PROCEEDINGS

Note 1: Under Section 100 of the CGST/RGST Act, 2017, an appeal against this ruling lies before the Appellate Authority for Advance Ruling, constituted under Section 99 of CGST/RGST Act, 2017, within a period of 30 days from the date of service of this order.

Note 2: At the outset, we would like to make it clear that the provisions of both the CGST Act and the RGST Act are the same except for certain provisions. Therefore, unless a mention is specifically made to such dissimilar provisions, a reference to the CGST Act would also mean a reference to the same provision under the RGST Act. Further to the earlier, henceforth for the purposes of this Advance Ruling, a reference to such a similar provision under the CGST Act / RGST Act would be mentioned as being under the “GST Act”.

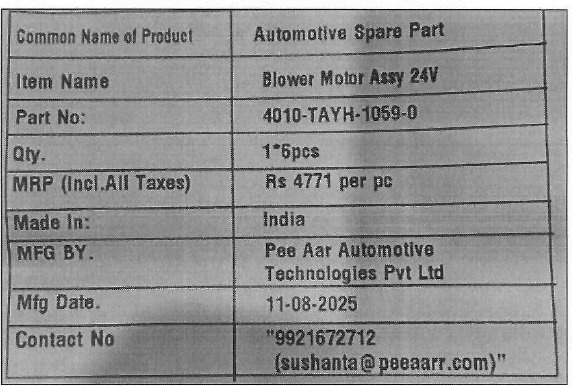

The issue raised by M/s PEE AAR AUTOMOTIVE TECHNOLOGIES PRIVATE LIMITED, E-311, E-312, General Zone, Industrial Area Ghiloth, Shahjahanpur, ALWAR- 301706, Rajasthan (hereinafter “the applicant”) is fit to pronounce advance ruling as they have deposited prescribed Fee under CGST Act and it falls under the ambit of the Section 97(2) given as under:

| (a) |

|

classification of goods and/or services or both |

| (b) |

|

determination of the liability to pay tax paid or deemed to have been paid |

A. SUBMISSION OF THE APPLICANT (in brief):-

Brief facts of the case:

The Applicant, M/s PEE AAR Automotive Technologies Pvt. Ltd., is presently engaged in the manufacturing and supply of Condenser Fans and Blower. These fans & blower are designed for air circulation in a bus engine system and do not incorporate any temperature control. The manufacturing takes place entirely at the Applicant’s own production facility at Ghiloth, Alwar, Rajasthan, which is equipped with dedicated machinery, motor assembly units, blade fabrication lines, and shroud fitting stations to ensure quality and uniformity in production.

The condenser fan & blower produced by the Applicant has a high-capacity exhausting function that removes hot air from the bus condenser section or engine compartment and expels it to the outside atmosphere, enabling fresh air intake.

The product is essentially a mechanical air-moving device which facilitates forced ventilation, thereby qualifying as an “Air Circulator.” The technical nature of the product aligns with the scope of HSN 8414 59 30, which covers Industrial fans and blowers.

1.1. Nature of Airflow and Operating Mechanism

The condenser fan consists of three major components (1) motor, (2) shroud, and (3) blade, integrated into a robust assembly.

The electric motor powers the rotation of the aerodynamic blades housed inside the shroud, ensuring directional airflow.

When in operation, the fan creates a negative pressure (vacuum) in the immediate surrounding area, causing hot or stale air to be evacuated. This vacuum is then replaced with fresh ambient air, completing the air circulation cycle.

The design is tailored for high static pressure performance to match the operational needs of large vehicles like buses, where airflow efficiency and durability are critical.

