ORDER

Girish Agrawal, Accountant Member.- These three appeals filed by the assessee are against the orders of National Faceless Appeal Centre (NFAC), Delhi, vide order nos.

| (i) |

|

ITBA/NFAC/S/250/2025-26/1079786277(1), dated 20.08.2025, passed against the assessment order by ACIT, Circle-3, Thane, u/s. 143(3) of the Income-tax Act (hereinafter referred to as the “Act”), dated 29.12.2019, for Assessment Year 2017-18. |

| (ii) |

|

ITBA/NFAC/S/250/2025-26/1079827201(1), dated 21.08.2025, passed against the assessment order by National e-Assessment Centre, Delhi, u/s. 143(3) of the Act, dated 26.04.2021, for Assessment Year 2018-19. |

| (iii) |

|

ITBA/NFAC/S/250/2025-26/1079786406(1), dated 20.08.2025, passed against the assessment order by Assessment Unit, u/s. 143(3) of the Act, dated 03.08.2022, for Assessment Year 2020-21. |

2. Grounds taken by the assessee are reproduced as under:

ITA No. 6609/MUM/2025

“A)That in the facts and circumstances of the case and in the law the ld. Commissioner of Income Tax Appeals has erred in confirming the order u/sec 143 3 of the Act passed by the ld. Assessing Officer who has erred in disallowing the deduction of Rs.91,71,179 claimed by the 1 appellant us.36 1 vir of the Income Tax Act, 1961, on account of Bad Debts Written off during the year, by incorrectly considering the same as Prior Period Expenses by not appreciating the fact that the Bad Debts are allowable as deduction us.36 1 vil of the Act, only in the year of write off of such debts in books of account and not in any other year

B) That in the facts and circumstances of the case and in the law the ld. Commissioner of Income Tax Appeals has erred in confirming the disallowance of deduction of Rs. 91,71,179 claimed by the appellant us. 36 | vii of the Act, on account of Bad Debts written off during the year, by not considering the decision of Hon’ble ITAT, Mumbai Bench in case of ACIT 111 Mumbai v. Ms. Abhyudaya Co op. Bank Limited ITA No. 1128Mum2023 dated 30062023, relied upon by the appellant in the submissions filed before the ld. CIT Appeals which has been mentioned at page 11 and 12 of the ld. CIT Appeals order, wherein the facts are identical and similar to the facts in case of the appellant

C) That in the facts and circumstances of the case and in the law the ld. Commissioner of Income Tax Appeals has erred in confirming the disallowance of deduction of Rs. 91,71,179 claimed by the appellant us. 36 1 vin of the Act, on account of Bad Debts written off during the year, by relying on the decision 3 of Hobble Tribunal in case of JCIT OSD v. Indian Bank Chennai Trib. 20112024, by not considering the fact that the issue in the Indian Banks case was regarding allowability of deduction us. 36 1 via, of the Act. whereas the issue in the case of appellant is regarding deduction us. 36 1 vin of the Act i.e. Bad Debts Written off.”

ITA No. 6610/MUM/2025

(a) That in the facts & circumstances of the case and in the law the ld. Commissioner of Income Tax (Appeals) has erred in confirming the disallowance of deduction of Rs. 1,03,17,024 claimed by the appellant us.36(1)(vii) of the Income Tax Act, 1961, on account of Bad Debts Written off during the year, by incorrectly considering the same as Prior Period Expenses, by not appreciating the fact that the Bad Debts are allowable as deduction us. 36(1)(vit) of the Act, only in the year of write off of such debts in books of account & not in any other year

(b) That in the facts & circumstances of the case and in the law the ld. Commissioner of Income Tax (Appeals) has erred in confirming the disallowance of deduction of Rs. 1,03,17.024 claimed by the appellant us 36(1)(vii) of the Income Tax Act. 1961, on account of Bad Debts Written off during the year, by incorrectly considering the same as Prior Period Expenses, and by not considering the fact that the reasons given by the ld. assessing officer in the order u/sec 143(3) are altogether different than the reasons given in Show Cause Notice (SCN) cum Draft Assessment Order (DAO) regarding proposed disallowance of bad debts written off, which is not in accordance with the procedure regarding issue of SCN and dealing with the reply filed in response to SCN in the scrutiny assessment proceedings.

