ORDER

Madhusudan Sawdia, Accountant Member.- The captioned appeal is filed by the Revenue feeling aggrieved by the order passed by the Learned Commissioner of Income Tax (Appeals), Guntur (“Ld. CIT(A)”) dated 23/06/2011 for the Assessment Year (“A.Y.”) 1995-96. The assessee has also raised Cross Objection for the A.Y. 1995-96. As the Revenue’s appeal and the Cross Objection are pertaining to the same assessee and the issues raised in both the Revenue’s appeal and the assessee’s Cross Objection are interwoven, therefore, for the sake of convenience and brevity, they were heard together and are being disposed of vide a consolidated order. Firstly, we shall take up the appeal filed by the Revenue.

ITA No.709/Hyd/2012(Revenue’s Appeal) :

2. The brief facts of the case are that the assessee is a society registered under the Societies Registration Act, New Delhi on 10.01.1983. The assessee filed its return of income for the A.Y. 1995-96 on 31.10.1995, declaring Nil income after claiming exemption under section 11 of the Income Tax Act, 1961 (“the Act”). This appeal represents the second round of litigation before the Tribunal. In the first round, the assessment was completed by the Learned Assessing Officer (“Ld. AO”) under section 143(3) read with section 147 of the Act, determining the total income of the assessee at Rs.14,28,17,985/- on 29/03/2000. The assessee preferred an appeal before the Ld. CIT(A). The Ld. CIT(A) confirmed an addition of Rs.13,76,58,674/- and set aside other additions aggregating to Rs.51,59,311/- to the file of the Ld. AO. Against the said order of the Ld. CIT(A), both the assessee as well as the Revenue filed appeals before the Tribunal. The Tribunal, vide its order in ITA Nos.10 & 12/Hyd/2001 dated 07.10.2002, dismissed the appeal of the Revenue and set aside the addition of Rs.13,76,58,674/- to the file of the Ld. AO with a direction to decide the issue afresh after providing proper opportunity to the assessee. Pursuant thereto, the Ld. AO passed a consequential order under section 143(3) read with sections 147 and 254 of the Act on 26.03.2004, assessing the total income of the assessee at Rs.13,76,58,674/-, mainly by invoking section 11(3) of the Act.

3. Aggrieved with the order of the Ld. AO, the assessee filed an appeal before the Ld. CIT(A). The Ld. CIT(A), after considering the submissions of the assessee, deleted the entire addition of Rs.13,76,58,674/-, holding that there was no accumulation under section 11(2) of the Act available for taxation under section 11(3) of the Act in the year under consideration.

4. Aggrieved by the order of the Ld. CIT(A), the Revenue is in appeal before the Tribunal and the assessee has filed cross-objections (“C.O.”). The grounds of appeal of the Revenue are as under :

“1. The order of the Ld. CIT(A) is erroneous both on facts and in law.

2. The decision of the Id. CIT(Appeals) in deleting the addition of Rs. 13,76,58,674/- is erroneous both in facts and in law.

3. The observation of the CIT(A) that exemption u/s.11 was granted upto the A.Y.1989-90 only and no exemption was granted for the A.Ys. 1991-92, 1992-93 and 1994-95 and hence provisions of section 11(2) are not applicable in respect of the income accumulated in these years is erroneous on the facts of the case.

4. The CIT(A) failed to see that for the A.Y.1991-92, the assessment was completed u/s.143(3) accepting the income returned by the assessee. It is erroneous on the part of the CIT(A) to observe that exemption was not granted for the A.Y.1991-92.

5. The observation of the CIT(A) that exemption u/s.11 was not granted for the A.Y.1992-93 is erroneous on the facts of the case. The CIT(A) failed to see that the Asst. for the A.Y.1992-93 was completed u/s.143(3) r.w.s.147 on 29.03.2000, without disallowing the exemption claimed by the assessee u/s.11.

6. The observation of the CIT(A) that exemption u/s.11 was not granted for the A.Y.1994-95 is erroneous on the facts of the case. The CIT(A) failed to see that the Asst. for the A.Y.1994-95 was completed u/s.143(3) r.w.s.147 on 29.03.2000, without disallowing the exemption claimed by the assessee u/s.11.

7. The decision the CIT(A) is erroneous both in facts and in law that the A.O. denied exemption against the income earned for the A.Ys. 1991-92, 1992-93 and 1994-95 and accordingly, the same can not be considered as accumulation u/s.11(2) of the 1.T.Act. The Id.CIT(A) failed to see that exemption was granted for all these years and hence provisions of Sec. 11(2) is applicable.

8. The Id.CIT(A) failed to appreciate that an amount of Rs. 15,54,18,245/accumulated from the earlier years was available for the A.Y.1995-96 to which the provision of Sec. 11(3) is applicable.”

5. At the outset, the Learned Departmental Representative (“Ld. DR”) submitted that the solitary issue arising from the grounds raised by the Revenue is the deletion of the addition of Rs.13,76,58,674/- by the Ld. CIT(A). The Ld. DR submitted that the Ld. CIT(A) erred in deleting the addition by holding that no accumulation under section 11(2) of the Act was available in the year under consideration for invoking section 11(3) of the Act. In this regard, the Ld. DR invited our attention to the computation of income filed by the assessee for A.Y. 1995-96, placed at page nos. 338 to 342 of the paper book. She specifically drew our attention to page nos. 338 and 339 of the paper book and submitted that at page no. 338, the assessee itself claimed utilisation of Rs.16,24,96,970/-out of accumulated income under section 11(2) of the Act of earlier years. Further, at page no. 339, the assessee furnished a detailed working showing brought forward of accumulated income, accumulation during the year, and utilisation thereof, and carry forward of the accumulated income to the next year. The Ld. DR contended that these computations clearly demonstrate that the assessee had accumulated income under section 11(2) of the Act in earlier years and the assessee had utilised the same during the year under consideration. Therefore, according to the Ld. DR, the finding of the Ld. CIT(A) that there was no brought forward accumulation till A.Y. 1994-95 is factually incorrect. She further submitted that once accumulation under section 11(2) of the Act is admitted by the assessee in its own computation, the provisions of section 11(3) of the Act become applicable, and the Ld. AO was justified in making the addition. Accordingly, she prayed that the order of the Ld. CIT(A) be set aside and that of the Ld. AO be restored.

