ORDER

Manish Agarwal, Accountant Member.- The captioned cross-appeals are filed by the assessee and the Revenue against the order dated 11.12.2025 by Ld. Commissioner of Income Tax (A)-3, Noida [“Ld. CIT(A)”] in Appeal No. CIT (Appeal), Noida- 3/10072/2022-23 passed u/s 250 of the Income Tax Act, 1961 [“the Act”] arising from the assessment order dated 30.03.2025 passed u/s 143(3) of the Act pertaining to Assessment Year 2023-24.

2. Both cross-appeals filed by the assessee and by the Revenue for same assessment years therefore, they are decided by a common order for the sake of convenience.

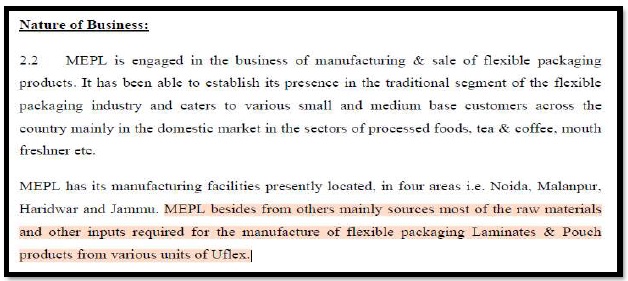

3. Brief facts of the case are that the assessee is a company, engaged in the business of manufacturing and sale of flexible packaging products. The return of income for the year under appeal was e-filed on 27.12.2023, declaring total income of INR 1,12,12,40,187/- after claiming set off of loss of INR 14,02,69,507/-. A search and seizure action u/s 132 was carried out on 21.02.2023 at Uflex-Montage Group of which assessee is one of the member and its business premises as well as manufacturing units spread all over the country were also covered. The AO in its order has discussed in details about the various manufacturing plants situated at Noida, Malanpur, Haridwar, Jammu etc. The AO further discussed the product profile of the assessee and the entire manufacturing process. Thereafter, the AO discussed about the major customers and major suppliers of the assessee and then material found as a result of search comprising of some dairy marked as D-19 to D-28 wherein various details of payments received and made were noted. The AO alleged the same as unrecorded transactions of sales. The relevant extract of pages of such diaries are reproduced in para 14 at pages 37 to 55 of the assessment order and the AO has computed the total cash receipts found recorded in the said diaries at INR 18,27,44,58,759/-. Thereafter, the statements of Directors and key employees of the companies are discussed. The AO thereafter, concluded that the books of accounts of the assessee are not reliable and invoked the provision of section 145(3) of the Act. The AO observed that G.P. declared during the year under appeal by the assessee is very less and had estimated the profits on the turnover declared at INR 2362.02 crores by applying the GP rate of 18% and after reducing the declared G.P. rate, net addition of INR 3,41,78,50,023/- was made. Besides this, out of the total cash receipts found noted in the diaries seized during the course of search at INR 1827.44 crores, AO allowed the credit of sums matched with RTGS entries of INR 1188.00 crores as recorded in the regular books of account and remaining cash receipts of INR 639.44 crores was held as undisclosed cash sales on which profit rate of 18% was applied resulting into further addition of INR 1,15,10,02,577/-. Accordingly, total addition on account of manufacturing and trading activity was computed at INR 4,56,88,52,600/- (3,41,78,50,023+1,15,10,02,577). Besides this, AO further alleged that assessee has paid commission @ 4% to the entry operators for obtaining RTGS entries of INR 1188.00 crores and made addition of INR 47.52 crores as unexplained expenditure u/s 69C of the Act as commission paid. Further, during the course of search, cash of INR 43.68 Lakhs was found which was claimed as out of withdrawal from the bank however, the AO has not accepted the explanation tendered and made the addition for the same. Thus, the total income of the assessee was computed at INR 5,04,84,20,600/-.

4. Against the said order, the assessee filed an appeal before Ld.CIT(A) who vide order dated 11.12.2025 has confirmed the findings of the Ao that the cash receipts noted are related to disclosed and undisclosed sales made however, as against the RTGS entries deduction by the AO, ld. CIT(A) has reduced the total sales made to the traders and thus the total undisclosed sales was computed at Rs. 328 crores as against 639.44 crores taken by the AO. Ld. CIT(A) further confirmed the application of provisions of section 145(3) of the Act and however, has reduced the GP rate to 9.463% as per Industry average as against 18% applied by the AO on both the declared turnover as well as on undisclosed turnover. Further, though the allegation of the AO that the assessee has paid the commission for obtaining the accommodation entries of sales was confirmed however, by allowing the benefit of telescoping out of the profit estimated separate addition made on account of alleged commission of INR 47.52 crores was deleted and also the addition made towards cash found during the course of search of INR 43.68 Lakhs was deleted by accepting the contention of the assessee.

5. Aggrieved by the said order of Ld.CIT(A), both parties are in appeal before the Tribunal. The assessee has raised following grounds of appeal:

| 1. |

|

“That the Ld. CIT(A) has erred in law and on facts in partly sustaining the addition of Rs.127,08,44,242/-by applying a gross profit rate of 9.463% as against 3.53% declared by the appellant in its duly maintained books of accounts. |

| 2. |

|

That the Ld. CIT(A) has erred in law and on facts in arbitrarily applying a Gross Profit rate of 9.463%, [i.e. [(11.75% (past history) +7.176% (industry average))/2] without considering significant cost inflation, stagnant sale prices, and other relevant business factors, due to which the appellant had rightly declared a GP of 3.53%. That CIT(A) erred in mechanically relying on past history and a restricted industry sample, which by itself cannot constitute a valid basis for GP estimation. |

| 3. |

|

That the Ld. CIT(A) has erred in law and on facts in applying an industry GP rate of 7.176% by mechanically relying on the limited sample of companies adopted in his earlier order for A.Y. 2022-23, while ignoring the larger and more representative sample of comparables dealing in the same product line furnished by the appellant during the proceedings. That CIT(A) erroneously computed the industry average GP at 7.176% as against the correct average of 3.536% duly placed on record by the appellant. |

| 4. |

|

That the Ld. CIT(A) has erred in law and on facts in computing the alleged undisclosed turnover at Rs. 328 crores without excluding contra entries and without reconciling totaling differences, and in ignoring the assessee’s submissions and seized material. That the actual undisclosed sales aggregate to only Rs.27.90 crores as against Rs. 328 crores taken by the CIT(A). |

| 5. |

|

Without prejudice to the foregoing grounds, the Ld. CIT (A) has erred in law and on facts in denying the benefit of expenses below the line against the estimated income. |

| 6. |

|

That the Ld. CIT(A) erred in upholding the assessment under section 143(3), which is bad in law as the notice issued under section 143(2) of the Act, having been issued without obtaining the mandatory approval Pr. CIT/pr. DIT/CIT/DIT is in violation of Instruction No. F.NO.225/72/2024/ITA-II, dated 03-05-2024, and hence the assessment so framed is bad in law and liable to be quashed. |

| 7. |

|

That the Ld. CIT(A) erred in upholding the assessment under section 143(3), which is bad in law as he approval dated 30.03.2025 granted by the Ld. Addl. CIT, Central Range, Meerut is mechanical without application of mind, and void ab initio. The assessment was framed under Section 143(3), whereas the approval was taken under Section 148B, contrary to law, rendering it invalid. |

| 8. |

|

The Ld. CIT(A) further failed to appreciate that no commission was ever paid and, therefore, telescoping the alleged commission with the addition made on account of gross profit element is wholly unjustified and unwarranted, particularly when the entire case rests solely on statements without any corroborative material being brought on record. |

| 9. |

|

That the Ld. CIT(A) has erred in law and on facts in sustaining the addition by relying upon the alleged modus operandi deposed by Shri Manoj Khandpal, while ignoring the discrepancies in the statement of the authorized officer recorded during the course of search and further denying the appellant the right to cross-examine, thereby violating principles of natural justice and rendering the assessment liable to annulment. |

| 10. |

|

That the Ld. CIT(A) has erred in law and on facts in sustaining the addition made on the basis of documents seized during the search is illegal and void ab initio, as the panchnama suffers from serious infirmities – the witnesses thereto were not local inhabitants, no neighbours were made witnesses, and the Authorised Officer failed to issue an order in writing to the persons selected to attend and witness the search – all in clear violation of the CBDT Search and Seizure Manual, 2025; hence, the entire search and consequential assessment stand vitiated. |

| 11. |

|

That without prejudice to above grounds of appeal the Ld. CIT(A) has erred in law and on facts in sustaining the addition based upon the assessment framed under Section 143(3) of the Income Tax Act, 1961, despite invoking Section 145(3) and rejecting the books of account, whereas the assessment ought to have been completed under Section 144 as per the statutory mandate. |

| 12. |

|

That the appellant craves leave to add, amend, or modify the grounds of appeal as may be necessary during the course of the proceedings.” |