(c) That in the facts & circumstances of the case and in the law the ld. Commissioner of Income Tax (Appeals) has erred in confirming the disallowance of deduction of Rs 1,03,17,024 claimed by the appellant us. 36(1) (vii) of the Act, on account of Bad Debts written off during the year, by not considering the 3 decision of Hon’ble ITAT, Mumbai Bench in case of ACIT 1(1)(1), Mumbai v. Ms Abhyudaya Co op. Bank Limited (ITA No. 1128Mum2023 dated 30062023), relied upon by the appellant in the submissions tiled before the ld. CIT (Appeals) in appellate proceedings for AY 2017 18, WHARE in the facts are identical & similar to the facts in case of appellant.

(d) That in the facts & circumstances of the case and in the law the ld. Commissioner of Income Tax (Appeals) has erred in confirming the disallowance of deduction of Rs 1.03.17.024 claimed by the appellant us. 36(1)(vn) of the Act, on account of Bad Debts written off during the year by relying on the following decisions Hon’ble Tribunal in case of ICIT (OSD) v Indian Bank (2024) 169 tasmann.com 246 (Chennai Trib) (20112024), by not considering the fact that the issue in the Indian Bank’s case was regarding allowability of deduction us 30(1)(viia), of the Act, whereas the issue in the case of appellant is regarding deduction us. 36(1)(vii) of the Act (i.e., Bad Debts Written off).

2. (a) That in the facts & circumstances of the case and in the law the ld. CII (Appeals) has erred in confirming the addition of interest on Tax Free Bonds amounting to Rs. 4,80,32,803 which is exempt us. 10(15) of the Act as part of taxable income of the appellant, by forming an incorrect opinion that the income assessed in the order passed us. 143(3) is as per income determined under section 143(1) of the Act, by not considering the fact that the said addition of Rs. 4,80,32,803 has been made as an specific addition to the income as per return of income in the order us. 143(3) of the Act, and that the ld. assessing officer has also given reasons for making the sard addition of Rs. 4,80.32,803 in the order passed us. 143(3) of the Act, and therefore, the cause of action (Le. filing of appeal arises from the order passed under section 143(3) of the Act

(b) That on the facts & circumstances of the case and in the law the ld. CIT (Appeals) has erred in confirming the addition of interest on Tax Free Bonds amounting to Rs. 4,80,32,803 which is exempt us. 10(15) of the Act as part of taxable income, by not considering the fact that the said addition of Rs 4,80,32,803, has been made by the ld. assessing officer without following the due procedure i.e. by not issuing any 6 Show Cause Notice (SCN) cum Draft Assessment Order (DAO) regarding proposed addition on account of considering an exempt income as taxable income, considering the fact that as per prescribed procedures the assessing officer has to issue SCN cum DAO stating the variations to income which are prejudicial to the interest of the assessee, by not considering the fact that variation of Rs. 4,80,32,803 to the returned income is a significant and substantial variation

(c) The ld. Commissioner of Income Tax (Appeals) has erred in confirming the addition of Interest on Tax Free Bonds amounting to Rs. 4,80,32,803 (which is exempt usec 10(15) of the Act as part of taxable income of the appellant, without raising any questionquery regarding the same during the course of assessment proceedings, without discussing the same in the bode of the order, by adding the same to the returned income in the computation of total income section, at the end of the order passed usec 143(3) of the Act, by stating ADD Exempt income disallowed by system as per order us 143(1), by giving the reason for addition only in the NOTE below the Computation of Income in the order passed us 143(3) of the Act.

(d)The ld. Commissioner of Income Tax (Appeals) has erred in confirming the addition of Interest on Tax Free Bonds amounting to Rs. 4,80,32,803 (which is exempt usec 10(15) of the Act) as part of taxable income of the appellant, without appreciating the fact that the appellant, while filing the return of income for computing the Gross Total Income in the computation of income statement has simultaneously made an disallowance of Its 60.53,100 as per the provisions of see 14A of the Act, read with Rule 8D of Income Tax Rules, 1962, which pertain to disallowance of expenses pertaining to exempt income

