ORDER

Girish Agrawal, Accountant Member. – Present appeal filed by the assessee is against the order passed by ld. CIT(A) under section 250 vide order dated 7.10.2025 for A.Y. 2022-23.

2. Grounds of appeal raised by the assessee read as under:

Ground of Appeal No. 1: General

1. erred in upholding the assessed income of Rs. 2,65,09,80,230 as against the returned income of Rs. 1,04,15,22,410

Ground of Appeal No. 2: Improper dismissal of appeal as not maintainable:

2. erred in dismissing the Appellant’s appeal as not maintainable on the merely on the basis that a rectification application as well as an appeal has been filed against the intimation under section 143(1) of the Act without appreciating that the issue pertaining to addition under section 35(1)(iv) of the Act amounting to Rs. 1,17,96,086 was unique only to the impugned appeal.

Ground of Appeal No. 3: Addition under section 145A of the Act – Rs. 159,76,61,725:

3. failed to appreciate that the addition amounting to Rs. 1,59,76,61,725 has been made under section 145A of the Act without allowing the corresponding decrease in profit amounting to Rs. 1,59,76,61,725 in terms of section 145A of the Act which has also been reported in the Tax Audit Report and therefore, the addition is bad in law and ought to have been deleted.

Ground of Appeal No. 4: Disallowance under section 35(1)(iv) of the Act – Rs. 1,17,96,086:

4. failed to appreciate that the proposed disallowance under section 35(1)(iv) of the Act amounting te Rs. 1,17,96,086 was not made in the intimation order under section 143(1) of the Act dated 27 Jul 2023 but the learned assessing officer while passing the impugned order under section 143(3) rea with 1448 of the Act dated 30 March 2024 has inadvertently considered the same in the computation sheet while computing the total income and therefore, the same ought to have been deleted.

Ground of Appeal No. 5: Levy of interest under section 234B of the Act -Rs. 8,97,61,008:

5. erred in levying interest amounting to Rs. 8,97,61,008 under section 234B of the Act:

Ground of Appeal No. 6: Levy of interest under section 234C of the Act – Rs. 35,91,272:

6. erred in levying interest amounting to Rs. 35,91,272 under section 234C of the Act.

3. Moot point raised by the ld. Counsel for the assessee in the present appeal is on account of dismissal of first appeal by CIT(A) as not maintainable by observing that a separate appeal against intimation issued under section 143(1) of the Act, filed by the assessee is pending for adjudication and also noting about the pendency of rectification application filed under section 154 of the Act. He further noted in this regard that relief sought by the assessee is already under consideration by way of rectification application and therefore, relief sought in the appeal filed against the order passed under section 143(3) of the Act does not arise.

4. Facts in this regard as sculled out from the records are that assessee had filed its return of income on 30.11.2022, reporting total income at Rs. 104,15,22,410/-. This return of income was processed by the Centralized Processing Centre of the Department, Bengaluru (CPC) and intimation under section 143(1) was issued dated 29.07.2023 whereby total income was determined at Rs. 263,91,84,140/- by making adjustment pertaining to increase/decrease in profit because of deviation in the method of valuation as per section 145A of the Act discussed in clause 14(b) of Form 3CD (tax audit report). Most clinching fact pertaining to the present appeal which is arising out of the assessment order passed under section 143(3) subsequent to the processing of return under section 143(1) is that notice under section 143(2) was issued on 02.06.2023 which is prior to the date of processing of return under section 143(1). Case of the assessee was selected for scrutiny assessment on 02.06.2023 and return was processed subsequently, under section 143(1) on 29.07.2023 wherein an upward adjustment was made of Rs. 159,76,61,725/-, resulting into demand of Rs. 45,20,88,480/-.

5. In this regard, strong reliance was placed by the ld. Counsel on the decision of Hon’ble Supreme Court in the case of CIT v. Gujarat Electricity Board 260 ITR 84 (SC), which held that where summary procedure under section 143(1) has been adopted, there should be scope available for the revenue, either suo moto or at the instance of the assessee, to make a regular assessment under section 143(2) of the Act. Hon’ble Court held that converse is not available as regular assessment proceeding having been commenced under section 143(2), there is no need for a summary proceeding under section 143(1)(a). The appeal filed by the Revenue was thus dismissed.

5.1. Hon’ble jurisdictional High Court of Bombay in the case of Spaco Carburettors India Ltd. v. Raj Kumar, Dy. CIT 284 ITR 611 (Bombay) followed the decision of Hon’ble Supreme Court in the case of Gujarat Electricity Board (supra), which held that the AO is not justified in issuing intimation under section 143(1)(a) after issuance of notice for regular assessment under section 143(2) of the Act.

5.2. Useful reference is also made to the decision of Coordinate Bench of the ITAT, Kolkata in the case of SRBC & Co. LLP v. Dy. CIT [IT Appeal No. 236/Kol/2022, dated 24-11-2022] , wherein similar issue has arisen and it was held that once assessment order under section 143(3) has already been passed, intimation under section 143(1) gets merged with the aforesaid assessment order. Relevant paragraph from this decision is extracted below for ready reference:-

“5. From the perusal of the assessment order passed u/s. 143(3) of the Act, we note that Ld. AO has proceeded to compute the assessed income by making an addition to the returned income of the assessee and not the income processed u/s. 143(1) of the Act. However, it is noted that in the said order u/s. 143(3) of the Act, there is no addition made in respect of dividend income received from investment in units of mutual funds u/s. 115BBDA of the Act. We note that since the assessment order u/s. 143(3) of the Act has already been passed in the present case before us, the intimation u/s. 143(1) of the Act against which the assessee is in appeal before us got merged with the aforesaid assessment order. Once the present intimation u/s. 143(1) of the Act having got merged in the assessment order passed u/s. 143(3) of the Act, the cause of action for the present appeal itself has vanquished, rendering the instant appeal as infructuous. While doing so, we would make it very clear that we have not expressed any views in respect of the matter raised in the assessment order passed u/s. 143(3) of the Act for which appeal by the assessee before the Ld. CIT(A) is pending for adjudication. That is a separate proceeding and the outcome of the same may be taken up in separate appellate proceedings under the relevant provisions of the Act at the section of the concerning parties. Considering the above observation and finding, we dismiss the appeal of the assessee as infructuous.”

