Analysis of Model GST Law of India

Analysis of Model GST Law : General Points

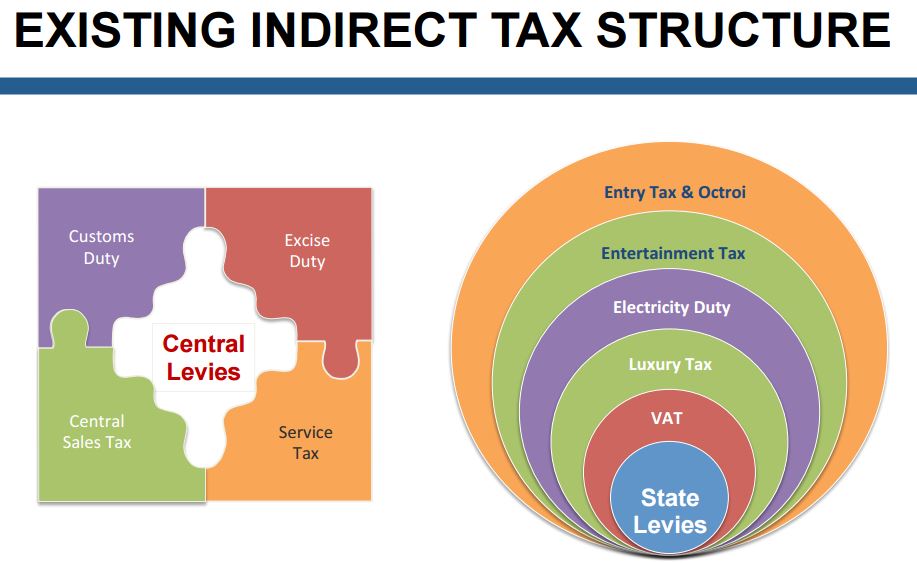

- Need for GST

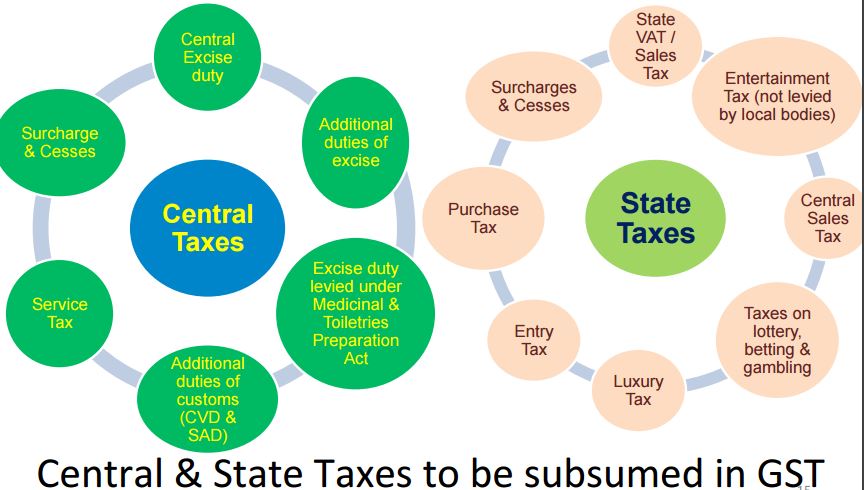

- Taxes Subsumed in GST

- Model GST Law

- Empowered Committee of State Finance Ministers has released the ‘Model Goods and Services (GST) Law’ on 14th June 2016

- The GST would extend to whole of India

- The concepts of ‘sale of goods’ and ‘rendering of services’ , Manufacturing of goods, have been replaced with ‘supply of goods’ and ‘supply of services’ respectively

- Separate Model Acts for the intra-State and inter-State transactions provided

- Registration

- Every person would be required to obtain registration in each State he operates

- A person having multiple business verticals in a State may obtain separate registrations for each verticals in that State

- Taxable person means a person who carries on any business at any place in India and is registered or required to be registered

- Threshold limit prescribed of Rs. 10 lakhs and Rs. 5 lakhs (for North Eastern States and Sikkim). However as per the decision of GST Council , this limit has been raised to Rs 20 Lakh and Rs 10 Lakh respectively.

