ORDER

Laxmi Prasad Sahu, Accountant Member.- This is an appeal filed by the revenue against the order passed u/s 250 of the Income Tax Act, 1961 (hereinafter referred to as “the Act”) by the Ld. Commissioner of Income Tax (Appeals)-22, Kolkata [hereinafter referred to as “the Ld. CIT(A)] dated 23.02.2017, Appeal No. 229/CIT(A)-22/2010-11/2014-15/Kol on the following grounds of appeal:

“1. Whether on the facts and in the circumstances of the case and in law, the Ld. CIT/(A) was justified in deleting the upward Adjustment of Rs. 12,37,50,000/- by the TPO, without acknowledging that manual book and other technical documents demonstrated by the Assessee had been developed in previous year and no new services had been performed in A.Y. 2010-11.

2. Whether on the facts and in the circumstances of the case and in law, the Ld. CIT(A) was justified in deleting the addition of Rs. 94,49,341/-, without considering the point that the adjustment could not be a payment under the condition u/s. 438 of the Act.

3. Whether on the facts and in the circumstances of the case and in law, the Ld. CIT(A) was justified in deleting the addition of Rs. 5,62,59,722/- as Royalty Payment, when the payment of Royalty could have been given the status of a capital expenditure owing to its enduring nature.

4. Whether on the facts and in the circumstances of the case and in law, the Ld. CIT(A) was justified in deleting the addition of Rs. 9,40,18,765/- as Rent payment without considering that the ‘rent’ calculated on Straight Lining of lease Rent Method’ was notional and had no bearing with the actual expenditure on account of rent.

5. Whether on the facts and in the circumstances of the case and in law, the Ld. CIT(A) was justified in deleting the addition of Rs. 63,181/-, without considering that the river bank embankment and renovation could not be dealt with under that block of assets.

6. Whether on the facts and in the circumstances of the case and in law, the Ld. CIT(A) was justified in deleting the addition of Rs. 39,01,000/- on account of warranty, without going into the fact that the Assessee could not produce or file any such documents on the basis of a scientific method and thereby failed to justify the warranty claim.

7. Department craves leave to add, alter or modify any or all of the above grounds of appeal at or before the time of hearing of the appeal. “

3. Briefly stated the facts of the case are that the assessee filed return of income on 03.10.2010 declaring total income of Rs. 1,17,75,73,659/-. Subsequently, the return was revised on 23.03.2012 declaring total income of Rs. 1,06,71,45,980/-. The case was selected for scrutiny and statutory notices were issued to the assessee on the observation of documents it was observed that the assessee has made international transactions u/s 92B of the Act, therefore, the case was referred to the Transfer Pricing Officer (TPO) after obtaining duly approval from the competent authority. The TPO had determined the arm’s length price of the international transactions and suggested for upward adjustment of Rs. 12,37,50,000/-. Accordingly, the AO made adjustment towards international transactions as caried out by the assessee. During the course of assessment proceedings, the AO made various additions/disallowances which were challenged before the Ld. CIT(A) and the Ld. CIT(A) partly allowed the appeal of the assessee. The Revenue contested before the ITAT against the following deletions which is as under;-

| SI. No. |

Issue raised by the revenue |

Amount involved |

| 1. |

Royalty paid towards fees for technical services to AE Global Footwar Services Pte. Ltd., Singapore |

