Post office withdrawal form sb-7 pdf download

Post office withdrawal form sb-7 pdf download & Filling Guide for easy understanding with FAQS

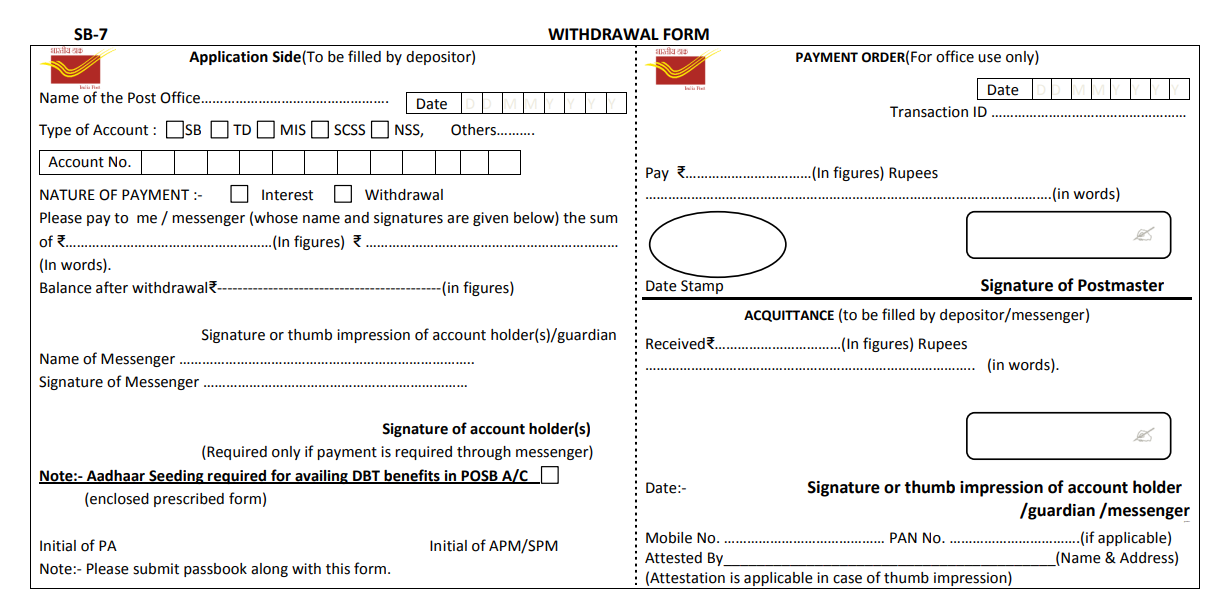

Format of Post office withdrawal form sb-7

What is Form SB-7 (Post Office Withdrawal Form)?

Based on the India Post , here are the key features and details of the Form SB-7 (Withdrawal Form):

1. Purpose & Account Types Covered

This is a unified form used for making withdrawals or claiming interest from various Post Office Savings Bank (POSB) schemes. It caters to:

-

SB: Savings Bank Account

-

TD: Time Deposit

-

MIS: Monthly Income Scheme

-

SCSS: Senior Citizens Savings Scheme

-

NSS: National Savings Scheme (and others)

2. Dual-Section Layout

The form is divided into two distinct vertical sections:

-

Left Side (Application Side): To be entirely filled out by the depositor before submission.

-

Right Side (Payment Order): Strictly reserved for official office use, transaction recording, and the Postmaster’s signature.

3. Key Data Fields Required

-

Account Details: Name of the Post Office, Type of Account, and Account Number.

-

Nature of Payment: Tick boxes to specify whether the transaction is for Interest or a Withdrawal.

-

Amount: Must be explicitly written in both figures and words, along with the expected balance after withdrawal.

-

Identity Details: Fields for the depositor’s Mobile Number and PAN Card Number (if applicable).

4. Third-Party / Messenger Adjustments

-

The form permits a designated Messenger to withdraw money on behalf of the account holder.

-

If used, the specific name and signature of the messenger are mandatory, alongside an additional authorization signature from the account holder.

5. Mandatory Submissions & Compliance

-

Passbook: The physical passbook must accompany this form for verification.

-

DBT Benefit Notice: The form contains a specific note highlighting that Aadhaar Seeding is mandatory if you wish to avail Direct Benefit Transfer (DBT) benefits through your Post Office Savings Bank account.

Download Post office withdrawal form sb-7 pdf

Post office withdrawal form sb-7 pdf download CLICK HERE

Step-by-Step Guide: How to Fill Post Office Withdrawal Form SB-7

what are the steps for Post office withdrawal form fill up ?

Here is a step-by-step guide to filling out the India Post SB-7 Withdrawal Form, based on the official layout.

The form is split into two vertical halves. You only need to fill out the Left Side (Application Side) and the Acquittance section at the bottom right. Leave the Payment Order section on the top right blank for the postmaster.

Step 1: Top Section (Account & Post Office Details)

-

Name of the Post Office: Write the name of the specific branch where you are transacting.

-

Date: Enter the current date in the

DD/MM/YYYYboxes. -

Type of Account: Check the box that applies to your account (e.g., SB for Savings Bank, MIS for Monthly Income Scheme, SCSS for Senior Citizens).

-

Account No.: Write your complete Post Office account number clearly.

Step 2: Transaction Details

-

Nature of Payment: Check Withdrawal (or Interest if you are only drawing the accumulated interest).

