ORDER

Sandeep Gosain, Judicial Member.- This appeal is filed by the Assessee against the order of Ld. CIT Appeal (NFAC) vide DIN: ITBA/APL/S/250/2025-26/1078723279(1) dated 21-Jul-2025 for the Assessment Year 2013-14. The Assessee has raised the following grounds of appeal:

| 1. |

|

The CIT Appeal and Assessing officer erred in not considering the fact that the assessee had invested the entire amount of sale proceeds from old house/flat in the purchase of the new house/ flat and hence the disallowance of claim of section 54 cannot be done. |

| 2. |

|

The CIT Appeal and Assessing officer erred in not considering the fact that the assessee’s wife was unwell and with the intention to give her mental peace to the wite, assessee included the name of the wife and that the assessee’s funds from sale of flat have gone in to the purchase of the new property and therefore the claim of section 54 was allowable. |

| 3. |

|

The CIT Appeal and Assessing officer erred in disallowing claim of section 54 of assessee of Rs 55,48,955/- based on surmises and conjectures. |

| 4. |

|

The assessee craves leave to add, alter amend or delete any of the above grounds of appeal. |

2. All the grounds raised by the assessee are interrelated and interconnected and relates to challenging the order of the Ld. CIT(A) in upholding the disallowance of the claim made by the AO under Section 54 of the Act. Therefore, we have decided to adjudicate these grounds through the present consolidated order.

3. Ld. AR reiterated the same arguments as were raised before the Revenue Authorities and also submitted that the facts put up before the Ld. CIT(A) may be treated as his arguments before us too. In this regard, reliance was placed upon Para No. 4 of the order of the Ld. CIT(A) and the relevant portion of the same is reproduced herein below:

Background of the Case:

The assessee filed his return of income on 10.10.2013, declaring a total income of Rs.3,72,770/-. The assessment order was passed on 18.03.2016 assessing total income at Rs. 59,21, 730/-. The primary reason for the addition was the partial disallowance of the deduction claimed under section 54 of the Income Tax Act.

2. Dispute Regarding Deduction under Section 54:

The assessee sold his residential property and reinvested the sale proceeds in another residential property, claiming exemption under section 54 of the Act. However, the Assessing Officer restricted the exemption to 50% of the investment amount, stating that the new property was jointly owned by the assessee and his wife, and that 50% of the investment was made by his wife.

Grounds of Appeal and Submissions

1. Erroneous Disallowance of Deduction u/s 54 of the Income-tax Act, 1961

AO’s Contention:

The AO restricted the deduction under section 54 to Rs. 55,00,000, alleging that the appellant lacks ownership/control over 50% of the new flat purchased jointly with his wife.

The assessee continued to report the entire property under his house property income in his tax return, supporting his claim that the full investment should be considered for exemption under section 54.

2. Fulfilling the Conditions of Section 54:

Section 54 requires that the assessee invest in a new residential property within the stipulated time frame, which has been duly complied with. The law does not restrict joint ownership as a condition for claiming exemption, provided the funds for investment are sourced from the capital gains of the assessee.

The denial of 50% of the exemption on the basis of ownership structure alone is not supported by any specific provision under section 54.

The appellant invested Rs. 1,10,48,955 (entire LTCG) into the new flat within the statutory timeline. The spouse’s contribution (Rs. 55,00,000) originated from the appellant’s gift, validated by bank statements and the gift deed (Annexure 1).

Joint Ownership and Beneficial Interest:

The new flat is jointly registered in the appellant’s name, establishing legal title. The AO’s reliance on “domain and control” is misplaced, as section 54 only mandates ownership, not exclusive possession.

In CIT v. R. Lakshmipathy [2021] 432 ITR 129 (Mad), the court held that joint ownership qualifies for full deduction if the investment is sourced from capital gains.

Conclusion:

The disallowance of Rs. 55,48,955 is untenable. The appellant is entitled to the full deduction of Rs. 1,10,48,955 u/s 54.

