ORDER

Brajesh Kumar Singh, Accountant Member. – These two cross appeals filed by the Revenue (ITA No.- 1821/Del/2024) and Assessee (ITA No.- 1449/Del/2024) are directed against the order dated 26.02.2024 of the National Faceless Appeal Centre, (NFAC) Delhi, [hereinafter referred to as the ‘Ld. CIT(A)] arising out of the assessment order dated 30.09.2021 passed under section 143(3) r.w.s. 144B of the Income Tax Act, 1961 (hereinafter referred to as the ‘the Act’) by the National Faceless Centre (NFAC), Delhi (hereinafter referred to as the ‘AO’) pertaining to Assessment Year (A.Y.) 2018-19. The two cross appeals were heard together and are being disposed of by way of this common order for the sake of convenience and brevity.

First, we take up the Revenue’s appeal in ITA No. 1821/Del/2024 for A.Y. 2018-19.

2. Brief facts of the case are: During the year, the assessee company was engaged in the business of broadcasting of news channels and FM radio broadcasting and the main source of income was from advertisement while broadcasting of news and FM radio broadcasting. The assessee filed its return of income for A.Y. 2018-19 on 01.12.2018 declaring total income at Rs. 1,83,72,00,100/- as per normal provisions of the Act and book profits of Rs. 1,23,47,00,498 as per provisions of section 115JB of the Act.

2.1 The return was processed and intimation under section 143(1) of the Act was issued and sent to the assessee. As per the said intimation, income as per normal provisions of the Act was arrived at Rs. 1,85,29,29,590/- and Rs. 1,87,92,26,859/- u/s 115JB of the Act. The return was selected for scrutiny under CASS (Computer Aided Scrutiny Selection). Subsequently, notice u/s 143(2) of the Act was issued on 22.09.2019 and the same was duly served upon the assessee through e-filing portal / ITBA. Further, vide a letter dated 15.10.2020, the assessee was intimated by the AO that the assessment proceedings shall now be completed under Faceless Assessment Scheme, 2019. Further, various notices u/s 142(1) of the Act as specified above were also issued and duly served upon the assessee through ITBA / e-filing portal during the course of assessment proceedings. In response to the notices issued, the assessee furnished the details called for electronically through e-filing portal. The additions are discussed issue wise hereinafter.

3. Disallowance of Interest Expenditure claimed as revenue Expenditure – Rs. 10,33,85,802/- .

3.1 The facts as summarized by the Ld. CIT(A) regarding this addition are reproduced as under:

“6. Disallowance of Interest Expenditure claimed as revenue expenditure

During the course of assessment proceedings, the AO observed that the appellant claimed an expenditure towards interest payment for delayed payment of license fee/renewal fee to the Ministry of Information and Broadcasting (MIB). The background of the issue is that the appellant had entered into a Grant of Permission Agreement (GOPA) with MIB to start operation its seven radio channels. The phase I commenced from the date of approval. After starting of Phase II, the appellant company sold its four radio channels to Entertainment Network India Ltd on 18.09.2015. For the remaining three Radio Channels, the appellant had applied to migrate these channels to phase III, for which the MIB declined the proposal of the company. The appellant after obtaining interim relief from the High court on this issue, paid renewal fee to the MIB to the tune of Rs. 71,36,79,767/-. The MIB also charged interest for delayed payment of license fee to the tune of RS. 13,78,47,736/-. The renewal fee for migration the channels to the phase III was capitalized by the appellant and the interest paid was claimed as revenue expenditure. The AO after analyzing the matter, observed that the interest paid for delayed , payment of license fee was also in the nature of capital expenditure. The AO after referring the section 37(1), treated the expenditure as capital in nature and after allowing 25% of depreciation on the interest paid arrived at the amount of disallowance of expenditure to the tune of Rs. 10,33,85,802/-(Rs. 13,78,47,736/- less depreciation of Rs. 3,44,61,934/-) and added it to the total income of the appellant. “

(emphasis supplied by us)

4. Aggrieved with the said order, the assessee filed an appeal before the Ld. CIT(A). The Ld. CIT(A) allowed the appeal of the assessee and the relevant extract of the said order is reproduced as under:

“7. Ground No. 1

The appellant through this ground of appeal agitated that the AO disallowed the expenditure claimed towards the interest paid for delayed payment of license fee/renewal fee. The appellant through its written submission argued that:

“1. The Assessee Company has been running radio stations for the last many years. During the month of December 2006, the assessee company entered into Grant of Permission Agreement (GOPA) with Ministry of Information and Broadcasting (MIB) and from the dates starting thereafter operationalized its 7 radio stations (i.e. Delhi, Mumbai, Kolkata, Amritsar, Jodhpur, Patiala and Shimla).

2. During the current assessment year the Assessee Company has paid renewal fees/license fees and capitalized the said expense in its books of accounts.

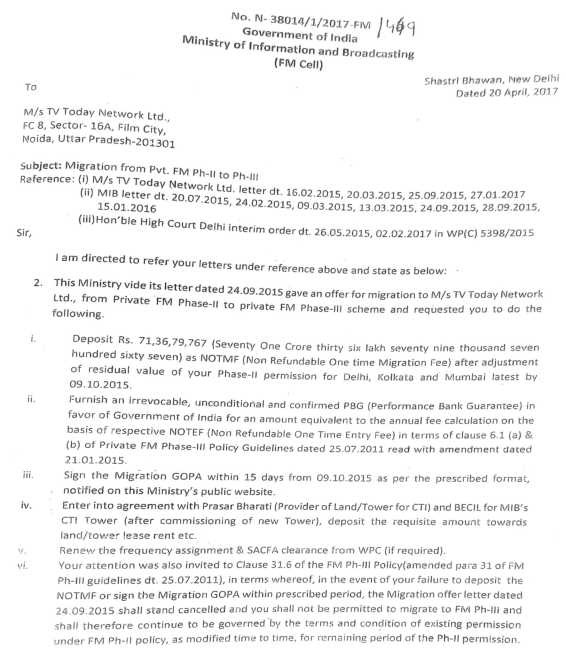

3. Based on letter dated 20.04.2017 from MIB it has also, paid interest to MIB as it has made delayed payment of renewal fees/license fees. As the interest has been paid by the Assessee Company on account of delayed payment of license fees and not for making the radio channels operational, hence the interest expense has been treated as revenue expenditure. The calculation of interest of Rs. 13.78 Cr along with copy of MIB letter dated 20.04.2017 raising said demand of interest had already been submitted during assessment proceedings.

4. Brief facts and note/ history of radio business are as under:-

December 2006 The Assessee entered into Grant of Permission agreement (GOPA) with Ministry of Information & Broadcasting (MIB) for making its 7 radio stations operational namely Delhi, Mumbai, Kolkata, Amritsar, Jodhpur, Patiala, and Shimla.

July 2011-MIB notified migration policy from Phase -Il to Phase – III

Dec 2013- MIB notified that all FM radio operators allowed to migrate to Phase-III on or before 30th June 2014

July 2014 MIB notified extension of timeline for migration to phase – III and new date fixed for migration was on or before 31st March 2015

Dec 2014 The assessee entered into agreement with Entertainment Network India Ltd (ENIL) to sell/transfer its all 7 stations. MIB gave permissions to sell /transfer of four stations but denied permission to sell/transfer three radio stations i.e. Delhi, Mumbai, and Kolkata. Thereafter, the assessee sold its four stations i.e. Amritsar, Jodhpur, Patiala, Shimla to ENIL as going concern on slump sale basis on 18th September 2015 after obtaining approval from MIB on 20th July 2015

May 2015 The assessee filed writ petition before Delhi High Court against such denial to sell three radio stations by MIB. MIB has demanded 71.36 Cr towards migration fees from Phase II to Phase III. The assessee obtained interim relief till the disposal of above writ petition.

Jan 2017 – The assessse withdrew above writ petition through which the order of MIB was challenged for denial of the sale of Radio business to ENIL. The assessee filed fresh application with MIB seeking approval for migration of its radio stations to Phase-III regime.

