ORDER

1. In these writ petitions, the petitioner has challenged the respective impugned Orders-in-Original as detailed below:

| S.No. |

Writ Petition No. |

Date of impugned Order-in-Original |

Date of Show Cause Notice |

Assessment Year |

| 1. |

18697 of 2025 |

26.12.2024 |

16.05.2024 |

2017-18 to 2021-22 |

| 2. |

18541 of 2025 |

04.02.2025 |

27.05.2024 |

2017-18 to 2022-23 |

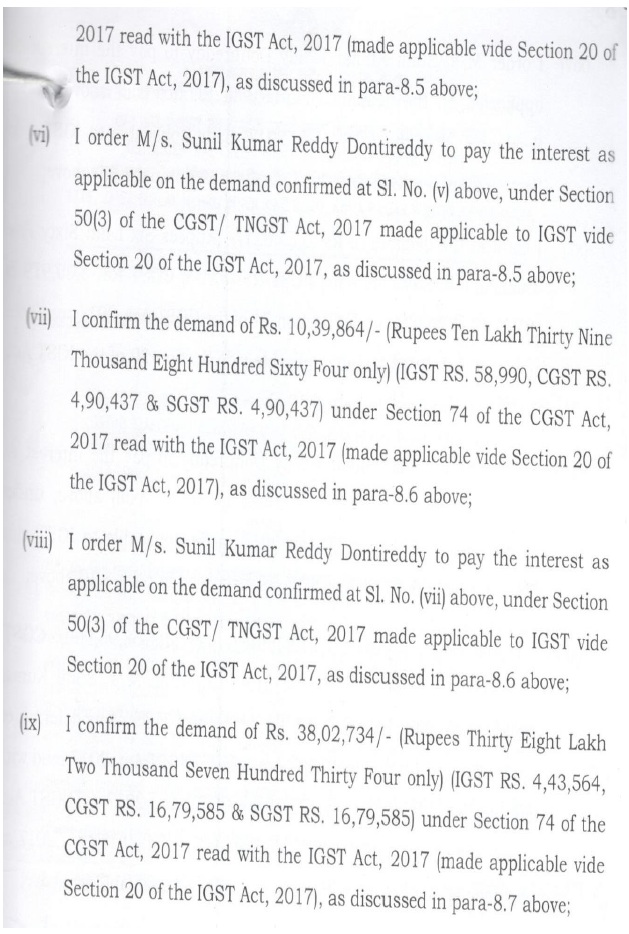

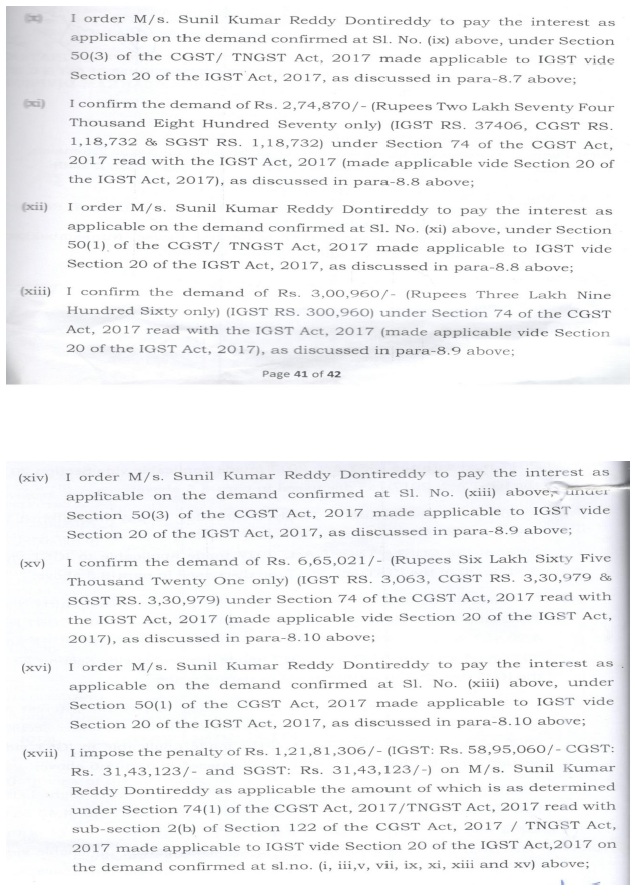

