Chartered Accountant Acting as Conduit for Client Tax Payments Cannot Be Taxed for Unexplained Bank Deposits

Issue

Whether substantial cash/credit deposits found in the bank account of a Chartered Accountant can be added to his income as “unexplained money” under section 69A of the Income-tax Act, when the corresponding debit entries and tax challans establish that the account was used merely as a conduit to collect and remit statutory taxes on behalf of his clients.

Facts

-

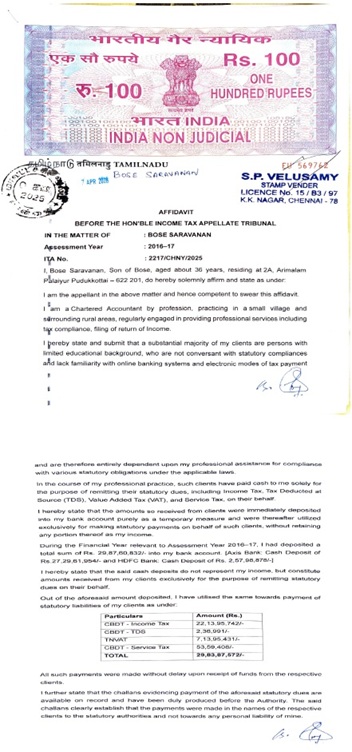

Assessee Profile & Filing: The assessee is a practicing Chartered Accountant who filed his return of income for the Assessment Year 2016-17, declaring a total income of Rs. 2.95 lakhs.

-

Purpose of Bank Account: The assessee maintained a specific bank account with the stated purpose of collecting advance funds from various clients to remit statutory taxes to government authorities on their behalf.

-

Reopening of Assessment: The Assessing Officer (AO) received information regarding massive deposits in this bank account. Finding the deposits non-commensurate with the declared income of Rs. 2.95 lakhs, the AO reopened the assessment.

-

Addition by AO: The AO rejected the assessee’s explanation that the deposits belonged to clients and made an addition of approximately Rs. 23 crores under section 69A, treating the credits as unexplained money.

-

Evidence of Remittance: Records indicated that the assessee had actually made tax payments totaling Rs. 29,83,87,572 through the said bank account.

-

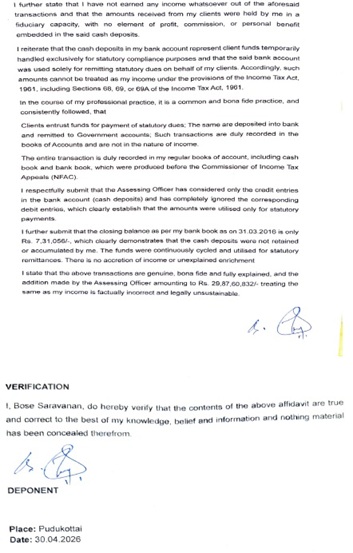

Overlooked Debits: Sample tax challans directly matched the debit entries in the bank account. The bank narrations explicitly named various government authorities, confirming that the funds were systematically deployed for client tax duties. However, the lower tax authorities completely ignored these debit entries when making the addition.

Decision

-

Role as a Conduit Established: It was held that the evidence clearly demonstrated the assessee was merely acting as a routing conduit or intermediary for his clients’ tax liabilities.

-

Ownership of Funds: The deposits reflecting in the impugned bank account did not beneficially belong to the assessee, as they were offset by corresponding debits to the government treasury.

-

Addition Deleted: Because the lower authorities failed to consider the narrative debits that validated the source and utilization of the funds, the addition of Rs. 23 crores made under section 69A could not be legally sustained.

-

Final Outcome: The ruling was decided completely in favour of the assessee.

Key Takeaways

-

Deeming Provisions Require Holistic Review: Section 69A is a deeming fiction. While evaluating unexplained bank credits, tax authorities cannot selectively look at deposit entries while completely ignoring corresponding debit entries that explain the nature of the account.

-

Importance of Banking Narrations & Challans: Verifiable audit trails—such as bank statement narrations naming government departments matched with official tax challans—serve as conclusive evidence to prove the fiduciary nature of transactions.

-

Fiduciary Accounts Are Non-Taxable: Funds received by a professional in a fiduciary capacity (holding client money for specific statutory disbursements) do not constitute the personal income or “unexplained wealth” of the professional.

and MS. PADMAVATHY. S, Accountant Member

[Assessment year 2016-17]