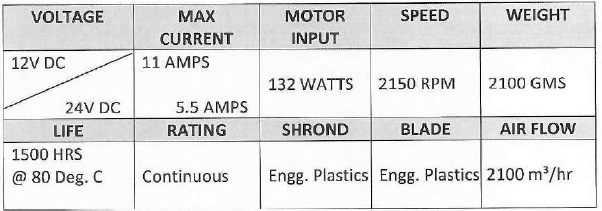

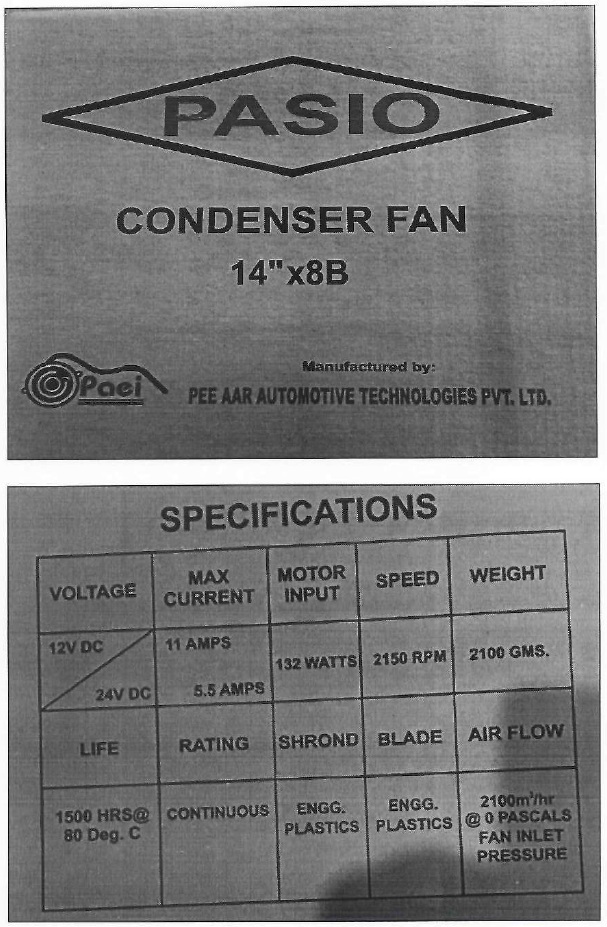

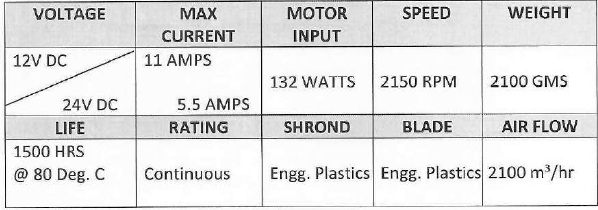

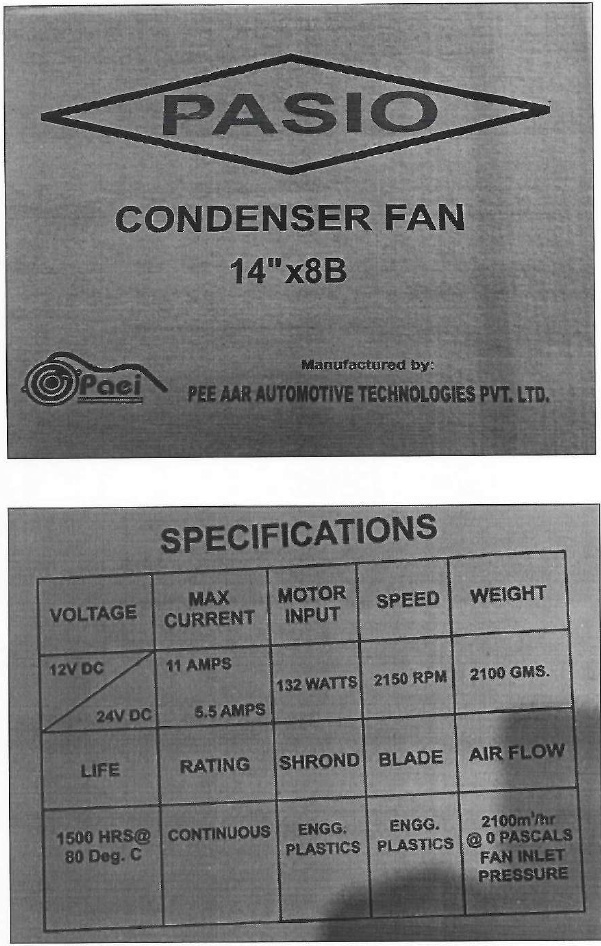

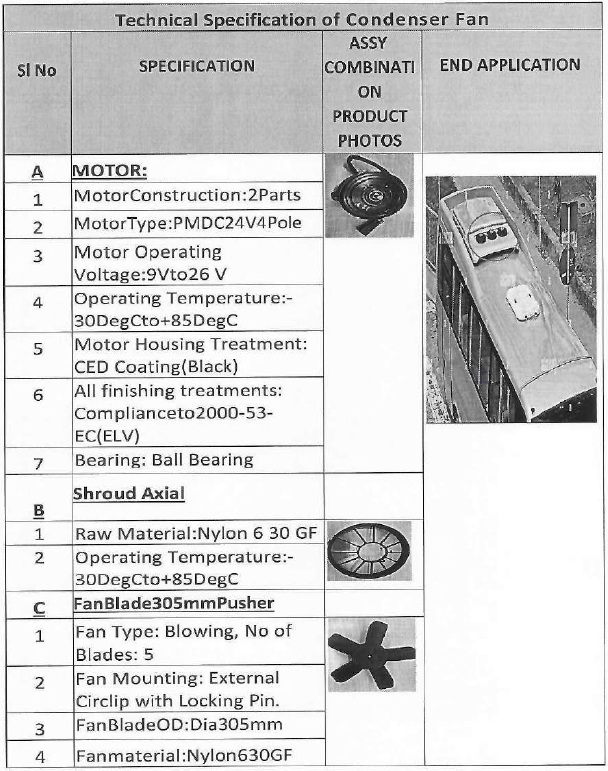

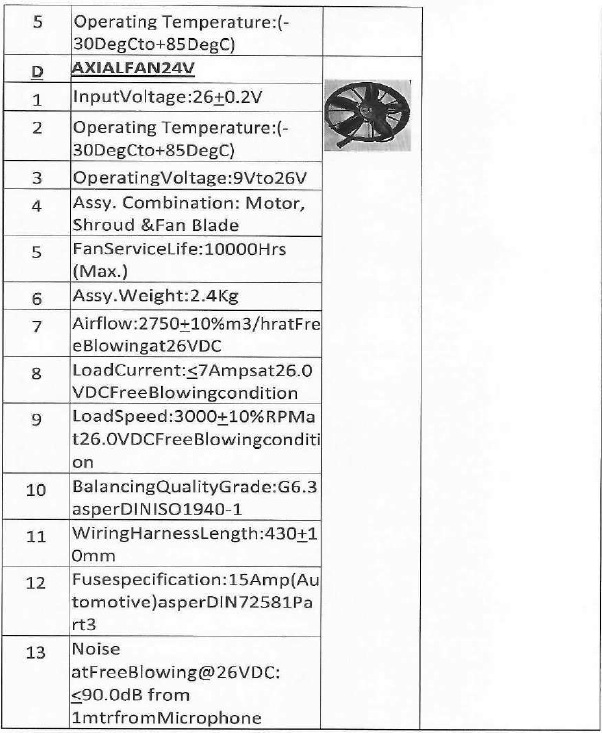

The specification of good viz., Condenser Fan is tabulated as under :

