ORDER

Dr. Arjun Lal Saini, Accountant Member.- Captioned appeal filed by the assessee, pertaining to Assessment Year 2023-24, is directed against the order passed under section 250 of the Income Tax Act, 1961 (hereinafter referred to as “the Act”) by Commissioner of Income-tax (Appeals) dated 09.01.2026, which in turn arises out of an assessment order passed by the Assessing Officer under section 143(3), r.w.s. 144B of the Income tax Act, 1961, vide order dated 29.03.2025.

2. Grounds of appeal raised by the assessee, are as follows:

1. That, the Ld. CIT(A) has wrongly confirmed the assessment order passed by the Ld. assessing officer u/s 143(3) r.w.s. 144B of the Income Tax Act, 1961.

(a) . The notice issued u/s 143(2) of the Act is in violation of CBDT Instruction F. No. 225/157/2017/ITA-II dated 23.06.2017.

(b) . That, the scope of limited scrutiny of the assessee has been expanded without following the mandatory procedure laid down by CBDT to expand the scope of a limited scrutiny or to convert limited scrutiny into a complete scrutiny.

2. That, the Ld. CIT(A) has wrongly confirmed the addition of Rs. 13,69,71,824/-by treating agricultural income as business income.

3. That, the Ld. CIT(A) has wrongly confirmed the addition of Rs. 23,643/- on account of unexplained cash credit u/s 68 of the Income Tax Act, 1961.

4. That, the Ld. CIT(A) has wrongly confirmed the addition of Rs. 8,95,024/- on account of unexplained expenditure u/s 69C of the Income Tax Act, 1961.

5. That, the Ld. CIT(A) has wrongly confirmed the addition of Rs. 6,444/- u/s 40(a)(ia) of the Income Tax Act, 1961.

6. That, the Ld. CIT(A) has wrongly confirmed the initiation of penalty proceedings u/s 274 r.w.s 270A and Section 271AAC of the Income Tax Act, 1961.

7. That, the Ld. CIT(A) has wrongly confirmed the levy of interest u/s 234A, 234B and 234C of the Income Tax Act, 1961.

8. That, the findings of the Ld. assessing officer and Ld. CIT(A) are not justified and are bad-in-law. The assessee craves to add, amend, alter and delete any of the above grounds of appeal.

Facts of the assessee’s case

3. The relevant material facts, as culled out from the material on record, are as follows. The assessee, before us, is a limited company and filed its Income Tax Return (ITR), u/s 139 of he Act, on 25.09.2023, declaring total income of Rs.4,34,55,388/-. The return so filed was processed u/s 143(1) of the Act and subsequently selected for scrutiny through CASS and notice u/s 143(2) of the Act, was issued to the assessee- company by the NaFAC, New Delhi. The case of the assessee has been selected for scrutiny under CASS to examine the issues of High Creditors / liabilities & Substantial payments shown to entities not registered under GST.

4. However, assessing officer has himself observed that no addition should be made on the issue for which the assessee’s case was selected for limited scrutiny, hence assessing officer, held as follows:

“3 Issues where variation is not proposed:

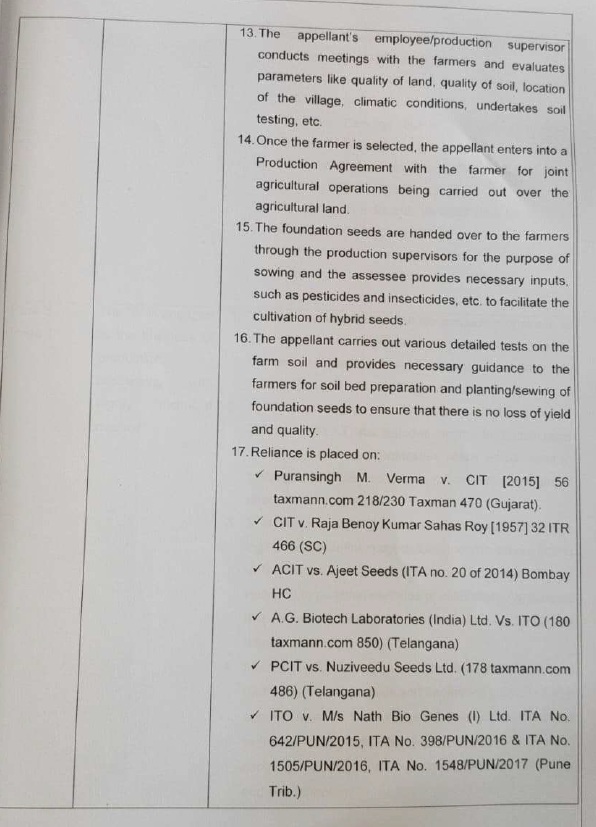

One of the reasons for selection of the case for scrutiny assessment is Substantial payments shown to entities not registered under GST. Assessee has submitted that the company is engaged in production and processing of seeds which are produced by company and also by farmers who are not registered under the GST. It may be noted that the Seeds are not subject to levy of GST. Necessary details/information filed by the assessee along with reply has been verified. Hence, no variation is being proposed on this issue.”

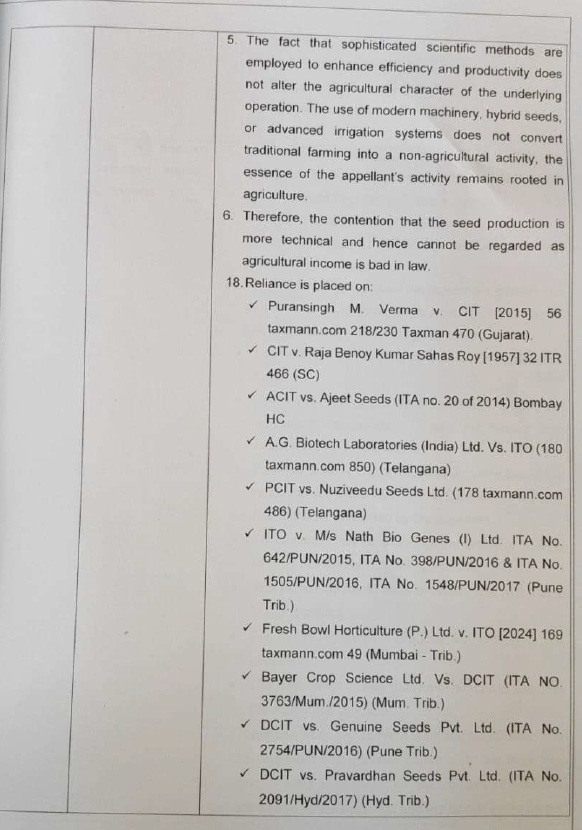

5. Then after, the assessing officer picked another issue for examination/scrutiny.

During the assessment proceedings, it was noticed by the assessing officer that in the assessee’s computation of total income, agriculture income of Rs.13,69,71,874/-, has been shown. In order to verify the genuineness of the same, notices u/s 142(1) of the Act, were issued requiring the assessee to provide the following:

| (a) |

|

Evidence of land ownership. |

| (b) |

|

Evidence of agriculture activity actually performed i.e. sowing/watering/ reaping etc |

| (c) |

|

Report of patwari/revenue authority regarding the same. |

| (d) |

|

gross receipts and expenses. |

| (e) |

|

Evidence of crop sale |

6. In response to the above notice of the assessing officer, the assessee furnished his reply on 26.11.2024, along with necessary documentary evidences. The relevant portion of his reply is reproduced hereunder:

“The company is engaged in production and selling of hybrid seeds of various grains, pulses, and vegetables. The company has also in-house research and development facilities for development of hybrid seeds approved by DSIR. The company takes on lease land from farm land owners and engages the people for production of seeds on that land. The company compensate the growers engaged by it for fertilizers, labour, pesticides, and other Agri-operations. The company owns the risk of quality of seeds and expenditure that may be incurred, therefore, these seeds are then sorted, tested, and processed for selling to the farmers for raising the crops. The company enters into agreements with the seed growers. Computation of income for assessment year 202324 is enclosed. Annexure-1

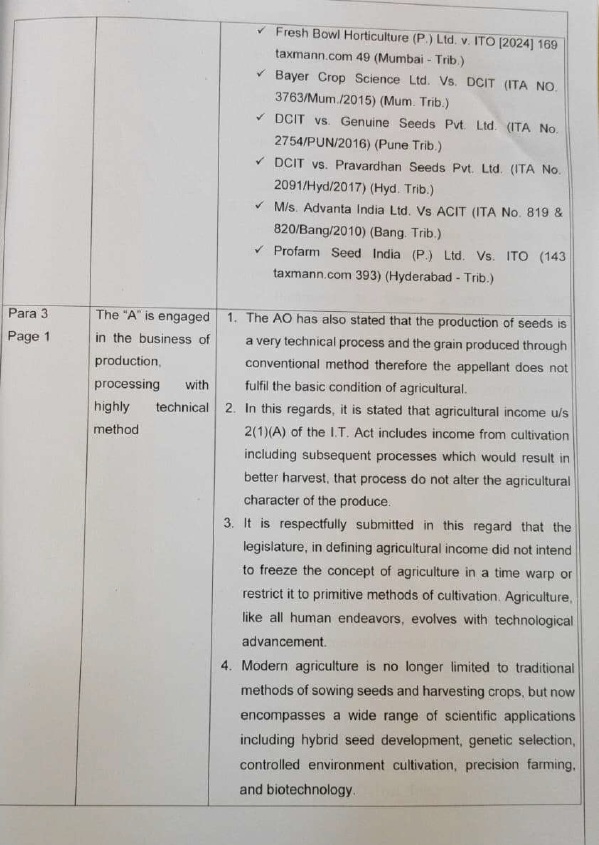

The company is engaged in production and processing of seeds which are produced by company and also by farmers who are not registered under the GST. The company has spent on seed production Rs.107,88,92,508/- on its leasehold land. In addition to its own seed production, the company has also purchased seeds from the farmers and other parties amounting to Rs.127,45,53,630/-. It may be noted that the Seeds are not subject to levy of GST. The balance amount of Rs.7,89,58,571/- represents cost of manpower, power, finance etc which are also beyond the purview of GST in respect of TDS deducted, you may please refer Annexure -4.”