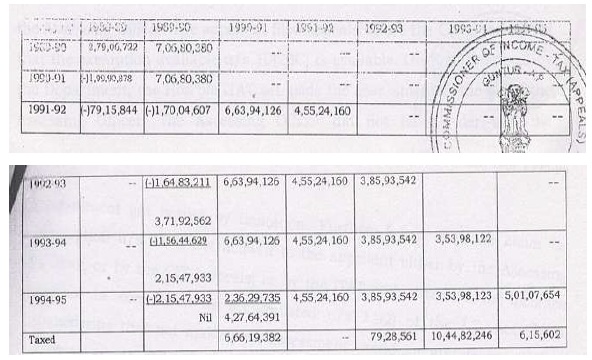

6. Per contra, the Learned Authorised Representative (“Ld. AR”) supported the order of the Ld. CIT(A) in detail. The Ld. AR submitted that the entire foundation of the Revenue’s case rests on an incorrect appreciation of facts relating to accumulation under section 11(2) of the Act in earlier years. He submitted that unless there exists a legally valid and subsisting accumulation under section 11(2) of the Act, no addition under section 11(3) of the Act can be made in the year under consideration. The Ld. AR submitted that the issue of accumulation under section 11(2) of the Act for the year under consideration is required to be check w.e.f. A.Y. 1989-90. In this regards the Ld. AR invited our attention to para no. 4.4 of the order of the Ld. CIT(A), wherein the Ld. CIT(A) in the order has reproduced a table containing the details of the amount of accumulation under section 11(2) of the Act of the assessee from A.Y. 1989-90 to A.Y. 1994-95. He further submitted that the Ld. CIT(A) after verifying the same, came to the conclusion that there was no brought forward accumulation till A.Y 1994-95 and therefore, no addition under section 11(3) of the Act can be made in the hand of the assessee in the year under consideration. He then explained the position year-wise as under:

| (a) |

|

For A.Y. 1988-89, the assessee had accumulated balance of Rs.2,79,06,722/- under section 11(2) of the Act at the end of A.Y. 1989-90. Out of the said accumulation, the assessee utilised Rs.1,99,90,878/- in A.Y. 1990-91 and Rs.79,15,844/- in A.Y. 199192. Thus, the entire balance accumulation for A.Y. 1988-89 stood at the end of A.Y. 1989-90 was fully utilised by A.Y. 1991-92, and no balance survived thereafter. |

| (b) |

|

For A.Y. 1989-90, the assessee had accumulated Rs.7,06,80,380/- under section 11(2) of the Act. The said accumulation of A.Y. 1989-90, the assessee utilised Rs.1,70,04,607/- in A.Y. 1991-92, Rs.1,64,83,211/- in A.Y. 199293, Rs.1,56,44,629/- in A.Y. 1993-94 and Rs.2,15,47,933/- in A.Y. 1994-95. Thus, the entire accumulation for A.Y. 1989-90 stood fully utilised by A.Y. 1994-95, and no balance survived thereafter. |

| (c) |

|

As far as the issue of accumulation from A.Ys. 1990-91 to 1992-93 is concerned, the Ld. AR submitted that the assessee was granted exemption under section 10(23C) of the Act for these years. He invited our attention to the exemption certificate placed at page nos. 726 & 727 of the paper book. He further invited out attention to the order of Ld. CIT(A) for A.Y. 1990-91 placed at page nos. 59 to 85 of the paper book as well as the order of Ld. CIT(A) for A.Y. 1992-93 placed at page nos. 140 & 141 of the paper book and submitted that the assessee’s claim of exemption under section 10(23C) of the Act for A.Ys. 1990-91 and 1992-93 was allowed by the Ld. CIT(A). He further submitted that the Revenue had filed appeal before the Tribunal against the said order of Ld. CIT(A) for A.Ys. 1990-91 & 1992-93. Further inviting our attention to the consolidated order of the Tribunal for A.Ys. 1990-91 & 199293 in ITA nos. 8 & 9/Hyd/2001 dated 24/08/2007, the Ld. AR submitted that, though the matter was set aside by the Tribunal to the file of the Ld. AO, no consequential orders were passed by the Ld. AO within limitation. Therefore, the orders of the Ld. CIT(A) granting exemption under section 10(23C) attained finality. For A.Y. 1991-92, though no appeal was filed by the assessee, the Ld. AR submitted that once exemption under section 10(23C) of the Act was accepted for A.Ys. 1990-91 and 1992-93, the same should be allowed for A.Y. 1991-92 also on the principle of consistency. In such circumstances, when the assessee is allowed exemption under section 10(23C) of the Act, the Ld. AR submitted that there was no question of any accumulation under section 11(2) of the Act for A.Ys. 1990-91 to 1992-93. (d) For A.Y. 1993-94, the Ld. AR invited our attention to the order of the Ld. AO for the year placed at page nos. 169 to 218 of the paper book and submitted that the entire receipts of the assessee for this year were taxed by the Ld. AO. The said action of the Ld. AO was ultimately upheld by the Hon’ble Andhra Pradesh High Court in 253 ITR 13 dated 28.03.2003. Therefore, no exemption under section 11 was allowed to the assessee for A.Y. 1993-94, and consequently, no accumulation under section 11(2) could arise for that year. (e) With regard to A.Y. 1994-95, the Ld. AR submitted that the case of the assessee for this year had reached to the Tribunal and the Tribunal vide it’s order in ITA no. 11/Hyd/01 dated 13/03/2009 had remanded the issue to the file of Ld. AO to redecide the issue. However, the consequential order pursuant to the Tribunal’s remand was not passed by the Ld. AO within limitation. Therefore, according to the Ld. AR no amount could be treated as accumulated under section 11(2) of the Act for the A.Y. 1994-95. |

7. Further, the Ld. AR also submitted that the reliance placed by the Ld. DR on the computation of income filed by the assessee for the A.Y. 1995-96, appearing at page nos. 338 to 342 of the paper book, is misplaced. He submitted that the said computation of income was prepared and filed without giving effect to the outcome of the appellate proceedings for A.Y. 1990-91 to 1994-95. Consequently, the balance of accumulation shown therein under section 11(2) of the Act and utilisation of the same during the A.Y. 1995-96 does not represent the correct legal position. The Ld. AR further submitted that, as already explained, the assessee did not have any balance of accumulation under section 11(2) of the Act up to the A.Y. 1994-95. Accordingly, the computation of income earlier filed by the assessee for the A.Y. 1995-96 requires suitable modification to that extent, as the accumulation reflected therein is not sustainable once the correct position emerging from the appellate proceedings is taken into account.

