ORDER

Dr. Dipak P. Ripote, Accountant Member.- This is an appeal filed by the Revenue against the order of ld.Commissioner of Income Tax(Appeal)[NFAC] passed under section 250 of the Income Tax Act, 1961 for A.Y.2017-18 dated 22.09.2025. The Revenue has raised the following grounds of appeal :

| “1. |

|

Whether on the facts and in the circumstances of the case, the fact that the Faceless Assessing Officer followed the procedure as per provisions 144C rws 144B of the Act? |

| 2. |

|

Whether on the facts and in the circumstances of the case, the CTT(A) is justified in Ignoring the letter regarding withdrawal of first draft assessment order (DAO 1) and issued revised DAO 2 dated 09.04.2021 followed by show-cause notice dated: 11.05.2021 the assessee? |

| 3. |

|

Whether in the facts and in the circumstances of the case, the LA CIT(A) is justified in allowing the Assessee’s claim of Advertisement and Sales Promotion Expenses incurred by the Assessee of Rs.5,18,65,26,221 and disallowed by the Assessing Officer, the expenditures being not wholly and exclusively for the purpose of business of the |

| 4. |

|

Whether on the facts and in the circumstances of the case, the Ld. CIT(A) is justified in not appreciating that the Assessing Officer had disallowed the Advertisement and Sales Promotion Expenses on the ground that such expenses benefited the business of the bottlers of the beverages and the assessee also failed to establish that the economic cost of advertisement was recovered from the bottlers? |

| 5. |

|

Whether on the facts and in the circumstances of the case, the Ld. CTT(A) is justified in allowing the bottlers were doing advertisement of their product and the assessee was doing reimbursement without entering into any agreement with the bottlers? |

| 6. |

|

Whether on the facts and in the circumstances of the case, the CIT(A) is justified is allowing the assessee’s claim of Marketing support charges and reclasificmom of marketing an inhere and discount of Rs. 3,10,00,13,750/-disallowed by the Assessing Officer u/s 37 of the Income Tax Act, 1961 the expenditure being not wholly and exclusively for the purpose of business of |

| 7. |

|

Whether in the facts and in the counts of the case, the L. CITIA) is justified in law in not appreciating the true nature of the arrangement between the assessee company and the brand owners whereby the assessee was saddled with such marketing expenses which are in fact and for all intent liability of the foreign company owning the brands and the trademarks? |

| 8. |

|

Whether on the facts and in the circumstances of the case, the Ld. CIT(A) is justified in allowing the Assessee’s claim of service charges incurred by the assessee of Rs. 11,11,54,092/-and disallowed by the Assessing Officer? |

| 9. |

|

Whether on the facts and in the circumstances of the case, the Ld. CIT(A) is justified in not appreciating that the Assessing Officer had disallowed the service charges on the ground that such service charges benefited either the bottlers of the beverages or the owners of the brand and trademarks and thus such expenses do not have direct nexus with the business operation of the assessee company? |

| 10. |

|

Whether on the facts and in the circumstances of the case, the Ld. CIT(A) is justified in not considering the fact that the assessee has not discharged its onus to prove that the service charges were wholly and exclusively incurred for the purpose of the assessee’s business? |

| 11. |

|

Whether on the facts and in the circumstances of the case, the Ld. CIT(A) is justified in allowing depreciation on coolers without appreciating the fact that one of the conditions mentioned u/s 32 of the Income-tax Act, 1961, to claim depreciation as an eligible expense viz. asset should be used for business/profession of the assessee is not fulfilled, since the coolers were used for the purpose of business activities of the bottlers and assessee’s business did not include bottling of concentrates? |

