ORDER

1.1 At the outset, we would like to make it clear that the provisions of the Central Goods and Services Tax Act, 2017 (the CGST Act, for short) and the West Bengal Goods and Services Tax Act, 2017 (the WBGST Act, for short) have the same provisions in like matter except for certain provisions. Therefore, unless a mention is specifically made to such dissimilar provisions, a reference to the CGST Act would also mean reference to the corresponding similar provisions in the WBGST Act. Further to the earlier, henceforth for the purposes of these proceedings, the expression “GST Act” would mean the CGST Act and the WBGST Act both.

1.2 The applicant is engaged in the manufacture and supply of PP packing boxes made of plastic and is duly registered under the Goods and Services Tax law in the State of West Bengal. The said products are currently being classified under HSN Code 392390 falling under Chapter 3923 covering “articles for the conveyance or packing of goods of plastics, stoppers, lids, caps and other closures of plastics”. The applicant has been charging GST at the rate of 18 percent (CGST 9 percent and SGST 9 percent) in terms of the applicable rate notification. In this background, the applicant has approached this Authority seeking clarification regarding the correct HSN classification of PP packing boxes and has submitted photographs of the product for reference.

1.3 The applicant has made this application under sub-section (1) of section 97 of the GST Act and the rules made there under seeking an advance ruling in respect of following question:

| (a) |

|

HSN code of the product named PP Packing Box? |

1.4 The aforesaid question on which the advance ruling is sought for is found to be covered under clause (a) of sub-section (2) of section 97 of the GST Act.

1.5 The applicant states that the question raised in the application has neither been decided by nor is pending before any authority under any provision of the GST Act.

1.6 The officer concerned from the Revenue has raised no objection to the admission of the application.

1.7 The application is, therefore, admitted.

2. Submission of the Applicant

2.1 The applicant submits that it is engaged in the manufacture of PP Packing Boxes and is duly registered under the Goods and Services Tax law in the State of West Bengal. The applicant carries on manufacturing activities on a regular basis and supplies the said products in the course of business.

2.2 The applicant submits that the PP Packing Boxes are manufactured by using plastic granules as the principal raw material. The manufacturing process is carried out with the help of semi-automatic machines installed at the applicant’s factory located at 284, Maharaja Nanda Kumar Road, Alambazar, Kolkata -700035. The plastic granules are processed through the said machinery to manufacture the finished product known as PP Packing Box.

2.3 The applicant further submits that the said product is presently being classified under HSN Code 392390 in terms of Chapter 39 of the Customs Tariff. As per the applicant’s understanding, the said goods fall under SI. No. 124 of Chapter 3923 covering “articles for conveyance or packing of goods of plastics, stoppers, lids, caps and other closures of plastics”. The applicant states that GST at the rate of 18 percent, comprising CGST at 9 percent and SGST at 9 percent under Schedule II, is being charged on the supply of the said goods.

2.4 The applicant submits that there is presently no dispute regarding the rate of tax being charged on the supply of the said goods, and the applicant has been regularly charging and discharging GST at the applicable rate of 18 percent.

2.5 The applicant submits that the purpose of filing the present application is to obtain clarification regarding the exact HSN Code applicable to the product namely PP Packing Box. The applicant has therefore approached this Authority seeking an advance ruling for determination of the correct HSN classification of the said product.

2.6 The applicant further submits that the product PP Packing Box appears to fall under HSN Code 392390 as per its understanding based on the classification provided in Chapter 39 of the Customs Tariff. However, the applicant seeks confirmation of the exact HSN Code from this Hon’ble Authority for the sake of clarity and proper compliance under the GST law.

2.7 The applicant has also submitted photographs of the product for reference and record in order to assist the Authority in determining the correct classification of the goods.

3. Submission of the Revenue

3.1 The concerned officer from the revenue has not expressed any view on the merit of the issue raised by the applicant.

4. Observations & Findings of the Authority

4.1 We have gone through the records of the issue as well as submissions made by the authorized representative of the applicant during personal hearing. The Revenue has not given any submission in this regard.

4.2 According to the facts narrated by the applicant, he is a manufacturer of PP packing box. In the course of manufacturing of PP packing box the applicant uses plastic granules and with the help of semiautomatic machines duly installed in the factory located at 284 Maharaja Nanda Kumar Road, Alambazar, Kolkata – 700035 the applicant manufactures the said products. The manufactured goods are sometimes sold along with the respective stoppers, lids, caps and other closures of the packing boxes and sometimes without them.

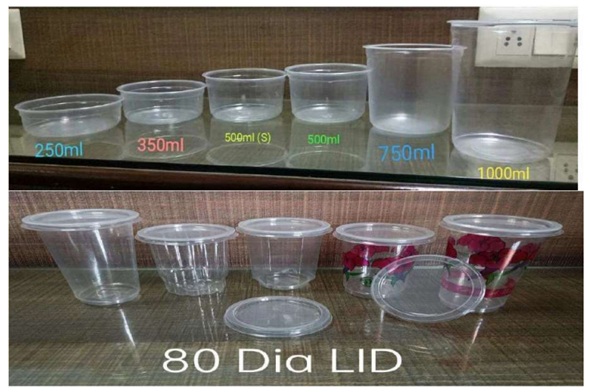

4.3 In this context the applicant wants to know the exact HSN code of PP packing box. The applicant has placed before us some specimen invoices in respect of supply of the referred goods and some images of the same for our consideration. From the furnished invoices it appears that the goods under question is sold under the description of ‘P P Packing Box’ of various categories.