- Central/ State Government may be regarded as a taxable person in respect of activities engaged as public authorities except otherwise specified

- Taxes

- Central Goods and Services Tax (CGST) and State Goods and Services Tax (SGST) would be levied on all intra-State supplies of goods and services, at a rate to be notified

- Integrated Goods and Services Tax (IGST) shall be levied on inter-State supplies of goods and services at a rate to be notified

- Invoice

- Every person making a taxable supply of goods or services would have to issue tax invoice containing the prescribed particulars

- Adjustment in tax charged in tax invoice can be made by issuing a credit note containing the prescribed particulars and within the prescribed time

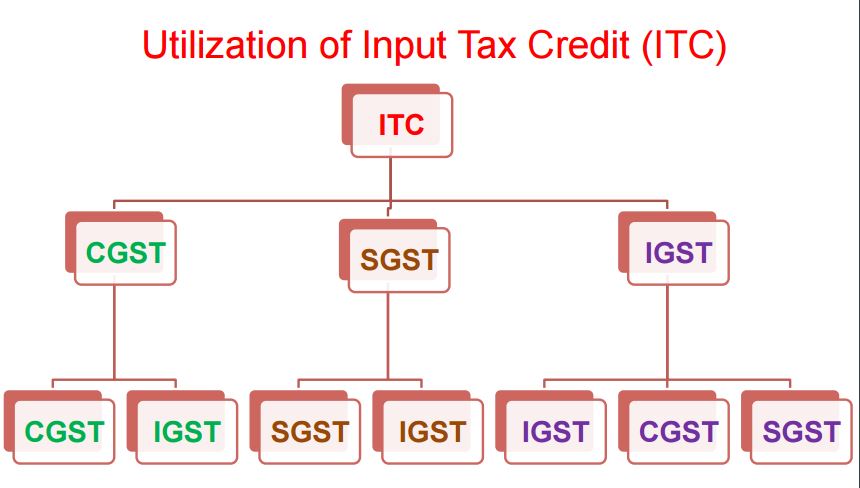

- Input Tax credit

- Electronic Cash Ledger and Electronic Credit Ledger is being introduced where all transactions of an assessee shall be recorded and maintained

- The input tax credit shall be credited in the electronic ledger as self assessed in the return and it may be used for the amount payable i.e. tax, interest, penalty etc

- Input tax credit of CGST shall not be utilised for the payment of SGST and vice versa

- Credit shall be allowed only in respect of the inputs attributable to taxable and zero rated supplies

- Unutilised credit available on account of exports (whereby no export duty is payable) can be claimed as refund

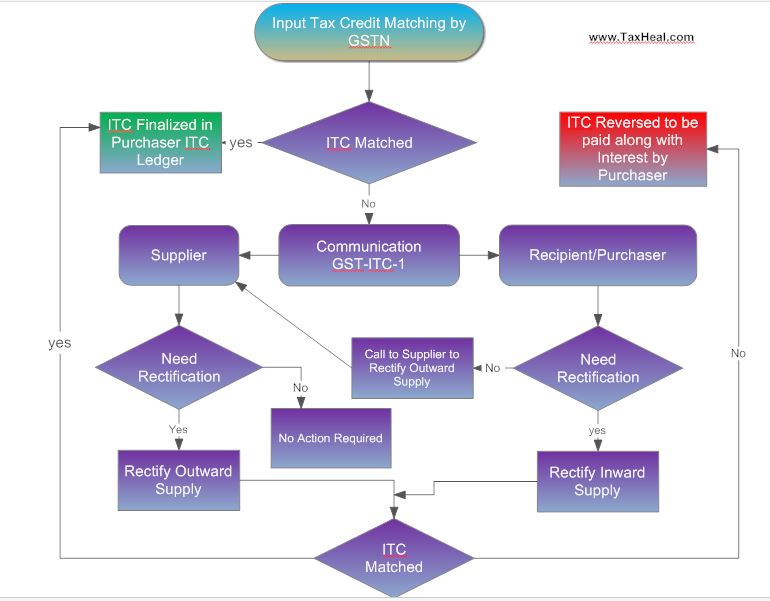

- Input credit Mismatch

- Return : Every taxable person(except certain person) in respect of each registration shall

- furnish details of outward supplies by 10th of the succeeding month;

- furnish details of input supplies by 15th of the succeeding month;

- furnish a return of outward supplies, inward supplies, input tax credit availed, tax payable and tax paid by 20th of the succeeding month

- No return can be filed unless the tax due as per the return has been deposited and consequently, his customers shall not be able to avail credit of the tax charged by him

- No return can be filed unless a valid return for the previous tax period has been filed

- In addition to the above mentioned periodic returns, each taxable person shall be required to file an Annual return as well

-

Read also GST Return filing Process in India

- Composition Scheme

- Composition Scheme available to a registered taxable person involved in intra-State supply of goods and services whose aggregate turnover is less than Rs. 50 lakhs (no availing credit and no recovery from the recipient) for more Read Composition Scheme under GST : Complete Analysis

- Appeal

- A National Goods and Service Tax Appellate Tribunal (Appellate Tribunal) will be established along with its branches (State GST Tribunals) each for every State

Analysis of Model GST Law :Matters to be treated as Supply of Goods or Services

- Any transfer of the title in goods or any transfer of title in goods under an agreement which stipulates that property in goods will pass at a future date upon payment of full consideration as agreed, would qualify as a supply of goods