7. The assessee has also furnished his reply on 31.01.2025, relevant portion of his reply is reproduced hereunder:

“The company is engaged in production, processing and trading of hybrid seeds. In order to produce seeds, the company takes on lease land spread over various areas of district by entering into Seed Production Agreement with landowners. Identity proof of the lessor and details of land like 7/12 abstract are attached to Agreement which describes the nature of expenses agreed to be reimbursed for taking seed production as per Company’s Program given to lessor. Seed Grower agreement (19 numbers on sample basis) with farmers are attached herewith in Annexure -2A, 2B, 2C, 2D and 2E”.

8. The Assessing Officer noticed that one of the reasons for selection of the case is high creditors / liabilities. In order to verify the issue a notice u/s 142(1) was issued to the assessee on 03.09.2024, requiring it to provide complete details of creditors shown in the balance sheet, as outstanding viz, name, PAN, e-mail ID along with confirmation of the closing balance from the respective parties and evidence to substantiate the genuineness of the transactions etc.

In compliance, the assessee provided only the name, PAN, email ID, closing balance but failed to provide confirmation from any of them. As per information provided by the assessee, an amount of Rs. 11,68,94,454/- has been shown outstanding as creditors. Since, assessee has not submitted confirmation from any of the party, whose names are appeared in the list provided by the assessee as creditors/other current liabilities, notices u/s 133(6) of the Act were issued to 2 parties shown under the head creditors, which were randomly selected for test check basis, on 26.12.2024, details of which are given in the assessment order.

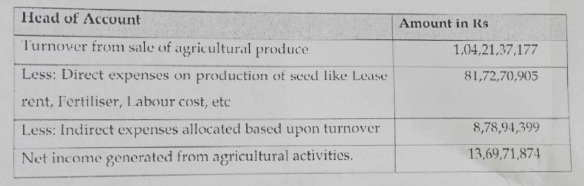

9. During the course of assessment proceedings, the Assessing Officer also noted that assessee has shown Gross Receipts from Agriculture at Rs.104,21,37,177/- against which, expenses have been claimed at Rs.90,51,65,303/-. Accordingly, net agriculture income has been shown at Rs.13,69,71,874/-, in its income tax return (ITR). The assessing officer noticed that in absence of complete details/evidences it is not verifiable how much land was there, how much crops/seeds were grown, at what rate agriculture produce were sold, what is gross receipts & what is gross expenses.

10. Further, assessee has submitted in its reply received on 31.01.2025, that the company is engaged in production, processing and trading of hybrid seeds. In order to produce seeds, the company takes on lease land spread over various areas of district by entering into Seed Production Agreement with landowners.

11. The Assessing Officer also observed that looking to the facts of the assessee’s, case, the agriculture activity is part and parcel of assessee’s business and the income originated from the same cannot be considered, as exempt, as agriculture income, as claimed by the assessee- company, rather the crops grown and sold, as part of its research and development and upon hybrid seeds, are in absolute terms, its business receipts. In view of these facts agriculture income of Rs. 13,69,71,874/-, disclosed by the assessee, in the income tax return (ITR) and claimed as exempt should be treated, as business income and to be added to the total income of the assessee- company. In view of the above, a final opportunity, vide show cause notice (SCN) of Assessing Officer, dated 03.03.2025, was accorded to show cause as to why the above proposed additions may not be made in the case of the assessee. Further, in order to negate the above proposed variation, the assessee has been required to substantiate its submissions and claims, with supporting evidences, if any.

12. In response, to the above show cause notice of the assessing officer, the assessee filed its reply on 10.03.2025, before the assessing officer. The relevant portion of the same is reproduced hereunder:

“Confirmation of Certain Creditors

In term of show cause notice issued by you, you have stated that you had sent notices u/s 133(6) to certain creditors who have not responded. In respect of all creditors, we have obtained the relevant account statements duly confirmed and also confirmation letters and copies of income tax returns filed in some cases. We list out below the name of the parties for your reference.

Adarsh Trading Company

Balram Agri Seeds

Harshad Trading Company

Super Seeds Pvt. Ltd.

KM Chauhan & Associates

SD Chotal

Sohan Lal Coqunodity Management Pvt. Ltd

Clarification for mismatch in closing balance.

1. Sohanlal Commodity Mgt. Pvt. Ltd.

As per cross ledger there is a difference of Rs.1,21,045/- in closing balance.

Reason – Party had issued 3 invoices in the last date in the month of march as shown in party ledger (i.e. Rs.71,428, Rs 5,173 and Rs. 43,718 dated 31st March, 2023). Our books of account had been finalised and audited before the issue of those invoices; therefore, we had not accounted for such invoices in our book. Therefore difference.

2. Adarsh Trading Co.

As per cross ledger there is a difference of Rs.3,67,166 in closing balance.

Reason: In the year 2021-22 goods received from Adarsh Trading Company, Discount were applicable on goods as per term and conditions mutually agreed between parties and we have also debited party for freight exp which are not payable by us as shown in invoices issued by party, therefore above accounting entries are not considered by party, accordingly difference.

3. Super Seed Pvt. Ltd.

As per cross ledger there is a difference of Rs.3,67,166/- in closing balance.

Reason: – During the year invoice of Rs.3,11,800 (dt. 08.10.2022 as shown in ledger) there was weight loss of Rs.50 kg in goods which are debited in party’s account same are not accounted by party, therefore difference.

4. Agricultural income

(a) Computation of Agricultural income and identification of growers.

The amount of Rs.1,27,45,53,630/- mentioned in the notice represents the value of purchases of traded goods, which is clearly reported on the face of the Statement of Profit and Loss. Thus, we humbly submit that above reported figure of Rs. 127,45,53,630/- is not agricultural income. The company has earned net agriculture income of Rs. 13,69,71,874/- from agricultural activities, for which the detailed computation/calculation is enclosed herewith. Refer Annexure-10.

The net agricultural income is arrived at as under:

You have stated in your notice that there are no complete details/evidences available for verifications as to how much land was there, how much crops/seeds were grown, at what rate agriculture produce were sold and what is gross receipts & what is gross expenses.

In connection with above, we would like to reiterate that the company is dealing with thousands of growers spread over various states. The company enters into Production Agreement which clearly mentions the lease area, items of production, reimbursement of certain expenses etc. In addition to this, the identity of farmer/landowners, identity of land i.e. 7/12 abstract, material inward also forms are enclosed with the production agreement. We had already submitted 19 production agreements for your reference, and we enclose here few more production agreements for your reference showing therein all the details as desired by you. Refer Annexure-11 to 13.

(b) Agriculture Receipt

You have mentioned in the above show cause notice that the agriculture activity undertaken by the company is part and parcel of its business and the income originated from the same cannot be considered as exempt as agriculture income, however, we would like to emphasise that the company leases farm land from land owners and employs individuals for seed production on the leased land. It compensates the growers for expenses related to fertilizers, labour, pesticides, and other agricultural operations. To maintain better control over costs and operations, the company makes payments to these parties based on a predetermined standard consumption basis, as agreed upon at the time of production agreement.

The above identical issue as raised by you is already decided by Hon’ble ITAT, Pune in case of DCIT, Circle-1/ Aurangabad v/s Nath Bio-genes (India) Limited. ITA No. 1548/PUN/2017. We reproduced para 23 of the said order for your reference.”

13. However, the assessing officer has rejected the above contention of the assessee and observed that assessee -company has neither performed the basic agricultural operation nor subsequent operations ordinarily employed by the farmer or agriculturist, as the assessee- company neither has derivative interest in the land nor it has actually cultivate the land. Further, production of seed is made with highly technical method, whereas grain is generally produced by conventional method. Therefore, assessee- company does not fulfil basic condition of agriculture. If the basic operation of agriculture is not carried on by the assessee -company, then the harvested foundation seeds purchased by him and converting them to certification seeds cannot be termed as integrated part of the foundation activity of agriculture. Thus, the net agriculture income shown in income tax return (ITR) of Rs.13,69,71,824/-, cannot be treated, as agriculture income and was treated by the assessing officer, as its business income of the assessee- company and accordingly the same was added to the total income of assessee.

14. In addition to above, the assessing officer noted that the assessee has shown outstanding liabilities of Rs.11,68,94,454/- in the balance sheet. Out of which assessee could not explain the liability of Rs.23,643/- (relating to KM Chauhan & Associates and SD Chotal). Hence, the same was considered as unexplained cash credit, and the same was added to the total income of the assessee u/s 68 of the Income Tax Act.

15. The Assessing Officer also noted that during verification of the outstanding liability shown in the balance sheet, it was found that there is net difference of 8,95,024/-, in respect of outstanding balance shown in the books of the assessee and the confirmation given by the respective party. This liability pertain to M/s Adarsh Trading Co., M/s Harshad Trading Company, M/s Super Seeds Pvt Ltd and M/s Sohan Lal Commodity Management Pvt Ltd. Since, the assessee has shown less liability to the extent of Rs.8,95,024/- which is neither paid out of books or not recorded in the books of account. As the liability is trade liability, the same was treated by assessing officer as unexplained expenditure u/s 69C and added to the total income of the assessee.