April 2017 The assessee received offer letter from MIB for migration of its three radio stations and demanded Rs 71.37 Cr as migration fees and Rs 13.78 Cr as Interest on delayed migration fees

May 2017 The assessee executed GOPA on 23.05.2017 for its three radio stations. Accordingly the assessee has paid the migration fees of 71.37 Cr along with interest of Rs 13.78 Cr in April and May 2017. The Company now stands migrated to Phase III with effect from 1st April 2015 for 15 years with respect to three radio stations. The assessee has capitalized migration fees of Rs 71.37 Cr in its books of accounts and claimed interest of Rs 13.78 Cr on delayed payment of migration fees as revenue expenditure in its Profit and Loss Account. We would like to further mention that all these radio stations were continued to be operational from April 2015 without any break and carried on broadcasting activities till the date when it paid license fees along with delayed payment of interest

5. As per para 3.3 of Assessment Order dated 30.09.2021, the learned Assessing Officer stated that “the interest of Rs 13.78 Cr , paid by the Company for migration of its three FM radio stations is in the nature of capital expenditure as migration of 3 FM radio stations was conditional upon the , payment of migration fees and interest. ” Here we would like to mention that correct facts have not been stated in the said statement as interest, payment was not conditional for radio station to continue but the interest was paid only since the license fees was not paid by Assessee Company within due time as per MIB. As the interest has been paid by the Assessee Company on account of delayed payment of license fees and not for running the radio channels, hence the interest expense has been treated as revenue expenditure.

6. Based on the judgment given by Delhi High Court in case of “MICROWAVE COMMUNICATIONS LTD (ITA 1738 & 1739/2010)”, the Apex Court has held that interest on delayed payment of license fees is revenue expenditure. Further, In the case of “Bharti Telenet Ltd v. DCIT (ITA Not 3309/Del/05 for AY 2001-02)” Delhi Tribunal has held that upfront fees charged by the banks on process of loan is revenue expenditures.”

7.1 The contention and the related submission of the appellant have been duly perused. It is settled law that the expenditure towards license fee and renewal of license fee is capital in nature Here question arises as whether the expenditure being interest , paid towards delayed payment of license fee is revenue expenditure or capital expenditure. The appellant has narrated in its submission that the license for commencing the operation was given by the MIB through Grant of Permission Agreement in 2006 and the same was required to be renewed. The appellant further stated as to why the interest for delayed payment was made to renew the license for commencing the operation of three radio channels in the phase III. The circumstances were arised for the appellant to close the issue for operation of the channels. The appellant further had made the payment on the basis of the estimation of the interest made by the MIB.

7.2 The undersigned has also gone through the decision of the Hon’ble High Court of Delhi in the Case of MICROWAVE COMMUNICATIONS LTD as relied upon by the appellant. Further, the undersigned has relied upon the decision of jurisdictional Hon’ble High Court ofDelhi in the case of Bharti Hexacom Ltd. in IT APPEAL NOS. 893, 1328, 1333, 1336, 1679 & 1680 OF 2010, 996 OF 2011, 114 & 177 OF 2012 AND 417 OF 2013 in which it was held that the expenditure related to continue the business is revenue in nature as it does not acquire any new assets.

7.3 It is also noticed from the record that the appellant got the license in the year 2006 and the same was being continued on the renewal of the said license in the phase manner like phase I, Phase II and Phase III. Therefore it cannot be said that the appellant acquired any new asset, only the expenditure towards interest paid to run the already established entity. Therefore following the decision of Hon’ble High court, and the discussion made above, the contention of the appellant is hereby accepted and the claim of the appellant in treating the interest , paid for delayed , payment of license fee is revenue in nature is allowed. Accordingly, the Ground No. 1 raised by the appellant is hereby allowed. ”

(emphasis supplied by us)

5. Aggrieved with the said order, the Revenue is in appeal before us on the following grounds of appeal:

“1. Whether, on the facts and circumstances of the case and in law the Ld. CIT(A) has erred in deleting the addition of Rs. 10,33,85,802/- on account of disallowance of interest expenditure.

6. At the time of hearing before us, the Ld. CIT(DR) relied upon the grounds of appeal and the assessment order.

7. On the other hand, the ld. Sr. Counsel for the assessee, while relying upon the order of the Ld. CIT(A) filed a brief synopsis and relied upon certain case laws. The said submissions and the case laws relied upon are reproduced as under:

Submission

“i. Reliance is placed on findings of learned CIT (A) at pages 12 to 15 and also case laws enclosed at S. No. 1 to 3 of PB-II.

ii. Reliance is also placed on Assessee’s reply dated 19.05.2021 before AO at pages 160 to 161 of PB – I and submission at pages 184 to 186 before CIT (A) along with letter issued by Ministry of Information & Broadcasting dated 20.04.2017 at pages 197 to 198 of PB -I, submitted that assessee is running its FM business for past many years i.e. right form December 2006 and as such, any amount paid for delayed interest has rightly been taken as revenue expenditure by ld CIT (A) as no new asset has been acquired by the assessee company”

Judgment to be relied upon

| • |

|

Bharti Airtel Ltd. v. PCIT (Delhi – Trib.) at pages 8 to 40, relevant pages 8 and 29 of PB – II |

| • |

|

Jetha Lal Properties (P) Ltd. v. CIT (Bombay) at [ages 1 to 4, relevant pages 1 and 4 of PB-II. |

| • |

|

Rajasthan Central Stores (P.) Ltd. v. CIT [1985] 156 ITR 90 (Rajasthan) at pages 5 to 7, relevant page 5 of PB – II. |

8. We have heard both the parties and perused the material available on record. In this case, the facts that are undisputed, is that the assessee executed on 23.05.2017 Grant of Permission Agreement (GOPA) with the Ministry of Information and Broadcasting, for its three radio stations namely Delhi, Mumbai and Kolkata for migrating it to Phase -III. Earlier, the assessee had challenged by way of writ petition before the Hon’ble Delhi High Court through which the order of MIB was challenged for denial of the sale of Radio business to ENIL. Thereafter, the assessee withdrew its writ petition and filed a fresh application with MIB seeking approval for migration of its radio stations to Phase-III regime. In April 2017, the assessee received offer letter from MIB for migration of its three radio stations to Phase-III demanding Rs 71.37 Cr as migration fees and Rs 13.78 Cr as Interest on delayed migration fees. Accordingly, the assessee paid the migration fees of Rs. 71.37 Cr along with interest of Rs 13.78 Cr in April and May 2017 and the company stood migrated to Phase III with effect from 1st April 2015 for 15 years with respect to three radio stations namely, Delhi, Mumbai and Kolkata. The assessee thereafter capitalized migration fees of Rs 71.37 Cr in its books of accounts and claimed interest of Rs 13.78 Cr on delayed payment of migration fees as revenue expenditure in its Profit and Loss Account. Further, all these three radio stations namely, Delhi, Mumbai and Kolkata continued to be operational from April 2015 without any break and carried on broadcasting activities till the date when the assessee company paid the license fees along with delayed payment of interest. Further, the Ld. AR submitted that as per para 3.3 of Assessment Order dated 30.09.2021, the learned Assessing Officer stated that “the interest of Rs 13.78 Cr paid by the Company for migration of its three FM radio stations is in the nature of capital expenditure as migration of 3 FM radio stations was conditional upon the payment of migration fees and interest” was not correct because interest payment was not conditional for radio station to continue but the interest was paid only since the license fees was not paid by Assessee Company within due time as per the GOPA with the Ministry of Information and Broadcasting. It has been further submitted that as the interest had been paid by the Assessee Company on account of delayed payment of license fees and not for running the radio channels, hence the interest expense has been treated as revenue expenditure. In this regard, the Ld. CIT(A) very aptly summed u/s the dispute in this case by posing the question that arose in this appeal was to as whether the expenditure being interest paid towards delayed payment of license fee was revenue expenditure or capital expenditure. In this regard, on similar facts, the Co-ordinate Bench of the Tribunal in the case of Bharti Airtel Ltd.(supra).) held as under:

” 10.8 After taking into consideration the aforesaid relevant clauses, we are of the considered view that the interest and penalty clauses are enshrined in the license agreement as compensatory mechanism for delayed. payment of three components i.e. entry fee, license fee and charges. Charges is not specifically defined but when we take into consideration the aforesaid clauses we find that apart from entry fee and license fee the Licensee was supposed to pay Radio Spectrum Charges and royalty for the use of spectrum for point to point links and access links. These charges admittedly were considered as revenue expenditure. Thus sub clause 10.2 mentions that for delayed payment of fee and other charges due to this provision of clause of termination of license can be invoked. It is very much apparent from the clauses of license agreement that the interest is payable on the quantum of delayed payment of license fee determined as per the license agreement. Penalty is payable in case the total amount paid as quarterly License Fee for the 4 (four) quarters of the financial year, falls short by more than 10% of the payable License Fee, Delayed payment of penalty shall also be liable to interest.

