ORDER

Sachin Datta, J.- The present petition has been filed by the petitioner alleging wilful disobedience/ non-compliance of the directions contained in the order dated 10.02.2025 passed in Truth Fashion v. Commissioner of DGST Delhi (Delhi)/W.P(C) 486/2025. The said order reads as under:-

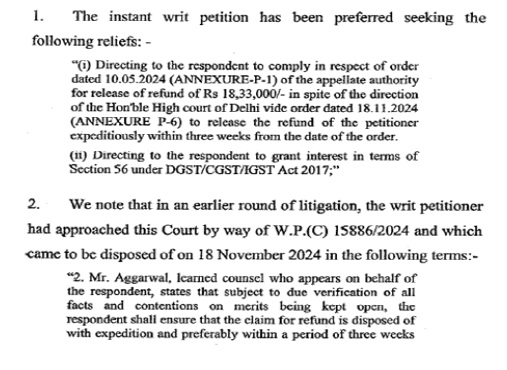

2. The background of the matter is that an appeal came to be filed by the petitioner before the Objection Hearing Authority/GST Additional Commissioner, Department of Trade and Taxes, Government of NCT of Delhi against a Refund Rejection Order dated 05.02.2024 passed by the Proper Officer/Assistant Commissioner, Department of Trade & Taxes, Government of NCT of Delhi in GST RFD 06. Vide an order dated 10.02.2025, the said appeal preferred by the petitioner came to be allowed by the Objection Hearing Authority and the aforementioned order dated 05.02.2024 was set aside. The operative directions contained in the order dated 10.05.2024 are as under:

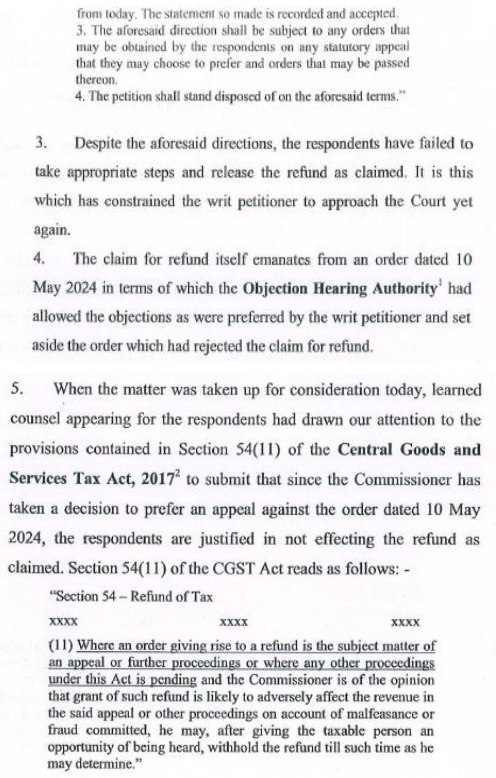

“8. Upon a careful perusal of above deliberations and the facts of the case alongwith other available records and provisions thereof, I am of the considered view that the impugned rejection orders passed by the proper officer appears to be not justified and not tenable in accordance with the provisions of the CGST/DGST and rules made therein under. Accordingly, the appeal preferred by the Appellant is allowed and hence the impugned Rejection orders of refund dated 05.02.2024 for the period April 2022 to March 2023 is hereby set aside in the aforesaid terms. This is in accordance with the prescribed procedure under the GST Act and Rules.”

3. Subsequently, the petitioner filed W.P(C)15886/2024 before this Court on account of the failure of the respondent to process the refund application of the petitioner submitted in consequence to the order dated 10.05.2024 passed by the Objection Hearing Authority. Vide order dated 18.11.2024, this Court in W.P(C)15886/2024 directed as under: –

“1. The solitary grievance of the writ petitioner is a failure on the part of the respondents to process the refund application of the petitioner submitted in consequence to the order dated 10th May 2024 passed by the Objection Hearing Authority, the Additional Commissioner.