Grounds related to the TP Issues:

| 12. |

|

Whether, on the facts and circumstances of the case, the Ld. CIT(A) is justified in holding that the expenditure incurred by the assessee towards Advertisement, Marketing and Promotion (AMP) activities does not constitute an international transaction within the meaning of Section 92B of the Income-tax Act, 1961 thereby wrongly deleting the transfer pricing adjustment proposed by the TPO without appreciating the fact that the same is leading to brand building of intangibles owned by AE and hence the same is reimbursable expenses qualifying as an international transaction u/s 92B of the Income Tax Act. |

| 13. |

|

Whether on the facts and circumstances of the case, the Ld. CIT(A) was correct in allowing the assessee not to benchmark AMP as an international transaction when the requirement of law is that arm’s length price of every international transaction has to be determined. |

| 14. |

|

Whether in the facts and circumstances of the case, the Ld. CIT(A) is justified by ignoring the well-established doctrine of ‘substance over form’ (applied by the Courts in numerous judicial decisions) indicating that transfer pricing regulations are to be applied keeping in mind the overall scheme of the taxpayer’s business arrangement. The learned CIT(A) failed to appreciate that the AMP functions undertaken by the assessee resulted in creation and enhancement of marketing intangibles owned by the AE, thereby warranting arm’s-length compensation. |

| 15. |

|

Whether in the facts and circumstances of the case, the learned CIT(A) erred in deleting the AMP adjustment without considering that no independent comparable data or third-party evidence was provided by the assessee to demonstrate that AMP was for its own business purposes only? |

| 16. |

|

Whether in the facts and circumstances of the cases, the learned CIT(A) erred in deleting the transfer pricing adjustment by disregarding the comparability analysis undertaken by the TPO, and in accepting the assessee’s comparables which were brand-owning and functionally dissimilar companies, thereby failing to adhere to the principles of comparability under Rule 10B(2)(a) and (b); and in ignoring the TPO’s finding that independent comparable manufacturers with materially lower AMP-to-sales ratios performed comparable DEMPE functions, demonstrating that the assessee had incurred nonroutine brand promotion expenditure benefiting its Associated Enterprise, thus rendering the order contrary to Rule 10B(2) and 10B(3) of the Income-tax Rules, 1962. |

| 17. |

|

The appellant craves to add, amend, alter or delete the above grounds of appeal during the course of appellate proceedings before the Hon’ble Tribunal.” |

Findings & Analysis :

2. We have heard both the parties and perused the records.

2.1 Ld.AR has filed an elaborate paper book. Ld.AR submitted that the issue of Disallownace of Advertisement and Sales Promotion expenses including Market Support expenses on which additions has been made are covered in favour of the assessee by ITAT orders in Assessee’s own case. Ld.AR invited our attention to ITAT orders for AY 1997-98,98-99 to 2004-05 which are part of the Paper book.

2.2 Ld.AR also submitted that issue of services charges is decided by ITAT in earlier years in favour of Assesse for AY 1997-98,9899, 2000-01 to 2004-05.

2.3 Ld.AR also submitted that Issue of Depreciation on coolers is alos covered in favour of Assessee by ITAT orders in assessee’s own case.

2.4 Ld.AR submitted that AMP adjustments made by TPO has been decided by ITAT for earlier years in favour of the assessee.

3. Ld.DR has accepted that issues mentioned have been decided by ITAT in assessee’s own case for earlier years. Ld.DR has not brought on record any distinguishing factor.

4. In this case Assessee Coco Cola India Private Limited is a domestic company engaged in the business of manufacturing and sale of beverage concentrates , dairy whiteners, etc . The Assessee is 100% subsidiary of Coco Cola South Asia India Holding Limited, Honkong. The Assessee filed its Return of Income electronically declaring Total Income at Rs.751,93,44,180/-. The assessee’s case was selected for scrutiny and Notice u/s 143(2) was issued on 13/08/2018. The AO made a reference to Transfer Pricing Officer. The Transfer Pricing Officer (TPO) passed an order u/s 92CA(3) of the Income Tax Act 1961 on 14/01/2021 proposing an upward adjustment of Rs.6,54,19,31,488/-