6. On the other hand, the revenue has taken following grounds of appeal:

| 1. |

|

Whether on the facts and circumstances of the case and in law, the Ld. CIT A has erred in restricting the addition of Rs. 115,10,02,577 to Rs. 31,05,97,994, made on account of gross profit on out of books sales amounting to Rs. 639.44 crores, by accepting the submissions of the assessee that certain entities were dummy entities, without making any independent enquiries and by overlooking the indicators adopted by the Investigation Wing and the Assessing Officer, who had analyzed and computed the total sales made to traders at Rs. 1,128 crores. |

| 2. |

|

Whether on the facts and circumstances of the case and in law, the Ld. CIT A has erred in restricting the addition of Rs. 115,10,02,577 to Rs. 31,05,97,994, without appreciating the fact that the seized reference documents, notepads, reflected cash transactions amounting to Rs. 1,128 crores, which were subsequently routed back into the regular books of account through traders. |

| 3. |

|

Whether on the facts and circumstances of the case and in law, the Ld. CIT A has erred in estimating the gross profit at 9.463 percent as against 18 percent applied by the Assessing Officer, by relying upon cherry picked facts and selective industry data furnished by the assessee, without conducting independent enquiries OR verifying the authenticity and applicability of such data with cogent evidence. |

| 4. |

|

Whether on the facts and circumstances of the case and in law, the Ld. CIT A has erred in restricting the addition of Rs. 341,78,50,023, 14.47 percent of Rs. 2362,02,48,949, made during assessment proceedings on account of suppressed profits to Rs. 140,13,89,370. |

| 5. |

|

Whether on the facts and circumstances of the case and in law, the Ld. CIT A has erred in overlooking the monetary benefits derived by the assessee from out of books cash sales, the prevailing business circumstances and overall industry standards, which clearly indicate an increase in profit margins during the post COVID period relevant to the year under consideration. |

| 6. |

|

Whether on the facts and circumstances of the case and in law, the Ld. CIT A has erred in estimating the gross profit of the assessee by mechanically adopting an alleged industry average of 7.167 percent, without appreciating the specific facts of the assessees case, without independent verification, analysis, OR application of mind and while ignoring the post COVID recovery that benefited the entire sector and the anomalous decline in the assessees gross profit during the year under consideration. |

| 7. |

|

Whether on the facts and circumstances of the case and in law, the Ld. CIT A has erred in deleting the addition of Rs. 47.52 crores, made on account of commission allegedly paid on sales through dummy traders OR entities, despite having rejected the assessces explanation regarding such expenditure, thereby clearly attracting the provisions of section 69C of the Income tax Act, 1961, which were rightly invoked by the Assessing Officer. |

| 8. |

|

Whether on the facts and circumstances of the case and in law, the Ld. CIT A has erred in deleting the addition of Rs. 47.52 crores by disregarding the proviso to section 69C of the Act, which expressly prohibits allowance of any deduction in respect of unexplained expenditure and by wrongly applying the theory of telescoping, which is not permissible in view of the said proviso. |

| 9. |

|

Whether on the facts and circumstances of the case and in law, the Ld. CIT A has erred in deleting the addition of Rs. 47.52 crores by contradicting his own findings, wherein the gross profit was estimated at 9.463 percent, being only 5.9 percent higher than the declared profit, whereas the alleged commission was paid at 4 percent, thereby rendering the availability of sufficient funds implausible and making the application of telescoping untenable, as the expenditure remained unexplained and unaccounted. |

| 10. |

|

Whether on the facts and circumstances of the case and in law, the Ld. CIT A has erred in deleting the addition of Rs. 43.68 lakhs made under section 69A of the Act, on account of unexplained cash seized during the course of search, without appreciating that the assessee failed to establish any direct, proximate and credible nexus between the alleged bank withdrawals and the cash found, particularly in view of substantial time gaps, repeated small withdrawals and absence of evidence regarding retention of such cash. |

| 11. |

|

That the order of Ld. CIT A 3, Noida being erroneous in law and facts be set aside and an order of the A.O. be restored. |

| 12. |

|

That the above grounds are without prejudice to each other and appellant craves leave to add, alter OR amend any ground OR grounds on OR before the date of hearing of appeal. |

