ORDER

1. Captioned appeal filed by the assessee, pertaining to Assessment Year 2014-15, is directed against the order under section 250 of the Income Tax Act, 1961 (hereinafter referred to as “the Act”) by Commissioner of Income-tax (Appeals), (hereinafter referred to as “the Ld.CIT(A)”), dated 21.08.2025, which in turn arises out of an assessment order passed by the Assessing Officer u/s. 147 of the Act, on 18.03.2022.

2. The grounds of appeal raised by the assessee, are as follows:

“1 . Ld. CIT(A), NFAC, Delhi has erred in law and on facts to upheld A.O.’s reopening of assessment u/s 147 and issue of notice u/s 148 of the Act.

2. Ld. CIT(A), NFAC, Delhi has erred in law and on facts to upheld A.O’s decision for treating assessee’s agriculture land bearing block/ survey no.90 and 91/1/2/3/4 at village-Koparli, Tal.- Pardi, Dist- Valsad as capital asset and thereby charges STCG of Rs.2,94,295/- ignoring the fact that the land was purely agriculture land as on the execution of sale deed and handing over the possession in favor of the buyer

3 Ld. CIT(A), NFAC, Delhi has erred in law and on facts to upheld A.O.’s addition of Rs. 66,705/- on account of purchase consideration as worked out by the A.O. at Para No. 8.8 of Assessment Order.

4. Ld. CIT(A), NFAC, Delhi has erred in law and on facts to confirm A.O.’s action for charging of higher rate of tax u/s 115BBE of the Act ignoring the law that STCG cannot be taxed u/s 68 to 69C of the I.T. Act; consequently section 115BBE of the Act cannot be applicable.”

3. When the matter was called for hearing, the Ld. Counsel for the assessee at the outset submitted that the appeal has been filed by the assessee belatedly before the Tribunal. The Ld. Counsel therefore adverted my attention to the affidavit filed in this regard citing the reasons for condonation of delay and urged for a benign view and sought condonation of delay of 109 days in filling the appeal before the Tribunal. The contents of the petition for condonation of delay are reproduced below:

“I, the undersigned, Chakravati Chiman, aged about 38 years, occupation- agriculture and residing at, have to state following facts pertaining to my petition for condonation of delay in filing of appeal in the office of the ITAT, Surat.

[1] That the appeal order of Ld. CIT[A], NFAC, Delhi is dated 21/8/2025 for A.Y. 201415 was served through ITBA portal. So the date of service is taken as date 25/09/2025. Second appeal is probably filed to the office of Honorable Income Tax Appellate Tribunal on date 18/03/2026, which is delayed by -109-days.

[2] The reason for delay is that I was not aware of the appeal order delivered by Ld. CIT(A), NFAC, Delhi to me through ITBA portal of Income Tax Department. The fact of CIT[A], appeal order came to my knowledge when I received demand notice of Rs. 20,307/-from the I.T. Department on date 26/2/2026. At that time, I made contact of my tax consultant Shri D.T. Jadav at his Office. At that time, he informed me regarding dismissal of my appeal by the Ld. CIT[A], NFAC, Delhi. He advised me to file 2nd appeal as require under the I.T. Law because identical decision has been taken by the I.T. Department in favour of one of the co-owners of the same agriculture land. Following his advice, I took the decision to file appeal. As a result, appeal can be file on date 18/3/2026, which is delayed by -109-days. However, it is not intentional nor deliberate. But it is due to the above stated circumstances, beyond my control.

[3] Honorable Apex Court, High Courts and ITATS of our country have ever taken liberal views in the matter of condonation of delay in filing of appeal in light of sufficient cause. It is the philosophy of taxing laws that “None should be deprived of an adjudication on merits unless the Court of law or the Tribunal/Appellate Authority found that litigant deliberately and intentionally delayed filing of appeal.” Reliance is placed on Bombay High Court Judgement in the case of

Vijay Vishan Meghani v.