6. Before we delve on the issue, we take note of the flow of event on the addition/disallowance made. In the course of processing of return by the CPC, following adjustments were processed on the amount mismatched with the tax audit report filed by the assessee, details of which are tabulated below:-

| Particulars |

Amount (Rs.) |

| Adjustment pertaining to increase/decrease in profit because of deviation of method of valuation as per section 145A of the Act |

1,59,76,61,725 |

| Adjustment pertaining to section 35(1)(iv) of the Act |

1,17,96,090 |

| Total |

1,60,94,57,815 |

6.1. From the aforesaid proposal, adjustment pertaining to section 35(1)(iv) for Rs. 1,17,96,090/- was dropped by the CPC after taking into consideration the explanations furnished by the assessee. Return was finally processed by issuing intimation under section 143(1) on 29.07.2023, by retaining proposed adjustment of Rs. 1,59,76,61,725/. Assessee moved rectification application against the said intimation before the ld. Jurisdictional Assessing Officer (JAO) which remained pending for disposal. As ready noted, notice under section 143(2) had already been issued on the assessee against which the assessee has made its submissions vide letter dated 14.6.2023. Ld. AO has recorded this fact in the impugned assessment order in paragraph 2.1. Subsequently, notices under section 142(1) were also issued in the course of impugned assessment proceedings which were duly complied with by the assessee. Ld. AO observed in paragraph 3.1 that the submissions made by the assessee were duly examined and on the basis of the same, contentions of the assessee were accepted with no adverse inference. However, while completing the impugned assessment, ld. AO adopted the total income determined on processing of return under section 143(1) for which intimation was issued on 29.07.2023 by assessing total income at Rs. 263,91,84,140/-.

6.2. Further, while computing tax liability in the computation sheet, ld. AO also included adjustment pertaining to section 35(1)(iv) of Rs. 1,17,96,090/-, which had already been dropped by the CPC while processing return under section 143(1). He thus, took total income assessed at Rs. 265,09,80,226/- while arriving at demand of tax liability on the assessee.

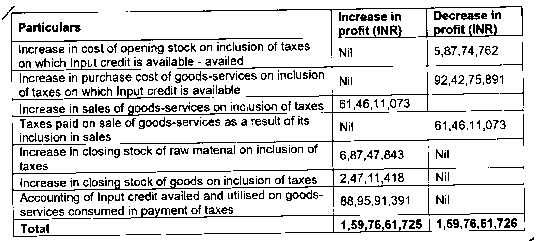

7. Before us, ld. Counsel for the assessee strongly asserted that adoption of total income determined while processing return under section 143(1) is not in accordance with the provisions of law as well as judicial precedent laid down in the case of Gujarat Electricity Board (supra) and Spaco Carburettors India Ltd. (supra). Furthermore, adjustment which has already been dropped by the CPC cannot be included to impose tax demand on the assessee without calling for any show-cause on the assessee in course of assessment proceedings. In respect of adjustment which has been retained by the ld. AO pertaining to increase/decrease in the profit because of deviation of the valuation under section 145A. ld. Counsel submitted that CPC while making proposed adjustment had stated that there is inconsistency in the amount mentioned in serial no. 4D of Part-A OI “increase in the profit or decrease in loss because of deviation, if any from the method of valuation specified under section 145A”, in the return of income as compared to amount mentioned in clause 14(b) of Form 3CD. In this regard, the assessee had furnished its explanation which was not accepted and proposed adjustment was made. Assessee reiterated its submissions and explanation contending that there is an increase in profit i.e. taxable income to the extent of Rs. 159,76,61,726/-. However, at the same time, there is a decrease in profit i.e. taxable income to the extent to the same amount. Thus, net impact to the total taxable income is ‘Nil’. All these computations were duly disclosed in the tax audit report. Relevant extract in this regard from clause 14(b) is reproduced as under :-

7.1. According to the ld. Counsel, these factual submissions have remained to be considered while completing assessment even though specific query was raised by the ld. AO while issuing notice under section 142(1) and show-cause notice. Also, ld. CIT(A) has dismissed the appeal as not maintainable in view of the appeal already pending against intimation issued under section 143(1).

8. In the conspectus of the above factual narration, we find it appropriate to remit the matter back to the file of ld. CIT(A) for adjudication on the issue contended by the assessee by passing a speaking order after taking into consideration the submissions made by the assessee. It is necessary that the appeal pending against the intimation under section 143(1) and present appeal against the assessment order passed under section 143(3) are taken up together so as to avoid multiplicity of proceedings and duplicity of the addition. Accordingly, grounds raised by the assessee are allowed for statistical purposes.

9. In the result, appeal filed by the assessee is allowed for statistical purposes.