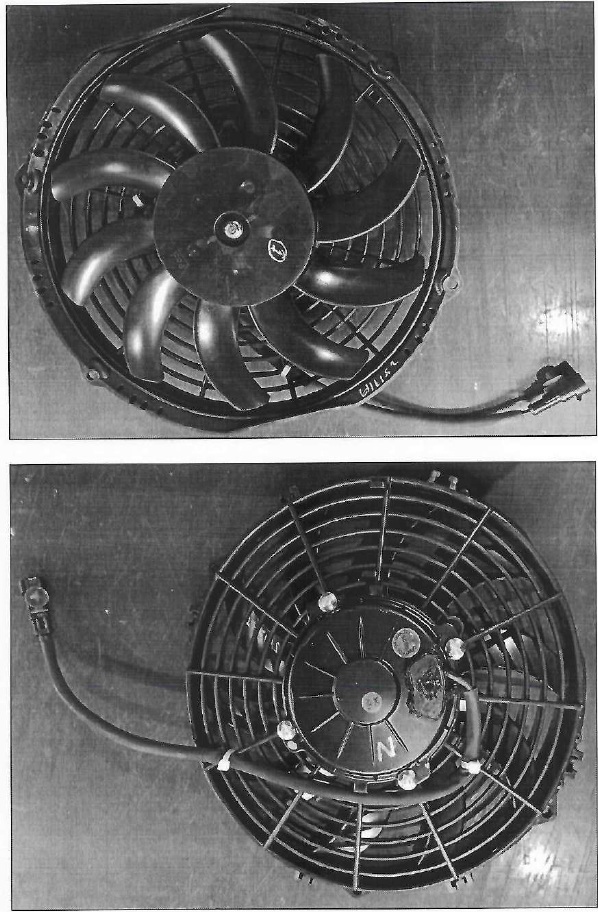

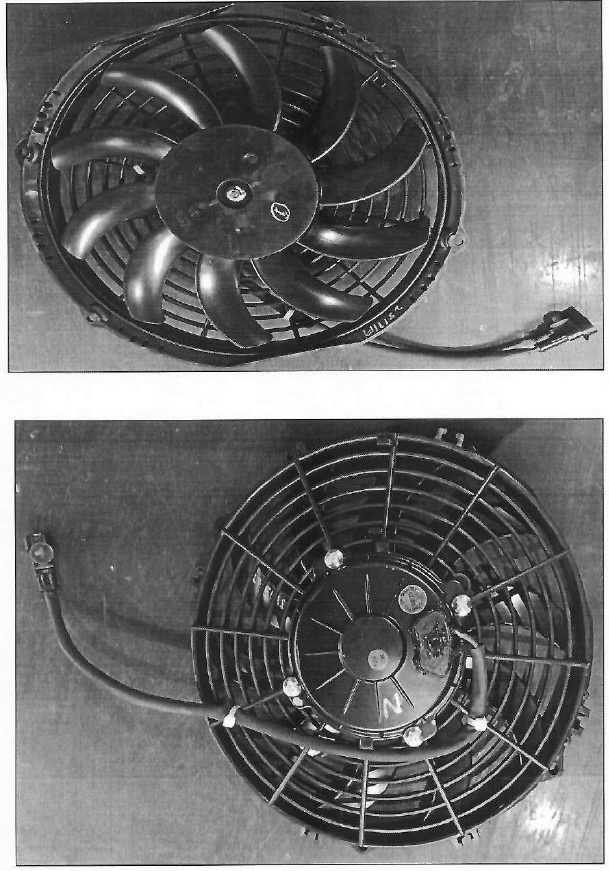

The image of goods viz. , Condenser fan is as follows:

The image of goods viz., Blower is as follows:

1.2. Seeking Classification and Rate Clarity Under the GST Regime

The advance ruling is being sought in relation to the classification of Condenser Fan and Blower under the GST Tariff Schedule. The Applicant is engaged in the ongoing manufacture and supply of this product and is seeking a ruling to determine whether the appropriate classification is under Heading 8414 as a Industrial fans and blowers (specifically under HSN 8414.59.30) or any alternate classification.

The objective of the ruling is to obtain legal clarity and certainty on the applicable GST classification and tax rate for Condenser Fan and Blower, considering its Industrial fans and blowers.

B. INTERPRETATION AND UNDERSTANDING OF APPLICANT ON QUESTION RAISED (IN BRIEF)

1.3. Description of the Product – Condenser Fan

The product manufactured by the Applicant is a Condenser Fan designed for use in heavy-duty bus rooftop and engine applications. It consists of an electric motor that drives aerodynamic blades housed in a protective shroud, creating high-volume axial airflow. The primary function is to force hot air away from the condenser coil or radiator. The condenser fan operates purely as a mechanical air-moving device and does not have any integrated temperature control, refrigeration, or air-conditioning unit within itself.

1.4. Composition of the Product – Condenser Fan

The condenser fan assembly comprises the following major components:

| • |

|

Electric Motor: An industrial-grade, high-efficiency electric motor designed for continuous operation in high-temperature environments. |

| • |

|

Fan Blades: Precision-moulded blades, often made of reinforced engineering plastic or aluminium alloy, optimized for aerodynamic performance and reduced noise levels. |

| • |

|

Shroud/Housing: A circular or semi-circular enclosure made from powder- coated steel or polymer, guiding airflow and providing physical protection. |

| • |

|

Mounting Brackets/Frame: Fabricated steel components for secure attachment in the bus’s condenser compartment or engine bay. |

| • |

|

Electrical Connectors and Wiring Harness: Heat-resistant cables for safe and efficient power transmission from the vehicle’s electrical system. |

The specification of good viz., Condenser Fan is tabulated as under:

The image of goods viz., Condenser fan is as follows:

The technical specification of the Condenser Fans with end application is as follows:

1.5. Manufacturing Process & Technical Features of the Product – Condenser Fan

| • |

|

The manufacturing process begins with sourcing raw materials such as motor components, blade mouldings, and sheet metal for shrouds. |

| • |

|

The motor assembly undergoes winding, insulation, rotor-balancing, and performance testing. |

| • |

|

Fan blades are moulded using precision tooling and tested for aerodynamic balance. |

| • |

|

The motor and blades are integrated into the shroud, followed by dynamic balancing to ensure vibration-free operation. |

| • |

|

Each assembled unit undergoes quality inspection, airflow testing (measured in m3/hr), and electrical safety checks. |

| • |

|

Technical features include: |

| • |

|

Optimized blade pitch for maximum airflow with minimum energy consumption. |

| • |

|

Operating voltage compatibility with commercial buses (typically 24V DC or as per OEM requirement). |

1.6. Intended Use and Target Market of the Product – Condenser Fan

The condenser fan is intended for B2B supply to bus manufacturers. Its application is specific to:

| • |

|

Rooftop bus air-conditioning systems for expelling hot air from the condenser section. |

| • |

|

Engine compartment in certain heavy vehicles |

The target market consists of OEM bus manufacturers, public transport corporations, private fleet operators, and service workshops.