ITA No. 6611 /MUM/2025

1. (a) That in the facts & circumstances of the case and in the law the Learned Commissioner of Income Tax (Appeals) has erred in confirming the order passed u/sec 143(3) r w s 144B of the Act by the Learned Assessment Unit of the Income Tax Department [AU (ITD)] who has erred in completing the assessment by determining the assessed income of the appellant as per the income processed u/s. 143(1) of the Act at .168, 45,76,960/-, by mentioning that the submissions made by the appellant are against the additions made in order u/sec 143(1), but by ignoring the fact that, the additions which have been made in order u/s 143(1), have been retained in order u/s 143(3) and as the Learned AU(ITD) has completed the scrutiny assessment u/sec 143(3) of the Act, and has determined the assessed income as per the income processed u/s. 143(1) of the Act, the doctrine of merger is applicable, therefore the impugned adjustments by CPC merge into order passed u/s. 143(3) of the Act and order passed u/s. 143(3) only survives, as has been held in

| (i) |

|

Hon’ble Calcutta High Court in case of C.E.S.C Ltd v. DCIT (2003) 262 ITR 243 |

| (ii) |

|

Hon’ble ITAT, Mumbai Bench in case of National Stock Exchange of India Limited v. DCIT Circle- 7(1)(1) [TA No. 732/Mum/2023 (A.Y.2020-21)-Date of order 22/09/2023] |

| iii) |

|

Hon’ble ITAT, Delhi Bench, in case of South India Club v. ITO [2024] (Delhi Trib.) (22.05.2024) |

(b) That in the facts & circumstances of the case and in the law the Learned Commissioner of Income Tax (Appeals) has erred in not considering the fact that, the non-acceptance of the rectification application by CPC against intimation u/s 143(1) of the Act, by mentioning.

“Kindly contact AO for further information as ITR has been selected for scrutiny” itself goes on to indicate that the e-filing portal (of which CPC & NFAC are two arms) has merged the two proceedings i.e the order u/s 143(1) of the Act & Scrutiny proceedings u/s 143(2) of the Act.

(c) That in the facts & circumstances of the case and in the law the Learned Commissioner of Income Tax (Appeals) has erred in confirming the order passed u/sec 143(3) r ws 144B of the Act by the Learned AU(ITD) who has erred in completing the assessment u/s. 143(3) rws 144B of the Income Tax Act, 1961 by determining the assessed income of the appellant as per the income processed u/s. 143(1) of the Act at .168, 45,76,960/- by not considering the fact that the return of income processed with demand vide intimation u/s. 143(1)(a) of the Act, issued by CPC on 25th December, 2021, itself has been issued by CPC by not following the due procedure as prescribed in First Proviso to Sec. 143(1) of the Act, thereby rendering the said intimation u/s. 143(1)(a) of the Act, dated 25th December, 2021 as invalid, null & void and consequently the order u/s. 143(3) rws 144B of the Act, passed on 03rd August, 2022 (where in the assessed income has been determined as per income processed u/s. 143(1) of the Act) is also invalid, null & void and accordingly deserves to be cancelled/annulled.

(d) That in the facts & circumstances of the case and in the law the Learned Commissioner of Income Tax (Appeals) has erred in confirming the order passed u/sec 143(3) rws 144B of the Act, where in the assessed income of the appellant has been determined as per the income processed u/s. 143(1) of the Act at .168,45,76,960/- without considering the contents of the submissions made by the appellant during the course of assessment proceedings, in respect of intimation order u/s 143(1) of the Act, dated 25th December, 2021, which has been passed nearly six months after the issue of notice u/s 143(2) of the Act and after the issue of few notices u/s 142(1) of the Act and after the details submitted by the appellant in response to said notices issued u/s 142(1) of the Act.

2) That in the facts & circumstances of the case and in the law the Learned Commissioner of Income Tax (Appeals) has erred in confirming the order passed u/sec 143(3) rws 144B of the Act, which has been passed without following the ‘due procedure’ as prescribed in Sec 144B, of the Income Tax Act, 1961 specifically sub-clause (b) of clause (xii) of Sec 144B, (which is regarding issuing a show cause notice stating the variations to income which are prejudicial to the interest of the assessee) by not considering the fact that variation of 2.5,06,75,550/- is a significant variation, more so where the appellant has filed detailed explanation regarding the said amount of Rs.5,06,75,550/-.