16. The Assessing Officer also noted that M/s Om Agri Brokers to whom payment of Rs. 21,480/- was made during the year, the assessee did not deduct tax. In some cases TDS was not deducted as the payments made were below the threshold limit for deducting TDS on brokerage/commission. Since, the assessee itself has accepted that TDS liable to be deducted on brokerage payments to M/s Om Agri Brokers to whom payment of Rs.21,480/- and the same was not deducted by mistake, accordingly, 30% of the same i.e. Rs.6,444/- was disallowed u/s 40(a)(ia) of the I.T. Act, and accordingly the same was added to the total income of the assessee.

Findings of the learned CIT(A)

17. Aggrieved by the order of assessing officer, the assessee carried the matter in appeal before Ld. CIT(A), who has confirmed the action of assessing officer. About the treatment of agricultural income of Rs.13,69,71,824/-, as business income, by assessing officer, the ld.CIT(A) observed that assessee is engaged in the business of production, processing and trading of hybrid seeds. The assessee has neither performed the basic agricultural operation nor subsequent operations ordinarily employed by the farmer or agriculturist, as neither has derivative interest in the land nor it has actually cultivated the land. Therefore, assessee-company does not fulfil basic condition of agriculture and the income claimed as agricultural is inseparably linked to the assessee’s organised commercial activity involving research and development of parent seeds, controlled hybridisation and extensive post-harvest processes such as testing, treatment, certification and packaging. The basic agricultural operations of tilling, sowing and harvesting were not carried out by the assessee itself but by farmers engaged under seed production agreements. Therefore, ld.CIT(A) confirmed the action of the assessment officer, and dismissed the ground raised by the assessee.

18. About the addition of Rs. 8,95,024/-made by the assessing officer, on account of unexplained expenditure u/s 69C of the Act, the ld.CIT(A) noted that there were material differences between the balances shown in the assessee’s books and the balances confirmed by the respective creditors. In all such cases, the assessee reflected lower outstanding liabilities as compared to the confirmations received, giving rise to a reasonable inference that the liabilities had either been settled outside the books or had ceased to exist. The explanations offered by the assessee attributing such differences to discounts, quantity loss or unaccounted invoices were not considered by ld.CIT(A). The ld.CIT(A) noted that in the absence of credible explanation or documentary evidences, the assessing officer was justified in holding that the liability to the extent of Rs. 8,95,024/-had ceased and in invoking the provisions of section 41(1) of the Act, the assessing officer was correct. Accordingly, this addition was confirmed by ld.CIT(A).

19. About the addition of Rs. 23,643/-made u/s 68 of the Act in respect of two creditors for whom confirmations were not furnished, the ld.CIT(A) noticed that despite specific request of the assessing officer, the assessee failed to submit confirmation from the concerned parties and merely produced ledger accounts maintained in its own books. In the absence of third-party confirmation or any supporting evidence to establish the genuineness and subsistence of the liabilities, the assessee failed to discharge the onus cast upon it u/s 68 of the Act, therefore, ld.CIT(A) confirmed the addition made by the assessing officer.

20. Regarding addition of Rs.6,444/-made by assessing officer, it was observed by ld.CIT(A) that during the assessment proceedings, the assessee itself has accepted that TDS liable to be deducted on brokerage payments, M/s Om Agri Brokers was not deducted, accordingly, assessing officer taking 30% of the payment made of Rs. 21,480 i.e. Rs. 6,444/ was disallowed u/s 40(a)(ia) of the I.T. Act, 1961. Therefore, the assessing officer was justified in his actions and the addition of Rs.6,444/- was therefore confirmed by ld.CIT(A).

21. Aggrieved by the order of the learned CIT (A), the assessee is in further appeal before us. We note that as per the assessment order, the case was selected for scrutiny under CASS to examine the issues of high creditors / liabilities & substantial payments shown to entities not registered under GST. The Assessing Officer has passed assessment order u/s 143(3) making the following additions:

| (i) |

|

Additions of Rs. 13,69,71,824/- on account of net agriculture income treated as business income. |

| (ii) |

|

Addition of Rs. 23,643/- on account of unexplained cash credit, |

| (iii) |

|

Addition of Rs 8,95,024/- on account of unexplained expenditure u/s 69C and |

| (iv) |

|

Addition of Rs. 6,444/- on account of disallowance u/s 40(a)(ia) of the I.T. Act. |

The assessee is in appeal before us against the above additions made by the assessing officer. However, we note that the assessee, does not press ground pertaining to addition of Rs. 6,444/-, on account of disallowance u/s 40(a)(ia) of the I.T. Act. We shall adjudicate the above disputed additions one by one, as follows.

Arguments of learned Counsel for the assessee for addition of Rs. 13,69,71,824/- on account of net agriculture income, treated as business income.

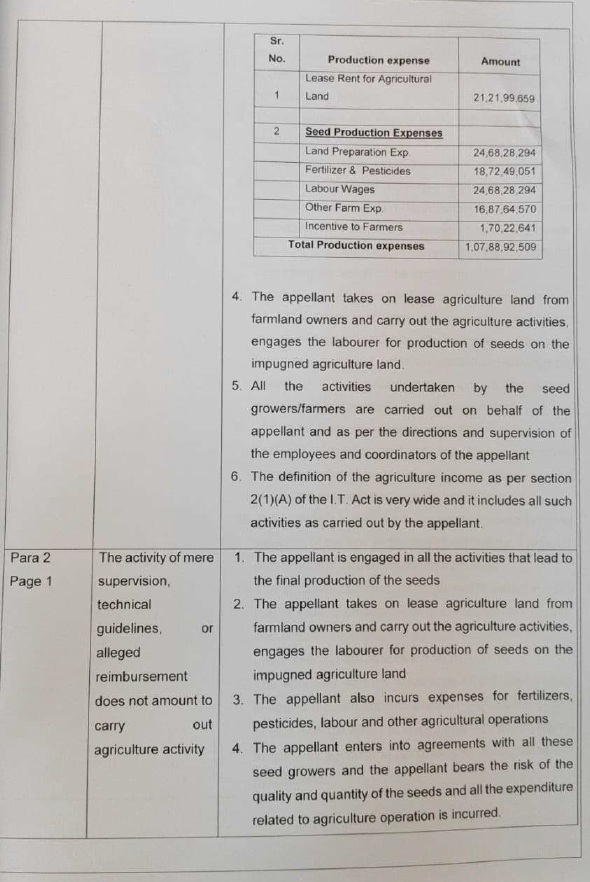

22. Shri Kalpesh Doshi, Learned Counsel for the assessee, begins by pointing out that assessee has carried out agriculture activities and claimed income from agriculture as exempt income as per section 10(1) r.w.s. 2(1A) of the Income Tax Act. The assessee takes land on lease, that is lease agriculture land from farmland owners and carry out the agriculture activities, and engages the labourer for production of seeds on the agriculture land. The assessee incurs expenses for fertilizers, pesticides, labour and other agricultural operations. Moreover, the assessee enters into agreements with all these seed growers and the assessee bears the risk of the quality and quantity of the seeds and all the expenditure related to agriculture operation is incurred. The copy of the lease agreement was submitted before the assessing officer. It can be observed from the lease agreement that the assessee also appoints a Coordinators for supervisions for coordinating with various farmers and seed growers and also to guide them in carrying out the agricultural operations on behalf of the assessee. The agreement also clearly states that labourers and labour -farmers has to carry out agricultural operations exclusively for the assessee during the period of the agreement. The assessee is engaged in all the activities that lead to the final production of the seeds. The assessee is responsible for the quality of the hybrid seeds that are produced and ultimately these seeds are sorted, tested and processed for selling to the farmers for raising the crops. The lease agreement, which is for long period, also clearly states that the assessee will have the ownership of all the agriculture produce from the agriculture land for the period of the agreement. Considering these facts, the net profit of the assessee should not be assessed under the head “income from business and profession”, as the assessee, himself is doing agricultural activities.

23. Learned Counsel further submitted that the assessee is in complete control of all aspects of the sowing activities, namely, determining the area under cultivation, the quantum of seed to be sown, sowing pattern, reconciliation of seed stocks, etc, and on a continuous basis the agricultural activity is monitored by the production supervisors and Coordinators. Further, the process of detasseling (i.e. process of removing the male part (tassel) from the female parent) is performed by the assessee through a coordinator who engages a casual labour for this purpose. The assessee can appoint the labourers, including farmer, labour, and assessee has right to remove them if they do not work as per the instructions of the assessee. The assessee under consideration takes its own decision and bears the entire risk and rewards. If there is a loss by doing agricultural activities, the assessee has to bear entire loss, and assessee has to decide in what way the land is to be utilised. Therefore, assessee exercises, entire control on land, and on agricultural activities and does the agricultural activities himself. Therefore, income generated from these activities are the income from doing agricultural activities. Therefore, assessee is a real owner of agricultural income, which is exempted from Tax. Hence, such income should not be assessed under the head income from business. To support his arguments, learned Counsel for the assessee relied on the following judgements:

| (i) |

|

ACIT v. Ajeet Seeds Ltd. [IT Appeal No. 20 of 2014 , dated 18-6-2015]. |

| (ii) |

|

A.G. Biotech Laboratories (India) Ltd. v. ITO (Pune – Trib.). |

| (iii) |

|

PCIT v. Nuziveedu Seeds Ltd. (Telangana) |

| (iv) |

|

ITO v. Nath Bio Genes (1) Ltd. [ITAppeal Nos. 642(PUN) OF 2015 and 1548(PUN) OF 2017, Dated 2-11-2018] |

| (v) |

|

Fresh Bowl Horticulture (P.) Ltd. v. ITO (Mumbai –Trib.) |

| (vi) |

|

Bayer Crop Science Ltd. v. DCIT (Mumbai – Trib.)/(ITA NO. 3763/Mum./2015) (Mum. Trib.) |

| (vii) |

|

DCIT v. Genuine Seeds Pvt. Ltd. [IT Appeal No. 2754(PUN) OF 2016, DATED 27-6-2019] |

| (vii) |

|

DCIT v. Pravardhan Seeds Pvt. Ltd [ITA No. 2091(Hyd) of 2017, dated 26-4-2023]) |

| (ix)Advanta |

|

India Ltd. v. ACIT (Bangalore – Trib.)/ (ITA No. 819 & 820/Bang/2010) (Bang. Trib.) |

| (x) |

|

Profarm Seed India (P.) Ltd. v. ITO ITD 113 (Hyderabad – Trib.) |

24. The ld.Counsel, also submitted written submission before the Bench, which we have gone through. The sum and substance of the written submission is that assessee was engaged in business of producing seeds, by conducting agricultural operations on agricultural lands and had been selling same to various farmers. Further the assessee was not in business of selling, licensing, or otherwise transferring research material/knowhow to any outside party nor did assessee carry out research for third party on job basis. The assessee took agricultural lands on lease and was conducting normal agricultural operations to produce hybrid variety of seeds in order to sell them in open market to seed industries, and farmers. As the assessee does himself agricultural activities and bears the risk and rewards hence, such a lease would not ipso facto make agricultural operations of assessee, as a contract farming. Hence, addition made by the assessing officer may be deleted.

