proceedings

A. SUBMISSION OF THE APPLICANT (in brief):-

Brief facts of the case:

| 1. |

|

The applicant Arti Pitaliya (M/s. Shree Rubber & Polymers) (hereinafter referred to as ‘Applicant’) has sought an Advance Ruling on the Entry No. 195B of Schedule Il of notification no 01/2017 dated 28.06.2017 as inserted vide notification no 06/2018 dated 25.01.2018 i.e. classification of rubber ring specifically and only used in sprinkler irrigation system or drip irrigation system. |

| 2. |

|

The applicant seeks advance ruling over the coverage of various items used in the sprinklers and drip irrigation systems sold individually as well as part of a complete system. |

| 3. |

|

The applicant is engaged in manufacturing and trading of various plastic and metallic items which are used in agricultural irrigation. These items are rubber rings etc. All these items are used as part of sprinkler or Drip irrigation system depending upon the requirement of each farmer. These items are supplied as part of a complete sprinkler or drip irrigation system and also as spares separately as and when required by farmer for replacement. |

| 4. |

|

All above items are used by the farmers and most of the items do not have an independent use. They are used only as part of Sprinkler or Drip irrigation system for the purpose of irrigation. |

Statement of relevant facts having a bearing on the question(s) raised

| 1. |

|

That the applicant is engaged in the business of manufacturing/trading of rubber parts of sprinkler system and drip irrigation system used in agricultural irrigation. The parts comprise of Rubber Ring etc which are exclusively made for use and to fit only in various types of Sprinkler/drip irrigation system and have no other use. |

| 2. |

|

That it seeks advance ruling on whether based on rules of interpretation of HB codes, the items made of vulcanized rubber like Rubber Ring falling under the heading 4016 are taxable as specific rubber items having a GST rate of 18 per cent or an components of sprinkler/Drip irrigation system having a tax rate of 5 per cent under heading 84249000. |

| 3. |

|

That the applicant seeks advance ruling over the coverage of various items used in the sprinklers and drip irrigation systems sold individually as well as part of a complete system. |

| 4. |

|

That the rubber rings etc. are used as part of sprinkler or Drip irrigation system depending upon the requirement of each farmer. These items are supplied as part of a complete sprinkler or drip irrigation system and also as spares separately as and when required by farmer for replacement. |

| 5. |

|

That the parts comprise of Rubber Ring which are exclusively made for use and to fit only in various types of Sprinkler/drip irrigation system and have no other use. These parts are designed and shaped that these can be used only in sprinkler/drip irrigation equipment. |

| 6. |

|

That the Rubber Ring are made of Vulcanized Rubber and have no other use. These parts are designed and shaped that these can be used only in sprinkler/drip irrigation equipment. |

| 7. |

|

That all above items are used by the farmers and most of the items do not have an independent use. They are used only as part of Sprinkler or Drip irrigation system for the purpose of irrigation. |

| 8. |

|

That the manufactured goods are sold to entities manufacturing sprinklers systems, sprinkler parts, Traders and consumers using sprinkler system as a part to be used in their sprinkler/ drip irrigation system. |

| 9. |

|

That PRESS RELEASE on GST Rate on goods as recommended by the GST Council in its 37th Meeting held on 20.09.2019 stated that-all “mechanical sprayers” falling under HS Code 8424 would attract 12% GST. |

| 10. |

|

That Entry No. 195B of Schedule II of Notification no. 01/2017 dated 28.06.2017 as inserted vide notification no.: 06/2018 dated 25.01.2018 covers vide Chapter/Heading/Sub-Heading/Tariff item 8424 (Sprinklers; drip irrigation system including Laterals) having overall GST @ 12%. |

| 11. |

|

That Circular number 81/55/2018-GST dated 31st December, 2018 has been issued as a clarification regarding GST tax rate for Sprinkler and Drip irrigation system including laterals and vide sr. no. 4 of the circular it has been stated: “Therefore, the term “Sprinkler”, in the said entry 195B, covers sprinkler irrigation system. Accordingly, sprinkler system consisting of nozzles, lateral and other components would attract 12% GST rate. |

| 12. |

|

That in circular no. 81 has been stated that lateral and other components would attract 12% GST rate. The HS Code 84249000 covers parts in the ambit of tariff item 8424. |