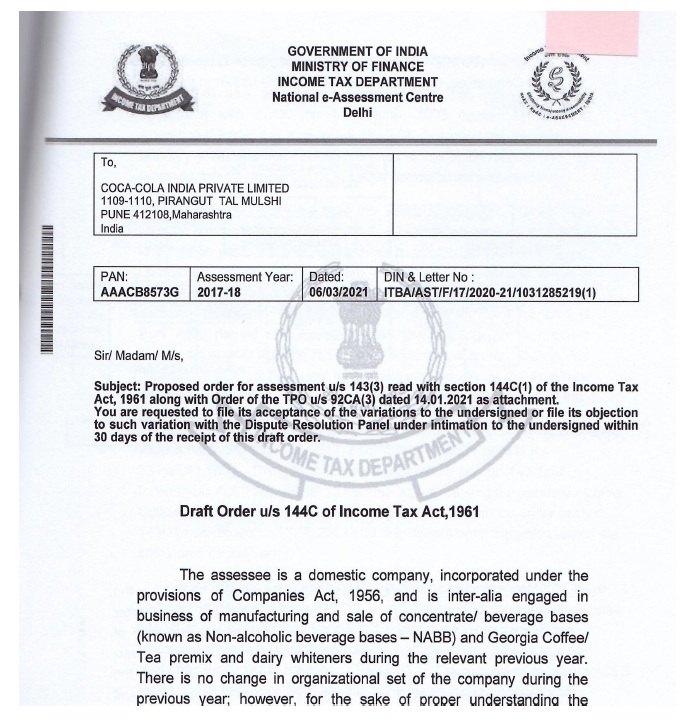

5. In this case , the Assessing Officer (National E Assessment Centre) passed an Order on 06/03/2021 titled as “Draft Order u/s 144C of the Income Tax Act 1961”. The first page of the said Order is scanned and reproduced here as under :

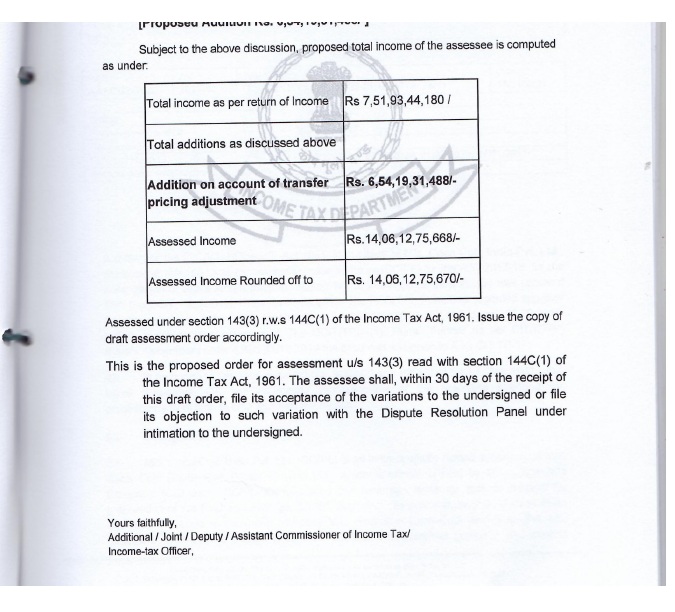

The Last page of the said Order dated 06/03/2021 is scanned as under :

5.1 However, the AO issued another Notice u/s 142 on 17/03/2021 seeking certain information. The assessee replied to the AO that once the Draft Assessment Order has been issued by the AO the Assessment Proceedings had been concluded and hence AO has no jurisdiction to issue such notice. AO issued a letter dated 23.03.2021 stating that the earlier 06.03.2021 communication was a letter and not draft assessment order. It was erroneously sent. Therefore, the letter dated 06.03.2021 was withdrawn with immediate effect vide letter dated 23.03.2021. Then the AO issued noticed dated 27.03.2021 u/s 142(1) of the Act and 30.03.2021 u/s 142(1) of the Act. The AO (National e-assessment Centre) passed a draft order u/s 144C of the Act for A.Y 2017-18 on 09.04.2021 (copy of the said order is at page No. 22 to 55 of paper book). Then AO passed a final assessment order on 15.06.2021 for A.Y 2017-18 assessing the total income at Rs. 17,33,01,53,480/-.

