ORDER

Manish Agarwal, Accountant Member. – The captioned cross-appeals filed by the assessee and the Revenue against the order dated 08.09.2025 by Ld. Commissioner of Income Tax (A)-3, Noida [“Ld. CIT(A)”] in Appeal No. CIT(Appeals) Delhi-2/10402/2019-20 passed u/s 250 of the Income Tax Act, 1961 [“the Act”] arising from the assessment order dated 23.12.2019 passed u/s 143(3) of the Act pertaining to Assessment Year 2017-18.

2. The issues involved in both captioned cross-appeals filed by the assessee and the Revenue are common, therefore, they have been heard together and accordingly, adjudicated by a common order.

3. Brief facts of the case are that the assessee filed its return of income on 26.10.2017, declaring loss of INR 1,07,95,144/-. The case of the assessee was selected for complete scrutiny under CASS and notice u/s 143(2) of the Act was issued on 16.08.2018. Thereafter, various notices u/s 142(1) alongwith questionaries were issued from time to time which were duly replied by the assessee. The AO alleged that assessee has received fresh loan of INR 80.00 Lakhs however, the genuineness of this loan is not proved nor commercial expediency is there for taking high loans. Besides this, the AO further disallowed interest expenses claimed at INR 1,12,02,629/- u/s 36(1)(iii) of the Act. In first appeal, Ld. CIT(A) has deleted the addition u/s 68 towards the unsecured loan and restricted the disallowance made u/s 36(1)(iii) to INR 22,87,300/- as against the disallowance made at INR 1,12,02,629/- by the AO.

4. Aggrieved with the said order of Id. CIT(A), both the parties are in appeal before the Tribunal by taking various Grounds of appeal as per appeal memo.

5. Ground of appeal Nos.l, 3, 4 & 5 taken by the assessee are with respect to the restriction of disallowance made u/s 36(1)(iii) of the Act at INR 22,87,300/- and Ground of appeal No.4 of the Revenue wherein Revenue has challenged the deletion of disallowance u/s 36(1)(iii) of the Act by Id. CIT(A).

6. Before us, Ld.AR submits that Ld. CIT(A) has accepted the contention of the assessee in part that the funds invested of INR 38.82 crores were substantially out of non-interest bearing funds available with the assessee in the shape of preferential share capital and interest free loans received from the Directors. Ld.AR submits that assessee has received fresh preferential capital of INR 28.10 crore which was utilized for making interest free advances. In the written submission, the assessee at page 3 & 4 has given tables showing that Ld. CIT(A) has held that total interest bearing loans of INR 4,17,17,087/- were utilized for making investment in shares and by applying interest rate @8% has computed the amount of disallowance. Ld. AR submits that, the assessee has paid total interest of INR 3,95,343/- on these loans however, by applying the interest rate of 8%, ld. CIT(A) uphold total disallowance of INR 16,01,050/-. Ld.AR thus submits that at the most, the addition could be sustained at INR 3,95,343/- u/s 36(1)(iii) of the Act.

7. Ld.AR further submits that Ld. CIT(A) has restricted the disallowance by applying 8% interest as against interest paid @ 4% to 12% by the assessee which is supported by the chart given at pages 3 & 4 of the written submission. Accordingly, the Ld. AR submits that disallowance made u/s 36(1)(

iii) of the Act at INR 22,87,300/- deserves to be deleted. He further placed reliance on the judgment of Hon’ble Supreme Court in the case of

S A Builder v.

CIT [2007] 288 ITR 1 (SC) .

8. On the other hand, Ld. SR DR vehemently supported the order of AO and submits that AO has discussed this issue in detail and from page 23 onwards of the assessment order has observed that the assessee has utilized interest bearing funds for making interest free advances/investments to the related parties and therefore, the AO has rightly made the disallowance of entire interest expenses claimed u/s 36(l)(iii) of the Act and requested that the disallowance made by AO deserves to be uphold.

9. Heard the parties and perused the material available on record. It is observed that during the year under appeal, assessee has received fresh share capital in shape of 8% non-convertible and non-cumulative preference shares of INR 100/- each by converting unsecured loans of INR 28.10 crores. Besides this, the assessee was having equity share capital of INR 9.24 crores though the same was eroded out of recurring losses incurred over the years but the fact remained that the fresh funds was received at INR 28.10 crores by converting the interest bearing loans into capital, thus interest liability to this extent stood reduced. It is further observed that assessee is having long term loans and advances of INR 1,23,05,197/- and short term loan and advances of INR 7,50,01,150/-. Besides this, assessee has received interest free loans from Directors of INR 13.65 crores and has interest bearing loans of INR 5.49 crores from related parties where interest @ 8-10 % was paid. If the total interest free funds in the shape of preferential share capital and loans from Directors are taken together, resultant interest free funds available with the assessee were of INR 41.75 crores for making investments/interest free advances. As observed above, assessee has made total investment of INR 38.64 crores and short terms advances were given of INR 7.50 crores thus, as against total interest free funds of INR 41.75 crores, assessee has made investment/interest free advances of INR 46.14 crores, therefore, apparently the observations of Ld. CIT(A) that unsecured interest bearing loans of INR 4.17 crores were utilized for making investments/advances is appears to be correct.