10.9 Therefore, in case of default in payment of three components referred above, which are part of consideration for license, the licensor has right to revoke or terminate the license but in case of default in payment of interest and penalty the licensor Department of Telecommunication had no right for suspension, revocation and termination of the license agreement. Thus the principle which Hon’ble Supreme Court has accepted, that the failure to pay the variable annual license fee will lead to revocation of the license vindicates the legal position that the said fees is paid towards the right to operate the telecommunication services and then to hold that license fee is part ofcapital expenditure, is not applicable in case of interest payments or penalty. Thus, in the absence of rights of revocation/termination of the agreement for default in payment of penalty/interest cannot be equated with consequences arising out of default in payment of the license fee which as per the judgement of the Hon’ble High Court in the case of Bharti Hexacom (supra) was similar to one time entry fee. Therefore, the interest/penalty , payment arising out of default in , payment of the license fee is merely compensatory in nature. “

(emphasis supplied by us)

8.1 In the present case, the letter dated 20.04.2017 (placed at page no. 197-198 of the P.B.) of the MIB regarding the terms and conditions of payments of Rs. 71.37 crores and Rs. 13.78 crores are reproduced as under:

8.2 Upon perusal of the same, at srl. no. 3 (ii) and (iii) it is seen that the payment of Rs. 3,40 21,994/-Rs. 10,38,25,741/- are for the payment of Non Refundable One Time Migration Fee (NOTMF) which is compensatory in nature. Therefore, in view of the facts, as discussed above, and relying upon the above order of the Co-ordinate Bench of Tribunal in the case of Bharti Airtel Ltd.(supra), we hold that the payment of Rs. 3,40 21,994/-Rs. 10,38,25,741/- are for the payment of Non Refundable One Time Migration Fee (NOTMF) are compensatory in nature and allowable as revenue expenditure. Therefore, we uphold the findings of the Ld. CIT(A). Ground no. 1 of the appeal is dismissed.

9. Disallowance u/s 14A of the Act- Rs. 67,71,000/-.

10. The facts as summarized by the Ld. CIT(A) in respect of this disallowance u/s 14A of the Act are reproduced as under:

“During the course of assessment proceedings, the appellant observed that the appellant has made investments in equity share and during the year the appellant company has total 6771 lakhs of investment. The appellant submitted that it has not made any expenditure towards the investment made. The AO did not satisfy with the response of the appellant. The AO referred the CBDT’s Circular 5/2014 dated 11.02.2014 in which the calculation of disallowance was narrated even when there is no exempt income was earned. Accordingly the AO calculated the disallowance u/s. 14A rwr 8D of the IT rules and made disallowance to the tune of Rs. 67,71,000/. The calculation of disallowance u/s. 14A rwr 8D was made as under:

11. Aggrieved with the said order, the assessee filed an appeal before the Ld. CIT(A). The Ld. CIT(A) allowed the appeal of the assessee and the relevant extract of the said order is reproduced as under:

“10.1 The contention of the appellant and related submission has been duly perused. On the issue of disallowance u/s. 14A of the Act, the core matter is related to whether any investment made yield any income during the year. In the instant case, the appellant did not receive any exempt income out of such investment. In the appellant own case for the AY 2012-13, the High Court has rendered its decision of which relevant para is reproduced as under:

“25. During the scrutiny proceedings, the AO observed that the assessee has made investments in its subsidiary and associate company and earned exempt income of Rs. 2,34,585/- in the relevant assessment year. The assessee had made a suo moto disallowance of Rs. 29,04,491/ However, the AO proceeded to invoke the provision of Section 14A of the Act r/w Rule 8D of the Income Tax Rules, 1962; computed a disallowance of Rs. 38, 94, 755/- and made an addition of Rs. 9,90,264/-. The CIT (A) reversed the said disallowance and deleted the addition on the ground that the AO has failed to record his satisfaction before invoking the provisions of Section 14 A of the Act and relying upon the decisions of this Court.

26. The ITAT in the impugned order has upheld the finding of the CIT (A) after observing that it is a settled principle of law that disallowance u/s 14A of the Act cannot be more than the exempt income and finding that AO had mechanically invoked the provisions of Section 14A without recording its satisfaction.

27. The learned counsel for the revenue has not disputed that the exempt income earned by the assessee in this assessment year was Rs. 2.34,585/- and the assessee has already made a suo moto disallowance of a sum of Rs. 29,04,491/-under Section 14 A in its computation.

28. As per the law settled by this court in the case of Cheminvest Ltd. v. CIT) (Del.); and PCIT v. IL & FS Energy Development Company Ltd. reported in 2017 SCC OnLine Del 9893, the disallowance to be made under Section 14A cannot be in excess of the exempt income earned by the assessee. The counsel for the revenue has placed reliance on the CBDT circular 5/2014 to contend that disallowance under Section 14A would be attracted even if corresponding exempt income is not earned during the financial year. The said circular cannot be relied upon since its contrary to the law laid down by this Court.

29. Further, there is no challenge to the finding of the CIT (A) and the ITAT that AO failed to record satisfaction before invoking the provisions of Section 14A of the Act, which is the condition precedent for making the addition. In this view of the matter the additional disallowance of Rs.9,09,264/- made by the AO is impermissible and contrary to law. The ITAT was correct in upholding the order of the CIT(A) deleting the disallowance of Rs.9,09,264/

10.2 While delivering the above said order, the Hon’ble High court has emphasized that it is a settled principle of law that disallowance u/s 14A of the Act cannot be more than the exempt income. On the basis of this principles, the disallowance made by the AO u/s. 14A was deleted. Further, it is also noticed from the record that the similar issue was also involved in the appellant’s case for the AY 2013-14 and AY 2016-17 as well in which the CIT(A) has deleted the addition u/s. 14A rwr 8D by the AO.

10.3 In the instant case, the appellant has submitted two important things. First, the appellant company has not earned any exempt income from the investment and second, the investment in did not fall under the category of exempt income in the year under consideration. The contention of the appellant has been duly considered and as the Hon’ble Jurisdictional High Court has given the decision on the similar issue in the favor of the appellant. Therefore, considering the facts and respectfully following the decision of the Hon’ble High Court in the appellant’s own case and following the principles of consistency, it is the undersigned’s considered view that as the appellant did not earn any exempt income during the year from the investment in question, the disallowance made by the AO was not warranted. Therefore the addition made by the AO to the tune of Rs. 67,71,000/- is hereby deleted. Accordingly, the ground No. 4 filed by the appellant is allowed.”

12. Aggrieved with the said order, the Revenue is in appeal before us on the following ground of appeal:

“2. Whether, on the facts and circumstances of the case and in law the Ld. CIT(A) has erred in deleting the addition of Rs. 67,71,000/- on account of disallowance u/s 14A of the I.T. Act, 1961 read with Rule 8D of the I.T. Rules, 1962.”

13. At the time of hearing before us, the Ld. CIT(DR) relied upon the order of the AO and the grounds of appeal.

14. On the other hand, the ld. Sr. Counsel for the assessee, while relying upon the order of the Ld. CIT(A) filed a brief synopsis relying upon certain case laws. The said submissions are reproduced as under:

Submission

| i. |

|

Since assessee company has earned no exempt income, section 14A disallowance does not arise. |

| ii. |

|

Reliance is placed on the judgment of High Court of Delhi in the case of Cheminvest Ltd. v. CIT (Delhi). |

Judgment to be relied upon

| • |

|

Reliance is placed on the judgment of High Court of Delhi in the case of Cheminvest Ltd.(supra) at pages 40A to 40F of PB II, relevant page 40A of PB – II. |

15. We have heard both the parties and perused the material available on record. In this case, it is undisputed that the assessee company has not earned any exempt income from the investments considered for disallowance by the AO during the year and secondly, the Revenue has not disputed the claim of the assessee that investments considered for disallowance by the AO do not fall under the category of yielding exempt income in the year under consideration. Therefore, in the given facts of the case, the order of the Ld. CIT(A) is justified and no interference is called for in the said order and the same is upheld. Ground no. 2 of the appeal is dismissed.

16. Disallowance of deduction claimed u/s 80G of the Act- Rs. 1,41,81,521/-

17. The facts as summarized by the Ld. CIT(A) in this regard are reproduced as under:

“6.3 Disallowance of deduction claimed u/s 80G of the Act, 1961- Rs. 1,41,81,521/-

The AO observed from the financial statement that the appellant has incurred expenditure of RS. 2,83,63,043/- toward CSR and its own disallowed the expenditure while computing the total income. Further the appellant has claimed 50% of such expenditure u/s. 80G(donation) to the tune of Rs. 1,41,81,521/-.

The AO further referred the section 80G in which it was clarified the categories in which the donation was to be made and sought the deduction u/s. 80G. The AO further stated that in the case under consideration, the amount has not been paid by the Assessee voluntarily to become eligible for entity specified under Section 80G of the Act. But the same has been paid by the Assessee as a mandatory requirement as per Section 135 of the Companies Act, 2013 to spend certain amount for specified activities as per. The expression “shall ensure” used in Section 135(5) of the Companies Act 2013 clearly implies that there is a mandate to spend 2% of average net profits of the preceding three years on CSR activity. Thus the required-to-spend amount is perceived by the legislature to be mandatory in nature and not voluntary.

