TDS Exemption Notification Proposal for IFSC Ship Leasing Company Lease Rent Payments

Proposal for notification under section 400 of the Income tax Act 2025 providing for exemption from TDS in respect of payments of lease rents to units of ship leasing companies in IFSC

![]()

The Gazette of India

CG-DL-E-03072026-274062

EXTRAORDINARY

PART II—Section 3—Sub-section (ii)

PUBLISHED BY AUTHORITY

No. 3475] NEW DELHI, FRIDAY, JULY 3, 2026/ASHADHA 12, 1948

MINISTRY OF FINANCE

(Department of Revenue)

(CENTRAL BOARD OF DIRECT TAXES)

NOTIFICATION

New Delhi, the 3rd July, 2026

S.O. 3610(E).— In exercise of the powers conferred by section 400(1) read with section 147 of the Incometax Act, 2025 (30 of 2025) (hereinafter referred to as the said Act), the Central Government hereby specifies that no

deduction of tax shall be made under section 393(1)[Table S.No.2] of the said Act on payment in the nature of lease

rent or supplemental lease rent, as the case may be, made by a person (hereinafter referred to as the lessee) to a person

being a Unit of an International Financial Services Centre (hereinafter referred to as the lessor) for lease of a ship

subject to the following, namely:-

1. (1) The lessor shall –

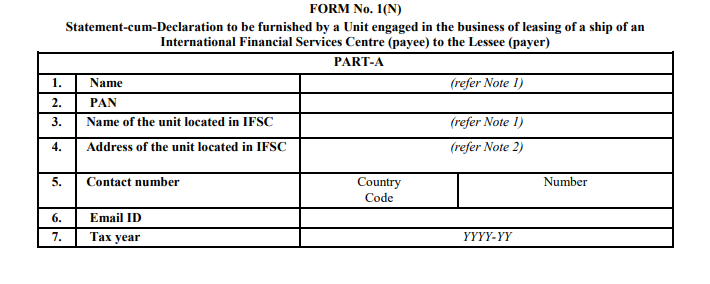

(a) furnish a statement-cum-declaration in Form No. 1(N) annexed to this notification (hereinafter

referred to as the said Form) to the lessee giving details of twenty consecutive tax years for which

the lessor opts for claiming deduction under section 147 of the said Act; and

(b) such statement-cum-declaration shall be furnished and verified in the manner specified in the said

Form, for each tax year out of twenty consecutive tax years for which the lessor opts for claiming

deduction under section 147 of the said Act;

(2) The lessee shall —

(a) not deduct tax on payment made or credited to lessor after the date of receipt of copy of statementcum- declaration in the said Form from the lessor; and

(b) also furnish the particulars of all the payments made to lessor on which tax has not been deducted in

view of this notification in the statement of deduction of tax referred to in section 397(3)(b) of the

said Act read with rule 219 of the Income-tax Rules, 2026.

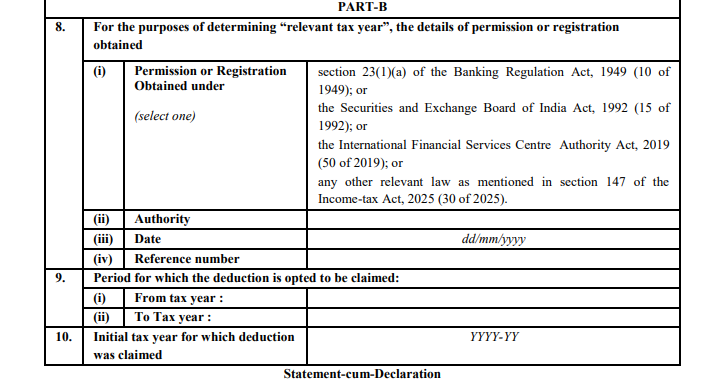

2. The above relaxation shall be available to the lessor only during the said twenty consecutive tax years as

declared by the lessor in the said Form for which deduction under section 147 is being opted and the lessee shall be

liable to deduct tax on payment of lease rent for any other year.

3. The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as

the case may be, shall lay down procedures, formats and standards for ensuring secure capture and transmission of

data and uploading of documents and they shall also be responsible for evolving and implementing appropriate

security, archival and retrieval policies.

Explanation. − For the purposes of this notification, −

(a) “ship” shall have the same meaning as assigned to it in Schedule VI (Note 3) of the said Act;

(b) “International Financial Services Centre” shall have the same meaning as assigned to it in clause (q) of

section 2 of the Special Economic Zones Act, 2005 (28 of 2005); and

(c) “Unit” shall have the same meaning as assigned to it in section 2(zc) of the Special Economic Zones Act,

2005 (28 of 2005).

4. This notification shall be deemed to have come into force on the 1st day of April, 2026.

I ………………(name of the declarant) having Permanent Account Number ………… in capacity as …………. of

…………..(name of the payee), do hereby declare that the above-mentioned Unit is engaged in the business of leasing

of a ship and is eligible for deduction under section 147 of the Income-tax Act, 2025 (30 of 2025).

I further declare that the above-mentioned International Financial Services Centre Unit has opted to claim the said

deduction for the period from the tax year……… to the tax year………

I further declare that the above mentioned Unit continues to be a unit working in International Financial Services

Centre and continues to be engaged in the business of ………… during the tax year ……………… in which this

statement-cum- declaration is being submitted.

Verification

I…………………. in capacity as………. of……………….. (name of the payee) do hereby certify that all the particulars

furnished above are correct and complete.

Place: Signature of the declarant

Date: Name:

Designation:

[To be signed by a person competent to sign the return of income as provided in section 265 of the Income-tax Act,

2025 (30 of 2025)].

Note:-1. The name shall be provided in full.

Note:-2. The address shall contain (i) Country/Region, (ii) Flat/Door/Building, (iii) Road/Street/

Block/Sector, (iv) PIN/ZIP Code, (v) Post Office, (vi) Area/locality, (vii) District, (viii) State

Note:-3. Some of the information in the form would be pre-filled to the extent possible.

[Notification No. 75/2026/F.No. 275/18/2026-IT(B)]

RAJENDRA KUMAR MEENA, Under Secy.

Explanatory Memorandum: It is hereby certified that no person is being adversely affected by giving

retrospective effect to this notification.

Download PDF Click here

Read more

for more refer Gazette website click here

for more refer YouTube Subscribe website click here