-

Amount Fields:

-

In the first blank space after “the sum of ₹”, write the amount you want to withdraw in figures (e.g.,

5,000/-). -

In the next space, write the exact same amount in words (e.g.,

Five Thousand Rupees Only).

-

-

Balance after withdrawal: Calculate and write the remaining balance left in your account after this transaction in figures.

Step 3: Signatures & Personal Details (Bottom Left)

-

Signature or thumb impression: Sign exactly as you did when opening the account.

-

Mobile No. & PAN No.: Enter your registered mobile number and your PAN card number in the designated fields.

Step 4: Acquittance Section (Bottom Right)

This section confirms you have received the cash. Fill this out at the counter:

-

Received ₹: Write the withdrawal amount in figures again.

-

Rupees (in words): Write the amount in words.

-

Signature: Sign again to acknowledge receipt of the money.

💡 Crucial Reminders

-

Passbook: You must present your physical Post Office passbook along with this form, or the transaction will be rejected.

-

Using a Messenger? If you cannot visit the branch yourself, write the Name of Messenger and have them sign the form. You must also sign the extra Signature of account holder(s) line on the left side to formally authorize them.

-

Aadhaar Seeding: If you are using this account to receive government subsidies (DBT benefits), ensure your Aadhaar is linked (there is a checkbox on the form to request this if it isn’t done yet).

General & Usage FAQs

Here are the most frequently asked questions (FAQs) regarding the India Post Form SB-7 (Withdrawal Form), designed to address the most common queries savers and financial practitioners have:

Q1: What is Form SB-7 used for?

A: Form SB-7 is a unified transaction form used to withdraw cash or claim accumulated interest from various Post Office Savings Bank (POSB) schemes, including Savings Accounts (SB), Time Deposits (TD), Monthly Income Schemes (MIS), and Senior Citizens Savings Schemes (SCSS).

Q2: Is it mandatory to submit the physical passbook with Form SB-7?

A: Yes. The physical passbook must accompany the form for verification and updating. The post office will reject the transaction if the passbook is not presented.

Q3: Can I use Form SB-7 to close my post office account?

A: No. Form SB-7 is strictly for partial/regular cash withdrawals or interest claims. For complete account closure or premature closure, you must use Form SB-7B or Form SB-4 (depending on the specific scheme rules).

Third-Party & Messenger FAQs

Q4: Can someone else withdraw money from my account using Form SB-7?

A: Yes. The form features a specific Messenger provision. You must fill out the left side, write the name of your messenger, and sign the authorization block. The messenger must also sign the form in front of the postmaster upon receiving the cash.

Q5: Do I need to sign the form twice if a messenger is withdrawing the money?

A: Yes. You must sign the standard “Signature or thumb impression of account holder” line, and you must also sign the secondary line that states “Signature of account holder(s) (Required only if payment is required through messenger)”.

Technical & Compliance FAQs

Q6: Are PAN and Mobile Number mandatory on Form SB-7?

A: Yes, there are dedicated fields at the bottom left for your registered Mobile Number and PAN Card number. Providing these ensures compliance with anti-money laundering regulations and helps track taxable interest components (like in SCSS or MIS).

Q7: What is the checkbox for “Aadhaar Seeding” on the form?

A: The form contains a crucial compliance note: if you wish to receive Direct Benefit Transfer (DBT) or government subsidies into your Post Office Savings Bank account, you must tick this box and enclose the prescribed Aadhaar seeding form.

Q8: Which sections of Form SB-7 should the depositor leave blank?

A: You must completely leave the top-right section (“PAYMENT ORDER”) blank. This area is strictly reserved for official use, where the postal assistant inputs the transaction ID and the Postmaster signs off on the release of funds.

Related Post

Post Office Account opening form Download

Acknowledgement Slip form Download

AEA Survival Benefit Form Download

Post Office Application for automatic transfer from SB to RD Download

Post Office Application for Availing Cheque facility form Download

Post Office Application for change of nomination from Download

Post Office Application for Fresh Cheque Book from Download

Post Office Application for issue of Duplicate Passbook From Download

Post Office Application for pledging of form Downloadfv

Post Office Application for settlement of deceased claim case from Download

Post Office Application for the issue of Duplicate Savings Certificates from Download

Post Office Application for transfer of account from Download

Post Office Application for transfer of Savings Certificates from Download

Post Office Application Form For Closure Of Account On Maturity from Download

Post Office Application Form For extension of RD/TD/PPF/SCSS Account From Download

Post Office Application Form For Loan/Withdrawl From RD/PPF and SSA Accounts form Download

Post Office Application Form For Opening of Account From Download

Post Office Application Form For Pre-Mature Closure Of Account from Download

YOUR QUERY SOLVED

SB 7,

SB 7 WITHDRAWAL FORM,

POST OFFICE SB 7 WITHDRAWAL FORM DOWNLOAD

#IndiaPost, #PostOfficeSavingsBank, #POSB, #FormSB7, #WithdrawalForm, #SavingsAccount, #TimeDeposit, #MonthlyIncomeScheme, #SeniorCitizensSavingsScheme, #NationalSavingsScheme, #CashWithdrawal, #InterestClaim, #PassbookRequired, #AadhaarSeeding, #DirectBenefitTransfer, #MessengerWithdrawal