3) (a) That in the facts & circumstances of the case and in the law the Learned Commissioner of Income Tax (Appeals) has erred in confirming the addition of Rs. 1,06,24,519/-, on account of sum received from employees as contribution to provident fund (PF) which the appellant has deposited with the PF Authorities after the due date prescribed under Provident Fund Act or rules, without considering that there was an nominal delay of 02 to 07 days in depositing the said amount and by not considering the fact that the same has been paid into government account before the due date of filing of return of income as specified in Sec. 139(1) of the Act.

(b) That in the facts & circumstances of the case and in the law the Learned Commissioner of Income Tax (Appeals) has erred in confirming the addition of Rs 1,06,24,519/- made by Learned ADIT, CPC, Bangalore while processing the return of Income u/s 143(1) of the Act, without appreciating the fact that the same was not a mistake apparent from record, were pertaining to an debatable issue and such type of additions are not permissible to be made while processing the returns u/s 143(1) of the Act, and that the payment of employees contribution to provident fund before the due date of filing the return of income prescribed u/s 139(1), have been held as an allowable expenditure by various judicial authorities.

4) (a) That in the facts & circumstances of the case and in the law the Learned Commissioner of Income Tax (Appeals) has erred in concurring with and confirming the addition of Rs. 4,00,50,981/-, made by the Learned ADIT, CPC ,Bangalore, being “written off bad debts recovered”, by not considering the fact that the said amount of Rs. 4,00,50,981/- has already been credited to the Profit and Loss Account of the appellant for FY 2019-20, and was included in the net profit before tax for FY 2019-20, which is starting point of computation of income statement and thus was already included in the taxable income of Rs. 163,39,01,458/- as per return filed.

(b) That in the facts & circumstances of the case and in the law the Learned Commissioner of Income Tax (Appeals) by concurring with the action of the Learned ADIT CPC, Bangalore in considering the said amount of Rs. 4,00,50.981/- as income in the intimation order u/s 143(1) of the Act and retaining the said addition in the order u/s 143(3) of the Act, has erred in concurring with taxing the same income more than once, which is not permissible under the Income Tax Act, 1961.

5) That in the facts & circumstances of the case and in the law the Learned Commissioner of Income Tax (Appeals) has erred in confirming the levy of interest u/s 234A of the Act, at Rs. 1,00,082/- by not considering the fact that the return has been filed by the appellant on 21st December, 2020, whereas the due date to file the return of income for AY 2020- 21 was 15th February, 2021.

3. All the three appeals relate to one assessee and there being certain common issues, hence these are taken up together for adjudication by passing this consolidated order. We first take up appeal for AY 2017-18. The only issue raised in this appeal is in respect of disallowance of Rs.91,71,179/- claimed as a deduction by the assessee under section 36(1)(vii) in respect of bad debts which have been treated by the ld. AO as prior period expenses.

3.1. Facts as culled out from records are that assessee is a cooperative society engaged in the business of banking. It filed its return of income on 28.10.2017 reporting total income at Rs.142,37,10,690/-. Assessee had granted loans, which were classified as non-performing assets (NPAs) which were treated as loss assets prior to 01.04.2006 in the books of accounts. Assessee actually wrote off these loans as bad debts in its books in the financial year 2016-17 relevant to AY 2017-18, claiming the same as deduction under section 36(1)(vii). According to the ld. AO, these write-offs are prior period expenses, claimed in the year under consideration which assessee ought to have been written off as soon as they were classified as loss assets, i.e., in the year relevant to period 01.04.2006. Ld. AO referred to RBI Master Circular on Prudential Norms on Income Recognition, Asset Classification and Provisioning pertaining to advances (DBOD No. BP.BC/20/21.04.048/2001-2002) dated 30.08.2001, which prescribes the treatment of loss assets. According to this Circular, ld. AO observed that the entire assets should be written off. If the assets are permitted to remain in the books for any reason, 100% of the outstanding should be provided for.

3.2. Assessee made its detailed submissions in the course of assessment proceedings explaining the provisions of the Act vis-a-vis section 36(1)(viia) and 36(1)(vii). It was submitted that the bad debts pertain to accounts which have been classified as NPAs prior to the year 31.03.2006 and the same were classified as loss assets on or before 31.03.2006. It was also submitted that, up to AY 2006-07, cooperative banks were not entitled to claim deduction under section 36(1)(viia), due to which there was no provision for bad and doubtful debts. Since no provision could have been created by the assessee in this respect, there was no credit balance available in the provision for bad and doubtful debts account in terms of section 36(1)(viia) and thus, applying the computation mechanism for claiming bad debts, the entire amount was claimed as a deduction. However, ld. AO did not accept the submissions made by the assessee and completed the assessment by disallowing the claim so made.