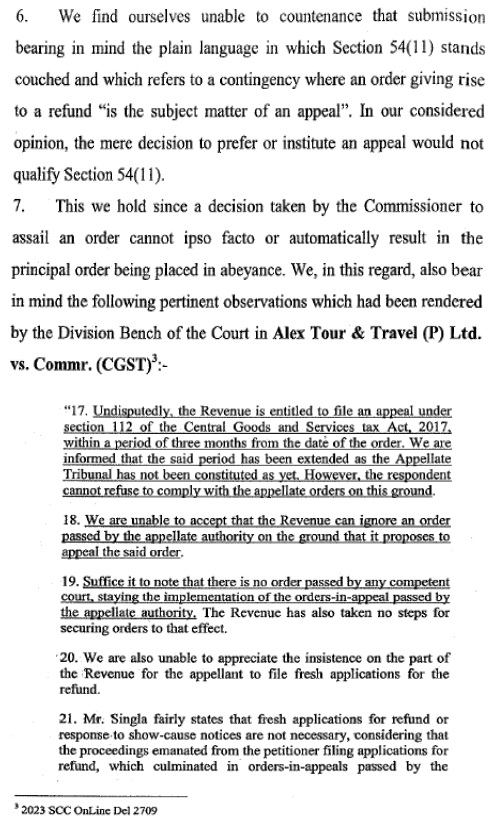

2. Mr. Aggarwal, leamed counsel who appears on behalf of the respondent, states that subject to due verification of all facts and contentions on merits being kept open, the respondent shall ensure that the claim for refund is disposed of with expedition and preferably within a period of three weeks from today. The statement so made is recorded and accepted.

3. The aforesaid direction shall be subject to any orders that may be obtained by the respondents on any statutory appeal that they may choose to prefer and orders that may be passed thereon.

4. The petition shall stand disposed of on the aforesaid terms.”

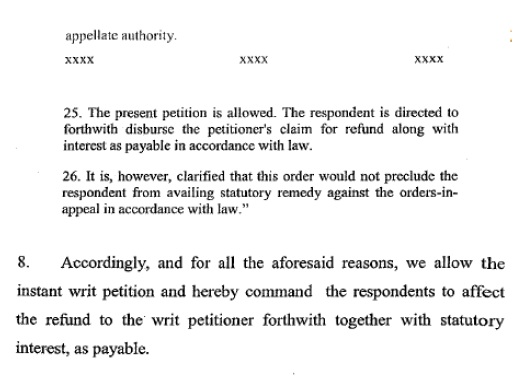

4. However, since the respondents failed to comply with the aforementioned orders, the petitioner filed W.P.(C) 486/2025 seeking to direct the respondent to comply with the directions contained in the order dated 10.05.2024 passed by the Objection Hearing Authority and order dated 18.11.2024 passed by this Court. Vide order dated 10.02.2025 passed in W.P(C) 486/2025 (contempt of which has been alleged in the present proceedings), this Court allowed the aforementioned writ petition and directed the respondents to refund the requisite amount to the petitioner along with the statutory interest, as payable.

5. Even after the passing of the aforesaid order, the requisite refund was not given to the petitioner, in view of the fact that an appeal bearing Commissioner of DGST Delhi v. Truth Fashion [W.P.(C) No. 6571 of 2025 & CM APPL. No. 29784 of 2025, dated 5-2-2026]/W.P.(C) No. 6571/2025 was filed by the Commissioner of DGST, Delhi, assailing the aforesaid order dated 10.05.2025 passed by the Objection Hearing Authority. Vide order dated 16.05.2025 passed in Truth Fashion (supra) it was, inter alia, directed as under:

“20. Under these circumstances, instead of processing the refund and granting the same in favour of the Respondent, since the appellate authority’s order is under challenge before this Court, the Department shall deposit the entire amount of refund with the Registrar General of this Court by 15th July, 2025. Upon the said amount being deposited, the same shall be kept in a fixed deposit on an auto renewal mode”

6. Subsequently, the said Truth Fashion (supra) came to be disposed of by this Court vide order dated 05.02.2026, in the following terms:

“1 . Since the Tribunal is being likely to be functional within a period of two weeks as was assured in other collateral proceedings, we dispose of the petition by relegating the petitioner to the remedy of filing an appeal before the Tribunal.

2. Time spent in prosecuting the petition be considered, in case, if the issue of issue of limitation crops up.

3. Needless to clarify, we have not appreciated the merits of the matter.

4. We take note of the fact that the Ms. Urvi Mohan, counsel appearing for the petitioner has stated that the entire liability under order impugned is discharged by depositing the said amount.

5. The present writ petition stands disposed of.”

7. As such, the respondents/DGST Department has been relegated to pursue the appellate proceedings before the concerned Tribunal. Admittedly, no interim order/s has been passed by the concerned Appellate Tribunal preventing release of the refund to the petitioner.

8. Accordingly, the amount lying deposited in this Court pursuant to the directions contained in the order dated 16.05.2025 passed in Truth Fashion (supra) is directed to be released to the petitioner. Needless to say, the same shall necessarily be subject to further orders in the appeal preferred by the respondent/DGST Department before the concerned Appellate Tribunal.

9. Let the aforesaid amount be released to the petitioner upon expiry of three weeks from today.

10. The present petition stands disposed of in the above terms.