8. Finally, the Ld. AR submitted that the entire foundation of the Revenue’s case rests on an incorrect appreciation of facts relating to accumulation under section 11(2) of the Act in earlier years. He submitted that unless there exists a legally valid and subsisting accumulation under section 11(2) of the Act, no addition under section 11(3) of the Act can be made in the year under consideration. As no brought forward accumulation under section 11(2) of the Act survive till A.Y. 1994-95, no addition under section 11(3) of the Act can be made in the hand of the assessee in the year under consideration. Accordingly, he prayed before the bench to uphold the order of Ld. CIT(A).

9. We have carefully considered the rival submissions and perused the materials available on record. The controversy before us is confined to the existence and quantum of accumulation under section 11(2) of the Act which could be brought to tax under section 11(3) of the Act in the A.Y. 1995-96. In this regards it is crucial to go through the provisions of section 11(2) and 11(3) of the Act, which is to the following effect :

” Income from property held for charitable or religious purposes.

| 11. (1) |

XXXXXX |

XXXXXX |

XXXXX |

| (1A) |

XXXXXX |

XXXXXX |

XXXXX |

| (1B) |

XXXXXX |

XXXXXX |

XXXXX |

(2) Where seventy-five per cent of the income referred to in clause (a) or clause (b) of sub-section (1) read with the Expla nation to that sub-section is not applied, or is not deemed to have been applied, to charitable or religious purposes in India during the previous year but is accumulated or set apart, either in whole or in part, for application to such purposes in India, such income so accumulated or set apart shall not be included in the total income of the previous year of the person in receipt of the income, provided the following conditions are complied with, namely :—

(a) such person specifies, by notice in writing given to the Assessing Officer in the prescribed manner, the purposes for which the income is being accumulated or set apart and the period for which the income is to be accumulated or set apart, which shall in no case exceed ten years;

(b) the money so accumulated or set apart is invested or deposited in the forms or modes specified in sub-section (5):

Provided that in computing the period of ten years referred to in Clause (a), the period during which the income could not be applied for the purpose for which it is so accumulated or set apart, due to an order or injunction of any court, shall be excluded.

(3) Any income referred to in sub-section (2) which—

(a) is applied to purposes other than charitable or religious purposes as aforesaid or ceases to be accumulated or set apart for application thereto, or

(b) ceases to remain invested or deposited in any of the forms or modes specified in sub-section (5), or

(c) is not utilised for the purposes for which it is so accumulated or set apart during the period referred to in clause (a) or that subsection or in the year immediately following the expiry thereof, shall be deemed to be the income of such person of the previous year in which it is so applied or ceases to be so accumulated or set apart or ceases to remain so invested or deposited or, as the case may be, of the previous year immediately following the expiry of the period aforesaid.”

10. On perusal of above, it is evident that section 11(3) of the Act can be invoked only if there exists a legally valid, subsisting accumulation under section 11(2) of the Act from earlier years, and such accumulation is either not utilised within the prescribed period or is utilised otherwise than for the objects of the trust or institution. In this regard, the Ld. CIT(A) at para nos. 4.1 to 4.10 of its order has given categorical findings that no accumulation under section 11(2) of the Act is available in the year under consideration to be taxed under section 11(3) of the Act and accordingly directed the Ld. AO to delete the entire addition in the hands of the assessee. The para nos. 4.1 to 4.10 of the order of the Ld. CIT(A) is reproduced as under :

“4.1. I have carefully considered the submissions made by the appellant. The assessing officer taxed the amount by virtue of the provisions of Sec.11 (3) of the I.T. Act. The provisions of Sec. 11 (3) mention that any income referred to in sub section (2) of Sec.11 not utilized for the purpose for which it is accumulated or set apart or if the said amount is applied for the purposes other than charitable or for the purposes as aforesaid, it shall be deemed to be the income of such persons of the previous year, in which it is so applied or seized to be accumulated or set apart.

4.2. The conditions for application of Sec. 11 (3) are therefore:

(a) The amount accumulated should have been an amount referred to in Sec. 11 (2) of the I.T. Act. According to Sec.11 (2) where an assessee did not utilize 85% of the income for charitable or religious purposes in India during the previous year such income so accumulated to set apart would not be included in the total income of the previous year provided the assessee filed an application before the Assessing Officer for being set apart for investment in future.

(b) It clearly indicates that the appellant’s income should have been exempted in an earlier year, the amount of income, which could not be utilized, was allowed to be carried forward to the later year and in such later year, the said amount was misappropriated.

4.3. According to the provisions of Sec.11(3), the basic requirement is that the provisions of Sec. 11 should have been applied for the income relating to an earlier year and was accumulated in accordance with the provisions of sec. 11(2) of the Act and was set apart for the purposes of future utilization. The basic requirement is that the appellant should have got the exemption for such accumulated income u/s 11 for such accumulated income in the year in which such income arose. Further reading of Sec.11(3) clearly indicates that the amount mis-utilised for any other purposes other than charity alone could be treated as deemed income.

44. In the light of the provisions of Sec.11(3) of the 1.T. Act, it is first to be determined what would be the amount accumulated out of the income exempted u/s 11 of the 1.T. Act for the earlier years. For this purpose, I required the appellant to prepare a statement from the records available which provides the following information.

4.5. It is seen that the Assessing Officer granted exemption u/s 11 of the I.T. Act up to the assessment year 1989-90. From the assessment year 1990-91, the Assessing Officer denied exemption u/s 11 of the I.T. Act.

4.6. The Assessing Officer denied exemption u/s 11 and, therefore, the income earned for the years 1990-91; 1991-92; 1992-93, 199394 and 1994-95 cannot be considered as accumulated u/s 11(2) of the I.T. Act.

