ORDER

Vimal Kumar, Judicial Member.- The appeal filed by the assessee is against final assessment order dated 29.12.2021 passed by the Assessing Officer/National Faceless Assessment Centre, Delhi (hereinafter referred to as ‘Ld. AO’) u/s 143(3) r.w.s 144C(13) read with section 144B of the Income Tax Act ((hereinafter referred to as ‘the Act’) in pursuance to the order dated 27.12.2021 of the ld. Transfer Pricing Officer (for short ‘TPO’) to give effect to directions dated 23.11.2021 of Hon’ble Dispute Resolution Panel-1 (for short ‘DRP’) for Assessment Year 2017-18.

2. Brief facts of the case are that, the assessee filed return of income on 03.11.2016 declaring total income of Rs. 2,48,97,272/-. The case was selected for complete through CASS on following issues:

| i. |

|

Double taxation relief u/s 90/91 |

| ii. |

|

Claim of ‘Any other amount allowable as deduction’ in Schedule BP. |

| iv. |

|

Sales turnover/receipts |

| vi. |

|

International transaction (s) |

| vii. |

|

Other income reported in Schedule A-O1 |

| viii. |

|

Loss from currency fluctuations |

2.1 Notice u/s 143(2) dated 24.08.2018 was issued. The case was transferred to the Regional Assessment Unit for completing the assessment under the faceless assessment Scheme (FAS), 2019 on 25/01/2019. Notice under section 142(1) along with questionnaire was issued on 08.05.2019, 29.05.2019, 17.02.2021.

2.2 As per Form 3CEB filed by the assessee for the relevant period, the assessee has entered into international transactions with its associated enterprises. So, the matter was referred to the TPO for determination of Arm’s Length Price in respect of international transaction made with its AEs. The TPO has passed its order u/s 92CA(3) of the IT. Act, 1961, on 24.01.2021 and proposed adjustment of Rs. 16,13,42,640/-.

2.3 The draft order u/s 143 r.w.s 144C of the Act was passed on 23.04.2021 by Ld. A.O.

2.4 Against Draft Assessment Order dated 23.04.2021, the assesse filed objections with Hon’ble DRP-1, New Delhi. The Hon’ble DRP gave final order u/s 144C(5) of the Act on 23.11.2021.

2.5 The Transfer Pricing Officer- 2(1)(1), Delhi passed order dated 27.12.2021 giving effect of the order of Hon’ble DRP. Accordingly, adjustment is revised to Rs. 17,99,43,815/- consequent to directions of Hon’ble DRP-1, New Delhi. The relevant part of order giving effect of Hon’ble DRP by TPO-2(1)(1), Delhi reads as: – “Accordingly, adjustment of Rs. 16,13,42,640/- was proposed in respect of function of market research and testing services”.

3. On completion of proceedings, Ld. AO passed final assessment order dated 29.12.2021 u/s 143(3) r.w.s. 144C(13) r.w.s. 144B of the Act making following adjustment: –

| Particulars |

Amount in Rs. |

| Income as per return of income |

2,48,97,272 |

| Additions |

|

| 1. Addition on account of ALP adjustment |

17,99,43,815 |

| 2. Disallowance of Excess Depreciation on Intangible Assets |

7,12,35,869 |

| 3. Disallowance on account of 40(a)(ia) of the I.T. Act, 1961 |

87,52,386 |

| Total Income |

28,48,29,342/- |

| Rounded off |

28,48,29,340/- |

3.1 The assesse vide letter dated 24.02.2022 requested to allow the correction of working capital adjustment as directed by ld. DRP. Accordingly, adjustment on account of market research and testing services revised to Rs. 7,90,92,551/- u/s 154 of the Act. Consequential rectification order dated 20.01.2023 was passed by mentioning as under: –

| Particulars |

Amount in INR |

| Operating Cost |

180,59,39,280 |

| Arm’s length margin(%) |

7.4756% |

| Arm’s length margin(Rs.) |

13,50,04,406 |

| Arm’s length Price |

1,94,09,43,686 |

| Price charged by the assesse |

186,18,51,135 |

| Difference between ALP and Price charged by assesse |

7,90,92,551/- |

4. Being aggrieved, the appellant/assessee preferred present appeal against final assessment order dated 29.12.2021 on following: –

| “1. |

|

That, on the facts and circumstances of the case and in law, the Ld. AO erred in assessing the income of the Appellant for the relevant assessment year at INR 28,48,29,340 as against the returned income of INR 2,48,97,272. |

