ORDER

Keshav Dubey, Judicial Member.- This appeal at the instance of the assessee is directed against the order of ld. DCIT Circle 4(1)(1), Bengaluru dated 29.12.2022 vide DIN & Order No. ITBA/AST/S/143(3)/2022-23/1048343764(1) passed u/s 143(3) r.w.s. 260 of the Income Tax Act, 1961 (in short “The Act”) for the assessment year 2017-18.

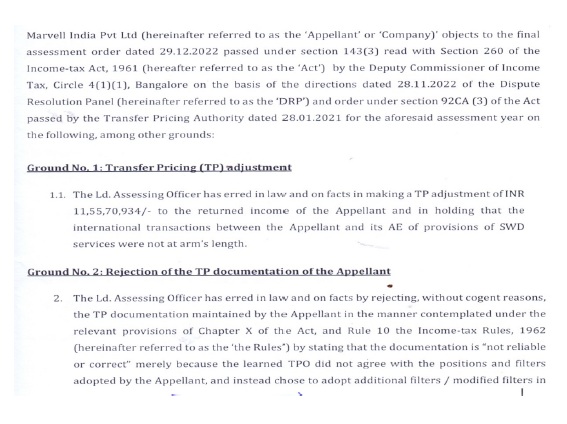

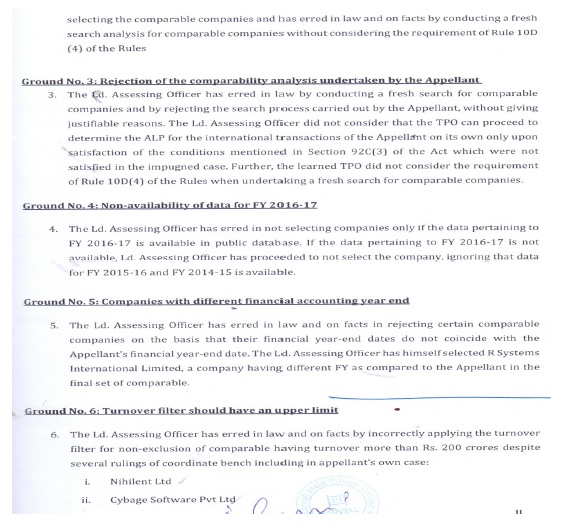

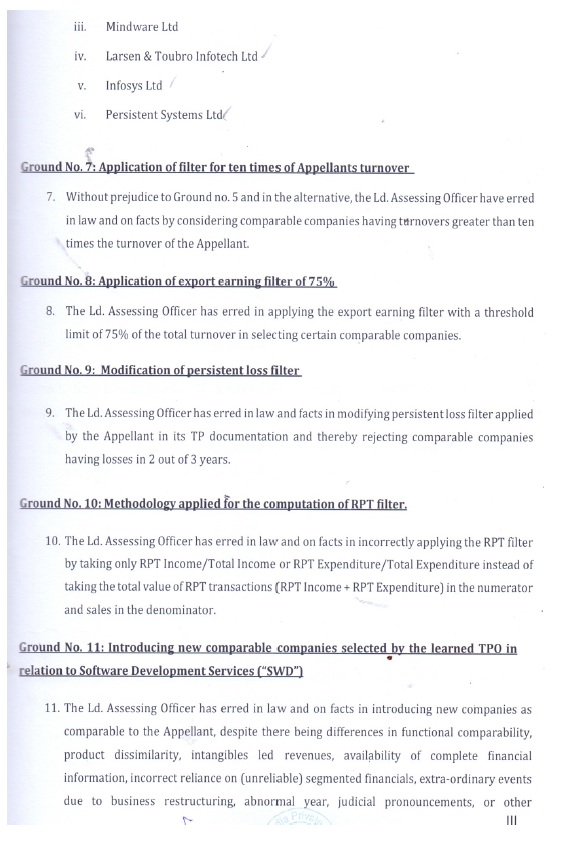

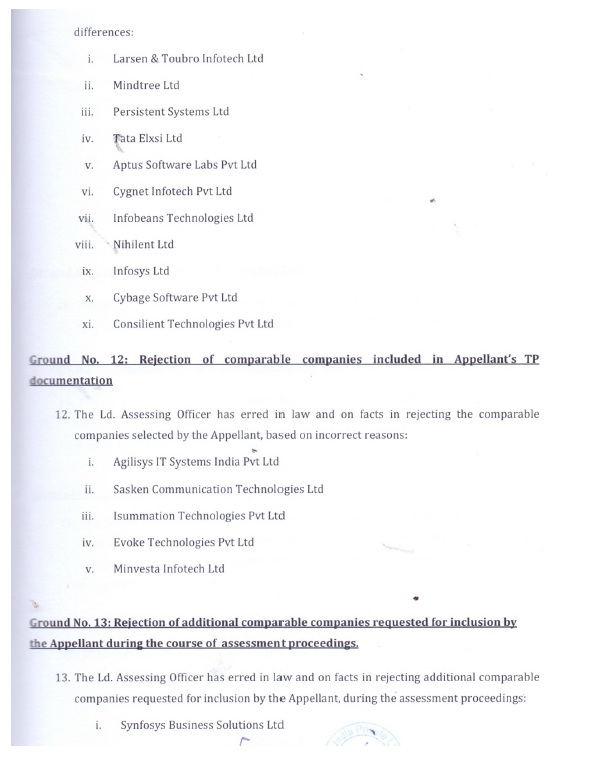

2. The assessee has raised the following grounds of appeal:

3. Brief facts of the case are that M/S. Marvell India Private Limited (hereinafter referred to as ‘Assessee’) is a subsidiary of Marvell Technology Group Ltd. and is engaged in provision of software development services to its Associated Enterprise (hereinafter referred to as ‘AE’). During the Assessment Year 2017-18, the Assessee filed its return of income by declaring total income of Rs.13,72,75,040/- and the same was taken up for scrutiny. During the assessment proceedings, the Ld. Assessing Officer (hereinafter referred to as ‘AO’) referred the international transactions entered by the Assessee to the ld. TPO for determining the Arm ‘s Length Price under Section 92CA of the Act. The learned Transfer Pricing Officer passed the Order u/s 92CA(3) of the Act on 28/01/2021 wherein transfer pricing adjustment of Rs. 13,32,47,187/- were proposed. Accordingly, the AO passed the Draft Assessment Order on 16.02.2021 by adding the transfer pricing adjustments of Rs. 13,32,47,187/- to the returned Income & show cause as to why the assessment should not be completed as per the draft assessment order. Subsequently, the objections against the Draft Assessment Order dated 16.02.2021 were filed before the DRP by the Assessee on 16.03.2021. After the filing of the objection to the DRP, another Show Cause Notice dated 15.04.2021 was issued by the AO to the Assessee, which contained only the corporate tax