The AO further stated that the Assessee could also have very well made payment to an entity not covered by Section 80G or it could have directly incurred the expenditure for the specified purpose, but it chose to spend only in those areas where it could claim deduction u/s 80G of the Act. Therefore, the sum paid by the Assessee cannot be considered as a ‘donation’ for the purpose of Section 80G of the Act as the element of charity is missing in it. Accordingly, the claim of the appellant towards deduction u/s.80G was not accepted and the AO disallowed the same.”

18. Aggrieved with the said order, the assessee filed an appeal before the Ld. CIT(A). The Ld. CIT(A) allowed the appeal of the assessee and the relevant extract of the said order is reproduced as under:

“11. Ground No. 5

Through this ground of appeal, the appellant agitated against the denial of claim of deduction of Rs 1,41,81,521/- u /s. 80G of the Act.

11.1 The appellant has contended that it has incurred an expenditure for CSR and paid an amount of Rs. 2,83,63,043/- and claimed 50% of such expenditure u/s. 80G of the Act as the appellant is satisfying the condition of provision of section 80G of the Act. The appellant also relied upon the decision of Hon’ble ITAT Bangalore in the case of Goldman Sachs Services Pvt Ltd v. JCIT in IT(TP)A No 2355/Bang/2019 for AY 201516 in which it was held that the other contributions made u/s 135(5) of the Companies Act are also eligible for deduction u/s 80G of the Income tax Act subject to assessee satisfying the requisite conditions prescribed for deduction u/s 80G of the Act

11.2 The undersigned has considered the contention of the appellant. There is no dispute that the appellant incurred expenditure of Rs. 2,83,63,043/- against the CSR and also claimed 50% such expenditure u/s. 80G. it is also pertinent to mention here that there is no specific provision in the Act that the expenditure towards CSR cannot be claimed u/s. 80G to the extent as provided in the provision. The appellant incurred expenditure to the entity i.e. Care Today Fund which has certificate of 80G. Therefore, the denial of deduction u/s. 80G by the AO was not warranted. Accordingly the Ground No. 5 raised by the appellant is hereby allowed.”

19. Aggrieved with the said order, the Revenue is in appeal before us on the following ground of appeal:

“3. Whether, on the facts and circumstances of the case and in law the Ld. CIT(A) has erred in deleting the addition of Rs. 1,41,81,521/-on account of disallowance of deduction u/s 80G of the Act.

20. At the time of hearing before us, the Ld. CIT(DR) relied upon the order dated 22.12.2023 of the Co-ordinate Bench of Tribunal in the case of Agilent Technologies (International)P. Ltd. v. ACIT / NFAC, Delhi Delhi–Trib.), where the Tribunal held that CSR expenditure shall not be allowed as business expenditure under section 37(1) of the Act and no deduction u/s 80G will be allowable.

21. On the other hand, the ld. Sr. Counsel for the assessee, while relying upon the order of the Ld. CIT(A) filed a brief synopsis relying upon certain case laws. The said submissions are reproduced as under:

submission

| i. |

|

Reliance is placed on judgments placed at S. No. 6 to 8 of PB II on the proposition that CSR expenditure incurred by assessee are eligible for deduction under section 80G of the Act. |

Judgment to be relied upon

| • |

|

Fluor Daniel India Pvt. Ltd. v. DCIT [ITA No. 3830/Del/2025, dated 26-3-2025] at pages 40 to 51, relevant pages 44 to 49 of PB – II. |

| • |

|

Cheil India (P) Ltd. v. DCIT (Delhi – Trib.) at pages 52 to 56, relevant pages 52 to 53 of PB – II. |

| • |

|

Ericsson India Global Services (P) Ltd. v. ACIT (Delhi – Trib.) at pages 57 to 60, relevant page 57 of Pb – II. |

| • |

|

Interglobe Technology Quotient (P) Ltd. v. ACIT207 ITD 360 (Delhi – Trib.). |

22 We have heard both the parties and perused the material available on record. In this case, the issue is regarding the claim of the assessee for deduction u/s 80G of the Act amounting to Rs. 1,41,81,541/- on CSR expenditure of Rs. 2,8,63,043/-. This issue is covered in favour of the assessee in several decisions as relied upon by the assessee as referred above. For ready reference, the relevant findings of the Co-ordinate Bench in the decision of Cheil India (P.) Ltd. (supra) are reproduced as under:

“5. We have heard both the parties and perused the records. 6. At the time of hearing, Ld. AR for the assessee submitted that the issue in dispute is squarely covered by the following catena of ITAT orders. Hence, he requested to follow the ratio of the following decisions in the instant case and allow the grounds raised in the appeal.

| 1 |

Ratna Sagar Pvt. Ltd. v. ACIT, Central Circle 4, New Delhi |

ITA No. 3256/Del/23 |

| 2 |

Honda Motorcycle & Scooter India Pvt. Ltd. v. ACIT, Circle 1(1), Gurugram |

ITA No. 1523/Del/22 |

| 3 |

Interglobe Technology Quotient Private Limited v. ACIT, Circle 10(1), New Delhi. |

ITA No. 95/Del/24 |

| 4 |

M/s Goldman Sachs Services Pvt. Ltd. v. JCIT, Special Range- 3, Bangalore. |

IT(TP)A No. 2355/ 19ng/2019 |

| 5 |

M/s JMSMining Pvt. Ltd. v. PCIT, Kolkata- 2, Kolkata. |

ITA No. 146/Kol/21 |

| 6 |

Ericsson India Global Services Private Limited v. DCIT, Circle 7(1), New Delhi |

ITA No. 1150/Del/22 |

| 7 |

Optum Global Solutions (India) Private Limited, Hyderabad v. DCIT, Circle 5(1), Hyderabad |

ITA-TP Nos. 145 & /80/Hyd/2O22 |

| 8. |

Societe Generale Securities India (P) Ltd. v. PCIT |

[2024] 204ITD 796 (Mumbai –Trib) |

| 9. |

Power Mech Projects Ltd. v. DCIT |

(Hyderabad Trib.) |

7. Per contra, Ld. DR could not controvert the statement of the Ld. AR that the issue in dispute is squarely covered in favour of the assessee.

8. Upon careful consideration, we note that the Coordinate Bench of the Delhi Tribunal vide its order dated 29.08.2024 passed in ITA No. 2556/Del/2023 (AY 2018-19) in the case of M/s Ratna Sagar Pvt. Ltd. v. ACIT has dealt the similar issue and held as under:-

“5. We have heard the rival contentions and perused the material available on record and also gone through the orders of the authorities below.

5.1 At the time of hearing, Ld. AR for the assessee contended that the issue in dispute is squarely covered by the several case laws of the ITAT. In this regard, he referred to the ITAT decisions dated 28.05.2024 passed in ITA No. 95/Del/2024 (AY 2020-21) in the case of Interglobe Technology Quotient Private Limited; Honda Motorcycle and Scooter India Pvt. Ltd. v. ACIT in ITA No. 1523/Del/2022 (AY 2017-18) dated 22.8.2023; & Ericsson India Global Services (P) Ltd. v. DCIT in ITA No. 1150/Del/2022 (AY 201516) dated 05.03.2024. In view of above, he requested to follow the ratio of the aforesaid Tribunal’s orders and allow the issue in dispute in favour of the assessee raised in the instant appeal.

5.2 Ld. Sr. DR did not controvert the aforesaid proposition made by the Ld. AR, but he supported the orders of the authorities below.

6. Upon careful consideration, we find considerable cogency in the contention of the Ld. AR that identical issue has been dealt by the Coordinate Bench of ITAT, Delhi vide order dated 28.05.2024 passed in ITA No. 95/Del/2024 (AY 2020-21) in the 5 case of Interglobe Technology Quotient Private Limited, wherein the Coordinate Bench has held as under:-

“7. Learned DR has failed to bring forth any decision to the contrary. Thus, we accept the plea of learned counsel on the basis of case law cited, denial of CSR expenditure u/s 37(1) of the Act is not embargo to claim deduction u/s 80G of the Act.

7.1 Further, we like to observe that as a matter of fact as per Section 135 of the Companies Act, 2013 (‘CA 2013), the qualifying Companies as mentioned therein are required to spend certain percentage of profits of last three years on activities pertaining to Corporate Social Responsibility (CSR). The expenditure on CSR, could be by way of expenditure on projects directly undertaken by said companies, such as setting up and running schools, social business projects, etc. Such expenditure would include expenditure otherwise falling for consideration under section 37(1) of the Act. On the other hand, companies, instead of undertaking or participating directly in a project, may choose to give donations to institutions that are engaged in undertaking such projects, which is also a recognized way of compliance of CSR obligation.