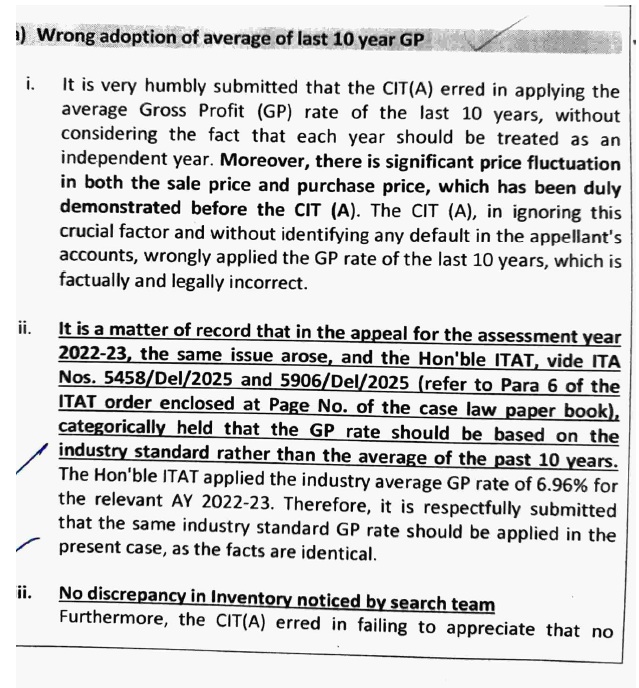

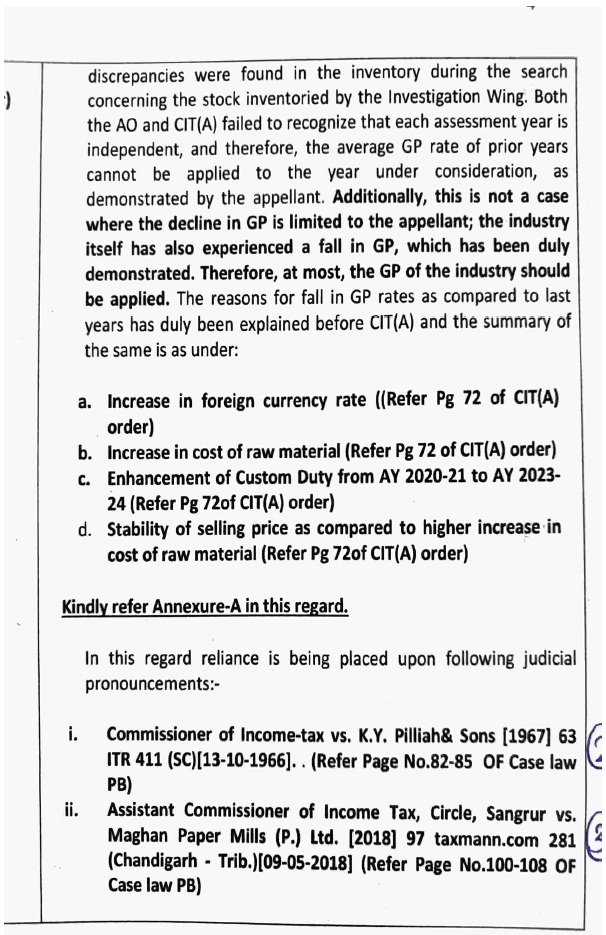

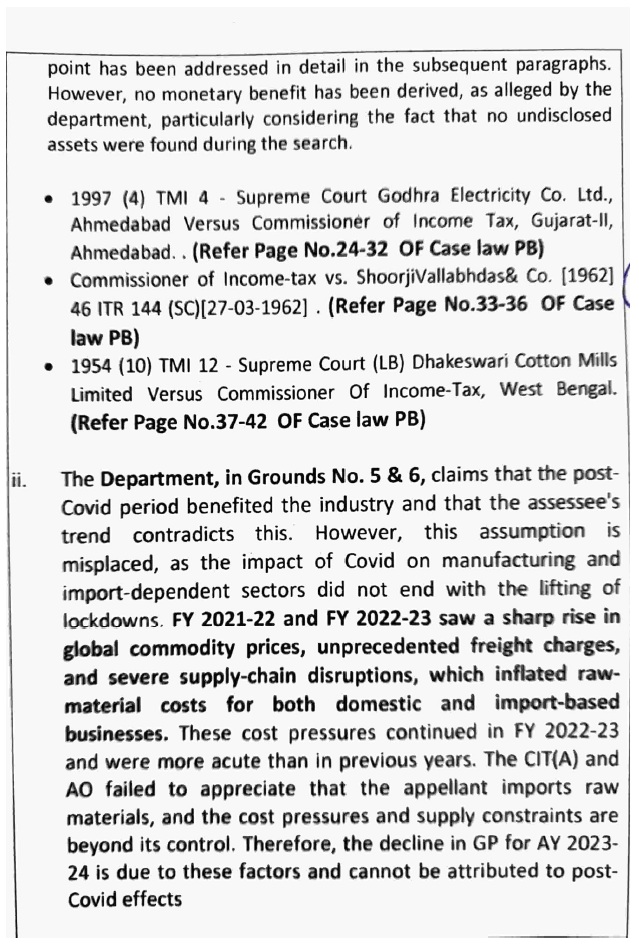

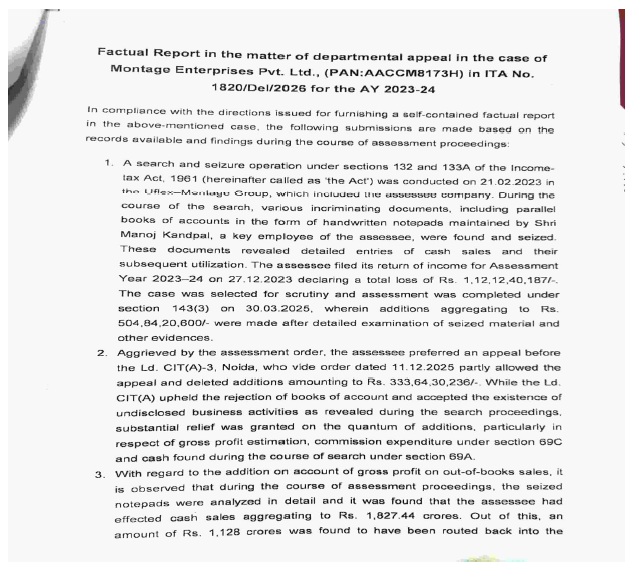

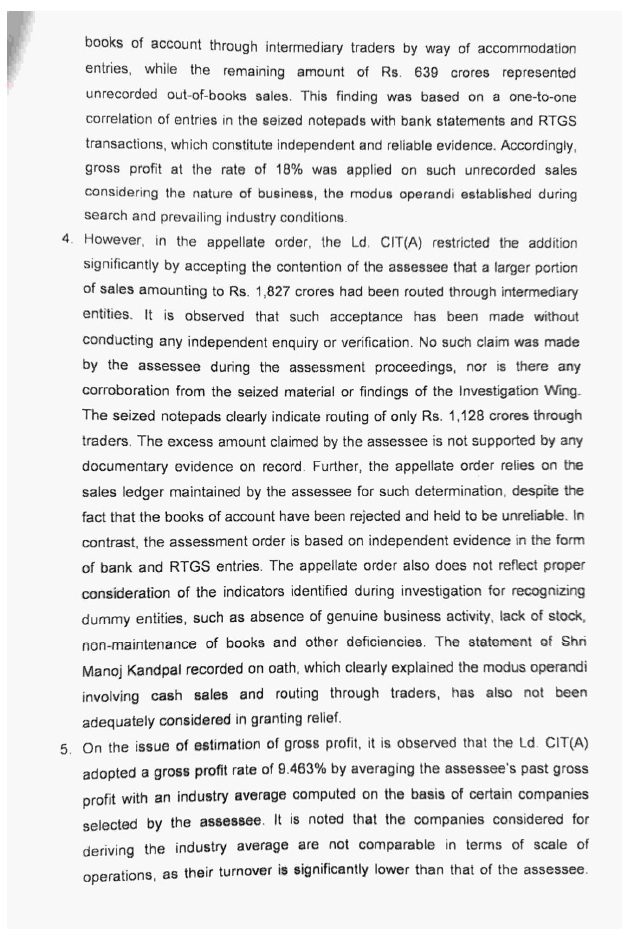

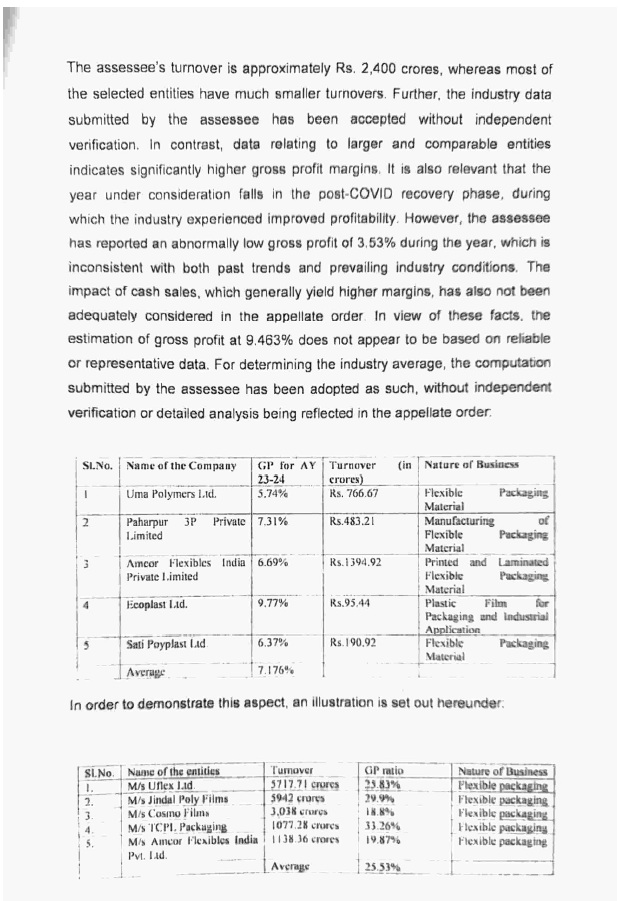

7. With regard to all the Ground of appeal Nos. 1 to 12 and Grounds of appeal No. 1 to 6 of the revenue, before us, Ld.AR for the assessee submits that G.P. rate applied by the Ao at 18% was exorbitant high and impossible in the similar line of business which was reduced to 9.463% by ld. CIT(A) by taking average of past 10 years GP rate of the assessee computed at 11.753% and Industrial average GP of 7.176%. Ld.AR submits that Ld. CIT(A) has not appreciated the reasons for fall in the G.P. rate as compared to preceding years and further wrongly computed the industrial average G.P. rate at 7.176% as against 3.536% industrial average G.P. rate computed by the assessee by taking average of Seven Industries having similar business as of assessee. Ld. AR submits that Ld. CIT(A) has ignored the fact that during the year under appeal, cost of raw material was increased by 38.62%. Further the turnover has already been increased and in support of this contention ld. AR drew our attention to the chart reproduced at page 18 of the order of Ld. CIT(A) according to which main reasons for fall in the G.P. rate to 3.536% was explained. Ld. AR submits that application of he G.P. rate of 9.463 % on declared turnover is very high and submits that in the immediately preceding year, the Co-ordinate Bench of the Tribunal in assessee’s own case has applied G.P.rate @ 6% by taking industrial average of the said year as the basis. Ld. AR further submits that during the year under appeal, there was no discrepancy noted by the survey team in respect to the inventory records maintained. AS per ld. AR the ld. CIT(A) has wrongly computed the industrial average GP at 7.176%. For this, Ld. AR drew our attention to page 73 of the appellate order wherein assessee has computed the average Industrial G.P. by taking average of Seven companies engaged in the similar line of trade. However, Ld.CIT(A) has excluded Three companies having substantially low GP or in loss by observing that these companies were not included in preceding year and therefore, as a principal of consistency, they must be ignored. Ld.AR submits that these companies are comparable companies with respect to the product and the sales and their data are available for the year under appeal therefore, the same should be included for computing the Industrial average. Ld.AR further submits that if these companies are included in, there was no difference in the G.P. rate declared by the assessee viz a viz Industrial GP. Thus the ld. AR submits that by following the judgement of the Coordinate bench of Delhi Tribunal in assessee’s own case for immediately preceding year, the average Industrial GP rate should be applied.