4. In the first appeal, ld. CIT(A) upheld the disallowance so made by the ld. AO for which he observed that assessee carried the loan assets in its books of accounts for a very long period even after these have become NPAs, which the assessee ought to have written off much earlier. According to him, the present write-off in the year under consideration is nothing but an afterthought for making a claim of deduction which should have been claimed in the earlier years. He further noted the absence of documentary evidence from the assessee to demonstrate that deduction of such provision was not claimed in earlier years. According to him, assessee cannot be allowed the claim of the deduction in any year of its choice. Aggrieved, assessee is in appeal before the Tribunal.

5. Ld. Counsel for the assessee reiterated the submissions made before the authorities below. He explained the position of law in terms of provisions of section 36(1)(viia) and 36(1)(vii) for their applicability on the facts of the case. Ld. DR submitted that assessee has not furnished computation to demonstrate the claim of deduction towards such provision in the earlier years and also that the earlier years have not been scrutinized in this regard and therefore, the disallowance so made is justified.

6. We have heard both the parties and perused the material on record. We have also gone through the paper book along with judicial precedents relied upon. At the outset, it is an undisputed fact that the loss assets under consideration were in fact written off in the books of accounts by the assessee during the year under consideration, i.e., AY 2017-18. Section 36(1)(vii) of the Act allows deduction in respect of bad debts written off in the books of accounts in the year of such write-off. It is not necessary for the assessee to establish that the debt has in fact become bad or the exact point of the debt becoming bad for which reference can be made to the decision of Hon’ble Supreme Court in the case of T.R.F. Ltd. v. CIT 323 ITR 397 (SC). We take note of the submissions made by the ld. Counsel of the assessee as to the decision to write off any loans in the books of accounts is based on bank’s policy and the same is governed by multiple factors such as period of classification as NPA, whether all avenues of recovery are exhausted including legal action and execution of decrees, if any, arbitrations and other legal measures, including measures under SARFAESI Act and Debt Recovery Tribunal. According to him, unless all the avenues of recovery are exhausted, the loans are not written off in the books of accounts. Thus, according to him, ld. AO has no jurisdiction to decide at what point of time the loans should be written off which is purely a commercial decision of the assessee Bank.

6.1. We note that prior to 01.04.2006, deduction under section 36(1)(viia) was not available to the cooperative banks. Thus, there was no question of claiming any deduction in respect of provision for bad debts made in the years prior to financial year 2006-07. Even if assessee created provision for bad debts in its books of accounts for accounting purposes, it was liable to be added back for the purpose of computation of total income and was thus, accordingly never claimed by or allowed to the assessee.

6.2. In this regard, assessee placed on record copies of profit and loss account and computation of income for the A.Ys. 2002-03 and 200506 to illustrate that the entire provision for bad debts made by it in its profit and loss account was added back in the computation of income. We also note that reliance placed by the ld. AO on RBI master circular as stated above is misplaced as it is applicable to commercial banks and not to cooperative banks. In respect of cooperative banks, the RBI master circular which governs them is under the circular UCBs (DCBR.BPD.PCB MC No.12/09.14.000/2015-16). From para 5.2.1 of this circular by which cooperative banks are governed, loss asset is defined as extracted below:

“Loss Assets

(a) The entire assets should be written off after obtaining necessary approval from the competent authority and as per the provisions of the Co-operative Societies Act/Rules. If the assets are permitted to remain in the books for any reason, 100 per cent of the outstanding should be provided for

(b) In respect of an asset identified as a loss asset, full provision at 100 per cent should be made if the expected salvage value of the security is negligible.”

6.3. From the above, it is noted that this circular requires obtaining of prior approval from the competent authority before writing off the loans and does not require automatic write off of the asset once it is classified as a loss asset. It requires provisioning in the books of accounts in respect of such asset. The factual position which emanates from the records as noted by us is that prior to 01.04.2006, deduction under section 36(1)(viia) was not available to cooperative banks and therefore, there was no provision for bad and doubtful debt account which was created in the books in terms of section 36(1)(viia) for the loss assets which have been written off in the year under consideration. Accordingly, there cannot be any credit balance in the provision for bad and doubtful debts account in terms of section 36(1)(viia) which is nil in the present case.