| 13. |

|

That thereafter, Circular No. 155/11/2021-GST dated 17.06.2021 clarified regarding GST rate on laterals/ parts of Sprinklers or Drip Irrigation System. |

| 14. |

|

That it is clarified that intention of the Entry 195B of Schedule Il of Notification no. 01/2017 dated 28.06.2017 as inserted vide notification no. : 06/2018 dated 25.01.2018 covers vide Chapter/Heading/Sub-Heading/Tariff item 8424 (Sprinklers; drip irrigation system including Laterals) has been to cover laterals (pipes to be used solely with sprinklers/drip irrigation system) and such parts that are suitable for use solely or principally with ‘ sprinklers or drip irrigation system’, as classifiable under heading 8424 as per Note 2(b) to Section XVI to the HSN. Hence, laterals/ parts to be used solely or principally with sprinklers or drip irrigation system, which are classifiable under heading 8424, would attract a GST of 12%, even if supplied separately. |

| 15. |

|

That as per 56th council meeting, GST rate of HSN 8424 i.e. Sprinklers; drip irrigation system including laterals; mechanical sprayers has been reduced from 12% to 5% with effect from 22.09.2025 |

| 16. |

|

Hence, product manufactured/traded by applicant should be chargeable at 5% GST rate. |

B. INTERPRETATION AND UNDERSTANDING OF APPLICANT ON QUESTION RAISED (IN BRIEF)

| 1. |

|

That it is submitted that these items fall under Chapter 84 of the Customs Tariff Act, 1975 under heading 8424 which reads as follows :- |

MECHANICAL APPLIANCES (WHETHER OR NOT HAND OPERATED) FOR PROJECTING, DISPERSING OR SPRAYING LIQUIDS OR POWDERS; FIRE EXTINGUISHERS, WHETHER OR NOT CHARGED; SPRAY GUNS AND SIMILAR APPLIANCES; STEAM OR SAND BLASTING MACHINES AND SIMILAR JET PROJECTING MACHINES.

| 2. |

|

That these items are used in the process of irrigation by primarily serving as seals to prevent leaks between pipes, fittings, and internal components like backflow preventers. They create a watertight seal by filling the space between two surfaces, and are crucial for maintaining water pressure and protecting the system from contaminants and external elements. which water is dispersed or sprayed on to the plants. |

| 3. |

|

That for heading 8424 there are 3 entries of taxation in notification no. 01/2017-Central Tax (Rate) dated 28.06.2017, as amended from time to time; all of them are given below:- |

| S.No. |

Chapter/Heading/Sub-heading/Tariff item |

Description of Goods |

CGST rate |

| (1) |

(2) |

(3) |

(4) |

| 195A* |

8424 |

Nozzles for drip irrigation equipment or nozzles for |

6% |

| 195B ** |

8424 |

Sprinklers; drip irrigation system including laterals; mechanical sprayers”; |

6% |

Schedulell-6%

* Inserted by Noti. No. 27/2017 Central Tax (Rate), dated 22.09.2017.

**- Inserted by Noti. No. 06/2018 Central Tax (Rate), dated 25-01-2018.

Schedule III-9%

| S.No. |

Chapter/Heading/Sub-heading/Tariff item |

Description of Goods |

CGST rate |

| (1) |

(2) |

(3) |

(4) |

| 195A* |

8424 |

Nozzles for drip irrigation equipment or nozzles for |

6% |

| 195B ** |

8424 |

Sprinklers; drip irrigation system including laterals; mechanical sprayers”; |

6% |

*** Amended vide notification no 27/2017 Central Tax (Rate) dated 22.09.2017 and 06/2018 Central Tax (Rate) dated 25-01-2018

| 1. |

|

That till 22.09.2017 all the items listed under tariff heading 8424 were taxable @18% (9% CGST + 9% SGST) vide entry no 345 of schedule III of notification no 01/2017. |

| 2. |

|

That vide notification no 27/2017 dated 22.09.2017 nozzles of the sprinklers and the drip irrigation system were carved out of this entry no 345 of schedule III of Notification no 01/2017and were put into Schedule Il as entry no 195A to be taxed @ 12% after representations were made from various sections of the industry being an agricultural input. |

| 3. |

|

That later vide notification no. 06/2018 dated 25.01.2018 a new entry was introduced as entry no 195B “Sprinklers; drip irrigation system including laterals; mechanical sprayers”. This entry included all the lateral parts of these irrigation systems into Schedule Il also, in addition to the Nozzles. |

