ORDER

Manish Agarwal, Accountant Member.- The captioned cross-appeals are filed by assessee and the Revenue against the order dated 18.09.2025 of Ld. Commissioner of Income Tax (A), National Faceless Appeal Centre (“NFAC”), Delhi [“Ld. CIT(A)”] in Appeal No. NFAC/2020-21/10201208 passed u/s 250 of the Income Tax Act, 1961 [“the Act”] arising out of assessment order dated 27.12.2022 passed u/s 143(3) r.w.s. 144B of the Act pertaining to Assessment Year 2021-22.

2. Both cross-appeals filed by the assessee and the Revenue for the same assessment years therefore, both cross-appeals filed by the assessee and the Revenue are decided by a common order for the sake of convenience.

3. Brief facts of the case are that the assessee is a company, filed its return of income on 10.03.2022, declaring loss of INR 21,48,54,609/-. The assessee is engaged in the business of real estate construction and during the year under appeal, assessee has continued the construction contracts awarded in preceding years. The case of the assessee was selected for scrutiny and in terms of the order passed u/s 143(3)/144B of the Act dated 27.12.2022, total income of the assessee was assessed at INR 4,23,64,299/- by making following additions/disallowances:-

| i. |

|

Disallowance of proportionate interest expenditure on interest free loan to related party u/s 36(1)(iii) of the Act of INR 11,11,84,813/-; |

| ii. |

|

Cessation of liability u/s 41 of the Act of INR 2,31,02,037/-; |

| iii. |

|

Disallowance of provision for expenses of preceding years of INR 50,37,723/-; and |

| iv. |

|

Estimation of profit by 8% on WIP of INR 3,31,65,737/ |

4. Aggrieved by the said order, the assessee filed an appeal before Ld. CIT(A) who vide impugned order dated 18.09.2025, has partly allowed the appeal of the assessee.

5. Aggrieved by the said order, both parties i.e. the assessee and the Revenue are in appeal before the Tribunal by taking various Grounds of appeal mentioned in the appeal memo.

6. First we take appeal of the assessee in ITA No.6597/Del/2025 [Assessment Year 2021-22].

ITA No.6597/Del/2025 [Assessment Year 2021-22]

[Assessee’s appeal]

7. All the Grounds of appeal are with respect to the estimation of income by applying 8% profit rate on the value of work-in-progress as at the last day of the previous year by holding that the assessee has not disclosed any income though it had received substantial amount as advanced against which work-in-progress was declared.

8. Briefly stated facts on this issue are that AO at page 39 of the order observed that assessee has shown work-in-progress of INR 50,00,44,299/- and has shown item-wise work-in-progress and no details were shown project-wise nor any substantial income was declared therefore, AO asked the assessee to file project-wise receipts. The assessee in reply has submitted that during the year under appeal, the assessee has received advances on following three projects;-

| (i) |

|

SKY Forest Project, Mumbai wherein advance of INR 4,13,83,95,229/- were received; |

| (ii) |

|

IFC Tower from where advances of INR 3,30,03,01,507/-were received; |

| (iii) |

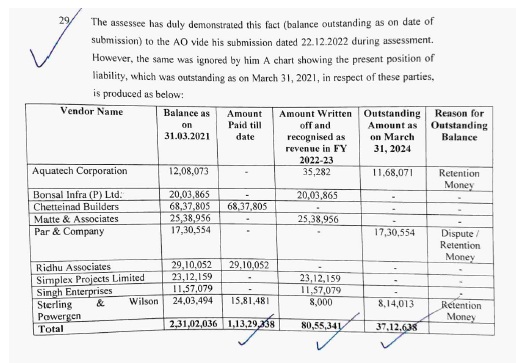

|

Besides this, a sum of INR 90,71,05,000/- was received from Lucina Land Development Ltd. It was stated by the assessee that the advance received from Lucina Land Development Ltd. was returned in subsequent years. |

9. The AO further observed that against the receipts of the projects awarded from India Bulls Properties Pvt. Ltd.& IFC Tower project, assessee has shown work-in-progress at INR 2,95,76,599/- & INR 38,49,95,116/- respectively on which why not 8% profit rate is to be applied as no substantial revenue was recognized by the assessee though substantial amount has been received by following POCM method for computing the income. After considering the replies filed by the assessee, AO observed that assessee has not followed POCM method which is mandatory and further has not filed details of estimated cost incurred etc. therefore, he applied profit rate of 8% on work-in-progress shown and made addition of INR 3,31,65,737/- for the same.

