ORDER

M. Balaganesh, Accountant Member. – The Assessee Sara Sae Pvt. Ltd (hereinafter referred to as ‘assessee) by filing the present appeal sought to set aside the impugned assessment order dated 28.06.2017 passed by the Assessing Officer (AO) u/s 143(3) r.w.s. 144C of the Income Tax Act, 1961 (for short ‘the Act’) inconsonance with the order passed by the Dispute Resolution Panel (DRP)-2, New Delhi dated 18.05.2017 u/s 144C(5) and order of the ld TPO dated 28.10.2016 passed u/s 92CA(3) of the Act.

2. Ground Nos. 1 and 2 raised by the assessee are general in nature and does not require any specific adjudication.

3. Ground Nos. 3 to 3.5 raised by the assessee are challenging the transfer pricing adjustment of Rs. 3,65,84,151 to the value of international transactions entered into by the Commodity Division of the assessee.

4. We have heard the rival submissions and perused the materials available on record. The assessee is engaged in the manufacturing of machinery and equipments that have its application in oil well drilling and production activities. The assessee has two different segments namely Capital Goods Segment and Commodity Products Segment. The Capital Goods Segment/ Division manufactures highly specialised and custom made equipment, which has application in oil and gas industry e.g. BOP units, accumulated units, high pressure test units, hydraulic power tongs, etc. The Commodity segment/Division produces fast moving commodity items and spare parts etc. like hammer, unions, swivel, joints and pub joints, ring joints, gaskets, flanges, valves, castings, MS products etc. These are used in oil and gas industry as well in various other industries. Though the assessee has entered into several international transactions with its Associated Enterprises (AE), the only dispute before us is with regard to the international transaction pertaining to sale of finished goods by Commodity Division of the assessee to its AE in USA amounting to Rs. 51.68 crores. The method applied for benchmarking the said International transaction by the assessee was Transactional Net Margin Method (TNMM) having a tested party as the assessee and applying Profit Level Indicator (PLI) as operational profit/operational cost (OP/OC). As per TP study of the assessee, the PLI of the assessee was 6.61%. The assessee selected five comparable and working capital adjusted arithmetical mean of the comparable was 1.55 %. Since the margin of the assessee was higher than the comparables margin, the total transaction of Rs. 51.68 crores on account of sale of finished goods by Commodity Division of assessee to its AE in USA was determined to be at Arm’s Length Price (ALP) by the assessee in its TP study report.

5. The assessee had considered foreign exchange fluctuation gain of Rs. 2,38,83,566 as part of operating profit. The assessee filed the audited accounts of the Commodity segment before the ld TPO vide reply dated 13.01.2016. That ld TPO sought to exclude the foreign exchange gain of 2,38,83,566 as non-operating item and arrived at the operating margin. Now, the issue is very well settled by the decision of the coordinate Bench of

Delhi Tribunal in the case of

D.E. Shaw India Advisory Services (P.) Ltd. v.

Dy. CIT [2017] (

Delhi –

Trib.), wherein it was held that foreign exchange gain or loss shall have to be treated as operating in nature as it emanates out of regular business activities of the assessee. The relevant operative portion of the said Tribunal order is reproduced below:-

“10.11 The only effective ground remaining to be adjudicated is on the plea of the assessee to treat foreign exchange gain/loss as operating in nature. This issue is squarely covered in favour of the assessee by the order of ITAT Delhi Bench in the case of Ericsson India (P.) Ltd. (supra) wherein the ITAT Delhi Bench in Para 17 of the said order, while ruling in favour of the assessee, directed the TPO to treat the foreign exchange gain/loss as operating in nature in calculating the operating margin of the assessee as well as final comparable companies. Respectfully following the same, we set aside this issue to the file of TPO/AO to treat the foreign exchange gain/loss as operating in nature in calculating the operating margin of the assessee as well as final comparable companies. Accordingly, this ground stands allowed for statistical purposes in all the three years before us. “

6. Similar view was taken by the Bangalore Tribunal in the case of

Global E-Business Operations (P.) Ltd. v.

ACIT [2021] (Bangalore –

Trib.). Same view was taken by the

Delhi Tribunal in the case of

Rampgreen Solutions (P.) Ltd. v.

Dy. CIT [2023] (

Delhi –

Trib.). Respectfully following the same, we hold that the foreign exchange gain of Rs. 2,38,83,566 should be considered as part of operating income for the purpose of determination of operating margin of the assessee.

7. The ld TPO sought to disturb the PLI of the assessee by disturbing the allocation of common expenses between the Delhi Office and Dehradun office by the assessee in Commodity Segment. The assessee had allocated the common expenses between the Delhi Office and Dehradun Office on the basis of net profit ratio as has been its consistent practice. The ld TPO sought to disturb the same by reallocating the expenses on the basis of turnover.

