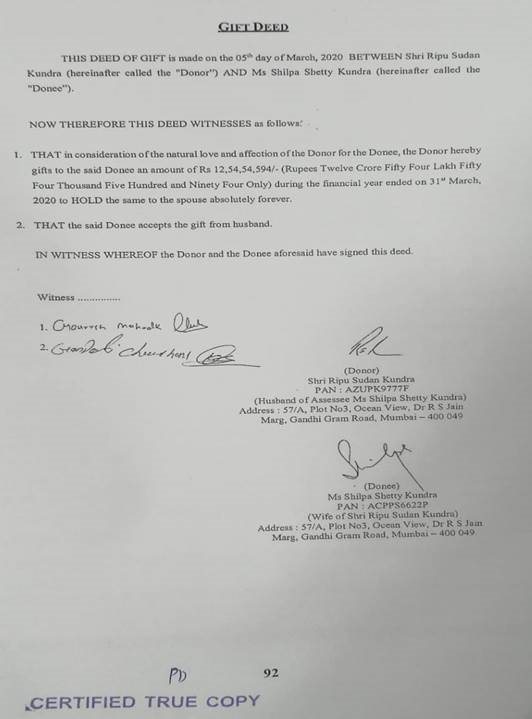

17. The Assessee before the AO, vide reply dated 15.09.2022 claimed that the Assessee’s husband has gifted the said amount during the year ended on 31.03.2020 out of natural love and affection to hold the same by the Assessee absolutely forever. The Assessee before the AO also filed the gift deed dated 05.03.2020 executed between husband and wife, along with acknowledgment of income tax return in form no.ITR-5 filed on dated 29.01.2021 by the Assessee’s husband.

18. The AO though considered the said reply and the gift deed filed by the Assessee. However, could not get impressed, as in spite of repeated opportunities, the Assessee except providing scanned copy of ‘gift deed’ failed to provide any evidence with regard to mode of payment/receipt and bank statement of Assessee and her husband, showing the actual transfer of the gifted amount. The AO also observed that the PAN of Assessee’s husband was provided only by reply dated 15.09.2022 i.e. at the fag end, so that no further enquiry could be made under Section 68 of the Act. Further the Assessee’s husband has shown his total income at Rs.27,71,020/- for the AY under consideration, which does not commensurate with the amount of gift given and therefore, the credit worthiness of the Donor could not be established. The AO therefore, more or less on the aforesaid reasons made the addition of the gifted amount under consideration.

19. We further observe from the impugned order that before the ld. Commissioner as well, the Assessee admittedly failed to file any copy of the bank statement of the Assessee and her husband despite being asked specifically and therefore the ld. Commissioner affirmed the addition made by the AO under Section 68 of the Act by considering the peculiar facts and circumstances specific to the effect that the Assessee failed to file the bank statement showing the corresponding bank entry pertaining to the gifted amount and the Assessee’s husband’s income to the tune of Rs.27,71,020/- for the AY 2020-21 does not commensurate with the gift amount. Further, the Assessee failed to furnish the source of fund.

20. We observe that before us, on being asked specifically the Assessee only provided the joint bank statement of account maintained with Punjab National Bank, which was/is operated jointly by the Assessee and her husband, wherefrom it appears that the amount of Rs.12,81,41,672/- is appearing, as deposit on dated 12.02.2020 vide remittance ID (4553 IMT 034914) and prior to that entry, as on 31.01.2020 in that particular account, the amount of Rs.3045,41,637/- is appearing as credit balance after entry of Rs.12,81,41,672/- on dated 12.02.2020. There are various transactions, appears to have been carried out. The Assessee has claimed that on 31.03.2020, she has received Rs.12,54,54,593/- through aforesaid bank account bearing no.6629009300000144 maintained with Punjab National Bank. However, as per bank statement dated 20.04.2024 submitted by the Assessee, it appears that as on 31.03.2020, the amount of Rs.24,82,29,633/- was available in such bank account and there is no clear cut transaction of the gifted amount under consideration, reflecting in such bank account.