Rs. 12,37,50,000/- |

| 2. |

Deletion of addition u/s 43B |

Rs. 94,49,341/- |

| 3. |

Royalty to be treated as capital expenditure |

Rs. 5,62,59,722/- |

| 4. |

Rent payment |

Rs. 9,40,18,765/- |

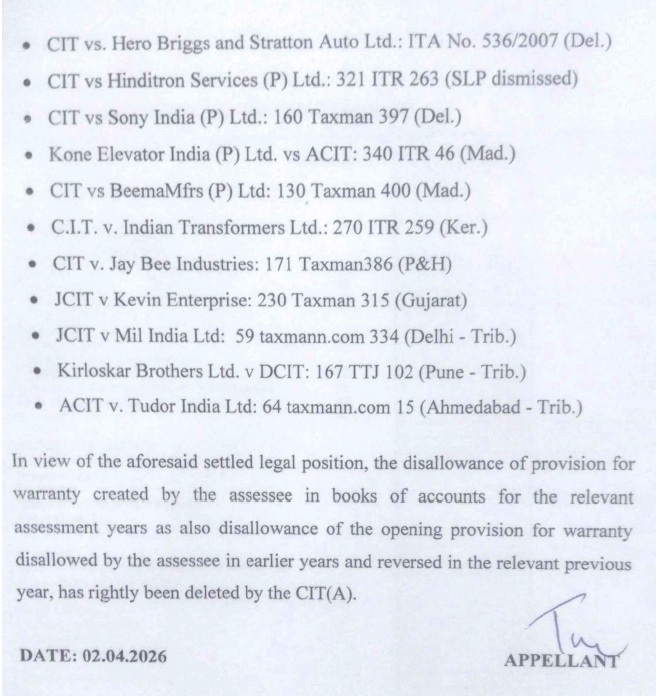

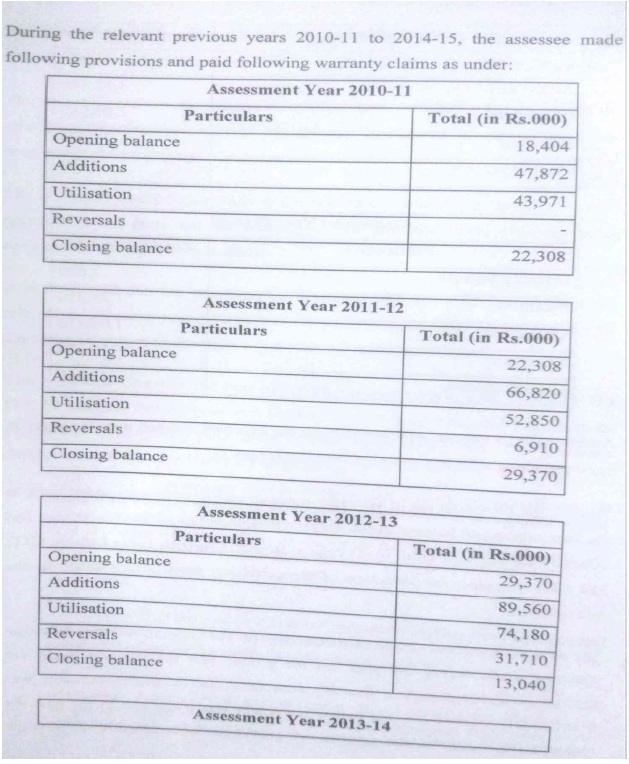

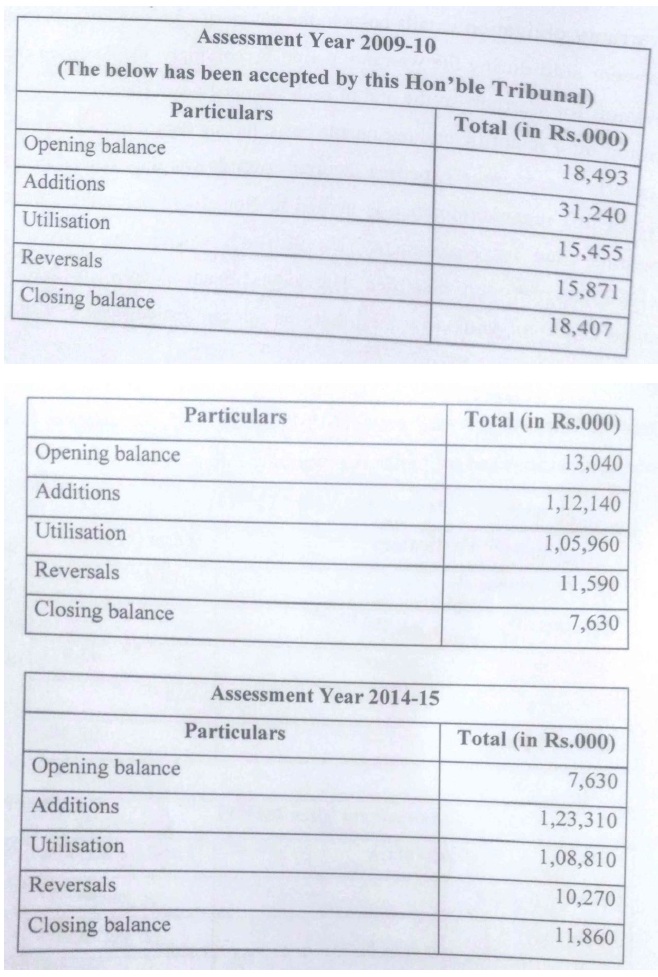

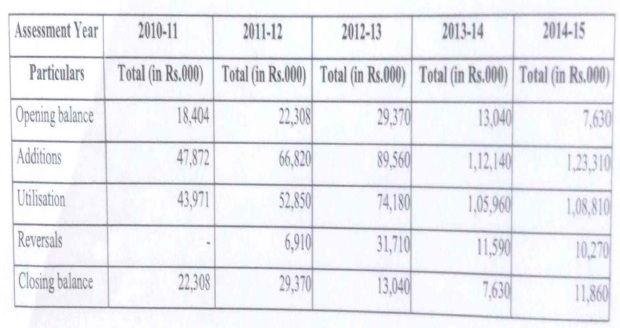

| 5. |

Capital (Block of assets) addition |

Rs. 63,181/- |

| 6. |

Warranty charges |

Rs. 39,01,000/- |

5. The Ld. DR strongly supported the order of AO. Further, in respect of disallowance u/s 43B of the Act, the AO noted that as per the TAR, there is total claim of Rs. 3,14,63,821/-, an amount of Rs. 66,23,569/ and Rs. 2,825/- actually not paid by the assessee but adjusted. Accordingly, it was disallowed. The Ld. DR further submitted that it relates to the employee’s contribution to PF/ESI and not paid within the due date but paid before filing the return of income. The Hon’ble Apex Court have decided this issue in favour of the revenue in the case of Checkmate Services (P.) Ltd. v. CIT 448 ITR 518 (SC) and the assessee has not paid within the due date specified in the respective Act. The ld. CIT(A) while deciding the issue has ignored the provision of u/s 36(1)(va) of the Act and not considered properly the way of submission of the assessee. The Act is very much clear that the assessee should have paid the employee’s contribution within the due date as per the respective Act. Therefore, the order of the AO should be upheld.

6. On the other hand, the Ld. AR relied on the order of Ld. CIT(A) and submitted that during the course of appellate proceedings detailed written submission were submitted which has been considered by the Ld. CIT(A), relying on various case laws he has allowed the appeal of the assessee on this point. He further submitted that similar issue has been decided by the coordinate Bench of the Tribunal in assessee’s own case in ITA No. 1844/Kol/2017 for the AY 2099-10, order dated 23.05.2025.

7. Further the Ld. AR drew our attention that this issue does not belong to employees’ contribution to PF & ESI but is related to the provisions made only.

8. Considering the rival submissions and perusing the entire material available on record and the orders of authorities below. We also gone through the order of AO and grounds taken before the Ld. CIT(A) in Ground No. 22 to 24, but the AO has not discussed the issue in detail about the employees’ contribution to PF & ESI but the addition made by the AO. We noted from the submissions made during the course of first appellate proceedings the figures are tallied and the submissions made before the Ld. CIT(A) are related to the section 2(24)(x) r.w.s. 36(1)(va) of the Act which are as under:-

“06. Grounds No. 22 to 25 by appellant arise on account of the disallowance of 94,49,341/- Rs.66,23,569 + Rs.28,25,772] u/s 43B of the Income-tax Act, 1961. The said matter has been dealt with by the Ld. AO as under:

Disallowance u/s.43B.

From the computation sheet, it appears that assessee had claimed credit of items covered u/s.438, amount to Rs.3,14,63,821/-, being payment made in the relevant previous year (which was disallowed in earlier years). From clause 21(1)(A) & 21(1)(B) and Annexures 13 & 14 of TAR, it appears that out of the total claim of Rs.3,14,63,821/-, on amount of Rs.66,23,569/- and Rs. 28,25,772/- not actually paid by the assessee, but were adjusted. As per provision of section 438, credit is allowable only on actual payment. Accordingly, condition of section 438 is not satisfied respect of these amount Hence, credit of Rs.66,23,569/- and Rs.28,25,772/, which were not actually paid but adjusted only, are disallowed. As a result, assessee company’s claim for credit of payment of items covered us.43B is reduced to Rs.2,20,14,480/-only.

07. During the course of the appeal, the appellant-company/Ld. A.R for the appellant company have submitted as under

In this connection, this is to submit that the whole of such amount having been deposited before due date of filing the return, question of any disallowance did not arise and in this connection your kind attention is drawn to Annexures-C-1, to C-3 of the Tax Audit Report, a copy of which is enclosed herewith at Page No 278-356 of Paper Book. From a perusal of which it will be seen that the earlier amount of Employees Contribution towards PF and ESI had been paid and deposited before due date of filing the return

1. In this connection, your kind attention is drawn to the decision of Hon’ble Kolkata High Court in the case of Arambagh Hatcheries Ltd. v. CIT Kolkata-XX wherein by their order dated 11.03.2011, it was held by Hon’ble Court as under- (underlined by us to lay emphasis)

“After hearing the leamed counsel for the parties and after going through the materials on record, we find that the most vital question involved in these three appeals is whether the amendment made in section 438 of the Income-tax Act 1961 by the Finance Act, 2003 is clarificatory and thereby retrospective in nature. If the aforesaid question, is answered in favour of the assessee, in that event. Point No.3 formulated in all these three appeals should be answered in favour of the assessee in as much as the Tribunal below disallowed the amount of deposit towards provident fund on the sole ground that those were delayed deposit in terms of Section 36(1)(va) read with Section 438 of the Act.

In our opinion, in view of the subsequent decision of the Supreme Court in the case of

Commissioner of Income Tax v.

Alom Extrusions Ltd reported in (2009) 318ITR 306 (SC) whereby it has followed the earlier decision of that Court in the case of

Allied Motors Pvt. Ltd. v.

CIT (1997) 224 ITR 677 (SC) to the effect that the said amendment is retrospective in nature, the assessee should get the benefit of the amended provision as the deposit made was within the time prescribed in section 139(1) read with Section 438 of the Act and, therefore, the order of the Tribunal below disallowing the benefit of the amendment to the assessee cannot be supported.” 2. Bihar State Warehousing Corporation v. CIT, Patna-

Held Although Technical reading of sec. 438 and sec. 2(24)(x) read with sec 36(1)(va) creates the impression that Employees Contribution would continue to be treated differently as the head of deduction is separate 1.1/S 438 and sec. 36 but on a broader realizing of amendments made to sec. 438 repeatedly and the intention of Parliament, there appears to be sufficient justification for taking the view that Employees’ and Employer’s Contribution ought to be treated in the same manner.

The aforesaid disallowance is illogical and incorrect. The Jharkhand High Court in ACIT v. Kaiser Industries Ltd. (

copy enclosed at Annexure -16) held that adjustment of statutory liability is as good as payment. Further, Hon’ble Jharkhand High Court in CIT v. Shakti Spring Ind. (P) Ltd. (TS-4-HC-2013) held that book adjustment constitutes actual payment u/s 438.

Annexures 13 & 14 of the Tax Audit Report contained the Particulars of amount claimed/ disallowed under Section 438 of the Income-tax Act, 1961. In the said Annexures the tax auditor had reported sums aggregating to Rs.94,49,341/- le Rs. 66,23,569/- at Annexure-13 and Annexure-14 Rs.2825772/- which were ‘adjusted and not paid during the year under consideration. Since the liability to pay the aforesaid sums did not exist on the return filing due date, no, disallowance was made under Section 438 of the Income-tax Act, 1961 or alternatively deducted was claimed. The AO however in his impugned order disallowed the amount of Rs94,49,341/- under Section 438 on the alleged ground that since it represented “amount adjusted and not paid”, it did not satisfy the conditions of Section 438 which required actual ‘payment of the (lability. The appellant submits that the AO never called upon the assessee to explain the issue and unilaterally computed the said disallowance. The appellant submits that the aforesaid disallowance was fallacious, absurd & illogical. The Delhi High Court in the case of ACIT v. Kaiser Industries Limited has held that adjustment of any statutory liability enlisted under Section 438 is as good as payment of the liability. The Jharkhand High Court also in case of CIT v. Shakti Spring Industries P. Ltd (TS- 4-HC-2013) held that Book adjustments constitutes actual payment for Sec-438 and therefore no disallowance is warranted under Section 438 of the Income tax Act, 1961. The appellant thus submits that the disallowance of Rs94,49,341/-deserves to be deleted in full.