8. By making the aforesaid two adjustments to the operating margins, the ld TPO reworked the operating margins of the assessee at (-) 1.39 %. The ld TPO also rejected four comparables of the assessee and accepted only one comparable company Hilton Metal Forgings having PLI of 5.59%. This PLI of 5.59% of the comparable was benchmarked with assessee’s PLI of (-) 1.39% and the ld TPO made a transfer pricing adjustment of Rs. 3,65,84,151 as under:-

| Particulars |

Amount (in Rs.) |

| Operating Cost |

84,36,88,039 |

| Arm’s length margin (%) |

5.59% |

| Arm’s length margin (Rs.) |

4,71,62,161 |

| Arm’s length Price |

89,08,50,200 |

| Price charged by the assessee |

83,19,60,967 |

| International Transaction |

51,68,44,659 |

| 3% of Price charged |

1,55,05,340 |

| Difference between ALP and price charged by the Assessee |

5,88,89,233 |

| Percentage of International transaction to total revenue |

62.12 |

| Proportionate difference for which adjustment is required to be made |

3,65,84,151 |

9. With regard to allocation of common expenses on the basis of net profit done by the assessee, the assessee pleaded that in assessee’s own case for AYs 2010-11 and 2011-12, the allocation of common expenses done by the assessee on the basis of profits was accepted by the ld TPO. However, the ld AO while allowing deduction u/s 80IA of the Act sought to allocate the common expenses in the ratio of turnover of the respective divisions. The assessee objected to the same before the ld CIT(A) and the ld CIT(A) agreed with the assessee’s contentions that allocation of common expenses should be done only on the basis of profit of the respective units.

10. We find that it is not in dispute that assessee had followed TNMM as the Most Appropriate Method (MAM) for benchmarking the impugned international transaction with its AE. Hence, allocation of common expenses on the basis of profit of the respective division would be apt. It is pertinent to note that in AY 2010-11, the ld CIT(A) accepted this contention of the assessee and revenue’s appeal to this tribunal was dismissed on the ground of low tax effect. However, in AY 2011-12, the ld CIT(A) following the order of his predecessor accepted the very same contention of the assessee. The revenue did not even prefer any appeal on this issue to the tribunal in AY 2011-12. This goes to prove that revenue had already accepted the stand of the assessee that allocation of common expenses need to be done only on the basis of profit in AY 2011-12. There is absolutely no change in the facts and circumstances of the case during the year. There is no need for the revenue to take a divergent stand during the year under consideration. Further, we find that the coordinate bench of this Delhi Tribunal in the case of Fujitsu India Ltd. v. Dy. CIT (Delhi – Trib.) dated 02.02.2017, had specifically held that allocation of common expenses cannot be done on the basis of turnover and the apt method would be to allocate on the basis of gross profit margins. The relevant observation in this regard is reproduced here under:-

“6. We are unable to countenance the view canvassed by the Id. AR. There can be no rationale in apportioning the costs on the basis of number of persons working in the three segments. A person working at a lower level, such as, a Helper or an Assistant, cannot be compared with a person working at a higher position, such as, a well qualified technician or a marketing expert, drawing more salary. One segment may need more lower staff drawing less salaries and the other segment may have more higher staff with higher salaries. If we consider the number of heads working in each segment, irrespective of their positions etc., and apportion unallocated costs in that ratio, the results are bound to be distorted. At the same time, we are also not agreeable with the apportionment of unallocated costs in the ratio of sales price or, say, gross revenue. It is so for the reason that the Trading segment’ will, naturally, have more gross revenue representing sale price of goods because it will also include cost of goods sold. On the other hand, the ‘Service segment will be relatively more work- intensive but entailing lower costs because of the absence of cost of material. In our considered opinion, a more logical way of apportioning ‘Unallocable costs’ is to divide them in the ratio of gross profit margins (not gross profit rate) earned by the assessee from the three segments. This will present a more realistic way of apportioning the unallocable costs. “

11. Respectfully following the aforesaid decision, we direct the ld TPO to accept to the assessee’s contention of allocation of common expenses on the basis of gross profit margins instead of turnover and re-compute the PLI of the assessee accordingly.

12. The next issue to be decided is on the inclusion of comparables chosen by the assessee. The assessee had chosen five comparables to benchmark the impugned international transaction. The list of those comparables together with its respective PLI are as under:-