21. We further observe from the gift deed submitted by the Assessee, which read as under: –

The Donor has mentioned in para no.1 of such deed that amount of Rs.12,54,54,594/- was gifted to the donee during the FY ended 31.03.2020 to hold the same to the spouse absolutely forever. However, in the gift deed, it is nowhere mentioned, the mode of transferring such gifted amount and/or the bank account details and/or the source of such fund/gifted amount. We further observe from the clarificatory affidavits dated 24.03.2025 filed by the Assessee of herself and her husband before this Court that in the said affidavits also, the mode of payment/mode of gift/detail of transferring the gifted amount, is nowhere mentioned.

22. Though the Assessee has filed the copy of ledger account qua Assessee’s husband for the AY under consideration showing the amount of Rs.12,81,41,672/- with a narration: Remittance ID (4553 IMT 03491420) realize Kuki – received towards repayment of loan of Ripu Sudan Kundra dated 12.02.2020 and thereafter two bank transactions of Rs.10 lakhs each carried out on dated 17.02.2020 and further shown the amount of Rs.12,54,54,593/- as on 31.03.2020 the gifted amount received from Shri Ripu Sudan Kundra however, it is a fact that from the bank statement referred to above, the actual movement of gifted amount, is no-where appearing. There is also no corelation in the bank entries, qua amount involved.

23. As observed above that in the above bank statement, as on 31.03.2020, the amount of Rs.24,82,29,633/- was available as balance and up to 31.03.2020, the mode/movement of aforesaid gifted amount, is nowhere appearing in the bank statement and also not clearly established by the Assessee.

24. We further observe that the Assessee before the authorities below has only filed acknowledgment of return filed by the Assessee’s husband for the AY under consideration, without its financials/profit and loss account. However, before us on being asked the Assessee has filed complete copy of ITRs of the Assessee’s husband for the AYs 2019-20 and 2020-2021.

Perusing the same, we observe that the Assessee’s husband in the Schedule FA (which pertains to the details of foreign assets and income from any source outside India) and in Column no. B of such schedule, which pertains to the details of financial interest in any entity held (including any beneficial interest) at any time during the relevant accounting period, has shown the total investment (at cost) 150, name of the entity: ‘Kuki investments’, address of the entity: ‘BAHAMAS Zip Code 1242’, nature of interest: ‘Direct’, Date since held: ‘02.02.2009’ income taxable and offered in the return: ‘No income during the year’. Further, the Assessee’s husband in Column no. D of such Schedule (which pertains to details of any other capital asset held (including any beneficial interest) at any time during the relevant accounting period), has mentioned the amount of Rs.72,12,33,650/- as investment being nature of asset: ‘BAHAMAS’ with ‘Direct ownership’ and acquisition made on ‘02.02.2009’ and having offered no income earned and taxable in the return of income as ‘NO income’ earned during the year.

25. Further in the Column-B of Schedule-FA filed alongwith ITR for the AY 2020-21, which is under consideration, the Assessee’s husband repeated the same entries, as mentioned in the ITR of AY 2019-20. Further, in the Column-D, which pertains to details of any other capital asset held (including any beneficial interest) at any time during the relevant accounting period, has shown the amount of total investment at ‘Rs.22,81,85,851/-‘. Further shown having ‘no taxable income and offered in the return of income ‘during the year under consideration.

26. In both the ITRs of 2019-20 and 2020-21, the income derived from the Asset has been shown as “0”. Admittedly in the bank statement, the credit amount of Rs.12,81,41,672/- having credited on 12.02.2020 having remittance ID (4553 IMT 034914) however, such amount is nowhere appearing in the FA Schedules of ITRs as filled up by the Assessee. There is also no co-relation of Schedule FA, with the aforesaid transaction dated 12.02.2020.