10. In first appeal, Ld. CIT(A) confirmed the addition made by the AO by observing that the methods of Revenue recognition should be in accordance with AS 7 and ICDS III or section 43B of the Act. Accordingly, the addition made was confirmed.

11. Against the said order, the assessee is in appeal before the Tribunal wherein the assessee has made detailed submissions contending that assessee is a construction contractor and recognized its revenue on Project Completion Method whereas AO has applied POCM method which is applicable to the real estate projects for recognized revenue of long term projects which usually extended for multiple years.

12. Ld.AR for the assessee submits that books of accounts of the assessee were accepted and the assessee has recorded the revenue whenever the work stood approved by the customer. As per ld. AR majority of income was recognized in preceding AYs where assessments were completed u/s 143(3) of the Act also. Ld.AR submits that in AY 2017-18, the revenue of more than INR 100.61 crore was declared from Sky Forest project awarded by India Bulls Properties Pvt. Ltd. and the assessment was completed u/s 143(3) of the Act where income declared was accepted by the Revenue. He further submits that in AYs 2018-19, 2019-20 and 2020-21, the revenue of INR 63.15 crores, INR 97.25 crores and 92.96 crores respectively, were declared which stood accepted by the Revenue in the order passed u/s 143(3) for AY 2018-19 and in subsequent year, no assessment was completed u/s 143(3) however, the proceedings were never initiated us/ 147 of the Act. Ld. AR further submits that though the AO in the year under appeal has taxed the work-inprogress by applying 8% profit rate however, in subsequent assessment year, revenue of INR 84.17 crores recognized by the assessee out of the same work-in-progress has been assessed u/s 143(3) of the Act.

13. Ld. AR for the assessee submits that AO has made double addition as in the year under appeal, income is estimated by applying 8% on work-in-progress declared at the end of the year and further in subsequent year when the Revenue is recognized by the assessee on such work-in-progress, the same was accepted by the AO. Likewise, in respect of other project awarded by One International Centre Pvt. Ltd. of IFC New Tower, Mumbai, the assessee has recognized the revenue (sales book of INR 0.83 crores in AY 2017-18; INR 71 crores in AY 2019-20; INR 110.12 crores in AY 2020-21; INR 24.97 crores in AY 2022-23). Ld.AR submits that in respect of AYs 2017-18, 2018-19 & 2022-23, the assessments were completed u/s 143(3) and income declared has been accepted.

14. Ld.AR submits that as a principal of consistency, no addition could be made when in preceding years, income declared by the assessee has been accepted and assessee has consistently and regularly adopted the method of accounting for recognizing its revenue.

15. In this regard, reliance is placed on the judgement of Hon’ble Supreme Court in the case of

CIT v.

Excel Industries Ltd. [2013] (SC).

16. With regard to the arguments that consistently adopted method of accounting cannot be discarded and for this, reliance is placed on the following judgements:-

| (i) |

|

United Commercial Bank v. CIT 240 ITR 355 (SC) |

| (ii) |

|

Investment Ltd. v. CIT 77 ITR 533 (SC) |

| (iii) |

|

Pr. CIT v. Indrapuram Habitat Centre (P.) Ltd. [IT Appeal No. 476 (Del) of 2017, dated 6-11-2017] |

| (iv) |

|

CIT. – 15 v. Aditya Builders [2015] 378 ITR 75 (Bombay)/ITA No. 1738 of 2013 dated 14.09.2015 (Bom) |

| (v) |

|

CIT (Central), Gurgaon v. Principal Officer, Hill View Infrastructure (P.) Ltd. [2016] 384 ITR 451 (Punjab & Haryana) |

| (vi) |

|

Manjusha Estates (P.) Ltd. v. ITO 393 ITR 644 (Gujarat) |

| (vii) |

|

CIT -V v. Umang Hiralal Thakkar (Gujarat)/ITA No. 1000 of 2013 dated 18.11.2013 (Gujarat) |

16.1. Ld.AR therefore, requested that the deletion of addition so made.

17. On the other hand, Ld. CIT DR for the Revenue supported the orders of lower authorities and submits that Ld. CIT(A) in para 7.3 of the order has discussed this issue in detail wherein Ld. CIT(A) has concluded that assessee has not prepared its books of account by following the method mandated under AS 7 and ICDS III and section 43B of the Act. Ld. CIT DR thus, submits that the order of ld. CIT(A) be uphold. Regarding assessee’s claim that income was declared in subsequent years, ld. CIT DR drew our attention to the observations of ld. CIT(A) at page 72 of the order wherein it is observed as under:-