4.7. In the circumstances, no amount exempted under sec. 11 in the earlier years accumulated and is available for assessment for the assessment year 1995-96. This is precisely the contention of the appellant also. From the records of the Assessing Officer, it is clear that there is no accumulated amount available.

4.8. Even otherwise, I find that the income up to the assessment year 1990-91 was already taxed or was utilized by the assessment year 1994-95. Therefore, the receipts up to the assessment year 1990-91 cannot be considered as available for the assessment year under consideration. The income for the assessment year 1991-92 and 1992-93 was not exempted by the Assessing Officer. The appellant filed appeals before the CIT(A) who held that the exemption available u/s 10(23C) is available. On further appeal by the Department, the Hon’ble ITAT set aside the assessment to the file of the Assessing Officer. The Assessing Officer did not pass order and the assessment got barred by limitation. Further, I find that the claim for exemption u/s 11 is not allowed to the appellant either by the Assessing Officer, or by the CIT (appeals) or by the ITAT and, therefore, the incomes cannot be considered as accumulated u/s 11(2) of the 1.T. Act. Even considering that not making an assessment would amount to granting of exemption as claimed, for the assessment years 1991-92, 1992-93 and 1993-94, the aggregate amount earned was Rs.11,15,87,283/. As against this amount, the Assessing Officer already taxed Rs. 79,28,561/-for the Assessment Year 1992-93 and Rs. 10,44,82,246/- for the Assessment Year 1993-94. The aggregate amount of taxed income works out to Rs. 11,24,10,807/-. Therefore, the entire amount is to be considered as already taxed.

4.9. For the Assessment Year 1994-95, the Assessing Officer taxed an income of Rs.6,50,602/- but did not allow exemption u/s 11 of the Act. Therefore, no accumulation permitted u/s 11(2) is available to be taxed u/s 11(3) of the I.T. Act.

4.10. Therefore, I agree with the contention of the appellant that the provisions of Sec.11 (3) have no application at all to the amount utilized by the appellant. Therefore, I have to hold that no part of the amount is available to be taxed u/s 11(3) of the I.T. Act. Accordingly, the entire amount added by the Assessing Officer is directed to be deleted.”

11. Keeping the aforesaid legal framework and the findings of the Ld. CIT(A) in mind, we proceed to examine the facts year-wise, as argued by the Ld. AR and disputed by the Revenue. In this regard we have gone through the para no. 4.4 of the order of the Ld. CIT(A), wherein the Ld. CIT(A) in the order has reproduced a table containing the details of the amount of accumulation under section 11(2) of the Act of the assessee from A.Y. 1989-90 to A.Y. 1994-95, which has been reproduced herein above. On the basis of the said table, the Ld. AR has submitted that for A.Y. 1988-89, the assessee had accumulated balance of Rs.2,79,06,722/- under section 11(2) of the Act at the end of A.Y. 1989-90. It was further submitted that out of the said accumulation, the assessee utilised Rs.1,99,90,878/- during A.Y. 1990-91 and the balance amount of Rs.79,15,844/- during A.Y. 1991-92. In this regard we have gone through the computation of income of the assessee for the A.Ys. 1989-90 to 1991-92. On perusal of same, as placed in the paper book, we find that the utilisation claimed by the assessee tallies with the accumulation made for A.Y. 1988-89. Thus, the entire accumulation for A.Y. 1988-89 stood fully exhausted by A.Y. 1991-92. In view of the said factual verification, we hold that no accumulation pertaining to A.Y. 1988-89 survived beyond A.Y. 1991-92, and therefore, no amount relatable to A.Y. 1988-89 could form part of any carry forward accumulation for the year under consideration.