| 4. |

|

That the word lateral is not defined in the law. However its dictionary meaning is “A side part of something” or “Of, relating to, or situated at or on the side”. |

| 5. |

|

That in the instant case laterals in relation to irrigation system mean all such devices and equipment which help in the working of the system and without which it may not work. Therefore, the product of the applicant are laterals to the sprinkler and drip irrigation. |

| 6. |

|

That it is further submitted that, sprinkler and drip irrigation are 2 a different system designed for distinct uses. Sprinkler is in itself complete system designed for irrigation by use of water pumping. It has not been defined in the law. Dictionary/internet definitions are as follows:- |

“An Irrigation sprinkler is a device used to irrigate agricultural crops, lawns, landscapes, golf courses, and other areas. They are also used for cooling and for the control of airborne dust. Sprinkler irrigation is a method of applying irrigation water which is similar to natural rainfall. Water is distributed through a system of pipes usually by pumping”

| 7. |

|

That sprinkler include firing Nozzle, pipes, clamps, foot buttons, rubber ring and different other items through which the system works. |

| 8. |

|

That drip Irrigation is also not defined in the law. However its definition as per various sources is as follows:- |

“Drip irrigation, which is also sometimes referred to as micro-irrigation or trickle irrigation, consists of a network of pipes, tubing valves, and emitters. Drip irrigation is defined as any watering system that delivers a slow moving supply of water at a gradual rate directly to the soil”

| 9. |

|

That Drip irrigation system also includes nozzles, pipes, clamps, elbow, tee etc. to form a complete system and work. |

| 10. |

|

That it is submitted that the items supplied are necessarily part of the sprinkler and drip irrigation system and are helping in overall functioning of the system. It is submitted that they are not to be used independently anywhere and further they are part of the system without which whole system may not work. Thus they are laterals. |

| 11. |

|

That Circular No. 155/11/2021-GST dated 17.06.2021 clarified regarding GST rate on laterals/ parts of Sprinkler s or Drip Irrigation System. |

| 12. |

|

That it is clarified that intention of the Entry 195B of Schedule II of Notification no. 01/2017 dated 28.06.2017 as inserted vide notification no. : 06/2018 dated 25.01.2018 covers vide Chapter/ Heading/ Sub-Heading/Tariff item 8424 (Sprinklers; drip irrigation system including Laterals) has been to cover laterals (pipes to be used solely with sprinklers/drip irrigation system) and such parts that are suitable for use solely or principally with ‘ sprinklers or drip irrigation system’, as classifiable under heading 8424 as per Note 2(b) to Section XVI to the HSN. Hence, laterals/ parts to be used solely or principally with sprinklers or drip irrigation system, which are classifiable under heading 8424, would attract a GST of 12%, even if supplied separately. |

| 13. |

|

That later vide notification no. 06/2018 dated 25.01.2018 a new entry was introduced as entry no 195B “Sprinklers; drip irrigation system including laterals; mechanical sprayers” which included all the lateral parts of these irrigation systems into Schedule Il also . |

| 14. |

|

That on perusal of above entry it is clear that laterals related to both sprinklers and drip irrigation systems have been covered under the amended entry. |

| 15. |

|

That a clarification regarding Entry No. 195B of Schedule II of Notification No. 1/2017-Central Tax (Rate), dated 28-62017 was issued vide Circular No. 81/55/2018-GST, dated 31-12-2018. The said Circular reads as: |

Therefore, the term ‘sprinklers’, in the said Entry 195B, covers sprinkler irrigation system. Accordingly, sprinkler system consisting of nozzels, lateral and other components would attract 12 per cent GST rate.