related adjustment. The Assessee objected to the issuance of the Show cause notice on the ground that the same was issued post issuance of Draft assessment Order dated 16.02.2021 which was contrary to the provisions of Act. However, the final assessment order dated 26.04.2021 was passed, without waiting for the DRP’s direction. The Final Assessment Order dated 26.04.2021 made additions on corporate tax issues as well as on transfer pricing issue. It is to be highlighted that the corporate tax adjustments were never proposed in the draft assessment order dated 16.02.2021. The Assessee filed written submissions to the AO on 10.05.2021 wherein it was categorically stated that the corporate tax issues were never proposed in the draft assessment order dated 16.02.2021 and therefore, once Draft assessment Order dated 16.02.2021 was issued, neither any SCN could be issued nor any further adjustment to the income could be proposed.

3.1 Being aggrieved, the Assessee had approached the Hon’ble Karnataka High Court against the final assessment order dated 26.04.2021 as the same was passed without awaiting the outcome of the objections filed before the DRP. The Hon’ble Karnataka High Court vide Order dated 15.12.2021 quashed the Final assessment order dated 26.04.2021 as well as DRP Order dated 24/11/2021 and directed the DRP to proceed further by considering the objections dated 16/03/2021 filed by the assessee. Subsequently, the fresh DRP directions dated 28.11.2022 was issued. The DRP directed for transfer pricing adjustments as proposed in the draft assessment Order dated 16.02.2021. It is important to note that no direction was given on corporate tax additions by the ld. DRP as the same was not proposed in the Draft Assessment Order dated 16.02.2021. However, upon issuance of the DRP direction dated 28.11.2022, the Final Assessment Order dated 29.12.2022 was passed by the AO which again included corporate tax additions along with transfer-pricing adjustment.