7.2 The assessing officer and CIT (A) have relied upon General Circular 14/2021 dated 25.08.2021 issued by MCA and “Explanatory Notes to the provisions of the Finance (No.2) Act, 2014” to hold that donations made as part of CSR expenditure are not allowable as deduction. The foundation of their reasoning being that the donation is voluntary in nature, while CSR expenditures are under statutory obligations.

7.3 As we take notice of the fact that Parliament legislated that CSR expenses would not be eligible for deduction as business expenditure under section 37 of the Act by inserting Explanation 2 to section 37(1) vide the Finance (No.2) Act, 2014 (applicable from the assessment year 2015-16), which provided that any expenditure incurred by an assessee on the activities relating to CSR referred to in section 135 of the CA 2013, shall not be deemed to be an expenditure incurred by an assessee for the purpose of business or profession and shall not be allowed as deduction under section 37(1) of the IT Act. The intent of Parliament in bringing the aforesaid provision is given in the Explanatory Memorandum to the Finance (No.2) Bill, 2014 and is reproduced as under :

“CSR expenditure, being an application of income, is not incurred wholly and exclusively for the purposes of carrying on business, As the application of income is not allowed as deduction for the purposes of computing taxable income of a company, amount spent on CSR cannot be allowed as deduction for .computing the taxable income of the company, Moreover, the objective of CSR is to share burden of the Government in providing social services by companies having net worth/turnover/profit above a threshold. If such expenses are allowed as tax deduction, this would result in subsidizing of around one-third of such expenses by the Government by way of tax expenditure.” (emphasis supplied)

7.4 The aforesaid explanatory memorandum categorically expresses the legislative intent and the rationale of disallowance of CSR expenditure referred to in section 135 of the Companies Act, that such expenditure is application of income and not incurred for the purposes of business. We are of considered view that this in itself justifies the grant of deduction u/s 80G. As CSR 7 expenditure is application of income of the assessee under the Income Tax Act, that means it continues to form part of the Total income of the assessee. Section 80G(1) of the Act provides that in computing the total income of an assessee, there shall be deducted, in accordance with the provisions of this section, such sum paid by the assessee in the previous year as a donation. Further, section 80G(2) lists down the sums on which deduction shall be allowed to the assessee. Section 80G falls in Chapter VIA, which comes into play only after the gross total income has been computed by applying the computation provisions under various heads of income, including the Explanation 2 to section 37(1) of the Act. Thus, there is no correlation between suo-moto disallowance in section 37(1) and claim of deduction under section 80G of the Act. 7.5 As with regard to the reasoning that CSR expenditure are not voluntary but mandatory in nature due to penal consequences, we are of considered view that voluntary nature of donation is by nature of fact that it is not on the basis of any reciprocal promise of donee. The CSR expenditures are also without any reciprocal commitment from beneficiary being philanthropic in nature. The Act permits deduction of donations as per Section 80G of the Act, even though, assessee is not gaining any benefit out of any reciprocity from donee. Similar is the case of CSR expenditure. Thus, the reasoning of learned Tax Authority, the CSR expenditure is mandatory, does not justify disallowance of these expenditures u/s 80G, if other conditions of section 80G are fulfilled. There is no allegation of Revenue 8 that other conditions of Section 80G are not fulfilled. We, thus sustain the ground.”

7. After perusing the aforesaid findings, we find that the facts of the present case are identical to that of the aforesaid case of other assessee, hence, the issue in dispute involved in the instant appeal is squarely covered in favour of the assessee. Therefore, respectfully following binding precedent (supra), we delete the addition sustained by the Ld. CIT(A) and accordingly, allow the ground of appeal raised by the Assessee.

8. In the result, appeal of the assessee is allowed.”

7. Respectfully following the precedent as aforesaid, we set aside the orders of the authorities below and accordingly decide the issue in dispute in favour of the assessee.

8. In the result, the Assessee’s appeal is allowed.”

Respectfully following the above decision, we are inclined to allow Grounds No.2 to 5 raised by the assessee.”

22.1 Regarding the reliance by the Ld. CIT(DR) upon the order of the Co-ordinate Bench of the Tribunal in the case of

Agilent Technologies (International)P. Ltd. (

supra), which held that such deduction u/s 80G of the Act was not permissible in the case of CSR expenditure, we are of the considered view that in view of the decision of the Apex Court in the case of The Commissioner of Income-Tax, West Bengal-1 v. M/S. Vegetables Products Ltd reported in

88 ITR 192, wherein it was observed that, if two reasonable constructions of a taxing provision are possible then the construction which favours the assessee must be adopted, the findings of the Ld. CIT(A) is acceptable. Accordingly, Ground no. 3 of the appeal is dismissed.

23. In the result, appeal of the Revenue is dismissed.

24. Now, we take up the assessee’s appeal in ITA No.- 1449/Del/2024 for A.Y. 2018-19.

25. The facts as summarized by the Ld. CIT(A) regarding this addition are reproduced as under:

” 6.1 Disallowance of depreciation of Rs. 1,52,42,500/- on intangibles of Rs. 6,09,70,000/-. The AO observed that the appellant company during the year under consideration, acquired the “Business constituting operations of Digital business” (Digital Business) from Living Media India Limited (“Holding Company”, “LMIL”) as a going concern on slump sale basis by way of execution of Business Transfer Agreement w.e.f January 1, 2018 (i.e. the acquisition date). Further, out of total consideration of Rs. 200,000,000 paid to LMIL for acquisition of Digital Business, an amount of Rs. 6,09,70,000/- has been capitalized under intangible assets. The company also claimed depreciation on the same amount @ 25% under intangible assets. The AO further observed that the said claim of the depreciation on intangibles that has neither been acquired nor existed in the books of the merged entities is not as , per the , provisions of the Act. It was also observed by the O that the intangibles in the case of the assessee has arisen out of business acquisition on account of difference between the value of assets of that company and the consideration paid by assessee-company. As such the same does not arise out of transfer of any tangible assets eligible for claim of depreciation. The AO further observed that the assessee-company has acquired the said intangibles from its holding company and the valuation of the merged companies have been inflated by the assessee company creating an artificially inflated goodwill and claimed deprecation thereon to reduce the taxable , profits over the years.

Thus, The AO found that actual cost of the block of asset (intangible block in this case) in the hand of the succeeding companies would be written down value in the immediate preceding year in the case of predecessor company. Since, the written down value of the intangible block of asset was unascertained in the books of the respective , predecessor companies, the actual cost would remain zero in the hand of respective successor companies as well. Hence, the above provisions of law make it clear that the cost of intangible assets in the hand of successor companies shall be zero for the purpose of depreciation.

The AO referred the proviso 6 of Section 32(1) and accordingly to that in respect of both the tangible as well as intangible assets the depreciation shall not exceed in any Previous Year the deduction calculated at the prescribed rates as if the succession or the amalgamation or the demerger, as the case may be, had not taken place, and such deduction shall be apportioned between the predecessor and the successor, or the amalgamating company and the amalgamated company, or the demerged company and the resulting company, as the case may be, in the ratio of the number of days for which the assets were used by them. It is, therefore, evident that in the case of succession, amalgamation, merger, demerger depreciation can be claimed by the succeeding concerns only in respect of those assets on which the depreciation was being allowed to the predecessor concern. In other words, if any assets were not appearing in the books of the previous concerns, which has been succeeded by another concern, the succeeding concern would not be eligible for claiming any depreciation on any new asset which is claimed to have been acquired as a result of succession of business. The AO further stated that Since in the hands of the predecessor company, the cost of acquisition and consequent depreciation was unascertained, there cannot be depreciation in the hand of the successor company. AO further concluded the issue stating that the assessee failed to provide specific value of the intangibles for which the extra consideration was paid which was claimed to have been paid. It was necessary for the assessee to demonstrate and prove that the intangibles acquired as business or commercial rights, in the facts and circumstances of this case, was akin to any of the intangible assets being know-how, patents, copyrights, trademarks, licences, and franchises. Further, the intangibles recorded by the assessee as business or commercial rights on account of excess of payment over net assets taken over as a result of acquisition of Digital Business from its holding company as slump sale on going concern basis is not eligible for claiming depreciation. And therefore, the AO disallowed the depreciation of Rs. 1,52,42,500/- on the said business or commercial rights under intangible assets of Rs.6,09,70,000/-.