8. Ld.AR submits that the action of Ld.CIT(A) in taking average G.P. of past 10 years is not correct approach as they are drastically changes in the circumstances and assessee has also demonstrated that there were substantially increased in the cost of raw material which has affected adversely to the profitability of the assessee company. He therefore, prayed that G.P.rate applied on the declared amount of INR 2362.02 crores @ 3.536% should be accepted and the additions sustained by Ld.CIT(A) be deleted. In this regard, Ld.AR further submits a detailed written submissions which is reproduced as under:-

9. On the other hand, Ld.CIT DR for the Revenue submits that AO has applied profit rate @ 18% after considering the fact that in immediately preceding year, the assessee has declared G.P.rate @ 16.26%. Ld. CIT DR further submits that assessee has provided industrial G.P. rate where the companies taken are not comparable and therefore, as per Ld. CIT DR, if major companies manufacturing these products are taken into consideration the average G.P. rate comes to 25.53% as against 18% applied by the AO and 9.463 % by Ld. CIT(A). He thus prayed for restoration of application of GP rate of 18%. Ld. CIT DR further filed a detailed written submission which reads as under:-

10. In the re-joinder, Ld.AR filed a submission wherein it is stated that fresh companies selected by the AO for computing the average G.P. rate @ 25.53% is incorrect as all these entities are multi-national and listed entities. Moreover, they are directly importing the raw material whereas the assessee has purchased the raw material the raw material locally from 06 parties. Therefore, the results cannot be compared with the results of the assessee. Ld.AR further filed a detailed submissions on this issue which reads as under:-

“Reply to Factual Report in the matter of departmental appeal in the case of Montage Enterprises Pvt. Ltd.

During the course of hearing, the Ld. DR placed on record a factual report obtained from the Ld. AO raising various issues. In respect of all such issues, detailed written submissions have already been filed and are being relied upon. However, as regards the issue of Gross Profit (GP) rate, the observations of the Ld. AO, as recorded at page no. 3 of the factual report, are wholly misplaced, and the point-wise rebuttal to the same is set out hereunder.

1. Functional Dissimilarity in Business Operations

The Ld. AO has relied upon certain entities, prominently including Uflex Limited, and has broadly categorized them as engaged in flexible packaging. However, the appellant’s business model is materially different. The appellant mainly sources most of the raw materials and other inputs required for the manufacture of flexible packaging Laminates & Pouch products from various units of Uflex Ltd. and thereafter carrying out processing before effecting sales. The same fact has been known to AO and acknowledged at Pg 3 of AO order. The relevant part of AO order is reproduced as under:-

It is respectfully submitted that the comparison drawn by the Ld. AO with entities such as Uflex Limited and others is wholly misplaced. The said entities (at Sr. Nos. 1 to 4) are fully integrated manufacturers, whereas the appellant is merely engaged in processing and value addition after procuring raw materials, predominantly from Uflex Limited. Consequently, a substantial portion of the profit margins stands absorbed at the level of Uflex Limited itself, rendering any comparison with such entities inappropriate and untenable. At the outset, it is further submitted that M/s Cosmo Films Limited, as relied upon by the Ld. AO, is not even engaged in the same line of business as that of the appellant. Even otherwise, the remaining entities are also not comparable for the reasons elaborated in the subsequent paragraphs. Therefore, comparison with such entities is fundamentally flawed.

2. Multinational and Listed Entities – Not Comparable

It is respectfully submitted that the entities relied upon by the Ld. AO are large, multinational and listed companies having extensive global operations, diversified revenue streams and significant economies of scale. In contrast, the appellant is a purely domestic entity, operating solely within India and having no subsidiaries or business presence outside India. Accordingly, such entities cannot be regarded as valid comparables. It is further submitted that all the companies selected by the Ld. AO have substantial presence outside India, with operations across multiple countries and jurisdictions. The profitability of such entities is influenced by international markets, foreign exchange factors, and diversified global operations, which are entirely absent in the case of the appellant. Therefore, the comparison of Gross Profit rates with such globally diversified entities is wholly misplaced. In order to substantiate the above, a comparative chart demonstrating the global presence of these companies, along with the countries in which they operate, is enclosed herewith. In view of these material differences, the comparison made by the Ld. AO is arbitrary, lacks comparability, and is liable to be rejected.

| Particulars |

Details |

| Uflex. Limited |

GI()gyl presence in, UAE, Mexico, Egypt, USA. PoUntde CIU countries, Nigeria, Hunnaiy; extensive international manufacturing & distribution network |

| Cosmo Films Limited |

Preegnce in 100+ countries; key regions include India, USA, South Korea, Japan; global export-oriented operations |

| TCPL Packaging Limited |

Presence in 40+ countAes; sperateE in UAE, Netheilands, Poland, India, Israel; strong Urulppresence through UAE subsidiary |

| Jindal Poly Films Limited |

Presence in 40+ countries; operates in India, Europe (Germany, Spain), North America (USA, Canada), Middle East & Africa (UAE, Egypt) |

3. Presence of Non-Comparable Income Streams

It is pertinent to note that the entities relied upon by the Ld. AO have multiple streams of operating income, including income from foreign exchange fluctuations, job work, exports and other ancillary activities. Such diversified income components materially distort the Gross Profit margins and render any comparison with the appellant inappropriate and misleading. It is further submitted that these entities undertake substantial export-oriented transactions, including sales to group/sister concerns outside India, thereby earning higher margins attributable to their international operations. In contrast, the appellant operates purely in the domestic market without any such exposure.

Moreover, these entities function as integrated manufacturers, wherein raw materials are either produced in-house or sourced globally, resulting in a completely different cost structure and value chain. The appellant, on the other hand, is primarily engaged in processing and conversion, with dependence on external suppliers for raw materials. Accordingly, there exists a fundamental and material difference in business segments, operational structure and margin drivers, and therefore, the GP margins of such entities cannot be considered as representative industry standards for the appellant.

4. Incorrect Reliance on GP Figures

Without prejudice, it is submitted that even the GP rates adopted in the report are not reliable, as the same suffer from apparent computational errors. The Ld. AO has failed to consider the correct turnover and relevant expenses while determining the GP, resulting in an incorrect computation. That the Ld. AO has erred both on facts and in law in inadvertently considering the turnover and corresponding expenses pertaining to the preceding year instead of the year under consideration, and has further erred in not reducing the employee expenses while computing the Gross Profit. Such erroneous calculation itself renders the GP rates adopted by the Ld. AO unreliable and unsustainable.

| Particulars |

UFLEX |

JINDAL POLY |

TCPL PACK |

COSMO FILMS |

AMCOR |

| Revenue from sales |

6,77,889 |

2,48,132 |

1,43,185 |

2,74,173 |

1,39,492 |

| Ratu material Consumed |

4,50,483 |

1,22,660 |

87,147 |

1,85,050 |

1,12,189 |

| Purchase of Stock, in Trade |

8,110 |

7,305 |

122 |

755 |

|

| Manufacturing Expenses |

55,876 |

25,949 |

14,564 |

30,053 |

9,087.80 |

| Payment to Employees |

56,060 |

6,338 |

11,548 |

16,890 |

9,033 |

| Increase/ (Decrease) in Stock |

-2,282 |

34,252 |

-472 |

575 |

-947 |

| Gross Profit |

1,09,642 |

51,628 |

30,276 |

40,850 |

9,299 |

| Gross Profit Ratio |

16.17% |

90.81% |

21.14% |

14.90% |

6.69% |

5. Erroneous Computation by AO

It is a matter of record that in respect of M/s Amcor Flexibles India Pvt. Ltd., the Ld. AO has considered a GP rate of 19.87%, whereas the appellant has correctly computed the same at 6.69%, supported by detailed workings which have also been verified. This clearly demonstrates the fallacy in the approach adopted by the Ld. AO.

6. Comparative Analysis of Nature of Business – Appellant v. Alleged Comparable Entities

It is respectfully submitted that the Ld. Assessing Officer has erred in benchmarking the Gross Profit (GP) rate of the appellant by relying upon certain large industry players, namely M/s Uflex Limited, M/s Cosmo Films Limited, M/s TCPL Packaging Limited and M/s Jindal Poly Films Limited, without appreciating the fundamental differences in the nature of business, scale of operations, and functional profile.