“The appellant’s argument that future recognition would lead to double taxation is misconceived. If proper revenue was not recognized in earlier years, and profit was added by the AO, the appellant can claim appropriate exclusion in the later year under the principles of tax neutrality and matching. Deferral of income recognition cannot be allowed simply on the ground that it would be recognized in future years. Tax is imposed on real income arising during the relevant previous year, and not based on when the appellant chooses to invoice it.”

17.1. She prayed accordingly.

18. Heard the contentions of both the parties and perused the material available on record. It is observed that the assessee has regularly maintained its books of accounts and recognizing the revenue from construction activity whenever the work was recognized by the principal. This method of accounting was accepted by the Revenue in preceding AYs where the receipts from one project namely, “Sky Forest”, revenue of more than INR 350 crores have been accepted in various previous assessment years and revenue of INR 84.17 crores is accepted in subsequent years.

19. Since during the year under appeal, the assessee has declared sales of only INR 3.34 Lakhs, the AO alleged that that major revenue was not booked during the year. It is further observed that in subsequent year out of the work-in-progress of INR 2.95 crores, the assessee has recognized revenue of INR 84.17 crores. Likewise in respect of the other project, during the year, revenue of INR 40.81 Lakhs was recognized as against which revenue of INR 24.97 crores was recognized in subsequent AY. It is further observed in preceding Assessment years, assessee has recognized revenue from both the projects, which was accepted by the Department. Once the results declared in preceding assessment years were accepted by the revenue and method of accounting regularly and consistently followed by the assessee, was never doubted, in the year under appeal, the same cannot be disturbed by changing the method of recognizing the revenue from “Project Completion method” to “Percentage of completion method”, more particularly when the same method of recognizing the revenue was not doubted in subsequent years. The Hon’ble Supreme Court in the case of CIT v. Excel Industries Ltd. (supra) has held that principal of consistency should be maintained. Once the Revenue has accepted the turnover, declared in the preceding year as well as in subsequent year, doubting the same in the year under appeal without even invoking the provisions of section 145(3) of the Act, no income could be estimated.

20. In view of these facts, the additions made is hereby, deleted. All the Grounds of appeal raised by the assessee are allowed.

21. In the result, appeal of the assessee is allowed.

ITA No.8463/Del/2025 [Assessment Year 2021-22]

