ORDER

Madhusudan Sawdia, Accountant Member.- This appeal is filed by AML Motors Private Limited (“the assessee”), feeling aggrieved by the order passed by the Learned ADDL/JCIT(A), Udaipur (“Ld. First Appellate Authority”) dated 28.11.2024 for the A.Y.2023-24.

2. At the outset, it is observed that there is a delay of 241 days in filing the present appeal before the Tribunal. The assessee has filed a petition for condonation of delay along with an affidavit explaining the reasons for such delay. It has been submitted that the Finance Head of the assessee, who was primarily responsible for overseeing and coordinating tax litigation matters, was unable to attend to such responsibilities due to the serious medical condition of his wife during the relevant period. In support of the same, the assessee has placed on record the medical reports of the wife of the Finance Head. Therefore, the Learned Authorized Representative (“Ld. AR”) submitted that the delay in filing the appeal before the Tribunal was beyond the control of the assessee. Accordingly, the Ld. AR prayed before the Bench for condonation of delay and admission of the appeal for adjudication on merits.

3. Per contra, the Learned Departmental Representative (“Ld. DR”) objected to the condonation of delay and submitted that no sufficient cause has been shown by the assessee for such an inordinate delay. It was further contended that the responsibility to file the appeal ultimately lies with the Managing Director of the assessee company, and therefore, the reasons advanced regarding the medical condition of the wife of the Finance Head are not convincing. Accordingly, the Ld. DR prayed that the delay should not be condoned.

4. We have carefully considered the rival submissions and perused the material available on record. The Ld. AR submitted that the delay of 241 days occurred due to unavoidable circumstances, as the Finance Head of the assessee, who was entrusted with handling tax matters, could not attend to his duties owing to the serious medical condition of his wife. We have gone through the affidavit and the medical records placed on record and on perusal of the same, we find that the explanation furnished by the assessee is duly supported by documentary evidence. Though the Ld. DR has objected to the condonation of delay on the ground that the Managing Director is ultimately responsible for filing the appeal, we are of the considered view that practical realities of corporate functioning cannot be ignored, where specific responsibilities are delegated to concerned officials. When such an official is prevented by reasonable and bona fide circumstances, the same constitutes a sufficient cause for delay. Considering the totality of the facts and circumstances of the case, and in the absence of any material to suggest that the delay was deliberate or due to negligence, we are satisfied that the assessee was prevented by sufficient cause from filing the appeal within the prescribed time. Further, we find that the Hon’ble Supreme Court, in the case of Vidya Shankar Jaiswal v. ITO (SC), has held that a justice-oriented and liberal approach should be adopted while considering applications for condonation of delay. Respectfully following the said principle, we condone the delay of 241 days and admit the appeal for adjudication on merits.

5. The assessee has raised the following grounds of appeal:

| “1. |

|

The order of the Ld. Addl/JCIT(A) Udaipur [Ld. CIT(A)] and Ld. Deputy Director of Income Tax, CPC [Ld. AO], in denying the valid claim made under Section 80JJAA of the Act is totally contrary to the facts and evidence on record and therefore unsustainable both on facts and in law. |

| 2. |

|

The Ld. CIT(A)/Ld. AO ought to have appreciated that the Appellant complied with all the conditions under the Act and had also duly obtained Form No.10DA from a Chartered Accountant on 25th September 2023, and it was only due to technical glitches in the new IT portal that the form was filed on 17th October 2023. |

| 3. |

|

The Ld. CIT(A)/Ld.AO failed to note that mere procedural lapse ought to be condoned to prevent genuine hardships to the Appellant who has fulfilled all the conditions prescribed under Section 80JJAA of the Act. |

| 4. |

|

The Ld. CIT(A)/Ld.AO failed to consider that the Appellant had justified the reason for the delay in filing form 10DA was due to a technical glitch in the portal. |

