Non-Diligence in Checking GST Portal: Assessee Directed to Appeal Despite Wrong Tab Upload

Issue: Whether an order passed based on a Show Cause Notice (SCN) uploaded under the ‘additional notices and orders’ tab instead of the ‘notices and orders’ tab on the GST portal, coupled with the assessee’s alleged inability to access the portal and failure to reply to a reminder, warrants setting aside the order or directing the assessee to appeal.

Facts:

- The Department issued an SCN on the GST portal, but it was placed under the ‘additional notices and orders’ tab instead of the standard ‘notices and orders’ tab.

- A reminder notice was subsequently given in the matter, but the assessee failed to file a reply.

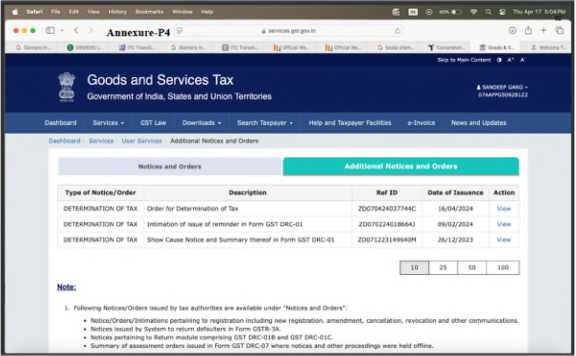

- The assessee contended that their accountant could not access the portal as it was not working at that time, preventing them from filing a reply.

- The Department argued that the assessee had not been diligent in checking the portal.

Decision: The court acknowledged that the assessee had not been diligent in checking the portal and therefore, the Department could not be entirely blamed. However, considering the specific facts and circumstances of the case, the assessee was permitted to file an appeal under Section 107 of the CGST/DGST Act.

Key Takeaways:

- Assessee’s Diligence Expected: While the Department has a duty to ensure proper service, assessees are also expected to be diligent in regularly checking the designated tabs on the GST portal for communications. The court implied that technical issues with the portal should be promptly reported or alternative means of communication explored if access is genuinely hindered.

- Impact of Reminder Notice: The issuance of a reminder notice by the Department weakens the assessee’s argument of complete lack of knowledge, as it indicates a further attempt to communicate.

- Balance of Equities: The court struck a balance by not outright setting aside the order (as in previous cases where no reminder was given or the assessee had no knowledge), but by still providing the assessee with an opportunity to present their case through the appellate mechanism.

- Appellate Remedy as Appropriate Forum: When there are factual disputes (e.g., regarding portal access or diligence) or a need for a detailed review of the case on merits, directing the assessee to the appellate authority is often considered the appropriate course of action.

- Partial Relief: This decision is partly in favor of the assessee as it grants them the opportunity to pursue their case further, rather than dismissing it outright due to their non-diligence.

HIGH COURT OF DELHI

Sandeep Garg

v.

Sales Tax Officer, Avato, Delhi

PRATHIBA M. SINGH and Rajneesh Kumar Gupta, JJ.

W.P.(C) No. 5846 OF 2025

CM APPLs. No. 26721 and 26722 OF 2025

CM APPLs. No. 26721 and 26722 OF 2025

MAY 5, 2025

Rajeev Aggarwal and Shubham Goel, Advs. for the Petitioner. Ms. Vaishali Gupta, Panel Counsel (Civil) for the Respondent.

ORDER

Prathiba M. Singh, J.- This hearing has been done through hybrid mode.

2. The present petition has been filed by the Petitioner- Sandeep Garg, Proprietor, M/s Aares Spring Industries under Article 226 and 227 of the Constitution of India, inter alia, assailing the impugned order dated 16th April, 2024 passed by the Respondent on the ground that the same has been passed without hearing the Petitioner and even the Show Cause Notice dated 26th December 2023 has not been served to the Petitioner.

3. The Petitioner is a proprietorship firm having its principal place of business at B-32/1, Wazirpur Industrial Area, Delhi, New Delhi-110058 and registered vide GSTIN 07AAFPG5092B1Z2. The Petitioner is engaged in the business of Trading and manufacturing of plastic components, nut bolts etc.

4. The case of the Petitioner is that the Show Cause Notice was issued by the Respondent in the ‘additional notices and orders’ tab instead of the ‘notices and orders’ tab and thus is not a proper mode of service.

5. This Court notices that the Show Cause Notice is dated 26th December 2023 and the change in the portal was on 16th January, 2024, however, Ms. Gupta points out that a reminder notice dated 9th February 2024 was given in this matter which is evident from Annexure P-4 which is a screenshot of the portal. The said screenshot is set out below:

6. A perusal of the above set out screenshot shows that the reminder notice was clearly visible on 09th February, 2024, even then no reply has been filed by the Petitioner.

7. Ld. Counsel for the Petitioner submits that the accountant of the Petitioner was not accessing the portal as it was not working at that time and, therefore, the reply could not be filed.

8. The total demand in this case is to the tune of Rs. 9,21,326/ and the tax amount due is to the tune of Rs. 4,52,956/-.

9. Ld. Counsel for the Respondent also submits that automated e-mails and SMSs are also sent whenever anything is uploaded on the portal.

10. Since the Petitioner has not been diligent in checking the portal, no reply to the Show Cause Notice has been filed by the Petitioner. Thus the department cannot be blamed.

11. However, in the facts and circumstances of this case, the Petitioner is permitted to file an appeal against the impugned order before the Appellate Authority under Section 107 of the Central Goods and Service Tax Act, 2017 along with the pre-deposit on the tax amount in terms of the said provision.

12. If the said appeal is filed within the 30 days, it shall be adjudicated on the merits and not be dismissed on the ground of limitation.

13. Accordingly, the present writ petition is disposed ofin above terms. All the pending applications, if any, are also disposed of.