27. Thus, on the aforesaid analyzations, we reiterate again:

| (i) |

|

That in the gift deed as submitted by the Assessee, the mode of transaction of gifted amount is not specified. |

| (ii) |

|

Further, how the gifted amount has actually been transferred is also not specified. |

| (iii) |

|

Further, the Assessee despite asking specifically on various time by the authorities below, also did not file the relevant bank statements. |

| (iv) |

|

Further, the Assessee also failed to co-relate the transacted amount with the appropriate evidence. |

| (v) |

|

Further, the claim of the Assessee that Assessee’s husband had received the amount of Rs.12,81,41,672/- from M/s. Kuki Investment, is not established clearly. |

| (vi) |

|

The Assessee has also claimed that a sum of Rs.72,12,33,650/- was receivable by Assessee’s husband from M/s. Kuki Investment, which has been disclosed in the ITR for the AY 2019-20 under “Schedule AL”, whereas in the AL-Schedule the amount of Rs.84,05,77,374/- is showing, as loans and advances given and there is no such bifurcation of such amount, as claimed by the Assessee. |

| (vii) |

|

Further, in the ITR of 2020-21 year, the Assessee’s husband has shown total investment in BAHAMAS to the tune of Rs.22,81,85,851/- in Column-D of Schedule-FA but in Schedule-AL, the Assessee’s husband left all columns as blank without giving any details. Therefore, various discrepancies remained to be proved by the Assessee to establish the genuineness of the gift transaction. |

| (viii) |

|

Further the Assessee’s husband income was not commensurate with the gifted amount. |

| (ix) |

|

Further legal sanctity/validity of ‘gift deed’ is also requires to be established. |

| (x) |

|

Further, in our considered view that details and documents available on record and to be filed further, to establish the genuineness of the transaction, requires clarifications and factual verifications. |

28. No doubt the Assessee has provided PAN no. of the Assessee’s husband, along with the copy of the ITR filed by the Assessee’s husband however, it is a fact as observed by the AO that the Assessee has provided the details of the Assessee’s husband at the fag end of the assessment proceedings and therefore, the AO was unable to carry out proper enquiries under Section 133(6) of the Act. Further it is also a fact that before both the authorities below, the Assessee despite being asked specifically, failed to file the bank statements depicting the actual transactions carried out with regard to the gifted amount. Further, in the gift deed and the clarificatory affidavits, as filed before us, the Assessee failed to specify the mode of payment received and/or the mode of gift amount. Further, it is also admitted fact that the Assessee though before us has filed complete ITRs of Assessee’s husband for the AYs 2019-20 and 2020-21 however, failed to establish the transaction clearly. Further, also failed to establish the source of the Assessee’s husband for gifting such huge amount in clear manner and with substantive documents. Even otherwise complete ITRs and the Punjab National Bank statement as filed by the Assessee before us were not made available before the authorities below, despite being asked specifically. Thus, in our view the Assessee deserve no leniency however, considering the peculiar facts and circumstances specific to the effect as well that the Assessee though filed certain details and documents but not discharged her prima facie onus cast under Section 68 of the Act completely by filing complete details/clarifications and relevant documents and in the absence of relevant details and documents and clarification, which the Assessee admittedly failed to file/offer, the issue involved also remained to be adjudicated in its right perspective and proper manner. Even otherwise in our considered view, the details and documents available on record and to be furnished by the Assessee in order to discharge her prima facie onus cast u/s 68 of the act completely, as observed above, requires factual verification. Thus, considering the peculiar facts and circumstances in totality for proper and just decision of the case and substantial justice, we are inclined to remand the instant case to the file of the Jurisdictional AO (JAO) for decision afresh, suffice it to say by affording reasonable opportunity of being heard to the Assessee.

29. We also deem it appropriate to direct the Assessee to establish her claim by filing/providing complete details/clarifications and documents before the JAO, without any default. We clarify that in case of subsequent default, the Assessee shall not be entitled for any leniency.

30. Thus, the case is accordingly remanded to the file of the Jurisdictional AO (JAO) for decision afresh, suffice it to say by affording reasonable opportunity of being heard to the Assessee.

31. The judgements relied on by the parties prima facie appears to be factually dissimilar to the peculiar facts and circumstances of this case and the issue involved and therefore are not strictly applicable to the case in hand and thus, we deem it appropriate not to explore the same in depth, as we have decided to remand the case to the file of the AO for ‘de novo decision’.

32. In the result, Assessee’s appeal is allowed for statistical purposes, in the above terms.