2. The demand confirmed in the respective impugned Orders-in- Original reads as follows:

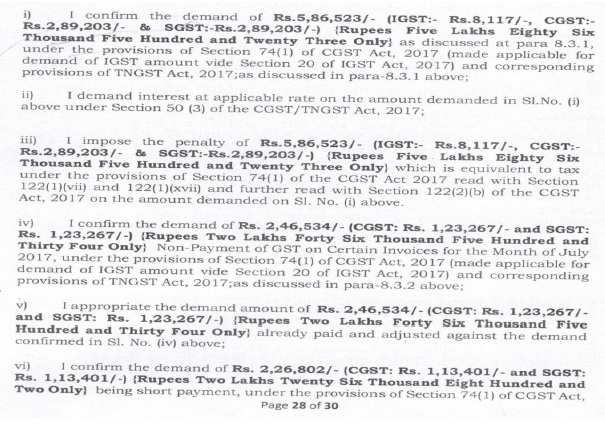

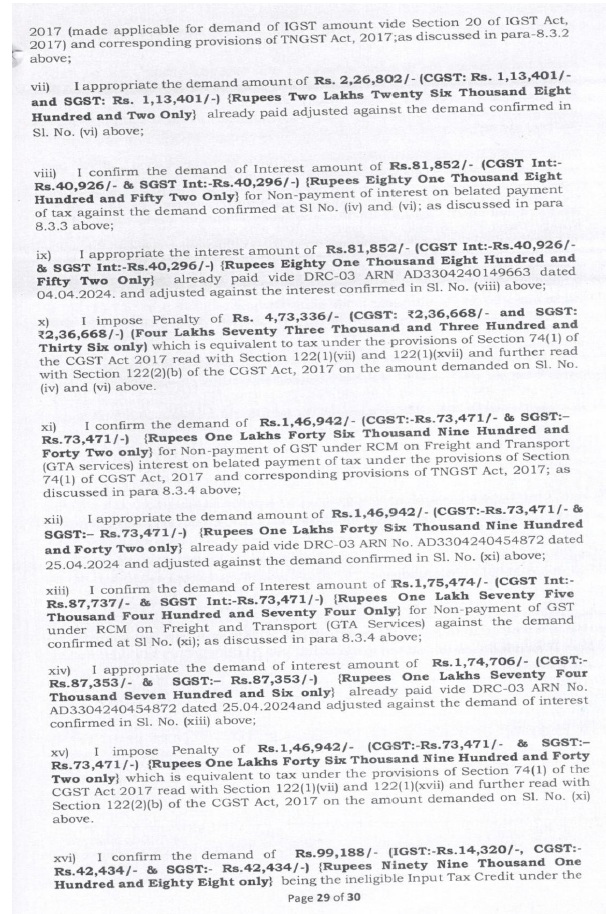

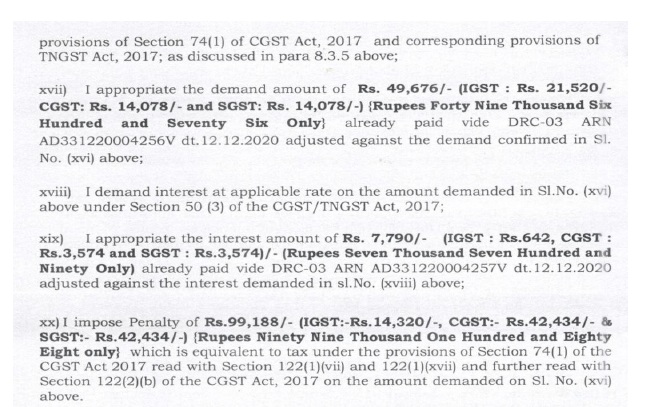

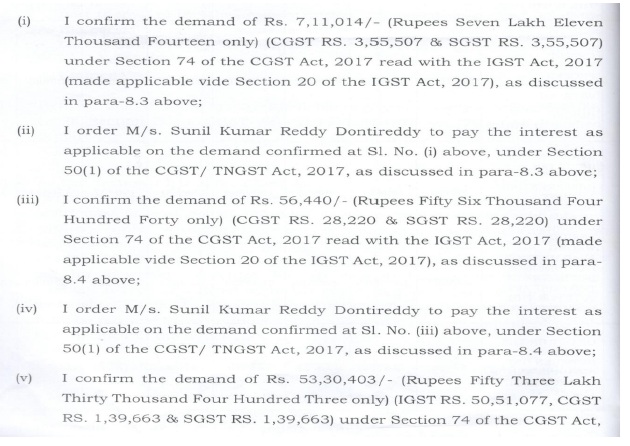

impugned Order-in-Original No. 04/2025-GST-(Supdt-R-II)

Impugned Order-in-Original No. 79/2024-GST

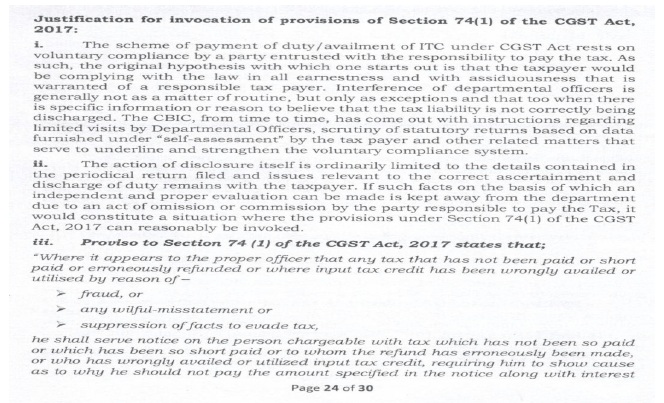

3. The respective impugned orders were preceded with a notice under Section 74 of the respective GST enactments.