Arguments of learned DR for the revenue for addition of Rs. 13,69,71,824/-on account of net agriculture income, treated as business income.

25. On the other hand, learned DR for the revenue argued that assessee has neither performed basic agricultural operations or subsequent operations that are ordinarily employed by the farmer or agriculturist. Therefore, assessee is not entitled to claim the exemption on account of agricultural income, and in real sense, the assessee is doing business. Therefore, income from agricultural operation should be assessable under the head ‘income from business’. Apart from this, learned DR for the revenue submitted written submission before the Bench, which we have gone through. The sum and substance of the written submissions are that the “Seed Production Agreements” relied upon by the assessee are not only illegal and void ab initio but also “colorable devices” (sham transactions) designed to evade tax by dressing up a procurement business as a farming activity. The assessee has not carried out the basic agricultural operations of tilling, sowing and harvesting. The assessee has neither performed the basic agricultural operation nor subsequent operations ordinarily employed by an agriculturalist. From the arrangement between the farmer and the assessee it is visible that the assessee is not carrying any agricultural operations required in terms of tests laid in the judgment of the Hon’ble Supreme Court in the case of CIT v. Raja Benoy Kumar Sahas Roy [1957] 32 ITR 466 (SC).

26. The ld.DR submitted that activity of mere supervision, technical guidelines or alleged reimbursement of cultivation expenses on predetermined terms does not amount to carrying on agricultural operations within the meaning of Section 2(1A) of the Act. Actually, it has also not reimbursed any cultivation expenses. The assessee has simply procured the seeds from the farmers at prevailing market prices and after certification process sold the same to its customers.The assessee has neither any derivative interest in the land nor it had actually cultivated the land. The assessee has failed to establish any substantial derivative interest in land, as the agreement relied upon do not confer effective control or possession of land so as to characterise the assessee as an agriculturalist. The ld.DR for the revenue, relied on the following judgements:

| (i) |

|

The Hon’ble F Bench of ITAT, Delhi in the case of P.H.I. Seeds (P.) Ltd. v. DCIT (Delhi – Trib.). |

| (ii) |

|

The Hon’ble Karnataka High Court in CIT v. Namdhari Seeds (P.) Ltd. (Karnataka). |

| (iii) |

|

The Hon’ble PUNE BENCH ‘B’ of ITAT in the case of ACIT v. R.J. Biotech Ltd. (Pune Trib.) |

| (iv) |

|

The Hon’ble Supreme Court in the case of . Raja Benoy Kumar Sahas Roy(supra). |

27. In rejoinder, learned Counsel for the assessee, distinguished the case law relied on by ld.DR for the Revenue. The ld. Counsel for the assessee submitted that none of the case law, relied on by assessing officer and by ld.DR for the revenue, is applicable to the assessee’s facts, under consideration. For this learned Counsel for the assessee submitted the following rebuttal of arguments made by the learned DR for the revenue and the case law relied on, by ld.DR. The learned Counsel also submitted various explanations which are reproduced below:

Analysis and conclusion

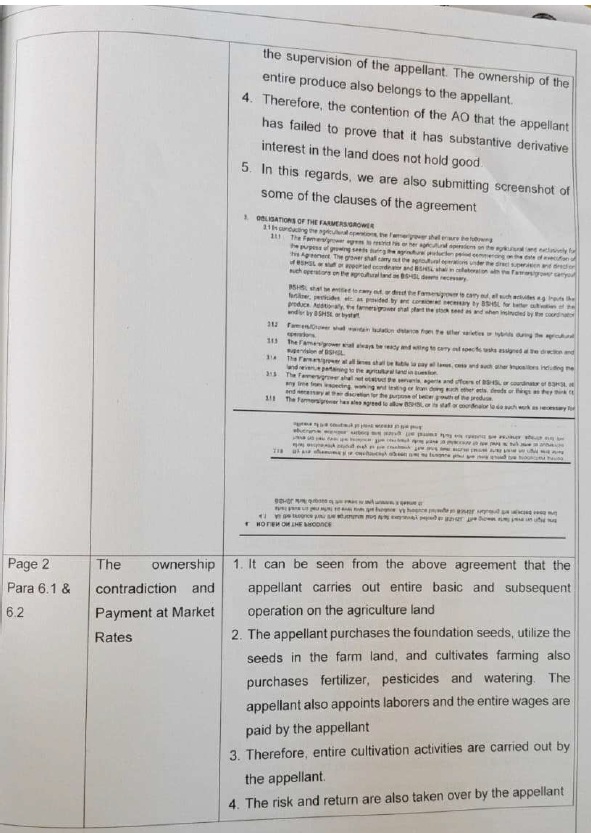

28. We have heard both the parties and carefully gone through the submission put forth on behalf of the assessee along with the documents furnished and the case laws relied upon, and perused the fact of the case including the findings of the ld CIT(A) and other materials brought on record. First of all, we should examine the fact whether assessee is engaged in agricultural activities and producing agricultural items and is an agriculturalist or not? In order to find out this answer, we should examine the important terms and conditions of the lease agreements, which are reproduced below:

“BACKGROUND TO THIS AGREEMENT

(A) BSHSL is engaged inter-alia in the business of growing, development, production and marketing and sale of seeds through various Farmers/growers with the help of coordinators.

(B) The Farmers/grower is the sole and absolute owner and is in the possession of agricultural and as defined and detailed in Schedule-1 and has absolute right of cultivation over the said agricultural land.

(C) BSHSL is desirous of entering into this agreement with the grower for leasing his land and for the purpose of producing seeds by utilizing the land owned by the farmers/grower. The Farmers/grower has agreed to provide the exclusive use of his land to carry out the agricultural operations & for production of crops to BSHSL on lease rental as per Schedule-II

(D) The Farmers/grower has agreed to provide the land for production of creps to BSHSL for the lease rental as per Schedule-Il The Company will also compensate for all production expenses for raising the crops such as land preparation, Irrigation, sowing, fertilization, combat against pests and diseases, weeding, harvesting, thrashing, incentive for crop cultivation etc. as detailed in Schedule II grower.

IT IS NOW AGREED BEWEEN THE PARTIES AS UNDER

1. DEFINITIONS AND INTERPRETTIONS

1.1 In this Agreement, the following terms and expressions shall have a meaning provided to them below unless the context provides otherwise:

Agriculture Land shall mean such agricultural and of which the grower is invalid possession and has absolute rights of use of the agricultural land and includes land leased by the grower for agricultural purposes, as more particularly described in Schedule-l of this Agreement.

Agriculture shall mean the performance of the agricultural land (which includes and preparation, irrigation, sowing of stock seeds, fertilization, combat against pests and diseases, weeding, harvesting, thrashing etc.) by BSHSL or its staff or by any other person (Including the farmer/grower) required to undertake the produce raised from the stock seeds/foundation seeds conforming to the specifications and be it to be marketed);

Coordinator shall mean any such person appointed BSHSL for supervision and direction and coordinating with various farmers/growers including the farmer/grower for carry ingot the process of agricultural operations on behalf of BSHSL;

Farmer/Grower means an individual engaged by BSHSL under this agreement. For growing the open pollinated. Cross Pollinated, Truthful, Foundation, Certified hybrid seeds, one or all from the above under the supervision and control of BSHSL employees, agents or coordinators engaged by BSHSL.

Seeds shall mean Open pollinated, Cross Pollinated, Truthful, Foundation, Certified Hybrid etc. one or all from the above.

Appointment of the Grower and Coordinator

The Farmers/grower is hereby engaged by BSHSL to carry out agricultural operations over the leased agricultural and exclusively for BSHSL during the term and in the manner indicated in this agreement and their whereby accepts his or her engagement under terms and condition of this Agreement.

Farmers/grower to carry out various agricultural activities under the guidance and supervision of the BSHSL, Company or staff or the appointed coordinator. Name of Coordinator for this activity and agreement is as mentioned in Schedule-IV. The BSHSL Company is entitled to carry out or direct the farmers to carry out agricultural activities considered necessary for the better production of seeds.

It is further agreed that BSHSL Company has a beneficial ownership of the land to carry out its agricultural operations as the farmer agrees to allow exclusive use of their land to the BSHSL company and the agricultural produce shall belong to the BSHSL entirely.

GROWERS REPRESENTATION

6.1 In consideration of the services rendered by the Farmers/grower in terms of this Agreement. BSHSL shall reimburse the agreed expenses incurred by Farmers/ grower for land preparation, cultivating the land, Irrigation, sowing, fertilization, purchases of pesticides, harvesting etc or any such other agriculture expenses, as detailed in Schedule-II The reimbursement of such expense would be made by BSHSL either directly to the farmer/grower account or through the coordinator appointed by the company to supervise the farmer/grower agriculture, land and activity.

