ORDER

Udayan Dasgupta, Judicial Member.- This appeal has been filed by the assessee against the order of the Ld. Commissioner of Income Tax (Appeals)-NFAC dated 28/06/2023, for the Assessment Year 2012-13, which has arisen out of the order of the AO passed u/s 143(3) / 147 of the Act, 1961, dated 29/12/2018.

2. The grounds taken by the assesee in revised form 36, are as follows:

“1. That learned CIT(A) has arbitrarily upheld initiation of reassessment proceedings on the basis of recorded reasons of judicial precedent which did not exist at the time of initiation and thus proceedings are illegal and void ab initio

2. That learned CIT(A) has wrongly upheld invocation of section 50C to sale of leasehold rights in land & building.

3. That the appellant was not allowed sought opportunity of hearing through video conference.

4. That appellant craves leave to add any other ground before the honourable bench.”

3. Brief facts emerging from records are that the original return filed by the assessee u/s 139(1) on 15th September, 2012, disclosing returned income at Rs. 19.52 lakhs (plus LTCG on sale of land Rs. 34.15 lakhs) , was selected under CASS for scrutiny on issues relating to interest expenses connected to exempted income (u/s 14A) and on account of capital gains disclosed in ITR being less than sale of property reported in AIR, and after necessary verification and examination of documentary evidences and submissions filed by the assessee the assessment was eventually completed with additions u/s 36(1)(iii) on account of disallowing interest claim , additions u/s 37(i) disallowing indirect expenses and separate addition on account of machinery scrap.

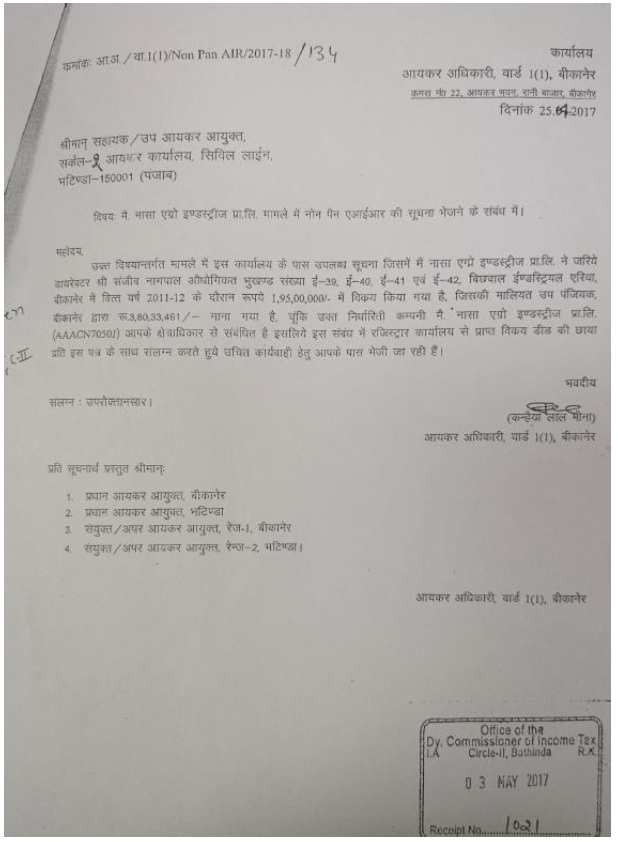

3.1 Thereafter, on the basis of information received by the AO of the assessee (Circle – II, Bhatinda) from the ITO – ward 1(1) Bikaner dated 25th July, 2017, that the stamp duty value of the asset sold by the assessee (being lease hold land and buildings) at Bikaner, during the year (under appeal) has been determined at Rs.3.80 crores, by the sub registrar, Bikaner, against which it was found that the assessee has disclosed an amount of Rs. 1.95 crores as sale proceeds of lease hold asset in ITR, being the deed value, explanation was sought from the assessee vide notice dated 09/05/2017, against which the assessee responded on 31st May, 2017, claiming that since the asset sold was lease hold, the provisions of section 50C was not applicable to lease hold assets transferred.