5.2 Aggrieved by the assessment order assessee filed appeal before Ld. CIT(A), raising legal grounds as well as grounds on merits of the addition. Ld. CIT(A)-13, Pune vide order dated 22.09.2025 for A.Y 2017-18 allowed the appeal of the assessee. Aggrieved by the order of ld. CIT(A) the revenue has filed appeal before this Tribunal.

6. We will discuss first the grounds related to additions made in the assessment order.

6.1 Ld. CIT(A) has discussed the addition under the head advertising and sale promotional expense of Rs. 5,18,65,26,221/- in para 47 onwards. Ld. CIT(A) has recorded in para 52 to 54 as under:

52. At the outset it must be pointed out that appellant’s claim with respect to the allowability of expenses relating to advertising and sales promotion expenses has been consistently allowed by the Hon’ble Pune Tribunal from AY 1997-98 to AY 2016-17. Key aspects emanating from the rationale underlying the decision of the Hon’ble Tribunal are as follows –

| i. |

|

Direct Nexus: The tribunal found a direct relationship between CCIPL’s business and the advertising expenditure. An increase in beverage sales directly led to an increase in the sale of concentrates manufactured by CCIPL. |

| ii. |

|

Primary Beneficiary: The tribunal determined that the primary beneficiary of the advertising and sales promotion expenditure was CCIPL itself, as the sales of concentrate directly depended on beverage sales. The benefits to bottlers or the parent company were considered incidental. |

| iii. |

|

Commercial Expediency: The expenditure was incurred based on commercial expediency. The tribunal was satisfied that the requirements of section 37(1) of the Income- tax Act were met. |

| iv. |

|

Economic Cost Recovery: The economic cost of advertising and services is indirectly recovered from the bottlers through higher concentrate prices, resulting in a high gross profit (GP) margin of CCIPL. |

| v. |

|

Incidental Benefit to Third Parties: Even if the brand owner or bottlers benefit from the advertisement expenditure, it should still be allowed as a deduction if it was incurred for promoting CCIPL’s business, and any incidental, direct or indirect benefit to the any other party should not be a ground for disallowance. ^T |

| vi. |

|

Wholly and Exclusively: Expenses incurred voluntarily and without necessity are permissible for deduction if it promotes CCIPL’s business. |

| vii. |

|

Consistency with Tribunal Orders: The ITAT consistently followed its own rulings in assessment Years (AY 1997-98 onwards) where the assessee’s case for earlier Assessment deduction for advertisement expenses had been allowed. |

53. Respectfully following the decision of Hon’ble Tribunal in appellant’s own case from AY 1997-98 to AY 2016-17, I hold the expenditure to be allowable and therefore delete the entire addition of Rs 518,65,26,221/- made on account of disallowance of advertising and sales promotion expenses by the AO.

54. The appellant succeeds on this ground of appeal; the ground is allowed.

6.2 Thus, Ld. CIT(A) allowed the assessee’s appeal by following the decision of Coordinate Bench of ITAT in assessee’s own case for A.Y 1997-98 to 2016-17.

6.3 Ld. DR has accepted that there is no distinguishing feature. Ld. DR accepted that the impugned issue is covered in favour of assessee by ITAT order in assessee’s own case.

6.4 Accordingly, having regard to the totality of the facts and circumstances of the case, and taking into consideration the decision rendered by the Coordinate Bench followed by Ld. CIT(A) on identical issue under similar factual circumstances in favour of the assessee. Respectfully following the decision of Coordinate Bench of ITAT and maintaining judicial consistency, particularly when identical additions made on similar facts have been deleted by the Coordinate Bench. No new facts or circumstances have been placed on record in order to controvert or rebut the findings so recorded by Ld. CIT(A). Therefore, we see no reasons to interfere into or to deviate from the lawful findings so recorded by Ld. CIT(A). Hence, these ground raised by the revenue stands dismissed.

7. As regards ground Nos. 6 & 7 raised by the revenue are interrelated and interconnected and relates to challenging the order of Ld. CIT(A) in deleting the addition on marketing support charges and discount made by the AO of Rs. 310,00,13,750/-.