Grounds specific to Transfer Pricing Adjustments

| 2. |

|

That, on the facts and circumstances of the case and in law, the Ld. AO/Ld. TPO have erred in making an adjustment of INR 17,99,43,815 in pursuance to the order passed under section 92CA (3) of the Act read with provisions of section 144C of the Act. |

| 2.1. |

|

That, on the facts and circumstances of the case and in law, the Ld. AO/TPO have erred in computing the margins of the comparable companies and in considering the operating cost of the Assessee, while giving effect to the directions issued by Hon’ble DRP, thereby leading to an adjustment almost thrice the amount of adjustment computation based on such calculations. |

| 3. |

|

That, on the facts and circumstances of the case and in law, the Hon’ble DRP/Ld. AO/Ld. TPO have erred in the facts and law by rejecting the scientific analysis carried out by the Appellant which was consistent with the Indian transfer pricing regulations prescribed under the Income Tax Act, 1961 and Income Tax Rules, 1962. |

| 4. |

|

That, on the facts and circumstances of the case and in law, the Hon’ble DRP/Ld. AO/Ld. TPO erred in law in re-determining the price of the impugned international transaction involving “provision of basic market research and testing services”, as the circumstances necessitating the determination of price by the Learned TPO as mentioned in sub-section (3) of section 92C did not exist in case of the Appellant. |

| 5 |

|

That, on the facts and circumstances of the case and in law, the Hon’ble DRP/Ld. AO/Ld. TPO erred in rejecting Unimed Diagnostics Private Limited, India Tourism Development Corporation Limited and Medall Healthcare Private Limited from the final set of comparables, without establishing their functional non comparability, and failed to undertake appropriate functional, asset and risk analysis of comparable visa-vis the Appellant. |

| 5.1. |

|

That, on the facts and circumstances of the case and in law, the Hon’ble DRP/Ld. AO/Ld. TPO have erred in disregarding the order of higher appellate authorities (“Hon’ble High Court”) in the Appellant’s own case for the Assessment Year 2005-06 and applying a flawed approach in rejecting “India Tourism Development Corporation Ltd.”, which is also inconsistent with the directions issued order passed by Hon’ble DRP / Ld. TPO in Appellants’ own case in past years. |

| 6. |

|

That, on the facts and circumstances of the case and in law, the Hon’ble DRP/Ld. AO/Ld. TPO erred in including IGT Solutions Private Limited and Fuzen Software Private Limited in the final set of comparables, without establishing their functional comparability, and failed to undertake appropriate functional, asset and risk analysis of comparable vis-a-vis the Appellant. |

| 6.1. |

|

That, on the facts and circumstances of the case and in law, the Hon’ble DRP erred in including IGT Solutions Private Limited in the final set of comparables, ignoring the submission of the Appellant that the company is liable to be rejected as having significant related party transactions during the subject year and thereby not passing a speaking order to that extent. |

| 6.2. |

|

That, on the facts and circumstances of the case and in law, the Ld. AO/Ld. TPO have erred in including IGT Solutions Private Limited in the final set of comparables, without appreciating that the company is liable to be rejected even on the quantitative filter as having significant related party transactions during the subject year. |

| 7. |

|

Without prejudice to the contention that the analysis undertaken by the Ld. AO/Ld. TPO is flawed, the Ld. TPO has grossly erred in undertaking an opaque analysis by not sharing the search methodology, keywords used, criterions of selection/rejection of companies, number of companies rejected by way of applying various filters etc., used for identification of fresh companies considered as comparable for the purpose of arm’s length evaluation and also by not allowing the sufficient opportunity to the Appellant to present its case. |

| 8. |

|

That, on the facts and circumstances of the case and in law, the Ld. AO/Ld. TPO have erred in applying inappropriate filters on selective basis to: |

| • |

|

Reject companies having export income less than 70% of total income |

| • |

|

Reject companies having employee cost less than 25% of total cost |

| 9 |

|

That, on the facts and circumstances of the case and in law, the Hon’ble DRP/Ld. AO/Ld. TPO have erred in ascertaining the risk profile of the Appellant by comparing it against the companies bearing substantial entrepreneurial risk, without giving due cognizance to the fact that. Appellant indeed enjoys a “No Risk” status, ie, all expenses incurred by the Appellant get reimbursed with an arm’s length mark-up, irrespective of their commercial success. |