1.7. Physical Characteristics and Packaging of the Product – Condenser Fan

| • |

|

Weight varies between 4 kg to 12 kg, determined by motor size and shroud construction. |

| • |

|

The blades are lightweight yet durable, capable of withstanding prolonged high- speed rotation. |

| • |

|

Packaging is carried out in heavy-duty corrugated cartons with internal foam padding to prevent transit damage. |

| • |

|

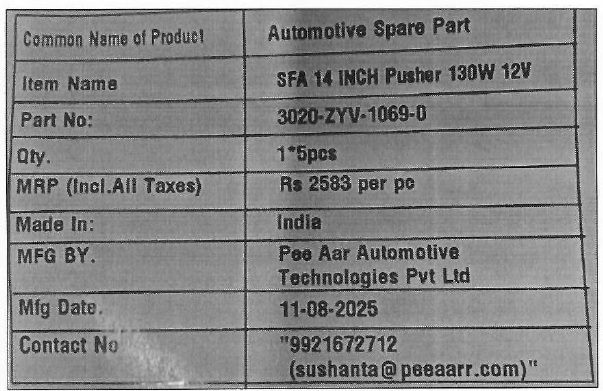

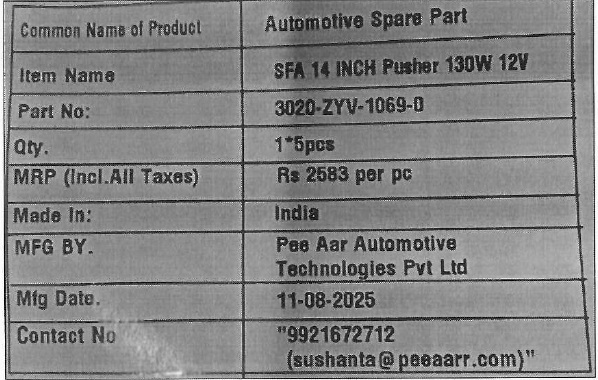

Each carton is labelled with product description, HSN code, quantity, batch number, and manufacturing date, ensuring traceability. |

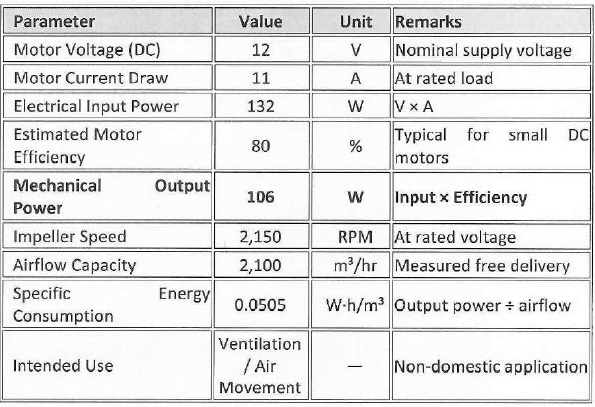

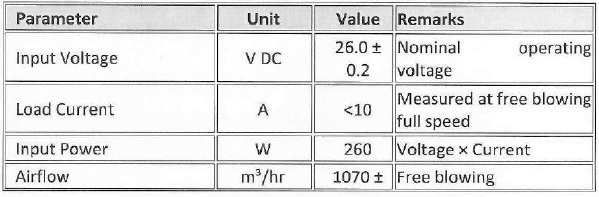

1.8. Performance Chart having Input power, output power, airflow, & specific energy consumption of the Product -Condenser Fan

The low output power per cubic meter indicates industrial fan characteristics, not household appliances.