| 16. |

|

That at this juncture, it is also important to refer to Rules of Interpretation appended to Customs Tariff Act, 1975, wherein Rule 1 provides that classification of excisable goods is to be determined according to the terms of the heading and in terms of section / chapter notes. Therefore, Rule 1 itself infers the importance of Section / chapter notes in order to arrive at classification of any goods. |

| 17. |

|

That Section or Chapter notes appended to the HSN classification under First Schedule to Customs Tariff Act, 1975 have strong persuasive value. Therefore, from the analysis made herein above, the Section Notes have a vital role to play in order to decide the classification of rubber ring used only for sprinklers. |

| 18. |

|

That Rule 2(a) provides that: Any reference in a heading to an article shall be taken to include a reference to that article incomplete or unfinished, provided that, as presented, the incomplete or unfinished articles has the essential character of the complete or finished article. It shall also be taken to include a reference to that article complete or finished (or falling to be classified as complete or finished by virtue of this rule), presented unassembled or disassembled. |

| 19. |

|

That from the perusal of the above said rule, it is clear that, if goods are in unfinished form but have the essential character of goods of particular heading then such goods will be classified in that heading only. |

| 20. |

|

That further, Rule 3(a) provides as under: The heading which provides the most specific description shall be preferred to headings providing a more general description. However, when two or more headings each refer to part only of the materials or substances contained in mixed or composite goods or to part only of the items in a set put up for retail sale, those headings are to be regarded as equally specific in relation to those goods, even if one of them gives a more complete or precise description of the goods. |

| 21. |

|

That from the perusal of the above said rule, it can be inferred that more specific description will always prevail over the general description. |

| 22. |

|

That while going through Entry No. 195B of Schedule II of Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017 read with Circular No. 81/55/2018-GST, dated 31-12-2018, and Circular No. 155/11/2021-GST dated 17.06.2021 and after applying rules of interpretations, it is submitted that the Sprinkler Irrigation System including laterals only will be covered under the said Notification and attract GST at the rate of 12 per cent. |

| 23. |

|

That as per 56th council meeting, GST rate of HSN 8424 i.e. Sprinklers; drip irrigation system including laterals; mechanical sprayers has been reduced from 12% to 5% with effect from 22.09.2025 |

| 24. |

|

Hence, product manufactured/traded by applicant should be chargeable at 5% GST rate. |

Additional Submission-

| 1. |

|

Issue for Determination |

The Applicant manufactures rubber rings which are designed and engineered to be used only as sealing / connecting parts in sprinkler and drip irrigation systems: The issue is whether such rubber rings, when supplied as spares/parts (even separately), are classifiable as parts suitable for use solely or principally with sprinklers/drip irrigation system under Heading 8424 (Tariff item 84249000), or whether they should be treated as ‘other articles of vulcanized rubber’ under Heading 4016.

| 2. |

|

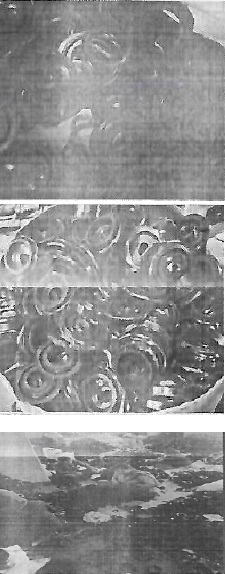

Product Description and End-Use (Rubber Rings) |

The rubber rings under reference are not general-purpose O-rings/gaskets. They are dimension-specific and application-specific rings made to fit particular sprinkler/drip components. They are supplied (i) along with complete sprinkler/drip irrigation systems and (ii) as replacement spares to farmers/OEMs/traders. Their sole function is to provide sealing/locking at joints so that the sprinkler/drip system operates leak-free and with proper pressure.

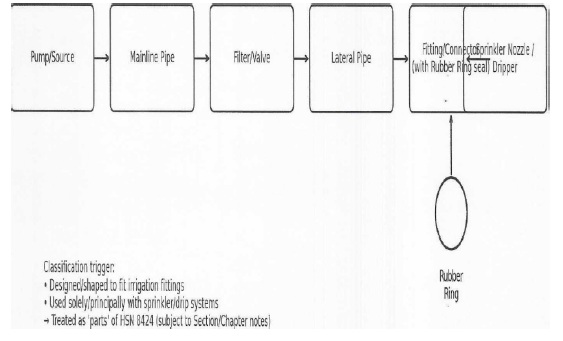

How the Rubber Ring becomes a ‘Part’ of Sprinkler/Drip Irrigation (HSN 8424)

Figure 2: Context – parts suitable for use solely/principally with sprinklers/drip irrigation system covered under Heading 8424 (illustrative).

| 3. |

|

Manufacturing Process (with photographs and flow diagram) |

The manufacturing process is a standard rubber processing and moulding sequence resulting in precision rings. The key stages (as shown in the submitted flow chart and the video frames) are set out below.