Legal Ownership and Clubbing Provisions (Section 64(1)(iv)):

The AO failed to consider that the Rs. 73,00,000 gifted to the spouse (Mrs. Samina Amin Fazlani) is deemed the appellant’s income under section 64(1)(iv). Consequently, the investment in the new flat by the spouse using these funds is constructively the appellant’s investment.

Judicial precedents (e.g., CIT v. Kamal Wahal [2013] 350 ITR 13 (Del)) affirm that clubbing provisions apply to investments made through transferred funds, satisfying the ownership requirement for deductions.

CIT v. KAMAL WAHAL CASE

-Capital gains–Deduction under section 54F-Purchase of residential house in the name of assessee’s wife.—Assessing officer disallowed deduction under section 54F claimed by assessee holding that investment in the residential house should be made in assessee’s name and not in the name of his wife. Held: Was not justified, as with regard to the rule of purposive construction and section 54F being beneficial provision it does not require that new residential property should be purchased in the name of assessee. Moreover, assessee purchased new house in name of his wife and not in the name of stranger, therefore, the entire investment had come out of the sale proceeds of assessee.

3. AO’s Misinterpretation of Rule 46A and Evidence

AO’s Contention:

The AO rejected additional evidence under Rule 46A, claiming the appellant had ample opportunity during assessment.

Appellant’s Submission: The remand report itself acknowledges the submission of critical documents (ITRS, gift deed, bank statements) to substantiate the source of funds. These documents were necessary to rebut the AO’s findings and fall under Rule 46A(1)(c) (evidence relevant to grounds of appeal).

The Delhi High Court in CIT v. Kabul Chawla

(2016) 380 ITR 573 ruled that evidence submitted during remand proceedings must be considered if it clarifies factual disputes.

Conclusion:

The CIT(A) must admit and evaluate the evidence to ensure a fair adjudication.

Prayer

The appellant respectfully prays that:

1. The disallowance of Rs. 55,48,955 u/s 54 be deleted.

2. The total income be revised to Rs. 3,72,770 as declared.

3. Penalty proceedings u/s 271(1)(c) be dropped.

Reasons why the additional evidence may be admitted: PREAMBLE 1 1 The said intention was put into action by declaring the intention in the ITR as “(1) Not coowned” and also “(2) 100% share belonging to the assessee” Copy of ITR annexed. The intention of the appellant was to make full investment of capital gains Rs.1, 10, 48,955 and claim deduction u/s 54 of the Income Tax Act, 1961. Which is on record in the e-filing portal of India Tax Filing. Thus, without prejudice to any submissions made earlier at the time of original hearing, the fresh evidence supersedes these and the fresh evidence replaces the earlier submissions which now stand redundant and which are specifically reproduced for rebuttal and rejection and elimination. Without prejudice: 2 Held “If an assessee does not claim exemption at initial stage, he is not debarred, prohibited or stopped from claiming such benefit at a later stage. Exemption can be claimed at adjudication stage even if not claimed at investigation stage, or erroneously claimed previously.

3 There is no res judicata or estoppel in taxation matters. Either taxable person or department can change its stand/views about taxability and exemption can be claimed.

4 Exemption can be claimed even at an appellate stage as it is a legal right.

5 .

20.6-1 Strict interpretation at first stage but not at later stage

In Mangalore Chemicals and Fertilisers Ltd. v. Dy. CCT 83 STC 234-55 ELT 437 = AIR 1992 SC 152 = 1992 Suppl (1) SCC 21, Hon. Supreme Court has held: “When the question is whether a subject falls in the notification or in the exemption clauses, the interpretation should be strict as it is in the nature of an exception. But once the ambiguity about applicability is lifted and it is held that the subject falls in the notification, then full play should be given to it and it calls for a wider and libera construction. It will be erroneous to attach equal importance to the non-observanc of all conditions irrespective of the purposes they were intended to serve.”

6 Rule 46A Cannot Override Principles of Natural Justice. In case the evidences surfaced after the assessment orders and appellant moved with such evidences and produces before the CIT (A) which are the vital evidences and touch the roots of the case, the admissibility of such evidences cannot be denied overriding the principles of natural justice.

7 The principle “Audi alteram partem”, i.e. no man should be condemned unheard is the basic canon principles of natural justice.