10. However, we find force in the argument of Ld.AR that Ld. CIT(A) has applied 8% rate of interest on the entire funds utilized for making interest free advances/ investments by ignoring the fact that the assessee has actually paid interest only of INR 3,95,343/- on such loans ranging the rate of interest between 4% to 8%. Thus, as against the total disallowance of INR 16,01,050/- sustained on these unsecured loans, we uphold the disallowance of INR 3,95,343/- u/s 36(1)(iii) being the actual amount of interest paid by the assessee.

11. It is further observed that, out of total sum of INR 4.17 crores of unsecured loan utilized in making interest free advances/ investments, a loan of INR 68.62 Lakhs was taken from M/s Sungrace Products India Pvt. Ltd. on which interest @ 10% was paid. Therefore, the same is to be considered for making total disallowances u/s 36(l)(iii) of the Act which comes to INR 10,81,593/- (INR 3,95,343/- + 10% of 68,62,500/- i.e. 6,86,250/-).

12. Now coming to the assessee’s contention that INR 4.17 crores is part of the total investment of 38.82 crores considered by Ld. CIT(A) is accepted then availability of interest free funds in the shape of preferential share capital and interest free loans from Directors are sufficient to cover up the total interest free advances of INR 38.82 crores. In this regard, we have already observed herein above that the total investment as well as interest free advances given were of INR 46.14 crores and the gross interest free funds were of INR 41.75 crores therefore, this contention of the assessee cannot be accepted. Accordingly, as discussed above, total disallowance u/s 36(1)(iii) of the Act is restricted at INR 10,81,593/-. The Ground of 1, 3, 4 & 5 of the assessee are partly allowed and Ground 4 of Revenue is dismissed.

13. The remaining Ground of appeal No. 2 is withdrawn by the assessee therefore, the same is dismissed as withdrawn.

14. Now coming to the remaining Grounds of appeal No. 1 to 3 raised by the Revenue wherein the revenue has challenged the deletion of addition of INR 80.00 Lakhs made u/s 68 by the AO is challenged.

15. Before us, Id. Sr. DR vehemently supported the order of AO and submits that AO has discussed this issue at page 2 onwards wherein the AO has discussed the financial position and the business activity of the assessee company and concluded that no effective business was carried on by the assessee and merely, funds received in the shape of unsecured loans / capital were utilized for making non-current investments and interest free advances to the related parties. Ld. Sr. DR further drew our attention to the statements of the Directors of certain companies from whom capital/loans were received where they stated having no knowledge about the business of the assessee company. He further stated that the AO after considering these facts and circumstances, hold the loans taken from M/s Gandhipati Infra Project Pvt. Ltd. of INR 75 lakhs and from M/s. Sungrace Products Pvt. Ltd. of INR 5 Lakhs as bogus. Ld. Sr. DR further submits that Ld. CIT(A) while deleting the addition had admitted the additional evidence filed by the assessee without obtaining Remand Report and therefore, requested that AO has rightly hold the loans taken during the year as bogus which order deserves to be restored.

16. On the contrary, Ld.AR for the assessee vehemently supported the order of Ld. CIT(A) and submits that the assessee has discharged the onus of proving the loans as genuine by submitting every possible detail of the lender companies. Ld. AR further submits that Ld. CIT(A) has appreciated these facts while deleting the addition made. He further submits that the loans taken were repaid in subsequent financial year where no doubts were raised. Ld. AR thus, submits that Ld. CIT(A) has rightly deleted the addition which order deserves to be uphold.