2. Statement of relevant facts having a bearing on the question(s) raised

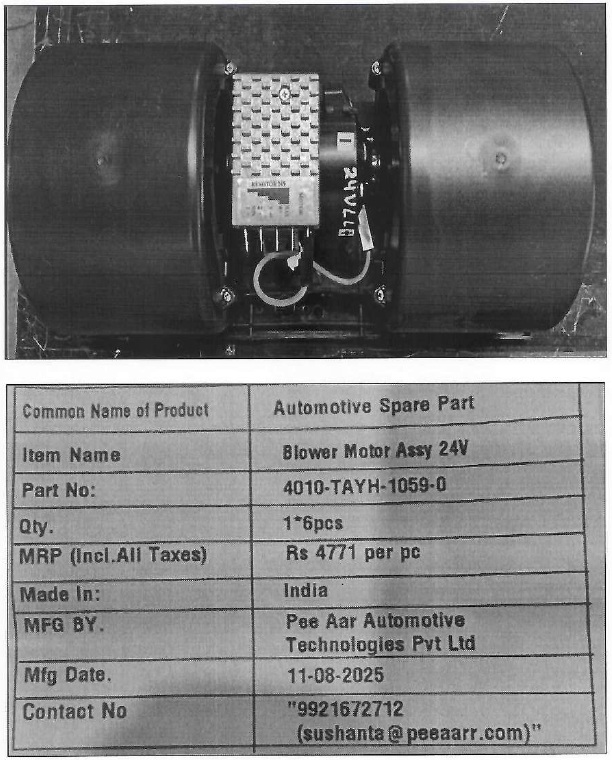

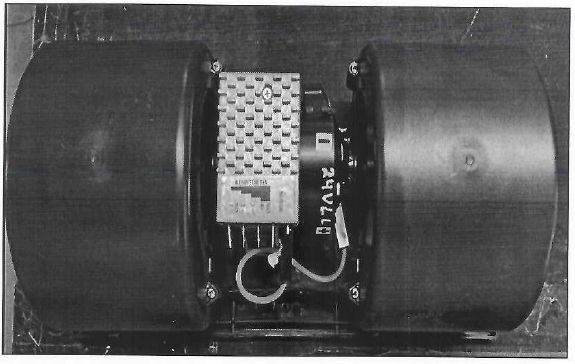

2.1. Description of the Product – Blower

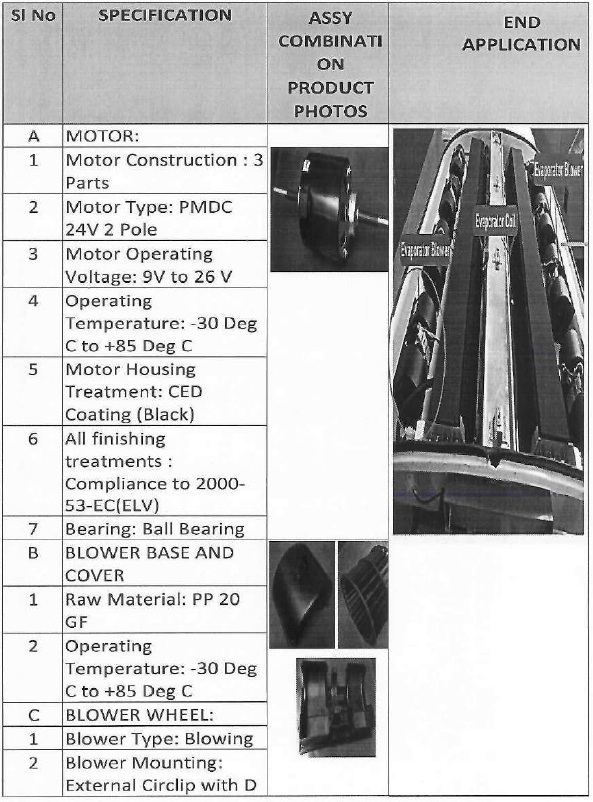

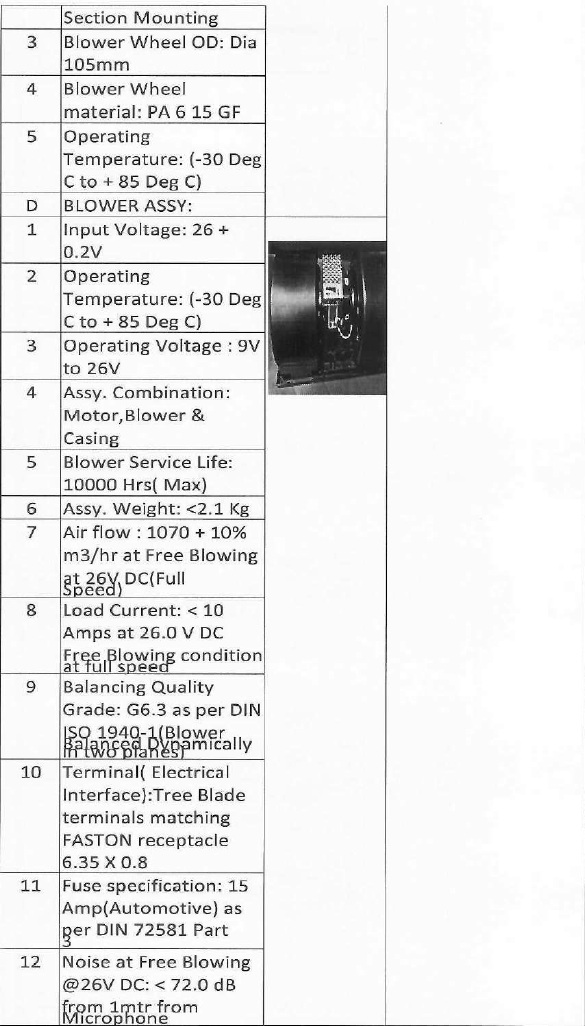

The product is a compact automotive-grade DC blower assembly designed for high airflow applications in demanding environments. It integrates a precision- engineered PMDC (Permanent Magnet Direct Current) motor with a dynamically balanced centrifugal blower wheel enclosed in a high-strength, thermoplastic housing.

The blower operates efficiently across a voltage range of 9V to 26V DC, with optimum performance at 26V DC, delivering a free-blowing airflow of approximately 1070 + 10% m3/hr. It is designed for long service life (up to 10,000 hours) and stable operation under extreme temperature conditions from -30°:: C to +85°C.

2.2. Composition of the Product – Blower

The blower assembly is composed of three primary sections: the motor, the blower wheel, and the housing (base and cover), along with associated electrical and safety components.

The motor is a 24V DC permanent magnet, 2-pole design with ball bearings, housed in a steel casing treated with CED black coating for corrosion resistance, and compliant with Directive 2000/53/EC (ELV).

The blower base and cover are molded from 20% glass-fibre-reinforced polypropylene (PP 20 GF), offering high strength, dimensional stability, and temperature resistance. The centrifugal blower wheel, made from 15% glassfibre-reinforced polyamide (PA6 15 GF), is dynamically balanced to G6.3 grade per DIN ISO 1940-1 for smooth operation.

Electrical connectivity is provided through tree-blade terminals compatible with FASTON 6.35 x 0.8 receptacles, and the assembly incorporates a 15A automotive fuse as per DIN 72581 Part 3 for overcurrent protection.

Fasteners and mounts are made of plated or stainless steel to ensure long-term durability and vibration resistance.

The image of goods viz., Blower is as follows:

The technical specification of the Blower with end application is as follows:

2.3. Manufacturing Process & Technical Features of the Product – Blower

The manufacturing of the blower assembly follows a structured process to ensure high performance, durability, and compliance with stringent automotive standards. Motor production begins with precision armature winding and commutator assembly, followed by rotor balancing and dynamic testing to achieve smooth operation. The motor housing undergoes CED (Cathodic Electro-Deposition) coating for corrosion resistance, after which ball bearings and the housing are assembled.

Plastic component molding is carried out through injection molding of PP 20% glass-fibre-reinforced housing components and PA6 15% glass-fibre-reinforced blower wheels, each subjected to dimensional and strength testing. Blower wheel balancing is performed dynamically in two planes to G6.3 grade as per DIN ISO 1940-1 to minimize vibration. In the final assembly stage, the motor is mounted to the blower wheel using a D-section external circlip, the housing and cover are fitted, and the electrical terminals are integrated.

Rigorous quality control follows, including airflow measurement, noise and vibration assessment, electrical load testing at full speed under free blowing conditions, and confirmation that noise levels remain below 72 dB at a distance of 1 meter. This combination of precision manufacturing and thorough testing ensures reliable performance across the blower’s full operating range of 9V to 26V DC, even under extreme temperatures from -30°C to +85°C.

2.4. Intended Use and Target Market of the Product – Blower

Intended Use

The blower is designed for forced air circulation in automotive and off-highway vehicle HVAC (Heating, Ventilation, and Air Conditioning) systems. It is suitable for applications where consistent airflow, long service life, and robustness in harsh environmental conditions are required

Target Market

The blower assembly is primarily intended for integration into HVAC systems across a wide range of vehicle segments. Its robust design, high airflow capacity, and long service life make it well-suited for automotive OEMs and Tier-1 suppliers involved in producing climate control systems for passenger and commercial vehicles. It is also a preferred choice for bus and coach manufacturers requiring reliable air circulation in large passenger compartments. Beyond on-road applications, the blower serves the needs of off- road and agricultural equipment manufacturers, where equipment operates in harsh environmental conditions and demands consistent ventilation performance. Additionally, specialty vehicle builders, such as those producing ambulances, defense vehicles, and custom transport solutions, benefit from its durability, adaptability, and compliance with stringent automotive standards.