3.2 Again aggrieved, the assessee preferred an appeal before this Tribunal by challenging the Final Assessment Order dated 29.12.2022 which includes Transfer Pricing adjustment along with Corporate Tax issues. This Tribunal vide Order in IT(TP)A No. 115/Bang/2023 dated 04.09.2024 granted relief on the Transfer Pricing adjustment relying on the assessee’s own case, however mistakenly did not adjudicate the ground no. 18 & ground no. 19 which relates to the Corporate Tax issues. The assessee thereafter filed a miscellaneous application registered as MA No 61/Bang/2024, seeking rectification of mistake in the Order dated 04.09.2024 to the extent it failed to adjudicate the Corporate Tax issues. Finally, this Tribunal passed the Order in MA No. 61/Bang/2024 dated 03/02/2025 & recalled the Order passed in respect of ground No. 18 & ground No.19 as there was apparent mistake on the face of the record.

4. Therefore, in the present appeal we have to adjudicate the ground No. 18 & ground No.19 only relating to the corporate tax issues which are again reproduced as below for ease of reference & convenience: –

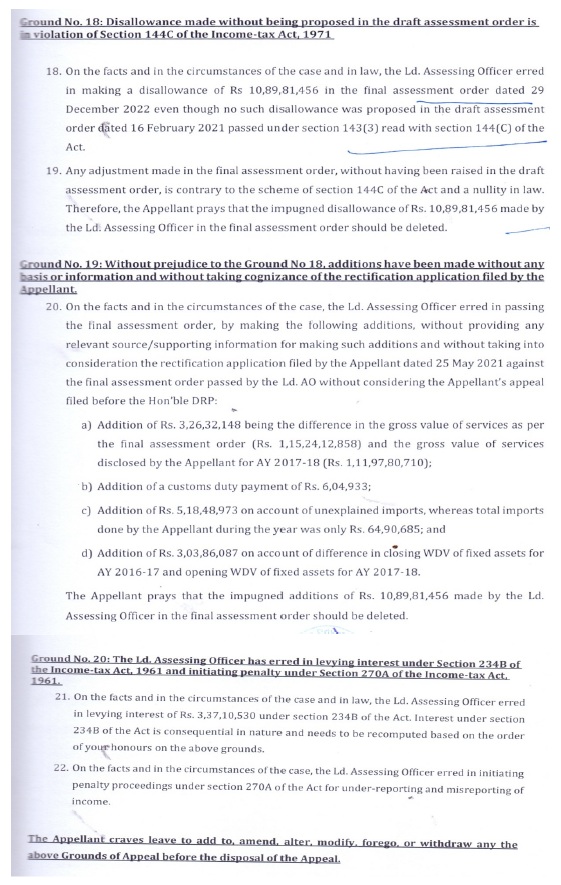

Ground No.18: Disallowance made without being proposed in the draft assessment order is in violation of Section 144C of the Income-tax Act, 1971

18. On the facts and in the circumstances of the case and in law, the Ld. Assessing Officer erred in making a disallowance of Rs 10,89,81,456 in the final assessment order dated 29 December 2022 even though no such disallowance was proposed in the draft assessment order dated 16 February 2021 passed under section 143(3) read with section 144C of the Act.

19. Any adjustment made in the final assessment order, without having been raised in the draft assessment order, is contrary to the scheme of section 144C of the Act and a nullity in law. Therefore, the Appellant prays that the impugned disallowance of Rs. 10,89,81,456 made by the Ld. Assessing Officer in the final assessment order should be deleted.

Ground No. 19: Without prejudice to the Ground No 18, additions have been made without any basis or information and without taking cognizance of the rectification application filed by the Appellant.