In this regard, a comparative analysis is set out hereunder:

a. Nature of Business – Appellant (MEPL)

| Particulars |

DetaUs |

| Product Range |

(i) Flexible Packaging Materials (ii) PET Chip8 (Refer Pg no. 5-8 of AO order of MEPL) |

| Flexible Packaging Materials |

| It is submitted that the appellant’s prodi.iet rangs primarily comprises flemible packaging materials manufacsured from, plastic films based on polymery such as Polyethylene, Cohn) ropyl one w CVC and Nylon, which are used in singZe-Zcn/er or multi-layer (laminated/ metallized/printed) forms depending upon the required barrier properties. These products include packhging laminates and. pouches used across sectors such as processed foods, FMCG. tea & coffee, mouth fresheners and tobacco. The product range is thus confined to conversion and processing of plastic films into flexible packaging materials, catering to specific end-use applications. |

| PET Ships, Segment |

| PET films ne generally classified based on mckrnss into nhin films (5olow 50 microns) and thick filnm (50-350 microns), depending on their ond-use applicntionc. In recent years, intermediate thickness film— (8-150 microns) have also emerged. |

b. Nature of Business – Entities Relied Upon by AO

| Company Name |

Nature |

Products Manufactured |

| M/s Uflex Limited |

Integrated Manufacturer |

Polyester films (BOPET, BOPP, CPP, Alox, pCR-arane, Metalizen; Flexible packaging (pouches. lubes, bags): Chemicals (inks, ngsesivse, (‘oalingss; Aseptic packaging (Tetra pack); Holograms; Printing cylindess; Packaging & allied machinery |

| M/s Cosmo Films Limited |

Not involved in fiexi packaging business |

Polyester films (BOPET, BOPP, PPP, Metalize); Rignd & medidne sheets; Injection. mouldedSr thermoformed containers; Chemicals; Synthetic paper; TEG-G |

| M/s TCPL Packaging Limited |

Integrated Manufacturer |

Folding cartons; Specialty/gift packaging; Food & pharma packaging; Flexible packaging (laminates, shrink sleeves, pouches); Rigid boxes |

| M/s Jindal Poly Films Limited |

Not involved in flex packaging business |

BOPET & BOPP films; Metallized & coated films; CPP films; Thermal films; Non-tearable paper (NTR); Lidding & label films |

c. Key Grounds of Non-Comparability

(i) Functional Dissimilarity (FAR Analysis)

• OF MEPL with UFLEX Ltd. and TCPL Packaging Ltd.:-

It is respectfully submitted that the appellant operates as a processing and conversion unit, whereas the entities relied upon by the Ld. AO are fully integrated manufacturers engaged in upstream as well as downstream activities. The appellant primarily undertakes value-addition processes such as printing, lamination, coating, slitting and pouch making on raw materials procured from third parties (predominantly from Uflex Group entities). In contrast, the comparable entities are engaged in the manufacture of base films (such as BOPET, BOPP, CPP), chemicals, and other primary inputs, and further undertake downstream conversion, thereby operating across the entire value chain.

Accordingly, in view of the stark differences in functional profile, asset base, and risk exposure, the said entities cannot be considered as valid comparables, and the GP rates derived therefrom are distorted, non-representative, and liable to be rejected.

• OF MEPL with Cosmo Films Limited and Jindal Poly Films Limited:-

That M/s Cosmo Films Limited and M/s Jindal Poly Films Limited are not primarily engaged in the business offlexible packaging materials and, therefore, are not comparable to the appellant.

(ii) Scale and Market Position

The entities relied upon are large, listed, multinational corporations with global operations and economies of scale, whereas the appellant is a domestic, mid-sized entity catering to a limited customer base.

(iii) Product and Segment Difference

The appellant operates in the mid-segment flexible packaging market, while the comparable entities operate in diversified segments, including rigid packaging, specialty films, chemicals, and capital goods.

(iv) Integrated v. Dependent Model

The appellant is dependent on external suppliers (notably Uflex Group) for raw materials, whereas entities like Uflex and Jindal are vertically integrated manufacturers, resulting in fundamentally different cost structures and margins.

(v) Multiple Revenue Streams

The said entities derive income from diverse business verticals, including exports, job work, chemicals, machinery, and other ancillary activities, which significantly distort the GP margins and make comparison inappropriate.

(vi) Geographic and Risk Differences

The comparable entities have global operations and exposure to international markets, currency fluctuations, and diversified risks, whereas the appellant operates solely in the domestic market. The same has been discussed earlier.

7. Conclusion

In view of the above, it is evident that the entities relied upon by the Ld. AO are functionally, structurally, and economically incomparable to the appellant. The adoption of their GP rates as industry benchmarks is therefore arbitrary, unjustified, and contrary to settled principles of comparability. Accordingly, the GP rates derived from such entities cannot be applied to the appellant’s case, and the comparison so made deserves to be rejected in toto.”

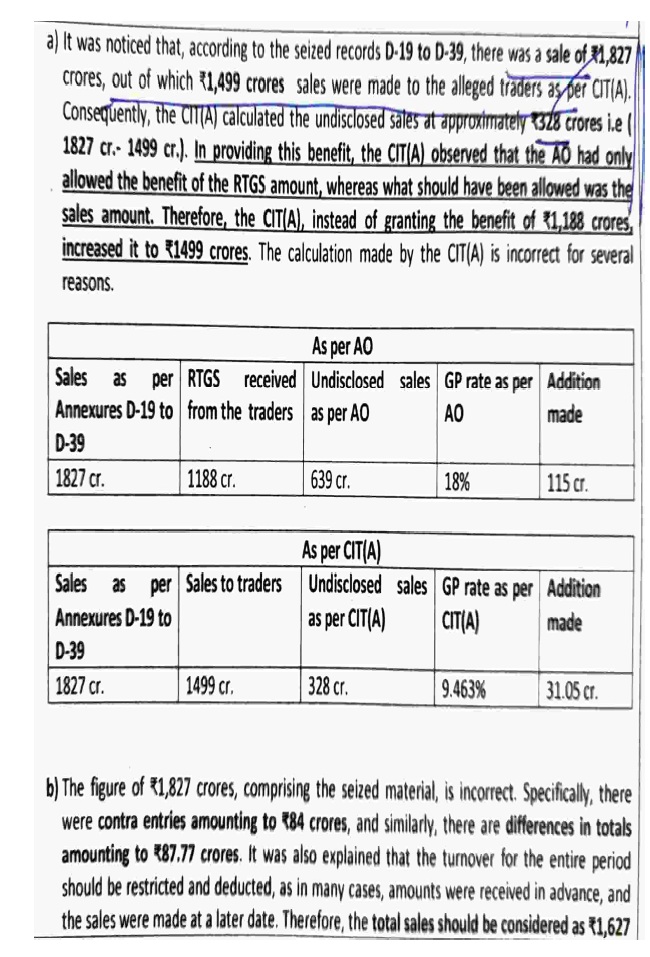

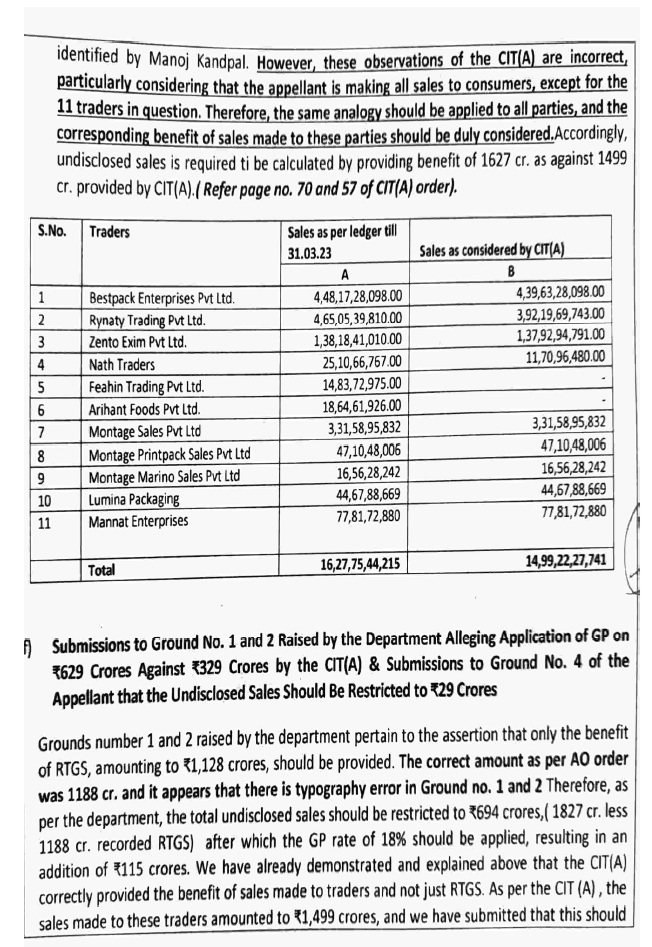

11. With regard to the computation of undisclosed sales as found noted in the seized diaries, ld. AR submits that based on the diaries found and seized marked as Annexure D-19 to D-39, total receipts of INR 1827.00 crores were found noted out of which the AO has reduced the RTGS entries of INR 1188.00 crores and treated INR 639.00 crores as undisclosed sales on which 18% G.P. rate was applied resulting into the addition of INR 115.00 crores. Ld.AR submits that Ld.CIT(A) has accepted part contention of the assessee reduced the total sales made to the traders and the remaining turnover of INR 328.00 crores was held as undisclosed sales. Ld. Thereafter CIT(A) applied G.P. rate @ 9.463% resulting into the addition of INR 31.05 crores.