| 9.1. |

|

That, on the facts and circumstances of the case and in law, the Hon’ble DRP/Ld. AO/Ld. TPO have erred in not making suitable adjustments to account for differences in the risk profile of the Appellant (no risk) vis-a-vis the comparables (bearing full-fledged entrepreneurial risk). |

| 10. |

|

That, on the facts and circumstances of the case and in law, the Ld. AO has erred in initiating the penalty proceedings under section 270A of the Act alleging underreporting of the income in consequence to mis-reporting of income. |

Grounds specific to Corporate Tax Adjustments

| 11. |

|

That, the Learned AO erred in facts and in law in treating computer software as ‘Intangible assets eligible for depreciation at the rate of 25 percent as against treating it as ‘Computers including computer software’ eligible for depreciation at the rate of 60 percent as claimed by the Appellant, a position which is supported by various judicial precedents. |

| 12. |

|

That, the Learned AO erred in facts and in law by considering the amount of software reported in the audited financial statements for calculating tax depreciation under the Act instead of computing the same based on written down value of software as appearing in the block ofPlant & Machinery in the Return ofIncome (ROI). |

| 13. |

|

That, the Learned AO erred in facts and in law as tax depreciation claimed by the Appellant on computer software at 60% in the ROI amounts to INR 2,61,74,379/- is less than the tax depreciation allowed at 25% on the intangible assets amounting to INR 5,08,82,763/- as computed by the Learned AO. |

| 14. |

|

That, the Learned AO erred in facts and in law by invoking Section 40(a)(ia) of the Act on account of non-deduction of taxes on international travel expenses amounting to INR 2,91,74,619/- without appreciating the documentary evidences submitted by the Appellant which substantiate that applicable taxes have been duly deducted on the entire expenditure ofINR 2,91,74,619/- under the Act.” |

5. Ld. Authorized Representative for appellant/assessee, regarding transfer pricing adjustment ground of appeal Nos. 2 to 10 submitted that ld. AO/TPO erred in making an adjustment of Rs. 17,99,43,815/- in pursuance to the order passed u/s 92CA(3) of the Act read with provisions of section 144C of the Act. The ld. AO/TPO have erred in computing the marigns of the comparable companies and in considering the operating cost of the Assessee, while giving effect to the directions issued by Hon’ble DRP, thereby leading to an adjustment almost thrice the amount of adjustment computation based on such calculations. The Hon’ble DRP/Ld. AO/Ld. TPO have erred in the facts and law by rejecting the scientific analysis carried out by the appellant/assessee which was consistent with the Indian transfer pricing regulation prescribed under the Income Tax Act, 1961 and Income Tax Rules, 1962.

6. The Hon’ble DRP/Ld. AO/Ld. TPO erred in law in re-determining the price of the impugned international transaction involving “provision of basic market research and testing services”, as the circumstances necessitating the determination of price by the ld. TPO as mentioned in sub-section (3) of section 92C did not exist in case of the appellant/assessee.

7. The Hon’ble DRP/Ld. AO/Ld. TPO erred in rejecting Unimed Diagnostics Private Limited, India Tourism Development Corporation Limited and Medall Healthcare Private Limited from the final set of comparables, without establishing their functional non comparability, and failed to undertake appropriate functional, asset and risk analysis of comparable vis-a-vis the Appellant.

8. The Hon’ble DRP/Ld. AO/Ld. TPO have erred in disregarding the order of higher appellate authorities (“Hon’ble High Court”) in the Appellant’s own case for the Assessment Year 2005-06 and applying a flawed approach in rejecting “India Tourism Development Corporation Ltd.”, which is also inconsistent with the directions issued order passed by Hon’ble DRP / Ld. TPO in Appellants’ own case in past years.

9. The Hon’ble DRP/Ld. AO/Ld. TPO erred in including IGT Solutions Private Limited and Fuzen Software Private Limited in the final set of comparables, without establishing their functional comparability, and failed to undertake appropriate functional, asset and risk analysis of comparable vis-a-vis the Appellant.