20. On the facts and in the circumstances of the case, the Ld. Assessing Officer erred in passing the final assessment order, by making the following additions, without providing any relevant source/supporting information for making such additions and without taking into consideration the rectification application filed by the Appellant dated 25 May 2021 against the final assessment order passed by the Ld.AO without considering the Appellant’s appeal filed before the Hon’ble DRP:

| (a) |

|

Addition of Rs. 3,26,32,148 being the difference in the gross value of services as per the final assessment order (Rs. 1,15,24,12,858) and the gross value of services disclosed by the Appellant for AY 2017-18 (Rs. 1,11,97,80,710); |

| (b) |

|

Addition of a customs duty payment of Rs. 6,04,933; |

| (c) |

|

Addition of Rs. 5,18,48,973 on account of unexplained imports, whereas total imports done by the Appellant during the year was only Rs. 64,90,685; and |

| (d) |

|

Addition of Rs. 3,03,86,087 on account of difference in closing WDV of fixed assets for AY 2016-17 and opening WDV of fixed assets for AY 2017-18. |

The Appellant prays that the impugned additions of Rs. 10,89,81,456 made by the Ld. Assessing Officer in the final assessment order should be deleted.

5. Before us, the ld. AR of the assessee vehemently contended as detailed below-

| (1) |

|

The Ld. AO acted in excess of its jurisdiction by assessing corporate tax additions which never formed part of the Draft Assessment Order dated 16.02.2021. |

| (2) |

|

Once the draft assessment order dated 16/02/2021 was issued, neither any further SCN could be issued nor any further adjustment to the income could be proposed. |

| (3) |

|

Since, there was no direction by the DRP on the corporate tax issues, no addition could be made by the AO in final assessment Order dated 29.12.2022. |

| (4) |

|

While passing the final assessment order, the AO cannot go beyond what is proposed in the draft assessment order. |

6. Per contra, the ld. DR heavily relied on the order of the AO & vehemently submitted that it is not true that the AO had not issued the draft assessment order before making additions on various corporate tax issues in the final assessment order. The AO had in fact on 15/04/2021 had issued the draft assessment order proposing the various corporate tax additions & show caused to the assessee as to why assessment should not be completed as per the draft assessment order. Thus, the AO had given opportunity to the assessee by issuing the draft assessment order as per the provisions contained in section 144C(1) of the Act before passing final assessment order. Further, the ld. DR submitted that Hon’ble Karnataka High Court vide Order dated 15/12/2021 had categorically directed the ld. DRP to consider objections dated 16/03/2021 filed by the assessee which were the objections to the adjustments proposed in the draft assessment order dated 16/02/2021 and accordingly prayed that the appeal of the assessee may be dismissed.

7. We have heard the rival submissions and perused the material available on record. It is an undisputed fact that the ld. TPO passed an order under section 92CA(3) of the Act on 28.01.2021 incorporating TP adjustment of Rs. 13,32,47,187/-. The AO, thereafter passed the draft assessment order on 16.02.2021 and accordingly issued a show cause notice to the assessee as to why assessment should not be completed as per the draft assessment order dated 16/02/2021. Further, on perusal of the draft assessment order passed under section 144C of the Act on 16.02.2021, we observed that the AO had only proposed the adjustment to the transfer pricing amounting to Rs. 13,32,47,187/-as proposed by the TPO vide order passed under section 92CA(3) of the Act dated 28.01.2021 and no corporate tax adjustments therein were proposed in the said draft assessment order. Against this said draft assessment order, the assessee filed its objections before the Ld. DRP on 16.03.2021 objecting to the transfer pricing adjustment proposed in the draft assessment order. Now the contentions of the AR of the assessee is that while passing the final assessment order, the AO cannot go beyond what is proposed in the draft assessment order and secondly the Ld. AO acted in excess of its jurisdiction by assessing corporate tax additions which never formed part of the Draft Assessment Order dated 16.02.2021. Undisputedly, the corporate tax additions totaling Rs. 10,89,81,456/- were never proposed in the draft assessment order dated 16/02/2021 as rightly contended by the AR of the assessee but we do not agree with the contention of the AR of the assessee that while passing the final assessment order, the AO had gone beyond what is proposed in the draft assessment order as in the present case after filling of objection to the DRP, the AO on 15.04.2021 passed another draft assessment order proposing therein the various corporate tax additions amounting to Rs.10,89,81,456/- and show cause to the assessee as to why assessment should not be completed as per draft assessment order. Thus, we observed that the AO had passed two different draft assessment order one dated 16.02.2021 incorporating the TP adjustment proposed by the TPO and another draft assessment order dated 15.04.2021 proposing the various corporate tax issues. Now the mute question arises for the consideration here is that whether the AO in respect of one assessment proceedings of the same assessee for the same assessment year can pass two different draft assessment orders ?