DCIT, Reported in

398 ITR 250.

4) Further, I also rely on Honorable Supreme Court judgment in the case of Collector of Land Acquisition, Anantnag v. Katiji & Ors. Reported in 167 ITR 471 in which, it has been held by the Honorable Supreme Court as under:

1. Ordinarily a litigant does not stand to benefit by lodging an appeal late.

2. Refusing to condone delay can result in a meritorious matter being thrown out at the very threshold and cause of justice being defeated. As against this when delay is condoned the highest that can happen is that a cause would be decided on merits after hearing the parties.

3. “Every day’s delay must be explained” does not mean that a pedantic approach should be made. Why not every hour’s delay, every second’s delay? The doctrine must be applied in a rational common-sense pragmatic manner.

4. When substantial justice and technical considerations are pitted against each other, cause of substantial justice deserves to be preferred for the other side cannot claim to have vested right in injustice being done because of a non-deliberate delay.

5. There is no presumption that delay is occasioned deliberately, or on account of culpable negligence, or on account of mala fides. A litigant does not stand to benefit by resorting to delay. In fact, he runs a serious risk.

6. It must be grasped that judiciary is respected not on account of its power to legalize injustice on technical grounds but because it is capable of removing injustice and is expected to do so.

Considering above facts and circumstances of my case, your judicial Honors is prayed to condone the delay of 109 days in filing of 2nd appeal before the Honorable ITAT and allow me to represent my case through A.R.”

4. On the other hand, Ld. DR for the Revenue opposed the prayer of assessee for condonation of delay. A perusal of the affidavit gives me an impression of existence of mitigating circumstances to enable me to exercise my discretion in favour of the assessee. Accordingly, the delay is condoned.

5. Succinctly, the factual panorama of the case is that assessee before me is an Individual and has not filed his return of income for the assessment year (A.Y.) 2014-15. As per details available, the assessee does not have any PAN. In this case, there is a non-PAN information received by the assessing officer on 26.07.2016 through proper channel from O/o the DIT (I & CI), Ahmedabad that the assessee has sold an immovable property for sale consideration amount of Rs.65,00,000/-, which was registered on 30.08.2013 in the office of the Sub Registrar office, Pardi. It was further reported that the transaction is mapped on the name of the assessee with nonPAN transaction details. The information so received has been verified and analysed and it was seen that assessee along with other 14 persons has sold an immovable property for sale consideration of Rs.65,00,000/- which was registered on 30.08.2013 in the office of the Sub Registrar office, Pardi during the F.Y. 2013-14 relevant to A.Y.2014-15. Moreover, the assessee has not filed any return of income for the year under consideration. In this regard, letter was issued to the assessee on 11.04.2017 regarding status of filing of return of income and whether the said transaction has been shown in the return of income by the assessee. In response, the assessee filed reply vide letter dated 02.05.2017 and stated that the said land (Moje: Koprali, B.S. No.90,91/1+2+3+4, Tal- Pardi, Valsad) was sold by 15 family members for consideration amount of Rs.65,00,000/- and assessee’s share was only of Rs.3,61,000/- as per details mentioned in the sale deed. The assessee further submitted that the said land being rural agricultural land did not attract capital gain tax liability. The reply so filed by the assessee was gone through by the assessing officer. The assessing officer noticed that the assessee did not submit any certified supporting evidence which can prove that the said land was not a capital asset as per provisions of Sec.2(14) of the I.T. Act. To verify the taxability of the transaction, return details of the assessee has been searched from the departmental records. A PAN database search has also been made from ITD database as well as in PAN directory in the case based on available details, but no match has been found. The transaction has been reported as non- PAN transaction which led the assessing officer to believe that either the assessee was having no PAN or has not given PAN to the reporting entity in relation to the above transaction and in resultant the income/profit derived from the said land transaction has not been accounted for by the assessee in the year under consideration.