In this connection, it may also be kindly be appreciated that similar disallowances were made in A.Ys 2005-06 82006-07 and he issue was ultimately decided in assessee’s favour by Hon’ble ITAT, Kolkata Benches in ITA No1826, 1827/K/2012(copy enclosed at Annexure-14). Against such order of the Hon’ble ITAT, the revenue had preferred an appeal before the Hon’ble Calcutta High Court and the Hon’ble Calcutta High Court in ITA No216/2013 (copy enclosed at Annexure-15) as affirmed the order of the Hon’ble Tribunal. Hence, this issue may kindly be considered accordingly.”

9. We noted that this issue has been raised by the revenue regarding not paid the statutory dues within the due date as specified in the respective Act as per section 36(1)(va) of the Act towards employees’ contribution to PF & ESI. During the course of hearing the ld. Counsel for the assessee restricted his arguments upto the order of the ld. CIT(A) and decision of the ITAT in his own case. However, this issue has been settled by the Hon’ble Apex Court in the case of Checkmate India Pvt. Ltd. (supra) and the said judgment has not been considered while deciding by the coordinate Bench in assessee’s own case in ITA No. 1844/Kol/2017 (supra). Considering the above decisions of Hon’ble Apex Court and submissions made before the ld. CIT(A) , This issue is remitted back to the AO and the AO is directed to find out the related issue under which section does it come. The AO has also not gone in details and documents in this regard.

10. From the submissions made before the ld. CIT(A) it appears that the issue is covered u/s 2(24)(x) r.w.s. 36(1)(va) of the Act, if it is so the AO is directed to decide this issue on the basis of judgment of Hon’ble Apex Court in the case of Checkmate Services Pvt. Ltd. (noted supra) above, The AO is further directed to look into the matter that there should not be double addition (taxation) on the same amount.

11. Respectfully following the above judgment, we are remitting this issue back to the AO for fresh decision on this point in above terms.

Ground No. 1

12. Ground No. 1 raised by the revenue pertaining to deletion the upward adjustment of Rs. 12,37,50,000/- as suggested by the TPO to AO on account of fees for technical support services paid to M/s Global Footwear Services Pvt. Ltd., Singapore AE. The AO TPO observed that the assessee failed to substantiate the genuine of the payments made to its AE (Associated Enterprises). During the proceeding before the TPO the assessee provided various documents to support that the there were various kinds of services were taken from its AE i.e. Engineering Services, Purchasing Services, Construction and technical Services and various kinds of services as submitted before the Appellate proceedings for 19 different kinds of services and detailed written submission was made which is incorporated by the ld. CIT (A). The ld. CIT(A) after considering the entire submission he allowed the appeal of the assessee. The ld. DR supported the order of the AO. The assessee counsel relied on the order of ld. CIT(A). Considering the rival submissions and perusing the entire materials available on record and order of authorities below we noted that the ld. CIT(A) has allowed observing as under:-

“05. Findings & Decision : (Ground No. 1 to 21)

I have considered the facts of the case. The issue pertains to payment of a sum of Rs.12,37,50,000/- which has been paid by the assessee-company as a royalty pursuant to Technical Collaboration Agreement with the said AE. The facts as emerging out of the Ld. TPO’s order and appellant’s submission is that the assessee have been paying such royalty towards Technical Collaboration Agreement and during the F.Y 2007-08 relevant to A.Y 2009-10 such agreement was assigned on 1.6.2007 to Global Footwear Services, Singapore (“GFS”) which is also an AE and hence such Impugned payment was to also an AE. The appellant has also submitted the salient services obtained from the AE pursuant to such technical collaboration agreement. As per the Technical Collaboration Agreement the following services were availed by the appellant from the AE “GFS:

| ii. |

|

Purchasing services 1. |

| iii. |

|

Construction and architectural services III. |

| iv. |

|

Research and Development services |

| v. |

|

Testing and quality control services; V. |

| vi |

|

Footwear Technology & General Technical Services Vi |

| vii |

|

Brand Development Services vil. |

| viii. |

|

Market Research Services |

| ix. |

|

Store location, Design and Layout services |

| x. |

|

Administration and Accounting Services |

| xi. |

|

Product development, Footwear Design and Construction services |

| xii. |

|

Information system services |

| xiv. |

|

Risking Insurance services. |

2. In terms of the said agreement, the assessee was paying royalty @ 1.5% on domestic sales & export sales to AE I.e. “GFS” and accordingly during the year payment of royalty of Rs.12,37,50,000/- was made to such concern. The fact of such transaction being. “International transaction” and the impugned transaction being with an “associated enterprises” (AE) has not been disputed by the assessee at any stage either before the Ld. TPO or in this forum. Since the payment of royalty partakes the nature of an international transaction with the AE, the price paid by the assessee-appellant had to satisfy the Arm’s Length Price (ALP) Criteria laid down in section 92 of the Act. In Transfer Pricing for the purpose of bench marking the assessee applied Cup Method, the most appropriate method and the assessee had accordingly Identified comparable companies paying an average rate of royalty on domestic sales and export sales and since the rate of royalty paid by the assessee was lower, the assessee claim that the price paid was claimed as the ALP. Before the Ld. TPO, the assessee submitted detailed replies explaining the aforesaid. international transactions. The Ld. TPO, however, added the entire amount paid to AE, i.e. Global Footwear Ltd, Singapore by treating the ALP at nil and added the entire sum paid I.e. Rs.12,37,50,000/- by way of adjustment to ALP.

3. In my considered view of the matter, the following aspects would require consideration in order to identify Intra group services requiring arm’s length remuneration:

Whether services were received from related party.

Nature of services including quantum of services received by the related party.

Services were provided in order to meet specific need of recipient of the services.

The economic and commercial benefits derived by the recipient of intra group services.

In comparable circumstances an independent enterprise would be willing to pay the price for such services?

An independent third party would be willing and able to provide such services?

Whether payment made to AE meets ALP criterion will be determined, keeping in mind all the above factors, as well.

4. The appellant’s submission in brief can be summarized as follows:

| a. |

|

Technical information relating to design methods and manufacturing techniques including drawings, tracings, etc.: In respect of the same the appellant submitted that the AE provided regular advice to Bata India on matters relating to manufacturing operations. It also assisted in development and design new types of footwear by advising on matters connected with product development such as materials, design methods, colour, etc. |

| b. |

|

Brand development services: With respect to this, it was submitted that it had got brand development services to enable it to compete against international brands and imported products. |

| c. |

|

Management support: The AE was assisting the appellant in identifying key personnel who had global experience and were experts in their own fields to manage the operations of the appellant. These managers were providing assistance in product development, quality control and distribution management, which were essential for success in the footwear industry. |

| d. |

|

Training of Bata India’s personnel to enhance their competence: The appellant submitted details of training programme undertaken by it with the help of AE. |

| e. |

|

In support of its contention that the transaction with AE was bona fide and genuine, the appellant also submitted that the Technical Collaboration agreement had the approval of RBI and Ministry of Finance. |

5. It was also brought to my notice that the nature of services rendered were identical and that observations of the Hon’ble Tribunal in the order for A.Ys 2003-04 & 2004-05 would equally apply to the present AY 2010-11also. It was also brought to my notice that in A.Y 2008-09 revenue has already accepted the transaction with the sald AE and held it at Arm’s length and hence no addition was made during such year and following the same addition was not warranted in A.Y 2009-10 as well. It was further contended that it is the assessee’s prerogative to decide whether to incur any expenditure or not for the purpose of business and the revenue authorities cannot sit in judgment over the same. In this regard attention was drawn to several Judicial pronouncements some of which are as follows:

| a. |

|

CIT v. Malabar Plantations 53 ITR 140 |

| b. |

|

Madhav Prasad Jhatia v. GIT 118 ITR 200 |

6. Reference was also made to the decision of the ITAT, Kolkata Bench in the case of NLC Nalco India Ltd. v. DCIT in ITA NO.529/Kol/2008 order dated 03.02.2016 wherein this Tribunal held on identical transfer pricing adjustment that the disallowance made cannot be sustained.

7. The material on record shows that the assessee entered Into a “Technical Collaboration Agreement” (“TCA”) with Bata Ltd., Canada, (successor of Bata Lim) with effect from January 1, 2001 to avail the desired advisory and technical services. The said agreement has been approved by Government of India, Secretariat for Industrial Assistance vide approval letter No. 120(2000)/564(2000) PAB-EL dated October23,2000. Bata Limited, Canada. Such agreement was assigned to Global Footwear Singapore (“GFS”) which is also an AE and which is engaged inter-alia in the business of providing comprehensive advisory services relating to production and distribution of footwear and associated products to clients across the world. The said company is stated to possess valuable knowledge expertise and experience and is stated to possess secret and specialized know-how, information and data in the field of production and distribution of footwear and associated products.