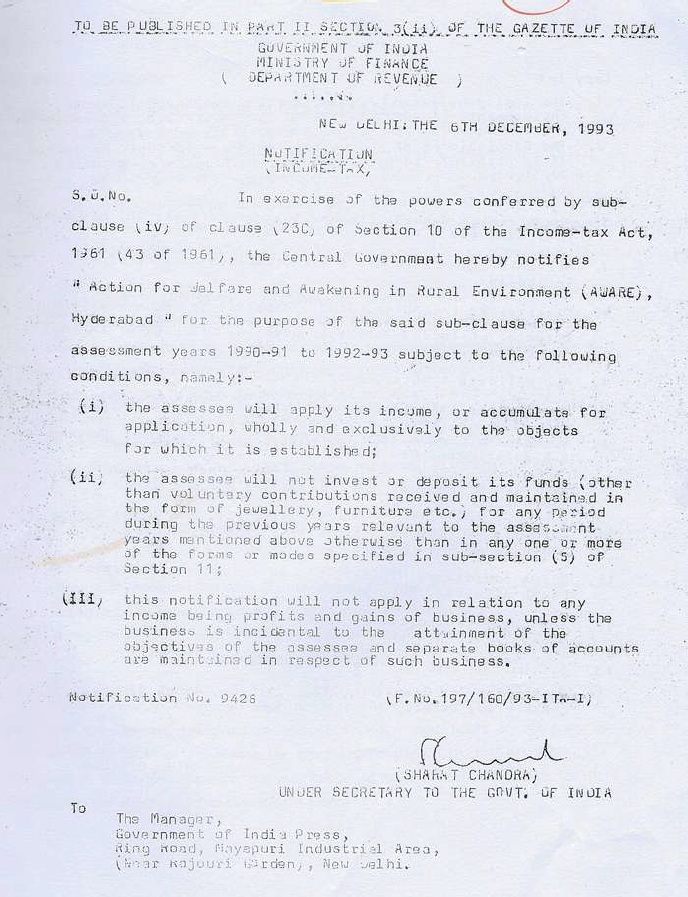

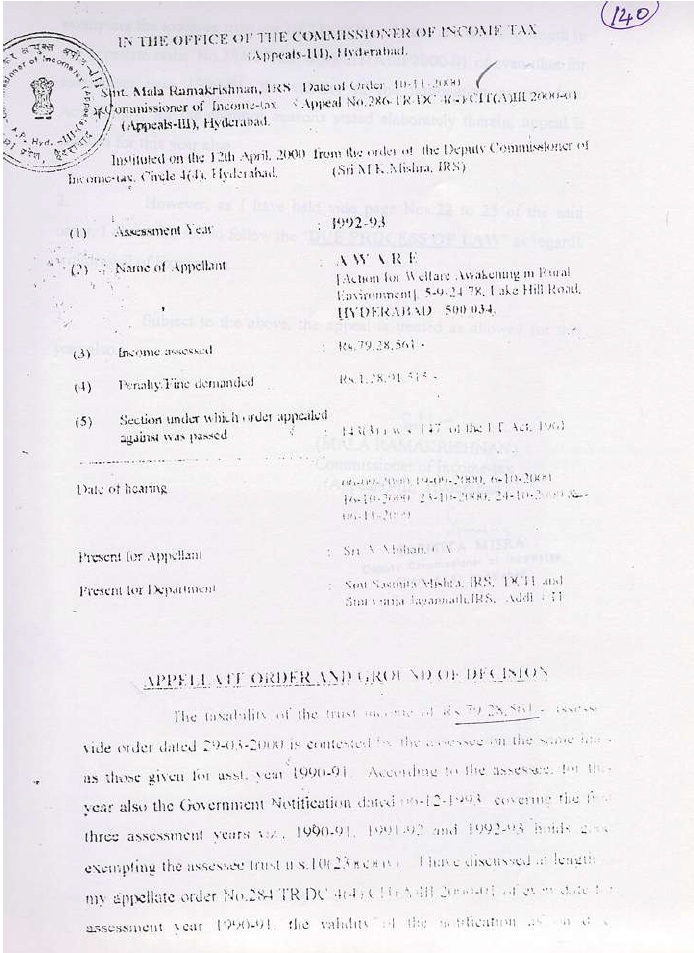

12. On the basis of the very same table, the Ld. AR has submitted that for A.Y. 1989-90, the assessee accumulated an amount of Rs.7,06,80,380/- under section 11(2) of the Act. He has further demonstrated, with reference to the year-wise utilisation statements that the said accumulation of A.Y. 1989-90, the assessee utilised Rs.1,70,04,607/- in A.Y. 1991-92, Rs.1,64,83,211/- in A.Y. 1992-93, Rs.1,56,44,629/- in A.Y. 1993-94 and Rs.2,15,47,933/- in A.Y. 199495. Thus, the entire accumulation for A.Y. 1989-90 stood fully utilised by A.Y. 1994-95, and no balance survived thereafter. In this regards we have verified the above figures with reference to the computation statements and utilisation schedules placed on record. On such verification, we find that the utilisation figures correspond exactly with the accumulation created in A.Y. 1989-90 and that the entire accumulation stood fully utilised by A.Y. 1994-95. Accordingly, we hold that no accumulation pertaining to A.Y. 1989-90 was available as brought forward accumulation in A.Y. 1995-96, and therefore, no part of the accumulation of A.Y. 1989-90 could be subjected to tax under section 11(3) of the Act in the year under consideration.

13. For A.Ys. 1990-91 to 1992-93, the Ld. AR has submitted that the assessee was granted exemption under section 10(23C) of the Act. In support of this contention, reliance was placed on the exemption certificate issued to the assessee, placed at page nos. 726 & 727 of the paper book, which is to the following effect:

14. It has also been submitted by the Ld. AR that the assessee’s claim of exemption under section 10(23C) for A.Ys. 1990-91 and 1992-93 was allowed by the Ld. CIT(A). In this regard we have gone through the para nos. 5.17 to 6 of the order od Ld. CIT(A) for A.Y. 1990-91 placed at page no. 85 of the paper book and the order of the CIT(A) for A.Y. 1992-93 placed at page nos. 140 & 141 of the paper book, which are to the following effect :

para nos. 5.17 to 6 of the order of Ld. CIT(A) for A.Y. 1990-91 :

“5.17. In lieu of the foregoing reasons, I hold that currently the appellant trust is entitled to the exemption granted vide the Govt. of India Notification filed before me u/s.10(23)(c)(iv) for the three assessment. years commencing from assessment year 1990-91 to 1992-93.

5.18. As regards the other minor additions made by the Assessing Officer cited supra, the replies given by the appellant reveals production of some sort of an evidence for the expenditure incurred. The taxability of these petty “unvouched expenditure” is not taken up by me for discussion of holding it as genuine or not as the same are also currently covered under the exemption granted by the Govt. of India Notification. However, if the Assessing Officer decides to withdraw the exemption through “due process of law” he may follow my directions contained in my appellate order for the assessment year 1995-96 on “unvouched expenditure”. Accordingly, this issue is restored.

6. In the result, the appeal is treated as allowed.”

Order of the CIT(A) for A.Y. 1992-93 :

15. On perusal of above, we find that the CIT(A) has given the categorical findings that the assessee is eligible for exemptions under section 10(23C) of the Act for A.Ys. 1990-91 to 1992-93 and allowed the exemptions to the assessee for A.Ys. 1990-91 and 1992-93 and accordingly allowed the appeals of the assessee for both these years. It has also been submitted by the Ld. AR that though the Revenue carried the matter for A.Ys. 1990-91 & 1992-93 to the Tribunal and the issue was set aside to the file of the Ld. AO, it is an admitted position that no consequential orders were passed by the Ld. AO within the period of limitation. The Revenue has also not disputed these facts before us. As no consequential orders were passed by the Ld. AO for A.Ys. 1990-91 & 1992-93 within the period of limitation, in our considered view, the orders of the Ld. CIT(A) granting exemption under section 10(23C) attained finality. Further, as the assessee has also been granted exemption certificate for A.Y. 1991-92 also, in our considered view, applying the principle of consistency the income the income of the assessee for A.Y. 1991-92 is also eligible for exemptions under section 10(23C) of the Act. Accordingly, once the assessee is governed by section 10(23C) of the Act for these three years, the question of accumulation under section 11(2) of the Act does not arise at all for A.Ys. 1990-91 to 199293, as the scheme of section 11(2) of the Act operates only when exemption is claimed under section 11 of the Act. Accordingly, we hold that for AYs 1990-91, 1991-92 and 1992-93, there was no accumulation under section 11(2) of the Act which could be brought to tax under section 11(3) of the Act.