- Any transfer of goods or of right in goods or of undivided share in goods without the transfer of title thereof, would qualify as a supply of services

- Any lease, tenancy, easement, licence to occupy land would qualify as a supply of services

- Any lease or letting out of the building including a commercial, industrial or residential complex or business or commerce, either wholly or partly, would qualify as a supply of services

- Any treatment or process which is being applied to another person’s goods would qualify as a supply of services

- Where, by or under the direction of a person carrying on a business, goods held or used for the purposes of the business are put to any private use or are used, or made available to any person for use, for any purpose other than a purpose of the business, whether or not for a consideration, the usage or making available of such goods would qualify as a supply of services

Analysis of Model GST Law : Time of Supply

The liability to pay CGST/SCST on GOODS shall arise at the time of supply. for more read Time of Supply under GST- Analysis

Analysis of Model GST Law : Value of Taxable Supply

- Value of taxable supply shall be the transaction value when supplier and recipient are not related and price is sole consideration

- The transaction value shall include the following

- any amount that the supplier is liable to pay in relation to such supply but which has been incurred by the recipient of the supply and not included in the price actually paid or payable for the goods and/or services;

- the value, apportioned as appropriate, of such goods and/or services as are supplied directly or indirectly by the recipient of the supply free of charge or at reduced cost for use in connection with the supply of goods and/or services being valued, to the extent that such value has not been included in the price actually paid or payable

- royalty and technical fees which was not included in the price actually paid or payable

- any taxes, duties, fees and charges levied under any statute other than the SGST Act or the CGST Act or the IGST Act

- incidental expenses such as commission or packaging in respect of supply of goods or service

- subsidies provided in any form or manner, linked to the supply

- any reimbursable expenditure or cost

- any discount or incentive allowed after the supply has been effected (however if such post supply discount was known before the time of supply and specifically linked with invoices, the same shall not be included in the transaction value)

Analysis of Model GST Law : Registration Forms

Following draft registration forms has been provided via draft registration formats for GST

| Sr. No | Form Number | Content |

| 1 | GST REG 01 | Application for Registration under Section 19(1) of Goods and Services Tax Act, 20– |

| 2 | GST REG 02 | Acknowledgement |

| 3 | GST REG 03 | Notice for Seeking Additional Information/ Clarification/ Documents relating to Application for<<Registration/Amendment/Cancellation>> |

| 4 | GST REG 04 | Application for filing clarification/additional information/ document for <<Registration/Amendment/Cancellation/ Revocation of Cancellation>> |

| 5 | GST REG 05 | Order of Rejection of Application for <<Registration /Amendment / Cancellation/ Revocation of Cancellation>> |

| 6 | GST REG 06 | Registration Certificate issued under Section 19(8A) of the Goods and Services Tax Act, 20– |

| 7 | GST REG 07 | Application for Registration as Tax Deductor or Tax Collector at Source under Section 19(1) of the Goods and Service Tax Act, 20– |

| 8 | GST REG 08 | Order of Cancellation of Application for Registration as Tax Deductor or Tax Collector at Source under Section 21 of the Goods and Service Tax Act, 20–. |

| 9 | GST REG 09 | Application for Allotment of Unique ID to UN Bodies/Embassies /any other person under Section 19(6) of the Goods and Service Tax Act, 20–. |

| 10 | GST REG 10 | Application for Registration for Non Resident Taxable Person. |

| 11 | GST REG 11 | Application for Amendment in Particulars subsequent to Registration |

| 12 | GST REG 12 | Order of Amendment of existing Registration |

| 13 | GST REG 13 | Order of Allotment of Temporary Registration/ Suo Moto Registration |

| 14 | GST REG 14 | Application for Cancellation of Registration under Goods and Services Tax Act, 20–. |

| 15 | GST REG 15 | Show Cause Notice for Cancellation of Registration |

| 16 | GST REG 16 | Order for Cancellation of Registration |

| 17 | GST REG 17 | Application for Revocation of Cancelled Registration under Goods and Services Act, 20–. |

| 18 | GST REG 18 | Order for Approval of Application for Revocation of Cancelled Registration |

| 19 | GST REG 19 | Notice for Seeking Clarification/Documents relating to Application for << Revocation of Cancellation>> |

| 20 | GST REG 20 | Application for Enrolment of Existing Taxpayer |

| 21 | GST REG 21 | Provisional Registration Certificate to existing taxpayer |

| 22 | GST REG 22 | Order of cancellation of provisional certificate |

| 23 | GST REG 23 | Intimation of discrepancies in Application for Enrolment of existing taxpayer |

| 24 | GST REG 24 | Application for Cancellation of Registration for the Migrated Taxpayers not liable for registration under Goods and Services Tax Act 20– |