8. The following are instances of the technical and managerial support received by Bata India:

| a. |

|

Technical Information relating to design methods and manufacturing techniques including drawings, tracings, etc.: It was the contention of the Assessee that the AE provided regular advice to Bata India on matters relating to manufacturing operations. It also assisted in development and design of new types of footwear by advising on matters connected with product development, such as materials, designs, design methods, colours, etc. The Ld. TPO was of the view that there was no indication as to wherefrom these drawings have originated or what procedures were to be followed for implementing the said designs in the footwear to be manufactured by the assessee company in India. Neither any indication was available as to when these ‘designs’ were created specifically for the assessee company nor was it discernible, whether these designs were created. He therefore concluded that no services were rendered in the nature of the technical information relating to design method and manufacturing technique, etc., as claimed by the assessee. He concluded that there were no services rendered in the nature of Brand related services as claimed by the assessee. It was submitted by the Assessee that royalty was paid as consideration for the right to use certain design, drawings and technical know-how etc. which are owned by the licensor. Detailed design and drawings were provided by the associated enterprise to enable the assessee to implement the know-how and manufacture shoes using such technology. Such technical know-how and design drawings etc. have been used by the assessee for its benefit. It was submitted that as long as the technology which is owned and provided by the associated enterprise is used by the assessee for manufacture of footwear products, whether such technology was developed exclusively for the assessee is irrelevant. It would be appreciated that without the payment of royalty, the assessee would not have been in a position to use such technical know-how. |

| b. |

|

Brand development services: It was submitted that in order to compete against international brands and Imported products, Bata India has, under the guidance of the associated enterprise, undertaken a revamp of the Bata brand in India. The AE advised Bata India on the development of the brand, brand marketing plans, brand policies, etc., in accordance with the Indian market conditions. A strategic alliance had also been formed with other major global brands, like, Nike, Reebok, Adidas, Lee Cooper, ID, Warner, etc. for marketing their products from Bata outlets in India. This strategy had given a big boost to Bata India by attracting the new generation of customers in Bata stores, resulting in an enhanced acceptability of Bata products. It was submitted that Bata India, with its established brand name, enjoyed an edge over its competitors and this has given it an acceptability and reach that all other brands can only aspire to achieve. |

The associated enterprise advised the assessee on the development of the brand, brand marketing plans, brand policies, etc. in accordance with the Indian market conditions. On the basis of the advisory services provided by the associated enterprise, the assessee was able to introduce new products in the Indian market and attract the new generation of customers in the Bata store, resulting in an enhanced acceptability of Bata products over the country.

On the above submission of the Assessee the Ld. TPO was of the view that none of the brand related work was specifically directed towards the assessee. In any case, the assessee was in India for more than 70 years and was an established brand in itself. He held that the Assessee’s brand in India does not need any brand enhancement through Bata Canada.

On the above conclusion, of the TPO, It was submitted that the associated enterprise has provided the assessee with strategic marketing insights in connection with set up, aesthetics and appearance of the showrooms. It was submitted that in order to meet the requirements of a highly competitive market characterized by the presence of various global players, It was imperative for the assessee to adopt global best practices. The associated enterprise, as a result of its global presence was abreast with prevailing trends and practices. The services provided by the associated enterprise plays a vital role in the survival of the assessee in a highly competitive market. The aforesaid services were specifically requisitioned by the Assessee and were rendered pursuant to the agreement entered into with the associated enterprise. It was submitted that the contention of the TPO that none of the brand related work were specifically directed towards the assessee, is incorrect and not borne out from the record.

| c. |

|

Management support: It was the plea of the Assessee that in order to meet the requirements of a highly competitive market characterized by the presence of various global players, it was imperative for the assessee to adopt global best practices, The associated enterprise, as a result of its global presence was abreast with prevailing trends and practices. The services provided by the associated enterprise played a vital role in the survival of the assessee in a highly competitive market. The aforesaid services were specifically requisitioned by the assessee and were rendered pursuant to the agreement entered into with the associated enterprise. The contention of the TPO that none of the brand related work were specifically directed towards the assessee, was incorrect and not borne out from the record. |

On consideration of submissions of the learned counsel for the Assessee In the light of the observations of the TPO and perusal of the paper book shows that it is a brand book and contains several instructions called” Bata and more Brand”. The manual gives all the characteristics and technical specifications in order to realize the labelling of Bata Non-Footwear lines. The brand book contains sections like corporate identity, logo of Bata how to construct and reproduce the same. Similarly, It is seen that guidelines provided by GFS relating to the display and position of footwear, boards, hoardings, window display etc. It cannot be disputed that the material contained in the brand books have in fact been practiced in reality. Hence notice of the existence of directions contained in the brand book and they were in fact put in practice in the various Bata stores in India. Hence it is held that services in the form of technical information relating to design methods and manufacturing techniques were in fact provided by the AE to the Assessee. So also, Brand Development services were provided by the AE to the Assessee.

| d. |

|

Management Manpower Support: It was the contention of the Assessee that the AE has been assisting Bata India in identifying key personnel who have global experience and are experts in their own fields, to manage the operations of Bata India. These managers/directors have been assigned tasks of spearheading Initiatives in product development, quality control and distribution management, all of which are critical determinants of success in the footwear Industry. |

The analysts studied the functions performed, risks assumed and returns earned at different categories of stores and thus assisting Bata India in deciding which on the most efficient category of retail stores and the category in which new stores should be opened. Based on AEs advice Bata has developed its retail stores in different niche categories in line with the customer profile at each location. AE advised on possible option for reduction of insurance costs. In light of this advice, Bata India management appointed Marsh India Private Limited to reduce its insurance costs.

On the above claim of the Assessee, the TPO was of the view that neither any specific instance was cited, nor the assessee furnished any detail of expenditure Incurred by GFS in providing such service. Therefore, he held that there was service rendered to the assessee by the AE In the nature of management support as claimed. It was submitted by the learned counsel for the Assessee that specific instances of services such as advise upon opening of new retail stores, reduction in insurance costs etc. were cited before the TPO. However, the TPO arbitrarily held that no specific Instances in connection with provision of management support services have been provided by the assessee. The aforesaid services were specifically requisitioned by the assessee and were rendered pursuant to the agreement entered into with the associated enterprise. The contention of the TPO that none of the brand related work were specifically directed towards the assessee, is incorrect and not borne out from the record.

Having considered all these matter, I am of the considered view that the AE has been assisting the Assessee in identifying key personnel who have global experience and are experts in their own fields, to manage the operations of the Assessee. Instances have been given in the submission beforeLd.AD/TPO. It cannot be disputed that though such personnel were from the same Bata group, the decision to relocate them in a specific country keeping in mind commercial interest of the AEs is taken by the intra group service provider, and this decision certainly appears to be a crucial one. In my considered view of the matter, the Assessee has thus demonstrated and established that services of the nature of management support were in fact provided by the AE to the Assessee.

| e. |

|

Training of Bata India personnel to enhance their competencies: It was the contention of the Assessee that the AE has been undertaking regular trainings, seminars, conferences, etc., for the development of Bata India’s personnel. Knowledge is the key in manufacturing and operational efficiency. The best practices have been transferred to Bata India through those trainings and conferences. Knowledge transfer has been a continuous process and Bata India has been able to significantly enhance the value of its human capital through such trainings. Under the said guideline, the associated enterprise provided services in relating to selection, recruitment and assessment of people for current and future roles within the assessee. Further, the associated enterprise also provided other human resource related services, such as identification and awareness of dress code of the employee, training of employee, awareness of code of ethics, etc. |

On the above submission of the Assessee, the TPO was of the view that if the courses claimed to have been held by the AE were being paid for separately, then how could these be claimed as technical services rendered under TCA for which another payment was made to the AE in the form of royalty. The activities claimed as “Training of Bata India’s personnel” by the AE fail on the touchstone of the arm’s length principle according to which one has to examine whether an independent enterprise in comparable circumstances would have paid for such activity it performed for it by another independent enterprise. He therefore concluded that it was clear that no services were rendered by the AE for which any Independent enterprise would have paid anything over and above the expenses of course fee, etc., which, in any case, were borne by the assessee company whenever its employees attended such trainings /seminars. Assessee has submitted relevant evidences to support its contention that AE on behalf of the Assessee is organizing seminars, conferences, meetings etc., for which costs are incurred separately by the Assessee is different and has nothing to do with the training services of the Assessee provided by the AE.