7.1 In this regard ld AR submitted that this issue is squarely coved by the decision of Coordinate Bench of ITAT in assessee’s own case for A.Y 1997-98 to 2016-17. Contra ld. DR has accepted that there is no distinguishing feature. Ld. DR accepted that the impugned issue is covered in favour of assessee by ITAT order in assessee’s own case.

7.2 We have heard the rival contentions of both the parties and perused the material placed on record. In this regard we noticed that Ld. CIT(A) has discussed this issue in para 59 to 62. The relevant paragraph is extracted below:

59. The AO has erroneously considered Rs. 329,77,47,918/- as the reclassified amount from rebates and discounts, whereas the correct amount based on computation and breakup submitted is Rs. 264,18,38,353/-

Further, upon perusal of para 12.3 of the assessment order (Page No. 25) dated 15.06.2021 passed under section 143(3) r.w.s. 144C(3) r.w.s. 144B of the Income-tax Act, it is observed Further, upon perusal of Para 12.3 of the assessment order (Page No. 25) dated 15.06.2021 that the marketing expenses reclassified as “Rebates and Discounts” have been disallowed to the extent of Rs. 2,64, 18,38,353/-.

However, while computing the disallowance under Section 37(1) of the Act on account of these reclassified expenses, the amount has inadvertently been considered as Rs. 3,29,77,47,918/-, resulting in an apparent discrepancy.

The arithmetical error in computation of reclassified expenses is rectified, and the correct figure of Rs. 264, 18,38,353/- is accepted. This ground is accepted.

60. It must be pointed out that appellant’s claim with respect to the allowability of expenses under the head / relating to marketing support charges has been consistently allowed by the Hon’ble Pune Tribunal from AY 1997-98 to AY 2016-17. Key aspects emanating from the rationale underlying the decision of the Hon’ble Tribunal are as follows –

i. Direct Nexus with the Assessee’s Business: The ITAT recognised a direct and clear link between the marketing support expenses and the assessee’s business of selling concentrate. These expenses, in the form of rebates, discounts, and incentives given to the bottlers, were aimed at increasing the sale of concentrate.

ii. Wholly and Exclusively for Business Purpose: The ITAT accepted the assessee’s contention that the marketing support expenses were incurred wholly and exclusively for the purpose of its own business as required under Section 37(1) of the Act. The Tribunal found that these expenses were a legitimate business expenditure incurred to boost the volume of concentrate sold to the bottlers, ultimately leading to an increase in the assessee’s revenue. OME TAX DEPART

Encouraging Bottler Sales: The ITAT underscored that by providing marketing support, the assessee was encouraging the bottlers to promote and sell more of the finished beverages in their respective areas. This increase in beverage sales directly translates to a higher demand for the concentrate manufactured by the assessee.

iv. Distinction from Advertisement: The assessee’s clarification that marketing support expenses were mainly in the nature of discounts, rebates, and incentives based on sales volume, and were distinct from brand advertisement expenditure was fund to be tenable by the Tribunal.

V. Recovered from Bottlers: Given that the advertisement cost is indirectly recovered from the bottlers (including HCCB) by way of higher margin/prices charged from them, it is wrong to assume the scheme’s sole motive is to reduce losses of HCCB.

vi. Consistency with earlier Tribunal Orders: The ITAT, in various orders across different Assessment Years (including AY 2005-06 to AY 2016-17), has consistently allowed the deduction for marketing support expenses in the assessee’s own case.

61. Respectfully following the decision of Hon’ble Tribunal in appellant’s own case from AY 1997-98 to AY 2016-17, I hold the expenditure to be allowable and therefore delete the entire addition of Rs. 375,59,23,315/- made on account of disallowance of marketing support charges by the AO.

62. The appellant succeeds on this ground of appeal; the ground is allowed.

7.3 Accordingly, having regard to the totality of the facts and circumstances of the case, and taking into consideration the decision rendered by the Coordinate Bench followed by Ld. CIT(A) on identical issue under similar factual circumstances in favour of the assessee. Respectfully following the decision of Coordinate Bench of ITAT and maintaining judicial consistency, particularly when identical additions made on similar facts have been deleted by the Coordinate Bench. No new facts or circumstances have been placed on record in order to controvert or rebut the findings so recorded by Ld. CIT(A). Therefore, we see no reasons to interfere into or to deviate from the lawful findings so recorded by Ld. CIT(A). Hence, these ground raised by the revenue stands dismissed.