4. A reading of the impugned order indicates that an audit was conducted under Section 65 of the respective GST enactments, and based on the discrepancies found in the audit, proceedings were initiated against the petitioner under Section 74.

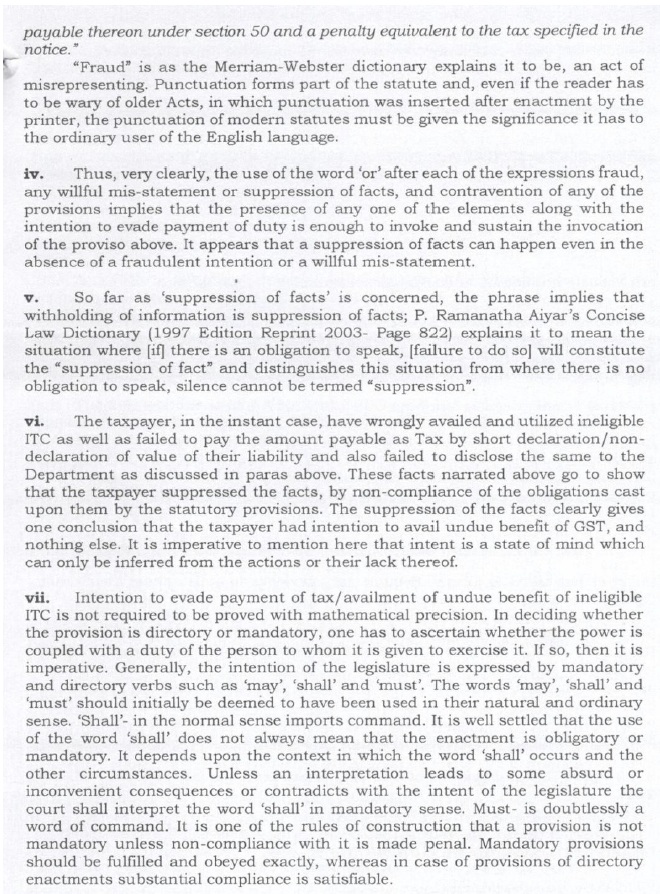

5. The case of the petitioner is that mere wrong availment of input tax credit or a mere failure to pay tax in time does not vest the department with the power under Section 74 of the respective GST enactments.