SUBMISSION: 1 The assessee could collect further evidences only after passing of the assessment order.

2 These additional evidences are vital documents which are required to be considered in order to adjudicate the issue in a judicious manner.

3 Further there was bona fide reason that the said ground could not be raised earlier in as much as a procedural lapse on the part of the accountant being an ITP and not a professional CA and who had appeared before the original AO and provided information and presentation which was not sufficient to allow the AO to arrive at a proper assessment order.

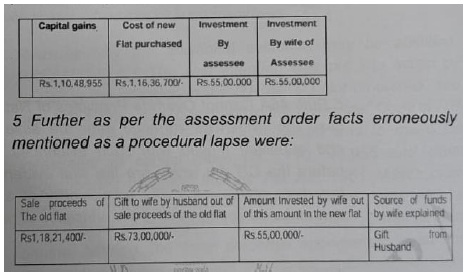

4 As per assessment order facts erroneously mentioned as a procedural lapse were

REBUTTAL: The procedural lapses as mentioned during the original assessment proceedings cannot fasten liability on an assessee as factually the assessee has invested the entire amount of Rs. 1,10,00,000/

8 As per the assessment order “the assessee had transferred 50% share of his property before the prescribed period and the wife became the owner for all the purposes of the 50% flat. The above-mentioned fact disentitled the assessee to claim deduction u/s 54 of the Act for the full payment of Rs.1,10, 00,000/- as the wife had declared investment of Rs.55 lakhs in the flat “in her balance sheet.” Rebuttal: The assessee’s balance sheet in the enclosed ITR does not reflect any

investment of Rs.55 lakhs which is factually correct which ITR need to be considered now as additional evidence. The ITR declares and reflects the following facts under the Head Income from House Property: “(1) Not coowned” and also “(2) 100% share belonging to the assessee” The assessee’s wife’s balance sheet in the enclosed ITR does not reflect any investment of Rs.55 lakhs in her balance sheet and which is factually a correct position and which need to be considered now as additional evidence. Her ITR is conspicuously absent of the following facts under the Head Income from House Property: “(1) Co-owned” and also “(2) 50% share belonging to the assessee” Thus the information given at the time of original hearing was a procedural lapse on the part of the ITP who presented the case and a misrepresentation which cannot fasten liability for paying tax which is factually not payable.

9 Further as per the assessment order, the wife’s case was selected under Cass for verifying the source of funds of Rs.55 lakhs by the wife for investing in the flat costing Rs. 1,10,00,000/-. The said assessing officer agreed that u/s 4(1) (a) (i) of the Wealth Tax Act, where the assessee transfers his assets to spouse without adequate consideration or without agreement to live apart, then such transferred asset shall be deemed to be the wealth of the transferor. Accordingly the investment of Rs.1, 10, 00,000/-was made by the assessee and it was accepted by the AO assessing the wife of the assessee. The original AO accepted in his assessment order that the clubbing provisions for wealth tax purpose could be considered only for the purpose of computation of wealth tax payable and not for the purpose of claiming deduction u/s 54 of the Income Tax Act, 1961.

Rebuttal: This is a contradictory statement because if once the clubbing provisions are accepted, it cannot be denied for claiming deduction u/s 54 of the Income Tax Act, 1961, as, for all practical purpose the said investment forms part of the assessee’s wealth and thereby a part of his balance sheet without which the wealth tax cannot be computed.

10 Further as per the assessment order the regular AO refused to agree to the above contentions and insisted that the assessee’s wife had a clear marketable title on the property. If the investment forms part of the assessee’s wealth and thereby a part of his balance sheet, this argument stands demolished.

11 Accordingly the AO denied deduction to the extent of Rs.55,00,000/- to the assessee and brought to tax the said amount. If the investment forms part of the assessee’s wealth and thereby a part of his balance sheet, the denial of deduction is not sustainable and addition cannot be made taxable. The further evidence is as follows:

1 ITR filed by the appellant which is on the e filing portal and a copy of which is enclosed clearly show that the house property at Akash Apartment Room No.1704, Mumbai 400 011 is not co-owned and the appellant’s share in property is 100%. Annexure ITR enclosed.

