Show Cause Notice for Penalty under section 272A(1)(d) of the Income Tax Act 1961

Why Show Cause Notice for Penalty under section 272A(1)(d) of the Income Tax Act 1961 is issued :

A penalty under Section 272A(1)(d) can be imposed if a person fails to:

- Comply with a notice under Section 142(1): These are notices issued by an Assessing Officer (AO) to produce accounts, documents, or other specific information.

- Comply with a notice under Section 143(2): This is a mandatory “scrutiny notice” requiring the taxpayer to produce evidence supporting their return of income.

- Comply with directions under Section 142(2A): These are directions for a special audit if the accounts are complex or the nature of transactions is cumbersome

Here is the section 272A(1) of Income tax Act 1961

Penalty for failure to answer questions, sign statements, furnish information, returns or statements, allow inspections, etc.

272A. (1) If any person,-

| (a) | being legally bound to state the truth of any matter touching the subject of his assessment, refuses to answer any question put to him by an income-tax authority in the exercise of its powers under this Act; or |

| (b) | refuses to sign any statement made by him in the course of any proceedings under this Act, which an income-tax authority may legally require him to sign; or |

| (c) | to whom a summons is issued under sub-section (1) of section 131 either to attend to give evidence or produce books of account or other documents at a certain place and time omits to attend or produce books of account or documents at the [place or time; or] |

| [(d) | fails to comply with a notice under sub-section (1) of section 142 or sub-section (2) of section 143 or fails to comply with a direction issued under sub-section (2A) of section 142,] |

he shall pay, by way of penalty, a sum of ten thousand rupees for each such default or failure.

Amount of Penalty under section 272A(1)(d) of the Income Tax Act

Under the Income Tax Act, 1961, Section 272A(1)(d) serves as a compliance tool that allows authorities to levy a fixed penalty of ₹10,000 for each failure

VIDEO IN HINDI ON INCOME TAX PENALTY NOTICE SECTION 272A(1)(d) ISSUED! STEP BY STEP GUIDE HOW TO REPLY

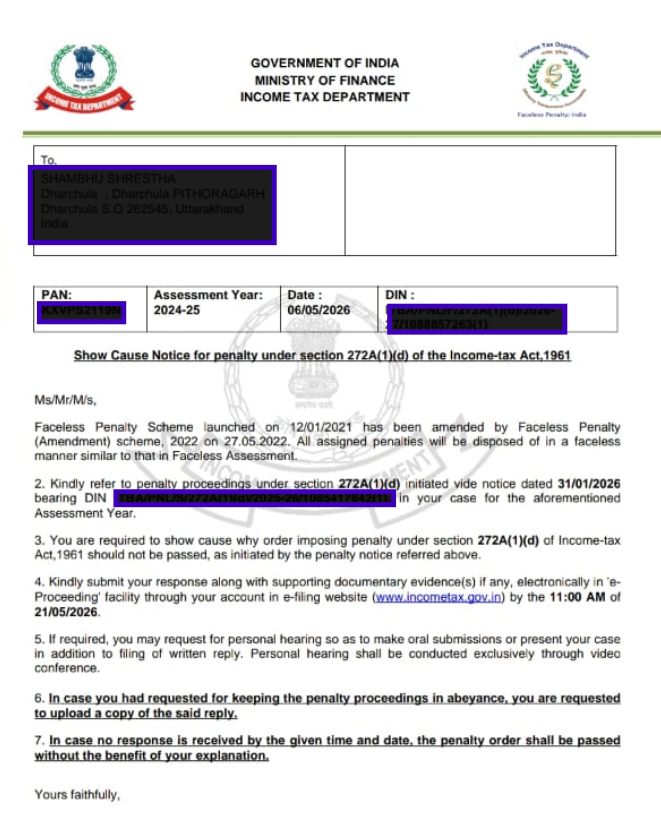

Format of Show Cause Notice for Penalty under section 272A(1)(d) of the Income Tax Act 1961

Important Legal Considerations for Show Cause Notice for Penalty under section 272A(1)(d) of the Income Tax Act 1961

- Reasonable Cause (Section 273B): Penalty is not automatic. Under Section 273B, no penalty shall be imposed if the taxpayer proves there was a “reasonable cause” for the failure. Examples of reasonable cause accepted by tribunals include lack of technological literacy or notices being sent to an old email ID.