12. With respect to the application of G.P.rate, detailed submission has been made by Ld. AR hereinabove. With respect to the computation of the undisclosed sales, Ld.AR submits that Ld.CIT(A) has not allowed the credit to the extent of contra-entries of INR 84 crores found noted in the same diaries and were brought tot eh notice of both the lower authorities. Ld.AR drew our attention to page 27 to 71 of the Paper Book containing the details of contra-entries appearing in the diaries found and seized. Ld.AR further drew our attention to page 27, 40, 42 to 45 of the Paper Book which are the summary of contra-entries of different parties /units such as “OMI, Shikar, Jammu” and also fled the corresponding ages of the diaries. Ld. AR thus prayed that the further deduction of these contra-entries should be allowed.

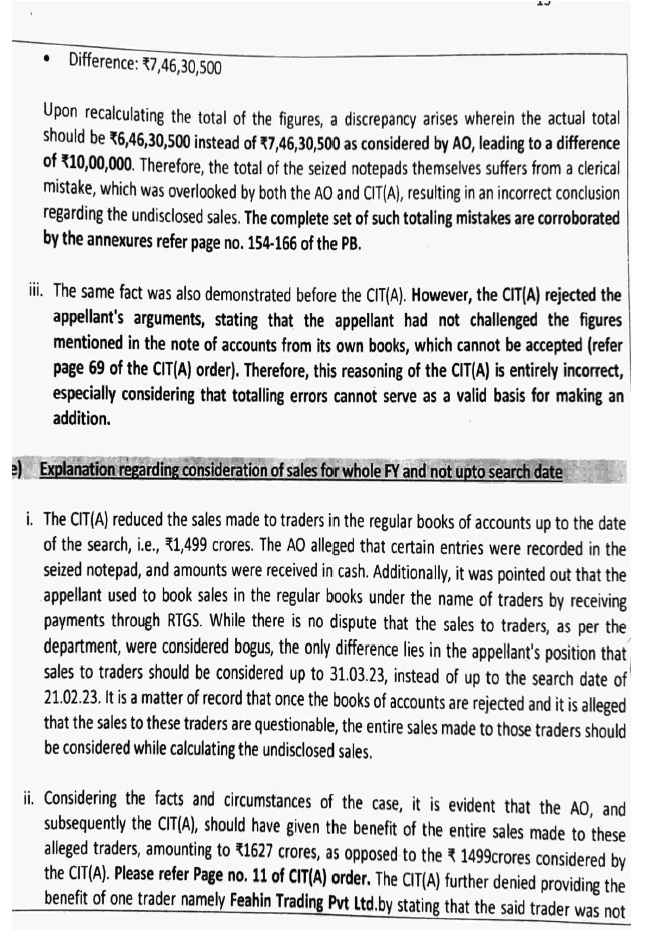

13. Besides this, Ld.AR submits that there were certain totaling errors in various pages of diaries found and seized during the course of search for which he drew our attention to pages 144 to 166 of PB wherein summary of such errors is tabulated at pages 154 & 155 and copies of certain papers of the diaries are placed at pages 156 to 166. Ld.AR submits that gross totaling error as per these papers comes to INR 87.77 crores, the deduction of should be further allowed.

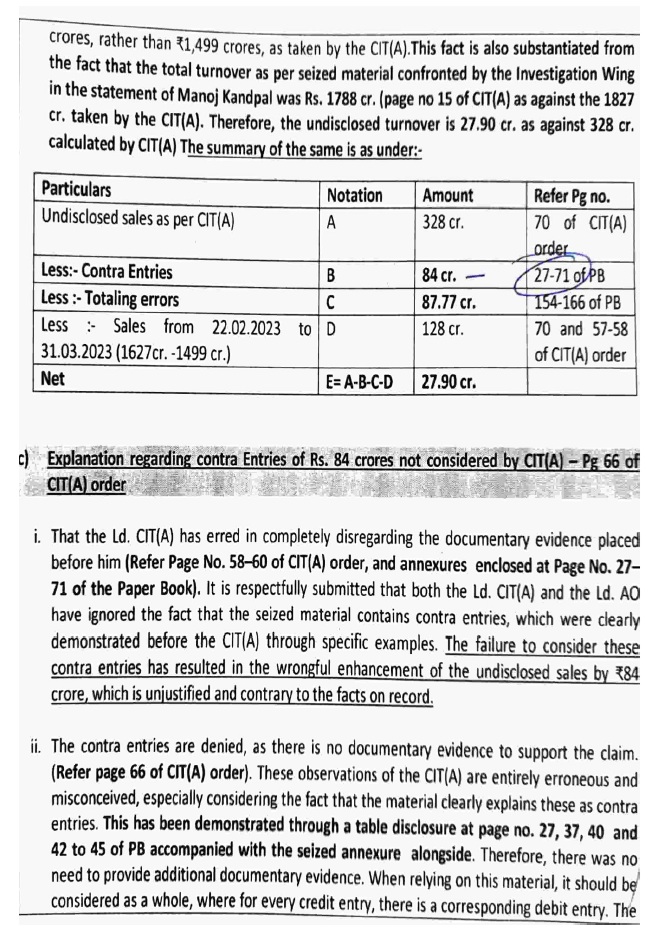

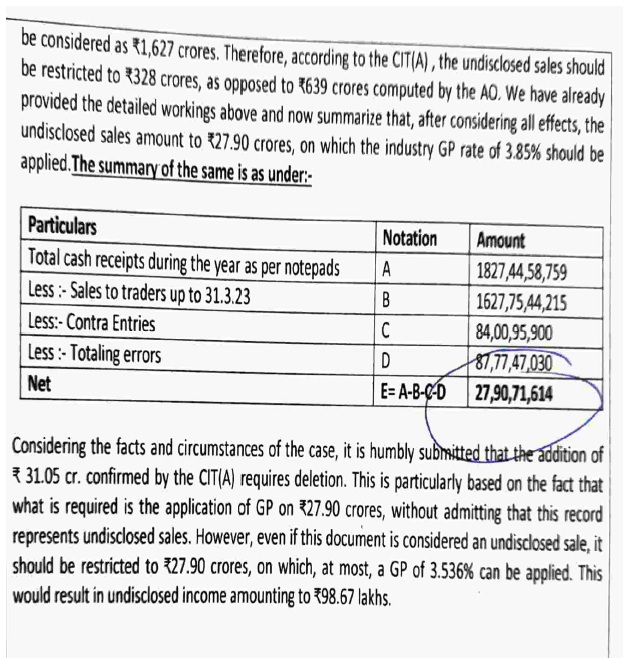

14. Ld.AR submits that Ld. CIT(A) had not allowed the deductions though all these details with respect to this claim were reproduced from pages 58 to 60 of the order. With respect to claim of deduction for contra-entries, Ld.AR submits that Ld. CIT(A) has not accepted the same by observing that he has taken gross value of the sales made to the traders of INR 1499.00 crores, therefore, as per Ld. CIT(A), contra entries had no relevance. Ld. AR submits that deduction on both the counts i.e. for Contra Entries and Totaling error should be allowed. Ld. AR further submits that besides this, the sales after the date of search of INR 128 crores has not been reduced by the Ld.CIT(A). Ld.AR submits that credit of the same should also be allowed and after reducing all the three claims, the net figure comes to INR 27.90 crores which can be taken as undisclosed sales on which Industry GP rate should be applied.

15. Ld.AR filed a detailed written submission which reads as under:-

16. On the other hand, Ld. CIT DR for the Revenue vehemently supported the orders of the AO on the issue of computation of undisclosed sales at INR 639.44 crores and submits that Ld. CIT(A) has allowed the credit of the sales to traders which is not the correct approach and the entries found noted in the diaries representing RTGS entries should only be deducted against the total receipts noted in the said diaries. Ld. CIT DR thus, submits that the unaccounted sales taken by the AO at INR 639.00 crores should be substituted.

17. Heard the contentions of both the parties at length and perused the material available on record. With respect to the trading additions made, the AO has made the addition by estimating the income of the assessee on two type of turnover:-

| (i) |

|

Estimation of profit by applying G.P rate on the turnover declared in the books of accounts of INR 2362.02 crores |

| (ii) |

|

Estimation of profit on undisclosed sales. |

18. In both types of estimation of profits, first and foremost issue if what would be the reasonable rate of gross profit to be applied. The AO has applied 18% G.P. rate which was reduced to 9.463% by Ld. CIT(A). It is observed that in the instant case, in immediately preceding year, the Co-ordinate Bench of

Delhi Tribunal in

Montage Enterprises (P.) Ltd. v.