2 ITR filed by the appellant’s wife which is on Government e filing portal and a copy of which is enclosed clearly show that the house property at Akash Apartment Room No.1704, Mumbai 400 011 is nowhere shown as house property in her return of income. Annexure ITR enclosed. This clearly show the intention of the appellant that the entire investment of Rs. 1,10,00,000/ was for purchasing the new flat entirely in his own name for the purpose of claiming deduction under section 54 of the Income Tax Act, 1961 of Rs. 1,10,00,000/-PRAYER; For all the above-mentioned reasons and explanations, it is requested that:

the additional evidence be taken on record and the case be remanded back to the learned AO for reassessment based on fresh evidence, or the demand raised cancelled.”

4. It was further submitted that the assessee is an individual who had sold an immovable property resulting in LTCG, and the assessee had invested the said proceeds from the sale of the original property for acquiring a new residential house property jointly with his wife. However, the exemption claimed under Section 54 of the Act against the LTCG arising on the sale of the original property was denied to the extent of Rs. 55 lakhs on the ground that half of the share in the new property was in the name of the wife of the assessee. In this regard, reliance was placed on the decisions in the following cases:

| • |

|

CIT v. Dr. Laxmichand Narpal Nagda 211 ITR 804 (Bombay) |

| • |

|

Prakash v. ITO [2009] 312 ITR 40 (Bombay) |

| • |

|

CIT v. V. Natarajan 287 ITR 271 (Madras) |

| • |

|

CIT v. Kamal Wahal 351 ITR 4 (Delhi) |

| • |

|

Balraj v. CIT 254 ITR 22 (Delhi) |

| • |

|

CIT v. Gurnam Singh [2010] 327 ITR 278 (Punjab & Haryana) |

5. The assessee had also submitted the following documents in support of his contentions:

| • |

|

Copy of Agreement of Sale dated 07.06.2012. |

| • |

|

Copy of Purchase Agreement dated 23.08.2012. |

| • |

|

Deed of Rectification dated 31.08.2012. |

| • |

|

Gift Deed dated 19.05.2012 between the Appellant and the Appellant’s wife. |

| • |

|

Extracts of the bank statement of the Appellant. |

| • |

|

Bank account summary of the Appellant. |

| • |

|

Extracts of the bank statement of Samina Fazlani (Appellant’s wife). |

| • |

|

Bank account summary of the Appellant’s wife. |

| • |

|

Copy of the Income Tax Return of the Appellant for Assessment Year 2013-14. |

| • |

|

Application seeking admission of additional evidence and acknowledgement dated 04.01.2023. |

6. Whereas, the Ld. DR placed reliance on the orders passed by the Revenue Authorities and also upon the decision of the Hon’ble Bombay High Court in the case of Prakash(supra).

7. We have heard the counsel for both the parties, perused the material placed on record, the judgments cited before us, and also the orders passed by the Revenue Authorities. From the records, we noticed that the assessee, being an individual, sold an immovable property (original asset) resulting in LTCG and invested the amount received from the sale of the said property for acquiring a new residential property jointly with his wife. In this manner, cumulatively, a sum of Rs. 1,10,00,000/- was invested.

8. As per the assessee, for the sake of convenience, the name of the assessee’s wife was also included as a joint owner in the registered sale agreement for the said new residential house property. In order to have equal contribution from both, the assessee transferred part of the sale proceeds received to his wife’s bank account, which was thereafter utilized for acquiring the new property. Accordingly, on the basis of the above arrangement, exemption under Section 54 of the Act was claimed against LTCG arising on the sale of the original property. However, the same was refused by the AO to the extent of Rs. 55 lakhs on the ground that half of the share in the new property belonged to the wife of the assessee.

9. Although the assessee preferred an appeal, the Ld. CIT(A) upheld the assessment order by observing that it was necessary and obligatory to make investment in the new property in the name of the assessee only and not in the name of any other person. It was further held that joint purchase of the new property does not qualify for deduction under Section 54 of the Act and that the deduction should be restricted only to the extent of 50% of the total investment. While doing so, reliance was placed upon the decision of the Hon’ble Bombay High Court in the case of Prakash (supra).