| f. |

|

Administration and accounting services: It was the plea of the Assessee that the AE has been providing administrative and accounting assistance in Bata India by designing various management and accounting reporting packages based on new administration and accounting systems and technologies and making recommendation on the implementation and use thereof and advise on matters connected thereto. The AE reviews the budgets prepared by Bata India and provides feedback on the same before they are finalized. Further, Bata India provides information to the AE on the proposed weekly business plan for the next year. The AE reviews the performance of Bata India from time to time and has played a crucial role in determination of Bata India’s growth plan, such actions are undertaken so that the AE can help provide any assistance regarding business strategies to be undertaken in the next year and also analyse the financial performance of Bata India compared to its business plans. The AE has also presented Bata India with its own accounting system in order to ensure that Bata India has the necessary tools for financial planning, control of assets and liabilities and management information systems, viz., Monthly Information Package (MIP), Business Plan, Finpack, Accounting manual. |

| g. |

|

Financial services: AE has also provided Bata India with various formulae devised by AE for calculation of ratio (on cash flow planning, assets management, etc.) and business indicators (like stock turns, forward weeks’ inventory etc.) which are essential for controlling the shoe business (placed on record). It would assist the company in analysing its financial performance and provide guidance in formulating future business plans and strategies. |

| h. |

|

Information system services: AE has developed a diverse range of Information systems for use by different departments for improving business efficiency. These systems have been adopted by Bata India under guidance of AE for installing and implementing of these information systems. Further, these systems have been modified to suit Indian conditions by the AE. It has also made recommendations to Bata India on their hardware and software to be used by Bata India to meet the requirements of the various information systems. The associated enterprise has developed a diverse range of information systems for use by different departments for Improving business efficiency. These systems have been adopted by the assessee under the guidance of associated enterprise for installation and implementation. Further, these systems have been modified to suit Indian conditions by the associated enterprise. |

9. The TPO was of the view that from the details submitted, it is seen that some of the activities performed by GFS were continuing from past and no royalty payment was made for the same. The further reasoning of the Ld. TPO was that the activities related to provision of accounting and other IT package and other financial monitoring activities are nothing but the owner shareholder’s activity to monitor the financial performance of its subsidiary company, i.e., the assessee company. These cannot be considered as services requiring payments as these were mere activities performed by the AE at the instance parent company as was done in the past also without necessitating payment of royalty, etc., to protect and enhance its interests in the entity (the assessee company) owned by it. He also held that no specific or discernible services were rendered by the AE to the assessee company in the nature of Administration and Accounting Services’ of ‘Information System Services’ or ‘Financial Services’, which were more than mere owner-shareholder activity.

10. The plea of the Assessee-company / Ld. A.R with reference to the above conclusion of the Ld. TPO was that the fact that no royalty was charged by the associated enterprise in the earlier years cannot be an estoppel against charging a fair or arm’s length rate of royalty in the subsequent years. Reliance was placed in this regard on the decision of the judgment of Hon’ble Supreme Court in the case of

Shahzada and Sons v.

CIT 1977 CTR (SC)246:

(1977) 108 ITR 358 (SC)

and CIT v.

Laxmi Cement Distributors (P) Ltd. 1976CTR (GuJ) 338:

104 ITR 711 (GuJ), wherein it has been held that remuneration paid for services rendered could not be disallowed merely because no remuneration for such services was paid in the past. Similarly, in the case of

Addl. CIT v.

Nestle India Ltd (2005) 94 TT J 53 (Del) the Hon’ble Tribunal held that it is not relevant that no royalty was paid in the past. Similarly in the case of

Dresser Rand India Pvt Ltd v.

Addl. CIT (ITA No 8753/Mum/2010) the Hon’ble Mumbai Bench of the Tribunal held that, whether the AE gave the same services to the assessee in the preceding years without any consideration or not is irrelevant. The AE may have given the same service on gratuitous basis in the earlier period, but that does not mean that arm’s length price of these services is ‘nil’.” It was further submitted that such services can, by no stretch of imagination be regarded as shareholder services.

| 11. |

|

In particular attention was drawn by the appellant / Ld. A.R to the OECD Transfer Pricing Guidelines which defines the shareholder activity as under: |

“Shareholder activity

An activity which is performed by a member of an MNE group (usually of the parent company or a regional holding company) solely because of its ownership interest in one or more other group members, l.e. in its capacity as shareholder.”

12. Further attention was drawn by the appellant to para 7.10 of the OECD Transfer Pricing Guidelines further provides the following examples of shareholder activity:

7.10 The following examples (which were described in the 1984 Report) will constitute shareholder activities, under the standard set forth in paragraph 7.6: (a) Costs of activities relating to the juridical structure of the parent company Itself, such as meetings of shareholders of the parent, issuing of shares in the parent company and costs of the supervisory board;

Costs relating to reporting requirements of the parent company Including the consolidation of reports;

(c) Costs of raising funds for the acquisition of its participations.”

I was thus submitted that shareholder activity is an activity which is performed by an entity solely because of its ownership interest in other company le in the capacity of shareholder. It was thus submitted that specific services rendered by the associated enterprises in the domain of IT, Finance and Accounts cannot be regarded as provided by the associated enterprise in the capacity of a shareholder.

13.1 have given a careful consideration to the rival contentions. After carefully analysing the issue, in my considered view, none of the reasons given by the Ld. TPO for disregarding the contentions put forth by the Assessee are found to be justified. I find that it has been quite rightly contended by the Assessee, the fact that no remuneration was paid for similar services rendered by the AE In the past is no ground to reject payment in a later financial year as for nonbusiness consideration. The activities performed by the AE were not in the capacity of a shareholder and for specific services. The conclusions of the Ld. TPO therefore that the activities performed by the AE were more in the nature of shareholder activity cannot be sustained. I am therefore of view that Information system services were in fact provided by the AE to the Assessee.

14.Store location, design and layout services / construction and architectural services: The associated enterprise supports the assessee on location, design and layout of a store. Special focus is on the layout of the store so as to ensure efficient utilization of space. The associated enterprise had provided assistance to the assessee in developing the Bata city store concept which targets to meet the needs of a typical urban neotraditional and contemporary consumer. Manual on development of city store concept along with its layout was placed on record. It was pointed out that during the relevant previous year, the associated enterprise also provided guidelines for setting up furniture and fixtures including drawings and designs of the furniture which should be installed at all Bata stores across the country. Drawings and designs provided by the associated enterprise were placed on record. Further, the associated enterprise has advised and provided guidelines to the assessee relating to the display and positioning of footwear, boards, hoardings, window display, etc., which were placed on record.

On the above submission of the Assessee the Ld. TPO was of the view that the services were directed towards protecting or improving interest of the ownership shareholder. On this matter, also, in my considered view of the matter, in dealing with similar conclusion, it is to be held that the conclusion of the Ld. TPO/AO in this regard cannot be sustained, the reasons given for such conclusions will equally apply here also.

15. Conclusion: In the light of the foregoing discussion, I hold that the Assessee established the nature of services including quantum of services received by the related party, that services were provided in order to meet specific need of the Assessee for such services, the economic and commercial benefits derived by the Assessee of intra group services.

16. The next question is as to whether the consideration paid to the AE is at Arm’s length. On this aspect, I have already observed that the Assessee in its Transfer Pricing Documentation, for the purpose of benchmarking, applied Comparable Uncontrolled Price (“CUP”) method as the most appropriate method. For application of CUP, the assessee identified following four comparable companies from the Secretariat for Industrial Assistance (SIA) database engaged in providing similar services paying an average rate of royalty of 3.95% and 3.5% on domestic sales and export sales respectively. It was claimed by the Assessee that since, the rate of royalty paid by the assessee at 1.5% was lower than the rate of royalty paid by the comparable uncontrolled enterprises in a similar condition, the Assessee claimed that the price paid in the transaction was to be regarded as having been undertaken at arm’s length price.

The Ld. TPO, however, following the Transfer Pricing assessment order determined the arm’s length price of payment of royalty as ‘nil’ allegedly holding that no services were actually received by the assessee. The entire amount paid to GFS was therefore added to the total income of the Assessee by way of adjustment to the ALP. The TPO has not disputed the most appropriate method for determination of ALP chosen by the Assessee viz., CUP method and comparability of the companies set out in the TP study of the Assessee with the Assessee. The arithmetic mean of the comparables chosen by the Assessee in its TP study was average rate of royalty of 3.95% and 3.5% on domestic sales and export sales respectively. The claim of the Assessee that the rate of royalty paid by the assessee at 1.5% was lower than the rate of royalty paid by the comparable uncontrolled enterprises in a similar condition has therefore to be accepted. The price paid by the Assessee to its AE has therefore to be held as at Arm’s Length.