16. For A.Y. 1993-94, the Ld. AR has submitted that the entire receipts of the assessee were taxed by the Ld. AO, and no exemption under section 11 of the Act was allowed. In this regard, we have gone through the relevant paragraphs of order of the Ld. AO placed at page nos. 207 of the paper book, which is to the following effect:

“Under these circumstances it is clear that the money advance by the AWARE of Rs.2.00 lakhs to the AOP is actually routed through the AOP (Which was formed to purchase the land for cancer hospital as explained by Sri Madhavan) to advance the money for the purchase of the property Vishakhapatanam By Sri Madhavan, thus utilising the trust money for the personal me This transaction also violates the provision of Sec 13(1)(c)(u) read with section 13(2)) no Sce (3) (d)

Thus in this assessment year on two occasions the provisions of Sec 13(1) Mit) road wit section 13(2)(b) and Sec 13 (3) (d) were violated. The total receipt which is income as rier die Sec 11 and 12 of the LT. Act is to the tune of Rs 9,99,62,664.00 and it has to be taxed in the AY 93-94.

Hence the total receipt of the trust is brought to Tax.

Addition: Rs. 9,99,02,664.00″

17. On perusal of above, it is evident that the Ld. AO has treated the total receipts of the assessee for A.Y. 1993-94 amounting to Rs. 9,99,62,664/- as income in the hands of the assessee. It was further pointed out that the said action of the Ld. AO was ultimately upheld by the Hon’ble Andhra Pradesh High Court in Action for Welfare & Awakening in Rural Environment (AWARE) v. Dy. CIT ITR 13 (Andhra Pradesh) dated 28.03.2003. The relevant para nos. 12 to 14 of the order of the Hon’ble Andhra Pradesh High Court is reproduced as under :

“12. Learned counsel for the revenue emphatically submitted that the question of examining the reasonableness and proportionality of the amount of money that should be brought to tax does not arise.

It is also argued on behalf of the appellant that this is a sole incident of misutiliztion of funds without there being any intention on the part of the assessee. Thus, this need not be taken very seriously for the amounts with which it deals with are nowhere can be compared with that of the amounts sought to be misutilized. This argument cannot hold good for the reason that for the purpose of the Act, every assessment year is a separate cause of action and neither the earlier nor the subsequent conduct of the assessee can be taken into consideration. The interpretation that requires to be given is strictly in the teeth of the provisions of the Act. In this case, the misutilization is glaring and it cannot escape the clutches of law, nor any sympathy or equities can be extended particularly for an organization, which receives donations purely for the welfare of the under privileged and needy class of the society.

Further it is noticed that the entire transaction was conducted by Babu Reddy behind the back of the assessee and the assessee or Madhavan were aware of the transactions. This was not believed by the authorities below. On the other hand, it was found that the top management of AWARE was well aware of the transaction from the very beginning. It is also noticed by the authorities below that the assessee came to know of the irregularities in the matter on 24-3-1994. It is surprising to note that Babu Reddy was continued in service upto May, 1995, i.e., one year four months thereafter. Further, as pet-the record, one instalment of repayment was deposited in the bank on 5-2-1998 by Satyanarayana, Assistant Cashier of AWARE. It is not the case of the assessee that Satyanarayana also played a fraud in the transactions. Further, though the irregularity was noticed by the assessee on 24-3-1984, no immediate action was taken by it against Babu Reddy. It is further noticed that it was more likely that after Delhi High Courts order dated 9-11-1998 and subsequent deep investigations by M/s. Batliboi & Company, the assessee tried to cover up its tracks by falsely claiming that Babu Reddy had undertaken the transaction fraudulently and created misleading evidence by filing false cases against Babu Reddy and to cover up the misdeeds of the Chairman of the Trust in siphoning off and misusing trust funds Babu Reddy was made a scapegoat. In fact, Babu Reddy made a clear statement that he air-ranged the loan on the direction of Madhavan after completion of all the formalities required by the bank for obtaining the loan of Rs. 12 lakhs against the pledge of FDRs of Rs. 16 lakhs belonging to the assessee. It is also proved from the record that the four pay orders of Rs. 3 lakhs each were prepared and given to Smt. Rama Anantram on the instructions of Madhavan. It has been admitted by Smt. Rama Anantram in her statement that she received the said money and utilized (lie same by her for the salaries, phone bills and office administrative expenditure of M/s. Omnitel Industries Limited, a company run by her husband-Anantram and she repaid the loan amount with interest totalling to Rs. 14,25,756, Viewed from any angle, the only conclusion that could be reached is that tile whole transaction was within the personal knowledge of the trustees and there is no scope to infer that the Chairman and other trustees are not aware of the same. In fact, it is a case where the funds of the trust were diverted and misutilized deliberately.

The further contention of the appellant that proper opportunity was not given to cross-examine the Government Examiner of Questioned Documents cannot be believed as it had riot summoned or stated specifically that it wanted to cross-examine him. In fact, when the opportunity was given cross-examine, it has failed establish its case that the opinion of the said Examiner is incorrect. Apart from this, all the questions raised are not substantial questions of law as contemplated under section 260A of the Act. They are mere questions of fact and the authorities below have taken on c plausible view and as such, it is not for this court to interfere into such findings of fact.

13. Insofar as the finding that for the purchase of land AWARE routed the entire transaction through association of persons in which all the members were directors and employee of AWARE is concerned, some amounts were paid directly to the land owner by AWARE, but an amount of Rs. 49,24,343 was paid to association of persons for the purchase of a property by K. Madhavan (in his personal capacity) an amount of Rs. 2 lakhs was advanced by AWARE to association of persons; thus, utilizing the trust money for personal gain. This is a pure question of fact and this court cannot interfere into the same under section 260A of the Act.

14. For all these reasons, the appeal fails and neither there is any perverse of finding of facts nor error apparent on the face of record. The order passed by the appellate authority is perfectly valid and justified in the circumstances of the case. Thus the appeal is dismissed; but, in the circumstances, without costs.

18. On perusal of above, it is evident that the Hon’ble High Court has upheld the action of the Ld. AO resulting in the denial of exemption under section 11 to the assessee for the A.Y. 1993-94. Therefore, in our considered view, once the entire receipts were brought to tax and exemption under section 11 of the Act was denied for A.Y. 1993-94, there could be no occasion for any accumulation under section 11(2) of the Act for that year under consideration. Accordingly, we hold that no accumulation under section 11(2) of the Act arose for A.Y. 199394, and consequently, no amount relatable to A.Y. 1993-94 could be treated as accumulated income for the year under consideration.