Revenue’s appeal

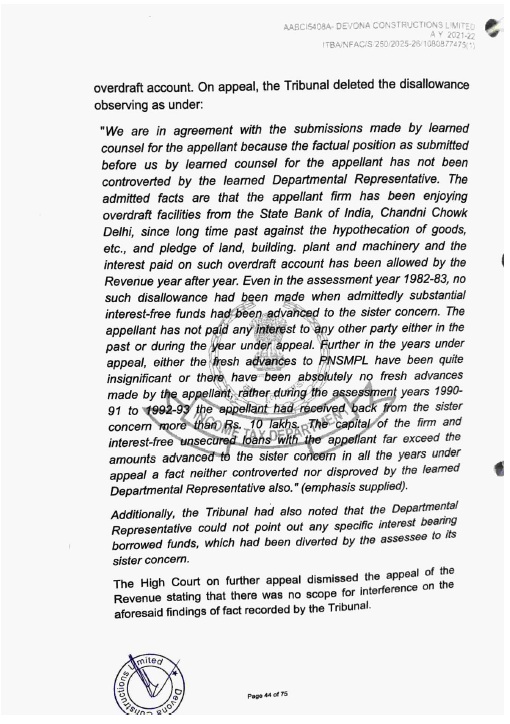

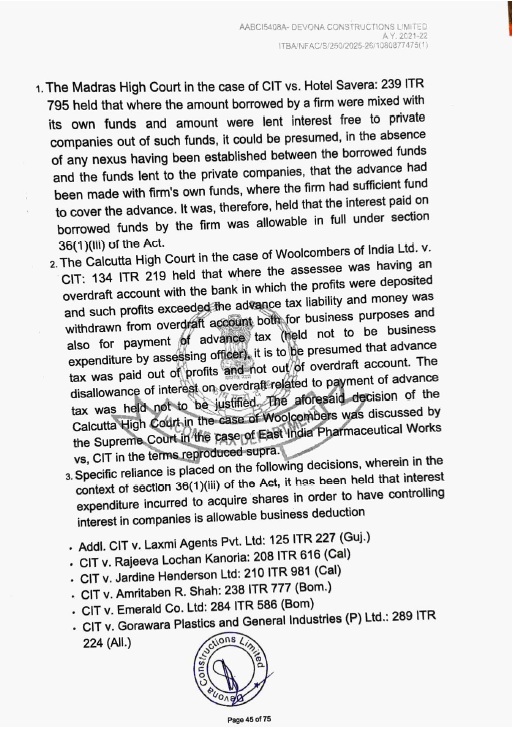

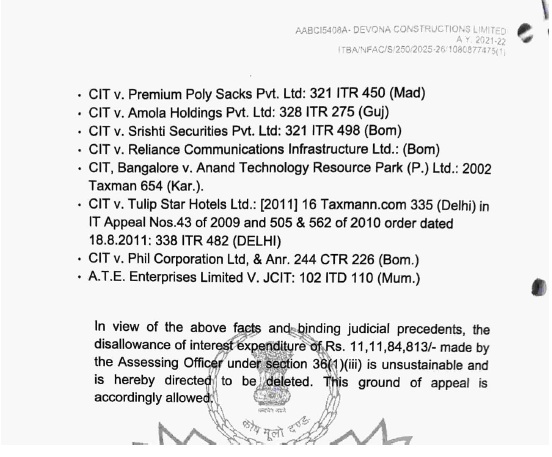

22. Ground of appeal No.1 raised by the Revenue is with respect to the deletion of the disallowance of INR 11,11,84,813/- made u/s 36(1)(iii) of the Act on account of interest free loans given to the various parties.

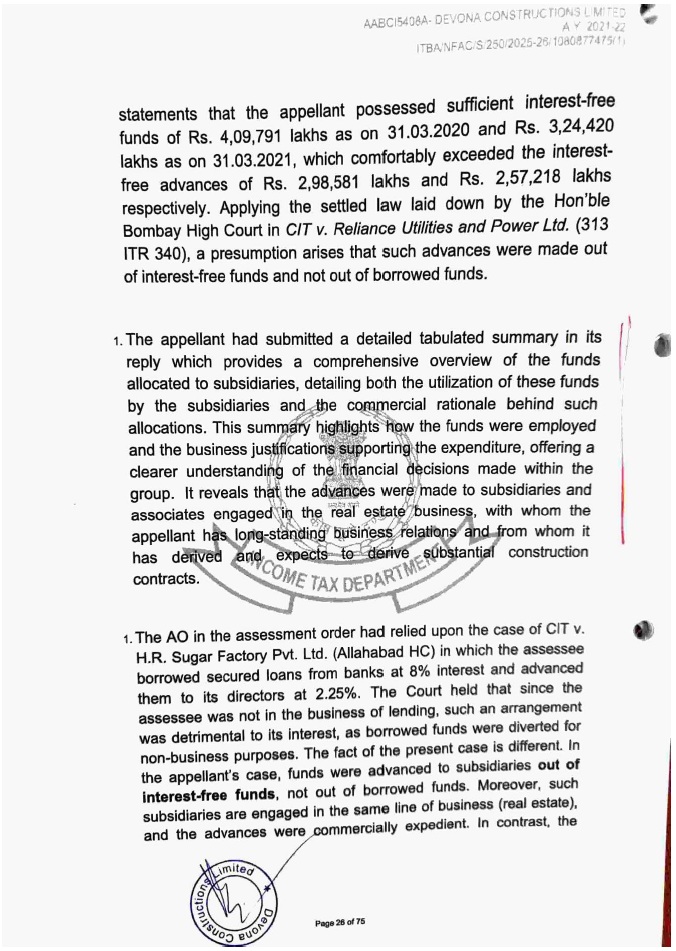

23. Before us, Ld. CIT DR submits that the assessee has failed to prove the commercial expediency and further has failed to prove the nexus of interest free loans taken and interest free advances made to sister concerns. Ld. CIT DR submits that AO has examined this issue in detail and had made the disallowance. Ld. CIT DR submits that assessee has claimed expenses of INR 1126.18 Lakhs on the loans taken in Profit & Loss Account as against which assessee has given interest free funds to the group companies of INR 2,57,218.85 Lakhs. The AO observed that assessee has failed to establish that the interest free funds were utilized for giving interest free advances and therefore the proportionate amount of interest was disallowed and requested for the confirmation of the same.