(The information from ITO, Bikaner is reproduced):

Copy of letter seeking explanation from assessee dated 09/05/2017 reproduced:

3.2 Thereafter, taking into cognizance the reply of the assessee, the case was reopened vide notice u/s 148 dated 08th July, 2017 (after necessary approval from higher authorities) in response to which the assessee filed return on 17/08/2017, copies of recorded reasons obtained and objections duly filed and disposed off, before proceeding with the reassessment.

4. The reasons as recorded for reopening are as under:

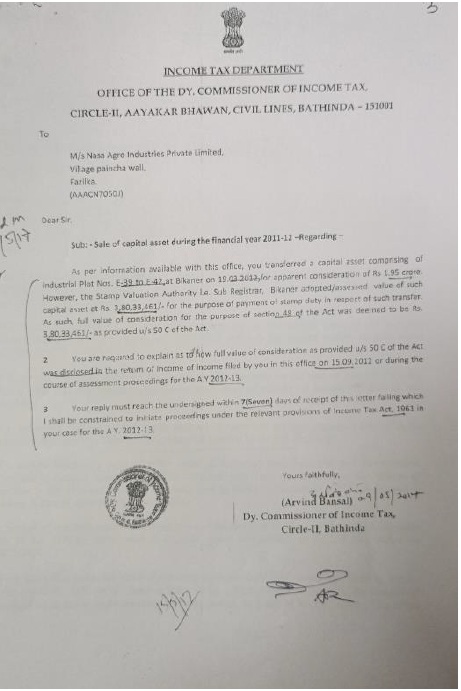

Return of income was filed by the assessee for the A.Y 2012-13 on 15.09.2012, declaring an income of Rs 53,68,282/-. Regular assessment in the case was framed u/s 143(3) on 29.12.2014 at an income of Rs 89,56,690/- As per information available with this office, the assessee transferred a capital asset comprising of industrial Plot Nos. E-39 to E-42 at Bikaner on 19.03.2012 for apparent consideration of Rs 1.95 crore. However, the Stamp Valuation Authority Le. Sub Registrar, Bikaner adopted/assessed value of such capital asset at Rs. 3,80,33,461/- for the purpose of payment of stamp duty in respect of such transfer. As such, full value of consideration for the purpose of section 48 of the Act was deemed to be Rs. 3,80,33,461/-as provided u/s 50 C of the Act. The assessee, vide this office letter dated 09.05.2017 was required to explain as to how full value of consideration as provided u/s 50C of the Act was disclosed in the return of income of income filed by it in this office on 15.09.2012 or during the course of assessment proceedings for the A.Y 2012-13. The assessee, vide reply dated 31.05.2017 has submitted that the land in question was leasehold land and hence provisions of section 50C were not applicable to it.

2 . As per provision of section 50C, where the consideration received or accruing as a result of transfer by assessee of a capital asset is less than the value adopted or assessed or assessable by stamp valuation authority for the purpose of payment of stamp duty in respect of such transfer, the value so adopted or assessed or assessable shall be deemed to be the full value of consideration received or accruing as a result of such transfer. In view of this, deemed full value of consideration in this case u/s 45(1) of the Act read with section 48 of the Act works out to Rs.3,80,33/461/-. The contention of the assessee that the land in question was leasehold land and hence provisions of section 50C were not applicable to it is not acceptable. The ITAT, Lucknow Bench in the case of ITO v. Hari Om Gupta, ITA No 222/LKW/2013 has held that leasehold right of land is a capital asset and provisions of section 50C are applicable on transfer of such leasehold land.

3. In view of the above facts, I have reasons to believe that an amount of Rs. 1,85,33,461/- which was chargeable to tax in the case of the assessee for the assessment year 2012-13 has escaped assessment within the meaning of section 147 of the Act by reason of the failure of the assessee to disclose fully and truly all material facts necessary for its assessment. To assess this income and also any other income chargeable to tax which comes to my notice subsequently in the course of assessment proceedings under this section, a notice u/s 148 is issued for the A.Y. 2012-13.

