ORDER

Anubhav Sharma, Judicial Member. – These are appeals preferred by the assessee against the orders of the Ld. Commissioner of Income-tax (Appeals)-3 (hereinafter referred to as the First Appellate Authority or ‘the ld. FAA’ for short) in appeals filed before him against the orders of the ld. Assessing Officer (hereinafter referred to as the Ld. AO, for short) passed u/s 153A(1)(b) of the Income-tax Act, 1961 (hereafter referred to as ‘the Act’). Further details of the orders of the lower authorities are as under : –

| ITA No. & AY |

Ld. FAA who passed the appellate order |

Appeal No. & Date of order of the Ld. FAA |

AO who passed the assessment order & Date of order |

| 5786/Del/25 2010-11 |

CIT(A)-3, Gurgaon |

Appeal No. 11245/CIT(A)-3/GGN/2016-17 Dated 26.08.2025 |

DCIT, Central Circle-1, Gurgaon Dated 22.03.2016 |

| 5787/Del/25 2011-12 |

CIT(A)-3, Gurgaon |

Appeal No. 11234/CIT(A)-3/GGN/2016-17 Dated 26.08.2025 |

DCIT, Central Circle-1, Gurgaon Dated 22.03.2016 |

| 5788/Del/25 2012-13 |

CIT(A)-3, Gurgaon |

Appeal No. 11237/CIT(A)-3/GGN/2016-17 Dated 26.08.2025 |

DCIT, Central Circle-1, Gurgaon Dated 22.03.2016 |

| 5788/Del/25 2013-14 |

CIT(A)-3, Gurgaon |

Appeal No. 11238/CIT(A)-3/GGN/2016-17 Dated 26.08.2025 |

DCIT, Central Circle-1, Gurgaon Dated 22.03.2016 |

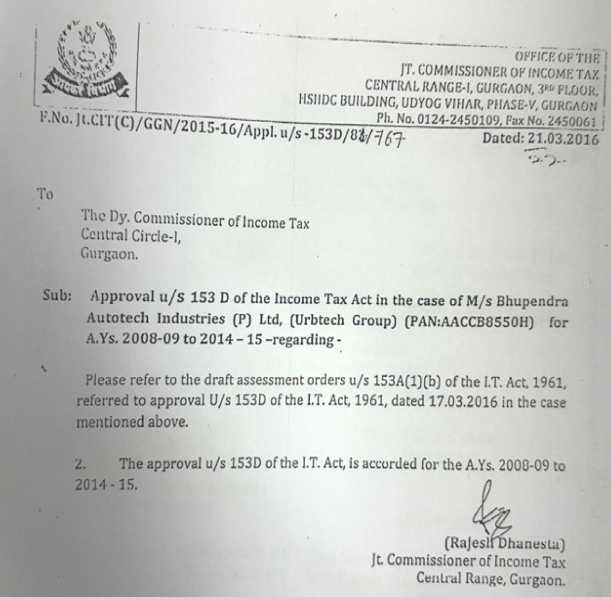

2. At the time of hearing Ld. Counsel has drawn our attention to Ground No. 7 by which assessee has challenged the impugned assessment order on the basis that approval granted u/s 153D of the Act and order passed without application of mind and is not in the eyes of law.

3. As for convenience we reproduced the approval letter:

4. Ld. DR has vehemently opposed the grounds submitting that Section 292BC has been introduced by way of amendment and the same holds that the approval is supervisory and administrative function and any deficiency in the reasons would not vitiated. It was submitted that the provision is applicable retrospectively. It was submitted on behalf of the department that the date referred 01.04.2021 in the amendment brought with the introduction of Section 292BC of the Act has to be read in consonance to the date of hearing of the appeal and when the Tribunal hears this appeal on that day the amendment u/s 292BC should be looked into.

5. Very apparently the approval no way indicates even if the assessment records were perused. Multiple assessment years approval has been granted but even not recording a satisfaction about the issues involved, the material relied and the reasoning so arriving on a conclusion. We find that vide Dy. CIT v. Bhupendra Steels (P.) Ltd. IT Appeal No. 710/Del/2020 for AY: 2011-12 by order dated 20.05.2025 the very same approval has been considered by the Coordinate Bench and found to be in violation of settled judicial principles indicating that the approval is not granted with application of mind. We find no distinguishing feature.

6. The aforesaid, pointed out, facts do not indicate insufficiency of reasons, but mere mechanical manner in which approval is granted. The law in this regard is settled that such mechanical exercise of powers u/s 153D of the Act, vitiates the assessment order. Reliance can be placed on decisions in

ACIT v.

Serajuddin & Co. (Orissa)/[2023 SCC OnLine Ori 992],

Pr. CIT (Central)-2 v.

Anuj Bansal 66 ITR 251 (

Delhi)/[ITA 368/2023]. The Co-ordinate Bench of the Tribunal while examining the similar issue in the case of

SEH Realtors (P.) Ltd. v.