24. On the other hand, Ld.AR for the assessee heavily placed reliance on the order of Ld. CIT(A) and submits that the assessee has sufficient interest free funds available in the shape of share capital and interest free loans and advances from the parties out of which interest free funds were given to related parties. Ld.AR submits that as on 31.03.2020, total interest free funds were of INR 4,09,791.76 Lakhs as against which the advances were to the sister concern of IRN 2,98,581.22 Lakhs likewise as on 31.03.2021, total interest free funds were available with the assessee were INR 3,24,420.27 Lakhs as against interest free advances were INR 2,57,218.85 Lakhs. Ld.AR submits that from the above, it is clear that the assessee is having sufficient interest free funds out of which the funds were given to the sister concerns. Ld.AR submits that where the mixed funds were available and assessee has given interest free funds, no disallowance could be made towards interest free advances made. In this regard, reliance is placed on the judgement of Hon’ble Supreme Court in the case of CIT v. Reliance Industries Ltd (SC) confirming the order of Hon’ble Delhi High Court in the case of CIT, New Delhi v. Bharti Televenture Ltd. (Delhi). He further placed reliance on various judgments and prayed for the confirmation of the order of Ld. CIT(A) deleting the disallowances made.

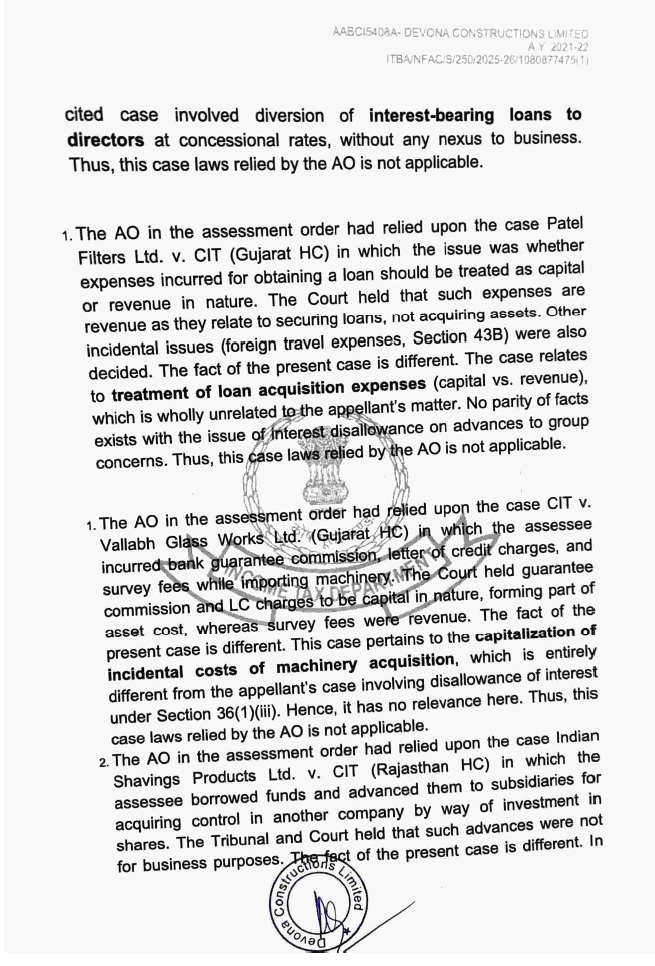

25. Heard the contentions of both the parties and perused the material available on record. Ld. CIT(A) has discussed this issue at length and in para 4.2 of the order, has relied upon the judgment of Hon’ble Supreme Court in the case of

S.A. Builders Ltd. v.

CIT (Appeals), Chandigarh 2007 288 ITR 1 (SC), Hon’ble

Delhi High Court in the case of

CIT v.

Dalmia Cement (P.) Ltd. [2002] 121 254 ITR 377 (

Delhi); Hon’ble Supreme Court in the case of

Hero Cycles (P.) Ltd. v.