5. In course of reassessment, queries were raised and replies were considered and various judicial precedents relied upon by the assessee in support of its contention that provisions of section 50C of the Act, is not applicable in the matter of transfer of lease hold lands and buildings, were considered but disallowed after detail observation in page – 7 of the assessment order as follows (relevant portion reproduced)

“The reply of the assessee has been considered but is not applicable. Let us discuss the brief facts of the case. The assessee had purchased through allotment lease hold right of a plot Nos. E-39 to E-42 at Bikaner (Rajasthan) for a period of 99 years for a total consideration of Rs.15,27,775/- in the year 1991. Thereafter assessee started its business operations at the premises and installed m/c and constructed a building on lease hold land. All these assets building, m/c and land were being reflected in the Fixed Assets schedule in the Balance Sheet of the assessee. The assessce had construed building and this shows that substantial rights were transferred to assessee including rights to construct building. The character of the lease hold property is totally changed.

Thereafter the assessee closed its business operation-at-the-said-location-and-continued-operating-at-other-business-premised in the Punjab. The assessee also gave this asset on rent for a rent of Rs.10,53,630/- per annum as per return of income for the A.Y. 2012-13. Thereafter in the year 2012, the assessee sold the Land & Building to M/8 Vision Star Agro Food Private Limited for a total consideration of Rs.1.95 Crore as per registered sale deed. The Stamp Duty value of the above Land & Building was Rs. 3,80,33,461/- as per the stamp value authority which is clearly reflected on the sale deed. Thus it is clear that the assessee has sold land & building though it had acquired lease hold rights in the land only. The assessee while selling the above rights adopted index value of acquisition on the land and on the difference amount of such consideration and booked of acquisition book Capital Gain Taxes. Therefore, section 50C is clearly applicable in the present case.

The judgments quoted by the assessee are mostly applicable in the cases where there is transfer of only lease hold land. In the present case, the assessee had taken the plots on lease in 1991, constructed building on the plots, installed machinery and business was started. Subsequently the business was closed and building and land was given on rent and rent was received in the previous years. Further the assessee sold the land with building-by-entering-into-sale-with M/s Vision Star Agro Foods (P) Ltd. and got it registered with Stamp Valuation Authority of the state. It is also seen from the purchase deed that M/s Nasa Agro Industries (P) ltd. had acquired leasehold rights in the plots vide deed dated 23.02.1991 and it also clearly says that the assessee had full rights to use, sale and transfer the said land (plots). However, on perusal of the sale deed dated 19.03.2012 between M/s Nasa Agro Industries (P) Ltd and M/s Vision Star Agro Foods (P) ltd., it is very much clear that the assessee had sold the land and building to the other party. Thus, it is very much apparent that it is sale of land and Building and not just sale of lease hold rights in land. Thus, provisions of section 50C are applicable in this case. Reliance is placed on the judgement of Hon’ble ITAT, Mumbai in the case of Shavo Norgren (P) Ltd. v. DCIT, Circle- 3(3), Mumbai.

Hence, section 500 is clearly applicable on the said transactions. The assessee has sold the land and building at Rs.1,95,00,000/-whereas the value adopted by the Stamp valuation authority Le Sub-Registrar, Bikaner is Rs.3,80,33,641/-. Therefore, there is difference of Rs.1,85,33,461/-.”

6. Thereafter, the matter carried in first appeal before the Ld. CIT(A) NFAC, has been dismissed by holding that provisions of section 50C of the Act, are applicable on transfer of lease hold land and buildings and the relevant portion of such observation are in para – 4.4 of the appeal order (which is reproduced for ready reference):