10. The Hon’ble DRP erred in including IGT Solutions Private Limited in the final set of comparables, ignoring the submission of the Appellant that the company is liable to be rejected as having significant related party transactions during the subject year and thereby not passing a speaking order to that extent.

11. That, on the facts and circumstances of the case and in law, the Ld. AO/Ld. TPO have erred in including IGT Solutions Private Limited in the final set of comparables, without appreciating that the company is liable to be rejected even on the quantitative filter as having significant related party transactions during the subject year.

12. Without prejudice to the contention that the analysis undertaken by the Ld. AO/Ld. TPO is flawed, the Ld. TPO has grossly erred in undertaking an opaque analysis by not sharing the search methodology, keywords used, criterions of selection/rejection of companies, number of companies rejected by way of applying various filters etc., used for identification of fresh companies considered as comparable for the purpose of arm’s length evaluation and also by not allowing the sufficient opportunity to the Appellant to present its case.

13. That, on the facts and circumstances of the case and in law, the Ld. AO/Ld. TPO have erred in applying inappropriate filters on selective basis to:

| • |

|

Reject companies having export income less than 70% of total income |

| • |

|

Reject companies having employee cost less than 25% of total cost |

14. The Hon’ble DRP/Ld. AO/Ld. TPO have erred in ascertaining the risk profile of the Appellant by comparing it against the companies bearing substantial entrepreneurial risk, without giving due cognizance to the fact that. Appellant indeed enjoys a “No Risk” status, ie, all expenses incurred by the Appellant get reimbursed with an arm’s length mark-up, irrespective of their commercial success.

15. The Hon’ble DRP/Ld. AO/Ld. TPO have erred in not making suitable adjustments to account for differences in the risk profile of the Appellant (no risk) vis-a-vis the comparables (bearing full-fledged entrepreneurial risk).

16. Ld. Departmental Representative submitted that ld. TPO had conducted proceedings fairly. Marketing research testing based on data compilation mistake of 70% is to be ignored. India Tourism Development Corporation Limited, Unimed Diagnostics Pvt. Ltd. and Medall Healthcare Private Limited were rightly rejected to comparables. IGT Solutions Pvt. Limited as well as Fuzen Software Pvt. Ltd. were included properly. Figures mentioned by the assessee in the balance-sheet were taken into consideration.

17. From examination of record, in light of aforesaid contentions, it is crystal clear that the ld. AO/TPO has made an adjustment of Rs. 17,99,43,815/-in pursuance to the order dated 27.12.2021 of ld. AO/TPO giving effect to the directions dated 23.11.2021 of Hon’ble DRP.

