HOW TO REPORT GIFT FROM PARENT IN ITR AY 2026-27

Video on HOW TO REPORT GIFT FROM PARENT IN ITR AY 2026-27

Steps to Report the Gift on the Income Tax Portal

- Log In: Access the official Income Tax e-Filing Portal.

- Navigate to Personal Information: Go to your active ITR form (ITR-1 or ITR-2).

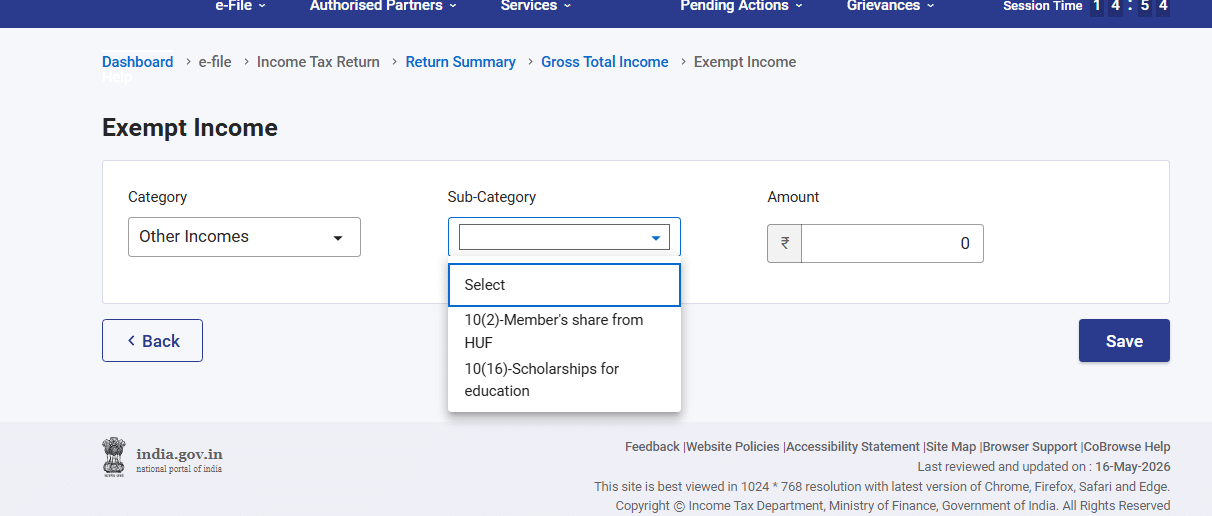

- Locate Exempt Income: Go to the Schedules or Income Details tab and find Schedule EI (Exempt Income).

- Add New Entry: Click on ‘Add Details’ under Exempt Income.

- Select Income Nature: From the dropdown menu, select “Others”.

- Provide Description: Enter a clear remark such as: “Gift received from relative (Father/Mother) – exempt under Section 56(2)(x)”.

- Enter Amount: Input the exact valuation or cash amount received and click save.

Reporting Gifts from relative in ITR forms

ITR forms, do not explicitly contain the tax rules regarding gifts.gifts received from parents (who fall under the definition of “relatives”) are completely exempt from income tax.

Because a gift from a parent is not chargeable to tax, you do not report it under standard income heads. Instead, you must report it under the specific “Exempt Income” reporting sections of your chosen ITR form for Assessment Year 2026-27.

Here is exactly where to report this exempt gift depending on the form you file:

- In ITR-1 (Sahaj): You must declare this under Part C (Deductions and Taxable Total Income) in field C3: “Exempt Income For reporting purpose and Income on which no tax is payable.” The e-filing utility will provide a drop-down menu for you to specify the nature of the exempt income under section 10 of Income Tax act. But Gifts from parents is not taxable as per Section 56(2)(x , hence it can not be reported here. You should keep the documents ready for gifts in case inquiry comes from income tax department.

- In ITR-2: You must report this in Schedule EI (Details of Exempt Income). Specifically, you will list it under field 3: “Other exempt income (including exempt income of minor child) (please specify)”. It is used to report exempt income under section 10 of Income Tax act. But Gifts from parents is not taxable as per Section 56(2)(x) of Income Tax act 1961 , hence it can not be reported here. You should keep the documents ready for gifts in case inquiry comes from income tax department.

- In ITR-3: Similar to ITR-2, this must be reported in Schedule EI (Details of Exempt Income) under field 3: “Other exempt income (including exempt income of minor child) (please specify)”. It is used to report exempt income under section 10 of Income Tax act.But Gifts from parents is not taxable as per Section 56(2)(x) of Income Tax act 1961 , hence it can not be reported here. You should keep the documents ready for gifts in case inquiry comes from income tax department.

- In ITR-4 (Sugam): You must declare this under Part D (Tax Computations and Tax Status) in field D20: “Exempt income only for reporting purposes… and Income on which no tax is payable.” You will use the provided drop-down menu to mention the nature of the exempt income.It is used to report exempt income under section 10 of Income Tax act. But Gifts from parents is not taxable as per Section 56(2)(x) of Income Tax act 1961 , hence it can not be reported here. You should keep the documents ready for gifts in case inquiry comes from income tax department.

(Note: If you were receiving a taxable gift—such as a large sum of money from a non-relative— that it would instead be reported under “Schedule OS: Income from Other Sources” as income referred to in section 56(2)(x). However, since this is from a parent, it goes in the Exempt Income sections mentioned above).

Crucial Reporting Rules and Restrictions

| Gift Category | Mode of Transfer | Tax/Reporting Rule |

|---|---|---|

| Monetary Gift | Bank Transfer (NEFT/RTGS/IMPS) | Fully exempt. Recommended to report in Schedule EI if amount is large. |

| Cash Gift | Physical Cash | Do not accept cash gifts of ₹2 Lakhs or more. Section 269ST prohibits cash transactions above ₹2 Lakhs and carries severe penalties equal to the cash amount received. |

| Movable Property | Jewellery, Shares, etc. | Fully exempt. Report the Fair Market Value (FMV) in Schedule EI. |

| Immovable Property | House, Land, Flat | Fully exempt. Property gifts valued above ₹45 Lakh are automatically tracked via the Statement of Financial Transactions (SFT). Ensure you file ITR-2 or higher to reflect property shifts. |

Keep This Documentation Ready

- Gift Deed: For high-value amounts or any real estate, execute a formal gift deed on stamp paper detailing the donor, recipient, relationship, and lack of consideration.

- Bank Statements: Retain bank passbooks showing the clean trail of funds from your parent’s account to your account.

- Donor Creditworthiness: Ensure your parents can explain their source of funds in their own tax profiles if audited.