The followings are the images of the products supplied by the applicant as placed before us:

4.4 According to the furnished invoices, the applicant is using HSN code 39239090 in respect of the goods supplied by him and charging tax @ 9% CGST + 9% SGST in respect of intra-state supplies and @ 18% IGST in respect of inter-state supplies.

The applicant believes that the products under question are covered under HSN 392390 and as such they fall under serial no. 124 of Schedule II of Notification No. 01/2017-Central Tax (Rate) Dated 28.06.2017 as amended by 09/2025-Central Tax (Rate) Dated 19.09.2025.

The description of the above noted serial number is ‘Articles for the conveyance or packing of goods, of plastics; stoppers, lids, caps and other closures, of plastics.’

4.5 Before going into the discussion, we should look at the relevant entries of the Customs Tariff Act, 1975. The relevant portion is reproduced as under:

| 3923 |

|

Articles for the conveyance or packing of goods of plastics; stoppers, lids, caps and other closures, of plastics |

| 3923 10 |

– |

Boxes, cases, crates and similar articles: |

| 3923 10 10 |

– – |

Plastic containers for audio or video cassettes, cassette tapes, floppy disk and similar articles |

| 3923 10 20 |

– |

Watch-box, jewellery box and similar containers of plastics |

| 3923 10 30 |

– – |

Insulated ware |

| 3923 10 40 |

– – |

Packing for accommodating connectors |

| 3923 10 90 |

– – |

Other |

|

– |

Sacks and bags (including cones): |

| 3923 21 00 |

|

Of polymers of ethylene |

| 3923 29 |

|

Of other plastics: |

| 3923 29 10 |

– – |

Of poly (vinyl chloride) |

| 3923 29 90 |

– – |

Other: |

| 3923 30 |

– |

Carboys, bottles, flasks and similar articles: |

| 3923 30 10 |

– |

Insulated ware |

| 3923 30 90 |

– – |

Other |

| 3923 40 00 |

– |

Spools, cops, bobbins and similar supports |

| 3923 50 |

– |

Stoppers, lids, caps and other closures |

| 3923 50 10 |

– |

Caps and closures for bottles |

| 3923 50 90 |

– – |

Other |

| 3923 90 |

– |

Other: |

| 3923 90 10 |

– – |

Insulated ware |

| 3923 90 20 |

– – |

Aseptic bags |

| 3923 90 90 |

– – |

Other |

4.6 Clearly the above entries are parts of Chapter 39 of Section VII of the Customs Tariff Act, 1975 which reads ‘Plastics and articles thereof; Rubber and articles thereof’. The Chapter note 1 stipulates as under:

1. Throughout this Schedule, the expression “plastics” means those materials of headings 3901 to 3914 which are or have been capable, either at the moment of polymerisation or at some subsequent stage, of being formed under external influence (usually heat and pressure, it necessary with a solvent or plasticiser) by moulding, casting, extruding, rolling or other process into shapes which are retained on the removal of the external influence.

The production process of the goods referred to in the application is the same as mentioned in the chapter note ibid. So the goods under question will qualify for Chapter 39. The applicant’s manufactured product is Poly Propylene Packing Box. Polymers of propylene are widely used for manufacture of heat- resistant and chemical-resistant containers, including food-grade containers and the polymers of propylene find entry in tariff heading no. 3902 that is included in the above referred chapter note.

4.7 Once we are sure that the products under question will come under Chapter 39, now we will discuss the exact HSN code for the said product specified as Poly Propylene Packing Box. As we see tariff heading 3923 covers ‘Articles for the conveyance or packing of goods, of plastics; stoppers, lids, caps and other closures, of plastics.’ The referred product is definitely an article for packing of goods and it is made of plastics. The lids, caps and covers of the containers are also made of plastics.

Being of the nature of boxes, cases, crates and similar articles, the containers manufactured by the applicant will come under sub-heading 392310. If we look at the entries under the said sub-heading, it is evident that the manufactured product will not come under tariff items 39231010, 39231020, 39231030 and 39231040. The said product will qualify for tariff item no. 39231090.

Again stoppers, lids, caps and closures will come under sub heading 392350 and will be covered by tariff item no. 39235090.

4.8 If we now look at the schedules of Notification No. 01/2017-Central Tax (Rate) Dated 28.06.2017 as amended by 09/2025-Central Tax (Rate) Dated 19.09.2025, we find that sub heading 3923 is included in Schedule II vide serial no. 124 and the description is the same as we find in the Customs Tariff Act, 1975 and as such all products under this sub heading are to be taxed @ 9% CGST + 9% SGST.

In view of the foregoing discussion, we rule as under:

RULING

PP packing box manufactured by the applicant is covered by tariff item 39231090 and the lids, caps and covers of the boxes are covered by tariff item 39235090.