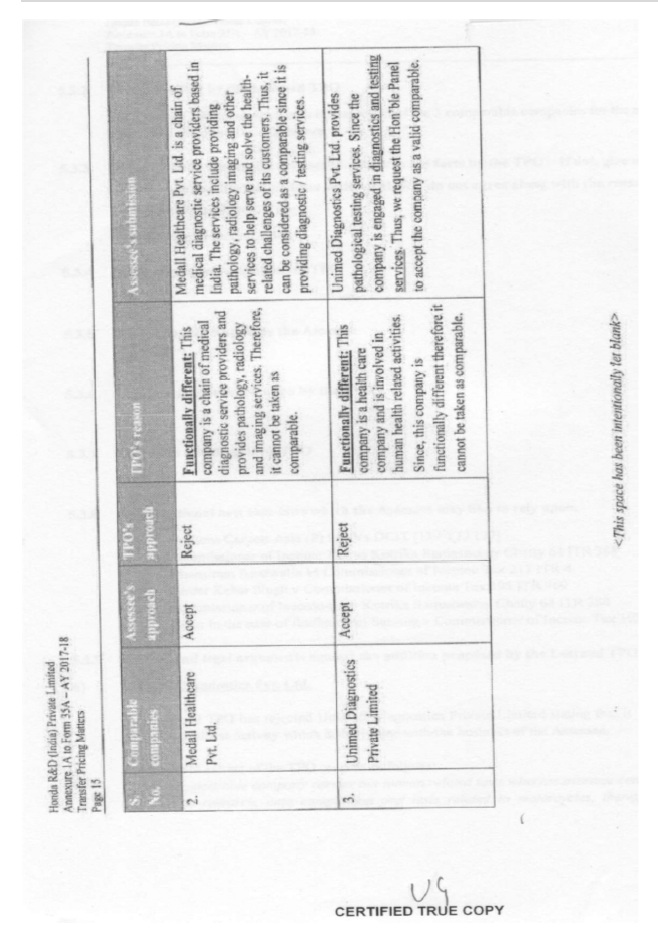

17.1 The appellant/assessee has challenged the action of ld. AO in rejecting scientific analysis carried out by the assessee which is consistent with the Indian Transfer Pricing Regulations prescribed under Income Tax Act, 1961 and Income Tax Rules, 1962 re-determining the price of the impugned international transaction involving “provision of basic market research and testing services” rejections of 3 comparables namely, India Tourism Development Corporation Ltd., Unimed Diagnostics Pvt. Ltd., and Medall Healthcare Pvt. Ltd. from the final set of comparables, without establishing their functional non comparability.

17.2 Hon’ble High Court of Delhi in the assessee own case in Honda R & D (India) (P.) Ltd. v. ACIT [IT Appeal No. 616 of 2015] for A.Y. 2005-06 decided on 02.08.2016 page no. 669 to 682 of Paper Book with para 27 providing as under:-

“27. As far as Question (ii) is concerned, as already noticed the ITAT overlooked the fact that the TPO in his remand report had accepted three comparables suggested by HRDI. The DRP in its order dated 12th July, 2011, gave cogent reasons why ITDC should be included as a comparable. This is consistent with the conclusion reached by the CIT(A). Consequently, Question (ii) is also answered in the negative, i.e., in favour of the Assessee and against the Revenue and it is held that the ITAT was not justified in remanding the matter to the CIT (A) on the issue of appropriate comparables.”

17.3 In view of above facts and judicial precedent, the action of ld. TPO in rejecting India Tourism Development Corporation Ltd. especially Ashok Events & Misc. Operations as a comparable, being illegal, is set aside. For aforesaid conclusion, the AO/TPO is directed to include India Terrorism Development Corporation Ltd. Especially Ashok Events & Misc. Operations in the list of comparables.

17.4 Ld. TPO had rejected Unimed Diagnostics Private Limited as a comparable as the company is a hospital and healthcare company involved in human health-related activities and was functionally different.

17.5 Ld. TPO held Medall Healthcare Private Limited company, as not a comparable, since the company is involved in a chain of Medical Diagnostics Service providing pathology, radiology imaging services. The company failed the export income and employee cost filters.