10. Whereas, on the contrary, we notice that although the property agreement bears the name of the assessee’s wife as co-owner, in our view, this by itself cannot disqualify the assessee from seeking deduction under Section 54 of the Act. In this regard, reliance is placed upon the decision of the Hon’ble Bombay High Court in the case of Dr. Laxmichand Narpal Nagda (supra) relevant extract of the same is reproduced herein below:

“6. Taking into consideration the letter as well as the spirit of section 54 and the word ‘towards’ used before the word ‘purchase’ in sub-section (2) of section 54, it seems to us that the said word is not used in the sense of legal transfer and, therefore, holding of a legal title within a period of one year is not a condition precedent for attracting section 54. In the instant case, the whole consideration was paid, possession of the flat was obtained and it was actually put to use for dwelling within 4 months, as a result exemption contemplated under section 54 was clearly attracted”

11. Reliance is also being placed upon the decision of Balraj(supra); the relevant extract of which is as under:

“3. The Assessing Officer, the appellate authority as well as the Tribunal rejected the claim of the assessee in respect of the assessment year 1975-76 on the ground that he did not become the owner of the property, as the said transaction was not evidenced by registration thereof as provided under section 17 of the Registration Act. For the purpose of attracting the provisions of section 54, it is not necessary that the assessee should become the owner of the property. Section 54 speaks of purchase. Moreover, the ownership of the property may have different connotations in different statutes. The question which arises for consideration appears to be squarely covered by a decision of the Apex Court in CIT v. T.N. Aravinda Reddy[1979] 120 ITR 461 where it has been held that the word ‘purchase’ occurring in section 54(1) of the Act had to be given its common meaning, viz., buy for a price or equivalent of price by payment in kind or adjustment towards a debt or for other monetary consideration. Each release in this case was a transfer of the releasor’s share for consideration to the release and the transferee, theassessee, “purchased” the share of each of his brothers and the assessee was, therefore, entitled to the relief under section 54(1).”

12. Even the decision of the Hon’ble Bombay High Court in the case of Prakash(supra), which was relied upon by the AO to deny the exemption to the assessee, is distinguishable on following grounds:

(i) In that case the deceased assessee had acquired the new property entirely in the name of his adopted son; thereby giving up his domain/right over the new property.

Whereas in the present case of the Appellant; the name of Appellant’s wife was included just for convenience of owning joint property. The Appellant had nowhere given up his domain/right over the new property.

(ii) The basis of the Hon’ble Court in Prakash(supra) was to debar creation of any third party right in the new property (step son in that case)

Whereas, in the present case the wife was made joint owner.

13. In the present case, the assessee’s wife was made a co-owner; therefore, the pari materia facts contained in Prakash (supra) are distinguishable from the present case and hence cannot be relied upon. Moreover, in Para 11 of the above judgment, i.e. , Prakash (supra), it has clearly been stated that:

“11. The concepts of the ‘assessee’, ‘own’, ‘owned’, ‘owner’, ‘ownership’, ‘coowner’, ‘owner of house property’ or ‘ownership of property’ as elaborated in sections 22 to 27 and 32 of the Income-tax Act, are very much inter-linked and connected for granting the benefit under the Income-tax Act. An assessee must have valid title legally conveyed to him after complying with the requirement of law or at least entitled to receive income from the property in his own right and have control and domain over the said property for all legal purposes, which basically excludes a third person of any right over the said property. Therefore, all these concepts are inter-linked.”

14. Therefore, drawing analogy from the above, we observe that for all practical purposes, Sections 27 and 64 of the Act also provide for assessment of income in the hands of the transferor spouse even when the asset/income is transferred to the transferee spouse. Thus, merely because the name of the wife is included in the property cannot debar the assessee from claiming the benefit of Section 54 of the Act. In this regard, we place reliance on the relevant extracts of Sections 27 and 64 of the Act:

“27. For the purposes of sections 22 to 26—

(i) an individual who transfers otherwise than for adequate consideration any house property to his or her spouse, not being a transfer in connection with an agreement to live apart, or to a minor child not being a married daughter, shall be deemed to be the owner of the house property so transferred.”