CIT (Central), Ludhiana [2015] (SC) and certain other judgements of Hon’ble Supreme Court and Hon’ble

Delhi High Court as well as Hon’ble Bombay High Court and reached to the conclusion that the assessee has sufficient interest free funds available thus no disallowance could be made u/s 36(1)(

iii) of the Act. The relevant observations of Ld. CIT(A) as contained in para 4.2 of the order are as under:-

26. It is further observed that assessee has made advances to the sister concern in preceding assessment years and had claimed interest on borrowed funds as expenses which were never doubted in the assessment completed u/s 143(3) thus, as a principal of consistency also, under identical circumstances where assessee was having sufficient interest free funds, no disallowance could be made u/s 36(1)(iii) of the Act. We thus find no infirmity in the order of ld. CIT(A) which is hereby upheld. The Ground of appeal No.1 raised by the Revenue is dismissed.

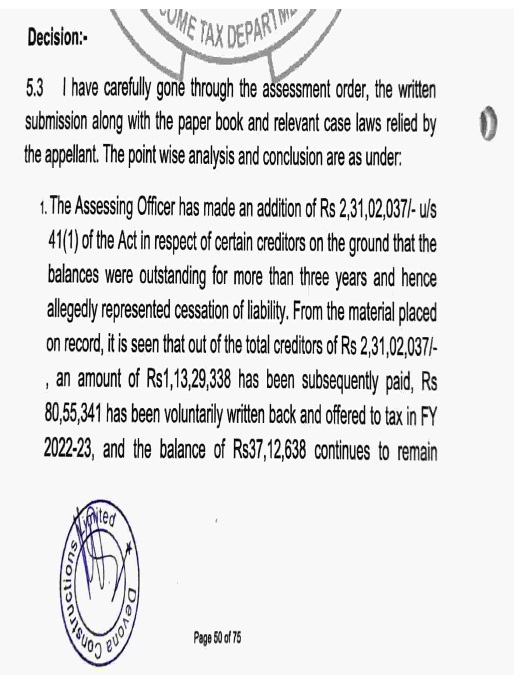

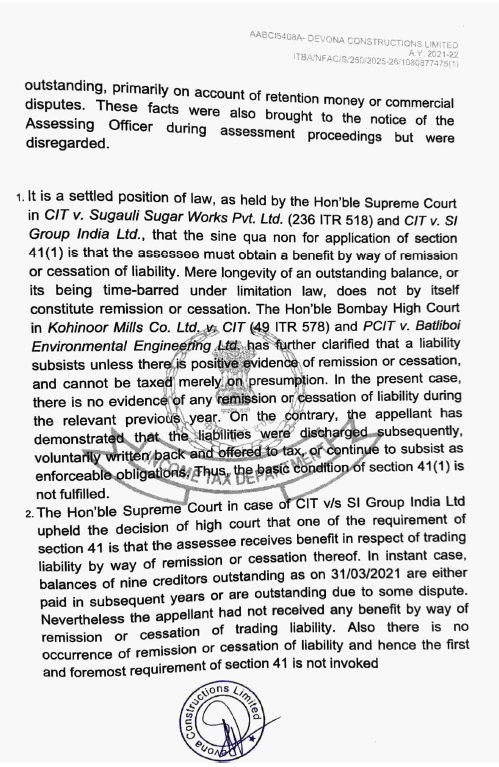

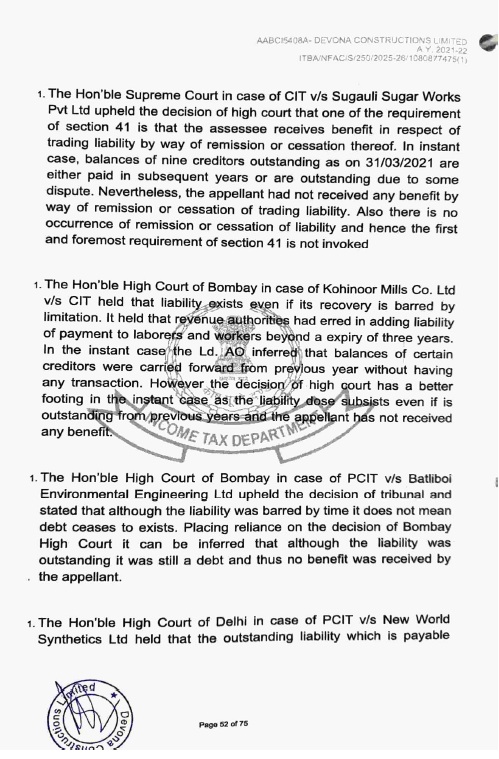

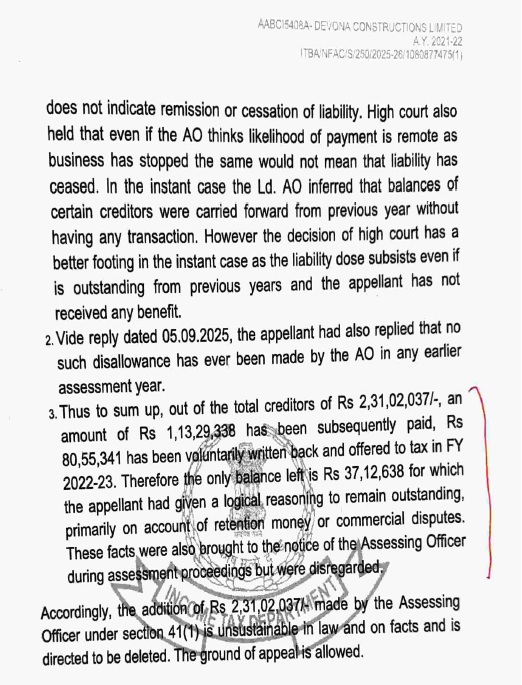

27. Ground of appeal No.2 raised by the Revenue is with respect to the deletion of addition of INR 2,31,02,037/- made by alleging the cessation of liability.

28. Ld. CIT DR for the Revenue vehemently supported the orders of the AO and submits that ld. CIT(A) has failed to appreciate the facts that said sum were added by the AO as there was no activity in these accounts during the year and assessee has failed to give the details of the transactions carried out with these parties during the year under appeal. Since no amount is claimed to be outstanding during the year under appeal, therefore, the AO has made the addition of the same which deserves to be upheld.

29. On the other hand, Ld.AR supports the order of Ld. CIT(A) and submits that Ld. CIT(A) at page 46 to 47 of the impugned order has given a table which was also filed before the AO, stating the nature of transactions with each party and further submits that during the year under appeal, transactions were carried out with all the parties. Ld.AR submits that Ld. CIT(A) has rightly deleted the additions which deserves to be confirmed.

30. In this regard, para 29 of the written submissions, the assessee has filed a chart explaining the transactions with these parties during the year which is reproduced in para 29 at page 32 as under:-