“4.4 In the present case, the assessee had taken the plots on lease in 1991, constructed building on the plots, installed machinery and business was started. Subsequently the business was closed and building and land was given on rent and rent was received in the previous years. Further the assessee sold the land with building by entering into sale with M/s. Vision Star Agro Foods (P) Ltd. and got it registered with Stamp Valuation Authority of the state. It is also seen from the purchase deed that M/s. Nasa Agro Industries (P) Ltd., had acquired leasehold rights in the plots vide deed dated 23,02.1991 and it also clearly says that the assessee had full rights to use, sale and transfer the said land (plots). However, on perusal of the sale deed dated 19.03.2012 between M/s. Nasa Agro Industries (P) Ltd and M/s. Vision Star Agro Foods (P) Ltd., it is very much clear that the assessee had sold the land and building to the other party. Thus, it is very much apparent that it is sale of land and building and not just sale of lease hold rights in land. Thus, provisions of section 50C are applicable in this case. During the appellate proceedings the appellant was time and again requested to furnish the document dated 23.02.1991 vide which AO has categorically pointed out that the appellant had ownership in the property so as to sell it. Thus, it is a capital asset attracting provisions of 50C. The AO has rightly placed his reliance on Hon’ble Mumbai ITAT Judgment in the case of Shavo Norgen (P) Ltd. v. DCIT, Mumbai. The addition made by AO is hereby confirmed and appeal by the appellant is dismissed regarding invoked of 50C. The appellant has also objected against the reopening of assessment u/s.147. But I do not see any reason to find the reopening bad. Proper reasons and proper approvals have been taken. Thus the ground of appeal is also not sustainable and hence rejected.”

7. Now the assessee is before the tribunal on the grounds contained in the memo of appeal and has filed additional grounds on 24th July, 2025, which are reproduced:

“1. That the reassessment proceedings u/s 147 were initiated after the expiry of 4 years without pointing out the failure on part of the assessee to disclose necessary facts are barred by limitation.

Since the above ground is purely a legal ground and all the facts are available on record the same may kindly be admitted as additional ground.”

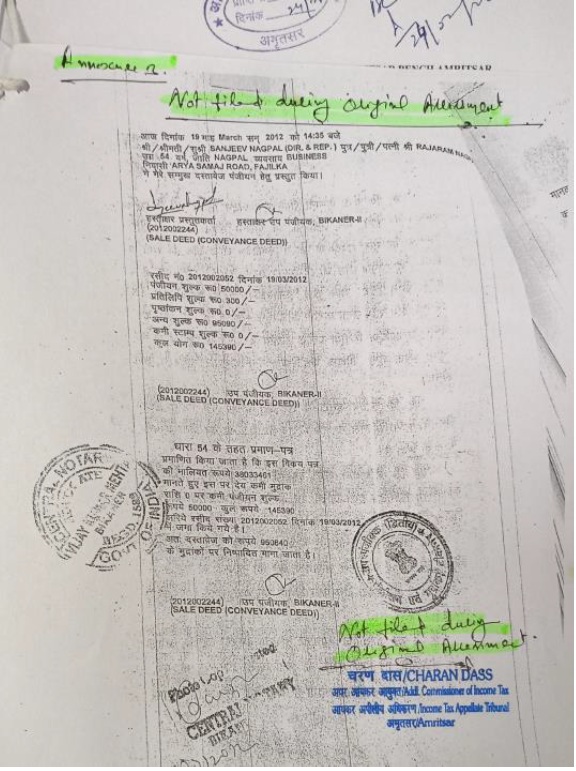

8. In course of hearing before the tribunal, the ld AR of the assessee has filed paper book containing audited financials, copies of sale deed of land and building, copy of valuation report, sale approval letter of Rajasthan State I D I C L, copy of land purchase deed in the year 1991 and other allied documents along with copies of ITAT decisions relied upon by the assessee in support of his contention that provisions of section 50C is not applicable in case of transfer of leasehold rights in land and buildings and the Ld. AR, relied on the following decisions (i) Kancast (P.) Ltd. v. ITO, Ward 9 (3), Pune 68 SOT 110 (Pune – Trib.)/ITA No. 1265/PN/2011 dated 19/01/2015, (ii) ITO v. Pradeep Steel Re-Rolling Mills (P.) Ltd. 155 TTJ 294/[2014] 61 SOT 104 (Mumbai)/ITA No. 341/MUM/2010 dated 15/07/2011, (iii) Shivdeep Tyagi v. ITO 207 ITD 568 (Delhi – Trib.)/ITA No. 484/Del/2024 dated 18/06/2024, (iv) Dy. CIT v. A. R. Sulphonates (P.) Ltd. (Kolkata – Trib.)/ITA No. 570/Kol/2022 dated 22/03/2024, to put forth his case that provisions of section 50C is not applicable on transfer of leasehold rights in land and buildings.