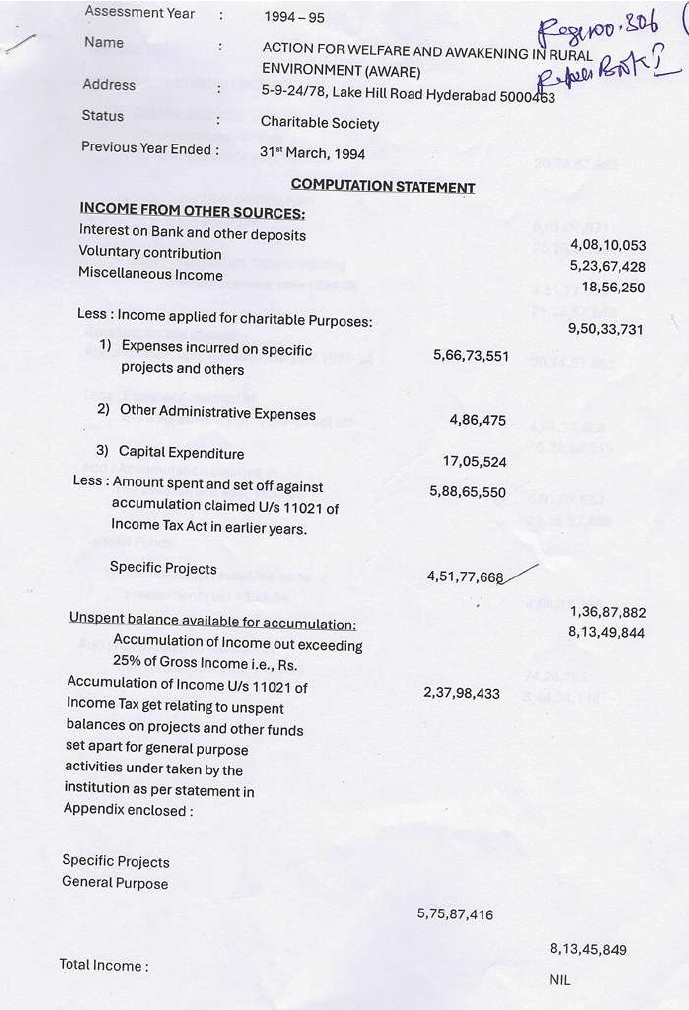

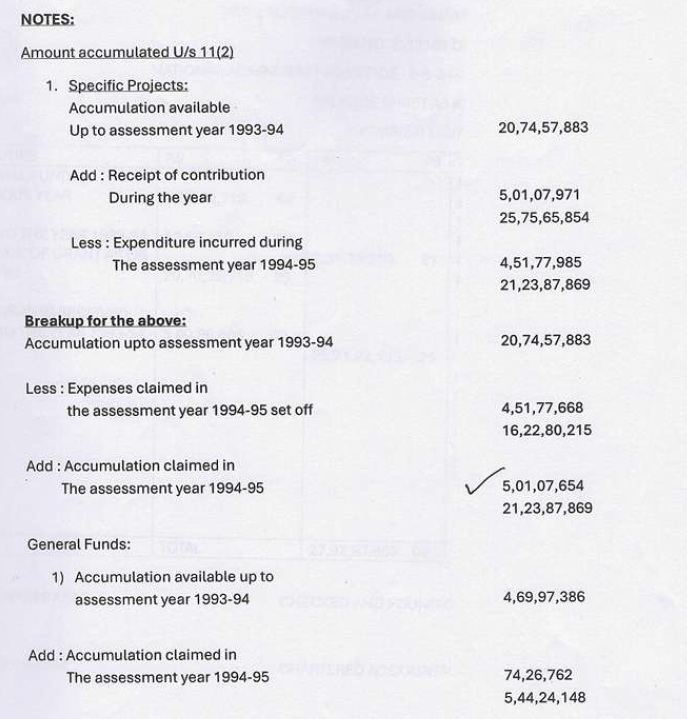

19. Coming now to A.Y. 1994-95, the Ld. AR has submitted that the case of the assessee for this year had reached to the Tribunal and the Tribunal vide it’s order in ITA No. 11/Hyd/01 dated 13/03/2009 had remanded the issue to the file of Ld. AO to redecide the issue. However, the consequential order pursuant to the Tribunal’s remand was not passed by the Ld. AO within limitation. Therefore, according to the Ld. AR no amount could be treated as accumulated under section 11(2) of the Act for the A.Y. 1994-95. Further, the Ld. CIT(A) at para no. 4.9 of it’s order has given the findings that, no accumulation permitted under section 11(2) of the Act is available to taxed under section 11(3) of the Act for the A.Y. 1994-95. In this regard, we have gone through the order of Ld. AO for the A.Y. 1994-95 placed at page nos. 309 to 317 of the paper book. On perusal of same, we find that the Ld. AO has not disturbed the claim of exemption under section 11 of the Act of the assessee and the issue regarding of exemption under section 11 of the Act was not the subject matter of the appeal before the Tribunal in earlier proceedings. In the assessment, the Ld. AO had only disallowed Rs. 6,15,602/- towards certain expenditure due to absence of adequate evidence. In such circumstances, merely because the Ld. AO failed to pass a consequential order pursuant to the Tribunal’s remand, it cannot be held that the accumulation allowed under section 11(2) of the Act in the original assessment ceased to exist. Therefore, we are not in agreement with the submission of the assessee as well as the findings of the Ld. CIT(A) that no accumulation permitted under section 11(2) of the Act is available to taxed under section 11(3) of the Act for the A.Y. 1994-95. Further, we have gone through the computation of income of the assessee for A.Y. 1994-95 placed at page nos. 306 and 307 of the paper book, which is to the following effect :

20. On perusal of above, we find that during A.Y. 1994-95, the assessee had total receipts of Rs.9,50,33,731/-. As per the statutory requirement applicable for the relevant year, the assessee was required to apply 75% of the total receipts, amounting to Rs.7,12,75,298/-, towards the objects of the society. However, it is evident from the above that the assessee had actually applied only Rs.5,88,65,550/- during the said year. The difference between the required application and the actual application thus works out to Rs.1,24,09,748/-. Therefore, in our considered view, this differential amount alone represents the maximum possible accumulation under section 11(2) of the Act for A.Y. 199495. Accordingly, we hold that for A.Y. 1994-95, the only accumulation under section 11(2) of the Act which can be recognised in law is Rs.1,24,09,748/, and no amount in excess thereof can be treated as accumulated income.