With such view of the matter, these grounds are allowed.”

13. After going through the above finding recorded by the Ld. CIT(A) and relying on the various case laws, we do not find any infirmity in the order of Ld. CIT(A). Accordingly, we dismiss the grounds of the revenue.

14. During the course of assessment proceedings, it was noticed that the assessee has claimed royalty payment of Rs. 5,62,59,722/- to various entities on monthly and quarterly basis. This amount was claimed under “Miscellaneous Expenses” the details is given as under:

| Sr. No. |

Name of entities to whom royalty was paid |

Amount (Rs.) |

| 1 |

Wolverine Worldwide Ince, USA |

1,12,08,316 |

| 2 |

SSL TTK Limited – Chennai |

2,39,07,975/- |

| 3 |

Wolverine Worldwide Ince, USA |

1,29,02,066 |

| 4 |

SSL International Plc. UK |

82,41,365 |

|

|

5,62,59,722/- |

15. In this regard, the assessee furnished reply and AO observed that the submission made is similar to the AY 2008-09 and 2009-10 and AO observed that in the above two assessment years the royalty payment was held as enduring nature and treated as capital expenditure against which the assessee filed appeal before the Ld. CIT(A) taking Ground No. 28 to 29 and filed details and submissions. The Ld. CIT(A) after going through the entire submissions and his previous order treated the expenditure claimed as revenue expenditure and allowed the grounds. On the other hand, the Ld. DR relied on the order of AO. During the course of hearing, the Ld. Counsel submitted that the issue is covered in favour of the assessee in assessee’s own case for AY 2009-10 in ITA No. 1844/Kol/2017.

16. Considering the rival submissions and going through the order of Ld. CIT(A) and order of assessee’s own case the Co-ordinate Bench in which it has been held as under:

“Similar disallowance on royalty was deleted by the ITAT in the appeals for AYs 2005-06 and 2006-07. The order of the Tribunal is also affirmed by the Hon’ble High Court.

In view of the fact that royalty payment under same agreement has been held to be an allowable revenue expenditure, there is no warrant for the assessing officer to have taken a different view in the absence of any change in facts or position in law.”

17. Respectfully following the above judgment in assessee’s own case, we dismissed the grounds raised by the revenue.

Ground No. 4

18. During the course of assessment proceedings, the AO observed that the assessee has followed straight line method for the payment of lease rent Further, the AO observed that from the computation of income (both original and revised), it appears that in the original computation of income, assessee had disallowed on its own the rent claim under straight lining method of lease rent. However, in the revised computation of income, the position was reversed and expenses were claimed. In the immediate assessment related with AY 2009-10, it was vividly discussed how the ‘rent’ calculated applying ‘Straight Lining of Lease Rent Method’ is notional in character and has no bearing with the actual expenditure on account of rent. In view of the discussion made in the assessment order for AY 2009-10, rent claimed following ‘Straight Lining Lease Rent Method’ is disallowed.

19. Before the Ld. CIT(A) the assessee furnished reply and submitted that during FY 2007-08 the Expert Advisory Committee of the ICAI had issued a clarification in respect of mandatory Accounting Standard-19 on account of operating lease rent expense. Pursuant to the said clarification the assessee was required to recognize in its annual audited accounts the schedule rent increments over the lease term on a straight line basis in respect of all existing operating lease agreements remained in force on or after 2001. He further submitted detailed reply which is incorporated by the Ld. CIT(A) after considering the entire submissions the Ld. CIT(A) noted that on similar circumstances and set of facts of the case for the AY 2009-10 the issue has been discussed and allowed accordingly, he allowed the ground and the revenue is in appeal against the above deletion.

20. The Ld. DR relied on the order of AO and submitted that the notional lease rent cannot be allowed.

21. On the other hand, the Ld. Assessee counsel relied on the order of Ld.CIT(A) and detailed written submission filed before the Ld. CIT(A). Further, he submitted that in assessee’s own case for the AY 2008-09 in ITA No. 225/Kol/2024 order dated 06.09.2019, the issue has been discussed in detail and decided in favour of the assessee. Considering the rival submissions and going through the same, we noted that in assessee’s own case for the AY 2008-09 the similar issue has been dealt as under in favour of the assessee on the similar set of facts which is as under:

“31. We note that Hon’ble Supreme Court explained the importance of mandatory accounting standards in the case of J. K. Industries Ltd. v. UOI (297 ITR 776) wherein the Court held that the main object sought to be achieved by Accounting Standards which are now made mandatory is to see that accounting income is adopted as taxable income and not merely as the basis from which taxable income is to be computed. The Supreme Court explained its position by citing examples. In case of inventories, the valuation rules are laid down in the Accounting Standards which are followed in the determination of accounting income. Since the income-tax law does not lay down any such rules, the tax authorities are not required to examine the computation of the valuation of inventories and its effect on computation of income. However, in case of depreciation on assets, different rules& accounting guidelines are laid down in the Accounting standards vis-a-vis Income-tax Act, 1961. Accordingly, in such cases the provisions & rules laid down in I.T Act, 1961 & I.T. Rules, 1962 are to be followed. The Apex Court observed that under Section 211 of the Companies Act, 1956 every company is mandatorily required to prepare its accounts in accordance with the Accounting Standard, presented by the Central Government in consultation with National Advisory Committee on Accounting Standards and at present the Accounting Standards prescribed by the Institute is deemed to be the Accounting Standards which are to be complied by all the companies. The Supreme Court therefore accorded judicial recognition to the accounting standards issued by ICAI and the profits determined in accordance with the accounting guidelines laid down by the prescribed accounting standards was held to be depicting true & fair state of affairs of a company for tax purposes. Accordingly, the Assessing Officer has to adopt the profit determined by the assessee company in consonance with the accounting standards while assessing taxable income if there is no explicit & contrary provision in the income-tax laws.

We note that this principle was reiterated by the Supreme Court in the case of

CIT v.

Woodward Governor India (P) Limited (

312 ITR 254) wherein it was held that the profits for income-tax purpose are to be computed in accordance with ordinary principles of commercial accounting unless such principles stand superseded or modified by legislative enactments concerning assessment of total income.

Applying the ratio laid down by the Supreme Court in the above cited judgments, we note that the method of accounting followed by the assessee cannot be doubted unless it is contrary to the generally accepted accounting practices or if the same has been superseded or modified by a specific legislation brought about in the Income-tax Act, 1961. In the facts of the present case the assessee being a company followed mercantile basis of accounting and prepared its accounts in accordance with Section 211 of the Companies Act, 1956 and the notified accounting standards. It is by now well settled that matching principle of accounting ensures purity of Profit & loss Account and ensures true & fair ascertainment of income. Accordingly, in light of Guidance Note issued by EAC of ICAI and the accounting guidelines laid down in Paras 23 & 24 of AS-19, the assessee had changed its accounting treatment of operating leases expenses. In consonance with AS-19 the lease rent expenditure was recognized on a straightline basis which was considered to be a more systematic and rational basis by accounting experts. On accounting of escalating rentals in the operating lease agreements, it led to creation of additional lease rental liability in the relevant year under consideration which was debited to the P&L A/ c under the head “Rent Straight-Lining”. This accounting treatment was in sync accounting guidelines laid down by ICAI which the assessee was required to mandatorily follow. The profits so determined after accounting for the expense towards straight-lining of lease rentals reflected a better & accurate picture of the true commercial profits of the assessee company. In light of the law down by the Apex Court since there are no contrary or specific provisions in the Income-tax Act, 1961 in respect of accounting of lease rentals, the expenditure of Rs.40,647,000/- so recognized in the Profit &Loss account is deductible while computing profits of the business. We note that ld CIT(A) has rightly held that assessee is entitled to claim deduction of Rs.40,647,000/-on account of lease rent, observing the following:

“13.4. I have considered the facts of the case. The assessee had taken several assets on operating lease basis. In certain agreements, there was clause for scheduled increase in lease rent. Earlier, the assessee was not taking into account such scheduled increase while debiting the least rent. However, ICAI issued AS-19 for accounting of operating lease and a clarification relevant to the issue was issued in the year under consideration. As a consequence, the assessee had to compute impact of straight-lining of lease rent from 01.04.2001 to 31.03.2007 which was determined at Rs.3,97,18,000/- and the same was accounted under the head ‘ prior period expenses’. For the current year, a further sum of Rs.4,06,47,000/- was determined on such straight-lining. In his computation of return income the assessee added back prior period expenses at Rs. 3,97,18,000/- as well as current year’s expense of Rs.4,06,47,000/-. Since the latter expense pertained to the year under consideration, the assessee was entitled to claim the sum in computation of taxable income. The assessee has claimed to have made such claim before the assessing officer. But the assessing officer has not discussed the same in the assessment order. As explained by the assessee, the clarification regarding AS-19 was issued by ICAI in July, 2007. Thus, the requirement of straight-lining the lease rent arose in the year under consideration. The assessee was thus justified to adopt straight-lining of lease rent during the year. The Karnataka High Court in the case of Prakash Leasing Limited v. Dy. CIT held that as long as Central Government has not notified anything to the contrary, an assessee was well within its right to follow AS and to claim lease equalisation charges in accordance with the same. Similar view was expressed by the Hon’ble Delhi High Court in the case of CIT v. Virtual Soft Systems Ltd 341 ITR 593. In the assessee’s case, it has followed accounting standard issued by ICAI relating to operating lease. As a result of straight-lining recommended by the accounting standard, there was a requirement to make provisions for scheduled rent increase. Such provision relating to the year under consideration was of Rs. 4,06,47,000/-. The accounting standard was not in conflict with any provision of the Act or notification made by the Central Government u/s 145(2) of the Act. It is also not the case of the assessing officer that the system of accounting followed by the assessee was such that the correctness and completeness of accounts was to be doubted. Rather, the assessee has followed accounting standard issued by ICAI. The assessee had made the claim in the assessment proceedings and the assessing officer has neither allowed nor given reason for its rejection. In the remand report dated 03.01.2014, the assessing officer has objected to the assessee’s claim on the ground that such claim was not made by way of filing revised return. Apparently, he intends to draw strength from the decision of the Hon’ble Supreme in the case ofGoetze India Ltd. 284 ITR 323, though he has not specifically mentioned the same. However, in the said decision itself, Hon’ble Supreme Court has clarified that the bar on claiming a deduction not claimed in the return does not apply on the appellate authority. In the decisions in the case of National Thermal Power Co Ltd. (supra) and Jute Corporation India Ltd. (supra) Hon’ble Supreme Court has held that appellate authority has power even to admit a claim not made in the proceedings before the lower authority. Power of CIT(A) to consider claim not made in the return has also been upheld in the decision of Delhi High Court in the case of CIT v. Jindal Saw Pipes Ltd. 328 ITR 338 and by Bombay High Court in the case of CIT v. Pruthvi Brokers and Shareholders P. Ltd. 349 ITR 336. It is also noted, that jurisdictional bench of tribunal, in the case of DCIT, Circle-50, Kolkata v. Ramesh Chandra Kedia ITA No. 2072/Kol/2007, has held after considering various decisions, including in the case of Goetze India Ltd. (supra) that CIT(A) has power to admit additional ground claiming relief not claimed in the return and without filing revised return, even if the same results in assessed income going below the returned income. In his report dated 3.1.2014, the assessing officer has not given any comment or adverse remark on merit of the claim and not pointed out any defect or shortcoming in the same. In the light of the facts discussed earlier, the assessee is entitled for deduction of Rs. 4,06,47,000/-. The assessing officer is directed to allow the same.

We do not find any infirmity in the order of ld CIT(A) in allowing the claim of the assessee in respect of lease rent of Rs.4,06,47,000/-, therefore, we decline to interfere in the order of ld CIT(A), his order on this issue is hereby accepted and the ground No. 5 raised by the Revenue in ITA No.77/kol/2014, is dismissed.

32. Now coming to the additional ground raised by the assessee about “Lease Rent Equalization, Rs. 39,718,000/-” disclosed under the head “Prior Period Items” in audited financials being impact on recognition of rent increases over the lease term on a straight line basis.

33. We note that the assessee had taken certain assets for operating lease basis. In lease agreement there were clauses for scheduled increase in lease rentals, which was not taken into account by the assessee while declaring lease rent. Pursuant to clarification issued by the Institute of Chartered Accountants of India (“ICAI”) in the context of Accounting Standard AS-19 for accounting for leases, the assessee had to compute the impact of straight lining of lease rent from 01.04.2001 to 31.03.2007 which was determined at Rs.3,97,18,000/-. The same was shown as ‘prior period expenses’ in the profit and loss account. Additionally, liability for the current year was debited to the profit and loss account in an amount of Rs. 4,06,47,000/-. The assessee had inadvertently added back the amount of Rs. 4,06,47,000 in the return of income but the same was subsequently claimed before the assessing officer during the course of assessment. The assessing officer omitted to deal with the said claim. The same was, however, allowed on appeal by the CIT(A) against which the Revenue has come up in appeal (S. No. 5 of Grounds of Appeal), which we have already adjudicated in para 31 of this order. In so far as the amount of Rs.39,718,000/- is concerned, assessing officer added back the same while computing book profit under section 115JB of the Act. The adjustment made by the assessing officer was deleted by the CIT(A) for which the Revenue is in appeal before us, vide S. No. 4 of Grounds of Appeal. The amount of Rs. 39,718,000/- was not claimed deduction while computing income under the normal provisions of the Act. The same is being raised by way of additional ground for the first time before this Tribunal.

We note that the amount of Rs.39,718,000/- represents liability accrued during the year on account of change in the method of accounting for lease rentals pursuant to adoption of AS-19 issued by the Institute of Chartered Accountant of India. Although, the said amount represents the incremental liability of lease rent payable for the period 1.04.2001 to 31.03.2007, the same having accrued during the relevant previous year is allowable deduction notwithstanding that the liability may relate to earlier years. For this, we rely on the Judgment of Hon’ble Delhi High Court in the case of

CIT v.

Whirlpool of India Ltd.: 242 CTR 245, allowed deduction for incremental liability for warranty on the basis of actuarial valuation relating to sales made in the earlier years, holding as under:

“20. The legal principle delineated in the aforesaid judgment would clearly demonstrate that whenever there is a warranty clause in the bulk product sold by the company/assessee to its customers, warranty provision can be made and it would not be treated as contingent liability. There is no quarrel to this proposition and in fact in this very case the assessee has been making the provisions for warranty every year which was accepted by the AO. The question that really calls for an answer is as to whether such a provision which has already been made in the previous years can be revised later on in a particular year as sought to be done by the assessee in the present case. Going by the reasons which justify making of such a provision and treating them as expenditure under s.37 of the Act, more particularly when it fulfils the accrual concept as well the matching concept, we see no reason as to why the assessee could be precluded from revising this provision after taking into consideration that warranty period of the goods sold under warranty was existing provision already provided in a particular year is falling short of the expected claims that may be received. It is, however, to be kept in mind that such a provision is based on scientific study and actuarial basis that is precisely done by the assessee in the instant case and, therefore, we see no reason to differ with the view taken by the Tribunal in the impugned order. ”

34. We note that in the context of change in method of valuation of closing stock, the Courts have in the undernoted judgements held that the impact of the change had to be allowed deduction in the year in which the changed method was adopted for the first time:

| – |

|

CIT v. Carborandum Universal Ltd. : [1984] 149 ITR 759 (Mad.) – SLP dismissed vide 187 ITR (St) 38; |

| – |

|

Melmould Corporation v. CIT: [1993] 202 ITR 789 (Bombay). |

We note that Hon’ble Gujarat High Court in the case of

Saurashtra Cement & Chemical Industries Ltd. v.

CIT: 213 ITR 523 held that:

“Merely because an expense relates to a transaction of an earlier year it does not become a liability payable in the earlier year unless it can be said that the liability was determined and crystallized in the year in question on the basis of maintaining accounts on the mercantile basis.”

In view of the aforesaid decision in law, the incremental liability on account of lease rental equalization provided for pursuant to the clarification issued by the Expert Advisor Committee of the ICAl, accrued during the relevant previous year and is allowable deduction in computing income for the said year, notwithstanding that such liability may relate to the earlier years. Therefore, we direct the assessing officer to allow the claim of the assessee in respect of lease rent of Rs.3,97,18,000/-.”