| Name of the comparable |

PLI (OP/OC) |

| Hilton Metal Forgings |

5.59 % |

| Carnation Industries |

7.32 % |

| Sanghvi Forgings and Engineering |

11.90% |

| Gontermann Pieper |

(-)13.34 % |

| Surindra Engineering |

(-) 2.17% |

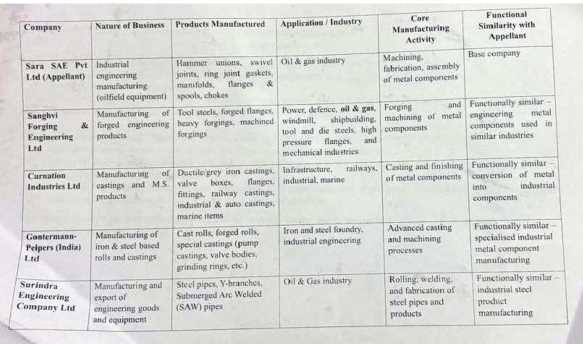

13. The ld TPO accepted only Hilton Metal Forgings as a good comparable with the assessee and rejected the remaining four comparables either on the ground of functional dissimilarity or on the ground of persistent losses. The ld AR before us submitted that in AY 2011-12, the ld TPO had accepted the very same comparables- Carnation Industries and Surindra Engineering as good comparable with the assessee as functionally similar. Similarly, the ld AR submitted that the ld TPO had accepted Gontermann Pieper and Surindra Engineering as good comparable with the assessee in AY 2012-13 on the ground of functional similarity. So effectively, all these three comparables i.e. Carnation Industries, Gontermann Pieper and Surindra Engineering were accepted by the ld TPO in AY 2011-12 and in AY 2012-13, as the case may be, as a good comparable on functional similarity. There is absolutely no change in the FAR analysis with those years when compared to the year under consideration. The ld AR before us has filed the details of functions performed by the assessee company, functions performed by all the comparable companies chosen by the assessee in tabular form, which is reproduced as under:-

14. From the above, it is very that all the four comparables have been wrongly rejected by the TPO. We find that all the aforesaid four comparables are functionally comparable with that of the assessee. Moreover, what is to be seen under TNMM is only the broader functional comparability than the product similarity. Further, we also find that the comparable Gontermann Pieper had also been rejected by the ld TPO on the ground that it had failed the filter of persistent losses. We find that the coordinate bench of Mumbai Tribunal in the case of Asstt. CIT v. MOL Maritime (India) (P.) Ltd. (Mumbai – Trib.) had observed that the expression ‘persistent loss’ is not defined under the Income Tax Act or the rules framed there under and accordingly, the persistent loss need to be understood as incurrence of losses in three consecutive financial years, including the financial year corresponding to the assessment year under dispute and immediately two preceding years. We find that the comparable Gontermann Pieper has shown PLI (OP/OC) as under:-

| Financial Year |

Assessment Year |

PLI |

| 2009-10 |

2010-11 |

12.28% |

| 2010-11 |

2011-12 |

8.21% |

| 2011-12 |

2012-13 |

(-) 7.94% |

| 2012-13 |

2013-14 |

(-) 13.34% |

15. Hence, it could be seen that the said comparable company had not shown loss in the consecutive three years including the year under consideration before us. Hence it cannot be construed as a persistent loss making company as on 31.03.2013 relevant to AY 2013-14, being the year under consideration. Hence, we hold that this comparable company to be a good comparable as the functions are also similar.

16. Ld TPO is directed to re-compute the operating margins of the assessee in the above mentioned terms and benchmark the same with the operating margins of the five comparable companies listed above and decide whether the international transactions carried out by the assessee is at Arm’s length or not. The Ground Nos. 3 to 3.5 raised by the assessee are restored to the file of TPO/ AO in the above mentioned terms.

17. Ground No. 4 raised by the assessee is challenging the disallowance of interest of 51,95,632/- u/s 57(iii) of the Act.

18. We have heard the rival submissions and perused the materials available on record. STS Products Inc. USA is the wholly owned subsidiary of the assessee since 2002. The said entity is a loss making entity. In FY 2011-12, the assessee availed External Commercial Borrowing (ECB) of US Dollar 7 million from Standard Charted Bank, London. Out of the said borrowing, USD 1.5 million was invested by the assessee in its wholly owned subsidiary i.e. STS Products Inc by way of investment in equity shares. The balance USD 5.5 million was advanced to the said company as a loan bearing interest of 6.6% per annum. During the year under consideration, the assessee received Rs. 2,00,21,236/- as interest from its wholly owned subsidiary on the loan which had been duly offered to tax under the head ‘income from other sources’. The assessee had paid interest to standard chartered Bank in the sum of 2,42,46,284 on the total loan of USD 7 million. The assessee claimed the same as deduction u/s 57(iii) of the Act against the interest income of Rs. 2,00,21,236. The ld AO noted that on the investment in equity shares made in subsidiary company, the assessee had not earned any dividend income. Accordingly, he proceeded to disallow the proportionate interest to the extent of borrowed funds utilized for making investment in equity shares in wholly owned subsidiary company and disallowed interest of Rs. 51,95,632 thereon. This action of the ld AO was upheld by the ld CIT(A).

19. We find that the issue in dispute is squarely covered by the decision of the Hon’ble Supreme Court in the case of

CIT v.

Rajendra Prasad Moody [1978] 115 ITR 519. Respectfully following the same, we direct the ld AO to allow the interest expenditure of Rs. 51,95,632/-. Accordingly, Ground Nos. 4 to 4.4 raised by the assessee are allowed.

20. Ground No. 5 raised by the assessee is challenging the initiation of penalty proceedings u/s 271(1)(c) act, which would be premature for adjudication at this stage and hence dismissed.

21. In the result, the appeal of the assessee is partly allowed for statistical purposes.