21. Further, the Ld. DR has contended that as per the computation of income filed by the assessee for A.Y. 1995-96, placed at page nos. 338 to 342 of the paper book, the assessee itself claimed utilisation of Rs.16,24,96,970/- out of accumulated income under section 11(2) of the Act of earlier years. Therefore, the Ld. DR argued that the findings of the Ld. CIT(A) and the contention of the Ld. AR that no accumulation under section 11(2) was available in the year under consideration for invoking section 11(3) of the Act is factually not correct. In this regard, we find merits in the submission of the Ld. AR that the said computation of income was prepared and filed without giving effect to the outcome of the appellate proceedings for A.Ys. 1990-91 to 1994-95. Consequently, the balance of accumulation shown therein under section 11(2) of the Act and utilisation of the same during the A.Y. 1995-96 does not represent the correct legal position and it requires suitable modification to that extent. Further, in our above observations, we have also find that as far as A.Ys. 1988-89 to 1993-94 is concerned, no accumulation permitted under section 11(2) of the Act is available to taxed under section 11(3) of the Act in the A.Y. 1995-96. However, as far as A.Y. 1994-95 is concerned, we have find that there exist an accumulated amount of Rs. 1,24,09,748/- under section 11(2) of the Act which has been brought forward for utilisation in A.Y. 1995-96. Accordingly, we partly accept the contention of the Ld. DR to the extent of Rs. 1,24,09,748/-, that there exist an accumulated amount under section 11(2) of the Act which has been brought forward for utilisation in A.Y. 1995-96.

22. On the basis of the above facts and discussion, as far as A.Ys. 1988-89 to 1993-94 is concerned, we find no infirmity in the findings of the Ld. CIT(A) that no accumulation permitted under section 11(2) of the Act is available to taxed under section 11(3) of the Act. However, as far as A.Y. 1994-95 is concerned, we are of the considered view that, the assessee has accumulated an amount of Rs. 1,24,09,748/- under section 11(2) of the Act and has been brought forward and utilised in A.Y. 1995-96. However, as far as the taxability of the accumulated balance of Rs. 1,24,09,748/- under section 11(3) of the Act in A.Y. 1995-96 is concerned, the Ld. AO has made the addition in A.Y. 1995-96 on the footing that the accumulated funds were either not utilised or were misutilised, whereas the Ld. CIT(A) deleted the addition solely on the ground that no accumulation existed. Hence, we find that the Ld. CIT(A) did not examine the factual aspect of utilisation, namely whether the accumulated amount of A.Y. 1994-95 was utilised during A.Y. 1995-96 in accordance with the objects of the society. Since this aspect goes to the root of applicability of section 11(3) of the Act, and since no categorical finding has been recorded by the Ld. CIT(A) on this issue, we are of the view that this limited issue requires fresh examination. Accordingly, in view of the detailed year-wise verification carried out by us, we hold as under:

| i. |

|

There was no subsisting accumulation under section 11(2) of the Act pertaining to A.Ys.1988-89 to 1993-94. |

| ii. |

|

Only the accumulation to the extent of Rs. 1,24,09,748/- pertaining to A.Y. 1994-95 can be considered as available accumulation for the purpose of section 11(3) of the Act in A.Y. 1995-96. |

| iii. |

|

The issue whether the said accumulation was utilised in accordance with the objects of the society during A.Y. 1995-96 requires verification. |

Accordingly, this limited issue is restored to the file of the Ld. CIT(A) for fresh adjudication in accordance with law after providing due opportunity of being heard to both parties.

23. In the result, the appeal of the Revenue in ITA No. 709/Hyd/2012 is partly allowed for statistical purposes.

C.O. No. 138/Hyd/2012 (C.O. of the assessee) :

24. The revised cross-objections filed by the assessee are as under:

“1. The learned CIT (Appeals) ought to have considered the fact that there was no mis-utilization of any of the amounts as held by the Assessing Officer.

2. The learned CIT (Appeals) ought to have deleted the addition on the ground that there was no misutilisation of amounts and also on the ground that the provisions of Sec. 11(3) have no application.

3. The learned CIT (Appeals) erred in not holding that interest u/s 234B of the I.T.Act cannot be charged under the circumstances.

25. Under grounds No. 1 and 2 of the C.O., the assessee has objected that the Ld. CIT(A) ought to have decided that the entire funds of the assessee were utilised strictly for achieving the objects of the society and that there was no misutilisation of funds at any point of time. In this regard, we note that in ITA No. 709/Hyd/2012, arising out of the appeal filed by the Revenue, we have already recorded a finding that the Ld. CIT(A) had not examined the factual aspect relating to the alleged misutilisation of funds by the assessee. Therefore, in ITA No. 709/Hyd/2012, the issue relating to alleged misutilisation of funds was set aside to the file of the Ld. CIT(A) for fresh adjudication in accordance with law, after examining the factual aspects in detail. In view of the said finding already rendered in the Revenue’s appeal, grounds No. 1 and 2 raised by the assessee in the present C.O. stand covered by the remand direction issued to the Ld. CIT(A) and do not require independent adjudication at this stage.

26. Under ground No. 3 of the C.O., the SSC has objected to the levy of interest under section 234B of the Act by the Ld. AO. On perusal of the provisions of section 234B of the Act, we find that the levy of interest under the said section is mandatory and consequential in nature. Once the conditions prescribed under the statute are satisfied, the charging of interest under section 234B follows as a matter of law and does not require any separate adjudication on merits. Accordingly, ground No. 3 raised by the assessee is dismissed.

27. In the result, the C.O. filed by the assessee is partly allowed for statistical purposes.

28. To sum up the appeal of the Revenue and the C.O. of the assessee are partly allowed for statistical purposes.