17.6 The assessee submitted functional analysis report as under: –

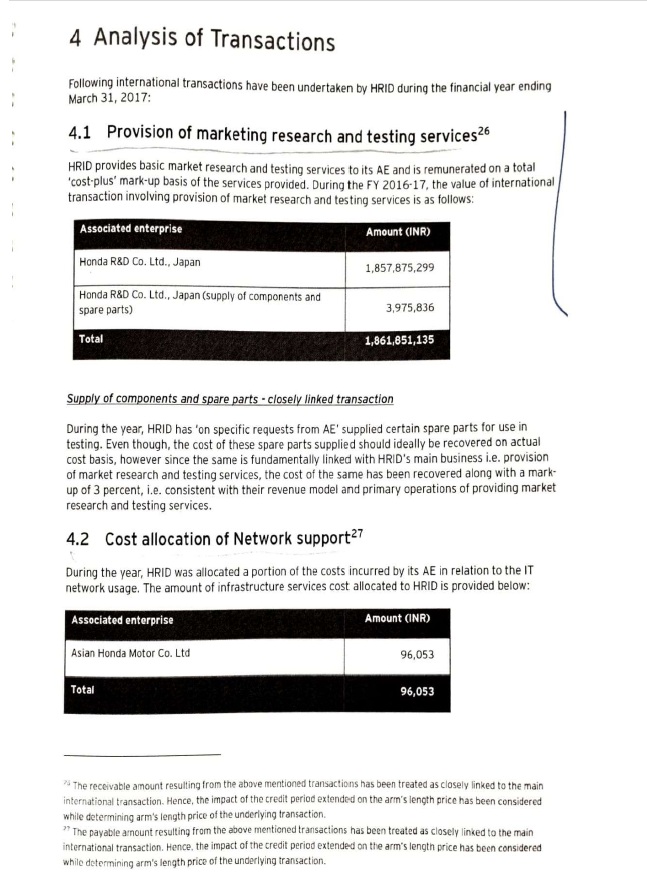

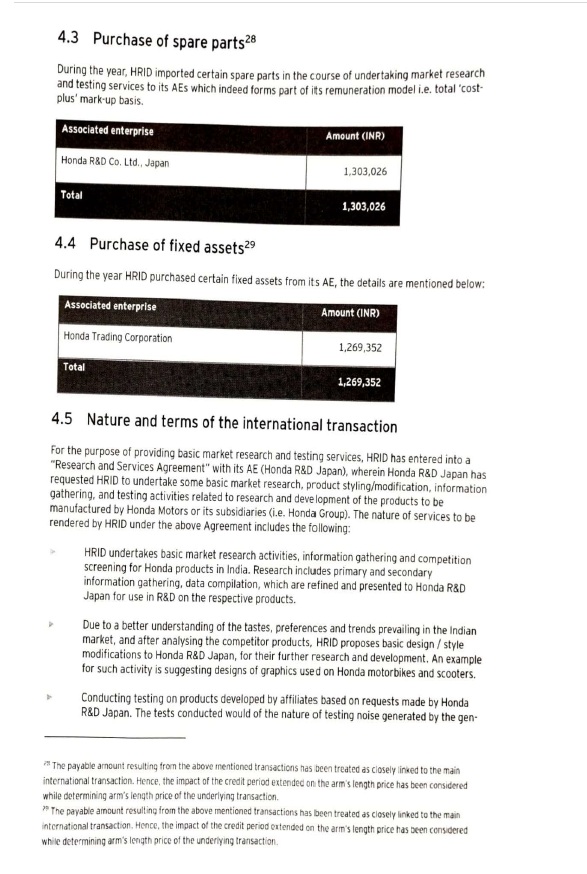

“Honda R& D (India) Private Limited (“HRID”) was incorporated under the provisions of the Companies Act, 1956 as a wholly owned subsidiary of Honda R&D Co. Ltd., Japan (“HG”). HRID is engaged in conducting basic market research and testing activity for two-wheeler and power products for HG and is remunerated on a cost-plus mark-up basis for the same.

HG is a fully integrated and independent unit of Honda Motor Co. Ltd., Japan (“HM Japan”) and serves as a central research and development organization for all Honda products. HG was spun off as an independent entity in 1960 from the research and development division of HM Japan.

The brief description of activities carried out by HRID are as follows:

For the purpose of providing market research and testing services, HRID has entered into a “Research and Services Agreement” with HG, wherein HG requests HRID to undertake certain basic market research, styling/modification

and testing activities related to research and development of the products to be manufactured by Honda Motors or its subsidiaries (i.c. Honda Group). The nature of services to be rendered by HRID under the above Agreement, for which it is being remunerated on a cost-plus mark-up, includes the following:

| • |

|

HRID provides support services in the form of market research activities, information gathering and competition screening for Honda products in India. Research includes primary and secondary information gathering, data compilation, which are refined and presented to HG for use in R&D on the respective products. The scope of work (ie. the nature of activities /analysis) to be performed by the HRID is identified and thereby sub-contracted by HG to HRID. |

| • |

|

Due to a better understanding of the tastes, preferences and trends prevailing in the Indian market, and after analysing the competitor products, HRID proposes basic design / style modifications to HG, for their further research and development. An example for such activity is suggesting designs of graphics used on Honda motorbikes and scooters. |

| • |

|

HRID is engaged in conducting testing on products developed by affiliates based on requests made by HG. The tests conducted are in the nature of testing noise generated by the gen-sets, rusting conditions of motorcycles, mileage achieved on Indian roads, etc. These tests are conducted by HRID to review the feasibility of products manufactured for the Indian climate and environmental conditions. |

| • |

|

Preparing proposals or information assessment on basic product styling variations depending on the preferences, tastes, trends, etc. prevailing in the Indian market. This would involve assistance in modifying existing styles and designs based on customer feedback. |