(emphasis supplied by us)

26. Aggrieved with the said order of the AO, regarding the above addition, the assessee filed an appeal before the Ld. CIT(A), who dismissed the appeal of the assessee on this issue. The relevant extract of the said order is reproduced as under:

” 8. Ground No. 2

Through this ground, the appellant agitated against the disallowance of depreciation on intangible assets to the tune of Rs.1,52,42,500/

8.1 The appellant through its submission, stated as follows: The Assessee Company acquired the “Business constituting operations of Digital business” (Digital Business) from Living Media India Limited (LMIL) as a going concern on slump sale basis by way of execution of Business Transfer Agreement w.e.f January 1, 2018. The total consideration for purchase of digital business was Rs 2000 Lacs and out of Rs 2000 Lacs an amount of Rs 609.70 Lacs was pertaining to intangible workmen force. The details of assets and liabilities acquired in pursuance of slump sales are as under.

| Sr. No. |

Particulars |

Amount (in Lacs) |

| 1 |

Property, plant and equipment |

133.11 |

| 2 |

Intangible under development |

T1.32 |

| 3 |

Non-current assets |

2.16 |

| 4 |

Trade Receivables |

1729.77 |

| 5 |

Loans |

11.15 |

| 6 |

Other cun ent assets |

211.36 |

| 7 |

Intangible assets |

609.70 |

| 8 |

Employee benefit obligation |

(202.95) |

| 9 |

Trade Payable |

(511.8S) |

| 10 |

Employee benefit payable |

(105.44) |

| 11 |

Capital creditors |

(19.39) |

| 12 |

Advance from customers |

(14.30) |

| 13 |

Statutory dues payable |

(16.55) |

|

Total |

2000.00 |

The intangible workmen force of Rs 6.09 Cr has been valued by an independent Chartered Accountant [PWC]. Based on the valuation report given by PWC, the said workmen force has been capitalized under Intangible assets and claimed eprecation as per section 32(1) of the IT Act. Year wise depreciation claimed on goodwill is as under:

| Particulars |

Amount (Rs) |

Remarks |

| Intangible workforce acquired |

6.09.70.000 – |

Capitalized in books duiing the AY 2018-19 |

| Depreciation claimed in AY 2018-19 |

1.52.42.500- |

|

| WDV as on 31.03.2018 |

4.5″ 27.500 – |

|

As the assessee company has not acquired any goodwill as a result of amalgamation / merger / demerger but has acquired under slump sale, hence all the provisions / case laws, referred to in the Assessment Order for disallowance of depreciation, are not applicable to the assessee company.

8.2 The undersigned has perused the submission made by the appellant. There is no dispute on the acquisition of “Business constituting operations of Digital business” (Digital Business) from Living Media India Limited (LMIL) as a going concern on slump sale basis by way of execution of Business Transfer Agreement w.e.f January 1, 2018. The question arises whether the depreciation can be allowed on acquisition of good will by making the payment over and above the amount of total asset. The appellant has contended that the same has been acquired by the agreement of slump sale not by demerger or amalgamation and hence the rule related to the amalgamation and demerger is not applicable to its case.

8.3 The contention of the appellant has been considered. However, the , point is to clarified that the claim of depreciation is regulated by the provision under section 32 of the Act. Accordingly to the Proviso 5 & Proviso 6 is squarely applicable in the instant case. First of all, when the predecessor company was not claiming the depreciation on such goodwill, how the new company who has acquired the same can claim the depreciation even it has paid a sum for the same over and above. Therefore, the undersigned is in agreement with the view of the AO in disallowing the depreciation claim to the tune of Rs. 1,52,42,500/-. Thus, the disallowance made by the AO is hereby confirmed. Accordingly, the Ground No. 2 is hereby dismissed.

(emphasis supplied by us)

27. Aggrieved with the said order, the assessee is in appeal before us on the following grounds of appeal:

“1. That the learned Commissioner (Appeals) has grossly erred in law and on facts in confirmed a disallowance of a sum of Rs. 1,52,42,500/- towards depreciation on intangibles/ goodwill which disallowance is unjustified and untenable in law and thus, should be deleted as such.

2. That in doing so, the learned Commissioner (Appeals) has failed to appreciate the fact that the depreciation so claimed on goodwill was with regards to purchase under slump sale basis, which is eligible for depreciation and the same should have been allowed, as such.

3. That in confirming the aforesaid disallowance, the learned Commissioner (Appeals) has relied on the provision of section 32 which was totally inapplicable to the facts of assessee – appellant and has also based the findings on mere suspicion and surmises which are contrary to material available on record and as such, the disallowance so made needs to be deleted.

4. That the appellant reserves the right to add alter amends delete any all grounds of appeal either before or at the time of the hearing of the appeal.”

28. During the hearing before us, the Ld. Counsel for the assessee filed a brief synopsis and relied upon certain judgements in a tabular chart, which is reproduced as under:

Arguments in brief

| “i. |

|

Both learned AO and CIT (A) have failed to appreciate the fact that assessee has not claimed any depreciation on goodwill, rather assessee has acquired intangible asset in the shape of workforce, which is part of business transfer agreement dated 01.01.2018 and also valued separately by valuer vide report dated 09.11.2017. Furthermore, in acquisition of digital business workforces which are heart and soul of business like content creators are major assets and that is why they have been valued separately. |

| ii. |

|

Further, in the assessment of Living Media India Ltd. for AY 2018-19, department had accepted the sale consideration received of a sum of Rs. 20 crores (kindly see pages 354 to 355 and 356 to 363 of PB-I), as such, Revenue cannot blow hot and cold, as accepting the sale consideration in hands of LMIL and disputing the acquisition price in the hands of assessee company. |

| iii. |

|

No enquiry learned AO either from LMIL or the valuer whatsoever, has been made by such, disallowance of suspicion and i.e. PWC, as depreciation merely on surmises is not justified. |

| iv. |

|

Even otherwise, goodwill is a depreciable asset whether acquired on amalgamation or slump sale provided it is backed by proper valuations. Reliance is placed on case laws enclosed at S. No. 11 to 13 of PB-II. |

Judgments to be relied upon:

| • |

|

“Areva T&D India Ltd. v. DCIT (Delhi HC) reported in 345 ITR 421 at pages 1 to 3 of PB III, relevant pages 2 and 3 (held portion). |

| • |

|

Brembo Brake India (P) Ltd. v. DCIT (ITAT Pune) reported in at pages 4 to 12, relevant pages 4, 5 and 11 of PB – III. |

| • |

|

SKS Micro Finance Ltd. v. DCIT (ITAT Hyderabad) at pages 13 to 24, relevant pages 13 to 14 of PB – III. |

| • |

|

No. Vodafone India Services Pvt. Ltd. v. DCIT (ITAT Ahmedabad) in ITA 2241/Ahd/2018 at pages 82 to 101, relevant pages 88 to 96 ofPB – II. |

| • |

|

Thermo Fisher Scientific India (P) Ltd. v. DCIT (ITAT Mumbai) reported in at pages 102 to 115, relevant pages 112 to 112 para’s 5.18 to 5.26 of PB- II. |

| • |

|

CIT v. Smifs Securities Ltd. (SC) reported in 348 ITR 302 at pages 116 to 117 of PB – II.” |

28.1 The Ld. AR further submitted that during the course of assessment proceedings, the assessee had intimated the AO vide letter dated 12.04.2021 (placed at page no. 120-121 of the P.B.) informing that the assessee company acquired the ‘Business constituting operation of Digital business (Digital Business) from Living Media India Ltd. as a going concern on slump sales basis by way of Business Transfer Agreement w.e.f. January 1, 2018 for which the total consideration for the purchase of the Digital Business was Rs. 2000 lacs. In the said letter, while giving the break-up of the said 2,000 lacs and amount of Rs. 609.70 lacs was shown under the head ‘Intangible assets’ which the Ld. AR submitted constituted the work force of the Living Media India P. ltd. Further, the Ld. AR submitted that the Business Transfer Agreement was placed at page no. 123-141 of the P.B., wherein the details of the agreement has been mentioned and in para 4 on page 127 of the P.B., it is stated that all the employees in employment of the seller shall stand transferred to the purchasers on the same terms and condition of employment as are offered by the seller on continuity in service basis to the purchaser which the assessee in this case. In view of these facts, the Ld. AR submitted that the assessee had rightly claimed the depreciation of Rs. 1,52,42,500/- on the said ‘Intangible assets’ amounting to Rs. 6,09,70,000/

