ORDER

Renu Jauhri, Accountant Member.- This appeal by the assessee is against the final assessment order dated 24.01.2025 passed by the ACIT, Circle Int. Tax- 1(1)(2), New Delhi, (hereinafter referred to as the ‘ld. AO’) under Section 147 read with Section 144 of the Incometax Act, 1961 (“the Act”), pursuant to the directions of the Hon’ble Dispute Resolution Panel-2, New Delhi (DRP) order dated 12.12.2024 for the Assessment Year 2015-16.

2. Grounds of appeal filed by the Assessee are reproduced as under:

“GROUND OF APPEAL NO. 1 The expenditure incurred on improvements to the Flat No. 140, Mall Road, Delhi in the Financial Years 1986-87 and 1994-95 of Rs. 5,17,041/-and Rs. 5,44,565/- respectively as estimated by an Approved and Registered Valuer of the Income Tax Department as per CPWD rates which have NOT been allowed as a cost of improvement of the respective years without appreciating the facts.

GROUND OF APPEAL NO. 2 Leave to amend or add grounds – The Appellant craves leave to add, alter, amend, vary the aforementioned grounds of appeal at or before the time of hearing of the said appeal, if necessary.”

3. The only ground of appeal in this case pertains to computation of the cost of acquisition to be taken while computing capital gain on sale of immovable property.

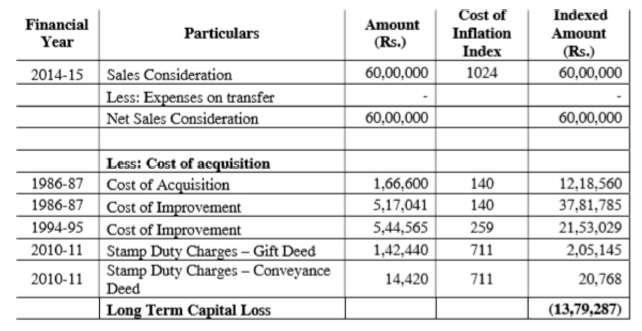

3.1 Brief facts are that the assessee, an NRI, sold a property for a consideration of Rs. 60,00,000/-. Since this amount was not disclosed by the assessee, proceedings u/s 147 were initiated and a notice u/s 148 was issued on 1.4.2022. In response, it was explained by the assessee, that the impugned property, was originally allotted to his uncle in F.Y. 1986-87 by the Delhi Development Authority (DDA) for Rs. 1,66,600/-. Subsequently, it was gifted to the assessee by his uncle on 18.03.2011. Since major renovations had been undertaken by the uncle of the assessee in 198687 as well as 1994-95, a valuation report dated 01.11.2014 of the Registered Valuer was obtained which determined the cost of improvement undertaken in 1986-87 at Rs. 5,17,041 and in 1994-95 as Rs. 5,44,565/-. Based on these, following computation of capital loss was submitted by the assessee to the AO:

3.2 In the absence of any documentary evidences to support the cost of improvement undertaken by the previous owner, the AO adopted the cost of acquisition at Rs. 166600/- and computed capital gain at Rs. 4,78,81,440/-. Vide the draft assessment order proposing to add Capital Gain of Rs. 4,78,14,440/-. Against the draft assessment order, the assessee filed objections before the DRP.

3.3 Ld. DRP, after observing that the cost of improvement of Rs. 5,17,041/-claimed in A.Y. 1986-87 and Rs. 5,44,565/- in F.Y. 1994-95 were exorbitant considering the cost of acquisition of Rs. 1,66,600/- in F.Y. 1986-87 and that the assessee did not produce any documentary evidence, whatsoever, in support of these improvements, rejected the objections of the assessee. Assessment was accordingly finalized vide order u/s 147 r.w.s. 144 of the Act dated 24.01.2025 at total income of Rs. 48,83,130/- after making addition of Rs. 45,55,527/- on account of capital gains. Aggrieved, the assessee has filed an appeal before the Tribunal.

4. Before us, the Ld. AR has argued that the DDA had allotted a basic structure in 1986-87 on which the uncle of the assessee had made substantial improvement in F.Y. 1986-87 as well as in 1994-95. Since, the flat was transferred to the assessee in 2011 by way of gift and was eventually sold in 2014, the requisite documentary evidences regarding cost of improvement were not available due to considerable lapse of time. Hence, based on the details provided by the assessee, the registered value computed the cost of improvement as per the prescribed rates prevalent in the corresponding years. It has further been submitted that if the AO was not satisfied with the registered valuer’s report, he should have made a reference to the Departmental Valuation Officer (DVO), which was not done. Ld. AR has further placed reliance on the decision of the coordinate bench in the case of Ms. Lalita Trehan v. Dy. CIT (IT) [IT Appeal No. 3352 (Del) of 2023, dated 23.10.2024] in support of his contention that the AO is bound to accept the report of registered valuer if reference to DVO has not been made u/s 55A of the Act.

4.1 On the other hand, the Ld. DR has submitted that the Valuation Report was made in 2014 and it does not specify as to how the value of construction / improvement undertaken in F.Y. 1986-87 and 1994-95 has been determined by the valuer. In the absence of any supporting documentary evidence regarding incurring of these expenses as well as any credible basis of estimation of historical cost by he valuer, the valuation report has rightly been rejected by the AO & DRP.