6. In view of above facts, the assessing officer observed that the assessee failed to offer the income incidental to sale transaction of immovable property for taxation by not filing return of income for the year under consideration, provisions of clause (a) to explanation-2 to Section 147 of the Income tax Act attracted in the case of assessee which provide that where no Return of income has been filed by the assessee, although he has total income or the total income of the any other person in respect of which he is assessable under this Act during the previous year exceeds the maximum amount which is not chargeable to income tax, shall be deemed to be the cases where income chargeable to tax has escaped assessment. Accordingly, the assessment of the assessee was reopened u/s 147 of the Act after recording the reasons for doing so. The notice u/s 148 of the Act was issued on 31.03.2021. The notice u/s.142(1) was issued on 15.09.2021 requesting the assessee to comply with notice u/s 148 and to furnish details and explanations in connection with the reopened assessment proceedings. In response, the assessee made on-line submission vide acknowledgement no. 605517051290921 dated 29.09.2021. The submission made by the assessee is reproduced as under:

“We have sold our ancestor Agricultural land bearing survey no.90 on 30/08/2013 for total consideration of Rs. 6500000/- out of which my share in the consideration comes to Rs. 3,61,000/-. Please note that the land was “Agricultural land” which is situated in Koparli village in Valsad district which has total population of 4450 therefore, the land is not capital assets, so the question of Capital Gain does not arise (State Census 2011 attached herewith for your ready reference). The Total Consideration received by me is only 3,61,000/- the same was also mentioned in sale deed (sale deed annexed herewith for your ready reference)”

7. The assessing officer also issued a detailed show cause notice along with draft assessment order and notice u/s.142(1) was issued to the assessee on 13.03.2022, seeking the explanation of the assessee on or before 17.03.2022. In response, the assessee uploaded on- line submission on 18.03.2022 and also furnished copy of an assessment order passed in one of the co-owners case, viz. Dharmistha Chiman by the NaFAC. The written submission of the assessee is reproduced below:

“Respected Sir, In reply to your show cause notice, I have to state with due respect that case of the one of the co-owners namely DHARMISTHA CHIMAN (PAN: BXIPC2840J) have been finalized by your good self by and order u/s. 143(3) r.w.s. 147 of the IT Act on 16.03.2022 vide DIN: ITBA/AST/S/147/2021-22/1040901807(1). Copy enclosed. I’m also one of the co-owners of the same rural agriculture land, have received Rs. 3,61,000/-. Therefore, your good self is requested to kindly follow the decision taken by your good self in the case of Dharmistha Chiman and oblige.”

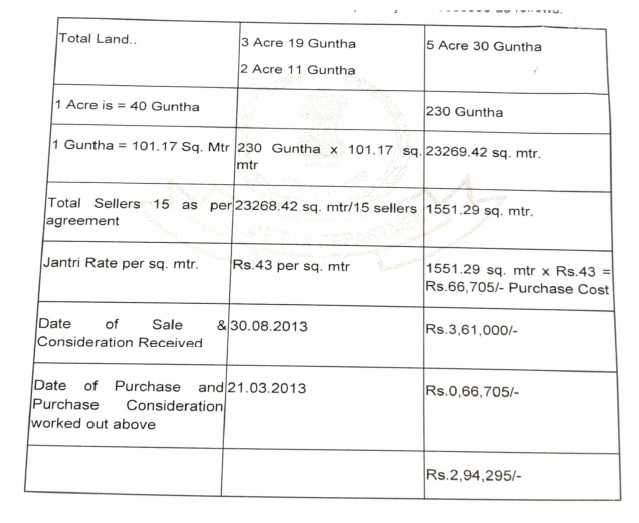

8. However, the assessing officer rejected the above contention of the assessee and made two additions in the hands of the assessee, the details of which are as follows:

| (i) |

|

The assessing officer did not allow the exemption claimed by assessee u/s 2(14) of the Act, and worked out the capital gain, liable to be paid by the assessee, as follows: |

| (ii) |

|

The assessing officer also noticed that assessee failed to explain the source of investment in purchase cost amounting to Rs.66,705/- of property in question and hence the same was being taxed u/s.69B r. w. section 115BBE of the Act. |

Therefore, assessing officer made the addition in the hands of the assessee to the tune of Rs.2,94,295/- and to the tune of Rs.66,705/-, respectively, as noted above.