9. However, at the very outset the Ld. DR pointed out that the issue has been recently delt with by the Hon’ble Bombay High court in the case of Vidarbha Veneere Industries Ltd. v. ITO [2026] 484 ITR 132 (Bombay)/ITA No. 34 of 2022, dated 1st April 2025 where the earlier decision of the court in the case of CIT v. Greenfield Hotels & Estates (P.) Ltd. (Bombay)/ (Bombay)/[2016] 389 ITR 68 (Bombay) has been considered and distinguished.

9.1 The relevant portion of the Hon’ble High court decision is reproduced for ready reference:

6. The expression used in Section 50C of the IT Act is ‘consideration KHUNTE 4-ITL34.22.odt received or accruing as a result of transfer of a capital asset, being land or building or both’. This will have to be related to the definition of ‘capital asset’, as occurring in Section 2(14) of the IT Act. A perusal of the definition of ‘Capital Asset’ as contained in Section 2(14) of the IT Act would indicate, that it includes property of any kind, “held by an assessee”. What is material to note is, that the expression is “held by an assessee” and not owned by an assessee. Insofar as the immovable property, i.e. land or building is concerned, there are number of ways, in which it can be held. The holding can be either as an owner, lessee, sub-lessee, allottee, tenant, licensee, gratuitous licensee or any other mode, permissible or recognized by law. The expression “held by an assessee” therefore does not restrict the manner in which the land or building can be held. The holding of land, is merely a method in which rights to the land, can be held or acquired, by a person. That cannot be in any manner equated with land or building, but rather, would be a species of the right to hold it, which as indicated above, are of multiple nature.

7. We, therefore, find that merely because the land was originally allotted by the MIDC by way of a lease to the predecessor of the appellant, who in turn has received the same by way of an assignment, that being one of the modes of transfer, of land or building, the mere use of a particular mode of transfer, cannot create any exception vis-a-vis the holding of the land or building by the Assesee. The word ‘transfer’ as used in Section 50C(1) of the IT Act, also cannot be used in a restricted sense and will have to be given widest amplitude, considering the nature and purpose of the section KHUNTE 4-ITL34.22.odt and thus would include all modes and methods of transfer as are permissible and recognizable in law.

8. Atul Puranik (

supra) relied upon by the learned counsel for the appellant does not consider the effect and import of Section 2(14)(

a) in conjunction with the language used in section 50C of the IT Act, and merely goes on to hold, that since the land is held in a leasehold right, it cannot be equated with land or building, which does not address the issue altogether, neither does it consider the position, that mode of holding of a property, cannot be equated with the property itself, as against which what Section 50C read with Section 2(14) of the IT Act speaks about, is the property. We are therefore, not in agreement with what has been held in Atul Puranik (

supra). In Commissioner of Income Tax v. Greenfield Hotels and Estates Pvt.Ltd.,

(2016) 389 ITR 0068 (Bom) , all that has been said, is that since the Tribunal did not challenge its earlier view, it was binding upon it. As indicated above, Atul Puranik (

supra), does not address the issue at all in light of the language of the statutory provision and therefore cannot be considered as a good law, in view of which, Greenfield Hotels and Estates Pvt. Ltd. (

supra) would also be of no assistance. In view of the above discussion, we do not see any reason to entertain the appeal. The same is therefore dismissed.

10. In absence of any other decisions being brought to our knowledge, we are bound by the Hon’ble High court decision referred to above, where the Hon’ble court has adopted a broader interpretation of the statutory language and has significantly relied on the term ‘held’ in the definition of capital asset to extend the scope of section 50C of the Act to include leasehold rights.

10.1 As such respectfully following the law laid down by the Hon’ble court in Vidarbha Veneer Industries Ltd” (supra), we decide the first two grounds (taken in revised form 36) against the assessee and in favour of the revenue.