2.5. Performance Chart having Input power, output power, airflow, & specific energy consumption of the Product – Blower

3. Statement containing the applicant’s interpretation of law and/or facts

3.1. Classification Principles under Customs Tariff

3.1.1. Relevance of General Interpretative Rule 3(b)

Under the Customs Tariff Act, 1975, classification of goods is governed by the General Rules for the Interpretation of the Harmonised System (HSN). As per Rule 3(b) of these rules, classification of goods shall be determined by the component or material which imparts the essential character to the product. In the present case, the condenser fan unit is essentially an industrial fan designed to move air. Its defining and sole function is air circulation, and therefore its essential character is that of a fan, not a complete air-conditioning machine.

3.2. Heading 8414 covers :

Entry No. 317B of Schedule III of Notification No.1/2017 dated 28.06.2017 covers the following items:

|

“Air or Vacuum pumps,

air or other gas compressors and fans;

ventilating or recycling hoods incorporating a fan,

whether or not fitted with filters other than bicycle pumps,

other hand pumps and

parts of air or vacuum pumps and

compressors of bicycle pumps.

“ |

Hence, Entry No. 317B of Schedule III of Notification No. 1/2017 dated 28.06.2017 specifically covers “Air or Vacuum pumps, air or other gas compressors and fans; ventilating or recycling hoods incorporating a fan, whether or not fitted with filters and parts thereof.” This clearly brings stand- alone fan units, such as the condenser fan in question, under the purview of HSN Heading 8414.

3.3. Applicability of Section XVI Notes to Parts:

We invite the reference to Notes 2 to 5 of Section XVI of the Customs Tariff Act, 1975, which are as below:

|

Subject to Note 1 to this Section, Note 1 to Chapter 84 and to Note 1 to Chapter 85, parts of machines (not being parts of the articles of heading 8484, 8544, 8545, 8546 or 8547) are to be classified according to the following rules:

(a)_parts which are goods included in any of the headings of Chapter 84 or 85 (other than headings 8409, 8431, 8448, 8466, 8473, 8487, 8503, 8522, 8529, 8538 and 8548) are in all cases to be classified in their respective headings;

(b) other parts, if suitable for use solely or principally with a particular kind of machine, or with a number of machines of the same heading (including a machine of heading 8479 or 8543) are to be classified with the machines of that kind or in heading 8409, 8431, 8448, 8466, 8473, 8503, 8522, 8529 or 8538 as appropriate. However, parts which are equally suitable for use principally with the goods of headings 8517 and 8525 to 8528 are to be classified in heading 8517, and parts which are suitable for use solely or principally with the goods of heading 8524 are to be classified in heading 8529;

(c) all other parts are to be classified in heading 8409, 8431, 8448, 8466, 8473, 8503, 8522, 8529 or 8538 as appropriate or, failing that, in heading 8487 or 8548.

|

Hence, as per Notes 2 to 5 of Section XVI, parts of machines are classified according to certain rules:

| 1. |

|

If the goods themselves are covered under a heading of Chapter 84 or 85, they must be classified under that heading, rather than as a part of another machine. |

| 2. |

|

A condenser fan is a complete article in itself under Heading 8414, and not merely an undefined part, since it performs an independent function of air circulation. |

| 3. |

|

Only in cases where the part does not independently fall under any heading would it be classified alongside the parent machine. This is not the case here. |

3.4. Independent Functionality of the Condenser Fan

The condenser fan unit serves only as a prime air mover in a ventilation or heat rejection system. It does not incorporate any air cooling, heating, or humidity control mechanism. It consists solely of a fan assembly together with an electric motor, functioning independently to move air across a heat exchanger. This independence in function means it cannot be considered as a “part” of an air- conditioning machine for classification under Heading 8415.

3.5. Guidance from HSN Explanatory Notes and ‘Supported Case Law’

The HSN Explanatory Notes clarify that when components of air-conditioning machines are presented separately, they are classified under their own appropriate headings, such as 8414 for fans, regardless of their intended incorporation into a complete unit.

The Supreme Court in CCE v. Carrier Aircon Ltd. upheld this principle, ruling that such parts should be classified based on their individual function, not solely on their end use. Accordingly, the products merit classification under Chapter 8414 59 30.

Furthermore, we submit that the end use of the product cannot be a determining factor. In the case of Indian Aluminium Cables Ltd. v. UOI (SC)/1985 (3) SCC 284, it is held that there are a number of factors which have to be taken into consideration for determining the classification of a product. For the purposes of classification, the relevant factors, inter alia, are statutory fiscal entry, the basic character, function and use of the goods. When a commodity falls within a tariff entry by virtue of the purpose for which it is put to, the end use to which the product is put to, cannot determine the classification of that product.

3.6. Absence of Temperature Control Functionality

It is important to emphasize that the Applicant’s condenser fan does not regulate or control temperature. The fan’s sole purpose is to move air to aid heat exchange in an external system (the bus AC condenser or radiator). Therefore, it does not fall under HSN headings that cover air-conditioning machines, refrigeration equipment, or temperature-regulating devices. Instead, it aligns more closely with HSN codes that cover independent fans or blowers without additional integrated functions.