7.1 According to section 144C(1) of the Act, the AO shall, notwithstanding anything to the contrary contained in this Act, in the first instance, forward a draft of the proposed order of assessment (draft order) to the eligible assessee if the AO proposes to make any variation which is prejudicial to the interest of assessee. We are of the considered opinion that section 144C(1) of the Act lay emphasis on the followings-

| (i) |

|

The AO, in the first instance forward a draft order to the assessee; |

| (ii) |

|

If the AO proposes to make any variation prejudicial to the interest of assessee. |

Thus, the legislatures at their own wisdom use the word ‘in the first instance’ as well as ‘a draft order’.

| (i) |

|

‘In the first instance’: We are of the considered opinion that this phrase is critical. It explicitly indicates that the forwarding of the draft order is an initial and singular event. It sets in motion a specific procedural chain for that assessment year concerning the proposed variations. Once this initial draft is forwarded, the subsequent steps, whether acceptance by the assessee or objections to the DRP, are all anchored to this one document. |

| (ii) |

|

‘a draft of the proposed order of assessment’: The use of the indefinite article ‘a’ coupled with the singular noun ‘draft’ further reinforces the notion of a single, specific document. Therefore, the said draft order is the sole reference point throughout the entire Section 144C mechanism. It implies a consolidated proposal of all variations prejudicial to the assessee’s interest at that initial stage, rather than piecemeal or successive draft orders. |

Further, in our considered opinion, the provisions of the Act also lay emphasis on “any variation proposed which is prejudicial to the interest of assessee”, which in our opinion includes not only the variation proposed relating to the TP issues but also variation proposed to the corporate tax issues which are prejudicial to the interest of the assessee must be proposed in a single draft order. Therefore, in the single draft order, the AO has to incorporate all the proposed variations which are prejudicial to the interest of the assessee. Thus, the AO cannot issue two formal draft assessment orders to an eligible assessee for the same assessment proceedings under Section 144C(1) of the Act to initiate separate DRP processes. The statutory language, particularly ‘in the first instance’ and ‘a draft order,’ along with the structured procedural flow and the limited powers of the DRP, clearly indicates a singular, initial formal communication that triggers the DRP mechanism. The DRP’s mandate is to review and modify the variations proposed in that specific draft order and therefore in our view, the Hon’ble Karnataka High Court vide order dated 15/12/2021 had rightly directed the ld. DRP to proceed further in accordance with law as contemplated u/s 144C(5) to 144C(13) of the Act by considering the objections dated 16/03/2021.

7.2 Further, we are also of the considered opinion that the entire procedural framework of Section 144C of the Act is built around this singular ‘draft order’:

| (i) |

|

Assessee’s Response (Section 144C(2)): Upon receipt of ‘the draft order’ (singular), the eligible assessee has a clear choice within thirty days: either accept the variations proposed by the AO or file objections with both the DRP and the AO. This choice is directly linked to ‘the draft order’ received. |

| (ii) |

|

Completion of Assessment (Section 144C(3)): If the assessee accepts the variations or fails to file objections within the stipulated period, the AO ‘shall complete the assessment on the basis of the draft order.’ Again, the singular ‘draft order’ is the foundation for the final assessment. |

| (iii) |

|

DRP’s Role and Scope (Section 144C(5), (6), (8), (13)): |

| (a) |

|

If the objections are filed, the DRP issues directions ‘for the guidance of the Assessing Officer to enable him to complete the assessment’ (Section 144C(5)). The DRP considers ‘the draft order’ and the objections thereto (Section 144C(6)). |

| (b) |

|

Crucially, Section 144C(8) explicitly limits the DRP’s powers: it ‘may confirm, reduce or enhance the variations proposed in the draft order so, however, that it shall not set aside any proposed variation or issue any direction under sub-section (5) for further enquiry and passing of the assessment order.’ This limitation is a strong indicator that the DRP operates within the confines of the initial draft order presented to it. It cannot direct the AO to issue a new draft or conduct extensive fresh inquiries that would necessitate a new draft, thereby restarting the process. |

| (c) |

|

Finally, the AO is bound to complete the assessment ‘in conformity with the directions’ issued by the DRP, ‘without providing any further opportunity of being heard to the assessee’ (Section 144C(13)). This reinforces the finality of the DRP’s directions based on the initial draft. |