- First Default Restriction: Courts and the Income Tax Appellate Tribunal (ITAT) have often ruled that if multiple notices are ignored for the same proceeding, the penalty should be restricted to the first default only, rather than multiplying ₹10,000 for every single notice issued.

- Show-Cause Requirement: Before levying the penalty, the AO must provide the taxpayer with an opportunity to be heard through a show-cause notice.

Who specifically can impose this penalty under section 272A(1)(d) ?

The “authorized person” varies depending on the nature of the default:

- Standard Assessment Units: In cases of failure to comply with a notice under Section 142(1) (inquires) or Section 143(2) (scrutiny), the penalty is imposed by the Income Tax authority that issued the notice.

- Special Audit Directions: If the failure relates to directions for a special audit under Section 142(2A), the authority who issued that direction will levy the penalty.

- Faceless Proceedings: Under the current faceless regime, a specialized Penalty Unit performs the drafting of the order, which is then finalized and served through the National Faceless Penalty Centre (NFPC).

- Higher Rank Authorities: For defaults occurring during proceedings before higher-ranking officials, the authority must be at least of the rank of Joint Director or Joint Commissioner.

How to reply Show Cause Notice for Penalty under section 272A(1)(d) of the Income Tax Act 1961

To reply to a Show Cause Notice (SCN) for a penalty under Section 272A(1)(d), you must submit a formal response via the Income Tax e-Filing portal justifying your non-compliance with “reasonable cause” under Section 273B.

Step-by-Step Submission Process

- Login: Access your account on the Income Tax Portal using your PAN as the User ID.

- Navigate to Notice: Go to ‘Pending Actions’ → ‘e-Proceedings’.

- View Notice: Click on ‘View Notices’ and select the relevant SCN for Section 272A(1)(d).

- Draft and Submit: Click on ‘Submit Response’. You can choose to ‘Agree’ or ‘Disagree’ with the proposed penalty. If disagreeing, you must provide a detailed explanation and attach supporting documents.

Framing Your Reply (Reasonable Cause)

Under Section 273B, the penalty can be waived if you prove a bonafide reason for the delay or failure. Common valid defenses accepted by Tribunals (ITAT) include: [1, 7]

- Technological Issues: Not receiving the notice because it was sent to an old email ID or an authorized representative’s (tax preparer) email who failed to inform you.

- Lack of Awareness: Being technologically illiterate or living in a remote area with poor internet access.

- Subsequent Compliance: If you eventually provided the requested information and the assessment was completed under Section 143(3), the initial default is often considered a “technical/venial breach” and the penalty may be deleted.

- Unreasonable Notice: Receiving a notice on a public holiday or with an extremely short response time (e.g., a few hours).

Draft Format Structure

Your uploaded letter should follow this professional structure:

- Header: Your Name, PAN, Address, and Date.

- Subject: Response to Show Cause Notice under Section 272A(1)(d) for AY [Year] – DIN [Number].

- Body: Acknowledge the notice, state that the non-compliance was neither intentional nor wilful, and detail the specific reasonable cause.

- Prayer: Request the Assessing Officer to drop the penalty proceedings as per Section 273B.

Draft Reply of Show Cause Notice for Penalty under section 272A(1)(d) of the Income Tax Act 1961

To,

The National Faceless Penalty Centre,

Income Tax Department.

The National Faceless Penalty Centre,

Income Tax Department.