3.7. Functional and Technical Basis for HSN 8414 Classification

| 1. |

|

Design and Construction: The product consists of a motor, fan blades, mounting frame, and electrical connectors – all characteristic features of industrial axial fans. |

| 2. |

|

Operational Function: It produces directed airflow to assist heat transfer, without modifying the air’s thermal properties by itself. |

| 3. |

|

Market Identification: In trade and technical literature, it is sold and recognized as a “condenser fan” or “axial fan” rather than an “air- conditioner” or “AC machine.” |

| 4. |

|

Precedents in Classification: Customs rulings and WCO guidelines consistently place such standalone fan units in Heading 8414, even if designed for specific applications such as refrigeration or HVAC. |

3.8. Inapplicability of HSN 8415

| (i) |

|

Heading 8415 covers: “Air-conditioning machines, comprising a motor- driven fan and elements for changing the temperature and humidity, including those machines in which the humidity cannot be separately regulated”. |

| (ii) |

|

For classification under 8415, the following conditions must be met: |

| 1. |

|

The product must be a complete machine. |

| 2. |

|

It must have both a motor-driven fan and temperature/humidity changing elements (such as a compressor, evaporator, condenser coil, and control devices). |

| 3. |

|

It must be capable of operating as a self-contained system. |

| (iii) |

|

The condenser fan in question does not meet these requirements because: |

| 1. |

|

It is not a complete air-conditioning unit; it lacks refrigerant circuits, evaporator, compressor, and controls. |

| 2. |

|

It cannot change temperature or humidity on its own. |

| 3. |

|

It functions solely as an air mover within a larger system. As such, it fails the “essential character” requirement for classification under Heading 8415. |

C. QUESTIONS ON WHICH THE ADVANCE RULING IS SOUGHT:

Q-1 Whether the Condenser Fan and Blower manufactured and supplied by the applicant is appropriately classifiable under Heading 8414 of the GST Tariff as industrial fans and blowers, specifically under HSN 8414.59.30, or whether it is classifiable under any other heading?

D. COMMENTS OF THE JURISDICTIONAL OFFICER: –

Comments received from the OFFICE, Assistant Commissioner, CGST Division Behror, Rajasthan vide letter No. GEXCOM/TECH/GST/1636/2021-TECH-CGST-DIV-BHR- COMMRTE-ALWAR/1491 dated 24.09.2025 are as under:

M/s PEE AAR Automotive Technologies Pvt. Ltd. (hereinafter referred to as “the applicant”) having GSTIN: 08AAECP5279P2ZK and its factory address at E-311, E-312, General Zone, Industrial Area, Ghiloth, Alwar, Rajasthan 301706.

2. Applicant has mentioned that he is presently engaged in the manufacture and supply of a Condenser Fan and Blower. This product has exhausting facility and removes the old air and fresh air is brought in from outside and does not have any temperature control. The same involves fans and these fans blow the air out and creates a vacuum in the area and this vacuum is filled by the fresh air. Hence, this allows circulation of air and, hence, is an Air Circulator which is covered under HSN 8414 59 30 which deals with Industrial Fans and blowers.

3. Advance Ruling is being sought in respect of the classification of the said product under the Customs Tariff/HSN between 8414 and 8415 and the applicable GST rate under the CGST Act, 2017.

Comments on the application of applicant are as under: –

| Para 1 No comments are required. |

| 1.1 |

|

to 1.2 No comments are required. |

| 1.3 |

|

Comments are as par para 4.8 below |

| 2 |

|

to 2.3 No comments are required. |

| 2.4 |

|

A condenser fan/ blower being specialized AC parts, are distinctly used under chapter head 8415. It is typically a component used in AC system, refrigeration units or heat pumps to circulate air over the condenser coils for heat dissipation. |

| 2.5 |

|

to 2.6 No comments are required. |

| 3 |

|

to 3.5 No comments are required. |

| 4 |

|

to 4.7 No comments are required. |

| 4.8 |

|

The chapter heading 8415 is also covered apparatus which, although not fitted with a device separately regulating the humidity of the air, change the humidity by condensation. |

| From the GSTR-1 returns of the applicant filed during the F.Y. 2024-25 & 2025-26, the recipients of goods are found to be dealing with Air Conditioning goods. The details are mentioned as below: – |

| GSTIN of the Recipient |

Name of the recipient |

| 08AADCT1573H3Z8 |

TRANS ACNR SOLUTIONS PRIVATE LIMITED |

| 07ADFPC9415R1Z4 |

Kanishka Motor Air-conditioning |

| 08AATFC7021J1Z5 |

COOL AIR |

| 18BQJPP3061L1ZE |

A.C. SOLUTION |

| 27AAAFP0442K1ZE |

PRAKASH REFRIGERATION COMPANY |

| 33AEOFS5126H1ZW |

SARVA AIRCONDITIONERS |

| 33AHIPP2728D1ZK |

RAMESWAR COOL SPARES |

| 37ABEPL6736F1ZK |

PRINCE REFRIGERATION |

| 27AABCS3910P2Z2 |

SUBROS LIMITED |

| 27AAFCV2265E1ZD |

VIRTUOSO OPTOELECTRONICS LIMITED |

| 33CZSPR4416E1Z6 |

PVM POLYMERS |

| 08AAACH0351E1Z5 |

HAVELLS INDIA LIMITED |

| 06AAACP1537C1ZZ |

Pranav Vikas (India) P Ltd |

From the above, it appears that applicant is manufacturing condenser fans and blowers and this product was used independently or jointly in Air Conditioning machine. Further, from the submission of the applicant, it appears that they have condenser fan/ blower with electric motor of an output exceeding 125 W which excludes the said products from classification under chapter heading 84145930. Further, the applicant is paying tax @28% on condenser fan and blower presently.

On the basis of the submissions of the applicant with the application, it appears that the applicant supplies condenser fans and Blower and maximum recipient uses these products in air conditioning machines/ refrigeration etc. They are Air Conditioner, Fridge, off-highway vehicle HVAC (Heating, Ventilation, and Air Conditioning) or motor vehicle cooling system etc.

From the above facts, it appears that condenser fan and blower, attracting HSN 8415 and liable to CGST at 14% SGST at 14% vide Sr no. 119 to Schedule IV of Notification 1/2017-CT(R) dated 28-6-17.

Further, no proceedings relating to the matter of classification of the said product namely condenser fan and blower is pending as on date.

E. PERSONAL HEARING:

In the matter, personal hearing was granted to the applicant on 04.09.2025. Mr. Amit Rustagi (C.A.) and Mr Pankajj Russtagi (MD of the Company) Authorized Representative appeared for personal hearing. They reiterated the submission already made by them.

F. DISCUSSIONS AND FINDINGS

1. We have carefully examined the statement of facts, the application filed by the applicant, the submissions made during the personal hearing, and the comments from the jurisdictional Tax Authority. We also considered the issues involved for which the advance ruling is sought, along with other relevant facts and documents placed on record.