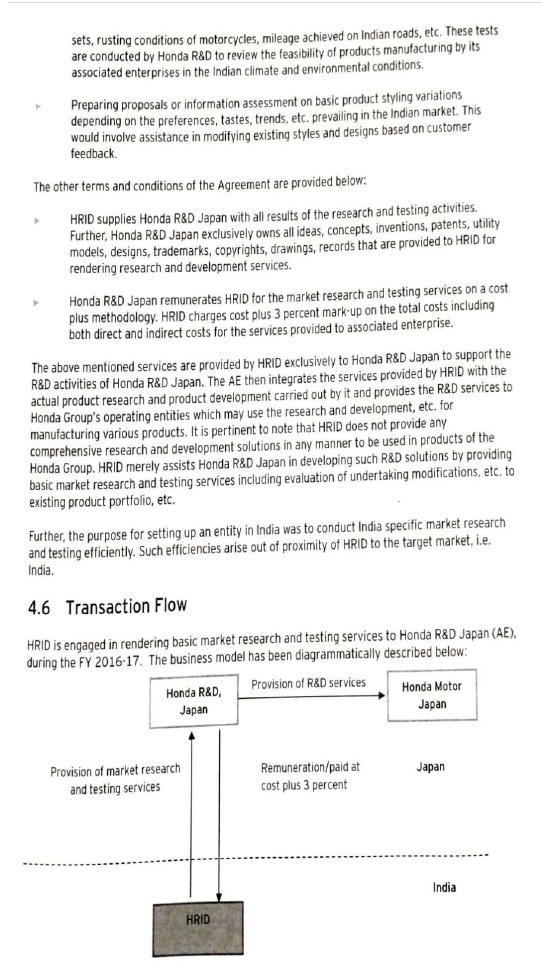

17.7 The diagrammatic representation of the flow of the international transaction is given below:

17. 8 Ld. Authorized Representative for appellant/assessee referred to transfer pricing, drew our attention to page no. 63 of appeal set as under:

17. 9 Annual report of Unimed Diagnostics Private Limited is at page no. 1122 to 1153 of paper book. Unimed Diagnostic P. Ltd. provides pathology testing services.

17.1 0 Transfer pricing paper book Volume II contains annual report of Medall Healthcare Private Limited at page 24 to 281 of paper book. Medall Healthcare Private Limited provides services of pathology, radiology, imaging and other services to help, serve and solve the health-related challenges of its customers, therefore, Medall Healthcare Pvt. Ltd.

17.1 1 On comparative study of the assesse, it is evident that the assesse provides market research and testing services by primarily gathering information data compilation. On the other hand, the annual report of unimed Diagnostics Private Limited and Medall healthcare Private Limited are providers of pathology, radiology, imaging and other services and healthcare related activities. In view of above different functions of the assesse and Unimed Diagnostics Private limited and Medall Healthcare Private Limited cannot be considered as a comparables.

17.1 2 Therefore grounds of appeal No. 5 and 5.1 are partly accepted.

18. In para No. 13.2 on page No. 168, Ld. TPO regarding IGT Solutions Pvt. Ltd. observed that the company refers in software maintenance, Data Processing/ Contact Centre Income & Software Development and Maintenance charges. The website of company mentions that;

“Big Data Analytics is the central pillar for any data innovation and serves as a primary driver for organizations in their digital transformation journey. Big Data can help companies with the identification of new revenue opportunities, enhanced customer experience, targeted marketing, cost optimization and improved operational efficiency”.

18.1 So, it is evident that the IGT Solutions has a different profile than that of the Assessee Company. Therefore, Ld. AO erred in including IGT Solutions Private Limited liable to be rejected.

19. Regarding Fuzen Software Private limited, ld. TPO in para No. 13 discussed principal business activities of the company as Data Processing and Export 100% which is a different profile from that a assessee company cannot be considered as a comparable. Accordingly, Grounds No. 6 to 6.2 are accepted.

20. Ground of appeal No. 7 is consequential in nature.

21. Ground of appeal No. 8 mentions that Ld. AO/TPO erred in applying inappropriate filters on a selective basis i.e., rejected companies having export income less than 70% of total income and rejected companies having employee cost less than 25% of total cost. Ld. AO erred in not following the rule of consistency in Assessment Year 2013-14, IDMA and ITDC were considered as comparables. Further, ld. AO/TPO failed to follow directions of the DRP thereby violated provisions of Section 144C of the Act. The additional evidence produced before Ld. DRP was not considered by Ld. AO. Therefore, Ground of appeal No. 8 to 10 are accepted.