31. Heard the contentions of both the parties at length and perused the material available on record. It is observed that out of the total sum of INR 2,31,02,037/- outstanding as on 31.03.2021, assessee has already paid INR 1,13,29,338/- and INR 80,55,341/- were already recognized as revenue in subsequent AYs i.e. in AY 2023-24 and the balance of INR 37,12,638/- were outstanding which represents the retention of money or disputed amounts. Therefore, it cannot be said that entire outstanding balance of INR 2,31,02,037/-is the liability which is seized during the year. Ld. CIT(A) appreciated these facts and deleted the addition by observing in para 5.3 as under:-

32. Before us, revenue has failed to controvert the findings of Ld. CIT(A) which were given after considering the factual aspects and nature of outstanding balances and further considering the fact that majority of amount was either repaid or already offered for tax. Therefore, we find no error in the order of Ld. CIT(A) which is hereby, upheld. Ground of appeal No.2 of the Assessee is thus allowed.

33. Ground of appeal No.3 raised by the Revenue is regarding disallowance of provision for expenses relating to preceding year of INR 50,37,723/-.

34. Heard the contentions of both the parties and perused the material available on record. Ld. CIT(A) while deleting the disallowance, observed that the assessee has already disallowed the said provision in preceding Year and thus disallowing the same in the year under appeal tantamount to double addition. This fact has been ignored by AO while making the disallowance. Once the assessee has been able to satisfy the ld. CIT(A) that these provisions have already been added to the total income and due taxes has been paid in preceding assessment year when the same were charged to P&L A/c, there is no reason for the AO for making disallowance of the same again more particularly, when the amount of provisions were not debited to Profit & Loss Account in the year under.

35. In view of these facts, we find no error in the order of Ld. CIT(A) in deleting the disallowance made by the AO which order is hereby upheld. Accordingly, Ground of appeal No.3 raised by the Revenue is dismissed.

36. In the result, appeal of the Revenue is dismissed.

37. In the final result, appeal of the assessee in ITA No.6597/Del/2025 [Assessment Year 2021-22] is allowed and appeal of the Revenue in ITA No.8463/Del/2024[Assessment Year 2021-22] is dismissed.