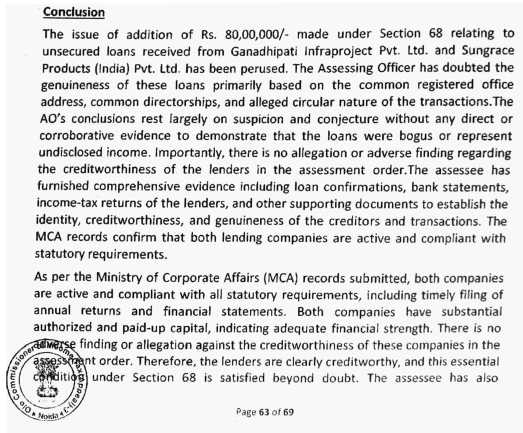

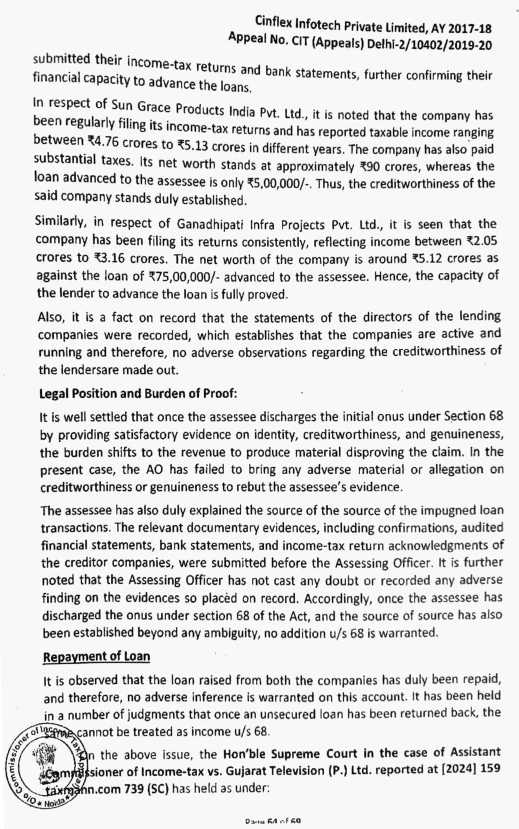

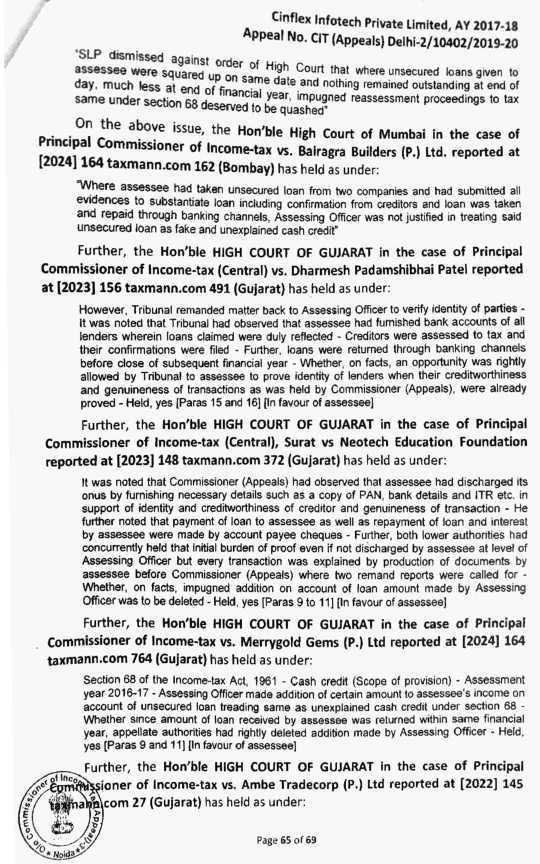

17. Heard the parties and perused the material available on record. In the instant case, it is observed that while making the addition in para 4.10 of the order, AO has observed that the two companies who had provided loans to the assessee has sufficient creditworthiness however, for the sole allegation of circular transactions, doubted the genuineness of the loan transactions and made the additions.

18. It is observed that assessee has filed the certificate of incorporation, PAN Nos, financial statements and the bank statements of the lender companies and thus has duly discharged the burden casted upon it u/s 68 of the Act of establishing the identity, creditworthiness of the lender companies and since the loans were taken through banking channels, the genuineness is also established. It is observed that both the loans were repaid in subsequent assessment year where no doubts were raised by the revenue. Once the assessee has established that the lender company has sufficient creditworthiness which was never in dispute merely on assumption that there were circular transactions, addition cannot be made. Ld. CIT(A) after considering these facts, has deleted the additions by making following observations:-

19. As could be observed that the Id. CIT(A) has deleted the addition by observing that the assessee has furnished comprehensive evidence as stated above, to establish the identity and creditworthiness and genuineness of the creditors and transactions. Ld. CIT(A) has further observed that the loans were repaid and additions were made on mere suspicion and on conjecture without any direct or corroborative evidence to demonstrate that the loans taken were bogus or represent undisclosed income. Before us, the revenue has failed to controvert these findings of ld. CIT(A) by placing any contrary material.

20. In view of the facts as discussed hereinabove and after considering the arguments of both the parties, we find that the assessee has duly complied with all the requirements of section 68 of the Act and duly discharged the burden casted upon it and Ld. CIT(A) after examining all the details which were already filed before the AO concluded that loans taken were genuine loans and deleted the addition which order is hereby upheld. The Ground of appeal No. 1 to 3 of the revenue are thus, dismissed.

21. In the final result, appeal of the assessee in ITA No.6823/Del/2025 for Assessment Year 2017-18 is partly allowed and appeal of the Revenue in ITA No.7308/Del/2025 for Assessment Year 2017-18 is dismissed.