6.4. For better understanding, provisions contained in section 36(1)(vii) and 36(2) of the Act are extracted below for ready reference:

“Section 36(1)(vii) of the Act is as under:-

(vii) subject to the provisions of sub-section (2), the amount of any bad debt or part thereof which is written off as irrecoverable in the accounts of the assessee for the previous year.

Provided that in the case of an assessee to which clause (viia) applies’, the ‘amount of the deduction relating to any such debt or part thereof shall be limited to the amount by which such debt or part thereof ‘exceeds the credit balance in the provision for bad and doubtful debts account made under that clause’.”

Relevant clause (v) of Section 36(2) of the Act is as under:-

(2) In making any deduction for a bad debt or part thereof, the following provisions shall apply –

(0)….

(ii)

(iii)

(iv)

(v) where such debt or part of debt relates to advances made by an assessee to which clause (viia) of sub-section (1) applies, no such deduction shall be allowed unless the assessee had debited the amount of such debt or part of debt in that previous year to the provision for bad and doubtful debts account made under that clause”

6.4.1. In respect of the above-mentioned debts which were already NPA (loss assets) as on 31.03.2006, there was no provision to claim deduction u/s. 36(1)(viia) of the Act. For the reason that, the provisions of Section 36 (1)(viia) of the Act, have been made applicable to the Co-op. Banks only with effect from A.Y. 2007-08, and all the borrowers account were already Non Performing Assets as loss assets as on 31.03.2006.

6.4.2. Clause (v) of sub-section (2) of section 36, is applicable only in respect of the advances which have been written off as bad debts to which the provisions of section 36(1) (viia) are applicable.

6.5. We also refer to CBDT Circular 3, dated 12.03.2008 in respect of deduction of any provision for bad and doubtful debts to be allowed in case of cooperative banks under section 36(1)(viia). In para 20.2, it is noted that deduction earlier allowable under section 80P in the case of cooperative society engaged in carrying on the business of banking that is cooperative banks has been withdrawn from assessment year 2007-08, barring in the case of a primary agricultural credit society or a primary cooperative agricultural and rural development bank. In para 20.3, it is noted that since profits of cooperative banks have become taxable after withdrawal of 80P deduction, Finance Act, 2007 has amended section 36(1)(viia) to allow deduction in respect of any provision for bad and doubtful debts to a cooperative bank other than a primary agricultural credit society or a primary cooperative agricultural and rural development bank. In terms of the above, provisions of section 36(1)(viia) are applicable to a cooperative bank only from AY 2007-08 and therefore, any provision towards bad and doubtful debts standing in the account of a cooperative bank prior to 01.04.2006 will not come under the ambit of section 36(1)(viia).