| 5. |

|

Any other ground(s) that may be urged at the time of hearing.” |

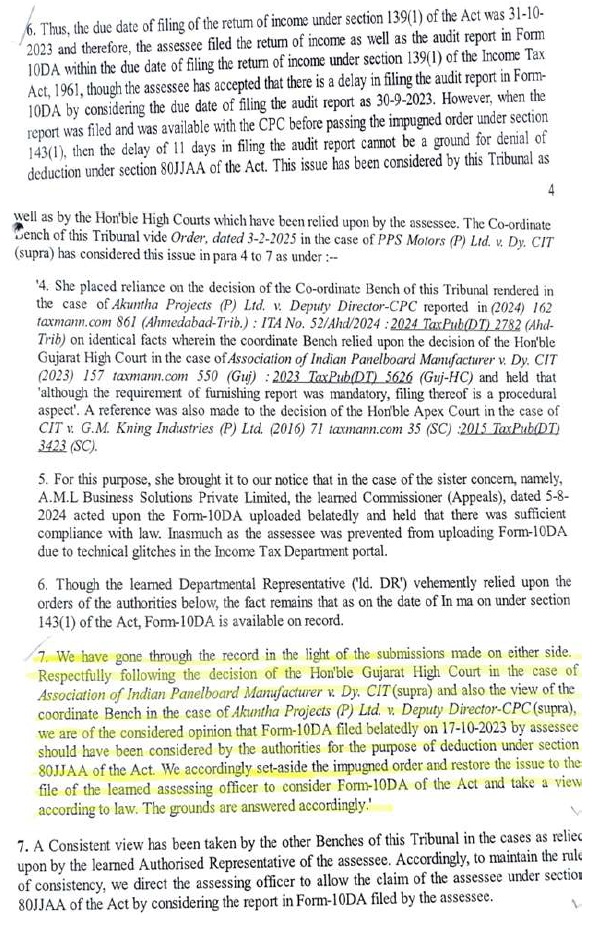

6. The brief facts of the case are that the assessee is a company engaged in the wholesale business and retail sale of motor vehicles along with maintenance and repair services and sale of related spare parts. The assessee filed its return of income under section 139(1) of the Income Tax Act, 1961 (“the Act”) for Assessment Year 2023-24 on 18.10.2023, declaring total income of Rs.12,87,460/-. In the return of income, the assessee claimed deduction under section 80JJAA of the Act amounting to Rs.75,08,759/-. As per the provisions of the Act read with Rule 19AB of the Income Tax Rules, 1962, the assessee was required to obtain a report in Form No. 10DA from a Chartered Accountant and furnish the same on or before the specified due date i.e., 30.09.2023 for the year under consideration. However, in the present case, the assessee filed Form No. 10DA on 16.10.2023 and thereafter filed the return of income on 18.10.2023. Subsequently, the return of income of the assessee was processed by Centralized Processing Centre (“CPC”) under section 143(1) of the Act on 22.12.2023, wherein the claim of deduction under section 80JJAA of the Act amounting to Rs.75,08,759/- was denied on the ground that Form No. 10DA was filed beyond the prescribed due date.

7. Aggrieved with the order of the CPC, the assessee preferred an appeal before the Ld. CIT(A). The Ld. CIT (A) confirmed the action of CPC and dismissed the appeal of the assessee.

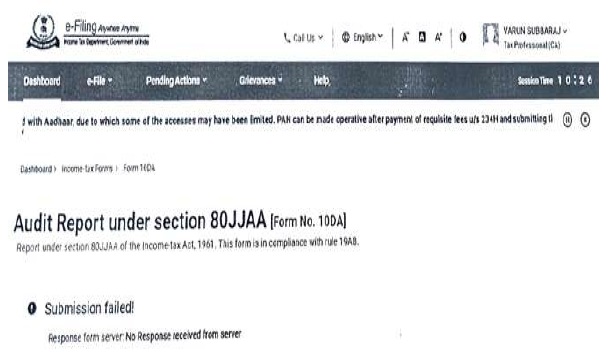

8. Aggrieved with the order of the Ld. CIT (A), the assessee is in appeal before the Tribunal. The Ld. AR submitted that the assessee had obtained the audit report in Form No. 10DA from the Chartered Accountant well within the specified due date. It was submitted that the auditor attempted to upload the said form on 25.09.2023; however, due to technical glitches on the income tax portal, the same could not be filed. In support, the Ld. AR drew our attention to the screenshot evidencing the failure of submission due to technical glitches, placed at page no. 15 of the paper book. The Ld. AR also referred to Form No. 10DA placed at page nos. 16 and 17 of the paper book and submitted that the same was eventually filed on 16.10.2023. It was further submitted that the assessee filed its return of income on 18.10.2023 and that Form No. 10DA, though filed belatedly, was filed prior to filing of the return of income and was very much available on record at the time of processing by the CPC under section 143(1) of the Act. Therefore, the CPC ought not to have denied the deduction. The Ld. AR also submitted that during the relevant period, the auditor was engaged in time-barring audit assignments of several assessees, and coupled with technical glitches, the form could not be uploaded within time. It was thus prayed that the delay in filing Form No. 10DA be condoned and the deduction under section 80JJAA of the Act be allowed. In support of the contention, reliance was placed on the decisions of the Hyderabad Bench of the Tribunal in the case of High Precision Engineering Composites (P.) Ltd. v. ITO [IT Appeal No. 328 (Hyd.) of 2025, dated 12-6-2025] and PPS Motors(P.) Ltd. v. Dy. CIT [IT Appeal No. 1133 (Hyd.) of 2024, dated 3-2-2025], wherein under similar facts, the deduction under section 80JJAA of the Act was allowed by the Tribunal.