Rubber Ring Manufacturing Process (as shown in the video)

| Raw materials (rubber + fillers + oils + curing system) received & verified |

?

| Compounding / mixing to make uniform rubber compound |

?

| Sheeting on two-roll mill (as seen in the video) to form rubber sheets |

?

| Cutting/weighting into strips of preforms for each cavity/size |

?

| Loading preforms into multi-cavity mould plates |

?

| Compression moulding + (heat & pressure) to cure the rings |

?

| De-moulding + trimming/deflashing of excess rubber |

?

| Inspection / QC (dimensions, defects, fitment, hardness) |

?

| Packing & dispatch as sprinkler/drip irrigation system seals (spares/with system) |

Figure 3: Rubber ring manufacturing flow (compiled from process video and flow chart).

| Step |

Activity (what happens) |

Supporting photo (from video) |

| Step 1 Raw materials & additives |

Receipt of rubber base and compounding ingredients (fillers, process oil, curing agents, accelerators, pigments etc.) as per formulation. Materials are staged for batching. |

Photo: Raw materials & additives

|

|

Oil

|

Chemicals

|

Filler Like Calcium or China Clay

|

| Step 2 Compounding / Mixing |

Ingredients are mixed to obtain a homogeneous rubber compound with the required elasticity, hardness and sealing performance. (Mixing stage may happen in an internal mixer/compounder; the video shows pre-mixing material staging.) |

Mixing process for make rubber compound

|

| Step 3 Sheeting on two-roll mill |

The compounded rubber is sheeted on a two-roll mill to obtain uniform thickness and workable sheets for mould loading. |

Photo: Sheeting on two-roll mill

|

| Step 4 Cutting into preforms (strips) |

Rubber sheets are cut/weighted into preforms (strips) suitable for each mould cavity to ensure consistent ring dimensions. |

Photo: Cutting into preforms (strips)

|

| Step 5 Mould preparation & cavity loading |

Multi-cavity tooling is prepared; preforms are placed into the mould cavities. This ensures uniform filling during compression. |

Photo: Mould preparation & cavity loading

|

| Step 6 Compression moulding + curing |

The mould is placed in a press and subjected to heat and pressure. Rubber cures (cross-linking) and takes final shape. |

Photo: Compression moulding + (curing)

|

| Step 7 De-moulding, trimming & inspection |

Cured rings are removed from the mould. Flash/excess is trimmed and rings are inspected for dimensions, surface defects and fitment. |

Photo: Trimming & inspection

|

| Step 8 Packing & dispatch |

Accepted rings are packed and dispatched as sealing parts for sprinkler/drip irrigation systems. |

Photo: Packing & dispatch

|

| 4. |

|

Legal Basis for Classification under HSN 8424 (and not under HSN 4016) |

| 4.1 |

|

Heading 8424 and parts thereof |

Heading 8424 covers mechanical appliances for projecting, dispersing or • spraying liquids/powders, and specifically covers sprinklers and drip irrigation systems (including laterals). Tariff item 84249000 covers parts of goods of heading 8424.

| 4.2 |

|

Clarification by CBIC – Circular No. 155/11/2021-GST dated 17.06.2021 |

CBIC has clarified that the intention of Entry 195B (Schedule II) for heading 8424 is to cover laterals and such parts that are suitable for use solely or principally with sprinklers or drip irrigation system, as classifiable under heading 8424 as per Note 2(b) to Section XVI of the HSN; therefore, laterals/parts used solely/principally with sprinklers/drip irrigation system remain classifiable under heading 8424 even if supplied separately.

| 4.3 |

|

Application of Section XVI Note 2(b) (HSN) |

Note 2(b) to Section XVI provides that parts which are suitable for use solely or principally with a particular kind of machine/apparatus are to be classified with the machines of that kind. Since the subject rubber rings are engineered to be used solely/principally with sprinkler/drip irrigation systems (heading 8424), they merit classification as parts under heading 8424 (i.e., 84249000).

| 4.4 |

|

Why classification under HSN 4016 is not appropriate |

Heading 4016 is a residuary heading for ‘other articles of vulcanized rubber (other than hard rubber)’. It applies where a rubber article is not identifiable as a part suitable for use solely/principally with a particular machine/system under Section XVI. In the present case, the rubber rings are not ‘general use’ rubber gaskets; they are applicationspecific parts, supplied and used only in sprinkler/drip irrigation systems. The CBIC clarification also distinguishes ‘parts of general use’ (classifiable elsewhere) from parts suitable for use solely/principally with sprinklers/drip irrigation systems (classifiable under 8424).