| 25 | GST REG 25 | Application for extension of registration period by Casual / Non-Resident taxable person. |

| 26 | GST REG 26 | Form for Field Visit Report |

Analysis of Model GST Law : GST Return

Sr.No |

Form |

Who to File ? |

What to file? |

When to File ? |

1 |

GSTR-1 |

Registered taxable supplier |

Outward supplies |

10th of the month succeeding the tax period |

2 |

GSTR-2 |

Registered taxable recipient |

Inward supplies /Purchases |

15th of the month succeeding the tax period |

3 |

GSTR-3 |

Registered taxable person |

Monthly Return |

20th of the month succeeding the tax period |

4 |

GSTR-4 |

Composition supplier |

Outward supplies, inward supplies |

18th of the month succeeding the Quarter |

5 |

GSTR-5 |

Non-resident person |

Outward supplies, inward supplies |

20th of the month succeeding tax period & within 7 days after expiry of registration |

6 |

GSTR -6 |

Input service distributor |

details of tax invoices on which credit has been received |

13th of the month succeeding the tax period |

7 |

GSTR-7 |

Tax deductor |

Details of tax deducted |

10th of the month succeeding the month of deduction |

8 |

GSTR-8 |

E commerce operator/tax collector |

Details of tax collected. |

10th of the month succeeding the tax period |

9 |

GSTR-9 |

Registered Taxable Persons |

Annual Return |

31st December of the next Financial Year] |

10 |

GSTR 9A |

Taxable Person paying tax u/s 8 (Compounding Taxable Person) |

Annual Return |

31st December of the next Financial Year] |

11 |

GSTR 9B |

Registered Taxable Person (if Turnover Exceeds 1Crore) |

Audit Report with Reconciliation Statement |

31st December of the next Financial Year |

12 |

GSTR 10 |

Taxable person whose registration has been surrendered or cancelled |

Final return |

within three months of the date of cancellation or date of cancellation order, whichever is later |

13 |

GSTR 11 |

Persons having Unique Identity Number and Claiming Refund |

Details of inward supplies |

28th of the month following the month for which statement is filed |

Analysis of Model GST Law :Transitional Provisions

- Carry forward amount of CENVAT credit/VAT input tax credit in return will be allowed as Input Tax Credit

- Unavailed CENVAT credit in respect of Capital Goods, which were not carried forward in return, would be allowed

- Price revised upwards/downwards on or after the appointed day for transaction in goods and/or services prior to appointed day, issuance of supplementary invoice or debit note is mandatorily required within 30 days of such revision. In case of downward revision, tax liability can be reduced if corresponding input tax credit has been reduced.

- Refund claim of duty/tax and interest filed before appointed day will be sanctioned in accordance with provision of earlier law; if in case rejected, amount shall lapse

- In the proceeding of appeal, revision, review or reference relating to a claim for CENVAT credit found admissible under earlier law shall be refunded in cash not as Input Tax Credit

Analysis of Model GST Law : Tax Return Preparer Form

Sr No |

Form No |

Purpose |

1 |

GST TRP 1 |

Application for Enrolment as Tax Return Preparer under GST |

2 |

GST TRP 1A |

Acknowledgement Receipt |

3 |

GST TRP 2 |

Enrolment Certificate for Tax Return Preparer |

4 |

GST TRP 3 |

Notice for Seeking Additional Information / Clarification / Documents for Application for Registration as Tax Return Preparer,or,Show cause for disqualification in case of misconduct in connection to proceeding by Tax Return Preparer |

5 |

GST TRP 4 |

Order of Rejection of Application for enrolment as Tax Return Preparer/Or Disqualification to function as Tax Return Preparer |

6 |

GST TRP 5 |

List of Tax Return Preparers enrolled |

7 |

GST TRP 6 |

Engagement of TRP |

8 |

GST TRP 7 |

Disengagement from the assignment |

Analysis of Model GST Law : GST Refund Forms

Sl. No |

Form Number |

Content |

1. |

GST RFD 01 |

Refund Application form-Annexure 1 Details of Goods–Annexure 2 Certificate by CA |

2. |

GST RFD 02 |

Acknowledgement |

3. |

GST RFD 03 |

Notice of Deficiency on Application for Refund |

4. |

GST RFD 04 |

Provisional Refund Sanction Order |

5. |

GST RFD 05 |

Refund Sanction/Rejection Order |

6. |

GST RFD 06 |

Order for Complete adjustment of claimed Refund |

7. |

GST RFD 07 |

Show cause notice for reject of refund application |

8. |

GST RFD 08 |

Payment Advice |

9. |

GST RFD 09 |

Order for Interest on delayed refunds |

10. |

GST RFD 10 |

Refund application form for Embassy/International Organizations |

Free Education Guide on Goods & Service Tax (GST)