9. Per contra, the Ld. DR relied on the orders of the lower authorities and submitted that as per the statutory mandate, the assessee was required to furnish Form No. 10DA on or before the specified due date i.e., 30.09.2023. Since the assessee filed the same only on 16.10.2023, the claim of deduction under section 80JJAA of the Act was rightly denied. The Ld. DR further submitted that the assessee had also filed an application for condonation of delay before the Learned Principal Commissioner of Income Tax (“Ld. PCIT”) under section 119(2)(b) of the Act, which was rejected vide order dated 06.06.2025. Therefore, it was contended that once the delay has been rejected by the competent authority under section 119(2)(b) of the Act, the remedy available to the assessee lies before the Hon’ble High Court and not before the Tribunal. In support of the contention, reliance was placed on the decisions of the Coordinate Benches of the Tribunal in the case of Shrishti Institute of Medical Science and Research Centre v. CIT (Exemption) (Raipur – Trib.), Seva Bharathi v. CIT (Exemption) [IT Appeal No. 365 (Hyd.) of 2025, dated 15-10-2025], and the judgment of the Hon’ble Karnataka High Court in the case of Devendra Pai v. Asstt. CIT (Karnataka)/[2021] 439 ITR 532 (Karnataka). Accordingly, it was prayed that the order of the lower authorities be upheld.

10. We have carefully considered the rival submissions and perused the material available on record including the case laws relied upon. In the present case, it is an undisputed fact that the assessee had obtained the audit report in Form No. 10DA within the prescribed time and had attempted to upload the same before the due date; however, due to technical glitches on the portal, the form could not be filed within time. In this regard, we have gone through the copy of screenshot placed at page no. 15 of the paper book, which is to the following effect:

11. On perusal of the above, we find merit in the contention of the assessee regarding technical difficulties faced during filing. It is further observed that Form No. 10DA was ultimately filed on 16.10.2023, which is prior to the filing of the return of income on 18.10.2023. Thus, at the time of processing of return under section 143(1) of the Act, the said report was very much available on record with the CPC. We have also gone through para nos. 6 and 7 the decisions of the Hyderabad Bench of the Tribunal in the case of High Precision Engineering Composites Pvt. Ltd. (supra), which is to the following effect:

12. On perusal of above, we find that under identical circumstances, the Tribunal relying on the decision of the Hyderabad Bench of the Tribunal in the case of PPS Motors Pvt. Ltd. (supra), has held that when Form No.10DA was available with the CPC at the time of processing of the return of income of the assessee, the delay in filing of Form 10DA cannot be a ground for denial of deduction under section 80JJAA of the Act. Accordingly, the Tribunal allowed the claim of deduction under section 80JJAA of the Act of the assessee. Therefore, respectfully following the decisions of the Coordinate Bench of the Tribunal in identical matters, we are of the considered view that in the present case the assessee is eligible for deduction under section 80JJAA of the Act. Further, as regards the objection of the Ld. DR that the application filed by the assessee under section 119(2)(b) of the Act has been rejected by the Ld. PCIT, we find that the order passed by the Ld. CIT(A), against which the present appeal is filed, is dated 28.11.2024, whereas the order passed by the Ld. PCIT under section 119(2)(b) of the Act is dated 06.06.2025, i.e., subsequent to the order of the Ld. CIT(A). Therefore, as on the date of passing of the appellate order by the Ld. CIT(A), there was no rejection under section 119(2)(b) of the Act. Furthermore, the present appeal is directed against the order of the Ld. CIT(A) and not against the order passed by the Ld. PCIT under section 119(2)(b) of the Act. Therefore, the objection raised by the Ld. DR in this regard is not tenable. Further, the decisions relied upon by the Ld. DR are distinguishable on facts, as in those cases, the appeals were directly against the orders passed under section 119(2)(b) of the Act. Considering the totality of the facts and circumstances of the case and respectfully following the decisions of the Coordinate Bench of Tribunal(supra) in identical matters, we direct the Ld. AO to admit Form No. 10DA filed by the assessee and allow the deduction under section 80JJAA of the Act in accordance with law.

13. In the result, the appeal of the assessee is allowed.