BSHSL would also pay to the Farmers/grower compensation at the rate indicated in schedule-V (charges) subject to the seeds meeting the specifications. The compensation shall be paid directly to Farmers/grower or to the nominated/authorized person. The compensation shall be pay able in one or more instalments. The compensation is subject to the seeds grown on the agricultural land and meeting the specifications of BSHSL as mentioned in Schedule-III. BSHSL shall pay compensation to the grower either directly or through the coordinator.

29. From the above important terms and conditions of the lease agreement, noted above, it is abundantly clear that Farmers/grower has agreed to provide the exclusive use of their land to carry out the agricultural operations & for production of crops to BSHSL on lease rental as per Schedule-II. It is also undisputed fact that agricultural activities can be carried on, by any person/company on the land taken on lease basis. The assessee under consideration has a beneficial ownership of the land to carry out its agricultural operations as the farmer agrees to allow exclusive use of their land to the BSHSL (assessee- company) and the agricultural produce shall belong to the BSHSL (assessee) entirely. If there is a loss while doing agricultural activities, the entire loss will be borne by the assessee under consideration. All the risk will be taken by the assessee company. The assessee company may change the labour. Therefore, on lease land, only assessee can do the agricultural activities and the income arising from such agricultural activities will fall under the definition of agricultural income, which is exempted from Tax. Considering these facts, we are of the view that assessee company is engaged in agricultural activities and producing agricultural items/seeds at its own risk, if there is loss to the assessee, because of heavy rain fall and flood, then assessee alone will be responsible to bear the losses, hence, in the circumstances, we hold that assessee is engaged in the agricultural activities and doing agricultural operation in lease land, and performed all the agricultural operations. The assessee, pays, water expenses, labour expenses, expenses on fertilisers, growing expenses, watering expenses, harvesting expenses, and other necessary expenses for doing the agricultural operation. The assessee has exclusive right to use the land. Hence, assessee is an agriculturalist and income arised and accrued on account of agricultural activities, would be exempt from tax, and therefore, not assessable under the head, “business income”.

30. Now, we shall examine the meaning of the agricultural income and the scope of agricultural income. That is, what are the items/things are included in the definition of agricultural income, for that we have to examine the provisions of Section 2(1A) of the Act, which is reproduced (to the extent, useful for our analysis):

(1A) “agricultural income” means:-

(a) any rent or revenue derived from land which is situated in India and is used for agricultural purposes;

(b) any income derived from such land by –

(i) agriculture; or

(ii) the performance by a cultivator or receiver of rent-in-kind of any process ordinarily employed by a cultivator or receiver of rent-in kind to render the produce raised or received by him fit to be taken to market; or

(iii) the sale by a cultivator or receiver of rent in-kind of the produce raised or received by him, in respect of which no process has been performed other than a process of the nature described in paragraph (ii) of this sub-clause;

(c) any income derived from any building owned and occupied by the receiver of the rent or revenue of any such land, or occupied by the cultivator of the receiver of rent-in-kind, of any land with respect to which, or the produce of which, any process mentioned in paragraphs (ii) and (iii) of sub-clause (b) is carried on: Provided that-

(i) the building is on or in the immediate vicinity of the land, and is a building which the receiver of the rent or revenue or the cultivator, or the receiver of rent- in-kind, by reason of his connection with the land requires as a dwelling house, or as a store-house, or other out-building and

(ii) the land is either assessed to land revenue in India or is subject to a local rate assessed and collected by officers of the Government as such or where the land is not so assessed to land revenue or subject to a local rate, it is not situated.. “

31. For the purpose of clarity Section 10 (1) of the Act, 1961 is extracted below:

“10. Incomes not included in total income.

In computing the total income of a previous year of any person, any income falling within any of the following clauses shall not be included

(1) agricultural income.”

32. From the above definition of agricultural income, it is vivid that the performance by a cultivator or receiver of rent-in-kind of any process ordinarily employed by a cultivator or receiver of rent-in kind to render the produce raised or received by him fit to be taken to market; is the agricultural activity. The sale by a cultivator or receiver of rent in-kind of the produce raised or received by him, is agricultural activity. Therefore, definition of agricultural income is wide enough and the person who is doing agricultural activities on leased land, is also agriculturalist, hence, assessee’s income, under consideration, falls in the definition of agricultural income and receiving agricultural income, by doing agricultural activities, on lease land, is exempt from tax.

33. We note that assessee has carried out agriculture activities and claimed income from agriculture as exempt income as per section 10(1) r.w.s. 2(1A) of the I.T. Act. The assessee takes on lease agriculture land from farmland owners and carry out the agriculture activities, engages the labourer for production of seeds on the agriculture land. The assessee also incurs expenses for fertilizers, pesticides, labour and other agricultural operations. Moreover, the assessee enters into agreements with all these seed growers and the assessee bears the risk of the quality and quantity of the seeds and all the expenditure related to agriculture operation is incurred. The assessee submitted copy of agreement before the assessing officer. It can be observed from the agreement that the assessee also appoints a Coordinators for supervisions for coordinating with various farmers and seed growers and also to guide them in carrying out the agricultural operations on behalf of the assessee. The agreement also clearly states that farmer has to carry out agricultural operations exclusively for the assessee, during the period of the agreement. The assessee is engaged in all the activities that lead to the final production of the seeds. The assessee is responsible for the quality of the hybrid seeds that are produced and ultimately these seeds are sorted, tested and processed for selling to the farmers for raising the crops.The lease agreement also clearly states that the assessee will have the ownership of all the agriculture produce from the agriculture land.

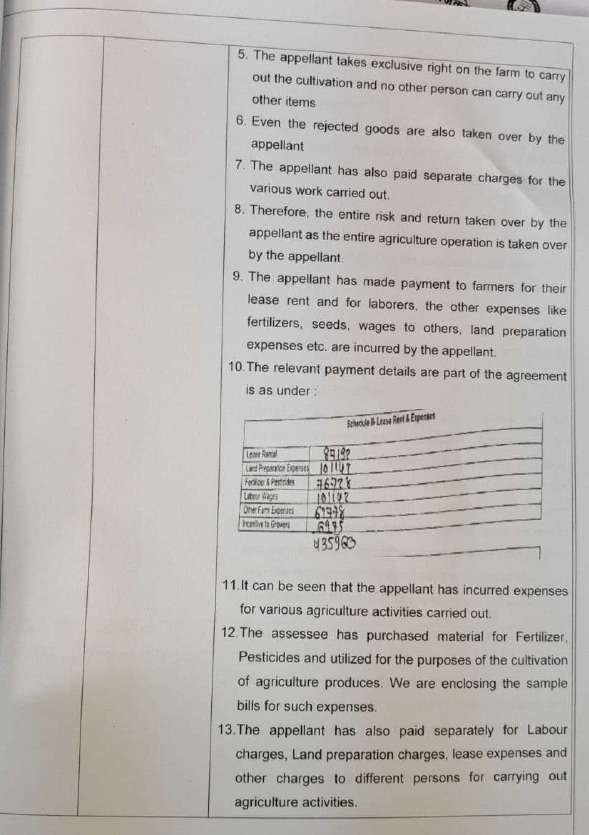

34. We note that assessee is engaged in the production and selling of hybrid seeds of various grains, pulses and vegetables. The assessee has also in house research and development facilities for the development of hybrid seeds approved by DSIR. It has been contended by the assessing officer that the assessee neither performed basic agricultural operations or subsequent operations that are ordinarily employed by the farmer or agriculturist. However, we find that the assessee is engaged in all the activities that lead to the final production of seeds. The seed growers/ farmers undertake the various activities such as land preparation, irrigation, sowing, fertilization, combat against pests and diseases, weeding, harvesting, thrashing etc, as directed and supervised by the coordinators appointed by the assessee. The assessee also incurs all the expenses pertaining to agricultural activities. All the activities undertaken by the seed growers/farmers are carried out on behalf of the assessee, and as per the directions and supervision of the employees and coordinators of the assessee. It was also contended by ld.Counsel that any revenue derived from the land and which is used for agricultural purpose and the activities carried on by the assessee is in the nature of agricultural activities and the income arising there from falls within the ambit of agricultural income under provisions of Section 2 (1)(a) the Act, 1961 and therefore, assessee is entitled for claim the exemption under Section 10 (1) of the Act. We note that assessee has also incurred expenses for various agricultural related expenses like land preparation expenses, fertilizers and pesticides, labour wages and various other expenses. The same has been duly reflected in the Schedule to the Agreements entered into with various seed growers. The details of expenses incurred during the year is as under:

| Sr. No. |

Production expense |

Amount |

| 1 |

Lease Rent for Agricultural Land |

21,21,99,659 |

| 2 |

Seed Production Expenses |

|

|

Land Preparation Exp. |

24,68,28,294 |

|

Fertilizer & Pesticides |

18,72,49,051 |

|

Labour Wages |

24,68,28,294 |

|

Other Farm Exp. |

16,87,64,570 |

|

Incentive to Labour/Farmers |

1,70,22,641 |

| Total Production expenses |

1,07,88,92,509 |

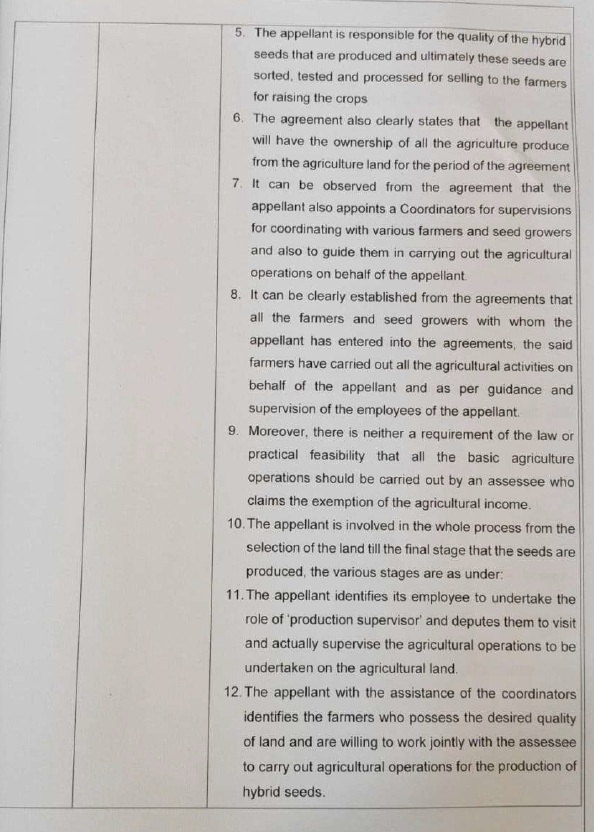

35. Therefore, we find that the assessee is involved in the whole process from the selection of the land till the final stage that the seeds are produced, the various stages are as under:

| (i) |

|

The assessee identifies its employee to undertake the role of production supervisor and deputes them to visit and actually supervise the agricultural operations to be undertaken on the agricultural land. |

| (ii) |

|

The assessee with the assistance of the coordinators identifies the farmers who possess the desired quality of land and are willing to work jointly with the assessee to carry out agricultural operations for the production of hybrid seeds. |

| (iii) |

|

The assessee’s employees conducts meetings with the farmers/labour and evaluates parameters like quality of land, quality of soil, location of the village, climatic conditions, undertakes soil testing, etc. |

| (iv) |

|

Once the farmer is selected, the assessee enters into a Production Agreement with the farmer for joint agricultural operations being carried out over the agricultural land. |

| (v) |

|

The foundation seeds are handed over to the farmers through the production supervisors for the purpose of sowing and the assessee provides necessary inputs, such as pesticides and insecticides, etc to facilitate the cultivation of hybrid seeds. |

| (vi) |

|

The assessee carries out various detailed tests on the farm soil and provides necessary guidance to the farmers for soil bed preparation and planting/sewing of foundation seeds to ensure that there is no loss of yield and quality. |

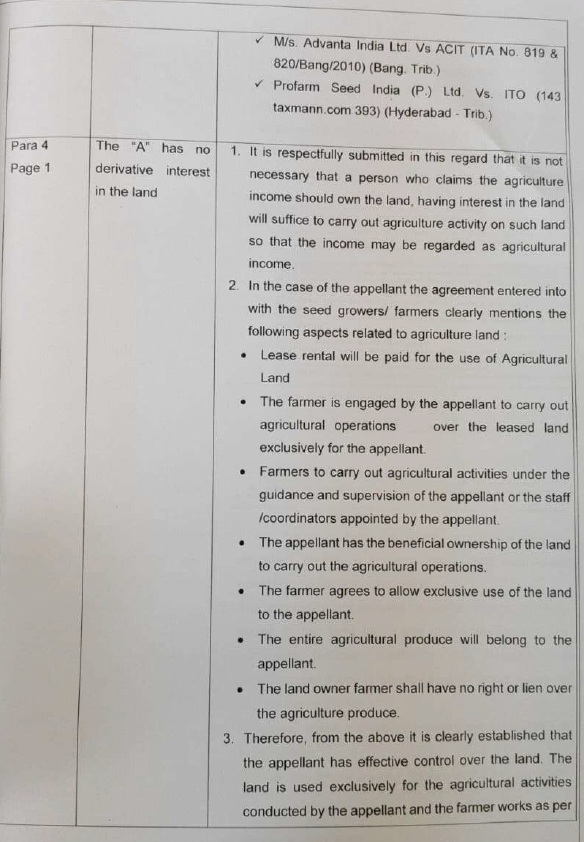

36. Therefore, we find that the assessee is in complete control of all aspects of the sowing activities, namely determining the area under cultivation, the quantum of seed to be sown, sowing pattern, reconciliation of seed stocks, etc, and on a continuous basis the agricultural activity is monitored by the production supervisors and coordinators. Further, the process of detasseling (i.e. process of removing the male part (tassel) from the female parent) is performed by the assessee through a coordinator who engages a casual labour for this purpose. The assessing officer has held that basic agricultural operations of tilling, sowing and harvesting were not carried out by the assessee, but independent farmers engaged in the production. The finding of the assessing officer is without any merit as it can be clearly established from the agreements that all the farmers and seed growers with whom the assessee has entered into the agreements, the said farmers have carried out all the agricultural activities on behalf of the assessee and as per guidance and supervision of the employees of the assessee. Moreover, there is neither a requirement of the law or practical feasibility that all the basic agriculture operations should be carried out by an assessee who claims the exemption of the agricultural income. Therefore, the contention that the assessee has not done any basic agricultural operations and therefore cannot claim the agriculture income, does not hold any merit. It has been further held by the assessing officer that the assessee does not hold any substantive derivative interest in the land and the agreements entered into with the farmers do not confer effective control or possession of the land. However, as we have noted earlier, also that it is not necessary that a person who claims the agriculture income should own the land, having interest in the land will suffice to carry out agriculture activity on such land so that the income may be regarded as agricultural income.In the case of the assessee, the agreement entered into with the seed growers/farmers clearly mentions the following aspects related to agriculture land:

| (i) |

|

Lease rental will be paid for the use of Agricultural Land. |

| (ii) |

|

The farmer is engaged by the assessee to carry out agricultural operations over the leased land exclusively for the assessee. |

| (iii) |

|

Farmers to carry out agricultural activities under the guidance and supervision of the assessee or the staff/coordinators appointed by the assessee. |

| (iv) |

|

The assessee has the beneficial ownership of the land to carry out the agricultural operations. |

| (v) |

|

The farmer agrees to allow exclusive use of the land to the assessee. |

| (vi) |

|

The entire agricultural produce will belong to the assessee. |

| (vii) |

|

The land owner farmer shall have no right or lien over the agriculture produce. |

Therefore, from the above it is clearly established that the assessee has effective control over the land. The land is used exclusively for the agricultural activities conducted by the assessee and the farmer works as per the supervision of the assessee. The ownership of the entire produce also belongs to the assessee. Therefore, the contention of the assessing officer that the assessee has failed to prove that it has substantive derivative interest in the land does not hold good.

37. We note that the assessing officer has also stated that the production of seeds is a very technical process and the grain produced through conventional method therefore the assessee does not fulfil the basic condition of agricultural. In this regard, it was stated by ld.Counsel for the assessee that agricultural income includes income from cultivation including subsequent processes which would result in better harvest, that process do not alter the agricultural character of the produce. We find that the legislature, in defining agricultural income did not intend to freeze the concept of agriculture in a time warp or restrict it to primitive methods of cultivation. Agriculture, like all human endeavours, evolves with technological advancement. Modern agriculture is no longer limited to traditional methods of sowing seeds and harvesting crops, but now encompasses a wide range of scientific applications including hybrid seed development, genetic selection, controlled environment cultivation, precision farming, and biotechnology. The fact that sophisticated scientific methods are employed to enhance efficiency and productivity does not alter the agricultural character of the underlying operation. The use of modem machinery, hybrid seeds, or advanced irrigation systems does not convert traditional farming into a non-agricultural activity, the essence of the assessee’s activity remains rooted in agriculture. Therefore, the contention that the seed production is more technical and hence cannot be regarded as agricultural income, is bad in law and cannot be accepted.

38. We also note that the details of the agriculture receipts as to the receipts from the sale of different types of seeds has been disclosed in the schedules in the Audit Report on Page no. 54 of paper book. Moreover, in each of the agreements entered with the farmers/ land owners the amount of lease rent paid as well as the amount of expenses for various agriculture activity, like land preparation expenses, fertilizer and pesticides expenses, labour expenses have been duly quantified and disclosed separately. This can be verified from the lease agreement. The assessing officer has wrongly relied on the decision of the Hon’ble Karnataka High Court in the case of Namdhari Seeds Pvt Ltd. (supra) The case of the assessee is distinguishable from the decision of the Hon’ble High Court, as follows:

| SI. No. |

Facts related to the Assessee |

Facts related to M/s Namdhari Seeds Pvt. Ltd. |

| 1. |

Land taken on lease and paid lease rent Rs. 21,21,99,659/-. Therefore, actively taken possession and control on agriculture land and carried out agriculture activity |

Land is not taken on lease and no lease rent is paid and no activity carried out on land |

| 2. |

Cultivates the agriculture produces on their own and entire produces belongs to the assessee |

Purchases hybrid seeds, if only as per specification from farmers |

| 3. |

Incurred entire cultivation expenses, Land Preparation Fertilizer & Pesticide Farm Expenses Labour Charges |

Not concerned with expenditure related to cultivation. |

| 4. |

Entire risk of crop failure is with assessee |

Risk of quantity, quality, failure & cost remains with farmers |

| 5. |

Various Courts have distinguished the decision of Namdhari Seeds(supra) in the case of:

• Puransingh M. Verma v. CIT (Gujarat)

• Ajeet Seeds Ltd. (supra)

• Bayer Crop Science Ltd. (supra)

• Nath Bio Gens (1) Ltd. (supra)

• Advanta India Ltd. (supra)

• . Genuine Seeds Pvt. Ltd. (supra)

|

|

Therefore, as can be observed above that the case of the assessee is distinguishable from the decision of the Hon’ble High Court’s decision in the case of M/s Namdhari Seeds, as in the said case the land was not taken on lease by the assessee nor did the assessee bear any of the expenses, and the assessee only purchased the seeds from the farmer if it met with specifications. In case of the assessee, the land is taken on lease, incurs lease rent, incurs various expenses for cultivation and labour, the land is used exclusively for the activities of the assessee and the assessee is the owner of the entire produces.