9. Aggrieved by the order of the assessing officer, the assessee carried the matter in appeal before the Ld.CIT(A), who has confirmed the action of the assessing officer. The ld.CIT(A) noticed that a perusal of the terms of Sale Deed, stamp duty paid and Collector’s conversion order clearly show that the land was no longer agriculture land at the time of transfer. The statutory provisions and judicial precedents are also clear. Hence, it is held that the impugned land was no longer agricultural land at the time of transfer and assessee’s contention that it was exempt from capital gains tax is untenable. Therefore, the Assessing Officer has rightly brought the gains to tax under the head “Capital Gains.” Therefore, learned CIT(A) confirmed the addition to the tune of Rs.2,94,295/-. The ld.CIT(A) also noticed that the assessee has failed to explain the source of investment in purchase of property in question amounting to Rs.66,705/-. Accordingly, the same was taxed u/s 69B r. w. section 115BBE of the Act.

10. Aggrieved by the order of the Ld.CIT(A), the assessee is in further appeal before this Tribunal.

11. I have heard both the parties and carefully gone through the submission put forth on behalf of the assessee along with the documents furnished and the case laws relied upon, and perused the fact of the case including the findings of the ld CIT(A) and other materials brought on record. At the outset, Shri Rajesh Upadhyay, Learned Counsel for the assessee submitted that when the land was sold, it was agricultural land. It is an ancestor agricultural land, and there are 15 co- owners of such land. The purchasers of the land, later on, converted the same land into non-agricultural land. There are 15 co-owners of such land and out of 15 co-owners, 3 co-owners reassessment were reopened under section 147 of the Act and rest 12 co-owners case were not reopened under section 147 of the Act. Therefore, Income Tax Department did not make any addition, in the hands of 12 Co-owners. Therefore, since the Department had not made addition in the hands of the 12 co-owners, therefore, assessee should not be treated differently, and addition should not be made in the hands of the assessee, under consideration.

12. On merit, the Ld. Counsel submitted that land sold by these co-owners was agricultural land. Hence, exempted from tax, therefore, no capital gain tax is attracted and the addition made by the assessing officer should be deleted.

13. On the other hand, the Ld. DR for the Revenue has primarily reiterated the stand taken by the Assessing Officer, which we have already noted in our earlier para and is not being repeated for the sake of brevity.

14. I have considered the submissions of both the parties and noted that assessee is an individual and has not filled return of income (ROI), as the assessee did not have income chargeable to tax. The assessing officer has issued notice u/s 148 of the Act, because assessee along with others 14 co-owners, have sold agricultural land bearing Block Survey. No. 90and 91/1-2-3-4 at village Koparli Taluka Pardi Dist, Valsad for sale consideration of Rs. 65,00,000/- and assessee’s share was of Rs.3,61,000/-. According to the assessing officer, the assessee was liable to pay tax on Rs 3,61,000/-. Therefore, assessee’s case was reopened. As the land is rural agricultural land located at Village- Koparli, and it is exempt from tax. There was no evidence with assessing officer, at the stage of reopening that the rural agricultural land sold by assessee is a capital assets u/s 2(14) of the Act. On the contrarily, registered sale deed and other documents available with the office of the sub registrar, Pardi suggest that the land sold by assessee is a rural agricultural land which is outside the scope of Section 2(14) of the Act. Therefore, addition made by the assessing officer in the hands of the assessee on account of long-term capital gain to the tune of Rs.2,94,295/-, needs to be deleted. Accordingly, I note that higher rate of tax u/s 115BBE of the Act, on Rs.66,705/-, the assessing officer stated that assessee incurred purchase cost amounting Rs.66,705/- for which source was not explained. Therefore assessing officer made addition u/s 69B and levy tax u/s 115BBE of the Act. In fact, both pieces of agricultural land that is, survey no 90 and 91 of Village- Koparli, Dist – Valsad are hereditary ancestral land for which no cost was incurred. The Revenue records and sale deed are direct evidences in support of these facts. I note that no cost has been incurred by assessee, therefore, assessing officer’s addition u/s 69B as well as invocation of provisions of Section 115BBE needs to be deleted, accordingly, I delete the same.

15. In the result, the appeal of the assessee is allowed.