8. As regard ground of appeal No. 8, 9 & 10 raised by the revenue are interrelated and interconnected and relates to challenging the order of Ld. CIT(A) in deleting addition on service charges made by the AO.

8.1 In this regard ld AR submitted that this issue is squarely coved by the decision of Coordinate Bench of ITAT in assessee’s own case for A.Y 1997-98 to 2016-17. Contra ld. DR has accepted that there is no distinguishing feature. Ld. DR accepted that the impugned issue is covered in favour of assessee by ITAT order in assessee’s own case.

8.2 We have heard the rival contentions of both the parties and perused the material placed on record. In this regard we noticed that Ld. CIT(A) has discussed this issue in para 66 to 68. The relevant paragraph is extracted below:

66. I have carefully perused and considered the contentions, submissions, including the evidence and case laws, and the arguments put forth by the appellant as well as those put forth by the AO in his assessment order.

67. It must be pointed out that appellant’s claim with respect to the allowability of expenses under the head / relating to service charges and reimbursement to Coca Cola India Inc (CCII) has been consistently allowed by the Hon’ble Pune Tribunal from AY 1997-98 to AY 2016-17. Key aspects emanating from the rationale underlying the decision of the Hon’ble Tribunal are as follows –

| i. |

|

Nexus to Assessee’s Business: The ITAT found a direct nexus between the services rendered by CCI Inc. (even those relating to bottlers’ plants or quality audits) and the assessee’s business of manufacturing and selling concentrate an increase in beverage sales directly impacts the sale of the assessee’s concentrate. |

| ii. |

|

Rejection of Strict Separate Entity View: While acknowledging the separate legal identities within the Coca-Cola group, the ITAT did not consider this a bar to deductibility if the expenditure ultimately served the assessee’s business objectives. The ITAT’s focus was on the economic benefit to the assessee’s concentrate business. |

| iii. |

|

Wholly and Exclusively for Business (Section 37(1)): The ITAT considered the expenditure to be wholly and exclusively for the purpose of the assessee’s business under Section 37(1) of the Income Tax Act. Incidental benefit to third parties (like bottlers) does not negate this if the primary purpose serves the assessee’s business interests. The term ‘exclusively’ does not mean that only the assessee should benefit. |

| iv. |

|

Consistency with Preceding Year Orders: The Tribunal followed its own rulings for immediately preceding assessment years, maintaining judicial consistency on the issue, even when the Revenue raised similar arguments, or that the service agreement(s) evolved over time. |

68. Respectfully following the decision of Hon’ble Tribunal in appellant’s own case from AY 1997-98 to AY 2016-17, I hold the expenditure to be allowable and therefore delete the entire addition of Rs. 11,11,54,092 / made on account of disallowance of marketing support charges by the AO.

8.3 Accordingly, having regard to the totality of the facts and circumstances of the case, and taking into consideration the decision rendered by the Coordinate Bench followed by Ld. CIT(A) on identical issue under similar factual circumstances in favour of the assessee. Respectfully following the decision of Coordinate Bench of ITAT and maintaining judicial consistency, particularly when identical additions made on similar facts have been deleted by the Coordinate Bench. No new facts or circumstances have been placed on record in order to controvert or rebut the findings so recorded by Ld. CIT(A). Therefore, we see no reasons to interfere into or to deviate from the lawful findings so recorded by Ld. CIT(A). Hence, these ground raised by the revenue stands dismissed.

9. The ground No. 11 raised by the revenue is relates to challenging the order of Ld. CIT(A) in deleting the addition on depreciation on coolers made by the A.O.

9.1 In this regard ld AR submitted that this issue is squarely coved by the decision of Coordinate Bench of ITAT in assessee’s own case for A.Y 1997-98 to 2016-17. Contra ld. DR has accepted that there is no distinguishing feature. Ld. DR accepted that the impugned issue is covered in favour of assessee by ITAT order in assessee’s own case.