29. On the other hand, the Ld. CIT(DR), relied upon the order of the authorities below. The Ld. CIT(DR) also submitted that the AO had rightly observed that the assessee-company had acquired the said intangibles from its holding company and the valuation of the ‘Intangible assets’ was inflated by the assessee company creating an artificially inflated goodwill and claimed deprecation thereon to reduce the taxable profits over the years. Further, the Ld. CIT(DR) also stated that since, the written down value of the intangible block of asset was unascertained in the books of the respective predecessor companies, the actual cost would remain zero in the hand of respective successor companies as well and the assessee would not be entitled for the depreciation as claimed by it. Further, the Ld. CIT(DR) also submitted that as per the provisions of section 32(1)(ii) of the Act, it was necessary for the assessee to demonstrate and prove that the intangibles acquired as business or commercial rights, in the facts and circumstances of this case, was akin to any of the intangible assets being knowhow, patents, copyrights, trademarks, licences, and franchises. Further, the Ld. CIT(DR) submitted that the intangibles recorded by the assessee as business or commercial rights on account of excess of payment over net assets taken over as a result of acquisition of Digital Business from its holding company as slump sale on going concern basis is not eligible for claiming depreciation. In this regard, the Ld. CIT(DR) relied upon the order dated 17.02.2026 of the Tribunal Pune Bench in the case of Aptara Technologies Private Ltd. v. DCIT (Pune – Trib.)/ ITA No. 63/pun/2020, in support of his above submissions. In this regard, the relevant paras relied upon by the Ld. CIT(DR) are reproduced as under:

“9. Ld. Senior Counsel for the assessee Mr. Percy Pardiwalla representing the assessee first made reference to the following written submissions which have been filed before ld. CIT(A) and before this Tribunal:

“A. Facts of the Case

1. The Appellant is a private limited company engaged in the business of providing IT enabled conversion services, including e-learning solutions, imaging, graphic arts and other related services. It is a wholly owned subsidiary of Aptara Inc., a company incorporated in USA. The Appellant filed its return of income for Assessment Year 2015-16 on 25 November 2015, declaring total income of Rs. 1,66,65,240. The computation of income is enclosed as Annexure-1 of Paper book-1.

2. The return was selected for scrutiny under CASS and a notice u/s 143(2) of the Income-tax Act, 1961 (the Act) was issued to the assessee. Detailed questionnaires were issued during the course of assessment, which were duly responded to by the Appellant. Upon considering the submissions made by the Appellant, an order dated 26 December 2017 was passed u/s 143(3) of the Act, making the following adjustments to the income returned by the Appellant,

(a) In relation to the tax on income of the Appellant, disallowing the Appellants claim for depreciation on goodwill,

(b) In relation to shares bought back by the Appellant, taxing the consideration paid on buyback u/s 115QA of the Act

B. Dis-allowance of depreciation on goodwill

B. 1 Facts relevant to dis-allowance of depreciation

3. The said goodwill arose due to the amalgamation of Maximize Learning Private Limited (MLPL) with the Appellant. MLPL was a wholly owned subsidiary of Aptara Inc., USA. While the Appellant was engaged in the business of publishing services, which entails digitisation of content for third parties, MLPL was engaged in providing e-learning services, rendering services solely to Aptara Inc.

………..

25. Further, the Appellant also took on its payrolls the employees of MLPL, who were highly skilled in the field of e-learning. MLPL had cleared a strong pool of talented free-lancing professionals who were in a position to provide quality development services at a very competitive , price. Development of e-learning portal required the following expertise, and a team of professional

| (a) |

|

Designing & Developing Content experiences & providing solutions to support the acquisition of new knowledge & skill |

| (b) |

|

Graphic Art & Designing, assembling images, Typography or Motion Graphics |

| (c) |

|

Translation, Localization & Voice over |

| (d) |

|

Applying principles & practices of software Quality Assurance. |

| Production of e-learning Modules |

| (g) |

|

Process breaking in steps to improve Quality & time Deliver |

| (h) |

|

Programmer specialized in development of web applications using client server model, Typically HTML, CSS, Java, PHP, Dotnet, Etc |

| (j) |

|

Web graphic Design, Authoring, Standardizing Code & search engine optimization. |

…………

29. Shortly put, the Appellant gained significantly from the amalgamation, in the form of highly skilled employees, increased talent pool, significantly increased revenue, increased client and customer base, additional skills imparted to existing employees, standard templates for providing basic services, etc. apart from the general synergies of amalgamation such as reduced costs, simpler management structure, etc. The observations of the Ld. AO are therefore completely devoid of merit.

…………..xxxx……………

14. We have heard the rival submissions and perused the records placed us. We have carefully gone through the decisions referred and relied on by both the sides. Following two issues have been raised before us (1) Generation of Goodwill of Rs.5,97,20,000/- and claim of depreciation on such Goodwill at Rs.1,49,30,000/- arising out of the amalgamation between the assessee (Transferee company) with MLPL is justified and in accordance with law and.

15. At the cost of repetition of the facts, we note that the assessee is a 100%b subsidiary of Aptara Inc. USA. There is another company namely Maximise Learning Pvt. Ltd. (MLPL) which is also 100% subsidiary of Aptara Inc. USA. During the year under consideration, MLPL (Transferor company) has been amalgamated with the assessee, i.e. ATPL (Transferee company) and after the sanction of the amalgamation arrangement scheme by the Hon’ble Bombay High Court vide order dated 19.09.2014 amalgamation has completed. Now as per the merger note exhibiting the value of Assets and Liabilities of MLPL taken over by ATPL at its book value, i.e. the assessee company, sum of Rs.6,07,20,000/- has been shown to be due to the shareholders of MLPL, i.e. the purchase consideration payable over and above the net assets book value of MLPL. In this merger note, on the Asset side, a new Intangible asset namely Goodwill has been stated at an amount of Rs.5,97,20,000/-. Now on the amalgamation of the books MLPL with ATPL the total amount due to the shareholders of MLPL is the face value of the share capital, i.e. Rs. 10,00 lakh and the value of Goodwill at Rs,5,97,20,000/-. In lieu thereof, ATPL has not passed on any consideration through banking channel but has merely issued 60.72 Equity shares in lieu of 1 Equity share held by the shareholders in MLPL. The assessee has booked the Goodwill for the year under consideration in depreciation thereon @25% amounting to Rs. 1,49,30,000/-. at Rs.5,97,20,000/- and has also claimed Ld. Assessing Officer on going through the chronology of facts came to the conclusion that the assesssee has adopted a colourable device by inflating the net assets of MLPL by way of inclusion of Goodwill even when no such asset existed in the books of the Transferor company-MLPL.

18. Now on carefully considering the finding of ld.CIT(A), so far as the first aspect about the creation of Goodwill is concerned, we find that after the transactions taking place between unrelated parties and that running business is taken over or amalgamated, then certainly the assets are valued on the date of amalgamation and in this process sometimes the consideration to be paid is much more than the net assets and such deficit can either be reduced from Capital Reserve of the Transferee company as provided under Accounting Standard-14 but if the scheme of amalgamation provides and there being genuine transaction, then Hon’ble Courts have consistently held that such deficit is to be considered as Goodwill and eligible for depreciation. So far as this ratio of creation of Goodwill in genuine transaction of Amalgamation is concerned, we truly concur and in support there are , plethora of decisions out of which some of them have also been referred and relied on by the ld. Counsel for the assessee which are as follows:

1. Disney Broadcasting (India) (P) Ltd. v. PCIT (Mumbai-Trib.)

2. Dow Chemical International (P) Ltd. v. DCIT (Mumbai-Trib.)

3. Padmini Products (P) Ltd. v. DCIT (Karnataka)

4. Altimetrik India (P) Ltd. v. DCIT (Bangalore-Trib.)

5. Geodis Overseas Pvt. Ltd. v. DCIT ITA No. 2305/Del/2015 dated 18.05.2020

19. However, in the instant case, the facts are different and ppeculiar. It is not the case of some independent transaction of amalgamation a company ‘A’ with Company ‘B’ for taking over the business but it is a case where one Holding Company is having two subsidiaries companies and two subsidiary companies are merged in the process of amalgamation but the owner remains the same. In the process of amalgamation, the 60.72 Equity shares have been issued by the Transferee company, i.e. the assessee company -ATPL to Transferor company-MLPL and after reducing the face value of Equity shares held by shareholder of MLPL, the excess amount of Rs.5,97,20,000/- is treated as Goodwill. It is clearly visible from the merger note that only against the creation of Goodwill 60.72 Equity shares in lieu of 1 Equity share of MLPL has been issued. It is a case where the owner himself is claiming that one of its subsidiary company has purchased the business on of its another subsidiary company at a higher amount and such higher amount is basically Goodwill and there being no banking transaction except the issue of fresh Equity shares in lieu of the Goodwill. It apparently seems to be an arrangement made at the instance of the Holding Company between its two subsidiary companies. Genuineness of the transaction of amalgamation between independent/unrelated companies is missing in the instant case.