22. Respectfully following the above judgment, we dismiss the ground raised by the revenue on this point.

Ground No. 5

23. During the course of assessment proceedings, it was observed that the assessee has claimed depreciation on River Bank embarkment and renovation thereof, since the depreciation was claimed in earlier year on the same assets which was not accepted by the AO observing that the depreciation claimed by the assessee does not fall under the block of assets and he disallowed against which before the Ld. CIT(A) the issue was raised. The Ld.CIT(A) noted that in the immediate preceding assessment year the depreciation has been allowed in the AY 2009-10. The Ld. DR relied on the order of AO. During the course of hearing, the Ld. Counsel submitted that in the assessee’s own case for the AY 200506 and 2006-07 the coordinate Bench has allowed the appeal in ITA Nos. 1826, 1827 and 1828/Kol/2012. Considering the rival submissions, we noted that the coordinate Bench has decided the issue in the similar set of facts in ITA No. 1826/Kol/2012 order dated 22.05.2012 in which it has been held as under:

“10. It was submitted by the ld DR that the AO had disallowed the depreciation on the river embankment and the renovation as it was not a building, nor road or bridge or culvert etc. and there was no business requirement of such an embankment. It was the submission that the ld. CIT(A) had allowed the same by following the order of his predecessor for A.Yr.2007-08 dated 23.06.2011 by holding that the embankment was for the protection of the factory building. It was the submission that the order of the ld. CIT(A) was liable to be reversed.

11. In reply the ld. AR drew our attention to the order of the ld. CIT(A) for A.Yr.2007-08. It was the submission that this issue was not a subject matter of appeal by the Revenue for the A.yr. 2007-08. In reply the ld. DR submitted that due to the tax effect no appeal has been filed.

12. We have considered the rival submissions. A perusal of the order of the ld. CIT(A) for A.Yr. 2007-08 clearly shows that there were other issues which were a subject matter of appeal before the Tribunal for the A.Yr. 2007-08. Admittedly the issue of depreciation on the river embankment was a small one but the revenue has not filed any appeal against the same. The depreciation having been allowed for A.Yr. 2007-08, it cannot now be denied for the A.Yr. 2005-06 especially when it has been accepted as part of the block of assets. In the circumstances we are of the view that the findings of the ld. CIT(A) on this issue is on a right footing and does not call for any interference.

13. In the result ground no.2 of the revenue’s appeal stands dismissed.”

24. Respectfully following the above judgment of the coordinate Bench in the assessee’s own case we dismiss the grounds raised by the revenue.

Ground No. 6

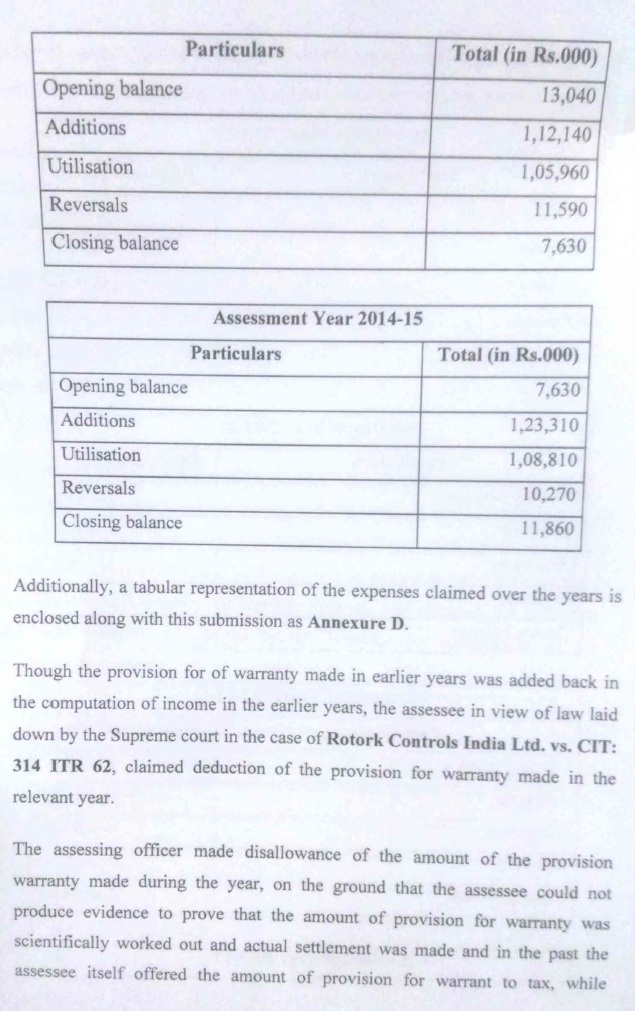

25. During the course of assessment proceedings, the AO observed that the assessee has made provision for warranty for Rs. 4,78,72,000/- and in rectification it was reduced to Rs. 39,01,000/- claimed as expenditure which was not allowed and the reversal of warranty is not material. Accordingly, the provision was disallowed. During the course of appellate proceedings, the Ld.CIT(A) referring to the assessee’s own case for AY 2009-10 in ITA No. 189/CIT(A)-22/2014-15/Kol and judgment of Hon’ble Apex Court in the case of Rotork Controls India (P.) Ltd. v. CIT 314 ITR 62 (SC) and various other judgements. The Revenue is in appeal before the ITAT against the deletion by the Ld.CIT(A). The Ld. DR relied on the order of AO and submitted that the Ld.CIT(A) has wrongly allowed this ground in favour of the assessee, the details are not provided to the AO for claiming actual expenditure incurred and there is no scientific method adopted by the assessee for making provision and utilizations as per the decision of Hon’ble Apex Court in the case of Rotork Controls India (P) Ltd. (supra).

26. On the other hand, the Ld. AR strongly supported the submissions made before the first appellate authority and he submitted that the Ld. CIT(A) has rightly allowed the provision for warranty. After considering the submission and similar issue has been decided by the coordinate Bench in assessee’s own case for AY 2009-10 in favour of the assessee observing as under:-.

“Ground No. 7: It was averred that the provision for warranty was made by the assessee for relevant assessment year on a reasonable and scientific basis as worked out by the actuarial valuer on the basis of past return/replacement ratio.

The Hon’ble Supreme Court in the case of

Rotork Controls India Ltd. v.

CIT: 314 ITR 62 has held that the provision for warranty made on a scientific basis, is an ascertained liability deductible under section 37(1) of the Act.

4. We have carefully considered the rival submissions and have also gone through the orders of authorities below and the documents filed by both the AR and DR. Regarding Ground No. 1, it is obvious that if the action of Ld. AO was to be sustained then it would amount to double taxation since the impugned amount was disallowed in the earlier years and has been credited to the Profit & Loss Account, on writing back of liability in the relevant previous year. Accordingly, we find no reason to interfere with the findings of the Ld. CIT(A) on this ground. In result, Ground no. 1 of the Revenue fails.”

27. Further the Ld. AR has filed written submission which is as under:

28. Considering the rival submissions, we noted that as per submission of Ld. Counsel, warranty is not provided for more than 75 days used by the purchaser which is clear from the below the table:

| Category of shoes |

Period used |

Replacement % |

| All shoes |

Upto 150 days |

100% |

| From 16 to 30 days |

75% |

| From 31 to 60 days |

50% |

| From 61 to 75 days |

25% |

| Over 75 days |

Nil |

29. The Ld. Counsel has filed outstanding (unexpired) provision for warranty as under:

30. On the observation of the replacement period (warranty period) as noted by the ld. CIT(A) in para No. 25 for ground No. 36,37&38 the replacement period and quantum is given. However, as per written submission (noted supra), the assessee counsel has submitted the warranty period is 60 to 90 days from the date of sales. We found deviation on the submissions made before the ld. CIT (A) as well as before us on the period of warranty and the assessee is also stated that the replacement varies between 25% to 100% depending upon nature of products and the terms applicable of the relevant period. Being a final fact finding authority, we have to ascertain whether the provision made by the assessee and utilisation of the warranty shown are correct or not, since, in this case on hand, the lower authorities have not examined correct utilisation of the warranty which are to be allowed to the assessee is not coming from the order of the authorities below as well as whether the AO has examined the utilisation of warranty in any previous years as relied by the Ld. AR in the judgments that any scientific method has been adopted for making provision or not tested. Therefore, it is directed to assessee to furnish the detail of the utilisation of the warranty with relevant documents and AO is directed to examine in depth. even before us. there is no any documents submitted regarding the provisions made except the financial data and the basis of creating provision. Even the actuarial valuation not submitted before us. Therefore, this issue is remanded back to the AO in above terms and decide the issue as per law. The only submission of statistical data is not sufficient to justify the provisions made. The data should be supported by the reliable documents in support of claims made. This ground is allowed for statistical purpose.

31. In the result, appeal of the revenue is partly allowed for the statistical purposes.