39. Further, we note that there are various judicial precedents where it has been held that for growing hybrid seeds, seeds are sown in field and usual agricultural operations, basic and subsequent, are undertaken utilizing human skill. In addition to this, measures are taken for restricting role of nature. Such measures are only taken in enhancing the yield. Such measures, thus, have nothing to do with the biological growth that takes place in the soil or such other substratum where the seeds are sown. An agriculturist while growing his crops, is known to have used conventional as well as scientific method for reducing hostile interplay of natural forces on his crop. When such activity is taken to highest standard, it would still not make the growing operation a synthetic one. Thus, growing seeds can never be non-agricultural and growing of such seeds would always be regarded as ‘agricultural”. In this regards, reliance is placed on the decision of the Gujarat High Court in Puransingh M. Verma(supra), that the attentions is invited in comparing with the nursery operations that were held to constitute agriculture income. The nursery activity involve basic agricultural operations like tilling, sowing, planting, watering, and manuring, which qualify the resulting income as agricultural despite involving pots and controlled environments, tissue culture operations. This process involves human skill and labour on the land itself transforming the scientifically developed material into marketable produce through traditional cultivation methods. Therefore, the income ultimately derives from agriculture activity that undergo complete agricultural operations on land, the income is be treated as agricultural income. In fact, the decision of the Hon’ble Supreme Court in the case of Raja Benoy Kumar Sahas Roy (supra)favours the assessee, under consideration.

40. We note that on the identical and similar facts and nature of agriculture activities, various courts have considered such activities as agriculture activities and income is duly allowed as exempt u/s 10(1) of the I.T. Act, the reliance is placed on following decisions:

| (1) |

|

Ajeet Seeds Ltd. (supra) |

The Assessing Officer held that growing breeder and foundation seeds would not be an agricultural activity and, therefore, they are not agricultural produce. The Hon’ble Court held that when breeder seeds and foundation seeds are grown successfully, lot of scientific help is required. The conditions are controlled and effect of natural forces are minimized. It is only after such skilful and scientific process, such seeds are grown. The question before the court is, whether growing such seeds does not amount to ‘agricultural activity. For growing breeder and foundation seeds, seeds are sown in field and usual agricultural operations, basic and subsequent, are undertaken utilizing human skill. In addition to this, measures are taken for restricting role of nature. Such measures are only taken in enhancing the yield. Such measures, thus, have nothing to do with the biological growth that takes place in the soil or such other substratum where the seeds are sown. An agriculturist while growing his crops, is known to have used conventional as well as scientific method for reducing hostile interplay of natural forces on his crop.

When such activity is taken to highest standard, it would still not make the growing operation a synthetic one. Thus, growing seeds can never be non-agricultural.

| (2) |

|

A.G. Biotech Laboratories (India) Ltd. (supra) |

Section 2(1A), read with section 10(1) of the Income-tax Act, 1961 – Agricultural income (Tissue cultured plants) Assessment years 2002-03 and 2003-04-Assessee-company was engaged in business of micro-propagation of plants through tissue culture technology – It earned income from sale of tissue cultured plants and claimed that same should be treated as agricultural income exempt from tax under section 10(1) – Revenue rejected assessee’s claim and treated income as business income subject to taxation It was noted that cultivation of mother plants on land involved all basic agricultural operations contemplated under section 2(1A) i e, filling, planting, nurturing, and harvesting – Whether tissue culture process that followed was merely an advanced method of propagating and multiplying plant material derived from those mother plants – Held, yes – Whether, therefore, income earned by assessee from sale of tissue cultured plants constituted agricultural income within meaning of section 2(1A) and was exempt from tax under section 10(1)-Held, yes (Paras 26 and 28) (In favour of assessee)

| (3)Nuziveedu |

|

Seeds Ltd .(supra) |

Section 10(1), read with section 2(1A), of the Income-tax Act, 1961 – Agricultural income (Hybrid seeds) Assessment year 2011-12- Assessee-company was engaged in research, production and sale of agricultural/hybrid seeds – it entered into agreements with farmers to utilize their lands, under which farmers performed normal agronomic practices for production of seeds from foundation seeds supplied by assessee under its supervision and control Assessee claimed exemption under section 10(1)-Assessing Officer disallowed same on ground that production on lands owned by farmers could not be treated as agricultural operations carried on by assessee – It was noted that parent seeds were produced by way of agriculture and cultivation and cultivation was done under assessee’s supervision and at its own costs and risks – Further, assessee played an active role of action of monitoring and nurturing plants cultivated by farmers – Whether since assessee was involved through farmers for production of hybrid yielding seeds for different types of hybridization and which were used for purpose of agriculture for deriving high yielding seeds, assessee was indirectly involved in said activity and, therefore, Tribunal was justified in allowing deduction under section 10(1) by taking income of assessee as an agricultural income – Held, yes [Paras 30 and 31] [In favour of assessee]

| (4) |

|

Nath Bio Genes (1) Ltd. (supra) |

The assessee has entered into an agreement with the agricultural landlords-cum growers for growing the foundation and breeder seeds as per the terms and conditions and also the scientific specifications provided by the assessee, the assessee bears all the expenditure on land development, irigation, fertilizers, pesticides, transportation etc., the assessee pays the land rent and also for the labour, when the landlord acts only as a grower and hands over the entire agricultural produce of foundation and breeder seeds to the assessee at the end. Grower never sold the agricultural produce to the assessee etc. The court held that the activity constitutes agricultural activity as the assessee constitutes an agriculturist and the entire activity of production and growing of said seeds becomes an agricultural activity. The procurement of seeds from the landlords-cum-growers is not the transaction of purchase of seeds for trading activity. Further, the judgment of Coordinate Bench of the Tribunal in the case of Ajeet Seeds Ltd. (supra) was confirmed by the Hon’ble Court of judicature Bombay, Aurangabad Bench in the said case. Therefore, the claim made by the assessee is proper.

| (5) |

|

Fresh Bowl Horticulture (P.) Ltd. (supra) |

Section 10(1) of the Income-tax Act, 1961-Agricultural income (Cultivation/sale of edible white button mushrooms) – Assessment year 2020-21-Assessee-company was engaged in cultivation and sale of edible white button mushrooms – It filed its return of income claiming gross agricultural receipts from cultivation of mushrooms as exempt under section 10(1)-Assessing Officer observed that mushrooms were grown by assessee in growing rooms’ under controlled conditions in racks placed on shelves and on compost (manure) which was prepared with paddy straw, horse manure, chicken manure, gypsum and urea, which was not land and income earned from processing of white button mushroom was in nature of business-He thus, treated said income as business income and made addition – It was noted that issue of treatment of income from cultivation and sale of white button mushrooms had been dealt with by Special Bench of Tribunal in Dy. CIT v. Inventaa Industries (P) Ltd. ITD 1 (Hyderabad –Trib.) (SB) wherein it was held that mushroom was an agricultural product raised from land and, thus, income derived from its sale was agricultural income Whether, following aforesaid decision, assessee’s claim for treating cultivation and sale of white button mushroom as agricultural activity resulting in agricultural income exempted under section 10(1) was to be allowed – Held, yes [Para 9] [In favour of assessee]

| (6) |

|

Bayer Crop Science Ltd. (supra) |

Section 10(1), read with section 2(1A), of the Income-tax Act, 1961 Agricultural income (General) – Assessment years 2009-10 and 2012-13-Whether ownership or possession of land is not a pre-condition for claiming agricultural operations to be carried out under section 10(1) – Held, yes-Assessee was engaged in growing and selling of hybrid corn seeds jointly with help of farmers – During year, it earned income from said activity which was claimed as exempt under section 10(1) Assessing Officer denied claim of assessee primarily on basis that assessee had not carried agricultural process ordinarily undertaken by cultivator and assessee was not in lawful possession of land -As per agreement between assessee and farmer, farmer agreed to perform agricultural operations such as sowing foundation seeds for purpose of production of hybrid seeds from foundation seeds jointly Further, said issue had been considered in earlier years in assessee’s favour – Whether since manner in which agricultural process was undertaken by assessee during year was similar to preceding years wherein issue was considered in favour of assessee, assessee was entitled to claim exemption under section 10(1)-Held, yes, [Paras 19 and 20] [In favour of assessee]

| (7)Genuine |

|

Seeds Pvt. Ltd. (supra) |

S. 10(1): Agricultural income-Growing high yielding hybrid seeds Agricultural activityEntitle for exemption. The assessee produced high yielding hybrid seeds. It purchased seeds and then produced hybrid seeds in the net houses and marketed the seeds. The assessing officer held that the activity carried on by assessee was not agricultural activity and treated the receipts as income of assessee and denied the exemption. The CIT(A) deleted the addition. Dismissing the appeal of the revenue the Tribunal held that growing of hybrid seeds could never be held to be non-agricultural activity. Accordingly entitle for exemption.

| (8) |

|

Pravardhan Seeds Pvt. Ltd . (Supra) |

The assessee is engaged in the business of production of hybrid seeds and open pollinated seed varieties of various crops like cotton, paddy, maize, sunflower, bajra, wheat, jowar, vegetables, etc. It is carrying out the agricultural operation in whole of India, that since it is not possible for the assessee to own all the land, as required for the purpose of its agricultural operations, it has accordingly taken certain land on lease from farmers and has also availed services of farmers by entering into seed production agreement for usage of their land, that the farmers are provided with foundation seeds for carrying out the agricultural activities/cultivation for multiplication of seeds under the guidance, specifications and supervision of the assessee; that the farmers are required to deliver the final produced hybrid seeds including un-utilized foundation seeds to the assessee; in lieu of the said activities, the assessee agrees to pay the farmers compensation for land usage and reimbursement of cultivation expenses and service charges as per terms of the agreement and the entire risk and reward of growing the hybrid seeds, with regard to the said agricultural activities/cultivations, is entirely borne by the assessee. The Hon’ble High Court held that the seed is a product of agricultural activity. When such agricultural activity is conducted and seeds are produced, merely because such seeds were sold commercially, the basic agricultural operations also cannot be dubbed as ‘commercial activities’, and not ‘agricultural activities. The court relied on M/s. Nuziveedu Seeds Ltd., and Prabhat Agri Biotech (supra), and dismissed the appeal filed by the Revenue.