DCIT/ACIT [

2026] (

Delhi –

Trib.)/ITA Nos. 5458 & 5906/Del/2025 has applied the Industrial average GP rate of 6.96% as the most reasonable G.P. rate in the facts and circumstances of the case. While applying the G.P. rate of 6.96 %, the Co-ordinate Bench has made following observations in para 6 of the order as under:-

6. “We next notice with the able assistance coming from both the parties that the learned CIT(A)’s impugned estimation has considered the assessee’s average GP @ 11.84% in AYs 201213 to AY 2021-22 alongwith the flexible packaging material industry’s comparable instances having the GP rate @ 6.96% (pages 122-123) in the lower appellate discussion to arrive at the “mean” profit rate of 9.40% i.e. 11.84% + 6.96%+ 2, which is challenged by both the parties. That being the case, the assessee takes us to case law CIT v. K.Y. Pilliah & Sons

(1967) 63 ITR 411

(SC), CIT v.

Surjeet Singh Mahesh Kumar (1994) 210 ITR 83

(Del.), Bimal Kumar Anant Kumar v.

CIT (All.), Salem Steel Co. v.

CIT (2010) 322 ITR 349

(Mad.), Telelinks & Ors. v.

CIT (2015) 377 ITR 158 (P&H), quoted in the lower appellate discussion at page 125 onwards that even such an estimation is not to be an unbridled and unguided one but to be based on the very sector’s book results ITA Nos.5458/Del/2025 & 5906/Del/2025 8 | P a g e at this relevant point of time. We thus reject the Revenue’s vehement contentions seeking to assess the assessee @ 18% and direct the learned Assessing Officer to estimate it’s GP @ 6.96% going by the segmental trends only. Ordered accordingly.

All other remaining issues between the parties stand rendered academic in forgoing terms.”

19. It is observed that in preceding year, Ld. CIT(A) has applied 9.40 mean profit rate of average 10 years G.P. of assessee and the Industrial average GP of the last year. However, the Co-ordinate Bench has restricted it to the industrial G.P. rate @ 6.96% as most reasonable GP rate. By following the aforesaid order, we hold that the Industrial GP rate declared during the year under appeal is the most appropriate indicator and thus the same should be applied. However, it is observed that in this year, ld. CIT(A) has raised some issue with respect to the Industrial GP computed by the assessee at 3.536%.The average G.P. of industry by taking Five companies was computed at 7.176% by Ld. CIT(A) as against the industrial G.P. rate @ 3.536% computed by the assessee. It is further observed that the assessee has computed the average Industrial G.P. of 3.536% by taking total seven comparable companies whereas Ld. CIT(A) has accepted Four companies and further included one additional company M/s Ecoplast which was taken in preceding year and not taken in the year under appeal by the assessee and computed the average Industrial G.P. rate at 7.176%. It is observed that assessee has claimed that during the year under appeal, there was substantial increase in the cost of raw material and further other factors have also impact over the GP as compared to preceding years. Thus, the assessee’s claim was that the average Industrial GP rate of 3.536% should be applied.

20. On the other hand, the claim of the Revenue is that G.P.rate is to be taken by taking similar type of industry according to which G.P. rate comes to more than 25% and thus, 18% G.P. rate applied by AO is quite reasonable.

21. On careful consideration of the facts, it is observed that the companies selected by the AO before us to work out the G.P. rate of 25% are entities engaged in the business of manufacturing of packing material by directly import of raw material from outside India whereas the assessee is purchasing the goods mainly from local parties and they cannot be compared with the assessee. Further, in the immediately preceding year also, the Revenue has not challenged the selection of some companies of this industry by Ld. CIT(A) for computing the industrial average. As observed above, assessee has taken Seven entities to compute the average industrial G.P. rate out of which Three are new companies. Whereas in immediately preceding year, the assessee has taken four out of Seven companies taken during the year and one other company was taken which was included by the ld. CIT(A) in the present year by excluding three new companies taken by the assessee. As per assessee, the average industrial G.P. rate comes to 3.536% as against the average rate of 7.176% computed by ld. CIT(A). Looking to the overall facts and further looking to the fact that both the assessee and ld. CIT(A) has not provided any valid basis for excluding the companies. Therefore, in the fitness of things and it would be fair and reasonable to take all the Eight companies taken by the assessee and ld. CIT(A) for computing the Industrial average GP of the year under appeal. Accordingly, by taking the results of all the eight companies into consideration, the average industrial G.P. rate comes to 4.315% . Thus, by following the order of Co-ordinate bench of Tribunal in assessee’s own case as stated above in immediately preceding year, the industrial G.P. rate @ 4.315% is directed to be applied as against the G.P. rate of 18% applied by AO and 9.463% applied by Ld.CIT(A). Accordingly, the AO is directed to re-compute the income of the assessee on the declared turnover of INR 2362.02 crores by applying G.P. rate of 4.315%.

22. Now coming to the other issue what would be the correct amount of undisclosed turnover as per the cash receipts noted in the diaries found and seized during the course of search. The AO has taken the gross amount of receipts noted in the said diaries at INR 1827.00 crores and after reducing the RTGS received of INR 1188.00 crores, remaining sum of INR 639 crores was taken as the undisclosed sales. Ld. CIT(A) as against RTGS receipts taken by the AO at INR 1188.00 crores allowed the deduction of total sales made to the traders of INR 1499.00 crores and treated the balance amount of INR 388.00 crores as undisclosed sales of the assessee and applied the profit rate @ 9.463% of the same.

23. Before us, the assessee has made three further claims which are:-

| (i) |

|

Claim of contra-entries of INR 88 crores |

| (ii) |

|

Claim of totaling error of INR 87.77 crores |

| (iii) |

|

Claim of deduction of sales for the period from 22.02.2023 to 31.03.2023 of INR 128.00 crores |

24. As per the assessee after allowing deduction for the aforesaid claimed, the undisclosed turnover would be reduced to INR 27.90 crores only.

25. With respect to the first claim of the assessee of INR 84.00 crores of contra-entries, relevant details are placed at page 27 to 71 of the Paper Book wherein the assessee has filed the copies of relevant pages of the diaries and statements claiming the contraentries. Such statements are – first of Unit ‘OMI’ at page 27 of the Paper Book wherein the claim of INR 22,82,95,900/- is made and the relevant sheets of the diaries seized are placed at pages 28 to 36 of the Paper Book; second is at page 37 of INR 20 Lakhs of Unit ‘HRD’ and corresponding sheets are at pages 38 & 39 of the Paper Book; third of Unit ‘Shikhar’, the chart is at page 40 and corresponding papers of diaries are at page 41 and last of unit ‘Jammu’ are at pages 42 to 45 of INR 42.58 crores and corresponding sheet are at pages 46 to 71 of the Paper Book.

26. On careful consideration of these sheets, we find that same amounts are written on left hand side as well as right hand side of the same day or on subsequent day with the same narration of name of Unit. Therefore, the claim of the assessee of contra-entries appears to be correct. After verifying the claim of the assessee, we direct the AO to reduce the amount of contra-entries as claimed by the assessee of INR 84 crores from the gross amount of cash receipts.

27. Second issue with respect to the totaling errors for which the assessee has drew our attention to pages 154 to 166 of the Paper Book and filed certain copies of the diaries. On careful consideration of the facts, the claim of the assessee appears to be correct however, since complete set of diaries containing the totaling error were not placed before us, we are unable to verify the same. Thus, the AO is directed to verify the totaling errors as claimed by the assessee from the chart placed at pages 154 to 156 of PB and allowed the deduction for the totaling errors after verification.

28. Third issue is regarding the claim of the assessee of allowing further deduction of sale of INR 128.00 crores made to traders for the remaining period from 22.02.2023 to 31.03.2023. We observed that the diaries contained the transaction upto date of search i.e. 22.02.2023 and ld. CIT(A) has already allowed the deduction of the sales made to traders upto date of INR 1499.00 crores which in our opinion is correct. Therefore, we are of the view that no further deduction could be allowed to the assessee. Regarding the claim of the revenue that deduction should be restricted upto RTGS entries only, we find no force in this argument as theses diaries contained the total transactions made through the traders and part of which were recorded in the books of accounts thus it is fair and reasonable to reduce the total sales made to the traders. Accordingly, this claim of the revenue is rejected.

29. In view of above discussion, out of the total receipts found noted in the diaries of INR 1827.00 crores, we allow the deduction of INR 1499.00 crores towards sales to the traders, deduction for contraentries of INR 84.00 crores and totaling error of INR 87.77 crores (subject to verification by the AO) and direct the Ao to apply the profit rate of 4.315% on the remaining amount of undisclosed sales. With these directions, Grounds of appeal Nos.1 to 12 raised by the assessee are partly allowed and Grounds of appeal Nos.1 to 6 raised by the Revenue are dismissed.