| 4.5 |

|

Supporting precedent – Advance Ruling in the case of Kriti Industries (India) Ltd. In Kriti Industries (India) Ltd., the Authority discussed Entry 195B, Circular No. 81/55/2018-GST and Circular No. 155/11/2021-GST, and held that sprinklers/drip irrigation system including laterals and parts used solely or principally with such systems are classifiable under heading 8424 and attract the rate applicable to Entry 195B, even if supplied separately (subject to the ‘general use parts’ exception). |

C. QUESTIONS ON WHICH THE ADVANCE RULING IS SOUGHT:

Q-Whether parts of sprinkler system or drip irrigation system sold by us like the rubber rings etc. exclusively meant for use in Sprinklers and Drip irrigation system but sold in isolation as parts and not as a complete system classified under the heading 8424 the tax rate applicable on such components/parts when sold separately and not as a part of the sprinkler/ drip as “Sprinklers; drip irrigation system including laterals; mechanical sprayers”. Rubber Rings is classified under HSN 8424 and applicable tax rate is 5%. details as per the notification No. 1/2017-Central Tax (Rate), dated 28-6-2017. The entry No. 195B was inserted vide notification No. 6/2018-Central Tax (Rate), dated 25th January, 2018. It is pertinent to note that these items are designed and shaped that these can be used only in sprinkler/drip irrigation equipment and have no other use. What shall be GST rate on such products system falling under HSN 8424 attracting CGST a 2.5% sad SGST a 2.5% or Not?

D. COMMENTS OF THE JURISDICTIONAL OFFICER:-

Comments received from the Office of Deputy Commissioner, State Tax, Circle-C, Zone-IV, Ward-I, JAIPUR, Divisional Kar Bhawan, Jhalana Dungri, Rajasthan vide letter No.114 dated 16.12.2025 are as under:-

In reference to the above, the comments from the jurisdictional officer regarding the Advance Ruling application filed by M/s Shree Rubber & Polymers (Legal Name: ARTI PITALIYA) GSTIN: 08BUWPP5130P1ZO are furnished below:

| S.N. |

Question Raised by Applicant |

Comments |

| 1. |

Whether parts of sprinkler system or drip irrigation system sold by us like the rubber rings etc. exclusively meant for use in Sprinklers and Drip irrigation system but sold in isolation as parts and not as a complete system classified under the healing 8424 the tax rate applicable on such components/parts when sold separately and not as a part of the sprinkler/drip as Sprinklers; drip irrigation system including laterals; mechanical sprayers”. Rubber rings is classified under HSN 8424 and applicable “tax rate is 5%. Details as per the notification No. 1/2017-Central Tax (Rate), date 28-06-2017. The entry No. 195B was inserted vide notification No. 6/2018-central Tax (Rate), date 25th January, 2018. It is pertinent to note that these items are designed and shaped that these can be used only in sprinkler/drip irrigation equipment and have no other use. What shall be GST rate on such products system falling under HSN 8424 attracting CGST a 25% and SGST a 2.5% or Not? |

The parts of sprinkler system or drip irrigation system such as rubber rings etc., exclusively meant for use in sprinklers and drip irrigation systems but sold in isolation as parts and not as a complete system, are not classifiable under heading 8424. Instead, they are classifiable under heading 4016 and attract GST at the rate of 18% (9% CGST +9% SGST).

This classification applies because, as per Note 1(g) to Section XVI of the Customs Tariff (which covers machinery and mechanical appliances under Chapter 84, including HSN 8424), articles of Chapter 40 (rubber and articles thereof) are specifically excluded from Section XVI. The rubber rings in question are article of vulcanized rubber falling squarely under Chapter 40, regardless of their exclusive design or use in irrigation systems. They do not qualify of the concessional rate under Entry No. 195B of Schedule Il to Notification no. 01/2017-Centeral Tax (Rate) dated 28.06.2017 (as amended), which covers sprinklers and drip irrigation systems (including laterals) at 5% GST but does not extend to such rubber components when supplied separately. |

Proceedings Pending: As per available records, no proceedings are pending against the applicant under the proviso to sub-section (2) of section 98 of the CGST/RGST Act 2017.