……..

21. In light of the above decision as well as the facts placed before this Tribunal including the observation of ld.CIT(A), we note that prior to amalgamation ATPL earned Revenue of Rs.2.23 crore whereas the Revenue of MLPL was Rs.1.97 crore which shows that turnover of ATPL is higher than MLPL. It is also observed that 100% of the sales of MLPL were effected majorly to the Holding Company Aptara Inc. USA where the sales ofATPL are to various customers in India. Interestingly, no sales have been effected to its related parties including the Holding Company by the assessee company, i.e. ATPL. Also post amalgamation, no sales have been effected to the Holding Company which indicates that the existing business of the subsidiary company prior to amalgamation has been discontinued post amalgamation and only the facilities or the assets appearing in the balance sheet prior to amalgamation as on 31.03.2014 has been transferred to the Transferee company ATPL. These facts again support the finding of ld.CIT(A) as well as the observation of ld. Assessing Officer that this is a mere colourable transaction and in the garb of inflating the value of assets and creation of Goodwill, assessee has intended to claim depreciation for the year under consideration and to be claimed in the subsequent years also. It is also an admitted fact that if new assets are added to the present set of assets on a running business then certainly some sales ought to increase but due to such amalgamation neither any new business has been added nor the profitability has increased much more than the situation prior to amalgamation as appearing from the records before us. We therefore are of the considered view that the creation of alleged Goodwill is merely a colourable transaction carried out between the Holding Company and the subsidiary company which is to create an Intangible asset, inflate the value of Equity shares of the Transferee company and to further evade tax by claiming depreciation on such fictitious asset created through such arrangement of transaction between related p parties. We therefore hold that claim of creation of Goodwill of Rs.5,97,20,000/- is only an Artificial creation and is classic case of lifting the corporate wheel as rightly observed by the ld. CIT(A). Therefore, in our considered view, no Intangible asset in the form of Goodwill is created at Rs.5,97,20,000/-. Further, since no Intangible asset has been created in the of amalgamation, depreciation claimed process Rs. 1,49,30,000/- also deserves to be disallowed. Ground No. 1 raised by the assessee is dismissed. “

(emphasis supplied by us)

30. In rejoinder, the Ld. Counsel for the assessee submitted that the decision of the Pune Bench was distinguishable on facts as it was a case of amalgamation whereas in the case of the assessee it was a case of slump sale. It was further submitted that in the case of the seller the slump sale at Rs. 20 crores have been accepted by the AO vide order u/s 143(3) of the Act dated 18.03.2021 passed in the case of Living Media India (P) Ltd. for A.Y. 2018-19, which was placed at 356-366 of the P.B. Further, the Ld. AR also submitted that the valuation of the ‘Intangible assets’ valued at Rs. 609.70 lacs were done by Price Waterhouse & Co. LLP, Chartered Accountant vide final report dated November 09, 2017, (placed at page no. 199-214 of the P.B.) in which the cost of Rs. 609.70 lacs have been worked out as page no. 211 of the P.B. which has not been disturbed by the AO. Therefore, the Ld. Counsel for the assessee submitted that the decision relied upon by the Ld. CIT(DR) will not be applicable in the case of the assessee.

31. We have heard both the parties and perused the material available on record. In this case, the assessee company acquired the ‘Business constituting operation of Digital business (Digital Business) from Living Media India Ltd. as a going concern on slump sales basis by way of Business Transfer Agreement w.e.f. January 1, 2018 for which the total consideration for the purchase of the Digital Business was Rs. 2000 lacs. The break-up of the said 2,000 lacs and amount of Rs. 609.70 lacs was shown under the head ‘Intangible assets’ which the Ld. AR submitted constituted the work force of the Living Media India P. Ltd. Further, as per the details of the Business Transfer Agreement dated 01.01.2018 all the employees in employment of the seller shall stand transferred to the purchasers on the same terms and condition of employment as are offered by the seller on continuity in service basis to the purchaser which the assessee in this case. Even though, the AO states that the value of the said ‘Intangible assets’ was inflated by the assessee company to claim higher depreciation but the AO did not reject the valuation report given by PWC, by giving any adverse tangible finding. Further, the reliance by the AO on the sixth proviso to section 32(1) of the Act will not be applicable in the present case of the assessee as it is a case of slump sale and not a case of amalgamation to which the said proviso applies. Further, the case laws relied upon by the Ld. CIT(DR) is distinguishable in the facts of the present case in as much as the in case law relied upon by the Ld. CIT(DR), there was a specific finding recorded by the Tribunal in para no. 21 of the order that it was a not a genuine transaction for the creation of the ‘Goodwill’ valued at Rs. 5,97,20,000/- in the cited case, whereas no such finding with any supporting facts has been established by the AO. Further, in this regard, the submission of the assessee that the slump sale value of Rs. 2000 lacs in the case of the seller i.e. Living Media India P. Ltd. having been accepted the AO vide order u/s 143(3) of the Act dated 18.03.2021 passed in the case of Living Media India (P) Ltd. for A.Y. 2018-19 supports the case of the assessee.

31.1 Further, the contention of the Ld. CIT(DR) that as per the provisions of section 32(1)(ii) of the Act, it was necessary for the assessee to demonstrate and prove that the intangibles acquired as business or commercial rights, in the facts and circumstances of this case should be akin to any of the intangible assets being know-how, patents, copyrights, trademarks, licences, and franchises to be eligible for the claim of depreciation under the head ‘Intangible assets’ has been carefully considered but not found to be acceptable. In this regard, on similar facts the Hon’ble High Court of Delhi in the case of Areva T & D India Ltd. v. DCIT 345 ITR 421(Delhi) held that on a perusal of the meaning of the categories of specific intangible assets referred in Section 32(1)(ii) of the Act preceding the term “business or commercial rights of similar nature”, it is seen that the aforesaid intangible assets are not of the same kind and are clearly distinct from one another. It was further held that the fact that after the specified intangible assets the words “business or commercial rights of similar nature” have been additionally used, clearly demonstrates that the Legislature did not intend to provide for depreciation only in respect of specified intangible assets but also to other categories of intangible assets, which were neither feasible nor possible to exhaustively enumerate. The Hon’ble Court held that in the circumstances, the nature of “business or commercial rights” cannot be restricted to only the aforesaid six categories of assets, viz., knowhow, patents, trademarks, copyrights, licenses or franchises. In this regard, the relevant findings of the Hon’ble Court in paras no. 12 , 13 and 14 of the order are reproduced as under:

“12. In the present case, it is seen that the assessee vide slump sale agreement dated 30th June, 2004, acquired, as a going concern, the transmission and distribution business of the transferor Company w.e.f. 1 st April, 2004. As a result thereof, the running business of transmission and distribution was acquired by the transferee lock, stock and barrel minus the trademark of the transferor which was retained by the transferor, for lump sum consideration of Rs.44.7 Crores. It is further seen that the book value of the net tangible assets (assets minus liabilities) acquired was recorded in the balance sheet of the transferor as on the date of transfer as Rs.28.11 Crores. The said assets and liabilities were recorded in the books of transferee at the same value as appeared in the books of the transferor. The balance payment of Rs.16,58,76,000/- over and above the book value of net tangible assets, was allocated by the transferee towards acquisition of bundle of business and commercial rights, clearly defined in the slump sale agreement, compendiously termed as “goodwill” in the books of accounts, which comprised, inter alia, the following:- (i) Business claims, (ii) Business information, (iii) Business records, (iv) Contracts, (v) Skilled employees, (vi) knowhow. It is also observed that the AO accepted the allocation of the slump consideration of Rs.44.7 Crores paid by the transferee, between tangible assets and intangible assets (described as goodwill) acquired as part of the running business. The AO, however, held that depreciation in terms of Section 32(1)(ii) of the Act was not, in law, available on goodwill. The CIT(A) and the ITAT approved the reasoning of the AO thereby holding disallowance of depreciation on the amount described as goodwill. It was thus argued on behalf of the assessee Company that Section 32(1)(ii) would mean rights similar in nature as the specified assets, viz., intangible, valuable and capable of being transferred and that such assets were eligible for depreciation. On behalf of the respondent it was argued that applying the doctrine of noscitur sociis the expression “any other business or commercial rights of similar nature” used in Explanation 3(b) to Section 32(1) has to take colour from the preceding words “knowhow, patents, copyrights, trademarks, licenses, franchises”. It was urged that the Supreme Court had clearly held in Techno Shares and Stocks Ltd.(supra) that “Our judgment should not be understood to mean that every business or commercial right would constitute a “licence” or a “franchise” in terms of section 32(1)(ii) of 1961 Act.