9.2 We have heard the rival contentions of both the parties and perused the material placed on record. In this regard we noticed that Ld. CIT(A) has discussed this issue in para 66 to 68. The relevant paragraph is extracted below:

| iv. |

|

Assessee’s Ownership and Control: A significant factor in the ITAT’s decision was that Coca-Cola India Pvt. Ltd. retained complete ownership of the coolers at all times. Furthermore, the assessee maintained a degree of control over the coolers, including the right to access outlets to verify their assets, move coolers between locations, and replace them as needed. These terms and conditions indicated that the coolers were not simply given away to the bottlers or vendors but remained the property and under the strategic control of the assessee, further solidifying their use for the assessee’s business. |

| v. |

|

Interlinked Businesses: The ITAT explicitly rejected the Assessing Officer’s argument that because the coolers store the final beverages (produced by the bottlers) and not the concentrate (manufactured by the assessee), they are not used for the assessee’s business. The Tribunal firmly established the inherent and inseparable connection between the assessee’s business of manufacturing concentrate and the bottlers’ business of producing and selling the final beverages. The demand for the final beverage directly dictates the demand for the concentrate. Therefore, any asset or activity that promotes the sale of the beverages indirectly but surely benefits the assessee’s core business. This recognition of the symbiotic relationship within the Coca-Cola system in India was central to the ITAT’s reasoning on the depreciation of coolers. |

| vi. |

|

Consistency (in some cases): In certain instances, the ITAT observed that the Assessing Officer or the Commissioner of Income Tax (Appeals) had allowed similar depreciation claims on coolers in preceding assessment years. |

74. Respectfully following the decision of Hon’ble Tribunal in appellant’s own case from AY 1997-98 to AY 2016-17, I hold the expenditure to be allowable and therefore delete the entire addition of Rs. 75,72,05,676/- made on account of disallowance of marketing support charges by the AO.

75. The appellant succeeds on this ground of appeal; the ground is allowed.

J. Discussion on Ground No. 8

9.3 Accordingly, having regard to the totality of the facts and circumstances of the case, and taking into consideration the decision rendered by the Coordinate Bench followed by Ld. CIT(A) on identical issue under similar factual circumstances in favour of the assessee. Respectfully following the decision of Coordinate Bench of ITAT and maintaining judicial consistency, particularly when identical additions made on similar facts have been deleted by the Coordinate Bench. No new facts or circumstances have been placed on record in order to controvert or rebut the findings so recorded by Ld. CIT(A). Therefore, we see no reasons to interfere into or to deviate from the lawful findings so recorded by Ld. CIT(A). Hence, these ground raised by the revenue stands dismissed.

10. Transfer pricing adjustment 12 to 16. Ld. CIT(A) has held that TPO has not arrived at mark-up of 4.6% based on any recognized method. Ld. CIT(A) observed that a mark-up arrived arbitrary without following any method is bad in law. Ld. CIT(A) also noted that assessee has demonstrated that its overall profitability provides adequate compensation for all its activities including so called brand building therefore ld. CIT(A) following ITAT order in assessee’s own case for earlier years, has allowed assessee’s ground regarding transfer pricing adjustment on account of AMP expenses. Therefore, we see no reasons to interfere into or to deviate from the lawful findings so recorded by Ld. CIT(A). Hence, the ground raised by the revenue stands dismissed.

11. The revenue has raised legal grounds, vide ground Nos. 1 & 2. We have heard the rival arguments made by both the sides, perused the orders of the Assessing Officer and Ld. CIT(A) / NFAC and the paper book filed on behalf of the assessee. We have also considered the various decisions cited before us. decided the issue of additions made in this assessment orders in favour of assessee, by following earlier years orders of ITAT in assessee’s own case, hence the legal ground Nos. 1 & 2 raised by revenue becomes academic. Accordingly, grounds Nos. 1 & 2 raised by revenue are dismissed unadjudicating.

12. In the result, the appeal filed by the revenue stands dismissed in above terms.