E. PERSONAL HEARING:

In the matter, personal hearing was granted to the applicant on 18.12.2025. Mr. Pankaj Ghiya (Advocate) and Mr. Ribhav Ghiya (C.A.) Authorized Representative appeared for personal hearing. They reiterated the submission already made by them.

F. DISCUSSIONS AND FINDINGS

| 1. |

|

We have carefully examined the statement of facts, the application filed by the applicant, the submissions made during the personal hearing, and the comments received from the jurisdictional tax authority. We have also taken into consideration the issues for which the advance ruling is sought, along with all relevant statutory provisions and documentary material placed on record. |

| 2. |

|

The applicant, M/s ARTI PITALIYA, 173, LAXMI NAGAR, NIWARU ROAD, JAIPUR-302012, Rajasthan, is engaged in the manufacture of rubber rings. The question raised pertains to the classification of such rubber rings and falls under clause (a) of Section 97(2) of the CGST/RGST Act, 2017, namely “classification of any goods or services or both”, and is therefore fit for pronouncement by this Authority. |

| 3. |

|

The subject goods under consideration are rubber rings manufactured through a process involving mixing, moulding and curing of rubber. From the manufacturing process and material description placed on record, it is evident that the goods are products of vulcanisation as provided in the manufacturing process by the applicant. However, the record does not conclusively establish whether the rubber manufactured is “hard rubber” or “other than hard rubber”. |

| 4. |

|

However, if the rubber rings are made of hard rubber then other question arises. Hard rubber is not excluded from Section XVI under Section Note 1(a) or any other section notes thereof. |

| 5. |

|

In line with chapter notes of Chapter 84, goods identifiable as parts suitable for use solely or principally with a particular machine or system, classification under Chapter 84 as parts may be examined in terms of Section XVI and the relevant tariff headings. In such cases, the classification would depend upon whether the goods are parts of general use or parts suitable for use solely or principally with a specific machine or system. |

| 6. |

|

In this context, reference is made to Circular No. 155/11/2021-GST dated 17.06.2021, wherein it has been clarified as under: |

i. “The intention of the said entry has been to cover laterals (pipes to be used solely with sprinklers/drip irrigation system) and such parts that are suitable for use solely or principally with ‘sprinklers or drip irrigation system’, as classifiable under heading 8424 as per Note 2(b) to Section XVI of the HSN. Hence, laterals/parts to be used solely or principally with sprinklers or drip irrigation system, which are classifiable under heading 8424, would attract GST of 12%, even if supplied separately. However, any part of general use, which gets classified in a heading other than 8424, in terms of section Note and Chapter notes to HSN, shall attract GST as applicable to the respective heading.”

| 7. |

|

Thus, if the rubber rings are articles of hard rubber and are established to be parts suitable for use solely or principally with a specific system classifiable under heading 8424, they may be classifiable under heading 8424 and attract the concessional rate applicable thereto. Conversely, if such goods are of general use and not confined to sole or principal use with a specific system, they would not qualify for classification under heading 8424 and would attract GST at the rate applicable to their respective tariff heading. |

G. In view of the foregoing facts, circumstances and provisions of the GST law, we pass the following ruling:

RULING

Q-Whether parts of sprinkler system or drip irrigation system sold by us like the rubber rings etc. exclusively meant for use in Sprinklers and Drip irrigation system but sold in isolation as parts and not as a complete system classified under the heading 8424 the tax rate applicable on such components/parts when sold separately and not as a part of the sprinkler/ drip as “Sprinklers; drip irrigation system including laterals; mechanical sprayers”. Rubber Rings is classified under HSN 8424 and applicable tax rate is 5%. details as per the notification No. 1/2017-Central Tax (Rate), dated 28-6-2017. The entry No. 195B was inserted vide notification No. 6/2018-Central Tax (Rate), dated 25th January, 2018. It is pertinent to note that these items are designed and shaped that these can be used only in sprinkler/drip irrigation equipment and have no other use. What shall be GST rate on such products system falling under HSN 8424 attracting CGST a 2.5% sad SGST a 2.5% or Not?

Answer-yes, if rubbers rings are made of hard rubber and solely used for irrigation purposes but I’ll not attract concessional duty if is either made of other than hard rubber or used for general purposes.