6. The learned counsel for the petitioner has drawn attention to the Board Instruction No.05/2023-GST dated 13.12.2023 from File.No.CBIC-20004/3/2023-GST. In this connection, reference was made to paragraph 3.3, which reads as under:

“3.3 From the perusal of wording of section 74(1) of CGST Act, it is evident that section 74(1) can be invoked only in cases where there is a fraud or wilful mis-statement or suppression of facts to evade tax on the part of the said taxpayer. Section 74(1) cannot be invoked merely on account of non-payment of GST, without specific element of fraud or wilful mis-statement or suppression of facts to evade tax. Therefore, only in the cases where the investigation indicates that there is material evidence of fraud or wilful mis-statement or suppression of fact to evade tax on the part of the taxpayer, provisions of section 74(1) of CGST Act may be invoked for issuance of show cause notice, and such evidence should also be made a part of the show cause notice.”

7. It is submitted by the learned counsel for the petitioner that the petitioner is a proprietary concern. It is submitted that no statements were recorded from the petitioner’s proprietor to conclude that the petitioner had indulged in fraud, wilful misstatement or suppression of facts to evade tax and to thereby justify the confirmation of demand.

8. It is further submitted by the learned counsel for the petitioner that, 5 defects were pointed out in the show cause notice, out of which, demand in respect of the 3 defects were dropped and that the petitioner also paid the tax due thereon. In this connection, a reference was also made to the decision of the Hon’ble Supreme Court in Uniworth Textiles Ltd. v. CCE (SC)/2013 (288) E.L.T. 161 (S.C.).

9. That apart, the learned counsel for the petitioner would submit that even otherwise, there is no scope for bunching of proceedings for different assessment years. In this connection, reference was made to the decision of this Court in Titan Company Ltd v. Joint Commissioner of GST & Central Excise (Madras).

10. The Learned Senior Standing Counsel for the respondent, on the other hand, would submit that the attempt of the parliament has been to simplify the procedure and that therefore, the department has withdrawn the control on the assessees and that GST Regime proceeds on the basis of trust.

11. It is further submitted by the Learned Senior Standing Counsel that assessees/registered persons are required to declare the property tax in their returns, and that the department relies on these declarations for completing assessments, and further that if the department finds that an assessee is not declaring the correct supply or has wrongly availed input tax credit, the machinery under Sections 73 and 74 of the Act can be invoked, depending upon the facts of each case.

12. The Learned Senior Standing Counsel for the respondent drew the attention from few procedures to indicate that the petitioner has availed ineligible credit as either tax was paid by the supplier nor returns were filed by the supplier. However, the petitioner has availed input tax credit in the returns filed in GSTR3B utilized the same for discharging the tax liability.

13. I have heard the learned counsel for the petitioner and the learned Senior Standing Counsel for the respondent.

14. Insofar as the challenge to the impugned Orders-in-Original (dated 04.02.2025 and 26.12.2024 in W.P.Nos.18541 & 18697 of 2025) is concerned, the officer has given a clear finding as to why the provisions of Section 74 were invoked in the show cause notices that preceded the respective impugned orders.

15. The reasons for justifying the extended period of limitation in the respective impugned orders read as under.

16. A detailed order has been passed in a batch today by a separate order, after considering the submissions of the petitioner on the larger question of law relating to the invocation of the extended period of limitation in W.P.Nos.35967, 35970, 35974 and 35976 of 2024 etc. , batch. The reasons stated therein are squarely applicable to the facts of this case.

17. Therefore, the challenge to the impugned proceedings on the ground that Section 74 was wrongly invoked, cannot be countenanced. In fact, the show cause notices also specified reasons for invoking the extended period of limitation.

18. As far as the bunching of the demand for multiple tax periods is concerned, as mentioned earlier, the issue now stands covered against the petitioner in terms of the decision of the Karnataka High Court in Chimney Hills Education Society v. Additional Commissioner of Central Tax (Karnataka)/2024 SCC OnLine Kar 21844.

19. Therefore, these writ petitions are liable to be dismissed, and accordingly, they are dismissed. However, liberty is given to the petitioner to file an appeal before the Appellate Authority, within a period of 30 days from the date of receipt of a copy of this order, if the petitioner desires so. No costs. Connected miscellaneous petitions are closed.