| (9). |

|

Advanta India Ltd. (supra) |

Section 2(1A) of the Income-tax Act, 1961 Agricultural income [Income from producing hybrid seeds) – Assessment years 2003-04 and 2004-05 – Whether definition of ‘agriculture’ given in section 2(1A) does not specify that produce should be fit for human consumption; only requirement is that produce should be out of cultivation by usage of land – Held, yes – Assessee-company was engaged in development and production of basic and hybrid seeds – Upto basic seed activity all primary operations were performed by assessee-company on its own lands or lands leased by it under its own direct supervision and guidance with help of casual labour engaged by it and then basic seeds were given to farmers for producing hybrid seeds on their own lands under supervision of assessee – Cost of production was reimbursed to farmers and produce was taken back by assessee Whether production of hybrid seeds from basic seeds was agricultural activity and income earned by assessee from this activity would be agricultural income exempt under section 10-Held, yes [Paras 9 and 10] [In favour of assessee]

| (10) |

|

Profarm Seed India (P.) Ltd. (supra) |

Section 2018), read with section 10(1) of the Income-tax Act, 1961-Agncultural Income (Seeds) Assessment year 2014-15-Assessee was engaged in business of producing foundation seeds, by conducting agricultural operations or agricultural lands and had been selling same to various seed companies – It claimed exemption under section 10(1) Assessing Officer denied claim of assessee for exemption under section 10(1) on ground that assessee departed from basic agricultural operation and indulged into production of parent seeds by taking land on lease and undertaking planned scientific and specialised procedures and considered it as contract farming However, Commissioner (Appears) deleted said disallowance it was found that assessee produced voluminous record to show engagement of labour and payment of salaries to supervisors apart from producing agreements with landowners – Further according to assessee they were not in business of selling, licensing, or otherwise transferring research material/knowhow to any outside party nor did they carry out research for third party on job basis -Assessee took agricultural lands on lease and was conducting normal agricultural operations to produce hybrid variety of foundation seeds in order to sell them in open market to seed industries, and in that pursuit they engaged labour, supervisors etc. Whether merely because assessee took land on lease for conducting their research operations to produce foundation seeds of hybrid varieties, such a lease would not ipso facto make operations of assessee as contract farming – Held, yes – Whether therefore, there was no illegality or irregularity in Commissioner (Appeals) deleting disallowance -Held, yes [Paras 16 to 18] [In favour of assessee]

41. Therefore, we note that the issue under consideration, is duly covered in favour of the assessee, by the above various decisions of various courts. The seeds and other agricultural production were produced by way of agriculture and cultivation and cultivation was done under assessee’s supervision and at its own costs and risks. Further, the assessee played an active role of action of monitoring and nurturing plants cultivated by labourers/farmers. The land is used by the assessee himself, and the assessee does the agricultural activities himself. Hence, based on these facts and circumstances, we allow the ground raised by the assessee.

42. In the result, ground no.2 raised by the assessee, is allowed.

43. Ground No 3, raised by the assessee pertains to addition of Rs 23,643/- on account of unexplained cash credit u/s 68 of the Income Tax Act, 1961.

44. Brief facts, qua the issue are that during the year under consideration, the assessee-company has declared outstanding creditors amounting to Rs. 11,68,94,000/-.The assessing officer called for various documentary evidences with respect to creditors outstanding during the year. The assessee- company has duly filed the documentary evidences being ledger account, confirmation ledger and income tax return. However, assessing officer made addition of Rs. 23,643/-on account of unexplained cash credit u/s 68 of the Act with respect to two creditors.

45. On appeal, the learned CIT(A) confirmed the action of the assessing officer, therefore, the assessee is in appeal before us.

46. Learned Counsel for the assessee submitted the following chart, before us, and explained that the amount of Rs. 23,643/- comprises of two creditors, which are given below:

| Name |

Amount (Rs.) |

Remarks |

| KM Chauhan & Associates |

11,700 |

• The ledger account is enclosed at page no. 151

• The contra ledger account is enclosed at page no. 152

• The creditors outstanding at year end pertain to ROC filing fees. The payment for the same has been made in the subsequent year through banking channel and the ledger account reflecting the payment is enclosed at page no. 151 A. |

| SD Chotal |

11,943 |

• The ledger account is enclosed at page no. 153

• The contra ledger account is enclosed at page no. 154

• The creditors outstanding at year end pertain to LEI work and Government fees. The payment for the same has been made in the subsequent year through banking channel and the ledger account reflecting the payment is enclosed at page no. 153A |

| Total |

23,643 |

|

Therefore, learned Counsel for the assessee contended that addition made by the assessing officer should be deleted.

47. On the other hand, learned DR for the revenue relied on the findings of the authorities below.

48. We have heard both the parties. We note that assessee has availed professional services from these parties for carrying out compliance work. The above creditors are creditors for expenses i.e. for the business purpose, therefore, the amount of Rs. 23,463/- is not in the nature of loan transactions. The assessee- company has not availed any loan from these parties, therefore, the provisions are not attracted. Further, the payment for expenses is made in the subsequent year, therefore, the genuineness of expenses is also proved.Therefore, the addition u/s 68 of the Act is not justified and required to be deleted.In this regard, reliance is placed on the following decisions:

| (1) |

|

PCIT v. Yogendrakumar Gupta (Gujarat) |

Section 68 of the Income-tax Act, 1961 Cash credits (Loan) – Assessment year 2006-07 – Assessee was engaged in business of trading in shares and securities -Assessing Officer, on basis of information received that assessee had obtained accommodation entries in form of loan and advances from one ‘B’ Ltd treated loan as unexplained credit under section 68. On appeal, Commissioner(Appeals) deleted addition on finding that amount received as loan by assessee from ‘B’ Ltd, was through regular banking channels and assessee had proved identity of creditor and genuineness of transactions, which had been further strengthened by filing confirmation from creditor. On further appeal, Tribunal found that assessee had furnished copy of audited accounts, balance sheet and Profit and Loss account along with copy of ledger of ‘B’ Ltd and during course of assessment proceedings ‘B’ Ltd, categorically confirmed entry of certain sum with copy of bank accounts reflecting transaction there in and accordingly, deleted addition-Whether since said B Ltd had been held to be a genuine party and its identity, genuineness and creditworthiness were established, revenue was not justified in proceeding against assessee on ground that loan taken from said ‘B’ Ltd was unexplained credit and that lender was not genuine – Held, yes [Para 5] [In favour of assessee)

| (2) |

|

CIT v. Pancham Dass Jain (Allahabad) |

The Tribunal had recorded a categorical finding of fact based on appreciation of materials and evidence on record that the said amounts represented the purchases made by the assessee on credit and, therefore, the provisions of section 68 could not be attracted in the instant case. The view taken by the Tribunal was correct and, therefore, there was no question of, making any addition under section 68. [Para 8]

49. Therefore, we find that the creditors are for expenses, that is, for the business purpose, therefore, the amount of Rs. 23,463/- is not in the nature of loan transactions. The assessee- company has not availed any loan from these parties. Further, the payment for expenses is made in the subsequent year, therefore, the genuineness of expenses is also proved, hence we delete the addition.

50. In the result, ground No.3 raised by the assessee, is allowed.

51. Coming to the ground No. 4, which pertains to the addition of Rs. 8,95,024/- on account of unexplained expenditure u/s 69C of the Income Tax Act, 1961.

52. Brief facts qua the issue are that during the year under consideration, the assessee -company has made purchases from various parties. The assessing officer has called for various details with respect to creditor’s outstanding at the end of the year. The assessee has duly filed various details with respect to the creditors. However, assessing officer made addition to the tune of Rs.8,95,024/-, on account difference in closing balance of the creditors, as per books of accounts and contra ledger account.

53. On appeal, by the assessee, the learned CIT(A) confirmed the addition made by the assessing officer, therefore, the assessee is in further appeal before this Tribunal.

54. Learned Counsel for the assessee argued that the difference in the closing balance of the ledger account is on account discount on purchases, loss of goods during transport, freight expenses, etc. The ld.Counsel submitted reconciliation and party- wise explanation with respect to each creditor, which is as under:

| Name |

Amount of Difference |

Remarks |

| M/s Adarsh Trading Co. |

3,67,166 |

The difference in the ledger account has arisen due to discount on purchases made.

The assessee- company has recorded freight expenses in the ledger account i.e. debited the party account since the freight was to be paid by the party, whereas the creditor has not recorded freight amount in its ledger account. The ledger account is enclosed at page no. 155 |

| M/s Harshad Trading Company |

39,647 |

The difference in the ledger account has arisen due to discount on purchases made, vide paper book page No. 156 |

| M/s Super Seeds Pvt. Ltd. |

3,67,166 |

The closing balance as per books of accounts is Rs. 9,15,65,827/- and the balance confirmed by the party is Rs. 9,15,71,642/-. Therefore, there is a difference of Rs. 5815/-only. Thus, the Ld. assessing officer has wrongly calculated the difference of Rs. 3,67,166/-.

The difference in the ledger account is on account of loss of goods. Out of the total value of goods, the assessee- company has received 50 kg of goods, less than the actual order quantity.

The assessee has debited the party account to the extent of such loss of goods which is not accounted by the party. Therefore, there is difference in the ledger account.

The ledger account is enclosed at page no. 159-161

|

| M/s Sohan Lal Commodity Management Pvt. Ltd. |

1,21,045 |