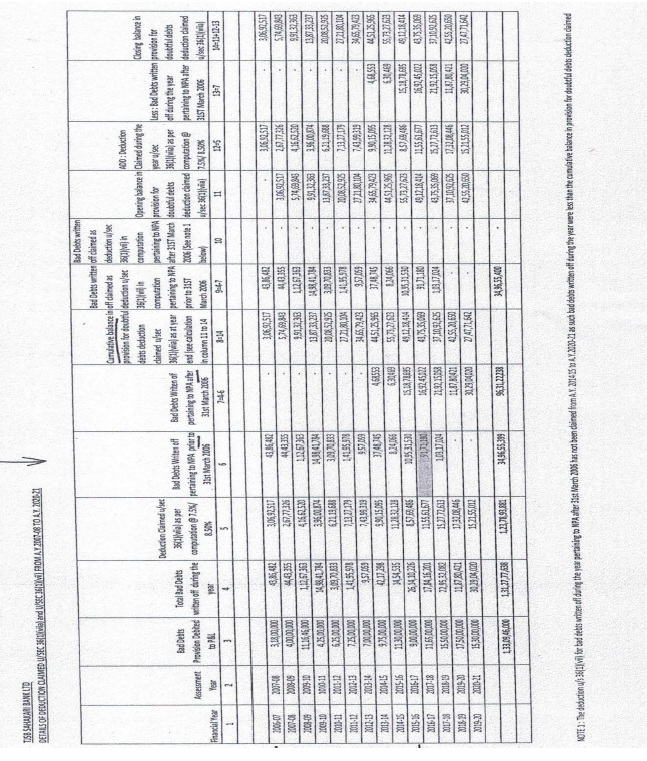

6.6. Assessee has placed on record details of deduction claimed by it under section 36(1)(viia) and under section 36(1)(vii) from AY 2007-08 to AY 2020-21. The same is extracted below for ready reference. From the said tabulation, it was submitted that for assessment year 200708 to 2016-17, claim of the assessee was always allowed to it. It is for the first time in this year under consideration, i.e., AY 2017-18 that such an adverse view has been taken by the Revenue, disallowing the claim of bad debts written off pertaining to NPAs prior to 31.03.2006.

7. In the conspectus of the above factual narration and the position of law, we hold that for the loan assets classified as NPAs prior to 01.04.2006, deduction under section 36(1)(viia) was never available to the assessee and therefore, entire write-off of such assets is eligible for deduction under section 36(1)(vii) in the year of write-off. Before parting, we would refer to the decision of Hon’ble Supreme Court of India in the case of Catholic Syrian Bank Ltd v. CIT(A) 343 ITR 270 (SC), where one of the substantial questions of law before the Hon’ble Court was in this respect. The same is extracted below for ready reference.

“(k) Whether the Full Bench was correct in reversing the findings of the earlier Division Bench that if the bad debt written off relate to debt other than for which the provision is made under clause (viia), such debts will fall squarely within the main part of clause (vii) which is entitled to be deduction and in respect of that part of the debt with reference to which a provision is made under clause (viia), the proviso will operate to limit the deduction to the extent of the difference between that part of debt written off in the previous year and the credit balance in the provision for bad and doubtful debts account made under clause (viia)?”

7.1. While answering this substantial question of law, the Hon’ble Court distinguished between the bad debts written off which relate to debt other than for which the provision is made under section 36(1)(viia). The conclusion drawn by the Hon’ble Court on this substantial question of law is extracted from Para 39 to Para 41 of the said judgment. Hon’ble Court held that the provisions of section 36(1)(vii) and 36(1)(viia) are distinct and independent items of deduction and operate in their respective fields. Bad debts written off in debts other than those for which the provision is made under clause (viia) will be covered under the main part of section 36(1)(vii), while the provision will operate in cases under clause (viia) to limit deduction to the extent of difference between the debt or part thereof written off in the previous year and credit balance in the provision for bad and doubtful debts account made under clause (viia) which is however, subject to satisfaction of requirements contemplated under section 36(2). The aforesaid distinction brought out by the Hon’ble Court is relevant in the present factual matrix of the case which has been elaborately narrated in the above paragraphs and the finding given to allow the claim of the section 36(1)(vii) as the bad debts written offs pertains to advances classified as NPA, prior to 01.04.2006. Grounds raised by the assessee in this regard are allowed.

7.2. In the result, appeal for AY 2017-18 is allowed.

8. We now take up appeal for AY 2018-19. Ground nos. 1, 2, 3 and 4 are identical to the grounds which we have already dealt in appeal for AY 2017-18 (supra), relating to claim of deduction towards writing off of bad debts which relates to period prior to 01.04.2006, under section 36(1)(vii). The variation is only in respect of quantum of deduction which is of Rs.1,03,17,024/-. Above observations and findings in this regard apply mutatis mutandis. Accordingly, ground nos. 1, 2, 3 and 4 are allowed.

9. Ground nos. 5, 6, 7 and 8 are in respect of addition of Rs.4,80,32,803/- made on account of exempt income which had remained to be included in disclosure schedule EI-exempt income in the ITR, while the return of the assessee was processed under section 143(1) for which intimation was issued on 01.08.2020. In this regard, it was submitted before us that assessee had filed an application for rectification of mistake under section 154 before the ld. Assessing Officer, which has been considered and the claim of the assessee has been allowed in the order passed under section 154, accepting the said claim. In view of this factual position, assessee submitted that ground nos. 5, 6, 7 and 8 are rendered infructuous and hence not pressed. Accordingly, these grounds are dismissed as not pressed.