22. The assessee had filed details relating to computers at page No. 148 of paper book. The corporate tax adjustments were challenged in Grounds No. 11 to 14. The copies of invoices in relation to computer software purchased during the year, on sample basis are at page Nos. 157-177 of paper book and the details of tax depreciation on computer software and hardware are at page Nos. 138-156 of Paper Book. The Ld. AO erred in facts and in law in treating computer software as ‘Intangible assets eligible for depreciation at the rate of 25 percent as against treating it as ‘Computers including computer software’ eligible for depreciation at the rate of 60 percent as claimed by the Appellant. The Ld. AO erred in facts and in law by considering the amount of software reported in the audited financial statements for calculating tax depreciation under the Act instead of computing the same based on written down value of software as appearing in the block of Plant & Machinery in the Return of Income (ROI). The Ld. AO not appreciating in facts and in law as tax depreciation claimed by the Appellant on computer software at 60% in the ROI amounts to INR 2,61,74,379/- is less than the tax depreciation allowed at 25% on the intangible assets amounting to INR 5,08,82,763/-as computed by the Learned AO.

22.1 A Co-ordinate Bench in Honda R & D (India) (P.) Ltd. v. Addl./Jt./Dy./Asstt. CIT [IT Appeal No. 703 (Delhi) of 2021, dated 15-1-2025] in assessee’s own case in para No. 9 held as under:

“9. The next issue in appeal is with regard to assessee’s claim of depreciation at the rate of 60% on intangible assets i.e. computer software. We find that the DRP while dealing with this issue had observed as under:-

“16.1.2. In Ground number 2 the assessee has contended disallowance of Rs.61,972,744/- as excess tax depreciation on computer software treated as intangible assets by the AO. The Panel directs the AO to verify the details of computer software provided by the assessee and treat the same as intangible asset if it involves kind of patent etc. and determined the rate of depreciation as per the Act. Ground number 2 is disposed off.”

The AO is directed to comply with the directions of the DRP and decide the issue, accordingly. Thus, ground no. 17 to 19 of appeal are allowed for statistical purpose.”

In view of above material facts and the judicial precedents, the AO is directed to comply with the directions of DRP and decided the issue of claim of depreciation @ 60% on intangible asset i.e. computer software. Accordingly, Grounds of Appeal Nos. 11 to 13 are allowed for statistical purposes.

22.2 In Ground of Appeal No. 14, the assesse assailed disallowance made u/s 40(a)(ia) of the Act for non-deduction of taxes on International Travel Expenses. The Learned AO erred in facts and in law by invoking Section 40(a)(ia) of the Act on account of non-deduction of taxes on international travel expenses amounting to INR 2,91,74,619/- without appreciating the documentary evidences submitted by the Appellant which substantiate that applicable taxes have been duly deducted on the entire expenditure of INR 2,91,74,619/- under the Act.

22.3 A Co-ordinate Bench in ITA No. 703/Del/2021 titled as Honda R & D (India) (P.) Ltd. (supra) in assessee’s own case in para No. 10 observed as under:

“10. In ground no. 20 of appeal, the assessee has assailed disallowance made u/s. 40(a)(ia) of the Act for non deduction of taxes on payment for International Travel Expenses. The short contention of ld. Counsel for the assessee is that the AO while passing final assessment order has not complied with the directions of the DRP. The DRP in para 16.1.3 of the order had given following directions in this regard:-

“16.1.3. Ground number 3 is with reference to disallowance under 40a(i)(a) of the Act. Vide submissions dated 27.07.2020 the assessee has submitted that out of Rs.8,988,520/- of disallowance so made, taxes on international travel expense of Rs.30,355,292/-was duly deducted and deposited. The AO is directed to verify this contention of the assessee and take necessary action as per law. Ground number 3 is disposed off.”

The AO is directed to decide this issue in accordance with the aforesaid directions. Ergo, ground no. 20 of appeal is allowed for statistical purpose.”

In view of above material facts by following the judicial precedents, the Ld. AO is directed to decide the issue afresh in accordance with law. Accordingly, Ground of Appeal No. 14 is allowed for statistical purposes.

23. In view of above decision of appeal, Stay Application has been rendered infructuous.

24. In the result, the appeal filed by the assessee is partly allowed and Stay Application is dismissed as infructuous.