11. Now coming to the additional ground taken by the assessee the Ld. AR argued that this being a legal ground goes to the root of the proceedings and the thrust of the argument is that regular return u/s 139(1) has been filed by the assessee and in course of original proceedings the case has been subjected to scrutiny u/s 143(3) where all papers and documents in support of capital gains on sale of land and buildings has been furnished which also included the copy of the registered sale deed dated 19/03/2012, which according to the Ld. AR also contained the deed value of the transaction and also the stamp duty value (circle rates) as determined by the stamp duty officer , and it was not possible for the AO to have overlooked the circle rates quoted therein and the AO has completed the assessment accepting the sale value disclosed by the assessee in the return filed .

11.1 He further submitted that the case is being reopened after four years from the end of the relevant assessment year and there is no failure on the part of the assessee to disclose fully and truly all material facts necessary for its assessment for that assessment year and as such the reopening in the instant case is legally not valid as per the first proviso to section 147, because the same would tantamount to change of opinion based on materials already on record, and in support of his contention he relied on a plethora of judicial pronouncement on the issue.

12. Per contra the Ld. DR objected to the additional grounds now taken by the assessee before the tribunal for the first time challenging the reopening u/s 147, and submitted that this issue was never agitated neither before the AO nor before the Ld. first appellate authority and was not even a part of the grounds of appeal contained in the memorandum of appeal in form 36, and in absence of the same the Ld. first appellate authority never had the opportunity to adjudicate on the issue.

12.1 The Ld. DR further submitted that there is no discussion in the body of the assessment order regarding the availability of the circle rates before the AO and the said amount is neither disclosed in the income tax return nor in the computation of income filed (where the full value of consideration is disclosed at Rs. 1.07 crores being the deed value and not the circle rate), and the circle rate is not even reflected in the copy of the registered sale deed filed before the AO.

12.2 He further submitted that the information has been gathered afresh (post assessment) on 3rd May, 2017 (vide letter of the ITO- Bikaner reproduced in para 3.1 of this order) which points to the difference in deed value and the stamp value of the lease hold assets transferred by the assessee and proceedings were initiated on the basis of this fresh material gathered post assessment and the registered sale deed filed by the assessee before the AO in course of original assessment proceedings u/s 143(3) was incomplete (ambiguous) deed , without any reflection of the stamp duty value adopted by the registration officer and in the instant case there has been a failure on the part of the assessee to disclose fully and truly all material facts necessary for the assessment in as much the full value of the sales consideration has never been disclosed by the assessee, neither in the ITR filed, nor in the computation and not even in the copy of the sale deed furnished (the same being an incomplete deed).

12.3 Without prejudice to the above submission the Ld. DR further referred to the explanation – 1 of section 147 to submit that the registered sale deed from which material evidence could, with due diligence, have been discovered by the AO, will not necessarily amount to disclosure, within the meaning of the proviso of the section.

12.4 As such he prayed for dismissing of this additional ground of appeal taken by the assessee and before concluding, he once again retreated that entire copy of the sale deed reflecting the circle rate was never furnished before the AO in course of original proceedings u/s 143(3) and he sought little time for furnishing copies of assessment records (which was in custody of the AO) and thereafter, has filed extract of the same with remarks, which are reproduced as under (the same being self-explanatory):

13. We have heard the rival counsels and considered the materials placed before us and the paper book on record and we are of the opinion that the assessment records needs to be examined, to ascertain the completeness of the disclosure, especially on the face of such contradictory claims by both parties, and also considering the fact that this legal issue, challenging the proceedings u/s 147, has not been adjudicated by the Ld. first appellate authority in absence of any grounds being taken before him , in the interest of justice we remand the matter back to the Ld. first appellate authority for adjudication on this additional ground after consulting assessment records, (or obtaining report from AO) , as per provisions of law and the assessee is also directed to fully cooperate in appellate proceedings by filing all necessary submission.

14. The assessee will be allowed reasonable opportunity of being heard and notice to be issued in email id in portal and email of the counsel and opportunity of video hearing (as claimed by the assessee) may also be allowed.

15. As such this additional ground taken by the assessee is allowed for statistical purpose.

16. In the result the appeal of the assessee is partly allowed for statistical purpose.