Tax authorities face prima facie contempt for defying explicit court orders to disburse GST refunds.

Issue

Whether the tax department’s subsequent order rejecting a GST refund claim constitutes prima facie contempt of court when a specific judicial order had already directed the sanction and disbursal of that refund with interest, and multiple deadlines for compliance had been set and ignored.

Facts

-

The Claim: The petitioner filed a refund application in Form GST RFD-01 for unutilized Input Tax Credit (ITC) covering the period from April 2020 to March 2022.

-

The Disbursal Order: On March 28, 2025, the Court issued an order directing the tax authorities to sanction and disburse the refund along with statutory interest within a period of four weeks.

-

Continued Default: The department failed to comply with the order, prompting the petitioner to file an application under Section 151 of the Civil Procedure Code (CPC). On July 16, 2025, the Court recorded the default and permitted the petitioner to file a fresh refund application with a directive for its expeditious processing.

-

Contempt Proceedings: The matter returned to the original Bench, which observed on February 13, 2026, that its initial order was clear and required no further clarification. A contempt plea was subsequently disposed of on March 13, 2026, granting the department a final three weeks to comply.

-

The Defiant Rejection: Instead of disbursing the funds as ordered by the Court, the respondent passed a fresh order on March 24, 2026, actively rejecting the petitioner’s refund claim.

Decision

-

Prima Facie Contempt Established: The High Court held that upon a plain reading of the sequence of prior judicial orders, the respondents were prima facie in contempt of the absolute order dated March 28, 2025.

-

Disregard of Deadlines: The Court took a strict view of the department’s persistent non-compliance and its subsequent attempt to bypass a binding judicial directive by passing a fresh rejection order.

-

Ruling in Favor of Assessee: The issue was decided in favor of the assessee, establishing that the tax department cannot overwrite or evade a direct court mandate to disburse a refund.

Key Takeaways

-

Judicial Orders Override Administrative Discretion: Once a High Court issues a specific directive to sanction and disburse a tax refund, the tax department loses its administrative jurisdiction to re-adjudicate or reject that same claim.

-

Consequences of Bureaucratic Defiance: Passing a fresh rejection order to counter an active court mandate to disburse funds constitutes a direct challenge to the authority of the judiciary and invites strict contempt of court proceedings.

-

Protection of Taxpayer Rights: Taxpayers are protected against endless administrative delays through contempt remedies, ensuring that final judgments for refund disbursals and accrued interest are enforced against non-compliant officials.

CM APPL. Nos. 33681 & 33682 of 2026

| (i) | Issue a writ in the seeking writ of mandamus and/ or any other appropriate writ, directing the respondent department to sanction the refund claims filed by the Petitioner under. Refund Application dated 30.11.2023 (Reference no.AA071123082463F) for the amount of Rs. 70,09,455/- for the period April 2020 to March 2022, along with the applicable interest as per the provisions of the Central Goods and Service Tax Act, 2017 and rules made thereunder; |

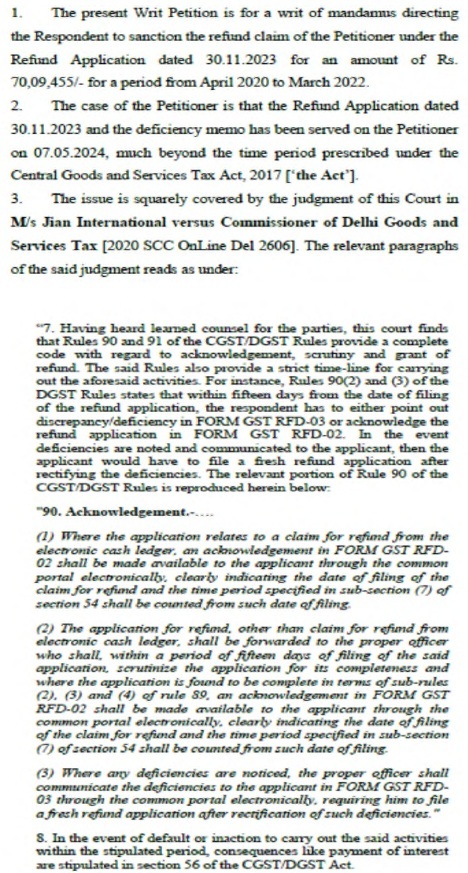

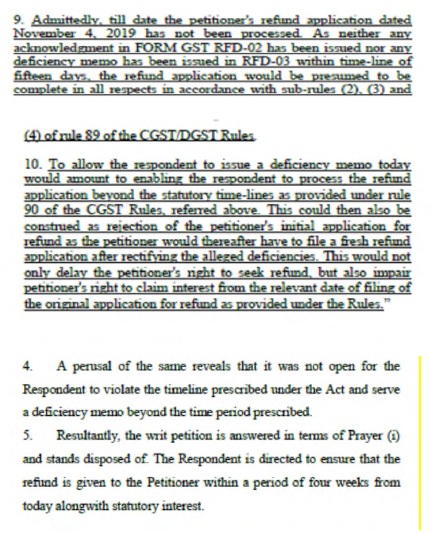

“5. Resultantly, the writ petition is answered in terms of Prayer (i) and stands disposed of. The Respondent is directed to ensure that the refund is given to the Petitioner within a period of four weeks from today alongwith statutory interest. ”

“5. Resultantly, the writ petition is answered in terms of Prayer (i) and stands disposed of. The Respondent is directed to ensure that the refund is given to the Petitioner within a period of four weeks from today alongwith statutory interest. ”

“CM APPL. 41655/2025

1. This is an Application filed by the Petitioner under Section 151 of the Code of Civil Procedure, 1908 seeking compliance of the Order dated 28.03.2025.

2. In the opinion of this Court, the Order dated 28.03.2025 does not require any clarification, since the Writ Petition was disposed of in light of the Judgment passed by a Co-ordinate Bench in M/s Jian International versus Commissioner of Delhi Goods and Services Tax, 2020 SCC OnLine Del 2606.

3. Needless to state, it is open for the Applicant to take necessary steps in accordance with law for compliance of the Order dated 28.03.2025.

4. With the above observations, the Application is disposed of.”