Subject: Response to Show Cause Notice for Penalty u/s 272A(1)(d) – AY 2024-25

Ref: DIN: [Insert DIN from your notice] dated 06/05/2026

Ref: DIN: [Insert DIN from your notice] dated 06/05/2026

Respected Sir/Madam,

I, …………… holder of PAN [Insert PAN], am currently serving in the …….Indian Army. I am writing in response to the Show Cause Notice dated 06/05/2026, proposing a penalty for the alleged non-compliance with the notice dated 31/01/2026.

I most respectfully submit that the non-compliance was neither intentional nor wilful, but due to the following reasonable causes under Section 273B:

-

- Remote Area Posting: During the period when the previous notice was issued, I was posted in a remote/border area in the line of duty. Due to the nature of my service and the geographical constraints of my posting, I had extremely restricted or no access to stable internet connectivity.

- Lack of Awareness: Because of the lack of communication facilities at my duty station, I was unable to check my registered email or the e-filing portal to view the statutory notices in a timely manner.

- Bonafide Default: My failure to respond was purely a result of my professional commitments toward national security and not an attempt to evade tax proceedings. I have always intended to be a law-abiding taxpayer.

Prayer:

In view of the above facts and the protection provided under Section 273B, I request your good self to kindly consider my service conditions as a “reasonable cause” and drop the penalty proceedings initiated against me. I am now ready and willing to cooperate fully with any pending assessment requirements.

In view of the above facts and the protection provided under Section 273B, I request your good self to kindly consider my service conditions as a “reasonable cause” and drop the penalty proceedings initiated against me. I am now ready and willing to cooperate fully with any pending assessment requirements.

Yours faithfully,

(………….)

Date: [Insert Date]

Place: [Insert Current Location/Unit]

Date: [Insert Date]

Place: [Insert Current Location/Unit]

Important Next Steps:

- Attach Proof: When you upload this on the portal, must attach a copy of your posting order or a simple certificate/letter from your Commanding Officer (CO) confirming your posting in a remote area during Jan–May 2026. This serves as vital evidence.

- Check the Deadline: Ensure you submit this on the e-filing portal before 11:00 AM on 21/05/2026, as mentioned in your notice.

- Compliance: If the original notice dated 31/01/2026 asked for specific documents, try to upload those as well to show you are now complying.

Difference between 271(1)b and 272A(1)(d)

Under the Income Tax Act, 1961, both Section 271(1)(b) and Section 272A(1)(d) deal with penalties for failing to comply with statutory notices. While they often cover the same defaults, they belong to different chapters of the Act and have different historical applications.

The Key Difference

The primary difference is their current status and applicability.

| Feature | Section 271(1)(b) | Section 272A(1)(d) |

|---|---|---|

| Applicability | Widely considered non-operative for defaults occurring after July 1, 2002. | The standard current section used for levying penalties for notice non-compliance. |

| Penalty Amount | Fixed at ₹10,000 per default. | Fixed at ₹10,000 per default. |

| Triggers | Failure to comply with notices under Sections 142(1), 143(2), or directions under 142(2A). | Identical triggers: Failure to comply with notices under Sections 142(1), 143(2), or directions under 142(2A). |

| Relief | Protected by Section 273B if “reasonable cause” is proven. | Protected by Section 273B if “reasonable cause” is proven. |

Why are they often mentioned together?

Even though Section 271(1)(b) was largely replaced by Section 272A(1)(d), they are frequently cited together in legal cases and older tax manuals because:

- Legal Precedents: Many landmark judgments regarding “reasonable cause” were originally delivered under Section 271(1)(b) but apply equally to 272A(1)(d).

- Administrative Overlap: In some older proceedings or reassessments of past years, authorities might still reference Section 271(1)(b), although modern “Faceless” notices like the one received specifically use Section 272A(1)(d).

Your Query Solved

Show Cause Notice for Penalty under section 272A(1)(d) of the Income Tax Act 1961,

272a1d applicable from which year,

difference between 2711b and 272a1d

272a1d penalty amount,

section 272a of income tax act,

272a 1 d in hindi,