ACIT IT Appeal No. 2503/Del/2017 and connected matters for Assessment Year 2013-14 vide order dated 23/07/2024, considered all the judicial pronouncements on the issue and has held as under: –

“8. We find as per the scheme of the Act, for framing search assessments, the Ld. AO can pass the search assessment order u/s 153A or u/s 153C of the Act only after obtaining prior approval of the draft assessment order and the conclusions reached thereon from the ld. JCIT, in terms of section 153D of the Act. This is a mandatory requirement of law. The said approval granting proceedings by the ld. JCIT is a quasi judicial proceeding requiring application of mind by the ld. JCIT judiciously. In order to ensure smooth implementation of the aforesaid provisions, in consonance with the true spirit of the scheme of the Act, it is the bounden duty of the Ld. AO to seek to place the draft assessment order together with copies of the seized documents before the ld. JCIT well in time much before the due date of completion of search assessment. The ld. JCIT is supposed to examine the seized documents, questionnaires raised by the Ld. AO on the assessee seeking explanation of contents in the seized documents, replies filed by the assessee in response to the questionnaires issued by the Ld. AO and the conclusions drawn by the Ld. AO vis- a-vis the said seized documents after considering the reply of the assessee. All these functions, as stated earlier, are to be performed by the ld. JCIT in a judicious way after due application of mind. Even though as vehemently argued by the Ld. CIT-DR, the ld. JCIT is involved with the search assessment proceedings right from the time of receipt of appraisal report from the Investigation Wing, still, the ld. JCIT, while granting the approval u/s 153D of the Act has to independently apply his mind dehors the conclusions drawn either by the Investigation Wing in the appraisal report or by the Ld. AO in the draft assessment order. The copy of the appraisal report submitted by the Investigation Wing to the Ld. AO and ld. JCIT are merely guidance to the Ld. AO and are purely internal correspondences on which the assessee does not have any access. Moreover, the Act mandates the Ld. AO to frame the assessment after getting prior approval from ld. JCIT u/s 153D of the Act. The ld. JCIT getting involved in the search assessment proceedings right from inception does not have any support from the provisions of the Act as no where the Act mandates so. The scheme of the Act mandates due application of mind by the Ld. AO to examine the seized documents independently dehors the appraisal report of the Investigation Wing and seek explanation/clarifications from the assessee on the contents of the seized documents. When the scheme of the Act provides for a leeway to both the Ld. AO as well as the ld. JCIT to even ignore the conclusions drawn in the appraisal report by the Investigation Wing and take a different stand in the assessment proceedings, the fact of ld. JCIT getting involved in the search assessment proceedings right from the receipt of copy of appraisal report, as argued by the Ld. CIT DR, has no substance. In other words, irrespective of the conclusions drawn in the appraisal report by the Investigation Wing, both the Ld. AO and the ld. JCIT are supposed to independently apply their mind in a judicious way before drawing any conclusions on the contents of the seized documents while framing the search assessments. As far as the argument of the Ld. CIT DR that the details were normally filed by the assessee at the last moment is concerned, the ld. AO has got every right to reject the said replies if not filed within the stipulated time. It is not the case of the revenue that the details were filed by the assessee in the instant case at the last moment. Even if it is so, as stated above, it is the prerogative of the ld. AO to accept the said letter containing details or reject the same as it was not filed within the stipulated time. On the contrary, if the ld. AO himself grants time to the assessee to furnish the details till the last moment, then no fault could be attributed to the assessee. In such circumstances, the only irresistible conclusion that could be drawn is that the ld. AO is not serious about the statutory deadlines provided in the Act. In our considered opinion, if the arguments of the Ld. CIT DR are to be appreciated that the ld. JCIT need not apply his mind while granting approval of the draft assessment orders u/s 153D of the Act as it is not provided in section 153D of the Act, then it would make the entire approval proceedings contemplated u/s 153D of the Act otiose. The law provides only the Ld. AO to frame the assessment, but, certain checks and balances are provided in the Act by conferring powers on the ld. JCIT to grant judicious approval u/s 153D of the Act to the draft assessment orders placed by the Ld. AO.

7. The contention on behalf of department that Section 292BC of the Act introduced by way of amendment by Finance Act, 2026 w.e.f from 1.04.2021 would be applicable in the case of present assessee also have not substance as we find that legislature has made the amendment applicable retrospectively w.e.f 01.04.2021 in regard to approvals granted after 01.04.2021. Thus, by no stretch of imagination we can accept the contention that because the matter is being heard subsequent to the amendment it becomes applicable to also in cases where approval was granted prior to 01.04.2021.

8. We also bring on record the fact that subsequent to the hearing a request was made on behalf of the department by ld. CIT, DR Shri Mahesh Kumar by letter dated 16.04.2026 that because a reference u/s 255 of the Act has been made to Hon’ble president on 16.04.2026 for constitution of special bench in the several cases, including the present, in regard to issue of approval u/s 153D of the Act, the case be released. We do not appreciate that after a matter has been kept heard and order reserved department can take a plea to release the matter as subsequently, reference has been made by the department for Constitution of Special Bench. We have found issue to be covered by decision of Hon’ble jurisdictional High Court, thus too, we find no reason to release the matter.

9. Accordingly, the ground No. 7 is sustained. The appeals of the assessee are allowed. The impugned assessment arising out of the vitiated approval u/s 153D of the Act stand quashed.