“64. (1) In computing the total income of any individual, there shall be included all such income as arises directly or indirectly—

(iv) subject to the provisions of clause (i) of section 27, to the spouse of such individual from assets transferred directly or indirectly to the spouse by such individual otherwise than for adequate consideration or in connection with an agreement to live apart.”

15. Apart from this, the Hon’ble Delhi High Court in the case of Kamal Wahal(supra) inter alia held that Section 54F does not mandate purchase of property in the assessee’s own name or exclusively in the name of such assessee. Purchase of property in the name of the wife is permissible, as the wife is neither a stranger nor an unconnected person to the assessee.

Relevant extract from the said decision:

“9. It thus appears to us that the predominant judicial view, including that of this Court, is that for the purposes of Section 54F, the new residential house need not be purchased by the assessee in his own name nor is it necessary that it should be purchased exclusively in his name. It is moreover to be noted that the assessee in the present case has not purchased the new house in the name of a stranger or somebody who is unconnected with him. He has purchased it only in the name of his wife. There is also no dispute that the entire investment has come out of the sale proceeds and that there was no contribution from the assessee’s wife.”

16. We also noticed that in the judicial precedents it has consistently been held that the benefit of Section 54 cannot be denied merely because the name of the wife/son was included in the property:

(a) V. Natarajan (supra):

“3. 3 It is admitted by the assessee that he sold a house property at Bangalore. Therefore, it is clear that the assessee owned a house property and sold the same. He also admits that he purchased a property at Madras in the name of his wife Smt. Meera out of the money obtained by him by sale of the property at Bangalore.

3.4 Section 54 of the Act clearly says that if the assessee is the owner of the property, he is not (sic) entitled for exemption.

3.5 In the instant case, the assessee purchased a house at Anna Nagar in the name of his wife Smt. Meera after selling the property at Bangalore. But the same was assessed in the hands of the assessee. Hence, as correctly held by the CIT(A) as well as by the Tribunal that the assessee is entitled for exemption under section 54 of the Act.

3.6 The assassee sold a property at Bangalore and purchased a property at Anna Nagar in the name of his wife is only a question of fact. It is a settled law that the factual findings of the Tribunal cannot be disturbed in exercise of the powers under section 260A of the Act vide M. Janardhana Rao v. Jt. CIT [2005] 273 ITR 501 (SC). Hence, we do not see any question of law much less, substantial question of law arises for consideration. Accordingly, the first question fails and the same is rejected.”

(b) Kamal Wahal (supra]

(c) Gurnam Singh (supra)

“. Undisputedly, in this case the assessee had sold the agricultural land which was being used by him for agricultural purposes. Out of sale proceeds of the said sale, the assessee has purchased other piece of land (land in question) in his name and in the name of his only son, who was bachelor and dependent upon him, for being used for agricultural purposes within the stipulated time. Further, it is not the case of the revenue that from the sale proceeds of the agricultural land earlier owned by the assessee, the land in question was purchased for any other purpose than the agricultural purpose. Undisputedly, the purchased land is being used by the assessee only for agricultural purpose and merely because in the sale deed his only son was also shown as co-owner, the ITAT has rightly come to the conclusion that it does not make any difference because the purchased land is being used by the assessee for agricultural purposes. It is not the case of the revenue that the said land is being used exclusively by his son. In our view, a pure finding of fact has been recorded by the ITAT which does not require any interference in this appeal.”

17. Therefore, considering the totality of the facts and circumstances discussed above, and also keeping in view the judicial precedents referred to hereinabove, we hold that the benefit of the provisions of Section 54 of the Act cannot be denied to the assessee merely on account of the fact that the sale proceeds from the sale of the original property were invested in acquiring a new property jointly with his wife as co-owner. Accordingly, we direct the AO to allow the claim of the assessee under Section 54 of the Act. Therefore, these grounds raised by the assessee are allowed.

18. In the result, the appeal of the assessee is allowed.