2. The issue raised by M/s. PEE AAR AUTOMOTIVE TECHNOLOGIES PRIVATE LIMITED, E-311, E-312, General Zone, Industrial Area Ghiloth, Shahjahanpur, ALWAR-301706, Rajasthan is fit to pronounce an advance ruling as it falls under the ambit of Section 97(2)(a) of the CGST Act, 2017 given as under :-

“Classification of any goods or services or both”

3. We have noted that the product described as a “Condenser Fan” is designed for use in heavy-duty bus rooftop and engine applications. It consists of an electric motor that drives aerodynamic blades housed in a protective shroud, creating high-volume axial airflow. Its primary function is to force hot air away from the condenser coil or radiator.

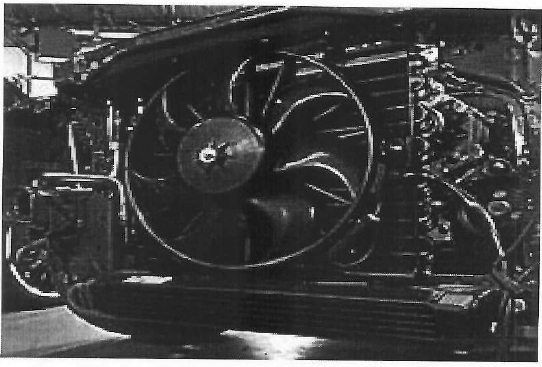

The applicant has claimed that this product is marketed and recognised in trade parlance as an industrial fan/axial fan and not as an air-conditioning machine. The technical specifications provided (24V DC PMDC motor, 305mm fan blade, airflow capacity 2750 + – 10% m3/hr, service life up to 10,000 hours) and but described its end application as B2B supply to bus manufacturers. Its application is specific to (a) Rooftop Bus Air-Conditioning systems for expelling hot air from the condenser section and (b) Engine compartments in certain heavy Vehicles. They have also submitted photograph (Photograph-1) of the end application/use of their product namely “Condenser Fan” manufactured and supplied by them which is as under:

Photograph-1

Photograph-2

We have also gone through the contents available on various website and it has been found that the product “Condenser Fan” is an essential component of a Bus/Truck Air Conditioner Cooling system. This fan plays a crucial role in cooling down the condenser, which is responsible for releasing the heat that is extracted from either Air Conditioner (Photograph-1) or Engine (Photograph-2).

4. Similarly, it is observed that the product described as a “Blower” is a compact automotive-grade DC blower assembly designed for high airflow applications in demanding environments. It delivers a free-blowing airflow and is designed for long service life under extreme temperature conditions.

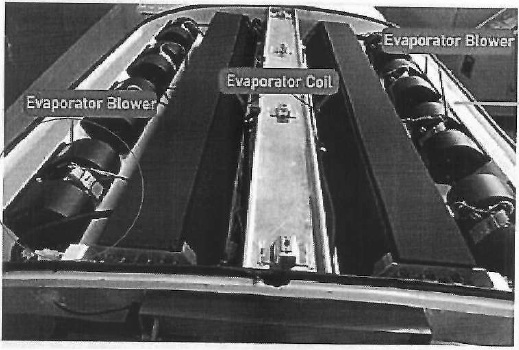

The applicant has claimed that the intended use of this product is for forced air circulation in automotive and off-highway vehicle HVAC systems (Heating, Ventilation, and Air Conditioning). It is integrated into HVAC systems across a wide range of vehicle segments and is supplied mainly to OEMs and Tier-1 suppliers involved in producing climate control systems for passenger and commercial vehicles. They have also submitted photograph (Photograph-3 & 4) of the end application/use of their product namely “Blower” manufactured and supplied by them which is as under:

Photograph-3

Photograph-4

5. Under the Customs Tariff (Chapter 84 and 87), the following headings are relevant;

| HSN 8415 |

– |

Air-conditioning machines, comprising a motor-driven fan and elements for changing the temperature and humidity, including those machines in which the humidity cannot be separately regulated; parts thereof. |

| 8415 10 |

– |

Of a kind designed to be fixed to a window, wall, ceiling or floor, self-contained or “split-system” |

| 8415 10 10 |

– – – |

Window or wall types, self-contained or split-system |

| 8415 10 90 |

– – – |

Other |

| 8415 20 |

– |

Of a kind used for persons in motor vehicles |

| 8415 20 10 |

– – – |

For buses |

| 8415 20 90 |

– – – |

Other |

| 8415 81 |

– – |

Incorporating a refrigerating unit and a valve for reversal of the cooling or heat cycle (“reversible heat pumps”) |

| 8415 81 10 |

– – – |

Sub-types |

| 8415 81 90 |

– – – |

Other |

| 8415 82 |

— |

Incorporating a refrigerating unit but without a valve for reversal of the cooling-heat cycle |

| 8415 82 10 |

– – – |

Split air-conditioners |

| 8415 82 90 |

– – – |

Other |

| 8415 83 |

– |

Not incorporating a refrigerating unit but incorporating elements for changing temperature and humidity |

| 8415 83 10 |

— |

Split air-conditioners |

| 8415 83 90 |

– – – |

Other |

| 8415 90 |

– |

Parts |

6. Note 2 (b) to Section XVI provides that parts which are goods included in any heading of Chapter 84 or 85 are classified in that heading; other parts suitable for use solely or principally with a particular kind of machine are to be classified with that machine.

7. The “Condenser Fan” and “Blower” manufactured and supplied by the applicant, when supplied as a component of or for use with air-conditioning machines such as bus rooftop air-conditioning systems, is classifiable under Heading 8415 90 (Parts of air-conditioning machines). Even the applicant himself has described its application is specific to rooftop bus air-conditioning systems for expelling hot air from the condenser section as well as engine compartment in certain heavy vehicles.

Even they have emphasised that blower is designed for forced air circulation in automotive and off-highway vehicle HVAC (Heating, Ventilation, and Air Conditioning) systems and is primarily intended for integration into HVAC systems across a wide range of vehicle segments which make it well-suited for automotive OEMs and Tier-1 suppliers involved in producing climate control systems for passenger and commercial vehicles.

8. In view of the foregoing facts, circumstances and provisions of the GST law, we pass the following ruling:

RULING

Q-1 Whether the Condenser Fan and Blower manufactured and supplied by the applicant is appropriately classifiable under Heading 8414 of the GST Tariff as industrial fans and blowers, specifically under HSN 8414 59 30, or whether it is classifiable under any other heading?

Ans-1 As discussed in para 7 above.