9.1. In the result, appeal of the assessee for AY 2018-19 is allowed.

10. We now take up appeal for AY 2020-21. Assessee filed its return of income on 21.12.2020, reporting total income at Rs.163,39,01,460/-. The said return was processed by CPC, Bengaluru under section 143(1) for which intimation was issued on 25.12.2021, when the impugned assessment proceeding under section 143(3) was in process. The additions made by CPC, Bengaluru as intimated under Section 143(1) are tabulated below:

| Income as per the return of income |

Rs. 163,39,01,460/- |

| Add: Disallowance u/s 36(1)(va) on account of delay in deposit of employee contribution to PF |

Rs. 1,06,24,519/- |

| Add: Addition u/s 41 on account of recovery of loans written off |

Rs. 4,00,50,981/- |

| Total Income determined u/s 143(1) |

Rs. 168,45,76,960/- |

10.1. In the course of impugned assessment proceedings, assessee made its submissions vide letter dated 31.01.2022 placed on record before us, whereby it explained the additions made in the processing of return and submitted that case of the assessee has already been selected for scrutiny under section 143(3) and raising demand subsequently, by an intimation under Section 143(1) is not correct which leads to conducting parallel proceedings for the same assessment year and is therefore ought to be avoided. In the said submission, assessee made out its case for the adjustment made in the intimation under Section 143(1) which relates to disallowance made under section 36(1)(va) on account of delay in deposit of employees’ contribution to provident fund and addition made under section 41 on account of recovery of loans written off.

10.2. Assessee furnished copy of its audited profit and loss account from where it was demonstrated that amount of Rs. 4,00,50,981/- has already been credited as income in respect of amount recovered towards bad debts written off which has been added in the intimation issued under Section 143(1) and therefore, tantamount to taxing the same amount twice. In the same submission, assessee contended that it had moved an application for rectification under section 154 of the Act on 25.12.2021. However, it was pointed out that the same was not acceptable on e-filing portal for which screenshot from the portal is placed on record.

11. We note that impugned assessment order has been passed subsequent to the intimation issued under Section 143(1) and more so, after specifically examining the aspects of disallowance under section 36(1)(va) and under section 41 of the Act by the ld. AO. The said intimation gets merged into the order of assessment passed under section 143(3) and it supersedes the intimation issued under section 143(1). On factual matrix, it is evident from the material placed on record that profit and loss account is credited by the amount recovered by the assessee towards bad debts amounting to Rs. 4,00,50,981/- and has thus been offered to tax. The addition made while processing the return under Section 143(1) is based on disclosure made by the assessee of this information under the head ‘other information’ of the return which has been adequately and corroboratively explained to the ld. AO in the course of impugned assessment.

11.1. In respect of disallowance made under section 36(1)(va) for delayed deposit of employees’ contribution to provident fund, aggregating to Rs.1,06,24,519/-, it is pertinent to note that Hon’ble Supreme Court in the case of Checkmate Services Pvt. Ltd. has held against the assessee, confirming the disallowance for belated payment of employees’ contribution to PF. The addition made is in the processing of return for which intimidation was issued under Section 143(1) by way of automatic adoption of the data reported in the tax audit report which has been again adopted by the ld. AO in the impugned assessment. Corroborative facts have not been verified in this respect. In the given set of facts, for this specific issue relating to disallowance under section 36(1)(va), we find it appropriate to remit the matter back to the file of ld. AO for the limited purpose of verification of the details and documents in this regard and consider the claim of the assessee in accordance with the provisions of the Act and the decision of Hon’ble Supreme Court in the case of Checkmate Services Pvt. Ltd. (supra). Accordingly, considering the overall factual position, ld. AO is directed to verify the records and details and allow the claim of the assessee accordingly.

11.2. In the conspectus of the above narration, we hold that addition made under section 41 on account of recovery of loans written off amounting to Rs. 4,00,50,981/- is deleted and issue relating to disallowance made under section 36(1)(va) on account of delay in deposit of employees’ contribution to PF is remitted back to the file of ld. AO in terms of our above stated observations and directions. Accordingly, grounds raised by the assessee in this regard are partly allowed.

12. In the result, appeal of the assessee is partly allowed for statistical purposes.

13. In the result, appeals of the assessee for AY 2017-18 and 2018-19 are allowed and for AY 2020-21 is partly allowed.