7.3 The mandatory nature of issuing a draft assessment order under Section 144C(1) of the Act before passing a final assessment order under Section 143(3) is well-established. Failure to issue this initial draft is considered a non-curable defect, leading to the invalidation of the subsequent final assessment order, demand notices, and penalty proceedings. This underscores the critical role of this initial draft as the trigger for the DRP mechanism. The Gujarat High Court in

Pr. CIT v.

Woco Motherson Advanced Rubber Technologies Ltd. /[2018] 406 ITR 375 (Gujarat) held that the Assessing Officer cannot make any addition and/or disallowance other than what is proposed in the draft assessment order. This reinforces that the draft order sets the boundaries for the assessment and the DRP’s review. Further, the Karnataka High Court in

CIT (International Taxation) v.

Cisco Systems Services B.V. [2023] 456 ITR 50 (Karnataka) highlighted the detailed procedure laid down in Section 144C, emphasizing the procedural importance of the draft order and the consequences of procedural errors. In view of the above discussion, we held that subsequent draft assessment order dated 15/04/2021 is illegal, bad in law and accordingly quashed.

7.4 We also take note of the fact that the AO passed the final assessment order on 26/04/2021 neither considering the objections of the assessee nor awaiting directions from the ld. DRP and accordingly, the Hon’ble High Court of Karnataka vide order dated 15/12/2021 had already quashed the assessment order dated 26.04.2021 as well as ld. DRP order dated 24/11/2021 and directed the ld. DRP to proceed further in accordance with law as contemplated under section 144C(5) to 144C(13) of the Act by considering the objections dated 16/03/2021 filed by the assessee. On perusal of the directions of the ld. DRP dated 28/11/2022, the ld. DRP had directed for the transfer pricing adjustments only as proposed in the draft assessment order dated 16/02/2021. On going through the final assessment order dated 29/12/2022, we observed that the AO had not only made additions towards total adjustments u/s 92CA of the Act as per the DRP directions amounting to Rs. 11,55,70,934/- but also added on various corporate tax issues totaling to Rs. 10,89,81,456/- & assessed on a total income of Rs. 36,18,27,430/- for the AY 2017-18. Now the ld. AR of the assessee contending that since no direction was given on corporate tax issues by the ld. DRP, the AO grossly erred in making corporate tax additions of Rs.10,89,81,456/- in the final assessment order dated 29/12/2022.

7.5 We are of the considered opinion that u/s 144C(10) of the Act, every direction issued by the ld. DRP shall be binding on the AO and u/s 144C(13) of the Act, the AO is duty bound to pass the assessment order in conformity with the directions within one month from the end of the month in which such directions are received. We also take note of the fact that the AO passed the final assessment order incorporating the directions issued by the ld. DRP with regard to TP adjustments & also made additions on various corporate tax issues amounting to Rs.10,89,81,456/- in the absence of any such directions, which in our opinion is in clear violation of section 144C of the Act. We are also of the considered opinion that the AO is bound by the directions issued by the DRP and required to pass the assessment order in conformity with the directions issued within one month from the end of the month in which such directions are received. Therefore, the additions of various corporate tax issues amounting to Rs. 10,89,81,456/- in the final assessment order dated 29/12/2022 in the absence of the ld. DRP direction is illegal & bad in law & the entire additions of Rs.10,89,81,456/- is liable to be deleted. We also make it clear that the subsequent draft assessment order dated 15/04/2021 issued by the AO proposing only corporate tax additions after filing of the objections by the assessee before the DRP as well AO is already quashed.

8. In the result the appeal filed by the assessee is allowed.