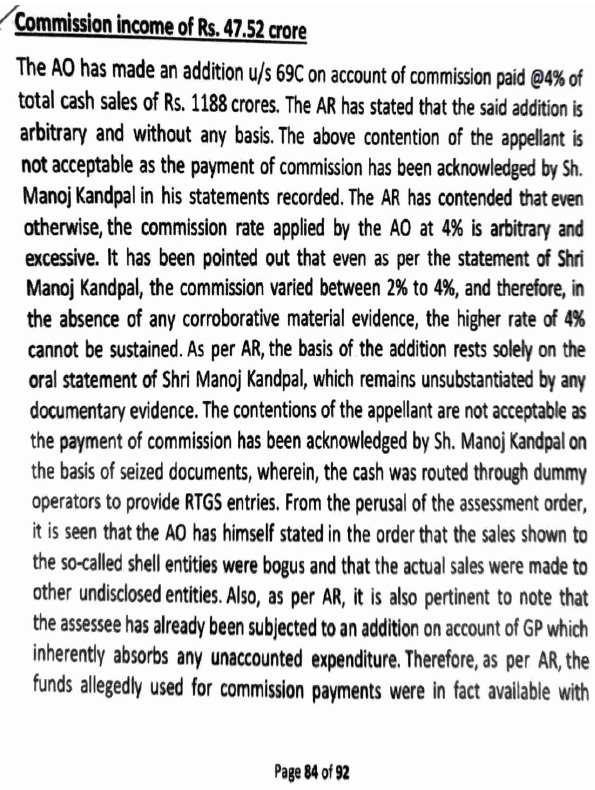

30. Grounds of appeal Nos. 7 to 9 of the Revenue are with respect to the deletion of addition on account of unexplained expenditure made u/s 69C of the Act for payment of commission for obtaining accommodation entries of RTGS.

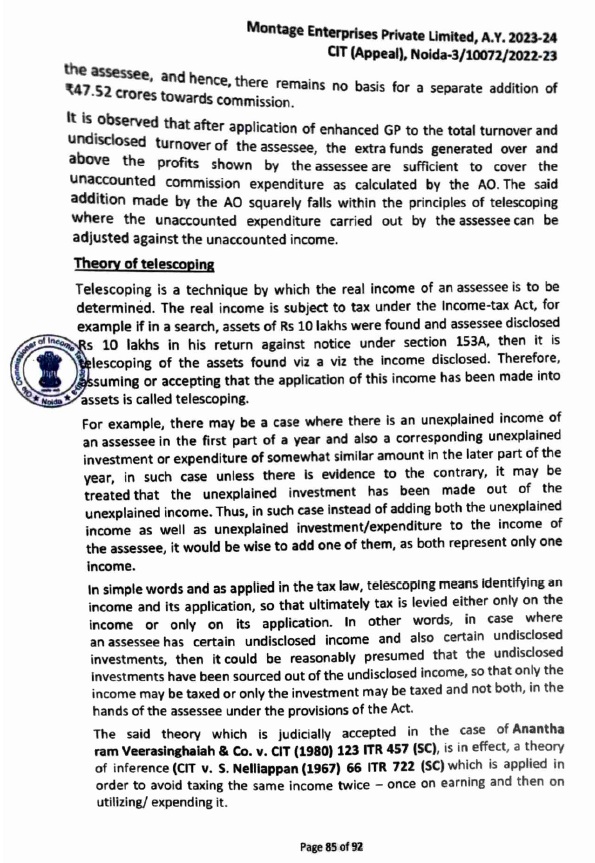

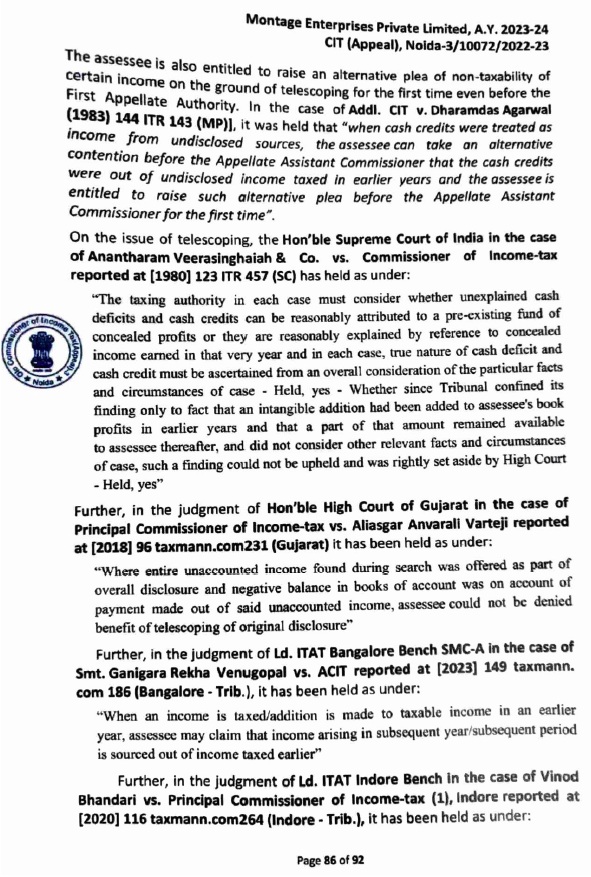

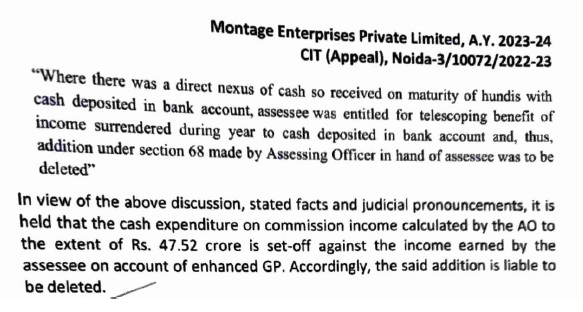

31. Heard the parties at length and perused the material available on record. Ld. CIT(A) though confirmed the observations made by the AO that the commission was paid for obtaining the accommodation entries of RTGS however, by allowing the benefit of telescoping to the assessee out of the profit sustained by applying G.P. rate on declared sales and also on undisclosed turnover which according to Ld. CIT(A) was higher than the amount paid towards the commission and therefore, no separate addition was made on this issue. The relevant observations of ld. CIT(A) are as under:

32. It is observed that based on the statement of Shri Manoj Kandpal, Manager of the assessee company, without any corroborative material brought on record by making independent inquiry from any of the trader with respect to such payment, the AO alleged that the sales to traders were made to obtain the accommodation entry and no actual transfer of goods has taken place. It is further observed that the addition has been made relying upon the statement of an employee and those statements were never re-affirmed by the Directors or principal officer of the assessee company. It is further observed that the AO has applied 4% rate of commission on the entire RTGS payment however, the said RTGS payments have been replaced by Ld.CIT(A) as the sales made to the traders as recorded in the books of accounts. It is also a fact that the action of Ld. CIT(A) in substituting the gross sale is uphold by us in this order herein above. Once we hold that the undisclosed sales are to be reduced by the amount of sales to traders which were recorded in the books of accounts, the allegation of obtaining accommodated entries in the shape of RTGS has no legs to stand. In view of these facts, we are of the opinion that no addition could be made on account of alleged commission for obtaining type of accommodation entries. Accordingly, the addition made by AO and sustained by Ld.CIT(A) though, no separate addition was made by allowing the benefit of telescoping , is confirmed. Therefore, Ground of appeal Nos.7 to 9 raised by the Revenue are dismissed.

33. Ground of appeal No.10 raised by the Revenue is with respect to the deletion of addition of INR 43.00 Lakhs on account of cash found during the course of search.

34. Heard the contentions of both the parties at length and perused the material available on record. The claim of the assessee is that at the time of search, books of accounts of the assessee were incomplete and the cash withdrawal made of INR 42.00 Lakhs from time to time form the bank was not recorded in cash book found at the time of search. Before the lower authorities, this claim was made which was rejected by holding the same as after-thought. However, the facts remained that the assessee has made cash withdrawals of INR 42.00 Lakhs which had not been recorded in the books therefore the credit of the same should be given as it is settled principal of law that the books of accounts on the date of search should be allowed to be completed. Since the cash withdrawal can be verified from the corresponding bank entry therefore, this fact cannot be held as afterthought. After reducing the said cash withdrawal of INR 42.00 Lakhs, there remained cash of INR 1,68,000/- found during the course of search, which could be held as unexplained. Since addition on account of profit at undisclosed sales was upheld, the ld. CIT(A) has allowed the benefit of the telescoping and deleted the total addition of INR 43,68,000/-. We find no error in the order of ld. CIT(A) which order is hereby upheld. Accordingly, Ground of appeal No.10 raised by the Revenue is dismissed.

35. In the final result, appeal of the assessee in ITA No.9182/Del/2025 for Assessment Year 2023-24 is partly allowed and appeal of the Revenue in ITA 1820/Del/2026 for Assessment Year 2023-24 is dismissed.