4.2 Detailed written submissions made by both the parties have been taken on record.

5. We have heard the rival submissions and perused the material available on record. The only issue for consideration is regarding computation of cost of improvement undertaken in F.Y. 1986-87 & 1994-95. Admittedly, the assessee had received the property as gift from his uncle in March, 2011. The property was sold in 2014 and before selling he got the valuation done from a registered valuer with regard to the cost of acquisition /improvement. Under Section 55A of the Act, the AO is empowered to make a reference to the DVO in case he is not satisfied with the report of the registered valuer. The relevant provisions of section are reproduced as under:

“Reference to Valuation Officer.

55A. With a view to ascertaining the fair market value of a capital asset for the purposes of this Chapter, the Assessing Officer may refer the valuation of capital asset to a Valuation Officer—

(a) in a case where the value of the asset as claimed by the assessee is in accordance with the estimate made by a registered valuer, if the Assessing Officer is of opinion that the value so claimed is at variance with its fair market value;

(b) in any other case, if the Assessing Officer is of opinion—

(i) that the fair market value of the asset exceeds the value of the asset as claimed by the assessee by more than such percentage of the value of the asset as so claimed or by more than such amount as may be prescribed in this behalf ; or

(ii) that having regard to the nature of the asset and other relevant circumstances, it is necessary so to do,

and where any such reference is made, the provisions of sub-sections (2), (3), (4), (5) and (6) of section 16A, clauses (ha) and (i) of sub-section (1) and sub-sections (3A) and (4) of section 23, sub-section (5) of section 24, section 34AA, section 35 and section 37 of the Wealth-tax Act, 1957 (27 of 1957), shall with the necessary modifications, apply in relation to such reference as they apply in relation to a reference made by the Assessing Officer under sub-section (1) of section 16A of that Act.

Explanation.—In this section, “Valuation Officer” has the same meaning, as in clause (r) of section 2 of the Wealth-tax Act, 1957 (27 of 1957).”

5.1 In this case, the estimate by registered value was rejected by the AO on the ground that the same appeared exorbitant and was not supported by any documentary evidence or credible basis of computation. However, in that case the AO should have made a reference to the DVO u/s 55A of the Act instead of rejecting the registered valuer’s report. We are of the considered view that the AO erred in simply rejecting the cost of improvement claimed on the basis of registered valuer’s report and computing the capital gain by adopting the cost of acquisition at Rs. 1,66,600/- (being the cost of purchase from DDA). Since he did not accept the assessee’s contention regarding substantial improvement undertaken subsequent to the purchase from DDA, he ought to have made a reference to the DVO as required u/s 55A of the Act. We further note that this issue has been decided in assessee’s favour in several decisions of the coordinate benches. Specifically in the case of Lalita Trehan (supra) under similar facts and circumstances, the coordinate bench has held as under:

“13….. Similarly, in the present case also, the AO disputed the valuation of the land as on 01.04.2001 and the cost of construction/improvement and land development charges incurred by the assessee in FY 2003-04 but did not refer the matter to the Valuation Officer for its valuation. Similarly, the Id. DRP also did not conduct any enquiry as provided u/s 144(7)(a) of the Act or directed the AO u/s 144(7)(b) of the Act to refer the matter to the Valuation Officer for valuation of the property sold during the year in which the quantum of capital gains on account of valuation of the land has been disputed. Therefore, respectfully following the aforesaid order of the Coordinate Bench of the Tribunal, we hold that the Assessing Officer was not right in discarding the report of the registered valuer regarding the determination of the fair market value of the land as on 01.04.2001 without making a reference to the DVO and, therefore, the rate adopted by the Assessing Officer for the purpose of computation of capital gains in the final assessment order cannot be upheld. Accordingly, we set aside the order of the AO and direct the Assessing Officer to re-compute the fair market value of the land as on 01.04.2001 at Rs.7,250/- per sq. yard as adopted by the registered valuer and allow indexation accordingly. Similarly, the cost of construction (Rs.91,09,820/-) and land development charges (Rs.21,31,493/-) incurred during FY 2003-04 was also valued by the registered valuer and being an integral part of the capital asset and which was again disputed by the AO but not referred to the Valuation Officer by the AO and therefore considering the same reasoning in the cited case of the Co-ordinate Bench of the Tribunal, the AO is directed to adopt the cost of construction (Rs.91,09,820/-) and land development charges (Rs.21,31,493/-) incurred during FY 2003-04 as adopted by the registered valuer and allow indexation accordingly.”

5.2 In view of the facts and circumstances of the case, the relevant provision of the Act and the decision of the coordinate bench in the case of Ms. Lalita Trehan (supra), we hold that the AO was not justified in rejecting the registered valuer’s report and taking the cost of improvement as Nil, without making a reference to the DVO. Under these circumstances, we direct the AO to allow the claim of the assessee regarding cost of improvement as per the registered valuer’s report and recompute the capital gains accordingly.

6. In the result, appeal of the assessee is allowed.